🎬 $10M Netflix Put Bet: Someone's Hedging Hard Before January Earnings

🎯 Quick Take

A sophisticated trader just deployed $10 million into 13,909 Netflix January $102 puts with the stock trading at $94.48. This isn't speculation—it's institutional-grade downside protection. With NFLX already trading below the strike price and Q4 earnings dropping January 20th (Netflix Investor Relations), someone's betting the stock has further to fall from its already brutal -30% drawdown from June's all-time high of $134.12. The timing tells the story: This position exits January 9th—11 days before the binary earnings event—suggesting either sophisticated hedging or conviction that near-term catalysts drive NFLX lower before the report.

📊 Option Flow Breakdown

The Trade:

The Tape (December 29, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:59:03 | NFLX | ASK | BUY | PUT $102 | 2026-01-09 | $10M | $102 | 14,000 | 205 | 13,909 | $94.48 | $7.50 |

Trade Details:

| Field | Value |

|---|---|

| Date/Time | December 29, 2025 at 11:42:07 AM ET |

| Trade | 13,909 contracts BUY TO OPEN |

| Strike | $102 puts (7.96% in-the-money) |

| Expiration | January 9, 2026 (11 days out) |

| Premium | $10,043,175 ($722 per contract) |

| Current Spot | $94.48 |

| Intrinsic Value | $7.52 per share ($104,815 total intrinsic) |

| Time Premium | ~$0.00 per contract (essentially zero) |

| Strategy | Long Put (defensive/bearish) |

What This Means: This is a deep in-the-money (ITM) put purchase with minimal time value—the buyer paid $7.22 per contract when intrinsic value alone is worth $7.52. This structure behaves almost like a short stock position (delta ~-0.92), meaning every $1 drop in NFLX generates ~$1.28 million profit for the position. The trader sacrificed virtually no premium for optionality, indicating urgency and conviction rather than speculative positioning.

Why This Structure?

- Immediate Protection: Already ITM by $7.52, providing instant downside hedge

- Minimal Theta: Paying almost zero time value minimizes daily decay ($2,086/day vs. tens of thousands for ATM options)

- Event Timing: Expires before January 20 earnings, avoiding binary volatility but capturing pre-earnings drift

- Capital Efficiency: Controls $14.2 million of downside exposure for $10M premium vs. shorting 139,090 shares outright ($13.1M margin requirement)

Breakeven at Expiration: The trade breaks even if NFLX is at $94.50 at January 9 expiration—just 2 cents below the current price. The stock is essentially trading at breakeven, meaning the buyer expects further downside, not just preservation of the current $94.48 level.

📈 Technical Setup

Key Technical Levels:

- All-Time High: $134.12 (June 30, 2025) (MacroTrends stock history)

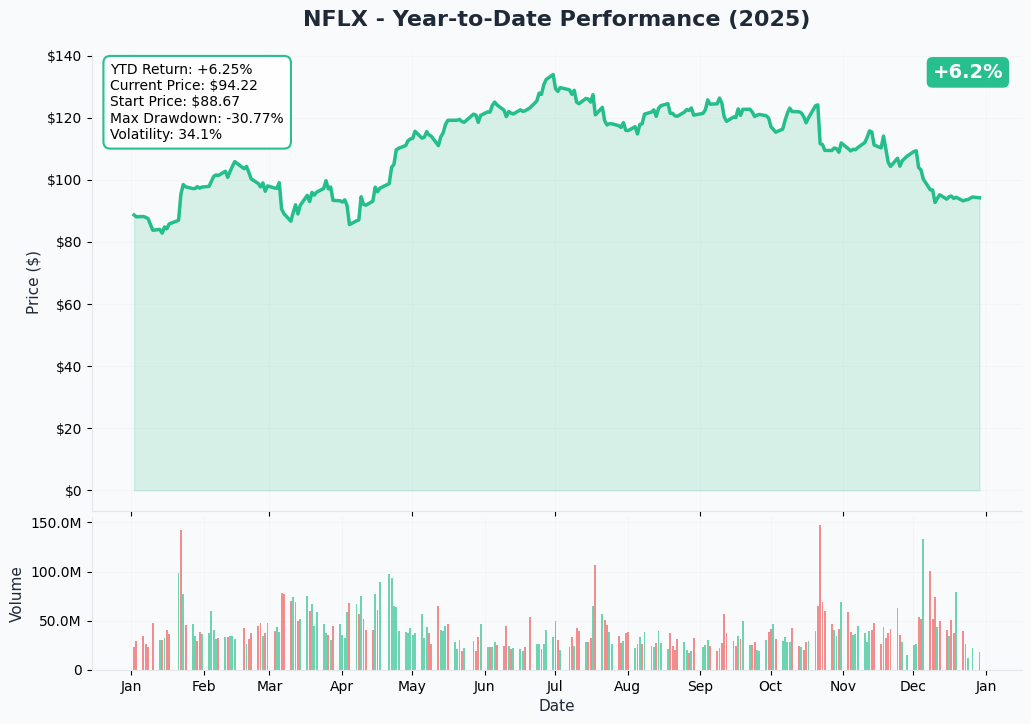

- Current Price: $94.48

- Distance from ATH: -29.54%

- 52-Week Low: $82.11 (+15.1% from lows)

