🛡️ MU Massive $42M Put Hedge - Smart Money Buying Insurance on Memory Supercycle Rally!

📅 January 28, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $42 MILLION on MU puts this morning at 09:37:59! This monster trade bought nearly 10,000 contracts of $390 strike puts expiring May 15th - protecting a massive position while Micron trades near all-time highs at $429.54 after an incredible 242% rally in 2025. With Q2 FY2026 earnings expected in March and HBM4 ramp uncertainties, smart money is locking in downside protection at the peak. Translation: An institution just paid $42M for an insurance policy on what could be a billion-dollar memory chip position.

📊 Company Overview

Micron Technology (MU) is one of the largest semiconductor companies in the world, specializing in memory and storage chips at the center of the AI boom:

- Market Cap: $461.7 Billion

- Industry: Semiconductors & Related Devices

- Current Price: $429.54 (near all-time high of $416.45 - already above prior 52-week high)

- Employees: 53,000 globally

- Primary Business: DRAM, NAND flash, and High Bandwidth Memory (HBM) for data centers, AI, mobile, automotive, and consumer electronics

💰 The Option Flow Breakdown

The Tape (January 28, 2026 @ 09:37:59):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:37:59 | MU | ASK | BUY | PUT $390 | 2026-05-15 | $42M | $390 | 10K | 137 | 9,819 | $429.54 | $43.00 |

🤓 What This Actually Means

This is a massive defensive hedge on a large long MU position! Here's what went down:

- 💸 Huge premium paid: $42M ($43.00 per contract x 9,819 contracts)

- 🛡️ Protection strike: $390 provides 9.2% downside cushion below current price

- ⏰ Strategic timing: 107 days to expiration captures Q2 FY2026 earnings (March), HBM4 production ramp updates, and DRAM pricing data through May

- 📊 Size matters: 9,819 contracts represents 981,900 shares worth ~$421M at current prices

- 🏦 Institutional insurance: This is sophisticated portfolio hedging, not a bearish bet

- 🔥 Vol/OI Ratio: 72.99x - This is off the charts! Volume was nearly 73 TIMES the existing open interest of just 137 contracts

What's really happening here: This trader likely holds a MASSIVE long position in MU accumulated during the memory supercycle rally. With the stock up 242% in 2025 and another 36% in January 2026 alone, they're paying $43.00 per share for the May 15 $390 puts as insurance. If MU drops below $390 by May 15th, these puts pay off dollar-for-dollar. Think of it like buying a $42M homeowner's policy when you live in a mansion worth hundreds of millions - you hope you never use it, but you sleep much better at night.

Unusual Score: 🔥 EXTREME - The Z-Score of 438.04 means this trade is roughly 438x the average size. That kind of activity shows up maybe a handful of times per year across all tickers. The Vol/OI ratio of 72.99x confirms this is entirely NEW positioning - there was virtually no open interest at this strike before today. Someone deliberately chose this strike and expiration to build a fresh hedge from scratch.

