🐋 NFLX $102M Complex Multi-Leg Bet - The Largest Single-Day Options Trade We've Ever Seen!

📅 February 25, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed $102 MILLION NET across a massive complex multi-leg options position in Netflix (NFLX) - buying 60,000 $90 calls, 184,000 $100 calls, and 121,000 $120 calls while selling 60,000 $110 calls, all expiring September 18, 2026. This is the largest single-day options trade we have tracked - a staggering institutional conviction bet that Netflix rallies 9-45% over the next 7 months. With 10.71x Vol/OI on the lead leg, this is brand new capital flooding in, not a hedge or a roll.

📊 Company Overview

Netflix Inc (NFLX) is the world's dominant streaming entertainment platform:

- 📺 What they do: Subscription-based streaming service delivering TV series, films, documentaries, games, and live events (WWE Raw, NFL Christmas Day) to 325M+ paid subscribers in 190+ countries

- 💰 Market Cap: $329.5B

- 🏢 Sector: Services - Computer Programming, Data Processing

- 📈 Exchange: NASDAQ

- 📊 Current Price: ~$82.80 (post 10-for-1 stock split completed November 17, 2025)

- 🎬 Key Story: Pursuing an $82.7B acquisition of Warner Bros. Discovery (HBO, DC, Warner Bros. studio), facing a competing $31/share bid from Paramount Skydance, with WBD shareholder vote on March 20

Important context on the stock price: Netflix completed a 10-for-1 stock split on November 17, 2025. The ~$82 price you see today is equivalent to ~$820 pre-split. All strike prices in this trade are post-split adjusted. If you're looking at this thinking "Wait, Netflix at $82?" - that's why. Pre-split, this $102M trade would have been on $900, $1,000, $1,100, and $1,200 strikes.

💰 The Option Flow Breakdown

📊 The Tape

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Strategy |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:54:54 | NFLX | MID | BUY | CALL $90 | 2026-09-18 | $45M | $90 | 60,000 | 5,601 | 60,000 | $82.80 | COMPLEX MULTI-LEG (BTO) |

| 10:54:54 | NFLX | MID | BUY | CALL $100 | 2026-09-18 | $27M | $100 | 122,000 | - | 122,000 | $82.80 | COMPLEX MULTI-LEG (BTO) |

| 10:54:54 | NFLX | MID | BUY | CALL $100 | 2026-09-18 | $27M | $100 | 62,000 | - | 62,000 | $82.80 | COMPLEX MULTI-LEG (BTO) |

| 10:54:54 | NFLX | MID | BUY | CALL $120 | 2026-09-18 | $19M | $120 | 121,000 | - | 121,000 | $82.80 | COMPLEX MULTI-LEG (BTO) |

| 10:54:54 | NFLX | MID | SELL | CALL $110 | 2026-09-18 | $16M | $110 | 60,000 | - | 60,000 | $82.80 | COMPLEX MULTI-LEG (STO) |

Net Premium: $45M + $27M + $27M + $19M - $16M = $102M NET DEBIT 💸

🤓 What This Actually Means

Let me break this down in plain English - because this trade is an absolute monster.

Five legs, one timestamp, one institution, one thesis: Netflix is going higher. WAY higher.

- 💸 $102 million net premium deployed: $45M + $27M + $27M + $19M in calls purchased, minus $16M from the short $110 calls = $102M net bullish bet. To put that in perspective, that's more capital than most hedge funds manage in their ENTIRE portfolio.

- 📈 10.71x Vol/OI on the $90 call leg - volume is nearly ELEVEN TIMES the existing open interest of 5,601. This is overwhelmingly a Buy-to-Open (brand new position, not closing or rolling)

- 🤝 MID fill on all five legs - every single leg executed at the midpoint of the bid-ask spread, a hallmark of institutional block negotiation. This is not a retail trader. This is a prime brokerage client with direct market access and billions under management.

- ⏰ 7 months to expiration (September 18, 2026) - this expiration was chosen deliberately to capture the WBD shareholder vote (March 20), Q1 earnings (April 21), Q2 earnings (July/August), price increases, and ad revenue trajectory updates

- 🎯 All five legs hit at the exact same second (10:54:54) - confirming this is a coordinated complex order executed as a single package, not separate trades

What's the actual strategy here?

This complex multi-leg position breaks down into two components:

Component 1: Bull Call Spread ($90/$110) - 60,000 contracts

- 📊 Buy 60,000 $90 calls ($45M) / Sell 60,000 $110 calls ($16M)

- 💰 Net cost: $29M for a $20-wide spread

- 🎯 Max profit: ($110 - $90) x 60,000 x 100 - $29M = $91M (if NFLX above $110 at expiration)

- 📈 Breakeven: ~$94.83 (only needs a +14.5% rally from $82.80)

- 🛡️ This is the "high-probability" component - defined risk, defined reward, clear structure

Component 2: Outright Long Calls - 305,000 contracts

- 📊 184,000 $100 calls ($54M total across two fills) + 121,000 $120 calls ($19M)

- 💰 Total cost: $73M in pure directional upside bets

- 🎯 The $100 calls need NFLX above ~$102.93 to breakeven; the $120 calls need NFLX above ~$121.57

- 🚀 If NFLX hits $130 (near the split-adjusted ATH of $133.91), the $100 calls alone would be worth roughly $552M

Why this structure? The bull call spread provides a high-probability base return ($91M max profit on $29M risk - a 3.1:1 payout). The outright $100 and $120 calls add massive convexity - if Netflix rips past $110, the upside is essentially uncapped on those 305,000 contracts. This is someone who EXPECTS a move to $100-$110 (the spread) but is positioning for an explosion to $120-$130+ (the outright calls).