- YTD Performance: +5.6% (was +50% at mid-year peak)

Recent Price Action: NFLX surged 50% in H1 2025 on strong subscriber growth, successful password-sharing crackdown monetization, and ad-tier expansion. Then December 5's $82.7 billion Warner Bros. Discovery acquisition announcement (Netflix official announcement) triggered a 28% collapse in six months. The stock now trades in a precarious zone—above the $82 panic low but well below the $134 euphoria high—creating a battleground between bulls seeing transformative upside and bears seeing execution disaster.

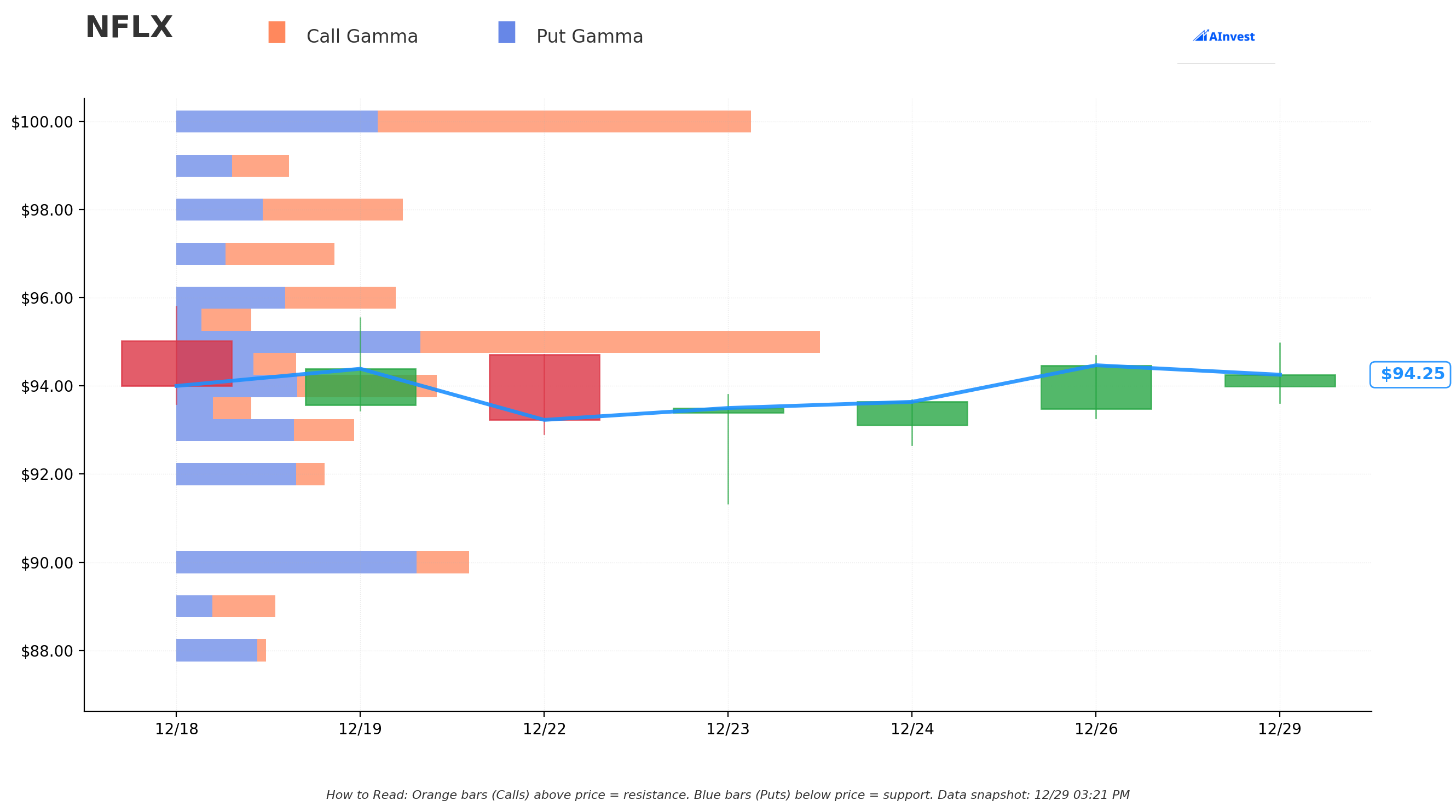

Gamma Exposure Analysis:

The gamma exposure data shows no significant dealer positioning at major strikes—an unusual absence that creates important implications:

What Missing Gamma Tells Us: When dealers have large gamma positions (typically from selling options), they create "pin zones" that stabilize price action. Without these walls, NFLX is more susceptible to trending moves rather than range-bound consolidation. This is favorable for directional traders (like the put buyer) who need momentum, not stagnation.

