🛡️ MU: Someone Just Dropped $4.7M on Deep OTM Puts - Hedging the AI Memory Supercycle?

📅 February 13, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just paid $4.7 MILLION for deep out-of-the-money puts on Micron Technology - betting on a 35% crash from current levels! With zero prior open interest, this is a brand new position opened at 09:56 AM today. Whether it's portfolio insurance from a massive long holder or a speculative bearish bet ahead of Q2 earnings on March 26, this whale is paying serious premium for downside protection on the AI memory darling.

📊 Company Overview

Micron Technology, Inc. (NASDAQ: MU) is one of the world's largest memory and storage semiconductor manufacturers, specializing in DRAM, NAND flash, and High Bandwidth Memory (HBM) products. The company sits at the heart of the AI infrastructure buildout, with its HBM chips powering NVIDIA's data center GPUs.

| Metric | Value |

|---|---|

| Industry | Semiconductors - Memory & Storage |

| Market Cap | ~$462B - $493B |

| Current Price | $400.13 |

| 52-Week Performance | +323% |

| YTD Performance | +44% |

| P/E Ratio | 39.01 |

💰 The Option Flow Breakdown

📊 What Just Happened

| Field | Value |

|---|---|

| Ticker | MU |

| Date | 2026-02-13 |

| Time | 09:56:05 |

| Option | MU20260402P260 |

| Type | PUT |

| Strike | $260 |

| Expiration | 2026-04-02 |

| Spot Price | $400.13 |

| Option Price | $5.00 |

| Size | 9,347 contracts |

| Volume | 10,000 |

| Open Interest | 0 (Brand New!) |

| Premium | $4.7M |

| Order Type | BTO (Buy to Open) |

| Direction | BUY |

| Strategy | Long Put (Deep OTM Protective Hedge) |

🤓 What This Actually Means

Translation for us regular folks: Someone with very deep pockets just paid $4.7 million for the right to sell MU shares at $260 - that's a full 35% below where the stock trades today!

Here's what makes this trade stand out:

🐋 Zero Open Interest - This is a brand new position. No one was sitting in this strike before. The buyer walked in and opened 9,347 contracts from scratch.

🛡️ Classic Hedge Profile - A strike this far OTM (35% below spot) typically signals portfolio protection rather than a directional bet. The buyer likely owns a massive long position in MU stock and wants insurance against a catastrophic drop.

📅 April Expiration - With 48 days to go, this covers Q2 FY2026 earnings on March 26, 2026, plus potential HBM4 qualification news with NVIDIA.

💸 Premium as Insurance Cost - At $5 per contract for $4.7M total, this buyer is paying about 1.25% of a theoretical $376M stock position for 48 days of crash protection.

