🚀 NOW $7.6M LEAPS Bull Call Spread Close - Taking Chips Off The Table Pre-Split! 💎

📅 December 15, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed a $7.6 MILLION LEAPS bull call spread on ServiceNow (NOW) this morning! This sophisticated trader exited a massive spread position (Sell $820 calls, Buy $720 calls) with 368 days to expiration, banking gains just 3 days before NOW's historic 5-for-1 stock split. With the stock at $779 and major catalysts ahead (split, $7B Armis acquisition, earnings Jan 28), smart money is derisking after an epic run-up. Translation: Institutions locking in profits at the peak!

📊 Company Overview

ServiceNow, Inc. (NOW) is a leading enterprise cloud computing company that structures and automates business processes through its SaaS platform:

- Market Cap: $179.48 Billion (95th most valuable company globally)

- Industry: Prepackaged Software / Enterprise Workflow Automation

- Current Price: $779.00 (will adjust to ~$156 post-split)

- Primary Business: IT service management (ITSM), AI-powered workflow automation (Now Assist), customer service, HR, and security operations

ServiceNow serves over 2,100 enterprise customers with Annual Contract Value (ACV) exceeding $1 million, competing in the $400B+ enterprise software market.

💰 The Option Flow Breakdown

The Tape (December 15, 2025 @ 10:05:55-56):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:05:55 | NOW | ASK | SELL | CALL $820 | 2026-12-18 | $3.1M | $820 | 300 | 283 | 270 | $779.00 | $115.98 |

| 10:05:56 | NOW | BID | BUY | CALL $720 | 2026-12-18 | $4.5M | $720 | 300 | 230 | 270 | $779.00 | $167.88 |

🤓 What This Actually Means

This is a LEAPS bull call spread being CLOSED after a profitable run! Here's the breakdown:

- 💸 Net premium received: $1.4M (Paid $4.5M for $720 calls, Received $3.1M for $820 calls = Net $1.4M to close)

- 📊 Original position: This trader had BOUGHT the $720/$820 bull call spread months ago, betting NOW would rally above $820 by Dec 2026

- 🎯 Profit taking: With stock at $779 (just 5.3% below the $820 short strike), they're exiting the entire position to lock in gains

- ⏰ Strategic timing: Closing 3 days before Dec 18 stock split and ahead of massive Armis acquisition close

- 🏦 Size matters: 270 contracts = 27,000 shares worth ~$21M notional exposure

What's really happening here:

When you BUY a bull call spread, you're bullish but capping upside. This trader originally:

- BOUGHT $720 calls (bullish bet)

- SOLD $820 calls (capped gains at $820)

- Max profit: $100 per spread ($820 - $720) if stock above $820 at expiration

Now they're REVERSING the trade to close it:

- SELL TO CLOSE the $720 calls they owned (collecting $167.88 per contract = $4.5M)

- BUY TO CLOSE the $820 calls they sold (paying $115.98 per contract = $3.1M)

- Net result: Walk away with the spread value of $51.90 per contract ($167.88 - $115.98)

Why close NOW instead of waiting?

- 🎪 Stock split complexity: 5-for-1 split on Dec 18 will adjust strikes to $144/$164 post-split - cleaner to exit beforehand

- ⚠️ Armis acquisition risk: $7B deal expected to close "within days" - stock dropped 11% on announcement, could create more volatility

- 💰 Capture gains: Already captured most of the $100 max spread value ($51.90 = 52% of max profit) with 368 days remaining

- 📊 KeyBanc downgrade: Recent analyst cut to Underweight at $775 target suggests near-term headwinds

- 🎯 Tax considerations: Locking in 2025 gains before year-end

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-score 5.19 and 4.27 for the two legs) - This happens maybe a few times per year for NOW. The size (270 contracts) is massive for LEAPS spreads, representing significant institutional derisking.