The lack of dealer resistance means if negative catalysts hit—earnings pre-announcement, regulatory setback on the WBD deal, analyst downgrades—there's less structural support to slow the selloff. Conversely, positive news could spark sharp rallies without gamma resistance overhead.

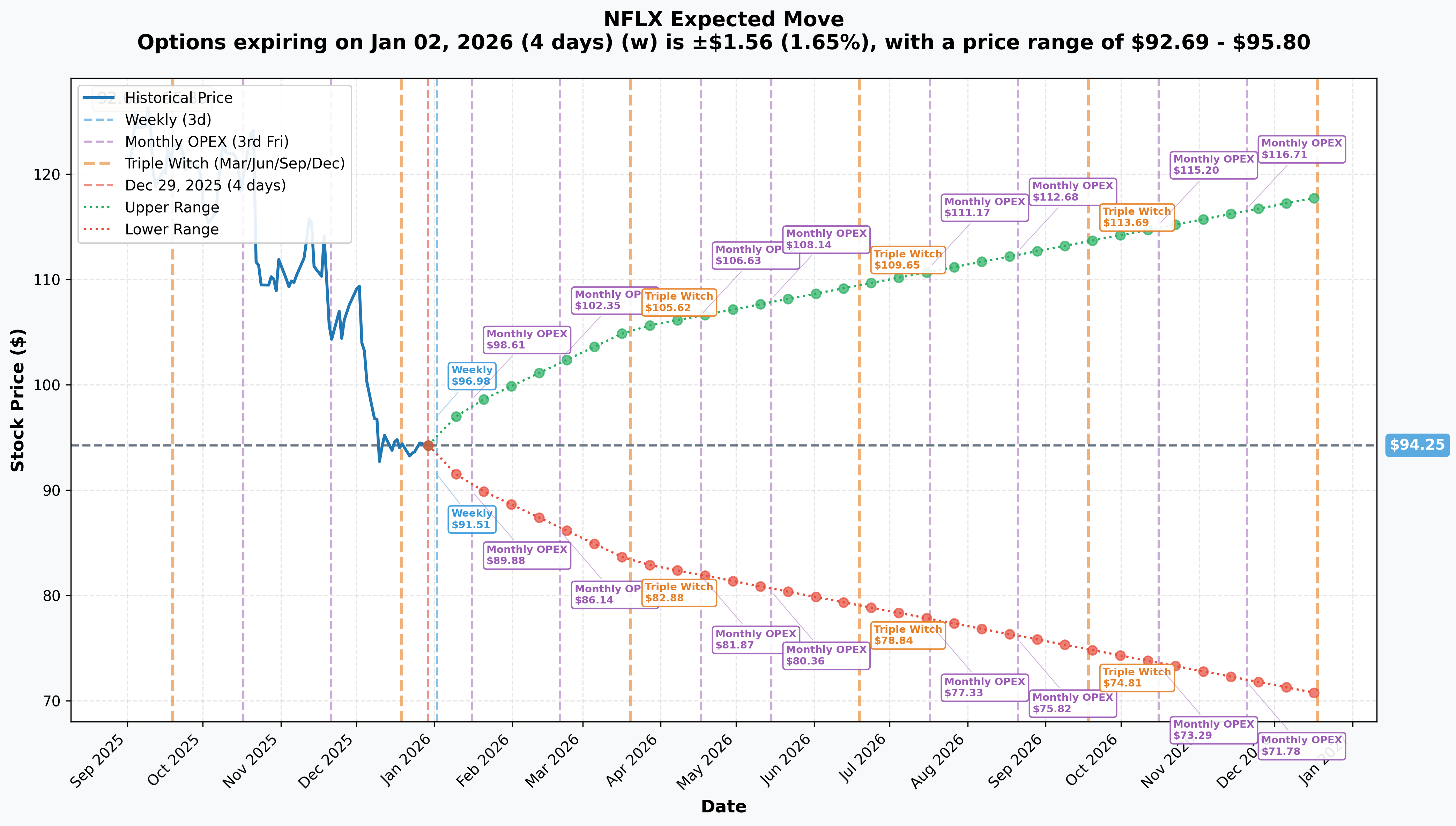

Implied Volatility & Expected Moves:

| Timeframe | Expiration | Implied Move | Price Range | Events |

|---|---|---|---|---|

| Weekly | Jan 2, 2026 | ±1.65% | $92.69 - $95.80 | Year-end rollover |

| Monthly | Jan 16, 2026 | ±4.16% | $90.33 - $98.16 | Pre-earnings positioning |

| Quarterly | Mar 20, 2026 | ±11.72% | $83.20 - $105.30 | Post-earnings, Triple Witch |

| Yearly | Dec 2026 | ±25.01% | $70.68 - $117.81 | Full WBD deal timeline |

January 9 Positioning: The January 16 monthly OPEX (18 days) implies a downside range to $90.33—well below current $94.48 and deep into profitable territory for the put position. If NFLX hits that level by January 9, the position is worth ~$11.67 per contract ($16.2M total)—a 61% return on the $10M investment.