📈 Technical Setup / Chart Check-Up

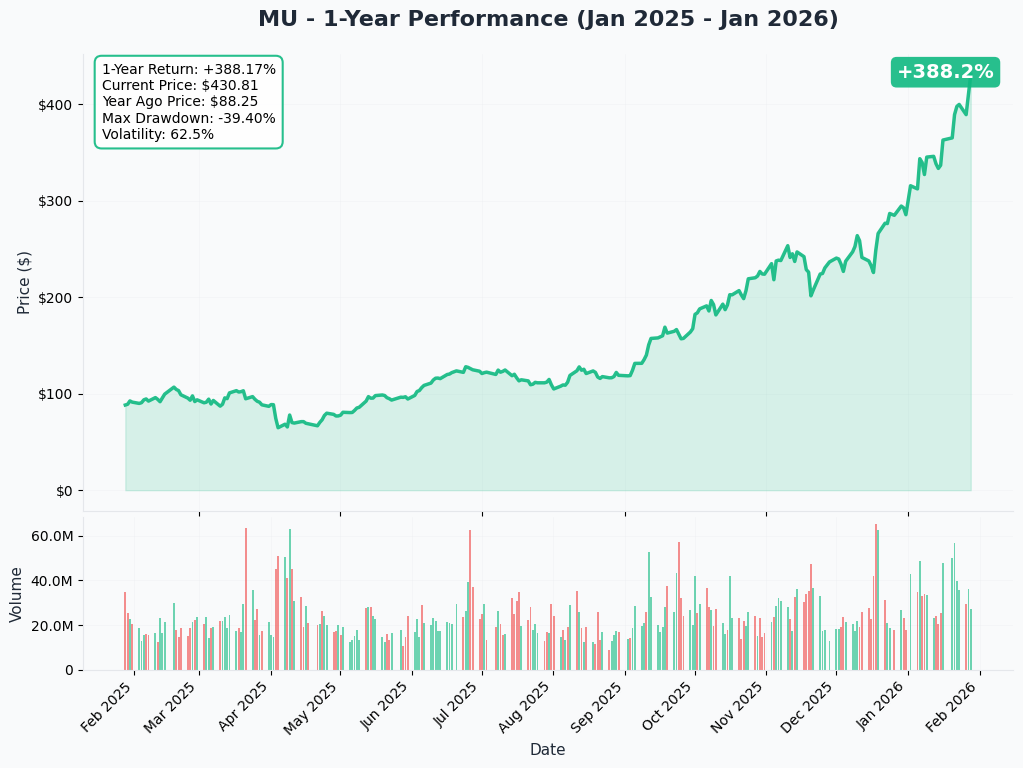

YTD Performance Chart

MU has been one of the best-performing mega-cap stocks over the past year - the AI memory supercycle is real and Micron is at the center of it. The stock rallied from the $60s in early 2025 to $429+ today, driven by record HBM demand, surging DRAM prices, and sold-out capacity through 2026.

Key observations:

- 🚀 Parabolic rally: 242% gain in calendar 2025, then another 36% in January 2026 alone

- 📈 52-week range blown wide open: Prior high was $416.45 - stock is now in uncharted territory above that

- 🎢 High momentum: 3%+ gain on January 27 alone after the $24B Singapore fab announcement

- 📊 Volume surge: Institutional accumulation accelerating as analysts raise targets to $500

- ⚠️ Extended territory: After this kind of vertical move, consolidation or pullback risk is elevated

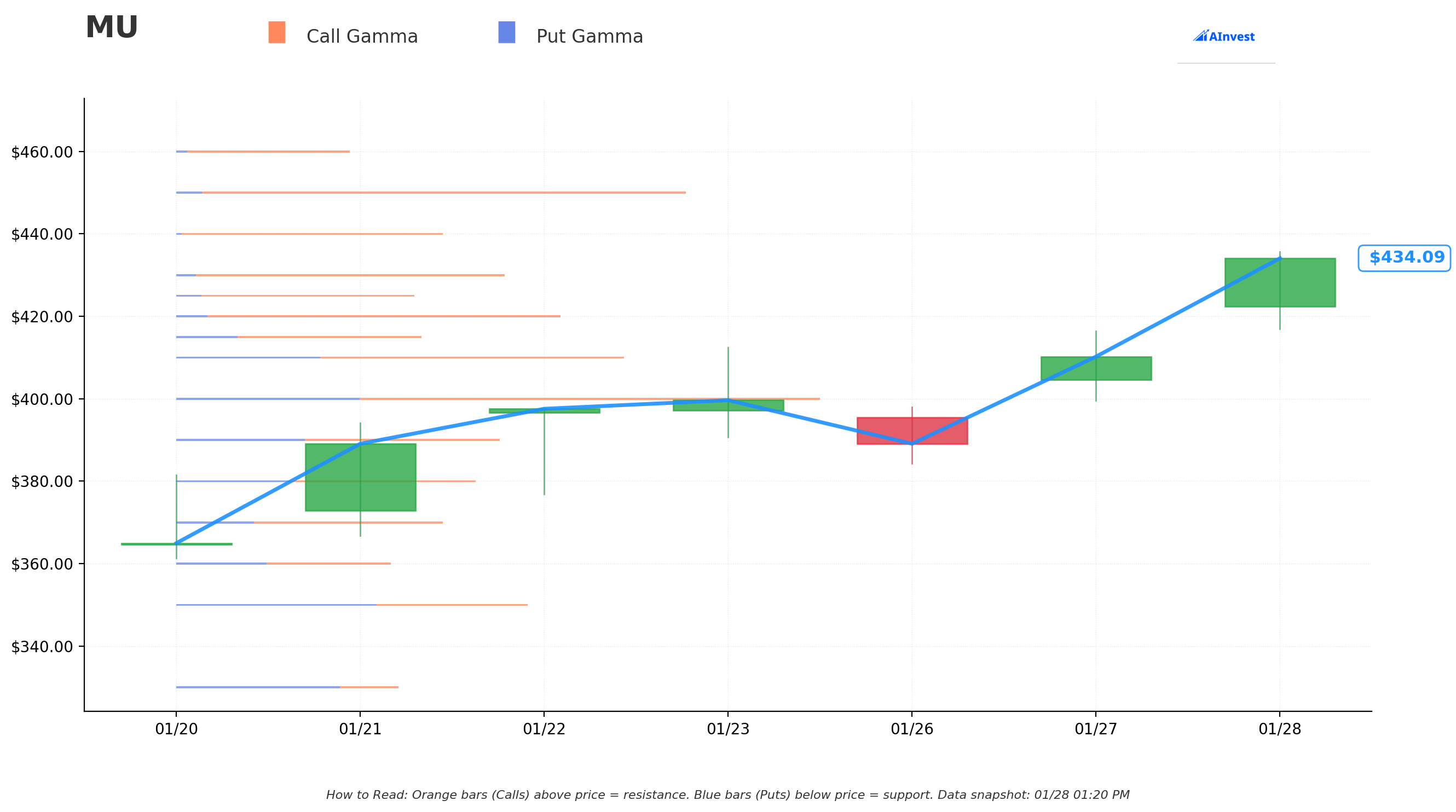

Gamma-Based Support & Resistance Analysis

Current Price: $434.01

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $430 - Immediate support with 3.8B total gamma exposure (closest floor, just 0.9% below)

