NKE $1.8M LEAPS Put - Institutional Bet on 2-Year Nike Turnaround Failure!

January 15, 2026 | Unusual Activity Detected

The Quick Take

Someone just dropped $1.8 MILLION on Nike LEAPS puts expiring in January 2028 - that's a 2-YEAR bearish bet on the athletic footwear giant! This trader bought 1,500 contracts of the $65 strike at-the-money puts, paying $11.95 per contract while NKE trades at $64.38. With Nike navigating a complex turnaround under CEO Elliott Hill, struggling in China (down 17% last quarter), and facing $1.5 billion in tariff headwinds, this institutional player is betting the Swoosh stumbles over the next two years.

Company Overview

Nike Inc. (NKE) is the world's largest athletic footwear and apparel company:

- Market Cap: $97.07 billion

- Industry: Athletic Footwear & Apparel (Rubber & Plastic Footwear)

- Current Price: $64.38 (near 52-week low of $57)

- 52-Week High: $82.44

- Primary Business: Designs, develops, and markets athletic footwear, apparel, and equipment under Nike, Jordan, and Converse brands across 190+ countries

Nike holds approximately 18% of the global sneaker market, more than double its closest competitor Adidas at 9%.

The Option Flow Breakdown

The Tape (January 15, 2026 @ 13:21:10):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 13:21:10 | NKE | MID | BUY | PUT $65 | 2028-01-21 | $1.8M | $65 | 1,500 | 1,400 | 1,500 | $64.38 | $11.95 |

What This Actually Means

This is a long-term directional bearish position - someone is betting Nike will be significantly lower in 2 years! Here's what went down:

- Massive time horizon: January 2028 expiration - 2 FULL YEARS out! This isn't a quick trade, it's a thesis.

- At-the-money strike: $65 strike vs $64.38 spot price - this trader wants maximum sensitivity to downside moves

- Premium paid: $1.8M ($11.95 per contract x 1,500 contracts x 100 multiplier)

- Volume > Open Interest: 1,500 volume vs 1,400 OI signals this is likely an OPENING position (new bet)

- Z-Score of 17.51: Classified as "EXTREMELY UNUSUAL" - this size of LEAPS put trade is rare

- Breakeven: Nike needs to fall below $53.05 by January 2028 for this trade to profit (18% decline from current price)

What's really happening here: This trader isn't hedging - they're making a multi-year directional bet that Nike's turnaround fails. By going 2 years out, they're giving themselves maximum time for the thesis to play out: China recovery stalls, tariffs bite margins, competition from On Running and Hoka accelerates, and the "Win Now" strategy doesn't deliver. LEAPS puts are expensive (cost $11.95 per share), but they provide the luxury of TIME - this position won't blow up on one bad quarter.

Why LEAPS puts make sense here:

- Nike is in the middle of a multi-year turnaround - takes time to prove success OR failure

- Q3 FY2026 earnings March 19, 2026, Q4 June 2026, FIFA World Cup catalyst June-July 2026 - all within first year

- By January 2028, we'll have 8+ quarters of data to judge CEO Elliott Hill's "Win Now" strategy

- If turnaround fails, stock could easily trade $45-50 (30%+ downside) - puts worth $15-20

