MU $7.6M Short Call Sale - Capping Upside on Memory Supercycle

January 12, 2026 | Unusual Activity Detected

The Quick Take

A sophisticated trader just sold $7.6 MILLION in premium by writing 6,000 short calls on MU at the $350 strike expiring February 2026. This premium collection strategy caps their upside just 1.6% above the current price of $344.55, suggesting the trader believes MU's explosive rally has reached a near-term ceiling. With a separate calendar spread (long $650 Dec 2027 / short $690 Jan 2028) adding another $3.5M in premium flow, smart money appears to be harvesting premium rather than chasing further upside. Translation: After a 247% rally in 12 months, institutional players are betting MU consolidates around current levels despite bullish HBM4 catalysts.

Company Overview

Micron Technology (MU) is the only U.S.-based memory chip manufacturer, riding the AI-driven HBM supercycle:

- Market Cap: ~$386 billion

- Industry: Semiconductors - Memory

- Sector: Technology

- Current Price: $344.55

- Primary Business: Micron designs and manufactures DRAM and NAND memory chips, with High Bandwidth Memory (HBM) products serving as the critical component for AI accelerators like NVIDIA's H200 and B200 GPUs. The company holds ~10-15% HBM market share and is targeting 30% by end of 2026.

The Option Flow Breakdown

The Tape (January 12, 2026):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:34:46 | MU | MID | SELL | CALL $350 | 2026-02-06 | $3.8M | $350 | 2,000 | 478 | 2,000 | $344.55 | $19.00 |

| 10:06:12 | MU | MID | SELL | CALL $350 | 2026-02-06 | $3.8M | $350 | 4,000 | 478 | 4,000 | $344.55 | $9.50 |

| 10:02:26 | MU | MID | BUY | CALL $650 | 2027-12-17 | $1.8M | $650 | 270 | 475 | 270 | $344.55 | $66.67 |

| 10:02:26 | MU | MID | SELL | CALL $690 | 2028-01-21 | $1.7M | $690 | 270 | 70 | 270 | $344.55 | $62.96 |

What This Actually Means

This is a premium selling strategy with two distinct components:

Primary Trade: Short $350 Calls (February 2026)

- Premium collected: $7.6M ($12.67 avg per contract x 6,000 contracts)

- Strike positioned: $350 is just 1.6% above current price of $344.55

- Time horizon: ~25 days until February 6, 2026 expiration

- Contract size: 6,000 contracts represents 600,000 shares worth ~$207M at current prices

What the trader is betting: By selling $350 strike calls expiring February 6, 2026, this trader collects $7.6M TODAY. As long as MU stays below $350 through expiration, they keep the entire premium with zero obligation. If MU rallies above $350, they either deliver shares at $350 (if covered) or face unlimited loss potential (if naked).

Secondary Trade: Calendar Spread ($650/$690)

- Long $650 Call Dec 2027: $1.8M invested

- Short $690 Call Jan 2028: $1.7M collected

- Net debit: ~$100K

This diagonal calendar spread is a longer-term position betting MU reaches the $650-$690 range within two years, but not immediately. The short leg at $690 reduces cost basis while capping maximum gains.

Combined interpretation: This trader believes MU faces near-term resistance at $350 (hence selling February calls at that strike), but remains constructive on the 2-year outlook (hence the LEAPS calendar spread targeting $650+). They are using February premium sales to fund longer-dated positions.