📈 Technical Setup / Chart Check-Up

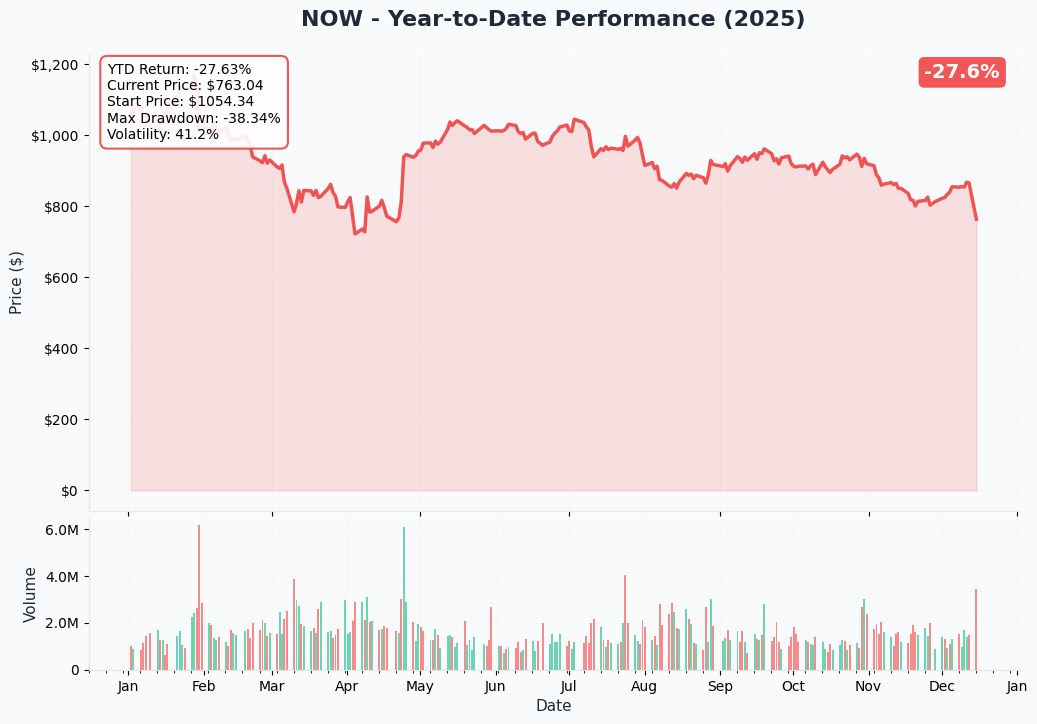

YTD Performance Chart

ServiceNow has had a volatile ride in 2025, currently trading at $779 - showing the extreme momentum and recent pullback story:

Key observations:

- 🚀 Epic rally to ATH: Stock rocketed to all-time highs above $1,000 in November on AI momentum and OpenAI partnership speculation

- 📉 Sharp pullback: Down ~22% from November peak following Armis acquisition announcement and KeyBanc downgrade

- 📊 YTD performance: Still up solid double-digits YTD despite recent weakness

- 🎢 High volatility zone: Recent 3-month decline of 11.4% shows the stock can move violently on news

- ⚠️ Trading below major averages: Currently below key moving averages after breaking down from the November highs

The chart tells the story: NOW had an incredible AI-driven run to $1,000+, but the massive $7B Armis acquisition spooked investors who worry about capital allocation and dilution. The stock has consolidated in the $750-800 range, searching for a floor ahead of the stock split catalyst.

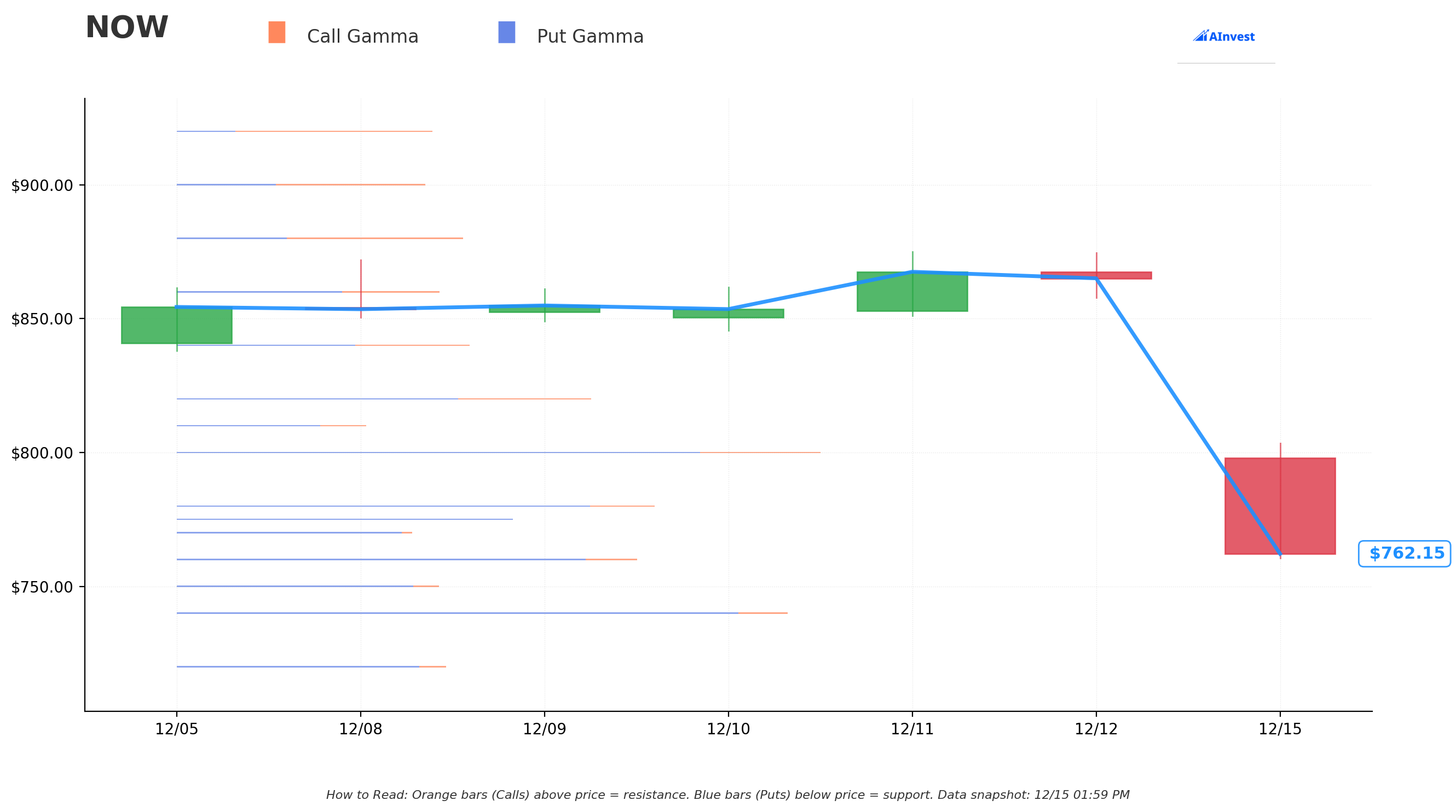

Gamma-Based Support & Resistance Analysis

Current Price: $762.18

The gamma exposure map reveals critical price magnets and barriers governing near-term action:

🔵 Support Levels (Put Gamma Below Price):

- $760 - Immediate support with 0.69B total gamma exposure (STRONGEST nearby floor - sitting right here!)