Technical Setup / Chart Check-Up

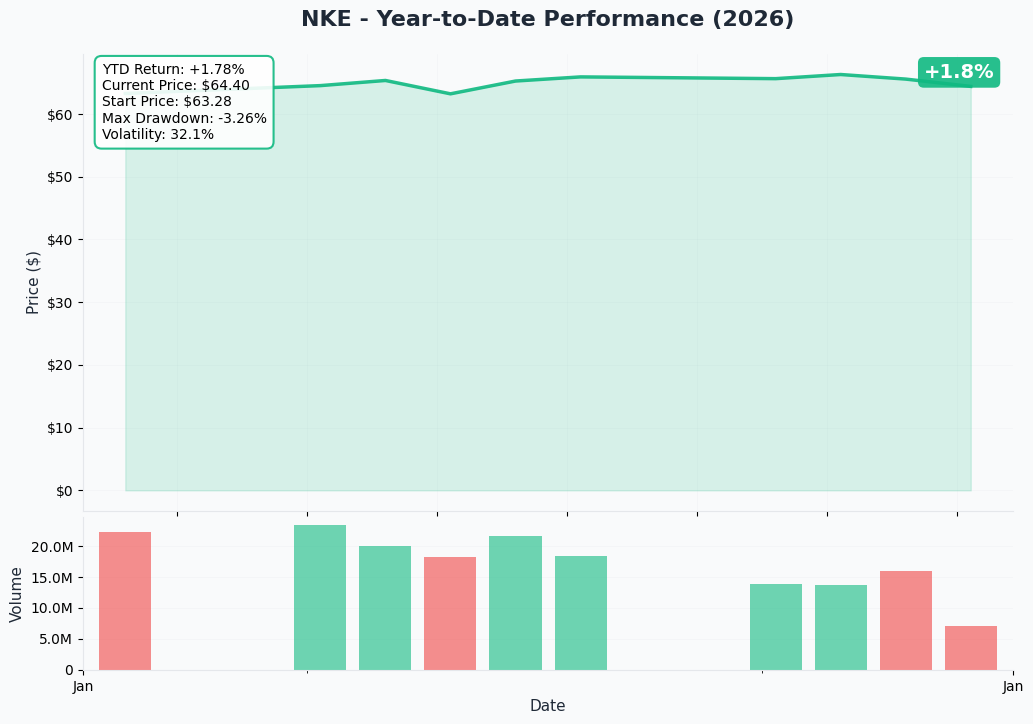

YTD Performance Chart

Nike has been a tale of disappointment for shareholders - down from $82.44 highs to current $64.38 levels, representing a 22% decline from peak. The stock has lost nearly half its value over the past three years, marking four consecutive down years. After a brief rally following CEO Elliott Hill's appointment in October 2024 and Q2 FY2026 earnings beat in December 2025, shares have drifted lower as China concerns persist.

Key observations:

- Multi-year downtrend: From $180 peak in 2021 to current $64 - massive wealth destruction

- 52-week range: $57 - $82.44 - currently trading near lower end

- Recent bounce: Rally from $57 December low to $65 on insider buying by Tim Cook, CEO Hill, and director Robert Swan totaling $4.45 million