One more thing to wrap your head around: The September 18 expiration captures the WBD shareholder vote on March 20 as the FIRST major catalyst, not the last. If the deal collapses or Paramount wins the bid, Netflix could rally hard on buyback resumption and balance sheet relief - and this trader still has 6 more months of runway to let the rest of the bull thesis play out.

📈 Technical Setup / Chart Check-Up

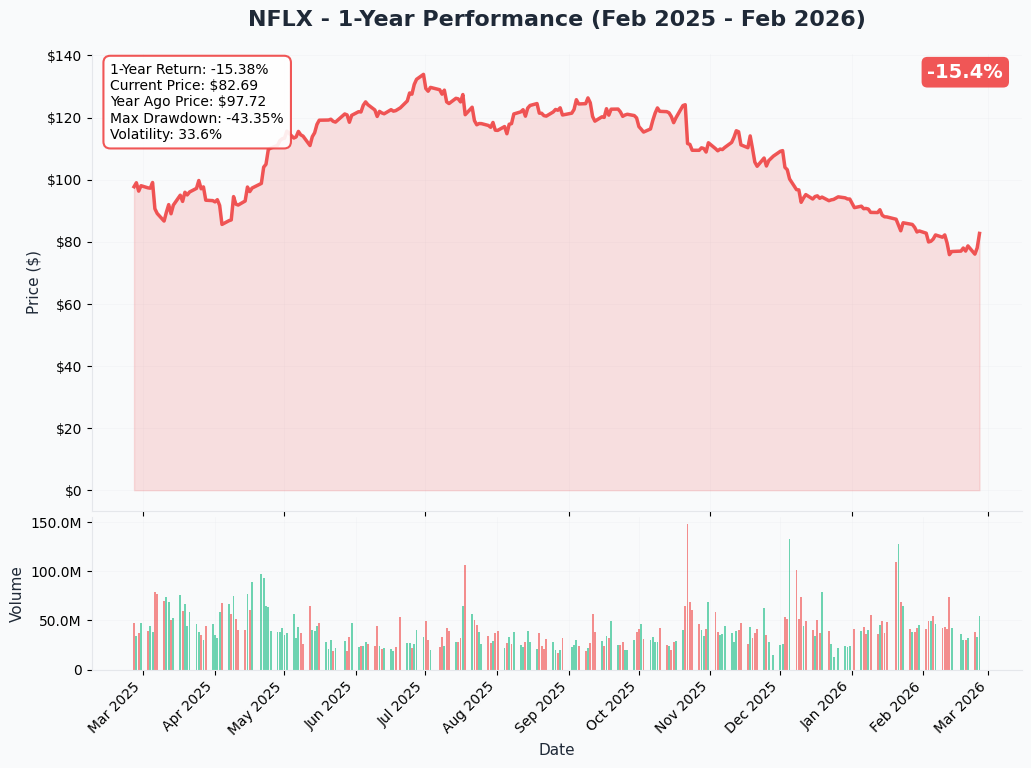

YTD Performance

NFLX is down ~38% from its split-adjusted all-time high of $133.91 in June 2025, and the chart tells a story of deal-related uncertainty crushing an otherwise excellent business:

- 📉 Down ~38% from ATH: The stock peaked at $133.91 in late June 2025 and has been under persistent pressure since the WBD acquisition announcement in December 2025

- 📉 Down ~14% YTD 2026: Started January 2026 around ~$90, now at ~$82.80 as the WBD deal uncertainty weighs on sentiment

- 📉 Down ~30% since late November 2025: The sharpest selloff coincided with the WBD deal announcement and the shift to all-cash structure

- 💸 Three factors driving the selloff: (1) $82.7B WBD acquisition balance sheet risk, (2) 2026 growth deceleration to 12-14% vs. 16% in 2025, (3) buyback pause to fund the all-cash deal

- 📊 Valuation compression: Forward P/E at ~25.4x versus the 3-year average of ~42.5x - near historical lows

- 🎯 Analyst consensus target: $116-$119 implying 50-57% upside from current levels

Key takeaway: Netflix's business is firing on all cylinders ($45.2B revenue, 325M subscribers, 29.5% margins, $9.5B FCF) but the stock is being hammered by deal uncertainty. If the WBD deal falls apart or resolves favorably, there's a LOT of room for a snapback rally. This $102M options trade is betting on exactly that rerating.