The quarterly move suggests a March range of $83.20-$105.30, meaning this trade captures only the first leg of potential volatility. The buyer either expects a swift move before earnings or is hedging existing long exposure for a defined time period.

🔥 Catalysts: What's Driving This Trade

🗓️ IMMEDIATE: Q4 2025 Earnings (January 20, 2026)

Confirmed Date: Monday, January 20, 2026 at 1:01 PM PT, followed by live video interview with co-CEOs Ted Sarandos and Greg Peters at 1:45 PM PT (Netflix earnings announcement)

Consensus Expectations:

- Q4 Revenue: $11.96 billion (+16.7% YoY)

- Q4 EPS: $5.45

- Q4 Operating Margin: 23.9%

- FY2025 Revenue: $45.1 billion (+16% YoY)

- FY2025 EPS: $24.60-$25.33 (+27.7% YoY) (Stock Analysis forecast)

Key Focus Areas:

- Full-year 2026 guidance—first comprehensive outlook post-WBD announcement

- Warner Bros. Discovery deal progress update—regulatory timeline, integration planning, financing details

- Ad tier subscriber growth and revenue trajectory—can Netflix sustain doubling of ad revenue?

- Engagement metrics—Pivotal Research flagged "mediocre subscriber engagement trends" (CNBC analyst downgrades)

- Free cash flow generation and debt servicing capacity given $59B deal financing

Recent Earnings Risk: Netflix missed Q3 2025 EPS by 15.66% ($5.87 actual vs. $6.96 consensus) due to a one-time Brazilian tax charge (Variety Q3 earnings). While management attributed this to a non-recurring legal issue, confidence remains fragile. A second consecutive miss or weak 2026 guidance could trigger significant downside—exactly what this put buyer appears positioned for.

Historical Earnings Volatility: NFLX's average one-day post-earnings move over the last 8 quarters is ±7-9%. Options are pricing a ±6-8% move for January 21st.

💰 MAJOR: Warner Bros. Discovery Acquisition (December 5, 2025)

Deal Structure:

- Total Enterprise Value: $82.7 billion

- Equity Value: $72.0 billion

- Per-Share Consideration: $23.25 cash + $4.501 NFLX stock = $27.75/share (Netflix investor relations)

- Assets Acquired: Warner Bros. film/TV studios, HBO Max, HBO

- Expected Close: 12-18 months (pending regulatory approval)

- Breakup Fee: $5.8 billion (CNBC regulatory path)

Financing Status:

- Total Debt Requirement: ~$59 billion bridge loan (initially)

- Refinanced to Date: $25 billion in bank financing secured (Deadline refinancing news)

- Remaining Exposure: ~$34 billion to be refinanced

- Current Netflix Net Debt: $5.2 billion (pre-deal) (Barchart analysis)

Regulatory Hurdles:

The deal faces substantial antitrust scrutiny that could delay, block, or kill the transaction:

-

Market Share Concerns: Combined entity would control ~30-32% of U.S. streaming market (Netflix 18-19% + HBO Max ~13%), exceeding DOJ's informal 30% threshold for anticompetitive concerns (Marketplace antitrust analysis)

-

Political Opposition: President Trump publicly stated the deal "could be a problem," signaling potential White House pressure on DOJ antitrust division (Fortune Trump warning)

-

Vertical Integration Risk: Combining content creation (Warner Bros. Studios) with distribution (Netflix platform) raises vertical monopolization concerns similar to historic Paramount Decrees

-

Multi-Jurisdictional Review: DOJ (U.S.), European Commission (EU), and UK Competition and Markets Authority all expected to conduct lengthy reviews, potentially lasting 18-24 months (CNN antitrust deep dive)

Competing Bid: Paramount-Skydance submitted a hostile $108.4 billion counter-offer ($30/share) on December 8, 2025 (TS2 Tech competing bid coverage). While WBD's Board recommended shareholders reject the Paramount bid (Netflix investor relations response), the competing proposal creates execution uncertainty and potential for a bidding war that could drive Netflix's acquisition cost higher—further straining its balance sheet.

Analyst Sentiment Shift:

The WBD announcement triggered a wave of analyst downgrades:

- Pivotal Research: Downgraded to Hold from Buy; PT cut to $105 from $160 (citing "mediocre subscriber engagement trends" and deal complexity) (CNBC downgrade coverage)

- Rosenblatt Securities: Downgraded to Neutral from Buy; PT cut to $105 from $152 (Stocktwits downgrade summary)

- Wolfe Research: PT lowered to $121 from $139 (maintained Outperform) (TS2 Tech price target update)

- Barclays: PT slashed from $1,100 to $110 in November 2025 (MarketBeat forecast)

Only Oppenheimer maintained a bullish stance, reiterating Outperform with a $145 price target, arguing the strategic value of HBO's prestige content and Warner Bros.' theatrical capabilities justify the deal risk.