- Support tested: $57 level held in December - critical floor to watch

- Dividend yield: 2.50% provides some downside cushion for equity holders

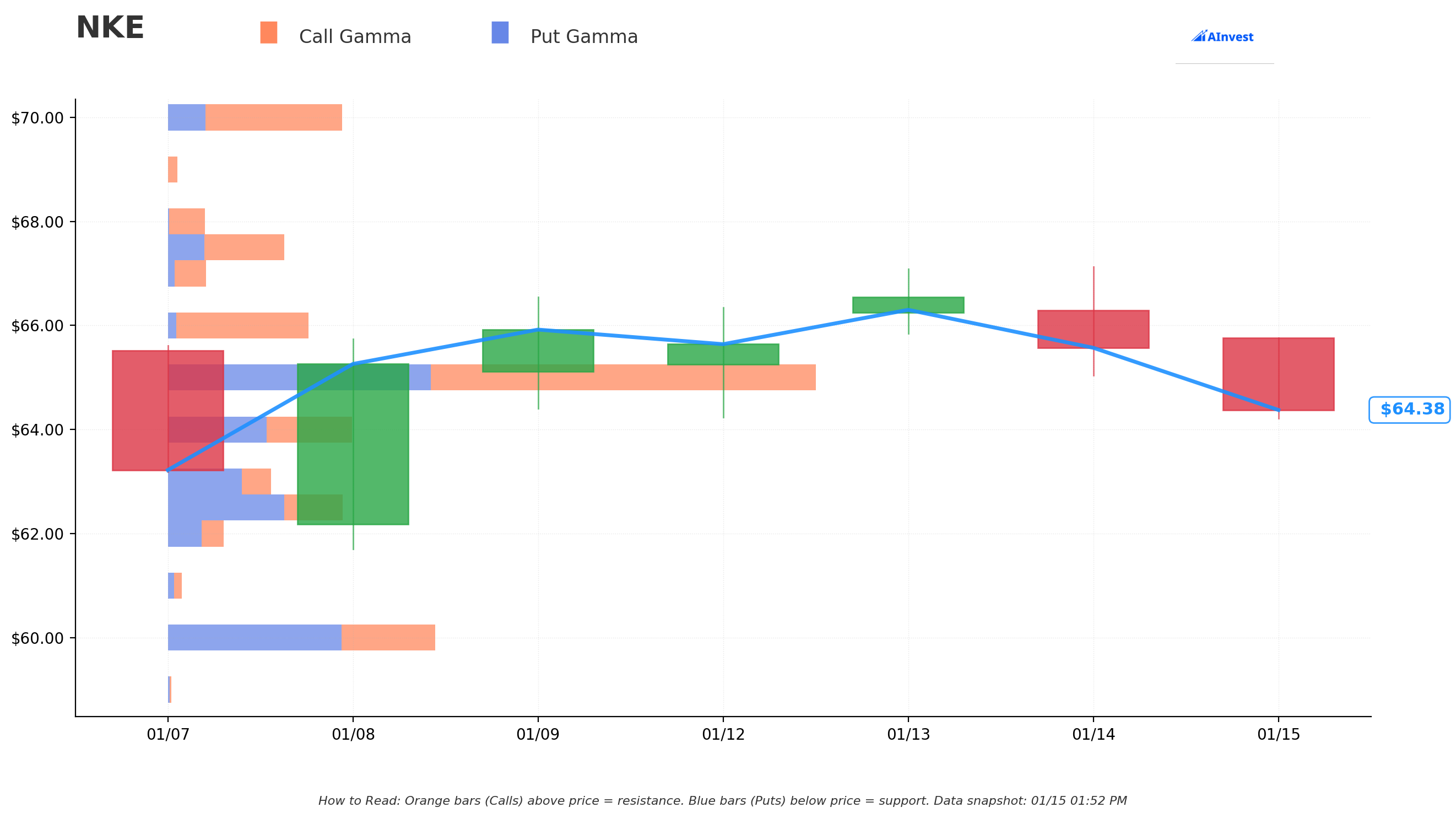

Gamma-Based Support & Resistance Analysis

Current Price: $64.37

The gamma exposure map reveals critical price levels where dealer hedging creates natural support and resistance:

Support Levels (Put Gamma Below Price):

- $64 - Immediate support with 24.9B total gamma exposure (strongest nearby floor, only 0.6% below current)

- $63 - Secondary support at 13.9B gamma (2.1% below)

- $62.50 - Major structural support with 23.4B gamma (2.9% below)

- $60 - Deep support at 35.6B gamma (6.8% below - CRITICAL LEVEL if downtrend accelerates)

- $55 - Extended floor at 7.6B gamma (14.6% below - disaster scenario)

Resistance Levels (Call Gamma Above Price):

- $65 - MAJOR resistance with 86.0B gamma exposure (STRONGEST LEVEL - massive dealer selling will cap rallies here)

- $66 - Secondary resistance at 18.7B gamma (2.5% above)

- $67.50 - Upper resistance at 15.6B gamma (4.9% above)

- $70 - Extended ceiling at 23.2B gamma (8.7% above)

- $75 - Long-term resistance at 11.6B gamma (16.5% above)

What this means for traders: The $65 strike where this put trade was placed is THE dominant gamma level! With 86.0B total gamma exposure, this is where dealers hold massive positions. The put buyer chose this strike because it's the exact point where call gamma overwhelms put gamma - if stock breaks below here, momentum could accelerate rapidly toward $60. Net GEX bias is "Bullish" overall (189.2B call vs 141.0B put gamma), but that bullish positioning creates a WALL at $65 that limits upside.

Notice the setup: The put buyer struck at $65 where there's maximum gamma activity. They're betting that if Nike can't break through $65 resistance, the stock will eventually fail and test deeper support at $60, then $55. The 2-year timeframe gives plenty of opportunities for this thesis to play out.