Technical Setup / Chart Check-Up

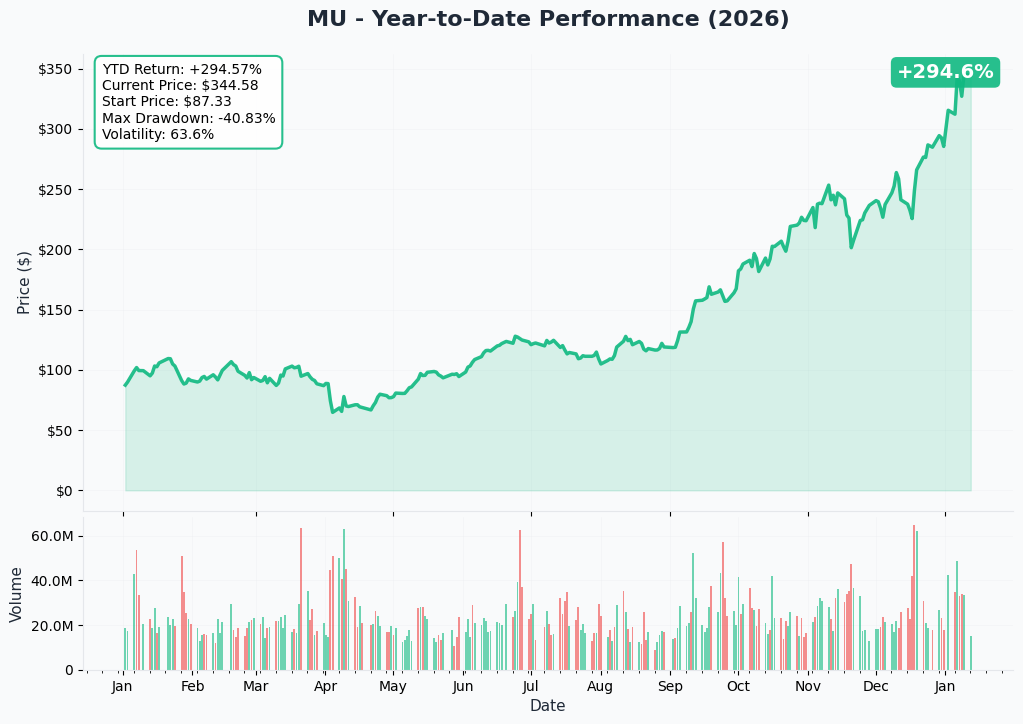

YTD Performance Chart

MU has been one of the best-performing large-cap stocks, up 247% over the past 12 months from its 52-week low of $61.54 to current levels near $345. The stock gained another 10.5% on the first trading day of 2026 following a Bernstein analyst upgrade, then continued rallying to all-time highs.

Key observations:

- 12-month performance: +247% driven by AI memory demand and HBM capacity sold out through 2026

- Recent momentum: +5.53% on January 9 alone, reaching all-time high of $345.09

- YTD 2026: Stock started the year with a 10.5% single-day gain

- Price action: Near all-time highs with limited overhead resistance but elevated valuation risk

- Volume profile: Heavy institutional accumulation with 80.84% institutional ownership

Gamma-Based Support & Resistance Analysis

Current Price: $344.55

The gamma exposure map reveals where options market activity creates natural price magnets:

Support Levels (Put Gamma Below Price):

- $340 - Strongest support and major gamma floor (1.3% downside cushion)

- $330 - Secondary support zone with solid put gamma concentration (4.2% below current)

- $320 - Extended support if momentum fades (7.1% downside)

- $300 - Major psychological and gamma support floor (12.9% below current)

Resistance Levels (Call Gamma Above Price):

- $345 - Strongest resistance right at current price (immediate ceiling)

- $350 - Key strike where 6,000 short calls were sold (1.6% above current)

- $360 - Extended resistance if breakout occurs (4.5% rally required)

- $375 - Upper bound of near-term range (8.8% upside)

What this means for traders:

MU is trading right into the strongest resistance zone at $345 with powerful support at $340. The gamma profile suggests the stock is pinned between these tight levels, creating a consolidation zone. The trader selling $350 calls is betting MU cannot break through this resistance into the February expiration.

Notice the GEX bias reads "Bullish" but resistance is just 0.15% above current price - this creates a "ceiling" scenario where bullish gamma positioning may keep the stock elevated but unable to break higher without a significant catalyst.