- $420 - Secondary support at 4.4B gamma (3.2% below - dealers will buy dips here)

- $410 - Structural support with 5.2B gamma (5.5% below - significant put gamma builds here)

- $400 - MAJOR floor with 7.5B gamma (STRONGEST SUPPORT - 7.8% below, this is the LINE IN THE SAND)

- $390 - Deep support at 3.8B gamma (10.1% below - EXACTLY WHERE THIS PUT IS STRUCK!)

- $380 - Extended support zone with 3.5B gamma (12.4% below)

- $370 - Deep buffer at 3.1B gamma (14.7% below)

- $350 - Disaster floor at 4.1B gamma (19.4% below - net gamma turns negative here)

🟠 Resistance Levels (Call Gamma Above Price):

- $440 - Immediate ceiling with 3.1B gamma (1.4% overhead)

- $450 - Major resistance at 5.8B gamma (STRONGEST RESISTANCE - 3.7% above current price)

What this means for traders: MU is trading in a zone between $430 support and $440 resistance. The $400 level stands out as THE critical support with 7.5B total gamma - the single strongest level on the board. Below that, $390 (where this put is struck) has meaningful gamma but not enough to act as an impenetrable floor.

Notice anything? The put buyer struck at $390 - just below the massive $400 gamma wall. They're positioning for a scenario where if MU cracks through the $400 support, momentum could accelerate lower toward $390 and beyond. Smart hedging at a technically significant level.

Net GEX Bias: Bullish (73.2B call gamma vs 31.5B put gamma) - Overall dealer positioning heavily skewed bullish, but the upside resistance levels are thinner than support, suggesting the move higher is getting stretched.