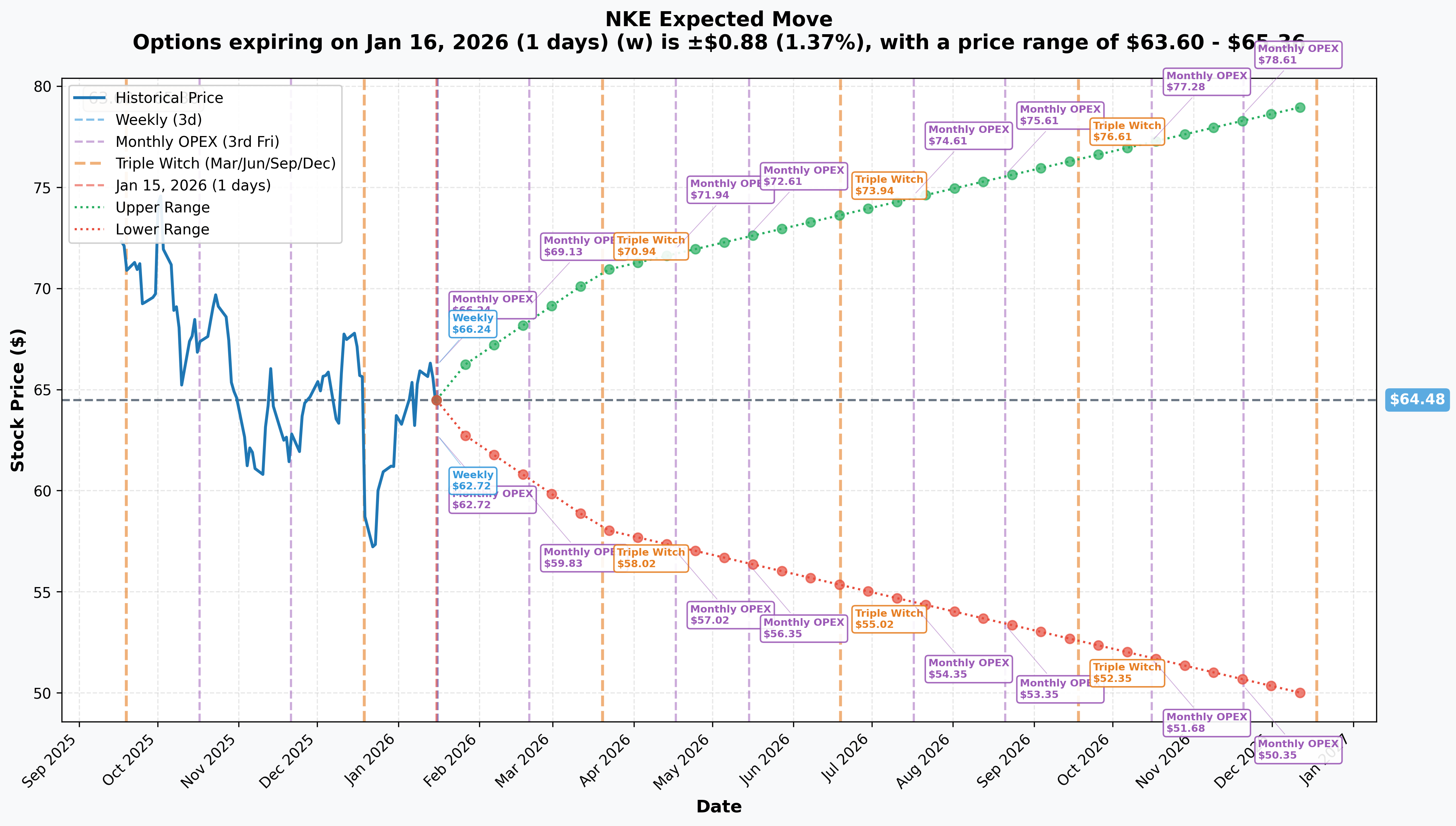

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 16 - 1 day): +/-$0.88 (+/-1.37%) - Range: $63.60 - $65.36