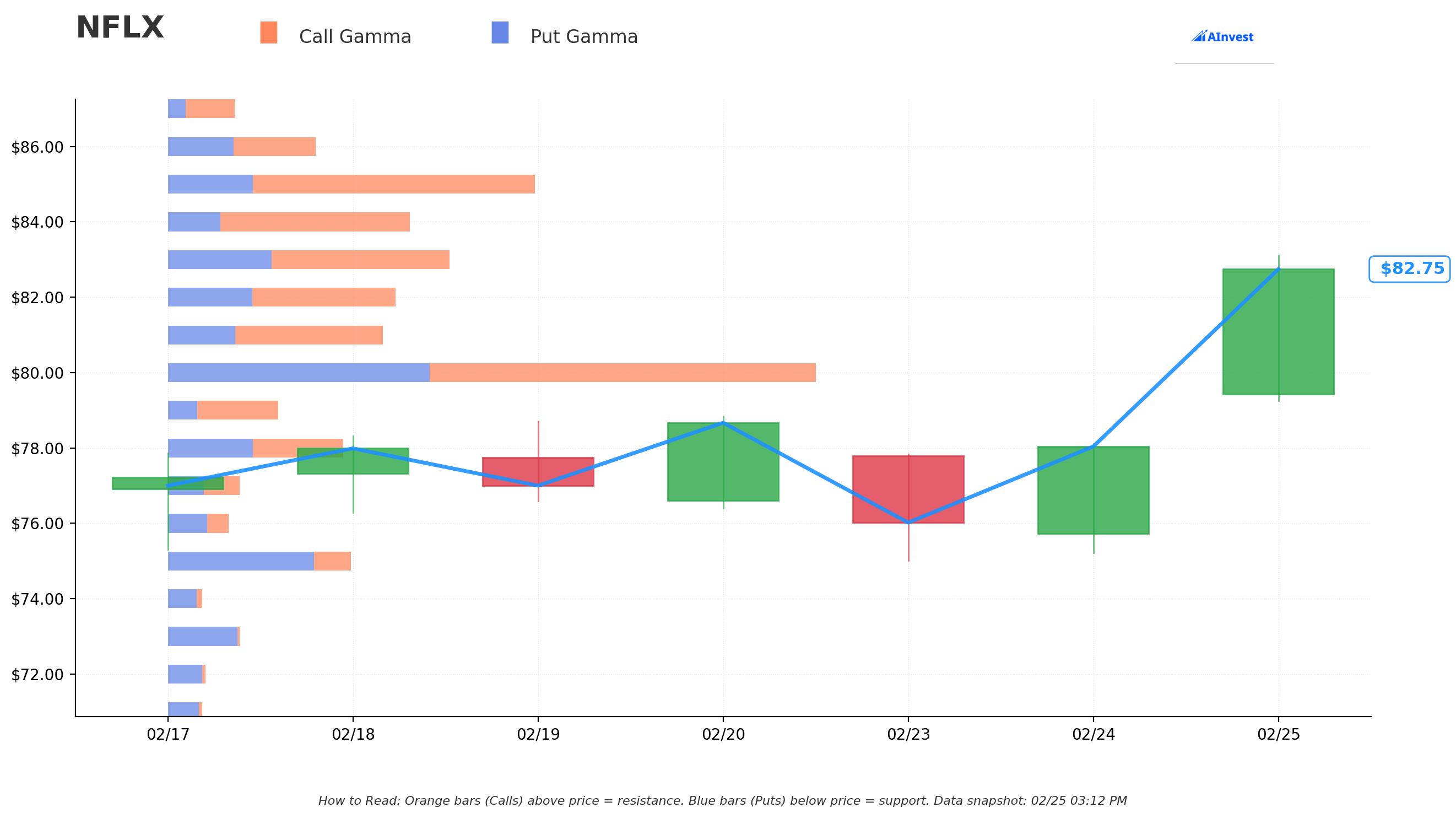

Gamma-Based Support & Resistance Analysis

Current Price: $82.62

The gamma exposure map reveals where options market maker positions create natural price floors and ceilings:

🔵 Support Levels (Put Gamma Below Price):

- $82 - Immediate support with 29.5B total gamma exposure (less than 1% below current price - tight floor!)

- $81 - Secondary support at 28.1B gamma (2.0% below)

- $80 - MASSIVE structural support with 84.0B total gamma (3.2% below - THE LINE IN THE SAND and the strongest gamma level on the entire board!)

- $78 - Extended support at 23.2B gamma (5.6% below)

- $75 - Deep floor at 24.0B gamma (9.2% below - put-dominated, net GEX turns negative here)

🟠 Resistance Levels (Call Gamma Above Price):

- $83 - First resistance at 36.2B gamma (just 0.5% overhead - easily reachable)

- $84 - Secondary resistance at 31.0B gamma (1.7% above)

- $85 - Strong resistance at 47.0B gamma (2.9% above - key near-term hurdle)

- $86 - Moderate resistance at 19.0B gamma (4.1% above)

- $90 - Extended resistance at 46.1B gamma (8.9% above - THIS IS THE FIRST LONG CALL STRIKE!)

What this means for traders: NFLX is sitting right on top of a $82 support floor with first resistance at $83 - a very tight range. The $80 level at 84.0B total gamma is the strongest level on the entire board and acts as a massive structural floor. A break above $85 (47.0B gamma) opens the path to $90, which is both a major gamma resistance AND the $90 strike on the lead call leg of this trade. The $100, $110, and $120 strikes sit well above all current gamma resistance, confirming this is a medium-term conviction play - not a near-term scalp.

Net GEX Bias: Bullish (413B total call gamma vs 259B total put gamma) - dealer positioning leans decisively bullish. Call gamma dominance means market makers are short calls and will need to buy stock as NFLX rises, creating a positive feedback loop that could accelerate any rally.