- $740 - Secondary support at 0.91B gamma (2.9% below current - major structural level)

- $720 - Deep support at 0.40B gamma (5.5% below - exactly where the long call strike sits!)

- $700 - Extended floor with 0.66B gamma (8.2% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $775 - Immediate ceiling with 0.51B gamma (1.7% overhead)

- $780 - Secondary resistance at 0.72B gamma (2.3% above - near-term barrier)

- $800 - Major ceiling zone with 0.96B gamma (5.0% rally required - psychological level)

- $820 - Significant resistance at 0.61B gamma (7.6% above - EXACTLY the short call strike!)

- $840 - Extended resistance at 0.43B gamma (10.2% above)

- $880 - Major ceiling at 0.42B gamma (15.5% above)

What this means for traders:

NOW is sitting RIGHT ON major $760 support (0.69B gamma) after the recent pullback from November highs. The stock faces a gauntlet of resistance overhead at $775, $780, and especially $800 (nearly 1B gamma) - these levels will be tough to break through without major positive catalysts.

Notice the pattern? The spread trader struck at $720 (support) and $820 (resistance) - hitting EXACTLY where gamma shows natural price floors and ceilings. This wasn't random - they positioned around key structural levels that options positioning creates.

Net GEX Bias: Bearish (4.52B call gamma vs 9.21B put gamma) - Overall positioning skews defensive with nearly 2:1 put to call gamma ratio. This suggests market makers are positioned for downside protection, creating natural support but also implying bearish sentiment.

The current $760 support is CRITICAL - hold this and we could bounce back toward $800. Break below and the next stop is $740, then $720 (where serious institutional buyers likely wait).

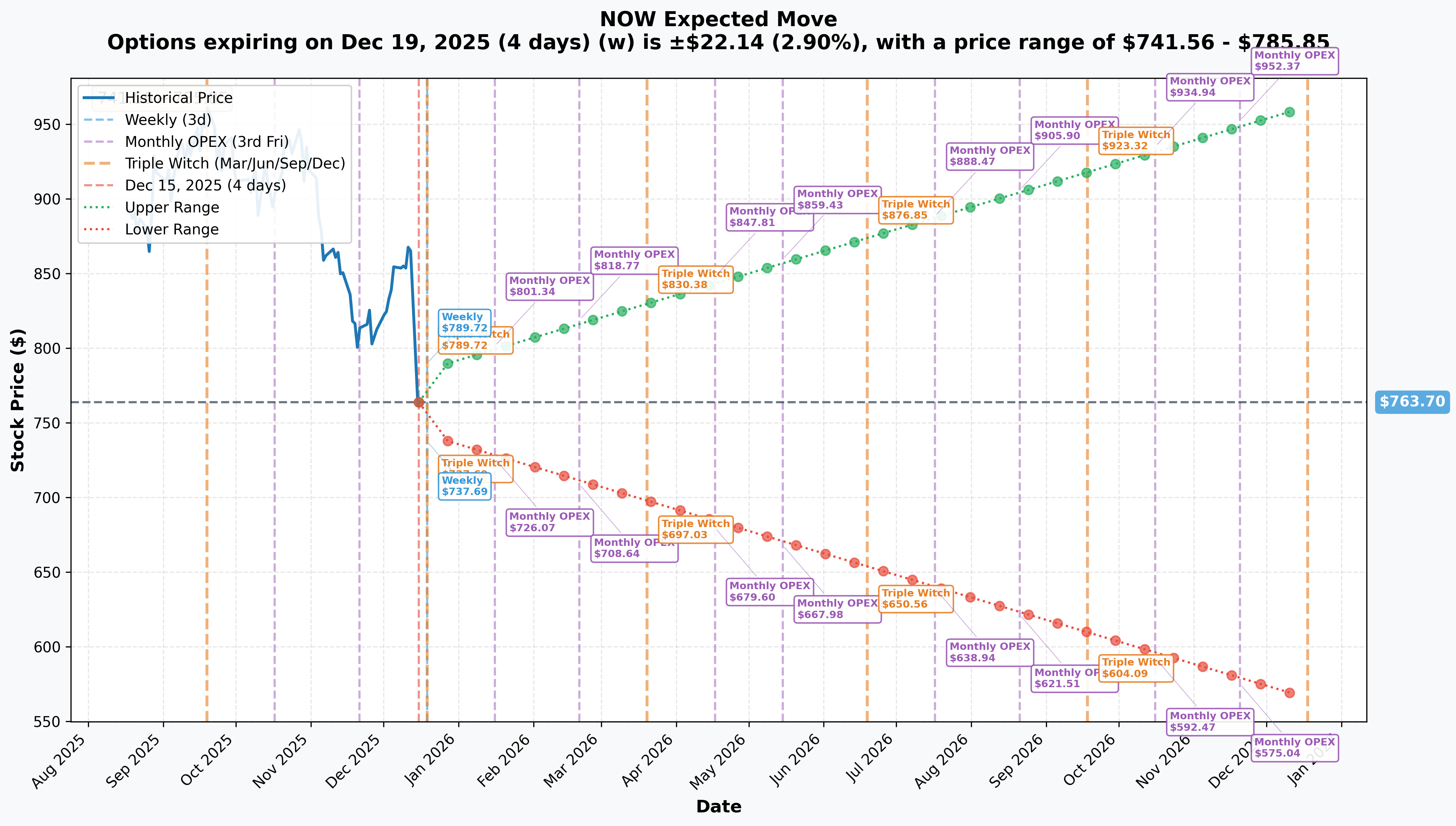

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 4 days - SPLIT DAY!): ±$22.14 (±2.9%) → Range: $741.56 - $785.85