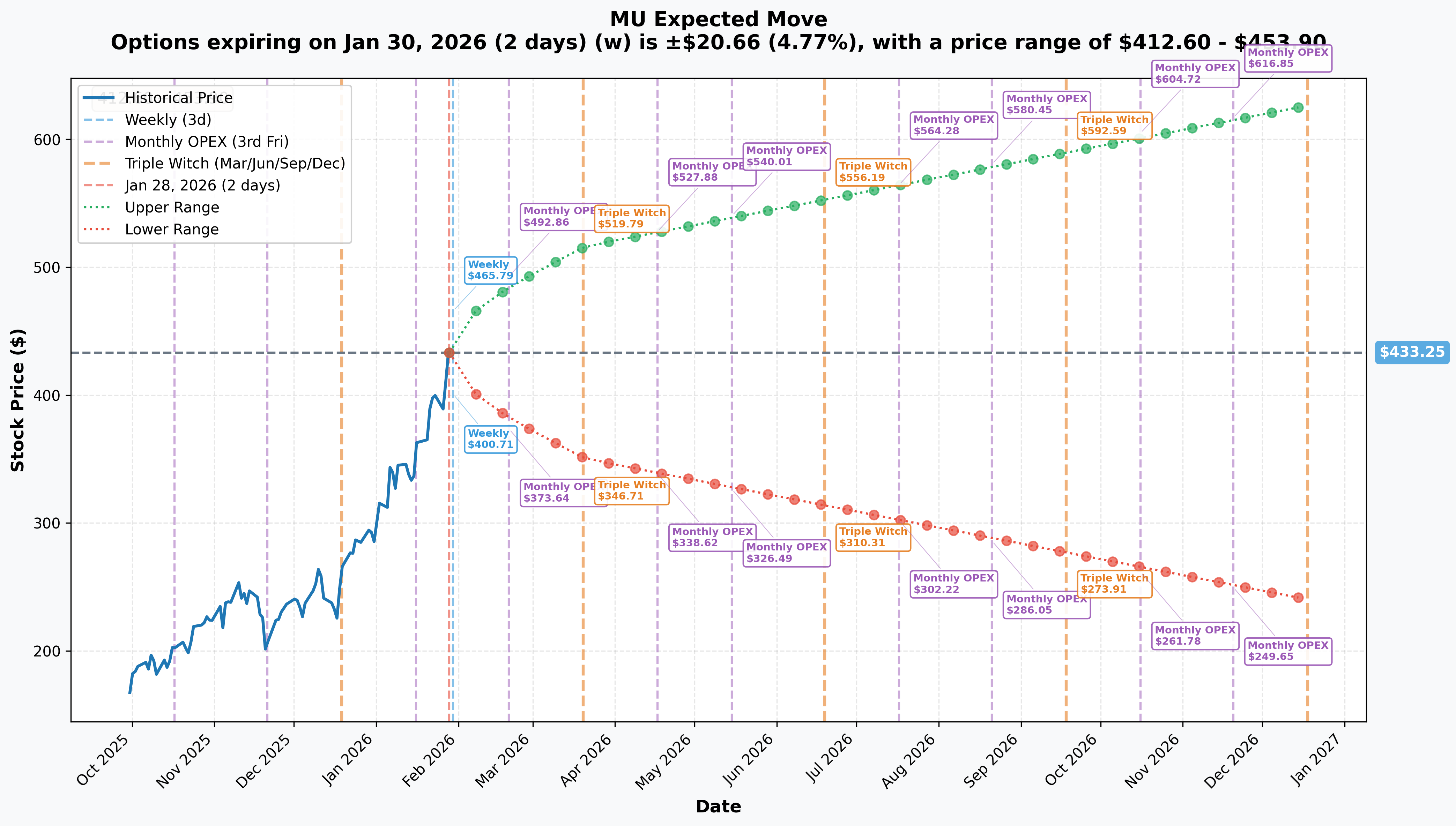

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 30 - 2 days): ±$20.66 (±4.77%) → Range: $412.60 - $453.90

- 📅 Monthly OPEX (Feb 20 - 23 days): ±$51.85 (±11.97%) → Range: $381.40 - $485.10

- 📅 Quarterly Triple Witch (Mar 20 - 51 days): ±$82.90 (±19.13%) → Range: $350.35 - $516.15

- 📅 May OPEX (May 15 - THIS TRADE!): Implied range: $326.49 - $540.01

Translation for regular folks: Options traders are pricing in a 4.8% move ($21) by Friday for weekly expiration, and a MASSIVE 12% move ($52) through February OPEX which could include early Q2 earnings guidance leaks or HBM4 production updates. The market expects big swings - that's extreme for a $462B company!

The May 15th expiration (when this $42M trade expires) has a lower range of $326.49 - meaning the market thinks there's a real possibility MU could trade below $330 over the next 107 days in a worst-case scenario. The put buyer's $390 strike sits well above that floor, suggesting they're not betting on catastrophe - they're hedging against a moderate 10-15% correction that would still leave the stock in an uptrend.

Key insight: The steep increase from 4.8% (weekly) to 19.1% (March Triple Witch) reflects massive uncertainty around Q2 earnings and the HBM4 ramp. The memory chip cycle is historically volatile, and the options market knows it.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

DRAM/NAND Pricing Data - Q1 2026 Contract Settlements 📊

Memory pricing remains THE key fundamental driver for MU. TrendForce forecasts for Q1 2026 show:

- 📈 Conventional DRAM: +55-60% QoQ price increases

- 🚀 Server DRAM: +60%+ QoQ (largest gains in the memory complex)

- 💾 NAND Flash: +33-38% QoQ price gains

- 💻 Client SSDs: +40%+ QoQ (strongest NAND category)

These are EXTREME price increases by any historical standard. If they hold, Q2 earnings will be a blowout. If they soften, the stock could correct sharply.

HBM4 Mass Production Ramp - End of Q1 2026 🏭

HBM4 mass production was delayed to end of Q1 2026 due to NVIDIA spec upgrades requiring speeds above 11 Gbps:

- 🔬 Micron confirmed HBM4 achieves industry-leading speeds above 11 Gbps on 1-beta node

- 🎯 HBM4 capacity target: 15,000 wafers/month by end of 2026 (~30% of total HBM output)

- ⚠️ Any further delays or yield issues could impact the stock significantly

- 🏆 All three memory suppliers (SK Hynix, Samsung, Micron) are competing for NVIDIA Rubin qualification

🚀 Near-Term Catalysts (Q1-Q2 2026)

Q2 FY2026 Earnings - Expected March 19-25, 2026 📊

This is THE big one. Micron's guidance for Q2 is nothing short of jaw-dropping:

- 📊 Revenue: $18.7B (+/- $400M), implying 132% YoY growth - this would be the LARGEST single quarter in Micron history

- 💰 EPS: $8.42 (+/- $0.20), up from $4.78 in Q1 (76% sequential growth!)

- 📈 Gross Margin: ~68% (+/- 1%), up from 56.8% in Q1 - approaching software-company margins for a CHIP maker

- 🤖 HBM Revenue: Annualized run-rate of $8B and growing

- 📊 Analyst consensus: Revenue $18.78B, EPS $8.22-$8.25

Why this matters for the put trade: The May 15 expiration captures this earnings report AND the market's reaction. If Micron misses even slightly on that $18.7B guidance or signals HBM4 ramp issues, the stock could give back 15-20% rapidly. At $429, expectations are sky-high.