📈 Technical Setup / Chart Check-Up

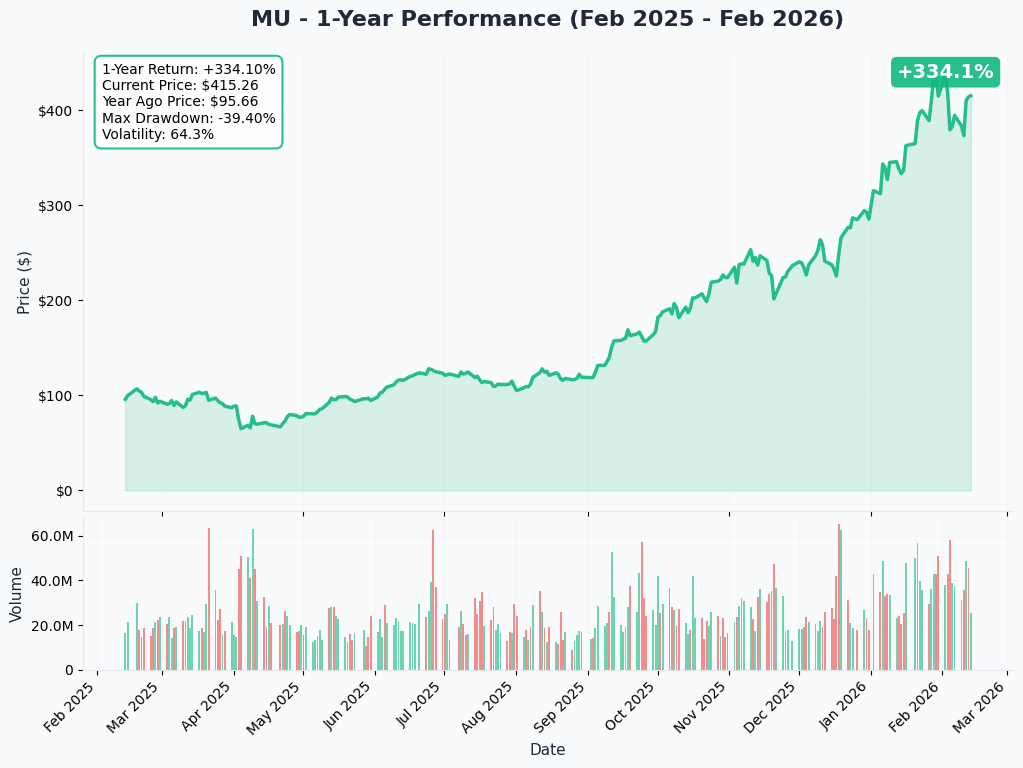

YTD Chart

MU has been on a tear in 2026, up 44% YTD and +323% over the past 52 weeks. The stock hit an all-time high of $455.50 on January 30, 2026, according to Capital.com's analysis, before pulling back to current levels around $400.

The current price of $400.13 represents:

- 📈 12% below the ATH of $455.50

- 📈 44% above year-start levels

- 📈 323% above year-ago prices

Gamma-Based Support & Resistance

Note: Gamma exposure charts are currently unavailable for this analysis.

Implied Move Analysis

Note: Implied move charts are currently unavailable for this analysis.

Key Technical Levels to Watch:

| Level | Price | Significance |

|---|---|---|

| All-Time High | $455.50 | January 30, 2026 peak |

| Current Price | $400.13 | Today's spot |

| Put Strike | $260.00 | 35% below current (hedge floor) |

🎪 Catalysts

🔜 Upcoming Catalysts

| Event | Date | Significance |

|---|---|---|

| Q2 FY2026 Earnings | March 26, 2026 | Company guided $18.7B revenue, $8.42 EPS - massive beat expected |

| HBM4 NVIDIA Qualification | Q2 2026 | Critical milestone for next-gen AI memory supply |

| NVIDIA GTC 2026 | March 2026 | Potential HBM4/AI memory updates |

✅ Recent Catalysts (Already Happened)

📊 Q1 FY2026 Earnings Blowout (December 17, 2025): According to Micron's official earnings release:

- Revenue: $13.64B (+57% YoY)

- GAAP EPS: $4.60 (+290% YoY)

- Gross Margin: 56.8% (+2,820 bps YoY)

- Operating Cash Flow: $8.4B (quarterly record)

🏭 $100B New York Fab Groundbreaking (January 2026): Per The Motley Fool's coverage, Micron broke ground on the largest semiconductor fab in U.S. history as part of a $200B domestic investment plan.

📈 HBM Sold Out Through 2026: Blocks and Files reports that Micron's entire HBM production capacity is completely sold out through calendar 2026.

💰 Analyst Upgrades: According to MarketBeat's analyst tracker:

- Morgan Stanley: Raised to $450 (February 11, 2026)

- UBS: Raised to $450

- Mizuho: Raised to $480

- Phillip Securities: Initiated at $500

- Rosenblatt: Reiterated $500

🎲 Price Targets & Probabilities

Based on the option flow activity and analyst consensus:

🐂 Bull Case: $480-$500 (20-25% upside)

Probability: 35%

If HBM4 qualification with NVIDIA succeeds and Q2 earnings meet the explosive $18.7B/$8.42 guidance, MU could retest ATH and push toward Mizuho's $480 or Phillip/Rosenblatt's $500 targets.

Triggers:

- ✅ Q2 revenue beats $18.7B guidance

- ✅ HBM4 passes NVIDIA qualification

- ✅ Memory prices continue rising (+55% DRAM QoQ per TrendForce)

⚖️ Base Case: $380-$420 (current range)

Probability: 45%

Stock consolidates around current levels as investors digest the massive 323% rally and await clarity on HBM4 competitive positioning. The $260 put buyer may be betting the stock stays elevated but wants crash protection just in case.

🐻 Bear Case: $300-$350 (15-25% downside)

Probability: 18%

If HBM4 qualification fails or Q2 guidance disappoints, the premium valuation (39x P/E) could compress rapidly. WCCFTech reports analysts believe "the HBM4 race is really between SK Hynix and Samsung" with Micron potentially losing share.