- 📅 Monthly OPEX (Jan 16 - 32 days): ±$37.63 (±4.9%) → Range: $726.07 - $801.34

- 📅 Quarterly Triple Witch (Mar 20 - 95 days): ±$67.03 (±8.8%) → Range: $697.03 - $830.38

- 📅 Yearly LEAPS (Dec 18 2026 - 368 days - THIS TRADE!): ±$198.35 (±26.0%) → Range: $565.36 - $962.05

Translation for regular folks:

The market expects 2.9% volatility ($22) by this Friday which captures the 5-for-1 stock split on December 18! That's actually MODEST implied volatility for such a major corporate action - suggesting the street thinks the split will be a non-event technically.

But look at the YEARLY LEAPS range: $565 to $962 - the market thinks NOW could trade ANYWHERE in a 70% range over the next year! This massive uncertainty reflects:

- Armis acquisition integration risk ($7B is HUGE)

- AI product monetization questions (Now Assist scaling)

- Microsoft competitive threat in 2026

- Q4 earnings execution (Jan 28)

- Macro enterprise IT spending uncertainty

Key insight: The spread trader's $820 short strike falls WITHIN the yearly implied range ($962 upper bound), meaning it was achievable but not guaranteed. By closing now at $779, they're taking the bird in hand rather than risking the stock stalls below $820 and the spread loses value.

🎪 Catalysts

🔥 Immediate Catalysts (Next 7 Days)

5-for-1 Stock Split - December 18, 2025 (3 DAYS AWAY!) 📊

Shareholders approved the split on December 5, 2025, with critical dates:

- 📅 Record Date: December 16, 2025 (TOMORROW!)

- 📅 Distribution Date: December 17, 2025 (after market close)

- 📅 Trading Begins: December 18, 2025 on split-adjusted basis

- 💰 Post-split price: ~$156 per share (from current ~$779)

- 📈 Option impact: All strikes divide by 5 ($820 becomes $164, $720 becomes $144)

Expected Impact:

- 🎯 Increased retail investor accessibility at ~$156 price point vs $779

- 📊 Improved options liquidity with more strike granularity

- 🔄 Potential S&P 500 index rebalancing flows

- 📈 Historical precedent: Tech stock splits often catalyze 5-10% rallies in following months (Nvidia, Tesla examples)

Why the spread trader closed before split: Options contracts adjust mechanically (5x contracts at 1/5th strikes), but it's cleaner to exit beforehand to avoid confusion and potential liquidity fragmentation in the immediate post-split period.

🚀 Near-Term Catalysts (Q4 2025 - Q1 2026)

Armis Security Acquisition - Expected Closure "Within Days" 🤝

ServiceNow in advanced talks to acquire cybersecurity startup Armis for up to $7 billion, potentially the company's largest acquisition ever:

- 💰 Deal Size: $7 billion (2.5x larger than previous record $2.85B Moveworks deal)

- 📊 Armis Metrics: $300M ARR (50% YoY growth from $200M), 40%+ of Fortune 100 as customers

- 🎯 Strategic Entry: Cybersecurity asset and information management market

- ⚠️ Market Reaction: Stock dropped 11.42% on acquisition announcement due to valuation concerns

- ⏰ Timeline: Deal expected to close "within days" per Bloomberg report

Why this matters for the spread trade:

The Armis acquisition represents a MASSIVE capital allocation decision - $7B is 3.9% of NOW's market cap! While strategically logical (expanding beyond core ITSM into cybersecurity), investors worry about:

- Dilution risk: Likely cash + stock deal could pressure EPS

- Integration complexity: Cybersecurity is adjacent but different from workflow automation

- Overpay concerns: $7B for $300M ARR = 23x revenue multiple (extremely rich)

- Execution risk: Largest acquisition ever - can NOW successfully integrate?

The spread trader may be closing BECAUSE of this uncertainty - why hold a capped-upside position when a megadeal could create volatility in either direction?

Q4 2025 Earnings Report - January 28, 2026 (44 Days) 📊

ServiceNow reports fiscal Q4 results on January 28, 2026 after market close. This will be THE catalyst to validate the AI-driven growth story:

Q4 2025 Guidance:

- 📊 Subscription Revenue: $3.42-$3.43 billion

- 📈 cRPO Growth: 23% YoY

- 💰 Non-GAAP Operating Margin: 30%

Full-Year 2025 Guidance:

- 📊 Subscription Revenue: $12.84-$12.85 billion (20% YoY growth)

- 💰 Operating Margin: 31%

- 💸 Free Cash Flow Margin: 34%

Key Metrics to Watch:

- 🤖 Now Assist ACV: Progress toward $1 billion 2026 target (exceeded $500M in Q3)

- 🏢 Enterprise deals: Number of >$1M ACV customer adds

- 🇺🇸 Federal contracts: Momentum from $432M Army contract and $250M HHS deal

- 📈 2026 Guidance: Critical to see if Armis contribution is included

- 🎯 Margin trajectory: Can NOW maintain 31%+ operating margins while integrating Armis?