$24B Singapore Fab Groundbreaking (January 27, 2026) 🏗️

Micron just broke ground on a massive new facility:

- 🏭 ~$24B (SG$31B) investment over 10 years; 700,000 sq ft of cleanroom space

- 🌏 Singapore's first double-story wafer fab; output scheduled for H2 2028

- 👷 Creates ~1,600 new jobs (3,000 total with HBM packaging facility)

- 📈 Total Singapore investment now exceeds $60B since 1998

- 💾 Micron produces 98% of its flash memory chips in Singapore

NVIDIA Vera Rubin Platform - H2 2026 🤖

Jensen Huang confirmed at CES 2026 that Vera Rubin entered full production:

- 💥 Rubin GPUs will use HBM4 exclusively - this is THE demand driver for Micron's next-gen memory

- 🏭 Volume availability expected H2 2026

- 📊 NVIDIA reportedly requested 16-Hi HBM delivery by Q4 2026, triggering development sprints across all three suppliers

- 🎯 Winning Rubin qualification = massive multi-year revenue stream; losing = significant share loss risk

📊 Recent Catalysts (Already Happened)

Q1 FY2026 Record Earnings (December 17, 2025) ✅

- 📊 Revenue: $13.64B (record), beating consensus by $640M-$1.02B

- 💰 EPS: $4.78, beating consensus of $3.77 by $1.01 (27% beat!)

- 📈 Gross Margin: 56.8%, up 11 percentage points sequentially

- 💵 Free Cash Flow: $3.9B (record)

- ☁️ Cloud Memory revenue: $5.3B, up 100% YoY

Consumer Market Exit (December 2025) 🔄

Micron announced wind-down of its Crucial consumer brand by end of January 2026:

- 🎯 Reallocating consumer output to higher-margin enterprise/AI products

- 💬 CEO Mehrotra stated Micron can only meet "half to two-thirds" of current demand

- ⚠️ DRAM drought could last until at least 2028 per management commentary

CHIPS Act Funding - $6.4B+ Secured (June 2025) 🇺🇸

Micron secured expanded U.S. investments:

- 🏗️ Approximately $150B in domestic manufacturing and $50B in R&D commitments

- 💰 Up to $6.4B in CHIPS Act direct funding for Idaho and New York fabs

- 👷 Expected to create ~20,000 jobs

HBM Capacity Sold Out Through 2026 🔒

Micron confirmed its entire calendar 2026 HBM supply is under price and volume agreements, including HBM4. This provides extraordinary revenue visibility - but also means any demand disappointment is unlikely to show in the numbers until 2027.

📈 Analyst Consensus

Street is overwhelmingly bullish: 26 Buy, 2 Hold, 0 Sell = Strong Buy

| Analyst | Rating | Price Target |

|---|---|---|

| HSBC (Ricky Seo) | Buy | $500 (Street High) |

| Rosenblatt | Buy | $500 |

| JPMorgan | Overweight | $350 |

| Morgan Stanley | Overweight | $350 |

| Bernstein | Outperform | $330 |

Insider Activity: 5 recent transactions totaling $10.23M between January 2-14, 2026, including 3 purchases. Notably, insider Teyin Liu made a $7.8M purchase - management is putting their own money where their mouth is.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through the May 15th expiration:

📈 Bull Case (30% probability)

Target: $480-$540

How we get there:

- 💪 Q2 earnings CRUSH the already-elevated $18.7B guidance, coming in at $19B+ with 70%+ gross margins

- 🚀 HBM4 qualification with NVIDIA confirmed ahead of schedule - Micron captures 25%+ HBM4 share

- 📈 DRAM pricing holds at +55-60% QoQ through Q2, exceeding TrendForce forecasts

- 🤖 NVIDIA Rubin volume ramp validates massive HBM demand thesis

- 📊 Analysts raise targets above $500 as HSBC's $84B FY2026 sales projection gains credibility

- 🏗️ Additional capacity expansion announcements signal long-term growth confidence

- 📈 Implied move upper range at May OPEX: $540.01

Probability assessment: 30% because the fundamental backdrop is genuinely exceptional - sold-out HBM, record DRAM pricing, and accelerating AI demand. But the stock has already priced in significant upside, and memory cycles can turn faster than expected.

🎯 Base Case (45% probability)

Target: $400-$460 range (CONSOLIDATION AFTER MASSIVE RUN)

Most likely scenario:

- ✅ Q2 earnings meet guidance (~$18.5-18.9B revenue, $8.20-$8.50 EPS)

- 📈 DRAM pricing remains strong but sequential gains moderate from +55-60% to +20-30% in Q2

- 🏭 HBM4 ramp progresses on schedule but without dramatic upside surprise

- ⚖️ Market digests the 242% rally from 2025 - profit-taking creates natural selling pressure

- 🔄 Stock consolidates between $400 gamma support and $450 gamma resistance

- 📊 Forward P/E of 10.5x seen as reasonable but not screaming cheap given cyclicality risk

- 💤 Volatility compresses post-earnings as uncertainty resolves

This is the put buyer's expected scenario: Stock chops around in the $400-450 zone, puts expire with little to no value, but the $42M insurance premium was worth paying for peace of mind during a period of maximum uncertainty. When you're protecting hundreds of millions in unrealized gains, $42M is a rounding error.