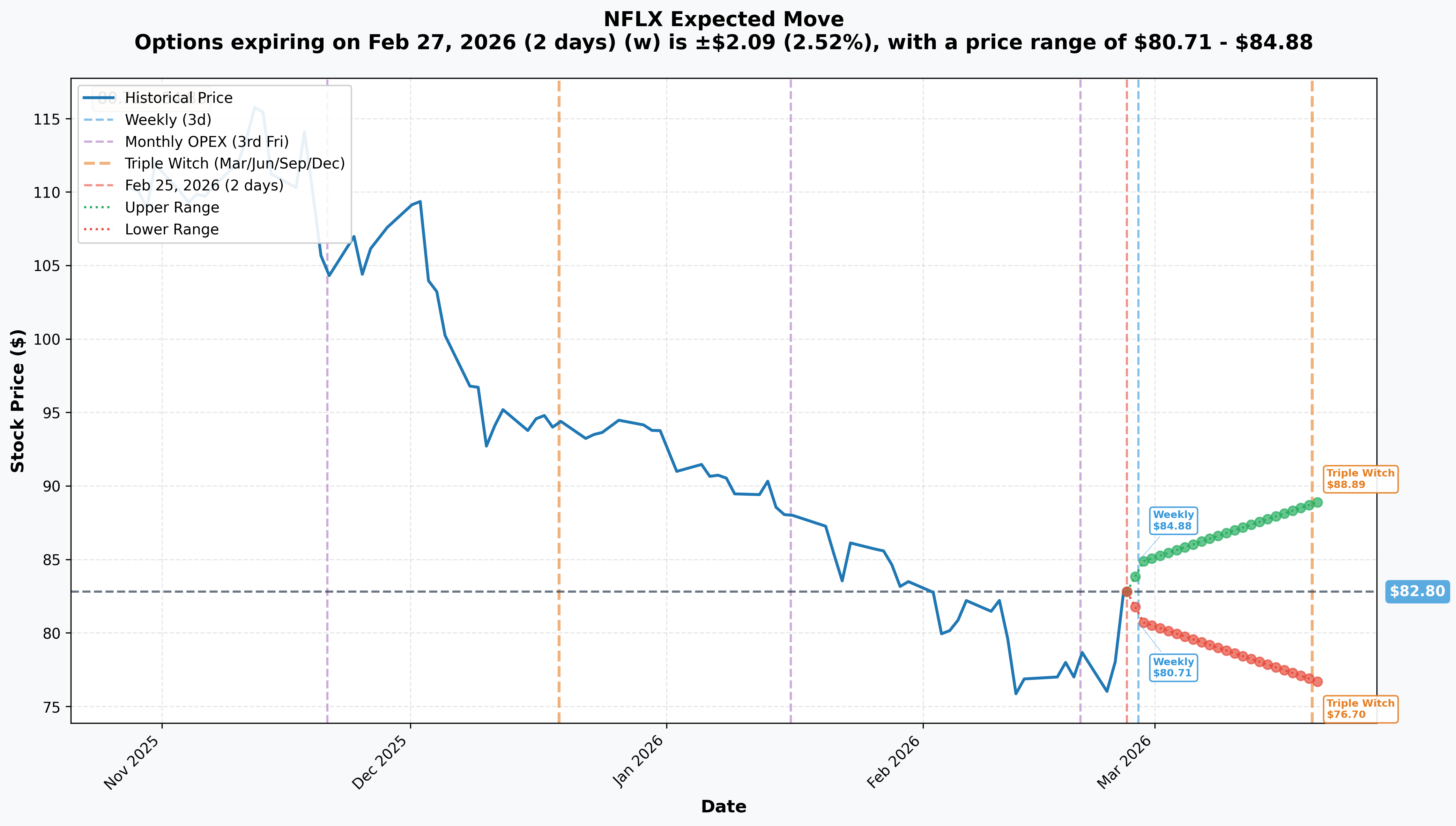

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Feb 27 - 2 days): ±$2.09 (±2.52%) --> Range: $80.71 - $84.88

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 23 days): ±$6.10 (±7.37%) --> Range: $76.70 - $88.89

- 📅 September 18 OPEX (THIS TRADE!): ~7 months out, extrapolated range roughly $60 - $115+

Translation: The options market expects NFLX could move ±2.5% this week and ±7.4% through the March 20 OPEX. That March 20 date is critical - it is the exact date of the WBD shareholder vote. That is NOT a coincidence. The market is pricing in a big move around that binary event.

The $90 strike on the lead call leg sits just above the monthly implied upper range of $88.89. That tells you this trader is not playing a near-term pop - they are positioning for the full 7-month catalyst calendar. The analyst consensus target of $116-$119 sits well within the expected September distribution, validating that the $100 and $120 strikes are achievable under favorable conditions.

Key insight: The weekly 2.5% implied move is relatively modest, but the monthly 7.4% move is elevated by the WBD vote. If the vote triggers a major repricing (deal collapse = bullish, deal proceeds = potentially bearish near-term), the initial jolt could set the trajectory for the remainder of the 7-month trade window.