💀 Tail Risk Case: $260 or below (35%+ downside)

Probability: 2-5%

This is what the $4.7M put buyer is hedging against. A black swan scenario combining:

- ❌ HBM4 qualification failure

- ❌ China trade escalation (per Morgan Lewis analysis)

- ❌ Memory cycle peak/reversal

- ❌ Broader market correction

💡 Trading Ideas

🛡️ Conservative: "Sleep Well Insurance"

Strategy: Follow the whale - buy protective puts on existing MU long positions

| Parameter | Value |

|---|---|

| Trade | Buy MU April 2, 2026 $350 Put |

| Cost | ~$8-12 per contract |

| Protection Level | 12.5% below current |

| Max Risk | Premium paid |

Why this works: If you're long MU stock and nervous about earnings volatility, buying puts closer to the money provides meaningful protection without paying for extreme OTM strikes. Covers Q2 earnings on March 26.

⚖️ Balanced: "Earnings Strangle Play"

Strategy: Play the expected volatility around Q2 earnings without picking direction

| Parameter | Value |

|---|---|

| Trade | Buy MU March 28, 2026 $420 Call + $380 Put strangle |

| Cost | ~$15-20 per contract combined |

| Breakeven | Below $360 or above $440 |

| Target | 50%+ gain on volatility expansion |

Why this works: With Q2 guidance calling for 37% sequential revenue growth, this earnings report could move the stock significantly. A strangle profits from big moves in either direction.

🚀 Aggressive: "Catch the HBM4 Wave"

Strategy: Bet on successful NVIDIA HBM4 qualification driving new highs

| Parameter | Value |

|---|---|

| Trade | Buy MU April 17, 2026 $450 Call |

| Cost | ~$10-15 per contract |

| Target | ATH retest at $455+ |

| Potential Return | 100-200% on qualification news |

Why this works: If Micron passes HBM4 qualification in Q2 2026, the stock could surge past its January ATH. Analyst targets up to $500 provide room for significant upside.

⚠️ Risk Factors

🔴 HBM4 Execution Risk (HIGH)

According to WCCFTech's industry analysis, Micron faces "significant challenges with its HBM4 base die, including customer validation issues, pin speeds, and foundry logic precision." SK Hynix is targeting 70% HBM4 market share.

🟠 Competitive Pressure (MEDIUM-HIGH)

Astute Group reports SK Hynix holds 62% of current HBM market share. Both SK Hynix and Samsung are HBM4 production-ready while Micron is still seeking qualification.

🟠 China Trade/Policy Risk (MEDIUM-HIGH)

Per Micron's risk disclosures, China represents >10% of revenue, and the CAC ban prevents sales to Chinese critical infrastructure operators. ITIF analysis warns of further export control impacts.

🟡 Valuation Risk (MEDIUM)

At 39x P/E versus historical 10-15x averages, MU is priced for perfection. Any earnings miss could trigger significant multiple compression.

🟡 Cyclicality Risk (MEDIUM)

Memory remains inherently cyclical. Neumonda's market analysis notes new fab capacity coming online in 2027-2028 could ease supply constraints and pressure prices.

🎯 The Bottom Line

Real talk: This $4.7M put trade isn't a bet that MU is about to crash - it's classic institutional portfolio insurance. Someone sitting on a massive MU long position (likely $300M-$500M worth) is paying roughly 1% of their position value to sleep well through Q2 earnings and HBM4 qualification news.

Here's the playbook:

📈 If you're bullish: The fundamentals remain exceptional. Q2 guidance of $18.7B revenue (+37% QoQ) and HBM sold out through 2026 support the bull case. Consider selling put spreads below $350 to collect premium from the fear.

👀 If you're watching: Mark your calendar for March 26, 2026 (Q2 earnings) and watch for HBM4 qualification announcements throughout Q2. The $260 strike tells you where the whale thinks the floor might be in a worst-case scenario.

🛡️ If you own MU: This trade is a reminder that even the biggest winners need protection. Consider adding some downside hedges before earnings, especially given the 39x P/E and HBM4 competitive risks highlighted by analysts.

The bottom line: This whale isn't panicking - they're protecting. At 35% OTM, the $260 puts are extreme insurance for a low-probability, high-impact event. But with $4.7M on the line, someone with very deep pockets thinks that insurance is worth paying for.

⚠️ Disclaimer

This analysis is for informational purposes only and does not constitute investment advice. Options trading involves significant risk of loss and is not suitable for all investors. The unusual options activity described may not indicate future price direction. Past performance does not guarantee future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.

Analysis provided by Ainvest Option Flow | February 13, 2026