MU Massive $23M Bullish Call Sweep - AI Memory Supercycle Play!

January 20, 2026 | Unusual Activity Detected

The Quick Take

Someone just loaded up on $23 MILLION in deep out-of-the-money Micron calls expiring in July 2026! This massive bet consists of two separate trades - $13M on the $430 strike and $10M on the $470 strike - both targeting a 17-30% move higher from current levels. With HBM capacity sold out through 2026, DRAM prices surging 55-60% QoQ, and Q2 guidance calling for record $18.7B revenue, this trader is betting big on the AI memory supercycle continuing.

Company Overview

Micron Technology, Inc. (MU) is one of the largest semiconductor companies in the world, specializing in memory and storage chips:

- Market Cap: $408.3B

- Industry: Semiconductors & Related Devices

- Current Price: $364.40

- Employees: 53,000

- Primary Business: DRAM (79% of revenue) and NAND flash memory production serving data centers, mobile devices, consumer electronics, and automotive sectors

- Website: micron.com

The Option Flow Breakdown

What Just Happened

The Tape (January 20, 2026 @ 12:45:35):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot Price | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-20 | 12:45:35 | MU | BUY | CALL | 2026-07-17 | $13,000,000 | $430 | 3,600 | 40 | 2,520 | $364.40 | $50.50 | MU20260717C430 |

| 2026-01-20 | 12:45:35 | MU | BUY | CALL | 2026-07-17 | $10,000,000 | $470 | 3,600 | 37 | 2,520 | $364.40 | $40.36 | MU20260717C470 |

What This Actually Means

This is a massive bullish conviction play on Micron's AI-driven memory supercycle! Here's the breakdown:

- $23M total premium deployed: Two separate long call positions, same expiration, different strikes

- $430 strike trade: 18% OTM, paying $50.50 per contract for ~6 months of time value

- $470 strike trade: 29% OTM, paying $40.36 per contract - even more aggressive bet

- Volume/OI ratios of 90-97x: These strikes had almost no existing open interest - brand new positions being established

Translation for regular folks:

This trader is betting that MU hits $430+ by July 17, 2026. That's a move from $364 to $430 - roughly 18% upside. For the second leg at $470, they need a 29% move. These aren't lottery tickets - at $23M total, this is serious institutional capital making a directional bet on continued AI memory demand.

Breakeven analysis:

- $430 calls breakeven: ~$480 (strike + premium paid per contract)

- $470 calls breakeven: ~$510

- For max profit, MU needs to be significantly above these levels at July expiration