🎪 Catalysts

🔥 Upcoming Catalysts

WBD Shareholder Vote - March 20, 2026 🗳️

This is THE catalyst that defines everything. WBD shareholders will vote on Netflix's $82.7B acquisition - and it just got complicated:

- 🤝 Paramount Skydance raised its competing bid to $31/share on February 24, with WBD saying the Paramount bid "could be preferable"

- ⚖️ Netflix has 4 business days to submit a counter-offer if the WBD board shifts its recommendation

- 🚨 Activist investor Ancora Alternatives is voting against the Netflix deal and backing Paramount

- 📊 Three possible outcomes: Netflix deal proceeds (~40%), Paramount wins (~35%), or no deal (~25%)

- 💡 Plot twist: If Netflix LOSES the WBD bid, that could actually be the most bullish outcome for NFLX stock - buybacks resume ($10.1B authorized), the balance sheet stays clean, and the WBD uncertainty premium evaporates overnight

DOJ Antitrust Review - March 23, 2026 Deadline 🔍

The DOJ issued a formal "second request" on January 16, probing whether the deal would "substantially lessen competition or create a monopoly":

- 📄 Document request recipients have until March 23 to respond

- 🏛️ Netflix co-CEO Ted Sarandos is scheduled to testify before the U.S. Senate

- ⏰ The inquiry is expected to add months to the regulatory timeline regardless of the shareholder vote outcome

- 🎯 If the DOJ signals opposition, the deal likely dies - which, paradoxically, many analysts view as bullish for NFLX shares

Q1 2026 Earnings - April 16-21, 2026 📊

Netflix guided Q1 2026 to $12.16B revenue (+15.3% YoY) with a 32.1% operating margin. Key things to watch:

- 📊 Consensus expects $12.16-$12.18B revenue and ~$0.76 EPS (split-adjusted)

- 💹 Ad revenue trajectory: is Netflix on track to $3B for full-year 2026 (doubling from $1.5B in 2025)?

- 👥 Subscriber growth: can they add meaningfully to the 325M base?

- 🤝 WBD deal status update and regulatory timeline clarity

- 📺 Impact of Universal first-window content and Sony Pay-1 deal on engagement metrics

Expected Price Increases - Q2 2026 💵

Management confirmed additional price increases planned for 2026 but hasn't specified timing or amounts. With 325M subscribers, even a $1/month increase represents ~$3.9B in annualized revenue uplift. The last increase was January 2025 (Standard went from $15.49 to $17.99).

Q2 2026 Earnings - July/August 2026 📊

- Second quarter of data under 2026 guidance - will reveal whether the $50.7-$51.7B revenue target is tracking

- WBD deal fate should be much clearer by then

- Early reads on summer content slate performance

- Ad revenue doubling trajectory checkpoint

September 18, 2026 - THIS TRADE EXPIRES ⏰

By expiration, the market will have digested: the WBD vote result, DOJ review progress, TWO full quarterly earnings reports, price increase implementation, ad revenue doubling trajectory, and the Sony/Universal content pipeline impact. The September date was chosen to capture maximum catalyst density.

✅ Recent Catalysts (Already Happened)

WBD Acquisition Announced - December 2025 🤝

Netflix announced it would acquire Warner Bros. Discovery for $82.7B total enterprise value ($72B equity + ~$10B assumed debt). Assets include Warner Bros. Entertainment, DC Comics/Studios, and HBO Max. Discovery Global Networks to be spun off separately. The deal was amended to all-cash on January 20, 2026. NFLX dropped ~30% on the announcement as investors worried about balance sheet leverage.

Q4 2025 Earnings - January 20, 2026 📊

Strong results but overshadowed by deal dynamics:

- 💰 Revenue: $12.05B (+17.6% YoY), beat Zacks estimate by 1.82%

- 📊 EPS: $0.56 split-adjusted (+30.2% YoY)

- 👥 325M paid memberships (+23M YoY)

- 💸 Full-year FCF: $9.5B (up from $6.9B in 2024)

- 📈 Full-year operating margin: 29.5% (up from 26.7% in 2024)

- 🔮 2026 guidance: $50.7-$51.7B revenue, 31.5% operating margin target, ~$11B FCF, $20B content spend

Sony Global Pay-1 Deal - January 2026 🎬

Netflix signed a $7B+ exclusive global Pay-1 deal with Sony Pictures - an industry first. Sony feature films will stream exclusively on Netflix worldwide after theatrical windows, with a rate card 40% higher than the previous deal. Upcoming titles include Spider-Man: Beyond the Spider-Verse and The Legend of Zelda (live-action).

Universal First-Window Deal - January 2026 🎥

Netflix replaced Amazon Prime Video as the first-window streaming home for Universal theatrical releases, with an exclusive 10-month streaming window before titles return to Peacock. Near-term titles: Jurassic World: Rebirth (Feb 28), Downton Abbey: The Grand Finale (Mar 7), Nobody 2 (Mar 14).