Upside scenario: Beat and raise with Now Assist crushing $500M run-rate, strong federal wins, 2026 guidance $14B+ including Armis synergies → Stock to $850-900

Downside scenario: In-line quarter but conservative 2026 guidance citing Armis integration costs, Microsoft competitive pressure, slower IT hiring → Stock to $700-720

⚠️ Risk Catalysts (Negative)

KeyBanc Downgrade - Competitive Threat Warning 🚨

KeyBanc downgraded NOW from Sector Weight to Underweight on December 13, 2025 with $775 price target (10% downside):

Analyst Jackson Ader's Concerns:

- 🤖 Microsoft Competition: Copilot ecosystem expected to challenge ServiceNow's AI orchestration lead in 2026

- 📉 IT Hiring Slowdown: Back-office IT hiring is slowing and demand hasn't bottomed yet

- ⚠️ SaaS Model Pressure: AI tools may reduce need for traditional human-operated workflow software

- 💰 Valuation: Stock fell ~3% on downgrade

Why this matters: This is the FIRST major sell-side downgrade in months, breaking bullish consensus. Coming just days after Armis announcement, it suggests mounting concerns about NOW's growth algorithm and competitive positioning.

Microsoft Competitive Dynamics:

While ServiceNow and Microsoft announced a partnership at Knowledge 2024, the two companies increasingly compete:

- 💻 Dynamics 365: Microsoft's workflow automation competing in same markets

- 🤖 Copilot bundling: Microsoft can bundle Copilot with Office 365 - powerful distribution advantage

- 🎯 Enterprise lock-in: Customers already on Microsoft stack may consolidate rather than use NOW

- ⚖️ Coopetition risk: Partnership could shift from collaborative to competitive in 2026

AI Cannibalization Risk:

KeyBanc raises existential question: Do AI agents COMPLEMENT traditional SaaS or REPLACE it?

- 🤖 If AI agents can handle workflows autonomously, do enterprises need human-operated platforms?

- 📉 Risk that NOW's own AI products (Now Assist) cannibalize core platform revenue

- 💰 Pricing power questions: Will AI features become table stakes vs premium offerings?

📊 Positive Catalysts (Longer-Term)

AI Product Momentum - Now Assist on Track for $1B ACV 🚀

NOW's AI platform showing explosive growth:

- 💰 Now Assist exceeded $500M ACV in Q3 2025, firmly on track for $1B by 2026

- 📈 CFO: "Now Assist continued to surpass net new ACV expectations, fueled by increase in both deal volume and size quarter-over-quarter"

- 🤖 AI agents for ITSM and CSM entered limited release November 2024, broader rollout through 2025

- 🎯 44 customers contributed >$1M ACV from Now Assist in Q3, with 6 deals >$5M and 2 >$10M

Xanadu Platform Launch:

- 🚀 ServiceNow launched Xanadu featuring integrated AI Agents for 24/7 productivity

- 💾 RaptorDB Pro provides ultra-scale performance for complex enterprise data

- 📊 Expanding use cases: IT, customer service, procurement, HR, software development

Federal Government Contracts - De-Risk Revenue Base 🇺🇸

NOW building substantial federal presence:

- 🏛️ 5-year, $250M blanket purchase agreement with HHS for digital workflow platforms

- 🎖️ Carahsoft awarded $432M Army procurement contract for ServiceNow products

- 🔒 FedRAMP certified - cleared for government use

- 🎯 Strategic national security positioning reduces commercial concentration risk

Enterprise Deal Flow Accelerating:

Q3 2025 showed continued strength:

- 📊 Closed 96 deals with net new ACV >$1M (14% YoY increase)

- 💰 15 deals exceeded $5M ACV

- 🚀 6 deals surpassed $10M ACV

- 📈 2,109 customers with >$1M ACV (12% YoY growth)

- 💎 Nearly 500 customers with >$5M ACV (21% YoY growth)

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst calendar, here are scenarios through January 28 earnings (44 days out):

📈 Bull Case (30% probability)

Target: $850-900

How we get there:

- 🎪 Stock split pop: 5-for-1 split catalyzes 5-8% rally as retail floods in at ~$156 price point

- 💎 Armis deal praised: Market reassesses acquisition as strategic masterstroke, cybersecurity synergies clear

- 🤖 Now Assist momentum: Q4 earnings reveal Now Assist hit $600M+ ACV run-rate, ahead of $1B 2026 target

- 📊 Beat and raise: Q4 revenue $3.5B+ (above $3.42-3.43B guide), 2026 guidance $14B+ including Armis

- 🏢 Federal wins: Additional major government contracts announced, reducing commercial dependency

- 📈 Margin expansion: Operating margins hold 31%+ despite Armis integration, proving operational leverage

- 🚀 Breakout: Clear $800 gamma resistance (0.96B), momentum to $820-850 range

Key metrics needed:

- Subscription revenue growth sustains 20%+ into 2026

- Now Assist customer count doubles Q/Q

- Gross margins >79% maintained

- Federal revenue becomes 15%+ of mix

Probability assessment: Only 30% because requires PERFECT execution on multiple fronts while overcoming serious headwinds (KeyBanc downgrade, Armis dilution concerns, Microsoft competition). Stock already priced for strong execution at current levels.

