🚢 NCLH: Someone Just Cashed Out $1.3M in Calls After the Earnings Wreck!

📅 March 4, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed out $1.3M worth of June $21 calls on Norwegian Cruise Line (NCLH) -- right after the stock got hammered 11% on a brutal earnings guide. That's 4,386 contracts unwinding at once, with a z-score of 8.7 (meaning this kind of size happens maybe a handful of times per year). A big player is taking their chips off the table, and we need to figure out why.

🏢 Company Overview

Norwegian Cruise Line Holdings (NYSE: NCLH) is the world's third-largest publicly traded cruise company by berths (~71,000). They operate three brands -- Norwegian (mainstream), Oceania (upper premium), and Regent Seven Seas (luxury) -- across a fleet of 34 ships serving about 700 global destinations. Market cap sits at roughly $9.7B, with about 455M shares outstanding and 41,700 employees headquartered in Miami. They've got 13 more ships on order through 2036, adding ~38,400 berths.

Right now, this company is in the middle of a leadership shake-up and a self-inflicted capacity problem. Let's break down the flow.

💰 The Option Flow Breakdown

📊 What Just Happened

| Detail | Value |

|---|---|

| 🕐 Time | 10:38:54 ET |

| 📌 Ticker | NCLH |

| 📋 Strategy | Close Long Call (BTC) |

| 📞 Type | Call |

| 💵 Strike | $21 |

| 📅 Expiration | 2026-06-18 |

| 📦 Size | 4,386 contracts |

| 💰 Premium | $1.3M |

| 💲 Price Per Contract | ~$2.88 |

| 📈 Spot Price | $21.36 |

| 🔢 Volume | 4,400 |

| 📂 Open Interest | 5,400 |

| 📊 Vol/OI Ratio | 0.815 (HIGH) |

| 🔥 Z-Score | 8.7 -- EXTREMELY UNUSUAL |

🤓 What This Actually Means

Let's break this down in plain English.

This is NOT a new bet. The trader tagged this as a Buy to Close (BTC) -- meaning someone who was already holding these June $21 calls is exiting the position entirely. They're buying back the contracts to close out.

Here's why that matters:

🔑 The Vol/OI ratio of 0.815 means this single trade represented over 81% of the entire open interest in this contract. That's not someone dipping a toe -- that's someone ripping off the whole bandaid at once.

🔑 Z-score of 8.7 puts this in the "happens a few times a year" territory. In any given trading day, you almost never see a single NCLH options trade this large. For context, that's roughly 8.7 standard deviations above the average trade size -- extremely rare.

🔑 Slightly in-the-money with the stock at $21.36 and the strike at $21. This call had about $0.36 of intrinsic value and roughly $2.52 of time value remaining. The trader is salvaging what's left rather than riding it further.

The big question: Why are they leaving now?

Most likely scenario -- this position was established before the earnings disaster. Someone was long June $21 calls as a bullish bet, the stock just cratered 11%, their thesis broke, and they're cutting losses while they still have $2.88 in value (rather than watching it bleed to zero). Smart risk management, honestly.

📈 Technical Setup / Chart Check-Up

NCLH just fell off a cliff. Here's what the chart looks like:

The stock gapped down from ~$24.80 to open around $21.30 on March 3, carving out an intraday range of $20.52 to $22.10 before settling near $21.44. That's a post-earnings gap of roughly 11-14%, and the stock is now trading well below its 200-day moving average ($22.54).

Key technical levels to watch:

📉 Immediate Support: $20.50 -- the March 3 intraday low. If this breaks, there's not much stopping a slide toward $19, which is where JPMorgan's new downgraded price target sits.

📈 Overhead Resistance: $22.54 (200-DMA) -- this was support, now it's a ceiling. Reclaiming this level would be the first real bullish signal.

📊 Volume: Massive spike on the March 3 selloff, confirming conviction behind the move. This wasn't thin selling -- institutions dumped.