- Monthly OPEX (Feb 20): +/-$4.65 (+/-7.2%) - Range: $59.83 - $69.13

- Triple Witch (Mar 20 - Q3 earnings!): +/-$6.40 (+/-9.9%) - Range: $58.02 - $70.94

- Yearly LEAPS (Dec 18): +/-$14.68 (+/-22.8%) - Range: $49.80 - $79.16

Translation for regular folks: Options traders are pricing in a MASSIVE 23% potential move over the next year, with a lower bound of $49.80. This aligns PERFECTLY with the put buyer's thesis - the market acknowledges significant downside risk exists. The put buyer's January 2028 expiration goes BEYOND even the yearly LEAPS pricing, suggesting they see even more extended downside potential.

Key insight: The implied move's lower range of $49.80 by December 2026 would put this $65 put trade deep in the money (worth $15.20 intrinsic value alone). The trader is essentially betting the market is correctly pricing this risk, and they want to capture it.

Catalysts

Upcoming Catalysts (Next 6-24 Months)

Milan Winter Olympics - February 6-22, 2026 The Winter Olympics provide a global marketing platform. StockX notes these events historically "drive spikes in demand for athlete and team-linked products". Nike could benefit from sponsored athlete performances and related product launches.

Q3 FY2026 Earnings - March 19, 2026 According to Nasdaq and TipRanks, this report will reveal critical turnaround progress. Consensus expects:

- Revenue: $11.25 billion (low single-digit decline expected)

- EPS: $0.32

- Key metrics: North America momentum, China reset progress, gross margin trajectory (guided down 175-225 bps)

2026 FIFA World Cup - June 11 to July 19, 2026 Nike's biggest marketing opportunity in years. According to Modern Retail and Yahoo Finance:

- Nike sponsors 13 of 48 participating nations including Brazil ($100M/year through 2038), France, England, and U.S. Men's National Team

- Potential revenue benefit of $1.3 billion spread across FY26

- Marketing expense expected to exceed $5 billion in 2026

- Bank of America analysts project "moderate boost" for both Nike and Adidas

Q4 FY2026 Earnings - June 2026 (Expected) Full-year results and FY2027 guidance. Management has framed FY2026 as a "reset year" per Simply Wall St - this report will reveal whether the reset is working.

Product Pipeline Through 2027:

- Caitlin Clark signature sneaker launch in 2026 per StockX

- Nike Mind series (neuroscience-enhanced performance footwear)

- Multiple Air Jordan retro releases per DraftKings Network

Recent Catalysts (Already Happened)

Q2 FY2026 Earnings - December 18, 2025 Per Nike Investor Relations and CNBC, results were mixed:

- Revenue: $12.43B vs $12.22B expected (beat by 2%)

- EPS: $0.53 vs $0.38 expected (beat by 39%)

- BUT Greater China collapsed: $1.42B (down 17% YoY) - major disappointment

- Gross margin: 40.6% (down 300 bps due to tariffs and discounting)

- Converse revenue: $300M (down 30% YoY)

- Nike Direct: Down 8%, Nike Digital down 36% in China

Insider Buying - December 22-31, 2025 Per CNBC and WWD, three insiders purchased $4.45M in stock:

- Tim Cook (Apple CEO, Nike Director): 50,000 shares at $58.97 ($2.95M)

- Elliott Hill (CEO): 16,388 shares at $61.10 ($1.0M) - first purchase since becoming CEO

- Robert Swan (Director): 8,691 shares at $57.54 ($500K)

Leadership Restructuring - December 2, 2025 Per Business Wire and Retail Dive, Nike eliminated CTO and CCO positions, elevated regional presidents, and promoted Venky Alagirisamy to new COO role to "remove layers" and improve execution speed.