🎯 Base Case (50% probability)

Target: $740-800 range (CONSOLIDATION)

Most likely scenario:

- ✅ Split non-event: 5-for-1 split executes smoothly, minimal technical impact on price action

- 🤝 Armis closes quietly: Deal completes, integration begins, takes 6-12 months to assess success/failure

- 📱 Solid earnings: Q4 meets guidance ($3.42-3.43B subscription revenue), margins in-line at 30%

- ⚖️ Conservative 2026 guide: Management guides cautiously citing Armis integration, macro uncertainty

- 🤖 AI growth continues: Now Assist solid but not spectacular, steady $1B trajectory maintained

- 🔄 Range-bound: Trading between $740 support (0.91B gamma) and $800 resistance (0.96B gamma)

- 💤 Digest gains: Market waits for Armis integration proof points and 2026 AI monetization data

This is the spread trader's outcome:

They already captured $51.90 per contract (52% of max $100 spread value) by closing at current levels. In this scenario, the stock would have stayed in $750-820 range through 2026 expiration, and they'd have collected maybe $60-70 total spread value (60-70% of max). By exiting now, they:

- Lock in the bulk of gains (52%)

- Avoid 368 days of theta decay and event risk

- Free up capital for other opportunities

- Avoid split complications

Why 50% probability: Stock at technical inflection - neither breaking out nor down. Fundamentals solid (21% growth, 31% margins, strong AI traction) but valuation rich (17x forward revenue). Most institutions will hold and wait for Q4/2026 catalysts.

📉 Bear Case (20% probability)

Target: $680-720 (TEST THE LONG CALL STRIKE!)

What could go wrong:

- 😰 Earnings disappointment: Q4 misses or guides conservatively - even small miss triggers -10-15% gap at this valuation

- 🚨 Armis buyer's remorse: Integration challenges emerge, customer churn, or revenue synergies overstated

- ⏰ Now Assist slowdown: AI product growth decelerates, pricing pressure emerges, customers wait for Microsoft Copilot

- 💸 Margin compression: Armis integration costs pressure operating margins below 30%, breaking multi-year expansion trend

- 🤖 Microsoft threat materializes: Copilot ecosystem gains traction faster than expected, NOW loses competitive deals

- 📉 Macro headwinds: Enterprise IT spending cuts accelerate, elongated sales cycles impact bookings

- 🔨 Break below $740: Gamma support fails, cascade to $720 (the spread's long call strike!), then $700

Critical support levels:

- 🛡️ $760: Current level - must hold or technical damage accelerates

- 🛡️ $740: Major gamma floor (0.91B) - critical bounce zone

- 🛡️ $720: Deep support (0.40B gamma) + spread's LONG CALL STRIKE - major institutional positioning here

- 🛡️ $700: Extended floor (0.66B gamma) - disaster scenario

Probability assessment: Only 20% because NOW's fundamentals remain strong (21% growth, industry-leading 79% gross margins, $11.35B cRPO backlog). Would require multiple negative catalysts to align. However, KeyBanc downgrade and Armis concerns show cracks are forming.

Why the spread trader closed here:

If the bear case plays out and stock drops to $720 by December 2026:

- Original spread value: $720 calls worth $0 (at-the-money), $820 calls worthless = $0 total value

- By closing at $779: Captured $51.90 per contract instead of $0 (saved 100% loss!)

By derisking NOW before potential downside catalysts (earnings miss, Armis issues, Microsoft competition), they protected significant capital.

💡 Trading Ideas

🛡️ Conservative: Wait for Post-Split Clarity

Play: Stay on sidelines through December 18 split and January 28 earnings

Why this works:

- 🎪 Split complexity: Options adjust mechanically but can create short-term liquidity fragmentation

- ⏰ Earnings in 44 days: Binary event risk with ±4.9% implied move - too dangerous without defined edge

- 💰 Armis uncertainty: $7B acquisition creates unknowable integration risk over next 6-12 months

- 📊 KeyBanc concern: First major sell-side downgrade suggests mounting competitive/execution risks

- 🎯 Better entries ahead: Post-earnings pullback to $720-740 would offer 10-15% margin of safety

- 🤔 Smart money exiting: $7.6M spread close signals institutions are DERISKING - why fight the tape?

Action plan:

- 👀 Watch December 18 split for any technical abnormalities or retail buying surge

- 🎯 Monitor January 28 earnings closely for subscription revenue ($3.42B+ needed), Now Assist traction, 2026 guidance quality

- ✅ Look for pullback to $720-740 gamma support post-earnings for stock entry

- 📊 Need to see Armis integration roadmap and Microsoft competitive positioning before committing capital

- ⏰ Revisit in Q1 2026 when Armis metrics start flowing and Now Assist $1B target visibility improves

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -15-20% drawdown if earnings/Armis disappoint. Get better entry if consolidation continues. Maintain optionality for clearer risk/reward setup.