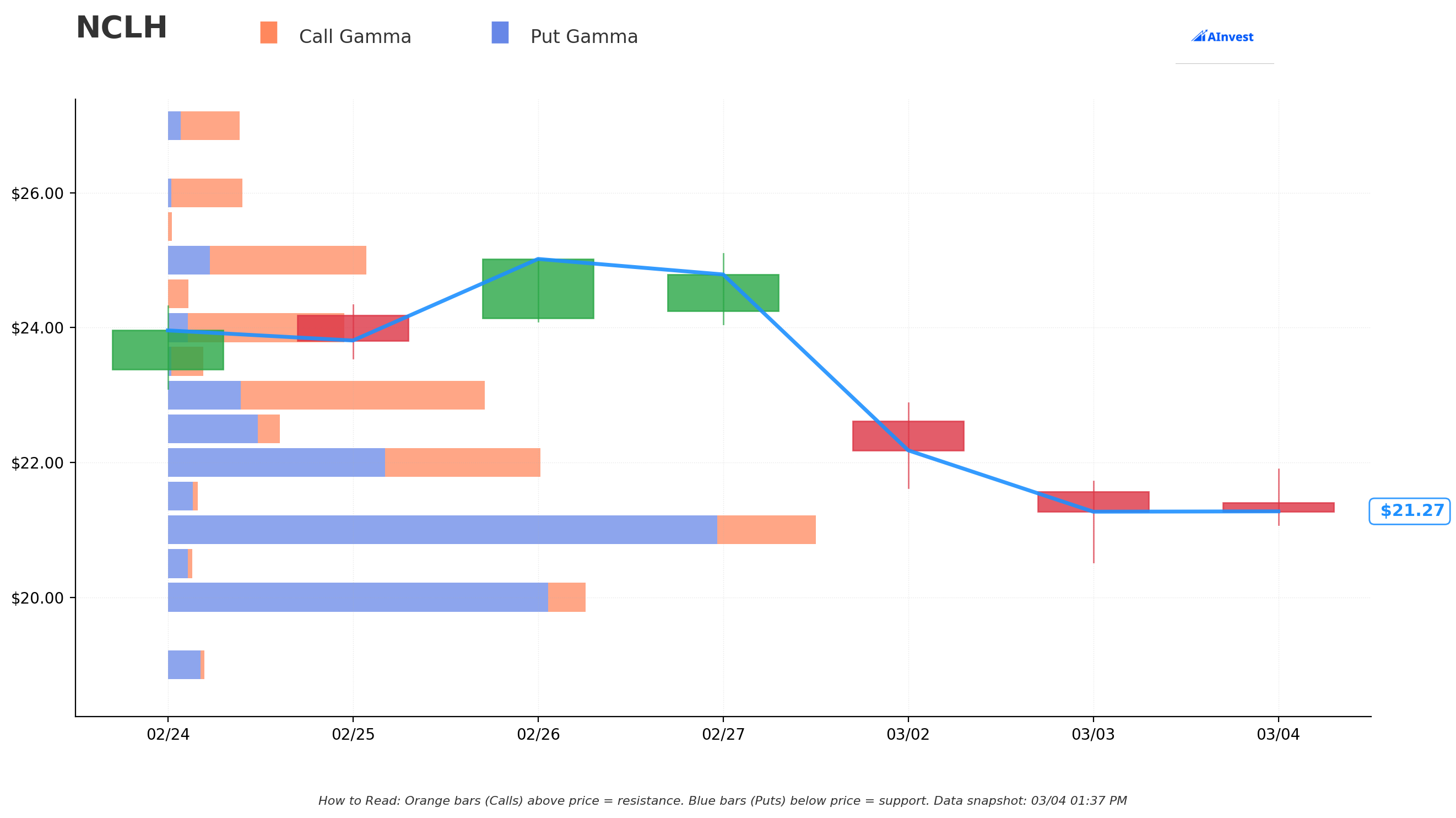

🔵🟠 Gamma-Based Support & Resistance

The gamma exposure (GEX) profile shows key strike concentrations at the following levels:

| Level | Type | Significance |

|---|---|---|

| $30 | Max Gamma Strike | Heavy call OI above -- distant resistance |

| $25 | Call Gamma | Near-term resistance zone |

| $20 | Put Gamma | Critical support floor |

| $19 | Put Gamma | Bear case magnet (aligns with JPM/Benchmark PTs) |

| $15 | Deep Put Gamma | Extreme downside level |

Translation: Options market makers have the most exposure around $20-$25, with the current price sitting right in the middle of that range. The $20 strike is your line in the sand -- if NCLH breaks below it, dealer hedging flows could accelerate the move lower.