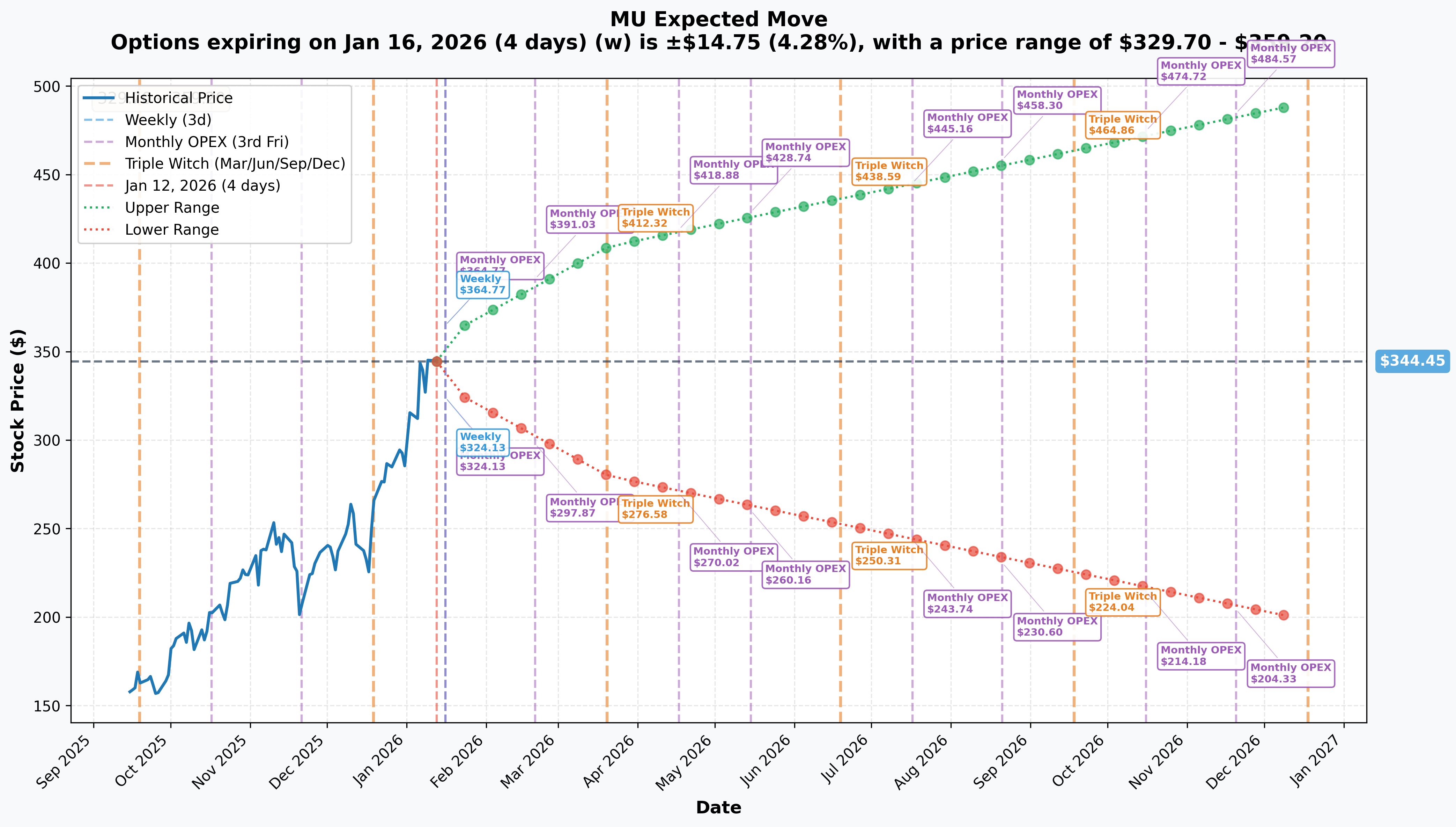

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 16 - 4 days): +/-$15.02 (4.36%) Range: $329.53 - $359.57

- Quarterly (Mar 2026 - 67 days): +/-$53.04 (15.39%) Range: $291.51 - $397.59

- Yearly (Dec 2026 - 343 days): +/-$151.22 (43.90%) Range: $193.33 - $495.77

Translation for regular folks:

Options traders are pricing in a 4.36% move over the next week, which would put MU anywhere from $330 to $360. The quarterly implied move of 15.39% reflects significant uncertainty around Q2 earnings (April 1) and HBM4 production ramp execution.