Price Targets & Probabilities

Based on gamma levels, implied move data, and catalysts, here are the scenarios through January 2028:

Bull Case (25% probability)

Target: $75-$85

How we get there:

- CEO Elliott Hill's "Win Now" strategy delivers - wholesale up 20%+ annually per CNBC

- FIFA World Cup 2026 drives meaningful revenue boost and brand heat

- China stabilizes and recovers to flat or positive growth by FY2027

- Gross margins recover to 42%+ as tariff mitigation kicks in

- Converse turnaround begins showing traction

- Stock breaks above $65 gamma wall, triggering momentum to $70, then $75

Probability assessment: Only 25% because turnaround requires multi-year execution with multiple headwinds. Current analysts per MarketBeat average PT of $75.16 suggests limited upside even in bull case.

Put P&L in Bull Case:

- Stock at $80 on Jan 2028: Puts worth $0, loss = -$11.95/share x 1,500 = -$1.79M (100% loss)

Base Case (50% probability)

Target: $55-$65 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- Turnaround shows mixed progress - North America solid, China still struggling

- FIFA World Cup provides modest boost but not transformational

- Gross margins remain pressured at 39-41% from tariffs per Investing.com

- Converse continues to drag (currently down 30%)

- Stock trades in range between $55 support and $65 resistance for extended period

- Dividend yield of 2.50% provides floor for equity holders

This is the put buyer's partial-win scenario: Stock consolidates around $55-60, puts gain intrinsic value of $5-10, representing 40-80% profit on the trade.

Put P&L in Base Case:

- Stock at $60 on Jan 2028: Puts worth $5.00 intrinsic + time value (~$2) = ~$7.00, loss = -$4.95/share x 1,500 = -$742K (41% loss)

- Stock at $55 on Jan 2028: Puts worth $10.00 intrinsic + time value = ~$11-12, profit = ~$0-1/share x 1,500 = breakeven to small profit

Bear Case (25% probability)

Target: $40-$50 (PUT BUYER'S THESIS PLAYS OUT)

What could go wrong for Nike:

- China recovery stalls further - 17% decline per CNBC becomes entrenched

- Competition accelerates - On Running and Hoka continue taking premium share per Business of Fashion

- Tariff costs exceed $1.5B annual impact per Supply Chain Dive

- Converse deterioration accelerates (already down 30%)

- DTC strategy continues failing - Nike Direct not expected to grow in FY2026 per Modern Retail

- Multiple analyst downgrades - Tom Nikic already moved to Hold citing "brand heat" concerns per Benzinga

- Stock breaks below $57 support, cascades toward $50 and potentially $45

Put P&L in Bear Case:

- Stock at $50 on Jan 2028: Puts worth $15.00+ (intrinsic), profit = $3.05/share x 1,500 = $458K (26% ROI)

- Stock at $45 on Jan 2028: Puts worth $20.00+ (intrinsic), profit = $8.05/share x 1,500 = $1.21M (67% ROI)

- Stock at $40 on Jan 2028: Puts worth $25.00+ (intrinsic), profit = $13.05/share x 1,500 = $1.96M (109% ROI)

Trading Ideas

Conservative: Watch and Wait for Better Entry

Play: Stay on sidelines until Q3 earnings (March 19, 2026) provides more data on turnaround

Why this works:

- Nike is mid-turnaround with mixed signals - insider buying bullish, China bearish

- FIFA World Cup catalyst (June 2026) could provide lift OR disappoint

- 2.50% dividend yield provides some cushion, but not enough to offset potential 20% drawdown

- Better to wait for either: 1) Stock breaks $65 resistance (bullish confirmation) or 2) Stock tests $55 support (better entry)

Action plan:

- Monitor Q3 earnings March 19 for China commentary and margin guidance

- If stock breaks above $65 with volume, consider small long position with $60 stop

- If stock breaks below $55, wait for stabilization before any position

- Use March Triple Witch implied move range ($58-$71) as guide for near-term expectations

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: Put Spread Mimicking Institutional Positioning

Play: Buy put spread targeting $60-$55 support zone, January 2027 expiration

Structure: Buy $60 puts, Sell $55 puts (January 2027 expiration - 1 year out)

Why this works:

- Defined risk spread ($5 wide = $500 max risk per spread)

- Targets gamma support zone at $55-$60 where significant put gamma exists

- 1-year timeframe captures Q3/Q4 FY2026 earnings, FIFA World Cup result, and initial FY2027 outlook