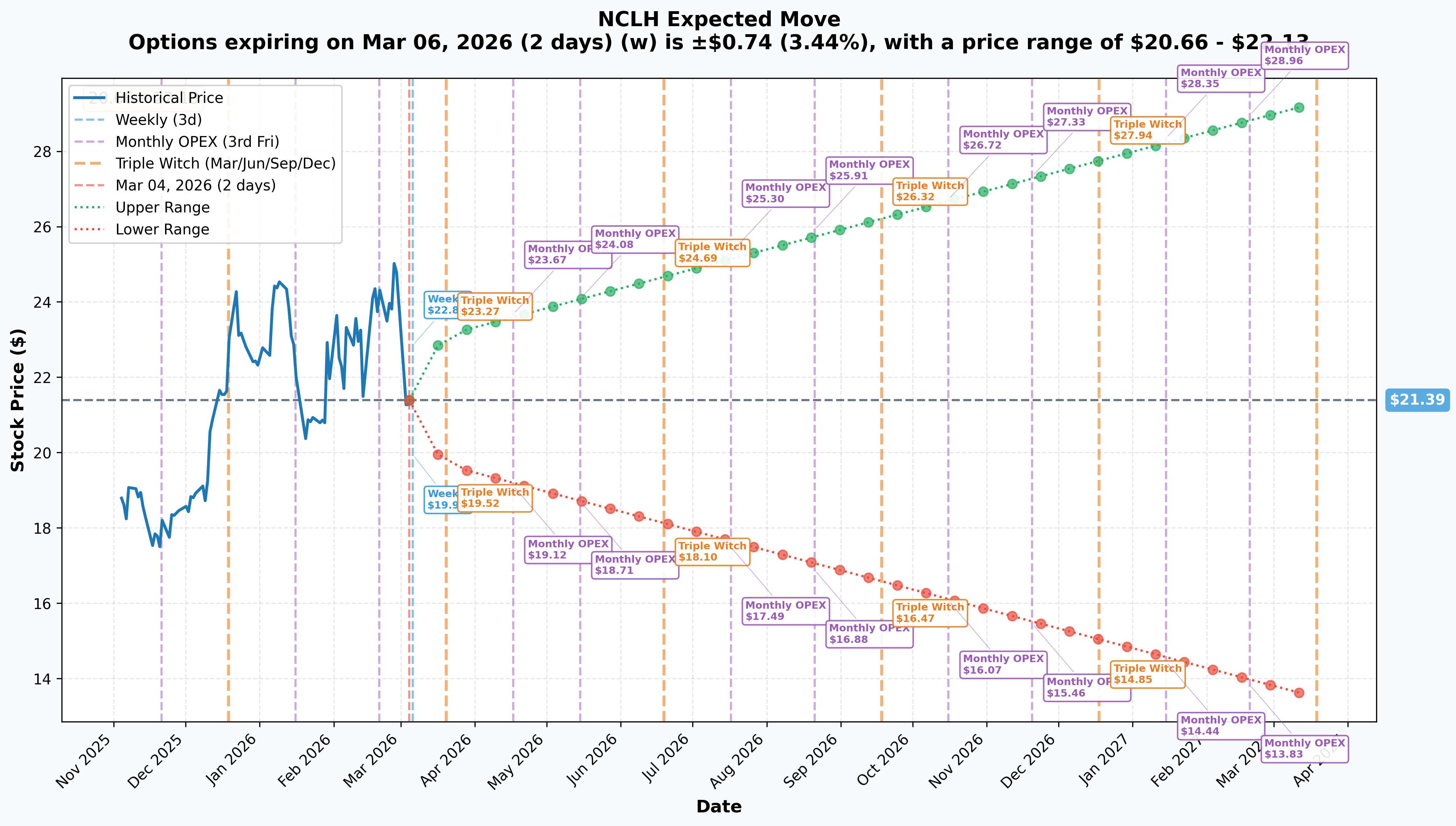

📐 Implied Move Analysis

The options market is pricing in some serious movement ahead:

| Timeframe | Implied Move | Range |

|---|---|---|

| 📅 Weekly (March 6) | +/-3.4% | $20.66 - $22.13 |

| 📅 Monthly OPEX (March 20) | +/-8.1% | $19.66 - $23.13 |

| 📅 June Triple Witch (June 19) | Wide range | $18.10 - $24.69 |

| 📅 LEAPS (March 2027) | +/-37.0% | $13.49 - $29.30 |

That 8.1% implied move into March monthly OPEX is especially interesting because it captures Carnival's (CCL) Q1 earnings on March 20 -- a huge sector read-through event. The market is bracing for continued turbulence.