The 43.90% yearly implied range ($193 to $496) shows massive two-way risk perception. The options market is saying MU could nearly double OR fall 44% over the next year - typical for a semiconductor stock at cycle highs.

Key insight: The $350 short call strike sits right at the upper weekly implied range boundary ($359.57). The seller is betting MU doesn't exceed the expected weekly move to the upside.

Catalysts

Immediate Catalysts (Next 30 Days)

NY Megafab Groundbreaking - January 16, 2026

Micron breaks ground on its $100 billion New York megafab in Clay, NY, on January 16, 2026. President Biden will attend the ceremony, generating significant media coverage.

- Total investment: $100 billion over multiple decades

- Jobs created: 50,000+ in New York

- Production start: Expected ~2030

- CHIPS Act funding: $3.4 billion allocated

Why it matters for the short call trade: The groundbreaking is a known catalyst that could drive a short-term pop. However, since production doesn't begin until 2030, the stock impact may be limited to announcement-day momentum rather than sustained rally.

Near-Term Catalysts (Q1-Q2 2026)

HBM4 Production Ramp - Q2 2026

Micron begins HBM4 mass production in Q2 2026 to supply NVIDIA's Rubin platform:

- 12-high stack, 36GB capacity, 2.0+ TB/s bandwidth per stack

- Target: 15,000 wafers/month HBM4 capacity by end of 2026

- 20% power efficiency improvement over HBM3E

- February 2026: Large-scale co-supply to NVIDIA begins

Q2 FY2026 Earnings - April 1, 2026

Management guided for record revenue of $18.7 billion and $8.42 EPS:

- Revenue: +37% QoQ from $13.6B to $18.7B

- EPS: +76% QoQ from $4.78 to $8.42

- Gross margin: 68% guidance (up from 56.8%)

NVIDIA Rubin Platform Supply

Micron confirmed as lead HBM4 supplier for NVIDIA's Rubin GPU platform:

- NVIDIA announced Vera Rubin "in full production" at CES 2026

- Micron supplying HBM4 for H200/B200 and next-gen GPUs

- Multi-year supply agreement with locked-in capacity

Risk Catalysts (Negative)

SK Hynix Dominance

SK Hynix commands ~60% HBM market share and UBS forecasts they could reach 70% by end of 2026:

- SK Hynix is NVIDIA's preferred HBM supplier

- HBM4 qualification race ongoing between all three suppliers

- Micron's 30% market share target may be aggressive

Memory Cyclicality

Memory remains a cyclical business despite the AI supercycle narrative:

- DRAM/NAND pricing historically volatile

- Oversupply could collapse prices if AI demand slows

- The 247% rally prices in near-perfect execution

China Headwinds

Micron barred from Chinese critical infrastructure since May 2023:

- Ongoing YMTC patent lawsuit

- China's 125% tariff on U.S. semiconductors

- Lost revenue opportunity in world's largest memory market

Price Targets & Probabilities

Bull Case (30% probability)

Target: $400-$450

How we get there:

- HBM4 ramp exceeds expectations with market share reaching 25%+ by mid-2026

- Q2 earnings beat $18.7B guidance with raised full-year outlook

- NVIDIA increases Micron allocation at expense of SK Hynix

- Stock breaks through $350 resistance and establishes new trading range $375-425

Short call seller outcome: Significant losses if naked. If covered, opportunity cost of missing upside above $350.

Base Case (50% probability)

Target: $320-$370 range (CONSOLIDATION)

Most likely scenario:

- Q2 earnings meet guidance but don't significantly exceed

- HBM4 production ramps on schedule without hiccups

- Stock consolidates between strong support at $340 and resistance at $350-360

- Premium sellers profit as theta decay works in their favor

Short call seller outcome: Strong win - collects full $7.6M premium as calls expire worthless or near-worthless.