10-for-1 Stock Split - November 17, 2025 ✂️

Netflix completed a 10-for-1 forward stock split. Shareholders received 9 additional shares for every share held. Pre-split price was ~$900+; post-split trading began at ~$90. The split made options more accessible for retail traders - and massively increased contract volumes, as we see in today's 425,000+ contract trade.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, analyst targets, and the catalyst calendar, here are the scenarios through the September 18, 2026 expiration:

📈 Bull Case (30% probability)

Target: $115-$135

How we get there:

- 🗳️ WBD deal collapses or Paramount wins the bid - Netflix avoids $82.7B cash outlay, resumes $10.1B authorized buyback program, uncertainty premium evaporates

- 📊 Q1 and Q2 earnings beat expectations, ad revenue tracking toward $3B 2026 target

- 💵 Price increases implemented in Q2 boost ARPU and push revenue growth above the 12-14% guidance range

- 📈 Forward P/E re-rates from 25x back toward the historical average of 35-42x on clean balance sheet + growth

- 🎬 Sony Pay-1 + Universal first-window content drives subscriber growth reacceleration

- 📊 Stock breaks through $85, $90 gamma resistance and analyst upgrades push consensus target above $125 (current high: $151)

Trade P&L at $120:

- Bull call spread maxed at $91M profit ($110-$90 = $20 x 60K x 100 - $29M cost)

- $100 calls worth ~$20/share = $368M (184K contracts x $20 x 100)

- $120 calls at-the-money, roughly breakeven

- Total position value: ~$460M+ on $102M invested (roughly 4.5x return)

Trade P&L at $135:

- Bull call spread maxed at $91M profit

- $100 calls worth ~$35/share = $644M

- $120 calls worth ~$15/share = $182M

- Total position value: ~$917M on $102M invested (roughly 9x return)

This is the scenario where NFLX reverts toward its split-adjusted ATH of $133.91. The analyst high target of $151 and 76% Buy/Strong Buy consensus support this as achievable. The Paramount competing bid makes a deal collapse increasingly likely - potentially the fastest path to this outcome.

🎯 Base Case (45% probability)

Target: $88-$105 range

Most likely scenario:

- ✅ WBD deal outcome resolves in some direction and the uncertainty premium dissipates

- 📊 Earnings meet guidance but don't blow away estimates

- ⚖️ Ad revenue growing but not yet at the $3B annual run-rate pace

- 🔄 Stock grinds higher through $85, then $90 gamma resistance as deal overhang fades

- 📈 P/E re-rates from ~25x forward toward ~30-35x (still below the 42x historical average)

- 💰 If deal collapses, buyback resumption ($10B+/year) provides an immediate floor under the stock

Trade P&L at $95:

- Bull call spread: ($95-$90) x 60K x 100 - $29M = $1M gain (modest profit, spread is partially ITM)

- $100 calls: OTM, losing value but still have some time value

- $120 calls: deep OTM, minimal value

- Net position: roughly breakeven

Trade P&L at $105:

- Bull call spread: ($105-$90) x 60K x 100 - $29M = $61M gain

- $100 calls: $5 intrinsic x 184K x 100 = $92M

- $120 calls: still OTM, minimal value

- Net position: ~$153M on $102M invested (~1.5x return)

In this scenario, the bull call spread component does the heavy lifting - it starts profiting as soon as NFLX crosses ~$95 and accelerates toward $110. The outright $100 calls contribute above $103, while the $120 calls likely expire with minimal value. The trader could also take profits on the $100 calls before expiration if the stock reaches $95-100 with months of remaining time value.

📉 Bear Case (25% probability)

Target: $65-$80

What could go wrong:

- 😰 Netflix raises its WBD bid to counter Paramount, making the balance sheet impact even worse

- 🚨 DOJ formally challenges the merger, creating 12+ months of additional uncertainty

- 📉 Growth decelerates further - subscriber adds plateau, ad revenue disappoints, password sharing tailwinds are fully exhausted

- 💸 Consumer spending weakens, driving churn at higher price points after 2026 increases

- 🏢 Competitive bundling (Disney+/Hulu/ESPN, Prime Video/Paramount+) erodes Netflix's standalone value proposition

- 📊 Break below $80 mega-support (84.0B gamma) triggers a cascade toward $75 and below

- 🌍 FX headwinds and macro weakness hit international revenue

Trade P&L: All legs expire worthless or near-worthless. Loss = -$102M (-100%). However, the trader could cut losses before expiration if the thesis breaks. With 7 months of time value at entry, there's meaningful runway to exit at a partial loss if early catalysts (WBD vote, Q1 earnings) disappoint.

The $80 level with 84.0B total gamma is the CRITICAL support. If that breaks, the next major floor is $75 with put-dominated gamma. At $65-$70, the stock would be trading below 20x forward earnings for a company growing revenue 12%+ - arguably oversold territory that would attract value buyers.

💡 Trading Ideas

🛡️ Conservative: "Piggyback the Whale" - September Bull Call Spread

Play: Buy the NFLX September 18, 2026 $85 calls, sell the September 18, 2026 $100 calls

Structure: $85/$100 bull call spread, 7 months to expiration

Why this works:

- 📊 Mirrors the institutional thesis but at a more favorable entry ($85 strike is only 3% away vs. $90)

- 🛡️ Defined risk: you can only lose the net debit paid (~$6-8 per spread)

- 💰 Max profit: $15 per spread minus debit (~$7-9 gain) if NFLX above $100 at expiry

- ⏰ Same September expiration captures all catalysts: WBD vote, DOJ review, two earnings cycles, price increases

- 📈 The $85 strike is the nearest major gamma resistance (47.0B) - once NFLX clears this, the path to $90+ opens quickly

- 🎯 The $100 short strike aligns with the institutional $100 call position - you're riding in the whale's wake

- ⚖️ 76% of analysts rate NFLX as Buy or Strong Buy with an average target of $116-$119

Position sizing: Risk no more than 3-5% of portfolio. 20 spreads at ~$7 each = ~$14,000 risk for ~$16,000 max profit.