🎪 Catalysts

✅ Already Happened

📉 Q4 2025 Earnings (March 2) -- Beat on EPS ($0.28 vs $0.27 consensus) but missed on revenue ($2.24B vs $2.34B). The real damage came from catastrophic Q1 2026 guidance: $0.16 EPS vs $0.40 consensus -- a jaw-dropping 60% miss. Full-year 2026 EPS guided to $2.38 vs $2.59 expected.

👔 CEO Change (February 12) -- Harry Sommer is out, John Chidsey is in. Chidsey ran Subway for 5 years and previously led Burger King. His first earnings call was brutal honesty -- calling out "self-inflicted wounds" and "siloed culture." Classic kitchen-sink quarter from a new CEO.

📉 Analyst Downgrades (March 3-4) -- A wave of price target cuts swept the Street. JPMorgan downgraded to Neutral with a $19 PT, Goldman cut to $20, Barclays to $22. Even the bulls got bruised -- Wells Fargo cut to $32, Mizuho to $28.

📅 Upcoming

| Date | Event | Why It Matters |

|---|---|---|

| March 10 | Norwegian Luna maiden voyage | New 3,550-passenger ship launches -- this is the capacity adding to Caribbean pressure |

| March 20 | CCL (Carnival) Q1 earnings | THE near-term catalyst. Strong CCL = NCLH's problems are company-specific. Weak CCL = industry-wide issue |

| March 21 | March monthly options expiration | Heavy OI unwind, potential pin risk |

| April 30 | RCL Q1 earnings | Second sector data point |

| Late May/Early June | NCLH Q1 2026 earnings | The moment of truth -- does actual Q1 match or beat the horrific $0.16 guide? |

| Summer 2026 | Great Tides Waterpark opening | Key to absorbing the 40% Caribbean capacity increase |

🎲 Price Targets & Probabilities

Based on the gamma levels, implied move ranges, and the current catalyst landscape:

🐻 Bear Case: $19.00 (-11% from here)

Probability: ~30%

This lines up with JPMorgan's $19 target and the $19 put gamma level. If CCL earnings on March 20 show broad cruise demand weakness, or if more analyst downgrades pile on, NCLH could easily slide below $20 support and gravitate toward $19. The implied move range supports $19.66 as a reasonable monthly floor.

⚖️ Base Case: $20.50 - $22.50 (chop zone)

Probability: ~45%

The stock settles into a range between the March 3 intraday low ($20.50) and the 200-DMA ($22.54). This is the "wait and see" scenario where the market digests the earnings shock, watches CCL for clues, and lets the new CEO get his feet under him. Gamma exposure keeps the stock pinned in this zone.

🚀 Bull Case: $24 - $26 (recovery trade)

Probability: ~25%

If CCL reports strong demand (isolating NCLH's problems as fixable execution issues), and the new CEO announces concrete restructuring plans, the stock could reclaim the 200-DMA and push toward the consensus analyst PT of ~$26.32. The bulls at Wells Fargo ($32), Stifel ($30), and Citi ($29) still see major upside if execution improves.

💡 Trading Ideas

🛡️ Conservative: "The Patient Collector" -- Cash-Secured Put

Sell the April 17 $19 Put for ~$0.60-$0.80 premium

✅ Why this works: You're selling insurance to scared traders at elevated IV (put IV at 58%). The $19 strike sits at JPMorgan's bear-case price target and below the implied move floor. If the stock stays above $19 by April OPEX, you keep the premium. If you get assigned, you're buying NCLH at an effective cost basis of ~$18.20-$18.40 -- well below every bull analyst target.

✅ Risk: You own the stock at $19 if it falls further. Max loss if NCLH goes to zero (unlikely for a $9.7B company).

✅ Best for: Traders who wouldn't mind owning NCLH at deep value prices and want to get paid to wait.

⚖️ Balanced: "The CCL Catalyst Play" -- March 20 Put Spread

Buy the March 20 $21 Put / Sell the March 20 $19 Put for ~$0.70-$0.90 debit

✅ Why this works: This captures the CCL earnings read-through on March 20 with defined risk. If CCL confirms industry weakness, NCLH could gap down again. Max profit of ~$1.10-$1.30 if NCLH drops to $19 or below by March 20 OPEX. Risk is limited to the debit paid.