Bear Case (20% probability)

Target: $275-$320

What could go wrong:

- HBM4 yield issues or production delays

- SK Hynix captures even more market share (70%+)

- AI infrastructure spending slows in H2 2026

- General semiconductor sector rotation following extended rally

- Stock corrects 20-30% to retest $275-300 support zone

Short call seller outcome: Maximum profit - calls expire worthless, and they may have protected long stock positions from downside.

Trading Ideas

Conservative: Wait for Consolidation, Then Reassess

Play: Stay on the sidelines until MU finds a clear direction after the January 16 groundbreaking event

Why this works:

- Stock at all-time highs after 247% rally - poor risk/reward for fresh longs

- Binary events: NY groundbreaking (Jan 16), HBM4 ramp updates (Feb)

- Premium sellers clearly positioning for consolidation

- Better entries likely if stock pulls back to $320-330 support

Risk level: Minimal | Skill level: Beginner-friendly

Balanced: Cash-Secured Put Sales at Support

Play: Sell cash-secured puts at $320 or $330 strikes (March expiration) to collect premium while expressing willingness to buy at lower prices

Structure:

- Sell March 2026 $320 puts

- Expected premium: ~$8-12 per contract

- Breakeven: $308-312 effective cost basis

- Probability of assignment: ~25-30%

Why this works:

- Aligns with institutional logic of premium collection

- $320-330 represents strong gamma support

- If assigned, you own MU at 7-10% discount to current price

- Premium income regardless of direction if support holds

Risk level: Moderate | Skill level: Intermediate

Aggressive: Short-Term Call Spread (February Expiration)

Play: Buy $345/$365 call spread if you believe the groundbreaking event creates breakout momentum

Structure:

- Buy Feb 2026 $345 calls

- Sell Feb 2026 $365 calls

- Net debit: ~$6-8 per spread

- Max profit: $20 - debit = ~$12-14 (150-175% ROI)

- Breakeven: ~$351-353

Critical requirements:

- Only enter with capital you can afford to lose 100%

- This fights the institutional short call positioning

- Requires stock to break through $350 resistance

- Binary event risk from January 16 groundbreaking

Risk level: High | Skill level: Advanced only

Risk Factors

Don't get caught by these potential landmines:

-

All-time high entry risk: After rallying 247% in 12 months, MU trades at cyclical peak valuations. Any disappointment in HBM4 ramp or Q2 guidance could trigger 15-25% correction. The institutional short call activity signals smart money expects consolidation, not continued rally.

-

Memory cyclicality returns: While the AI supercycle narrative is compelling, memory remains one of the most cyclical semiconductor segments. Current pricing power reflects supply constraints, not structural change. When HBM capacity expands in 2027-2028, pricing pressure could emerge.

-

SK Hynix dominance: SK Hynix holds ~60% HBM market share and is NVIDIA's preferred supplier. Micron's 30% market share target by end of 2026 requires taking significant share from established leaders during a capacity-constrained environment where customers are unlikely to switch suppliers.

-

NY megafab execution risk: The January 16 groundbreaking is ceremonial - actual DRAM production doesn't begin until 2030. The $100 billion investment occurs over decades, meaning near-term financial impact is negative (capex) not positive (revenue). Labor shortages and construction delays have already affected timelines.

-

China revenue headwind: Micron lost access to Chinese critical infrastructure since May 2023. With China representing the world's largest memory market and imposing 125% tariffs on U.S. semiconductors, Micron faces permanent revenue exclusion from a key market where domestic competitors (YMTC) are gaining share.

-

Valuation stretched: At ~386 billion market cap with trailing P/E reflecting 247% appreciation, MU prices in the bull case. Any miss on the $18.7B Q2 revenue guidance or HBM4 production timeline could trigger significant multiple compression.