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

⚖️ Balanced: "March Madness" - WBD Vote Event Play

Play: Buy the NFLX March 20 $82.50 straddle (buy both the $82.50 call AND the $82.50 put)

Structure: At-the-money straddle expiring on Triple Witch / WBD shareholder vote date

Why this works:

- 🗳️ The WBD shareholder vote on March 20 is a binary event - the stock moves big regardless of the outcome

- 📊 Implied move of ±7.37% ($76.70 - $88.89) for March OPEX means the market already expects a $12+ range

- 💡 If deal collapses: stock could rip to $90+ as buybacks resume and balance sheet fears lift

- 💡 If deal proceeds and Netflix raises bid: stock could drop to $74-76 on leverage concerns

- ⚖️ You don't need to pick a direction - just bet on the MAGNITUDE of the move exceeding what options are pricing

- 🎢 Triple Witch OPEX adds extra volatility to the mix

- ⏰ Only 23 days of time decay exposure - short and punchy

Position sizing: 10-20 straddles at roughly $6 each = $6,000-$12,000 total risk. You profit if NFLX moves more than ~$6 in either direction by March 20.

Risk level: Moderate (time decay is the enemy, need a big move) | Skill level: Intermediate-Advanced

🚀 Aggressive: "Full Send" - September $100 Calls

Play: Buy NFLX September 18, 2026 $100 calls outright - piggybacking the whale's LARGEST single leg (184,000 contracts worth $54M!)

Why this works (and why it's risky):

- 💥 The $100 strike is where this institution concentrated MOST of their capital ($54M across 184,000 contracts) - follow the money

- 📊 $100 aligns with the lower end of the analyst consensus zone ($116-$119 average target); needs ~21% move to reach the strike

- ⏰ 7 months captures WBD resolution, two earnings reports, price increases, and ad revenue trajectory

- 🚀 If NFLX hits $120, these calls would be worth ~$20, roughly 7x a ~$2.93 entry

- 🚀 If NFLX hits $135 (near ATH), they're worth ~$35, roughly 12x return

- 🎯 Analyst consensus implies 40-57% upside from current levels - $100 is only halfway there

Why it could blow up:

- 💸 The $100 strike is 21% OTM - that's a big move even with 7 months

- ⏰ 7 months of time decay eating at your premium every single day

- 📉 If WBD deal uncertainty drags on and NFLX stays range-bound at $80-85, these calls bleed value fast

- 🎢 Netflix has already dropped 38% from ATH - no guarantee the bottom is in

- 👥 Zero insider buying at these levels - if management isn't loading up, that's worth noting

Position sizing: Risk ONLY what you can afford to lose completely. 20 contracts at ~$293 each = ~$5,860 at risk.

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⚖️ WBD acquisition is a double-edged sword: The $82.7B all-cash acquisition would add massive leverage to Netflix's balance sheet. Paramount's competing $31/share bid could force Netflix to raise its offer, making the financial burden even worse. Activist investor Ancora is voting against the Netflix deal. The March 20 shareholder vote and DOJ antitrust review create binary outcomes that could swing the stock 10-15% in either direction.

-

🏛️ DOJ antitrust scrutiny is real: The DOJ's "second request" explicitly questions whether the deal would "substantially lessen competition or create a monopoly." Ted Sarandos testifying before the Senate adds political risk. Even if the deal eventually closes, regulatory overhang could suppress the stock for multiple quarters.

-

📉 Growth is decelerating: 2026 revenue guidance of 12-14% growth is a clear step-down from 16% in 2025 and 17%+ quarterly rates. Password sharing crackdown tailwinds are plateauing. At 30x trailing earnings vs. a sector average of ~21x, the premium valuation demands strong execution.

-

💸 $9B/year buyback floor is gone: Netflix paused share repurchases to accumulate cash for the WBD deal. In 2025, they bought back ~$9B+ in stock. That natural price support has been completely removed. Until the deal resolves, there is no corporate bid under the stock.

-

🏢 Competition is intensifying: Disney's combined streaming share reached 26% in the U.S., Amazon bundles Prime Video with Prime membership, and Apple TV+ is spending $7B+/year. The "frenemy" bundling trend could erode Netflix's standalone value proposition over time.

-

💰 Content spend escalation crimps margins: $20B in 2026 content spending (+10% YoY) is necessary to maintain competitive position but pressures near-term profitability. Any high-profile content misses could weigh on sentiment.

-

⏰ $102M in premium = massive time decay: Even for an institution, $102M is serious money. At roughly $14-15M/month in theta decay across all legs, this position bleeds meaningfully if NFLX doesn't make progress above $90 by early summer. If the stock stays range-bound at $80-85 through Q1 earnings, the position could lose 30-40% of value even without a selloff.

-

👥 No insider buying at these levels: Zero insider purchases in the past 3 months, with 5 insider sales totaling $3.0M in February 2026. If management believed the stock was a screaming buy at $78-82, you might expect to see some open-market purchases. The absence is notable.