Why 45% probability: The fundamental story is intact (sold-out HBM, record pricing), but the stock has moved so far so fast that consolidation is the natural next step. Most analysts already have targets at or near current prices.

📉 Bear Case (25% probability)

Target: $330-$390 (PUT PAYS OFF!)

What could go wrong:

- 😰 Q2 earnings miss or guidance disappoints - even a small miss at this valuation could trigger -15-20% gap down

- 🚨 HBM4 yield issues or further production delays beyond Q1 2026 - SK Hynix could capture 70% HBM4 share if Micron falls behind

- 📉 DRAM pricing cycle peaks and starts to reverse - memory stocks are NOTORIOUS for crashing when pricing turns

- 💸 Hyperscaler AI capex pullback (even temporary) crushes cloud memory demand (56% of Micron's revenue)

- 🇨🇳 New China export restrictions remove addressable market

- 🔨 Break below $400 gamma support triggers cascade to $390, then $370

- 📊 Memory cycle mean-reversion: historically, 55-60% QoQ price increases are NOT sustainable

Critical support levels:

- 🛡️ $400: Major gamma floor (7.5B - STRONGEST LEVEL) - MUST HOLD or momentum shifts bearish

- 🛡️ $390: Deep support (3.8B gamma) + this put strike - this is where the hedge activates

- 🛡️ $350: Disaster floor (4.1B gamma) - net gamma turns negative here, meaning selling could accelerate

Put P&L in Bear Case:

- Stock at $370 on May 15: Puts worth $20.00, loss reduced to $23.00/share (puts offset $20 of decline)

- Stock at $350 on May 15: Puts worth $40.00, loss reduced to $3.00 net cost on puts (nearly breakeven on hedge)

- Stock at $330 on May 15: Puts worth $60.00, profit = $17.00/share x 9,819 = $16.7M gain on puts

- Stock at $390 on May 15: Puts expire at-the-money, loss = $43.00 x 9,819 = $42.2M (full premium lost)

Probability assessment: 25% because it requires the memory cycle to turn or significant execution stumbles. But memory markets ARE cyclical - the current +55-60% QoQ DRAM pricing is historically extreme and unsustainable long-term. The put buyer clearly thinks this scenario has material probability, or they wouldn't spend $42M on protection.

💡 Trading Ideas

🛡️ Conservative: Wait for Q2 Earnings Clarity

Play: Stay on sidelines until March Q2 earnings report resolves the biggest uncertainty

Why this works:

- ⏰ Q2 earnings (March 19-25) is the next MAJOR catalyst - creating binary event risk with ±19% implied move through Triple Witch

- 💸 Options are EXPENSIVE right now - implied volatility reflects massive uncertainty around the memory cycle

- 📊 Stock trading at all-time highs after 278% rally (2025 + January 2026) - zero margin of safety at current levels

- 🎯 Better entry likely post-earnings after IV crush reduces option premiums significantly

- 📉 Memory stocks have a nasty habit of peaking BEFORE the pricing cycle turns - don't be the last one in

- 🤔 The $42M institutional put buy signals sophisticated players are WORRIED despite bullish fundamentals

Action plan:

- 👀 Monitor DRAM/NAND contract pricing data from TrendForce for any signs of price stabilization

- 🎯 Look for pullback to $400-$410 gamma support post-earnings for stock entry with 5-10% margin of safety

- ✅ Need to see Q2 actual results vs $18.7B guidance and updated Q3 outlook before committing capital

- 📊 Watch HBM4 qualification news from NVIDIA - confirmed qualification = green light

- ⏰ Revisit after March earnings when the picture is clearer

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -15-20% drawdown if the memory cycle shows any cracks. Get better entry if stock consolidates.

⚖️ Balanced: Post-Earnings Put Spread (Follow the Smart Money)

Play: After Q2 earnings volatility settles, buy a put spread mirroring institutional positioning

Structure: Buy $410 puts, Sell $390 puts (May 15 expiration - SAME expiration as the $42M trade)

Why this works:

- 🎢 IV crush after earnings makes put spreads much cheaper - buy AFTER volatility drops

- 📊 Defined risk spread ($20 wide = $2,000 max risk per spread)

- 🎯 Targets the $390-$410 gamma support zone where institutions are clearly positioned

- 🤝 Essentially "following" the smart money positioning at better prices post-IV crush

- ⏰ 50+ days remaining after earnings gives time for any memory cycle concerns to materialize

- 🛡️ Protects against "sell the news" scenario even if Q2 earnings beat

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Pay ~$6-8 net debit per spread post-earnings

- 📈 Max profit: $1,200-$1,400 if MU below $390 at May expiration

- 📉 Max loss: $600-800 if MU above $410 (defined and limited)

- 🎯 Breakeven: ~$402-404

- 📊 Risk/Reward: ~1.5:1 which is favorable for defined-risk play

Entry timing:

- ⏰ Wait 2-3 days after Q2 earnings (by March 22-25) for full IV collapse

- 🎯 Only enter if stock still trades above $420 (gives room to work)

- ❌ Skip if stock already below $400 (spread too close to at-the-money)

Position sizing: Risk only 2-5% of portfolio

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

🚀 Aggressive: Earnings Straddle - Bet on the Memory Cycle Fireworks (ADVANCED ONLY!)