- Cheaper than outright LEAPS puts - pays ~$2.50-3.00 instead of $11.95

Estimated P&L:

- Pay ~$2.50-3.00 net debit per spread

- Max profit: $2.00-2.50 if NKE below $55 at January 2027 expiration (67-100% ROI)

- Max loss: $2.50-3.00 if NKE above $60 (100% loss but defined)

- Breakeven: ~$57-58

Position sizing: Risk 2-5% of portfolio maximum

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

Aggressive: LEAPS Put Position (Copy the Institution)

Play: Buy January 2028 $60 puts - same expiration as the institutional trade but lower strike for better risk/reward

Structure: Buy $60 strike LEAPS puts, January 2028 expiration

Why this could work:

- Same thesis as the $1.8M institutional trade - Nike turnaround fails over 2 years

- Lower strike ($60 vs $65) costs less premium (~$8-9 vs $11.95), improves risk/reward

- 2-year timeframe gives maximum opportunity for bearish thesis to develop

- Breakeven around $51-52 - needs ~20% decline but has 2 years to get there

- Key catalysts: China continues struggling, competition intensifies, tariff costs persist

Why this could blow up:

- LEAPS puts are EXPENSIVE - $8-9 per share is significant premium

- Nike could stabilize and trade sideways - 2 years of theta decay kills position

- FIFA World Cup could reignite brand momentum

- Insider buying ($4.45M) suggests management believes in turnaround

- Stock already near 52-week lows - limited downside vs significant upside risk

Estimated P&L:

- Pay ~$8-9 per contract ($800-900 per contract, size appropriately)

- Max profit: Unlimited if Nike collapses (stock at $40 = puts worth $20, 100%+ ROI)

- Max loss: Entire premium if Nike rallies above $60 by January 2028

- Breakeven: ~$51-52 (21% below current price)

CRITICAL WARNING - DO NOT attempt unless you:

- Can afford to lose ENTIRE premium (real possibility!)

- Have conviction in bearish thesis lasting 2 years

- Understand LEAPS theta decay accelerates in final 6-12 months

- Plan position size to be <5% of portfolio

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced only

Risk Factors

Don't get caught by these potential landmines:

-

China structural challenges: Greater China revenue down 17% in Q2 with Nike Digital down 36%. Local competitors Anta and Li-Ning gaining share with nationalistic consumers per Nasdaq. CEO Hill warned China is "at the top of that list" for turnaround focus, but marketplace reset will "take time."

-

$1.5B annual tariff headwind: Supply Chain Dive reports tariff costs increased from initial $1B estimate to $1.5B annualized. Q3 guidance includes 315 bps gross margin headwind from tariffs alone. Almost 95% of Nike footwear comes from Vietnam, China, and Cambodia - all facing 19-30% tariff rates.

-

Converse brand collapse: Business of Fashion reports Converse revenue down 30% in Q2 to $300M. Brand has over-relied on Chuck Taylor while failing to generate excitement elsewhere. Management expects continued headwinds throughout FY2026.

-

Competitive pressure intensifying: RBC research via Business of Fashion shows 13 challenger brands (On Running, Hoka) growing at 29% annual rate vs incumbents' 8%. Projected to continue outpacing through 2026. Nike has lost shelf space to competitors who filled the void during DTC pivot.

-

Insider buying could be WRONG: Tim Cook, CEO Hill, and director Swan bought $4.45M of stock in late December - but insiders can be wrong! Nike has declined nearly 50% over past 3 years despite periodic insider purchases. Management conviction doesn't guarantee turnaround success.

-

Valuation still elevated despite decline: At 38.45x trailing P/E per CNBC and Yahoo Finance, Nike trades at premium to historical averages for a company with declining margins and negative China growth. Multiple contraction could continue.

-

DTC strategy pivot risk: Modern Retail analysis shows Nike Direct down 8% in Q2 FY2026. Company does not expect direct business to return to growth in FY2026. Wholesale rebuild (up 8%) is helping but represents lower-margin sales channel.