⚖️ Balanced: Post-Earnings Bull Put Spread

Play: After Q4 earnings volatility settles, sell bull put spread targeting gamma support

Structure: Sell $740 puts, Buy $720 puts (February 20 expiration - 23 days post-earnings)

Why this works:

- 🎢 IV crush: Earnings volatility collapse makes put spreads much cheaper - sell AFTER IV drops from current 26% to ~18-20%

- 📊 Defined risk: $20 wide spread = $2,000 max risk per spread

- 🎯 Targets gamma support: $720-740 zone where 1.31B combined gamma sits - strong institutional floor

- 🤝 Bullish but cautious: Collecting premium while defining risk if thesis breaks

- ⏰ 23 days post-earnings: Gives time for Armis integration clarity and Now Assist Q4 data to digest

- 🛡️ Aligns with long call: Mirrors institutional positioning at $720 support level

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Collect: ~$6-8 credit per spread (30-40% of width)

- 📈 Max profit: $600-800 if NOW above $740 at Feb 20 expiration (keep entire credit)

- 📉 Max loss: $1,200-1,400 if NOW below $720 (width minus credit)

- 🎯 Breakeven: ~$732-734

- 📊 Probability of profit: ~65-70% (selling puts below current $762 with gamma support)

Entry timing:

- ⏰ Wait 3-5 days post-earnings (by Feb 1-3) for full IV collapse

- 🎯 Only enter if stock above $750 (gives 10+ point cushion)

- ❌ Skip if stock already below $740 (too close to short strike)

- ✅ Best case: Earnings beat, stock rallies to $780-800, THEN sell this spread

Position sizing: Risk only 3-5% of portfolio (defined-risk income strategy with directional bias)

Management rules:

- 📈 Take profit: Close at 50% max profit ($3-4 credit) if hit early

- ⏰ Time stop: Exit at 7 days to expiration regardless to avoid gamma risk

- 📉 Loss limit: Cut at 100% loss ($20 spread goes to $18-19 debit) - don't hope

Risk level: Moderate (defined risk, neutral-to-bullish) | Skill level: Intermediate

🚀 Aggressive: Calendar Spread on Split Date (ADVANCED!)

Play: Exploit split-induced volatility and IV crush with calendar spread

Structure: Sell Dec 19 $780 calls, Buy Jan 16 $780 calls

Why this could work:

- 🎪 Split volatility play: Dec 19 expiration captures split (Dec 18), Jan 16 is 28 days later

- ⏰ Theta advantage: Dec 19 calls decay MUCH faster than Jan 16 calls (sell expensive near-term, buy cheaper longer-term)

- 📊 IV differential: Front-week IV likely elevated due to split uncertainty, back-month more normal

- 🎯 Sweet spot: Profits if stock stays near $780 through Dec 19 (time decay), then can rally into earnings for Jan calls

- 💰 Defined risk: Can only lose net debit paid (typically $8-12 per calendar)

- 🚀 Earnings optionality: Jan 16 long calls still alive for earnings on Jan 28 (if split goes well, hold for earnings run)

Why this could blow up (SERIOUS RISKS):

- 💸 Split gap risk: Stock could gap violently post-split (up or down), blowing through $780 and calendar loses

- ⏰ Directional exposure: Calendars profit from stagnation, not movement - wrong structure if stock trends hard

- 😱 Liquidity concerns: Post-split options may have wider spreads, harder to exit calendar cleanly

- 📊 Earnings proximity: Jan 28 earnings could inflate Jan 16 IV, making calendar more expensive to close

- ⚠️ Advanced Greeks: Requires understanding Vega, Theta interactions - not beginner-friendly

Estimated P&L:

- 💰 Cost: ~$8-12 debit per calendar

- 📈 Max profit: $15-20 if stock pins $780 at Dec 19 expiration (sell Dec calls at max value, Jan calls hold value)

- 🚀 Bonus scenario: Stock rallies to $820-850 post-split, Jan calls gain $40-70 in intrinsic (close calendar, ride Jan calls naked)

- 📉 Max loss: $8-12 (entire debit) if stock moves violently away from $780 in either direction

- 💀 Worst case: Stock crashes to $700 or moons to $900 - both legs worthless or equal value

Breakeven points:

- 🎯 Ideal scenario: Stock $775-785 at Dec 19 expiration

- 📈 Acceptable: Stock $760-800 range

- 📉 Danger zone: Stock <$740 or >$820

CRITICAL WARNINGS - DO NOT attempt unless:

- ✅ You understand calendar spread mechanics (long Vega, long Theta, Gamma-neutral)

- ✅ You can monitor daily and adjust if thesis breaks

- ✅ You're comfortable with split-adjusted options (Dec 19 adjusts to 5x $156 calls, Jan 16 adjusts same)

- ✅ You have plan to manage Jan 16 long calls post-Dec 19 expiration

- ✅ You accept that split could create total loss scenario

- ⏰ You commit to closing calendar by Dec 19 expiration (don't let Dec expire naked short)

Entry timing:

- 📅 Enter December 16-17 (1-2 days before split) when front-week IV likely peaks

- 🎯 Only if implied volatility on Dec 19 expiration >30% (need elevated near-term IV for edge)

- ❌ Skip if calendar costs >$12 (not enough edge)

Position sizing: Risk only 1-2% of portfolio (this is a SPECULATIVE volatility trade)

Management plan:

- 📊 If stock breaks above $800 or below $760 by Dec 17: Close entire calendar immediately (thesis broken)

- ✅ If stock near $780 at Dec 18-19: Let Dec calls expire, hold Jan calls for earnings run

- 🚀 If stock rallies hard post-split ($820+): Close Dec short, ride Jan long calls naked with trailing stop

Risk level: EXTREME (split + earnings binary events) | Skill level: Advanced only

Probability of profit: ~45% (lower than implied due to split unpredictability and directional risk)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎪 Stock split complexity (3 DAYS!): 5-for-1 split on December 18 creates mechanical adjustments to options (strikes divide by 5, contracts multiply by 5). While theoretically neutral, splits can create short-term volatility, liquidity fragmentation, and retail speculation. Historical precedent mixed - sometimes catalyze rallies (NVDA, TSLA), sometimes non-events. Options traders face execution risk in immediate post-split period.