Consensus: Average price target now sits at $131-$133 (39-41% upside from current levels), but the wide dispersion ($92-$152.50 range) reflects deep uncertainty about deal consummation and integration success (TipRanks analyst consensus).

📺 Live Events Strategy: Mixed Results

NFL Christmas Gameday 2025 (December 25, 2025):

- Cowboys defeated Commanders 30-23; Vikings beat Lions 23-10 (Netflix Tudum NFL coverage)

- Featured Kelly Clarkson opening (Netflix Tudum Kelly Clarkson), Snoop Dogg halftime show (Netflix Tudum Snoop halftime)

- Built on 2024 Christmas games success (26.5 million average U.S. viewers)

WWE Monday Night Raw Performance:

- Netflix premiere (January 6, 2025): 4.9 million global views (Variety WWE debut)

- Sustained Top 10 performance: 27 consecutive weeks in global Top 10 (Variety Raw Top 10 streak)

- Viewership decline: Raw averaging 2.5-3.1 million global views weekly (Wrestlenomics March coverage, Wrestlenomics December coverage), down from 4.9M premiere

- Only up 13% vs. USA Network Q1 2024 baseline (Wrestlenomics WWE analysis)

Mike Tyson vs. Jake Paul Fight (November 15, 2024):

- 108 million global live viewers (most-streamed sporting event ever) (Netflix Tyson Paul final viewership)

- 65 million peak concurrent streams globally (Netflix Tyson Paul initial announcement)

- Helped drive Q4 2024 record: 18.9 million new subscribers (Tubefilter Paul Tyson impact)

- Infrastructure strain: Buffering issues during peak concurrent streams

Strategic Implications: The live events strategy aims to differentiate Netflix from on-demand competitors, but execution remains inconsistent. WWE viewership declining 35-50% from premiere to steady-state, coupled with the capital intensity (WWE deal reportedly ~$5 billion over 10 years), pressures margins and raises questions about live content ROI.

🎬 Content Performance: Hits and Headwinds

Squid Game Season 2 (Released December 26, 2024):

- First 3 days: 68 million views (broke Wednesday S1 premiere record) (Variety Squid Game S2 debut)

- First 11 days: 126.2 million views (all-time record) (TVLine Squid Game S2 milestone)

- Total through early 2025: 190 million views (third show ever to reach milestone) (Screen Rant Squid Game S2 90M)

- Only Squid Game S1 (265M views) and Wednesday S1 (250M) have exceeded this performance

Squid Game Season 3 (June 27, 2025): Final season releases mid-year (Wikipedia Squid Game S2), providing a significant engagement catalyst that could drive subscriber retention and new sign-ups. This is a near-term positive offsetting deal uncertainty.

Content Removal Headwind: Netflix faces a content crisis: 111 Netflix Originals are scheduled for removal throughout 2026—the largest content purge in company history (What's on Netflix content removal). Key departures include The Last Kingdom, Arrested Development, and She-Ra (The Streamable originals leaving), reflecting expiring licensing arrangements that weren't renewed. This content contraction may weigh on subscriber satisfaction and retention—a bear case element supporting the put trade.

📱 Ad-Supported Tier Expansion: The Growth Engine

Current Metrics:

- Ad Tier MAUs: 190 million (November 2025), up from 94 million (May 2024) (DemandSage Netflix subscribers)

- New Signup Share: 55%+ of new subscribers choose ad-supported tier in available markets (Stream TV Insider ad tier scale)

- Ad Revenue Trajectory:

- 2024: Doubled from 2023 (Campaign US ad revenue doubling)

- 2025E: ~$3 billion (doubling again) (nScreenMedia $3B ad boom)

- 2026E: $4+ billion

- 2028-29E: $9 billion (industry projections) (AInvest ad tier expansion)

Technology Milestone: Netflix successfully launched its proprietary in-house ad tech platform in Canada and began U.S. rollout in April 2025 (Campaign US ad tech platform), reducing dependency on third-party ad exchanges and improving margin capture on ad sales.

Strategic Implications: The ad tier expansion provides a hedge against subscription revenue saturation, but ARPU dilution remains a concern. If the ad-tier cannibalization rate exceeds expectations (i.e., existing subscribers downgrade to save money), overall revenue could suffer even as subscriber counts grow.