✅ Risk: If CCL crushes it and NCLH rallies in sympathy, you lose the premium paid. The +/-8.1% implied move suggests the market expects fireworks either way.

✅ Best for: Traders who think the damage isn't done yet and want to play the next catalyst with controlled risk.

🚀 Aggressive: "The Kitchen Sink Rebound" -- June Call Spread

Buy the June 18 $22 Call / Sell the June 18 $26 Call for ~$1.20-$1.50 debit

✅ Why this works: The classic new-CEO kitchen-sink play. Chidsey deliberately sandbagged Q1 guidance to set a low bar. If actual Q1 results (due late May/early June) come in even slightly better than the horrific $0.16 guide, this stock rips. The June expiration captures Q1 earnings AND the Great Tides Waterpark opening. Max profit of $2.50-$2.80 on a $1.20-$1.50 investment -- nearly 2:1 reward-to-risk.

✅ Risk: If NCLH's problems are structural (not just kitchen-sink theatrics) and the stock stays below $22, you lose the debit. The position needs the stock to reclaim the 200-DMA.

✅ Best for: Traders who've seen the kitchen-sink playbook before and believe new CEO = low bar = future beat.

⚠️ Risk Factors

❗ Caribbean demand is a real problem, not just a headline. NCLH increased Caribbean capacity by 40% without a coordinated commercial strategy. The Great Stirrup Cay waterpark won't open until summer -- that's months of oversupply to absorb.

❗ CEO transition risk is real. John Chidsey just started. He came from Subway, not cruise lines. Organizational restructuring takes time, and there could be more bad news before things get better.

❗ Leverage is the highest among the Big 3. Net leverage at 5.3x with $14.59B total debt. While they recently refinanced ~$2B and earned an S&P upgrade, $2.7B in ship deliveries over the next two years adds to the debt pile.

❗ Macro headwinds. Tariff uncertainty, inflation pressure on consumer discretionary spending, and Alaska booking softness all weigh on the contemporary cruise segment.

❗ This flow is bearish signal, not bullish. A $1.3M call exit means a big player gave up on their bullish thesis. When institutional money leaves, retail should pay attention.

❗ Geopolitical wildcard. Strait of Hormuz tensions already drove a 6-8% fuel cost spike in early March, and bunker fuel volatility remains an unpredictable cost driver.

🎯 The Bottom Line

Real talk: A big player just bailed on their bullish NCLH bet, and honestly, you can see why. The Q1 guidance was genuinely terrible -- $0.16 EPS vs the $0.40 the Street expected. A new CEO from the fast-food world is using his first earnings call to light everything on fire. And the stock just fell through its 200-day moving average like it wasn't even there.

But here's the other side of the coin: consensus analyst PT is still ~$26 -- about 25% above where the stock sits right now. The luxury brands (Regent, Oceania) are booking at record levels. And the kitchen-sink playbook has worked before -- sandbag Q1, beat it in May, stock rebounds.

Here's your action plan:

📌 If you're bearish: Watch the $20.50 support level closely. A break below opens the door to $19. The March 20 put spread (Idea #2) gives you defined-risk exposure into the CCL earnings catalyst.

📌 If you're on the fence: Wait for CCL earnings on March 20. That's THE data point that tells you whether NCLH's problems are company-specific or industry-wide. No need to rush in.

📌 If you're bullish: The June call spread (Idea #3) is your play, but consider waiting until after CCL reports to put it on. If CCL is strong and NCLH dips on the relative comparison, that could be your entry.

🗓️ Mark your calendar: March 10 (Luna launch), March 20 (CCL earnings + March OPEX), and late May/early June (NCLH Q1 report). These are the dates that will move the stock.

The $1.3M exit we spotted today tells us one thing clearly: at least one institutional player decided the risk/reward no longer works at these levels. Whether they're right -- or whether the new CEO is playing 4D chess with that guidance -- we'll find out over the next few months.

Disclaimer: This is not financial advice. Options involve significant risk and are not suitable for all investors. You can lose your entire investment. Always do your own research and consider your risk tolerance before trading. Past unusual activity does not guarantee future price movement.