Technical Setup / Chart Check-Up

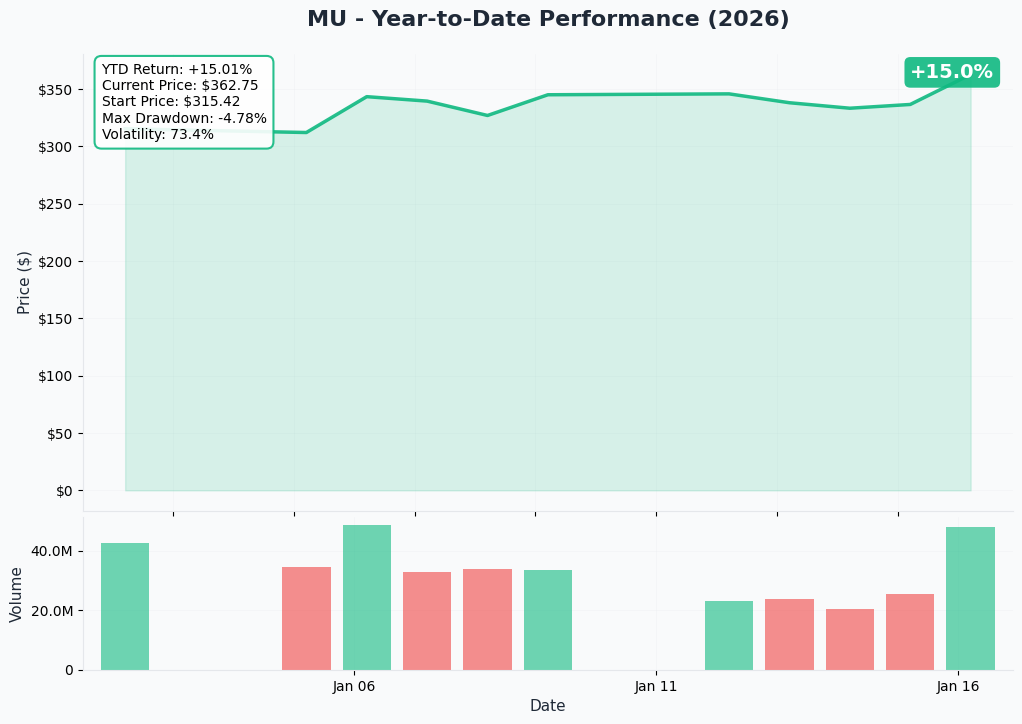

YTD Performance Chart

Micron has been on a tear, driven by the AI memory supercycle. According to Yahoo Finance, the stock is up 239% in 2025 alone, with shares currently trading at $364.40 after hitting a 52-week high of $365.81 on January 16, 2026.

Key observations:

- Strong momentum from HBM demand and DRAM pricing surge

- Stock jumped 10.5% on January 2, 2026 alone on positive analyst commentary

- Trading near all-time highs with continued bullish sentiment

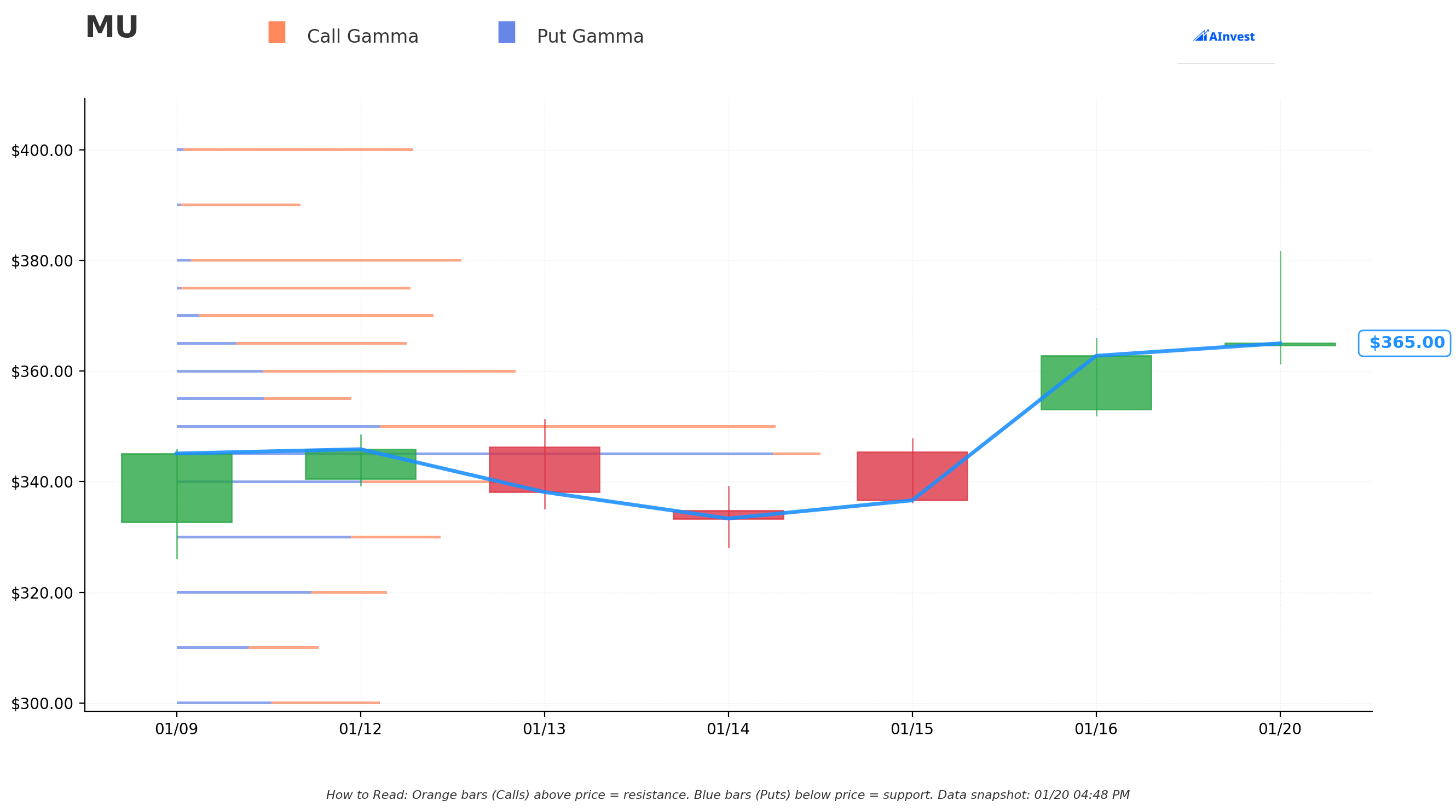

Gamma-Based Support & Resistance Analysis

Current Price: $367.24

The gamma exposure map reveals critical price magnets and walls around current levels:

Support Levels (Put Gamma Below Price):

- $365 - Immediate support with 4.2B total gamma (0.6% below)

- $360 - Secondary support with 6.2B gamma (2% below)

- $350 - Major floor with 10.9B gamma (4.7% below)

- $345 - Strong put gamma at 11.7B (6% below) - key level to watch

- $340 - Additional support at 5.8B gamma (7.4% below)

Resistance Levels (Call Gamma Above Price):

- $370 - First resistance with 4.7B gamma (0.75% above)

- $375 - Secondary ceiling at 4.3B gamma (2.1% above)

- $380 - Moderate resistance at 5.2B gamma (3.5% above)

- $400 - Major psychological level with 4.3B gamma (8.9% above)

What this means for traders:

The gamma data shows MU trading right above the strongest support at $365. Net GEX bias is bullish with 66.7B call gamma vs 46.0B put gamma. Market makers holding these positions will support the stock near $365 and create selling pressure approaching $380-$400. The trader buying these July calls is betting the stock breaks through these gamma levels on fundamental catalysts.