🎯 The Bottom Line

Here's the deal: Someone with extraordinarily deep pockets just put $102 MILLION on the table betting Netflix rallies from $82 to well above $100 by September 2026. This is the single largest options trade we have ever tracked - not by a small margin, but by a massive one. To put $102M in perspective: it is more capital than most hedge funds manage in their ENTIRE portfolios. Whoever did this has conviction measured in nine figures.

What this trade tells us:

- 🎯 Institutional money sees NFLX at $82 as deeply undervalued, well below the analyst consensus target of $116-$119

- 💰 They structured the trade intelligently: a bull call spread for high-probability base returns, plus outright long calls for explosive upside convexity

- ⏰ The September 18 expiration is surgical: it captures the WBD vote (March 20), DOJ review, Q1 earnings (April), Q2 earnings (July/August), price increases, and content catalysts - ALL in one trade

- 📊 The 10.71x Vol/OI on the lead leg confirms this is overwhelming new capital entering, not repositioning

- 🤝 The complex multi-leg structure with MID fills across all five legs confirms this is a single institutional order requiring prime brokerage execution

This IS a massive bullish signal, but with critical context: Netflix's core business is exceptional - $45.2B revenue, 29.5% operating margins expanding to 31.5%, 325M subscribers, $9.5B FCF growing to ~$11B. The stock is trading at its lowest forward P/E (25.4x) in years, well below the 3-year average of 42.5x. The entire selloff has been about the WBD deal, not business deterioration. If that deal overhang lifts, the stock has enormous room to re-rate.

If you're bullish on NFLX:

- ✅ Consider defined-risk strategies (call spreads, risk reversals) rather than naked calls to limit downside

- 📊 The $80 gamma support (84.0B total gamma) is your structural floor - set alerts if it breaks

- 📅 Mark March 20 (WBD shareholder vote) as the first and most critical catalyst

- 💡 If the WBD deal falls through, that could be the single biggest bullish catalyst - Netflix keeps its clean balance sheet, resumes $10B+ in buybacks, and the uncertainty premium evaporates

- 🎯 A break above $85 gamma resistance (47.0B) opens the path to $90 and begins unlocking the $102M whale's thesis

If you're watching from the sidelines:

- ⏰ Wait for the March 20 WBD vote to clarify the fundamental picture before committing capital

- 📊 76% of analysts rate NFLX as Buy or Strong Buy with an average target of $116-$119 and a high of $151 - that's 50-80%+ upside

- 📈 A deal collapse + buyback resumption could trigger a violent snapback rally from $82 to $95-100+ in weeks

- ⏰ Q1 earnings on April 16-21 will be the second major checkpoint for thesis validation

If you're cautious:

- ⚠️ The all-cash WBD deal at $82.7B could saddle Netflix with enormous debt and integration risk

- 📉 A break below $80 gamma support (the strongest level on the entire board) would change the technical picture dramatically

- 🛡️ Consider collar strategies or put spreads to protect existing positions through the March 20 vote

- 📊 No insider buying at these levels is a yellow flag worth acknowledging

Key dates to mark:

- 📅 February 27 (Thursday) - Weekly OPEX (±2.5% implied move)

- 📅 March 20 (Friday) - WBD shareholder vote + Triple Witch OPEX (±7.4% implied move - THE big event)

- 📅 March 23 (Monday) - DOJ document request deadline

- 📅 April 16-21 - Q1 2026 earnings report

- 📅 Q2 2026 (TBD) - Expected price increases

- 📅 July/August 2026 - Q2 2026 earnings

- 📅 September 18, 2026 - THIS TRADE EXPIRES - moment of truth for the $102M bet

- 📅 November 26, 2026 - Narnia IMAX theatrical release (Thanksgiving tentpole)

- 📅 December 25, 2026 - NFL Christmas Day games on Netflix (Year 3 of deal)

Final verdict: Netflix at $82 is a stock being punished for deal uncertainty, not business deterioration. Revenue growing 12-14%, margins expanding to 31.5%, ad revenue doubling to $3B, and content deals with Sony ($7B+) and Universal creating the widest content moat in streaming history. The $102M multi-leg bet is the loudest institutional bullish signal imaginable - someone with serious conviction and serious capital believes the WBD overhang resolves and NFLX re-rates toward $100-$120+. The risk is that the deal drags on, the balance sheet gets stretched, and the growth story cools. The smarter retail play is to use defined-risk strategies, let the March 20 vote clarify the path, and ride the aftermath at a fraction of the whale's risk.

$102 million in a single trade. 305,000 net long call contracts. Seven months of runway. Whatever this institution knows - or thinks they know - about Netflix's next chapter, they are putting generational capital behind it. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. Complex multi-leg options strategies involve multiple commissions and can result in total loss of all premiums paid. The $102M institutional trade analyzed here may represent hedging, structured product, or portfolio objectives not applicable to retail traders. The WBD acquisition creates binary event risk with potential for 10-15% stock moves in either direction around the March 20 vote. Always do your own research and consider consulting a licensed financial advisor before trading.

About Netflix Inc: Netflix is a subscription-based streaming entertainment service offering TV series, documentaries, feature films, mobile games, and live events to over 325 million paid members in more than 190 countries, with a market cap of $329.5B in the Services - Computer Programming, Data Processing industry.