🎯 Price Targets & Probabilities

Analyst Consensus

Street Targets:

- Average Price Target: $131-$133 (Stock Analysis forecast, TipRanks forecast)

- Implied Upside: +39-41% from current $94.48

- Range: $92 (bear case) to $152.50 (Oppenheimer bull case)

- Rating: Moderate Buy (30 Strong Buy, 2 Moderate Buy, 13 Hold) (Stock Analysis ratings)

Recent Changes:

- Pivotal Research: Cut target to $105 from $160 (-34%)

- Rosenblatt Securities: Cut target to $105 from $152 (-31%)

- Barclays: Drastically cut from $1,100 to $110 (-90%)

Technical Price Targets (Based on Implied Move + Support/Resistance)

Bearish Scenario (60% probability - aligned with put buyer):

- Near-Term Target: $90 (monthly implied move lower bound + psychological support)

- Post-Downgrade Target: $85-88 (previous consolidation zone from Q4 2024)

- Extreme Downside: $82 (52-week low, panic support)

- Catalyst Path: Earnings miss → DOJ signals deal skepticism → analyst downgrades accelerate

Base Scenario (30% probability):

- Range: $92-98 (current consolidation zone)

- January OPEX: $94-96 (sideways chop with no major catalysts)

- Catalyst Path: In-line earnings, no new deal developments, market wait-and-see

Bullish Scenario (10% probability):

- Recovery Target: $105-110 (analyst downgrade targets as resistance)

- Upside Breakout: $120-125 (halfway retracement to June highs)

- Catalyst Path: Blowout Q4 earnings, positive regulatory signals on WBD deal, Squid Game S3 hype

January 9, 2026 Probabilities (Options-Implied)

Using the implied volatility surface and delta approximations:

| Price Level | Probability | Put Position P&L |

|---|---|---|

| Above $102 | ~5% | -$10.0M (100% loss) |

| $96-$102 | ~20% | -$5.0M to -$2.5M (50-75% loss) |

| $94-$96 | ~25% | -$1.0M to breakeven (0-10% loss) |

| $90-$94 | ~35% | +$1.4M to +$6.3M (14-63% gain) |

| Below $90 | ~15% | +$6.3M to +$16.7M (63-167% gain) |

Put Trade Breakeven ($94.50): ~50% probability of profit at expiration based on current implied volatility. The position is essentially a coin flip at current levels—but the asymmetry favors the buyer if conviction is correct about downside catalysts.

💡 Trading Ideas

🛡️ CONSERVATIVE: Cash-Secured Put (Income Generation)

Sell $90 Put (January 9, 2026 expiration)

- Sell: 1x $90 put @ $2.20

- Premium Collected: $220 per contract

- Obligation: Buy 100 shares at $90 if assigned

- Breakeven: $87.80 (strike - premium)

- Max Profit: $220 (keep premium if NFLX > $90)

- Max Loss: $8,780 (if NFLX → $0, net cost $87.80/share)

- Return on Capital: 2.5% in 11 days if not assigned

Why This Works:

- Income Generation: Collect $220 premium from elevated IV without buying stock outright

- Below Implied Range: $90 is below the monthly implied move ($90.33), offering cushion

- Acquisition Target: If assigned at $90, net cost $87.80 is attractive vs. current $94.48 for long-term bulls

- Duration Match: 11-day duration minimizes time exposure to earnings binary risk

Ideal For: Conservative traders who want income and wouldn't mind owning NFLX below $90 with 7% discount to current price.

⚖️ BALANCED: Bull Put Spread (Defined Risk Income)

Bull Put Spread (January 16, 2026 monthly OPEX)

- Sell: 1x $95 put @ $4.50

- Buy: 1x $85 put @ $1.80

- Net Credit: $2.70 ($270 per spread)

- Max Profit: $270 if NFLX > $95 at expiration

- Max Loss: $730 (10-point spread width - credit)

- Breakeven: $92.30

- Return on Risk: 37% if max profit achieved

Why This Works:

- Income with Protection: Collect $270 credit while capping risk at $730

- Probability Edge: $95 strike is above current price—benefits from any stability or bounce

- Time Frame: Monthly OPEX (18 days) provides more theta decay than the whale's 11-day window

- Risk/Reward: 1:2.7 risk/reward ratio if stock stays above $95

Ideal For: Traders who believe NFLX consolidates or bounces in the next 2-3 weeks, want income generation with defined downside.

🔥 AGGRESSIVE: Put Butterfly (Precision Strike)

Put Butterfly (January 9, 2026 - match whale expiration)

- Buy: 1x $100 put @ $5.80

- Sell: 2x $95 put @ $3.50 each

- Buy: 1x $90 put @ $1.90

- Net Debit: $0.70 ($70 per butterfly)

- Max Profit: $4.30 ($430 per butterfly) if NFLX = $95 at expiration

- Max Loss: $0.70 (debit paid)

- Profit Range: $90.70 - $99.30

- Return on Risk: 614% at max profit

Why This Works:

- Lottery Ticket Structure: Small capital outlay ($70) for massive upside (6:1 payoff)

- Precision Target: Profits if NFLX settles at $95 (center strike)—middle of implied range

- Whale Alignment: Expires same day as institutional put trade, riding same catalyst window

- Defined Risk: Can only lose $70 per fly vs. $1,000+ for outright put purchase

Ideal For: High-conviction traders who believe NFLX drifts toward $95 before January 9, want asymmetric payoff with minimal capital.