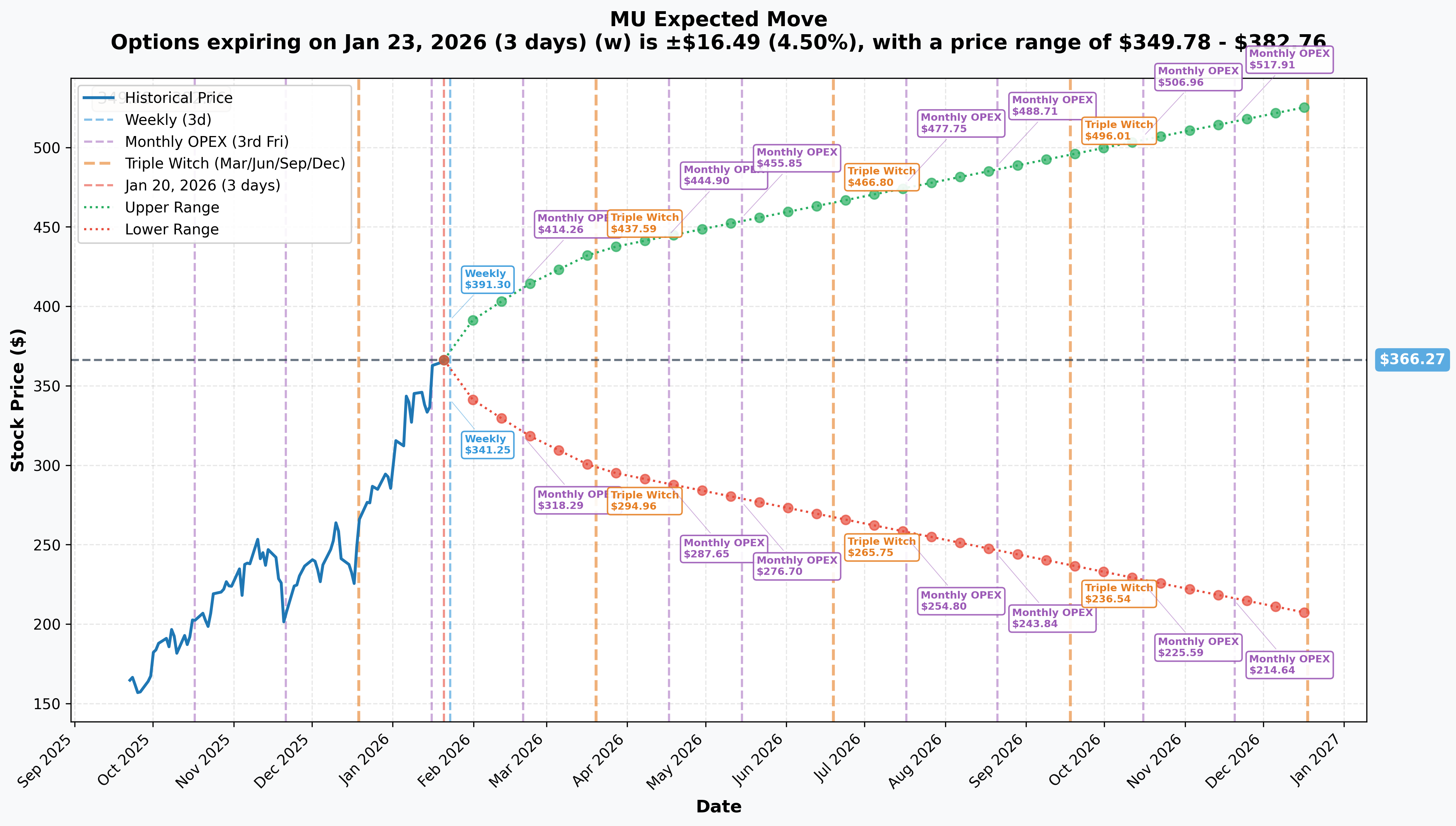

Implied Move Analysis

Options market pricing for upcoming expirations:

| Timeframe | Expiry Date | Days | Implied Move % | Implied Move $ | Upper Range | Lower Range |

|---|---|---|---|---|---|---|

| Weekly | 2026-01-23 | 3 | 4.5% | $16.49 | $382.76 | $349.78 |

| Monthly OPEX | 2026-02-20 | 31 | 12.66% | $46.37 | $412.64 | $319.91 |

| Triple Witch | 2026-03-20 | 59 | 18.84% | $69.00 | $435.27 | $297.28 |

| LEAPS | 2026-12-18 | 332 | 43.58% | $159.61 | $525.88 | $206.67 |

Translation:

Options traders are pricing in massive volatility for Micron:

- 4.5% weekly move - expect swings of $16+ in either direction this week

- 12.7% monthly move - range of $320-$413 by February OPEX

- 18.8% quarterly move - could see $297-$435 by March triple witch

- 43.6% yearly move - LEAPS pricing in $207-$526 range by year end

The July 2026 expiration for these call trades falls between the quarterly and yearly timeframes. The $430-$470 strike targets are within the implied move range for that timeframe, suggesting the market sees these as achievable (though aggressive) targets.

Catalysts

Past Catalysts (Already Happened)

Q1 FY2026 Record Results (December 17, 2025)

According to Micron Investor Relations, Micron delivered blowout numbers:

| Metric | Q1 FY2026 | YoY Change |

|---|---|---|

| Revenue | $13.64B | +57% |

| GAAP EPS | $4.60 | +157% |

| Non-GAAP EPS | $4.78 | +167% |

| Gross Margin | 57% | +20pp |

| Free Cash Flow | $3.9B | Record |

HBM4 Shipments Commenced (January 2026)

Per Micron Investor Relations, Micron announced shipment of HBM4 36GB 12-high samples with:

- 20%+ better power efficiency vs HBM3E

- Bandwidth exceeding 2.0 TB/s per stack (60% improvement)

- Data rates up to 11 Gbps

PSMC Acquisition LOI Signed (January 17, 2026)

According to TheStreet, Micron signed a $1.8B Letter of Intent to acquire Powerchip Semiconductor's Taiwan facility to boost DRAM wafer production capacity.

New York Megafab Groundbreaking (January 16, 2026)

Per Construction Owners, Micron broke ground on its $100B leading-edge memory manufacturing complex, supported by $6.4B in CHIPS Act funding.

Upcoming Catalysts

Q2 FY2026 Earnings (April 1, 2026)

According to MarketBeat, guidance calls for:

| Metric | Q2 FY2026 Guidance |

|---|---|

| Revenue | $18.7B (+/- $400M) |

| Gross Margin | 68% (+/- 100bps) |

| EPS (Non-GAAP) | $8.42 (+/- $0.20) |

This would represent 37% sequential revenue growth - a massive acceleration.