The Bottom Line

Real talk: Institutional traders collected $7.6 million selling short calls at $350, capping their upside just 1.6% above current prices despite MU's record-breaking earnings, sold-out HBM capacity through 2026, and the NY megafab groundbreaking on January 16.

What this trade tells us:

- Near-term ceiling belief: Sophisticated traders see $350 as strong resistance after 247% rally

- Premium over direction: They'd rather collect premium than bet on continued breakout

- Calendar positioning: The $650/$690 LEAPS spread shows longer-term bullishness, but not urgency

- Risk management: After such an extended rally, protecting gains matters more than chasing upside

The paradox explained: The catalysts are genuinely bullish - HBM4 production ramp Q2 2026, record $18.7B revenue guidance, NY megafab groundbreaking January 16, and NVIDIA Rubin supply wins. However, good news is already priced into a stock up 247%. Premium sellers are betting the market has already discounted these catalysts, leaving limited upside and elevated downside risk.

If you own MU:

- Consider selling covered calls at $360-$375 to generate income while capping upside

- Set mental stops at $320-$330 (strong gamma support) to protect 2025 gains

- Don't add at current levels - wait for pullback to $320 range if you want more exposure

- Take partial profits on 25-30% of position to lock in gains after historic rally

If you're watching from sidelines:

- Patience is likely rewarded - better entries at $320-$330 probable within Q1 2026

- The groundbreaking event (Jan 16) creates short-term binary risk in either direction

- Focus on Q2 earnings (April 1) as the next major fundamental catalyst

- If you must enter, use put sales at support rather than buying calls at resistance

If you're considering premium selling:

- The $350 short call strategy aligns with institutional positioning

- Selling puts at $320-$330 strikes offers better risk/reward than buying stock at $345

- Use February-March expirations to capture theta decay before Q2 earnings uncertainty

Mark your calendar - Key dates:

- January 16, 2026 - NY Megafab Groundbreaking (Biden attending)

- February 2026 - HBM4 Large-Scale Co-Supply to NVIDIA begins

- February 6, 2026 - Short call expiration date

- Q2 2026 - HBM4 Production Ramp begins

- April 1, 2026 - Q2 FY2026 Earnings (record $18.7B revenue guidance)

- Mid-2027 - Idaho First Wafer Output (U.S. DRAM production begins)

Final verdict: Micron is executing at the center of an AI memory supercycle with genuinely strong fundamentals - Q1 revenue up 57% YoY, HBM capacity sold out through 2026, and targeting 30% HBM market share. The catalysts are real.

BUT - after a 247% rally with the stock at all-time highs, resistance at $345, and institutional traders selling $350 calls rather than buying them, the risk/reward favors patience over aggression. The short call activity isn't bearish - it's a statement that most of the good news is already priced in. Premium sellers win in consolidation scenarios, and consolidation is the most probable outcome.

The smart money is collecting premium. Consider doing the same rather than chasing a stock that's already run 247%.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Short call positions have unlimited loss potential if uncovered. Always do your own research and consider consulting a licensed financial advisor before trading.

About Micron Technology: Micron Technology designs and manufactures memory and storage products for computing, data center, mobile, embedded, and automotive applications, with a market cap of approximately $386 billion in the Semiconductors industry. Micron is the only U.S.-based memory manufacturer and a key supplier of HBM for AI accelerators.

Sources

- Micron Q1 FY2026 Earnings Release - Investor Relations

- Why Micron Stock Popped Today - Motley Fool

- Micron Has Started 2026 With a Bang - Motley Fool

- NY Megafab Groundbreaking - Tom's Hardware

- NVIDIA Vera Rubin Full Production - Digitimes

- NVIDIA CES 2026 Presentation - NVIDIA Blog

- AI Memory Supercycle - Chronicle Journal

- HBM4 Memory War - Financial Content

- Micron Enters Profit Supercycle - Seeking Alpha

- SK Hynix Micron Memory Wave - NAI 500

- China Bans Micron - Computerworld

- HBM Supercycle Overview - Introl