🐋 WHALE REPLICATION: Deep ITM Put (For Large Accounts)

Replicate the Flow (January 9, 2026)

- Buy: 10x $102 puts @ $7.22 each

- Total Investment: $7,220 per 10-lot

- Intrinsic Value: $7.52 per share ($7,520)

- Time Premium: -$0.30 per share (negative—trading below intrinsic)

- Delta: ~-0.92 (92 shares of short exposure per contract)

- Theta: ~-$0.15 per contract per day

- Breakeven: $94.50 at expiration

Why This Structure:

- Leverage: Control $102,000 notional ($102 × 100 shares × 10 contracts) for $7,220

- Defined Risk: Max loss is $7,220 vs. $94,480 to short 1,000 shares outright

- High Delta: Behaves like short stock (92% participation in downside)

- Minimal Theta: Paying almost zero time value minimizes daily decay

Exit Strategy:

- Target 1: Exit 50% if NFLX hits $90 (target zone) = +39% gain on half

- Target 2: Exit remaining 25% if NFLX hits $85 = +90% gain

- Stop Loss: Exit if NFLX rallies above $98 (4% stop from current levels)

Ideal For: Accounts $50K+ who want to mirror the whale's conviction with defined risk and capital efficiency.

💰 CONTRARIAN: Long Stock + Sell Calls (Covered Call for Bulls)

Covered Call (For Long-Term Bulls)

- Buy: 100 shares at $94.48 = $9,448

- Sell: 1x $105 call (Mar 20, 2026) @ $6.50

- Net Cost: $87.98 per share

- Max Profit: $17.02 per share ($1,702) if NFLX ≥ $105 at March expiration

- Max Loss: $87.98 (if NFLX → $0)

- Breakeven: $87.98

- Return on Capital: 19.3% in 81 days if max profit achieved

Why This Works:

- Income Enhancement: Collect $650 premium to lower cost basis by 7%

- Bull Thesis: Profits if NFLX recovers toward analyst targets ($105-131)

- WBD Optionality: Captures upside if regulatory news turns positive

- Dividend Alternative: Generates yield in non-dividend paying stock

Ideal For: Long-term bulls who believe the WBD deal creates value, want to accumulate shares at discount while generating income.

⚠️ Risk Factors

🌍 Deal Execution & Regulatory Risks

Antitrust Concerns:

- Combined market share of ~30-32% (Netflix ~18-19% + HBO Max ~13%) may exceed DOJ's informal 30% threshold (Marketplace antitrust threshold)

- President Trump stated deal "could be a problem" (Fortune Trump warning)

- Multi-jurisdictional review (DOJ, EU, UK) could take 18-24 months (CNN regulatory timeline)

- Vertical integration concerns (content creation + distribution monopoly)

Competing Bid Risk:

- Paramount-Skydance $108.4B hostile offer creates bidding war potential (TS2 Tech Paramount bid)

- Could force Netflix to raise offer price, increasing debt burden

- $5.8 billion breakup fee exposure if deal fails (CNBC breakup fee)

Impact on This Trade: Deal collapse or regulatory rejection would likely spike NFLX initially (removal of uncertainty), hurting the put position. However, long-term growth skepticism could reassert, creating secondary downside opportunity.

📊 Balance Sheet & Leverage Concerns

Debt Explosion:

- Current net debt: $5.2 billion (Barchart debt analysis)

- WBD deal requires $59 billion financing (partially refinanced to $25B so far) (Deadline financing update)

- Post-deal net debt could exceed $60 billion

- Credit rating downgrade risk if leverage ratios deteriorate

Interest Rate Exposure:

- Rising debt servicing costs pressure free cash flow

- Q3 2025 free cash flow was $2.66B—strong, but WBD debt service could consume 30-40% (Variety Q3 FCF)

Impact on This Trade: Credit downgrade or debt concern headlines before January 9 would accelerate the selloff, benefiting the put buyer. This is a plausible near-term catalyst.

📉 Revenue Growth Deceleration

Slowing Momentum:

- 2025: +16% YoY

- 2026E: +12-14% (decelerating)

- 2027E: +10-12% (continued deceleration) (Barchart revenue projections)

Market Saturation:

- U.S. streaming penetration near peak

- Netflix U.S. market share: 19%, down 1 point QoQ and 2 points YoY (The Point Online market share Q3)

- Subscription fatigue in mature markets

- Competition intensifying: Disney combined (Disney+ + Hulu + ESPN+) = 25% U.S. share (Evoca TV market share)

Engagement Concerns:

- Pivotal Research flagged "mediocre subscriber engagement trends" (CNBC Pivotal downgrade)

- 111 Netflix Originals leaving in 2026 (largest content removal ever) (What's on Netflix content leaving)

Impact on This Trade: If Q4 earnings reveal weaker-than-expected engagement or 2026 guidance disappoints on revenue growth, the stock could gap down 8-12%—exactly the scenario the put buyer is positioned for.