Memory Pricing Surge (Q1 2026)

According to TrendForce, memory prices are exploding:

- DRAM contract prices forecast to rise 55-60% QoQ in Q1 2026

- Server DRAM prices projected to increase over 60% QoQ

- NAND Flash prices expected to increase 33-38% QoQ

HBM4 Mass Production Ramp (H2 2026)

Per DigiTimes, HBM4 expected to enter full-scale production in second half of 2026, aligned with NVIDIA Rubin platform.

Key Dates Calendar:

| Date | Event |

|---|---|

| January 16, 2026 | New York Megafab Groundbreaking (Completed) |

| January 17, 2026 | PSMC Acquisition LOI Signed |

| Q2 2026 | PSMC Acquisition Expected Close |

| April 1, 2026 | Q2 FY2026 Earnings Release |

| H2 2026 | HBM4 Mass Production Ramp |

| Mid-2027 | First Idaho Fab First Wafer Output |

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts:

Bull Case (35% probability)

Target: $450-$500+

How we get there:

- Q2 earnings beat the already-strong $18.7B guidance with upside to $19-20B

- HBM4 ramp accelerates with additional design wins beyond NVIDIA

- DRAM pricing surge of 55-60% QoQ sustains through Q2-Q3

- Analyst price target upgrades continue (Rosenblatt at $500, Piper at $400)

- Memory supercycle narrative strengthens, multiple expansion

According to MarketBeat, the average analyst price target is $319.79 with a high of $500 from Rosenblatt. The options market implied move to December 2026 has an upper range of $525.88.

This is what the $23M call buyer is betting on - a continuation of the supercycle pushing MU toward $450-500 by July.

Base Case (45% probability)

Target: $380-$420

Most likely scenario:

- Q2 earnings meet guidance of $18.7B revenue, $8.42 EPS

- HBM capacity remains sold out, pricing holds strong

- Gamma resistance at $380-$400 gets tested and partially broken

- Stock consolidates gains near implied move upper range

- Analyst upgrades support current valuation

The July $430 calls would be marginally profitable in this scenario, while the $470 calls would likely expire worthless.

Bear Case (20% probability)

Target: $300-$350

What could go wrong:

- Memory cycle peak concerns materialize earlier than expected

- Samsung's aggressive HBM4 push compresses margins

- Q2 guidance comes in below elevated expectations

- Broader tech selloff on macro concerns

- Implied move lower range of $297.28 by March gets tested

According to FinancialContent, DCF models suggest fair value may be closer to $163, implying significant downside if peak margins normalize.

Key support: Strong gamma at $345-$350 should provide floor unless fundamentals deteriorate significantly.

Trading Ideas

Conservative: Wait for Pullback Entry

Play: Buy MU shares on pullback to gamma support

Why this works:

- Strong support at $350-$365 from gamma levels

- Implied move lower range at $349.78 for weekly expiration

- Q2 earnings catalyst on April 1 provides clear event to target

- Fundamentals (HBM sold out, pricing surge) support long-term bullish thesis

Entry: Look for pullback to $350-$360 range Position size: 50-100 shares depending on account size Stop loss: Below $340 (gamma support breakdown) Target: $400-$420 (gamma resistance zone)

Risk level: Moderate | Skill level: Beginner-friendly

Balanced: April Call Spread

Play: Bull call spread targeting Q2 earnings

Structure:

- Buy $380 calls, April 2026 expiration

- Sell $420 calls, April 2026 expiration

Why this works:

- Defined risk spread ($40 wide = max $4,000 risk per spread)

- Targets gamma resistance zone breakout on earnings catalyst

- Q2 guidance of $18.7B revenue / $8.42 EPS provides clear catalyst

- Captures upside if memory supercycle continues without unlimited risk

Estimated P&L:

- Max profit: ~$2,500-$3,000 per spread if MU at/above $420 at April expiration

- Max loss: Premium paid (~$1,000-$1,500 per spread)

- Breakeven: ~$390-$395

Risk level: Moderate (defined risk) | Skill level: Intermediate

Aggressive: Follow the Flow

Play: Replicate the institutional trade with smaller size

Structure:

- Buy July 2026 $430 calls (same as institutional trade)

- Position size: 1-5 contracts ($5,000-$25,000 exposure)