Play: Buy straddle betting that Q2 earnings move exceeds implied expectations

Structure: Buy $430 calls + Buy $430 puts (March 20 Triple Witch expiration to capture earnings reaction)

Why this could work:

- 💥 Memory earnings historically produce OUTSIZED moves - 15-25% gaps are common when the cycle turns

- 🎰 Market may be UNDERPRICING the binary risk: $18.7B guidance is so extreme that any miss will be devastating, and any beat will be euphoric

- 📊 At 39x TTM P/E for a cyclical chip maker, the stock could EXPLODE either direction

- ⚡ HBM4 qualification news could drop alongside earnings, creating a double catalyst

- 🚀 Only need stock to move >15% either way to profit given high IV

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Straddle likely costs $60-80 per share ($6,000-8,000 per straddle) given elevated IV

- ⏰ TIME DECAY KILLER: Theta burns rapidly as earnings approaches

- 😱 IV CRUSH: Even if stock moves 10-12%, IV collapse could still result in LOSS on both legs

- 📊 Two-way risk: Stock could report in-line and barely move, destroying the straddle

- 🎢 Need 15%+ move to breakeven after IV crush

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded straddles through earnings before and understand IV crush mechanics

- ✅ Can afford to lose ENTIRE premium

- ✅ Understand you're betting AGAINST the options market's implied probability

- ✅ Can close the position within 24-48 hours post-earnings

- ✅ Accept that even being RIGHT on direction may not save you from IV crush

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35% (lower than implied due to IV crush dynamics)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q2 earnings binary event approaching (March 2026): Revenue guidance of $18.7B is the highest single-quarter target in Micron's history. That's a 132% YoY growth rate and 37% sequential growth. Even a small miss on that number could trigger a 15-20% selloff given the stock's vertical trajectory. Options pricing ±19% implied move through March Triple Witch, and memory stocks have historically delivered moves that large.

-

🎢 Memory cycle risk - DRAM pricing is historically extreme: DRAM contract prices surging 55-60% QoQ is NOT normal. Memory markets are notoriously cyclical with violent boom/bust dynamics. Every memory supercycle in history has ended with a sharp pricing correction. The question isn't IF pricing normalizes - it's WHEN. Any signs of demand cooling, inventory build, or capacity coming online faster than expected could trigger the reversal.

-

🏆 SK Hynix competitive dominance in HBM: SK Hynix holds 62% HBM market share vs Micron's 21%. UBS forecasts SK Hynix could capture 70% of HBM4 market share given their deep NVIDIA relationship. If Micron fails to win meaningful Rubin allocation, the highest-growth segment of the business could stall.

-

🔬 HBM4 yield and production risk: Mass production was already delayed to end of Q1 2026 due to NVIDIA spec changes. Further delays, yield issues, or performance shortfalls could push revenue recognition to the right and damage investor confidence. The 3:1 HBM trade ratio (every HBM bit consumes ~3x standard DRAM capacity) means HBM production directly constrains conventional DRAM supply.

-

📊 Valuation after 278% rally: At $429/share and $462B market cap, MU trades at 39x TTM earnings. Even at a seemingly cheap 10.5x forward P/E, that forward estimate assumes PERFECT execution on a $18.7B quarter and continued pricing strength. Memory companies historically trade at LOW multiples at cycle PEAKS because the market knows earnings will decline. Buying a cyclical stock at peak earnings with expectations of continued growth is one of the most common mistakes in semiconductor investing.

-

🐋 Smart money buying $42M insurance at the peak: This institutional put purchase - with a Vol/OI ratio of 72.99x and Z-Score of 438 - signals sophisticated players are WORRIED about downside despite the incredible fundamental backdrop. When funds managing billions pay $42M for puts rather than staying fully long at all-time highs, it's a major caution flag. This isn't normal hedging volume - it's deliberate, large-scale protection.

-

🌏 Geographic concentration risk: Micron produces 98% of its flash memory in Singapore with additional facilities in Japan and Taiwan. Any geopolitical disruption, natural disaster, or regulatory change affecting these regions could impact production. China export restrictions remain an ongoing risk for the broader memory addressable market.

-

💰 AI capex pullback risk: Cloud Memory (CMBU) revenue surged to $5.3B in Q1, representing the fastest-growing segment. Any slowdown in hyperscaler AI spending - even a temporary pause for infrastructure digestion - would disproportionately impact Micron given its 56% data center revenue concentration.

-

🏗️ Capacity coming online in 2027-2030: New fabs in Idaho (mid-2027), Singapore (H2 2028), and New York (~2030) will eventually alleviate the memory shortage. When supply catches up to demand, the pricing supercycle ends - and memory companies historically give back 40-60% of peak-cycle gains in the correction.