-

2-year timeframe is LONG: The put buyer is betting on a 2-year thesis. A LOT can change - management could be replaced, strategy could shift, macro conditions could improve. LEAPS positions require sustained conviction through multiple news cycles.

The Bottom Line

Real talk: Someone just bet $1.8 MILLION that Nike's turnaround FAILS over the next 2 years. This isn't a hedge - it's a directional thesis. They chose LEAPS puts (2-year expiration) because turnarounds take time to prove success OR failure, and they want maximum time for their bearish view to play out.

What this trade tells us:

- Sophisticated player sees structural challenges persisting: China down 17%, Converse down 30%, $1.5B tariff drag

- At-the-money $65 strike chosen at maximum gamma level - if stock fails here, momentum accelerates downward

- 2-year timeframe captures multiple catalyst windows: Q3/Q4 FY2026 earnings, FIFA World Cup, FY2027 full results

- Z-score of 17.51 ("EXTREMELY UNUSUAL") shows this is a conviction bet, not routine portfolio activity

- Needs Nike below $53 to profit - 18% decline from current price over 2 years

If you're bullish on Nike:

- Insider buying ($4.45M from Tim Cook, CEO Hill) provides some confidence signal per CNBC

- FIFA World Cup (June 2026) represents $1.3B revenue catalyst with Nike sponsoring 13 of 48 teams per Yahoo Finance

- Analyst consensus remains "Buy" with average PT of $75-80 suggesting 15-20% upside per TipRanks

- Dividend yield of 2.50% provides income while waiting for turnaround

- BUT watch $65 gamma resistance - can't break through = momentum stalls

If you're bearish on Nike:

- This $1.8M LEAPS put validates your thesis - institutional money shares the concern

- China structural challenges (local competition, economic weakness) may persist beyond FY2026 per Business of Fashion

- Tariff costs creating long-term margin compression - targeting 120 bps net impact but actual could be worse

- Competition intensifying - On Running and Hoka capturing premium market segment

- BUT be aware - LEAPS puts are expensive and require patience through multiple news cycles

If you're on the sidelines:

- Wait for Q3 earnings (March 19, 2026) for next data point on turnaround

- Key metrics to watch: China trajectory, gross margin stabilization, Converse turnaround signs

- FIFA World Cup result (June-July 2026) will provide clarity on brand momentum

- Better entry likely if stock tests $55 support OR breaks above $65 resistance

- Current $64 level is "no man's land" - not clearly bullish or bearish

Mark your calendar - Key dates:

- February 6-22, 2026 - Milan Winter Olympics (marketing opportunity)

- March 19, 2026 - Q3 FY2026 earnings (critical turnaround update)

- June 11, 2026 - FIFA World Cup begins (major catalyst)

- July 19, 2026 - FIFA World Cup Final (peak marketing moment)

- June 2026 (est.) - Q4 FY2026 earnings and FY2027 guidance

- January 21, 2028 - This LEAPS put expiration (thesis judgment day)

Final verdict: This $1.8M LEAPS put represents a patient, thesis-driven bet that Nike's structural challenges (China, tariffs, competition) persist through CEO Elliott Hill's "Win Now" turnaround window. The trader isn't betting on a crash tomorrow - they're betting the Swoosh continues to stumble over the next 2 years. Whether you agree or disagree, this trade highlights the REAL uncertainty surrounding one of the world's most iconic brands. For retail traders, the wisest approach is probably to stay nimble, wait for clearer signals from upcoming catalysts, and avoid getting caught between institutional bulls (insider buyers) and bears (this put buyer).

Nike's turnaround will either work or it won't - but we'll need multiple quarters of data to know for sure.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. LEAPS options carry significant time decay risk and can lose 100% of premium even if directional thesis is correct but timing is off. The Z-score of 17.51 reflects this specific trade's unusual size - it does not guarantee the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading.

About Nike Inc.: Nike Inc. designs, develops, and markets athletic footwear, apparel, equipment, and accessories under the Nike, Jordan, and Converse brands. The company holds approximately 18% of the global sneaker market and operates across 190+ countries, with a market cap of $97.07 billion in the Rubber & Plastic Footwear industry.