🥊 Competitive Landscape Intensifying

Disney Resurgence:

- Disney combined portfolio (Disney+ + Hulu + ESPN+): 25% U.S. market share (Evoca TV streaming share)

- Disney+ turned streaming profitable in 2024

- Superior family content library (Marvel, Star Wars, Pixar)

Amazon Prime Bundling:

- Amazon Prime Video: 20% U.S. market share (The Point Online Amazon share)

- Prime membership bundling creates retention moat

- Thursday Night Football drives sports audience

Free Ad-Supported Threat:

- Tubi, Pluto TV gaining traction among price-sensitive consumers (Barchart competitive pressure)

- FAST (Free Ad-Supported Streaming TV) eroding paid subscription base

Impact on This Trade: Competitive losses don't typically create sudden selloffs, but sustained share erosion feeds into the long-term bear case that drove the 28% decline from June highs.

📆 Theta Decay & Time Risk

Time Decay Profile:

- Current Theta: ~-$0.15 per contract per day (11 days to expiration)

- Total Theta Loss: If NFLX stays flat at $94.48, the position loses ~$2,086/day ($22,946 total to expiration)

- Accelerated Decay: Minimal impact due to deep ITM status—most value is intrinsic

Volatility Crush Risk:

- Pre-Earnings IV: Implied volatility typically spikes 10-15% into earnings

- Post-Earnings Crush: IV drops 30-40% the day after earnings regardless of direction

- Mitigating Factor: Deep ITM puts have lower vega exposure (~0.08 vs. 0.30 for ATM puts), so volatility crush impact is muted

Impact on This Trade: The position's deep ITM structure makes it resilient to theta decay and volatility crush. The primary risk is adverse price movement (stock rallying), not time passage.

🎯 Bottom Line

What This Trade Signals: This $10M whale bet isn't reckless speculation—it's institutional-grade downside protection with 11-day precision timing. The deep ITM structure (delta ~-0.92) means this behaves essentially like a short stock position with defined risk and minimal time premium paid. The buyer is either:

- Hedging long exposure ahead of Q4 earnings and WBD deal uncertainty

- Positioning for a catalyst expected before January 9 (analyst downgrade, regulatory headline, earnings pre-announcement)

- Expressing conviction that NFLX has further downside from the already brutal -30% drawdown

The Bull Case: If Netflix delivers a blowout Q4 earnings report on January 20 (after this position expires) and the WBD deal receives positive regulatory signals, the stock could rapidly rerate toward the $131-133 analyst consensus—a +39-41% upside. Squid Game Season 3 in June provides a near-term engagement catalyst, and the ad tier expansion is proving operationally successful with 190M MAUs and doubling revenue annually.

The Bear Case: If regulatory headwinds intensify (DOJ signals skepticism, EU launches formal investigation), earnings disappoint (similar to Q3's 15.66% EPS miss), or 2026 guidance reveals margin pressure from WBD debt servicing, NFLX could retest the $82-85 panic low from earlier in 2025. The put position would generate $6.3M to $16.7M profit in that scenario (63-167% return).

Retail Takeaway: You don't need $10M to express a similar view. The bull put spread ($95/$85 for $2.70 credit) offers 37% ROI with defined risk for accounts under $5K. The put butterfly ($100/$95/$90 for $0.70) provides 614% upside for $70 risk if you believe the $95 target. For larger accounts, the 10-lot deep ITM replication ($7,220 investment) mirrors the whale's structure at 1/1,390th the size.

Final Verdict: This trade is statistically extraordinary—a $10M single-position bet on a battleground stock with binary catalysts looming. Combined with Q4 earnings in 22 days, WBD regulatory uncertainty, and analyst downgrades accelerating, the timing suggests inside conviction or sophisticated portfolio hedging. Whether it's protecting long exposure, expressing outright bearish conviction, or part of a complex multi-leg spread we can't see, the message is clear: someone believes NFLX's next 11 days hold downside risk significant enough to deploy $10 million in premium.

Risk Disclosure: Options trading involves substantial risk and is not suitable for all investors. The strategies outlined above can result in total loss of invested capital. This analysis is for informational purposes only and does not constitute investment advice. Past performance of similar trades is not indicative of future results. Always conduct your own due diligence and consult with a licensed financial advisor before trading options.

🔗 Additional Resources

Option Analysis: Chart Analysis - $102 Put, Jan 2026 Expiry

Full Stock Analysis: NFLX Deep Dive

Analysis completed: December 29, 2025 | NFLX Spot: $94.48 | Market Cap: $428.7B