🎯 The Bottom Line

Real talk: Someone just spent $42 MILLION buying protection on a massive MU position while the stock trades at all-time highs after a 278% rally. This isn't bearish on Micron's long-term AI memory story - it's smart risk management by an institution that has made ENORMOUS money on the memory supercycle and doesn't want to give it back in one bad earnings print or cycle turn.

What this trade tells us:

- 🎯 Sophisticated player expects VOLATILITY through May (not necessarily crash, but protecting against a 10-15% correction scenario)

- 💰 They're worried enough about $430 dropping to $390 to pay $43.00/share for insurance (10% of stock price!)

- ⚖️ The Vol/OI ratio of 72.99x proves this is entirely NEW positioning - no existing open interest at this strike before today

- 📊 They structured at $390 strike (9.2% below current) which sits just below the massive $400 gamma wall - expects that IF the stock breaks $400, momentum accelerates to $390

- ⏰ May 15th expiration captures Q2 earnings (March), HBM4 production ramp, DRAM pricing updates, and early NVIDIA Rubin signals

This is NOT a "sell everything" signal - it's a "I've made incredible money and I'm protecting my gains" signal.

If you own MU:

- ✅ Consider trimming 20-30% at $425-440 levels (locking in multi-bagger gains is never wrong)

- 📊 If holding through Q2 earnings, set mental stop at $400 (major gamma support) to protect remaining position

- ⏰ Don't get greedy - you've already won! Up 278% is extraordinary for any stock. Protecting profits is smart.

- 🎯 If Q2 earnings beat AND HBM4 qualification confirmed, could re-enter trimmed shares on momentum toward $500

- 🛡️ Consider buying 1-2 protective puts per 100 shares if holding a large position

If you're watching from the sidelines:

- ⏰ March Q2 earnings is the moment of truth - DO NOT chase the stock at all-time highs before a major catalyst!

- 🎯 Post-earnings pullback to $390-$410 would be an excellent entry (10-15% off highs with gamma support)

- 📈 Looking for confirmation of: Q2 revenue hitting $18.7B+, HBM4 NVIDIA qualification, sustained DRAM pricing, and updated FY2026 capex guidance

- 🚀 Longer-term (6-12 months), the NVIDIA Rubin HBM4 ramp and $150B U.S. manufacturing commitment are legitimate catalysts for $500+ if execution delivers

- ⚠️ Current valuation after 278% rally requires continued pricing strength and HBM share gains - one stumble and it's back to $350-$380

If you're bearish:

- 🎯 Wait for Q2 earnings before initiating shorts - fighting memory supercycle momentum at all-time highs is extremely dangerous

- 📊 First support at $430 (gamma), major support at $400 (7.5B gamma wall), deep support at $390 (put strike)

- ⚠️ Post-earnings put spreads ($410/$390) offer defined-risk way to play downside after IV crush

- 📉 Watch for break below $400 - that's the trigger for cascade to $390, then $370

- ⏰ Memory cycles turn FAST when they turn - if you see DRAM contract prices flatten or decline, act quickly

Mark your calendar - Key dates:

- 📅 January 30 (Friday) - Weekly OPEX (±4.8% implied move)

- 📅 February 20 - Monthly OPEX (±12% implied move window)

- 📅 March 19-25 (estimated) - Q2 FY2026 earnings report (THE BIG ONE)

- 📅 March 20 - Quarterly Triple Witch (±19% implied move window)

- 📅 May 15 - Monthly OPEX, expiration of this $42M put trade

- 📅 H2 2026 - NVIDIA Vera Rubin volume production begins

Final verdict: Micron's fundamental story is the best it's been in the company's 42-year history - sold-out HBM capacity, record DRAM pricing, $18.7B quarterly revenue guidance, 68% gross margins, and NVIDIA Rubin demand on the horizon. BUT, at $429 after a 278% rally, with memory cycle peak risk and Q2 earnings approaching, the risk/reward is NO LONGER favorable for aggressive new positioning. The $42M institutional put buy is a CLEAR signal: smart money is locking in protection at the peak.

Be patient. Let Q2 earnings clear. Look for better entry points at $390-$410. The AI memory supercycle will still be here in 2-3 months, and you'll sleep better buying at $400 instead of $430.

This is a marathon, not a sprint. Protect your capital.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-Score of 438 and Vol/OI of 73x reflect this specific trade's unusual characteristics relative to recent MU activity - it does not imply the trade will be profitable or that you should follow it. Memory stocks are cyclical with potential for 30-50% drawdowns even during supercycles. Always do your own research and consider consulting a licensed financial advisor before trading.

About Micron Technology: Micron Technology is one of the largest semiconductor companies in the world, specializing in DRAM, NAND flash, and High Bandwidth Memory (HBM) for AI, data centers, mobile, automotive, and consumer electronics, with a market cap of $461.7 billion in the Semiconductors & Related Devices industry.