Why this could work:

- Following $23M institutional conviction bet

- 6 months of time value to capture HBM4 ramp and multiple earnings cycles

- Z-scores of 394+ indicate sophisticated buyers with edge

- Memory pricing surge could drive upside surprise

Why this could fail:

- 18% OTM requires significant move to profit

- Premium decay works against you over 6 months

- Cyclical peak could arrive before July expiration

- $50.50 per contract is expensive time premium

Estimated P&L:

- Breakeven: ~$480 (strike + premium)

- Max loss: 100% of premium paid (if MU below $430 at expiration)

- Profit scenarios: MU at $500 = ~$2,000 profit per contract; MU at $550 = ~$7,000 profit per contract

Risk level: HIGH (OTM options, time decay) | Skill level: Advanced

Risk Factors

Don't get caught by these potential landmines:

-

Cyclical peak concerns: According to FinancialContent, analysts anticipate Micron's earnings and margins will peak in 2026 or early 2027. The $20B CapEx plan historically signals cycle tops.

-

Valuation stretched: P/E ratio of 34.48 prices in peak margins as permanent. DCF models suggest fair value may be closer to $163, implying 50%+ downside if margins normalize.

-

Competition intensification: According to TechSpot, Samsung is staging an aggressive "counterattack" for 2026 targeting 30% HBM market share. SK Hynix maintains 53% share with deep NVIDIA partnership.

-

Potential oversupply risk (2027-2028): Per IO Fund, if SK Hynix or Samsung accelerate capacity expansions, the industry could move from shortage to oversupply. Memory markets are historically defined by "pig cycles" of overinvestment.

-

AI demand dependency: Primary risk is flattening of AI demand curve. Pullback in hyperscaler CapEx from Amazon or Microsoft could trigger price correction.

-

OTM options risk: The $430 and $470 strikes require 18-29% moves to be in the money. Time decay will erode premium over 6 months regardless of direction.

-

Geopolitical risks: CHIPS Act funding dependent on continued government support. Taiwan acquisition subject to regulatory approvals. Memory export restrictions to China remain a concern.

The Bottom Line

Real talk: Someone just dropped $23 million betting Micron hits $430-$470 by July 2026. That's not a gamble - that's conviction capital from sophisticated players who see the AI memory supercycle continuing.

What this trade tells us:

- Institutional money believes the HBM shortage and DRAM pricing surge extends through mid-2026

- The $430 strike (18% upside) aligns with analyst targets from Piper Sandler ($400) and momentum toward Rosenblatt's $500

- Same-day execution of both legs suggests coordinated institutional positioning

- Z-scores of 200-400 indicate this is extremely rare activity - sophisticated buyers with conviction

If you own MU:

- Hold through the supercycle but consider trimming if stock approaches $420-$430 gamma resistance

- Q2 earnings on April 1 is the next major catalyst - expect volatility

- Set mental stop below $345 gamma support to protect gains

- Monitor HBM pricing and Samsung competitive dynamics

If you're watching from sidelines:

- April 1, 2026 Q2 earnings is the moment of truth - mark your calendar

- Pullback to $350-$365 support would be attractive entry point

- Memory pricing data from TrendForce in coming weeks will signal direction

- Long-term thesis remains intact: HBM TAM projected to reach $100B by 2028

If you're bearish:

- Wait for signs of cyclical peak before initiating short positions

- Gamma support at $345-$350 is the first meaningful floor

- Watch for Samsung/SK Hynix capacity announcements signaling potential oversupply

- Put spreads offer defined risk way to play downside if cycle turns

The verdict: This is a high-conviction institutional bet on AI memory demand sustaining through mid-2026. With HBM capacity sold out, DRAM prices surging 55-60% QoQ, and Q2 guidance calling for record $18.7B revenue, the fundamentals support the bullish thesis. However, at 34x P/E near all-time highs, this is not a low-risk entry. The smart play is to wait for a pullback to gamma support or confirm the Q2 beat before committing significant capital.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. The extremely unusual Z-scores reflect this specific trade's size relative to recent history - they do not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading.

About Micron Technology, Inc.: Micron is one of the largest semiconductor companies in the world with a $408.3B market cap, specializing in memory and storage chips (DRAM and NAND) serving data centers, mobile devices, consumer electronics, and automotive sectors.