-

💸 Armis acquisition - MASSIVE capital commitment: $7 billion deal is 3.9% of market cap and 2.5x larger than any previous NOW acquisition. Stock dropped 11.42% on announcement signaling investor concerns. Risks include: integration complexity (cybersecurity different from ITSM), customer churn, overpay at 23x revenue, dilution from likely cash+stock structure. Takes 6-12 months minimum to assess success/failure.

-

⏰ Q4 earnings binary event (44 days): Results January 28, 2026 after close create volatility risk. Consensus $3.42-3.43B subscription revenue sets high bar. Key watch points: Now Assist ACV trajectory, 2026 guidance including Armis, operating margin sustainability, federal contract momentum. Implied move ±4.9% ($38) but actual moves could exceed if Armis integration roadmap disappoints or Microsoft competition addressed.

-

🚨 KeyBanc downgrade signals shifting sentiment: First major sell-side bearish call breaks bullish consensus (30 analysts, was all Buy/Strong Buy). Analyst Jackson Ader cites: Microsoft Copilot threat in 2026, slowing IT hiring, AI cannibalization of traditional SaaS. $775 target implies 10% downside from current $779. Could be early warning of broader re-rating.

-

🤖 Microsoft competitive threat emerging: While partnership exists, Dynamics 365 + Copilot ecosystem increasingly competes in workflow automation. Microsoft's bundling power with Office 365 (hundreds of millions of seats) creates distribution advantage NOW can't match. Risk of customers consolidating on Microsoft stack rather than multi-vendor approach. 2026 could be inflection point as Copilot capabilities mature.

-

📉 IT spending slowdown: KeyBanc warns IT back-office hiring is slowing and "demand for new workers has yet to bottom." ServiceNow's growth tied to enterprise IT expansion - if companies cut IT budgets in 2026 recession scenario, even strong products face headwinds. Sales cycles elongate, deal sizes shrink, churn risk rises. Federal contracts help but don't eliminate commercial dependency.

-

💰 Valuation offers zero margin of error: At ~17x forward revenue and 74.8x forward P/E, stock is priced for PERFECT execution. Requires sustaining 20%+ growth, expanding margins, and successful Armis integration. Any stumble (earnings miss, margin compression, AI slowdown) and stock could re-rate 20-30% lower to $600-650 range. Historical NOW volatility shows 15-20% corrections are normal even in bull markets.

-

🏦 Smart money derisking at peak: The $7.6M LEAPS spread close signals institutional caution. When sophisticated players exit capped-upside positions 368 days early (before split, before Armis close, before earnings), it reflects concern about downside scenarios. This wasn't forced liquidation - this was ACTIVE derisking. The Z-scores (5.19 and 4.27) show this happens maybe a few times per year - extremely unusual size.

-

🎢 Gamma resistance overhead: $800 strike has 0.96B total gamma (nearly 1 billion!), creating natural ceiling. Market makers will systematically SELL into rallies above $780-800 to hedge their exposure. Breakout requires sustained institutional buying to overcome. Current positioning at $762 sitting well below this resistance zone - path of least resistance may be sideways-to-down until major catalyst.

-

📊 Now Assist monetization uncertainty: While $500M ACV in Q3 sounds impressive, questions remain: Is this sustainable? Will pricing compress as AI becomes table stakes? Are customers just kicking tires or committed long-term? $1B by 2026 requires doubling in 12 months - achievable but not guaranteed. Any deceleration would crush valuation thesis.

-

🌍 Macro headwinds: Enterprise software highly cyclical. If recession emerges in 2026, NOW won't be immune. Digital transformation budgets get cut, renewals pressured, new logo acquisition slows. Federal contracts help but represent <15% of revenue. At 17x revenue, stock has ZERO recession protection built in.

-

🔐 Cybersecurity liability post-Armis: Acquiring Armis brings NOW into cybersecurity product liability - if Armis product fails and customer breached, NOW now owns that risk. Different risk profile than workflow automation software. Regulatory scrutiny increasing on cybersecurity vendors post-high-profile breaches.

🎯 The Bottom Line

Real talk: Someone just walked away from a $7.6 MILLION LEAPS bull call spread position on ServiceNow with 368 days remaining until expiration. This isn't a bearish bet - this is sophisticated profit-taking by institutions who've ridden NOW higher and are now managing risk ahead of multiple binary catalysts (stock split, Armis close, Q4 earnings).

What this trade tells us:

- 🎯 Locking in gains: By closing at $779 with spread worth $51.90, they captured 52% of maximum potential profit ($100 spread width) - bird in hand vs 368 days of uncertainty

- ⚖️ Timing is everything: Exiting 3 days before split avoids options adjustment complexity and liquidity concerns

- 💰 Armis uncertainty: $7B acquisition creates unknowable integration risk - why hold capped-upside position through that?

- 📊 KeyBanc warning heeded: First major sell-side downgrade (Underweight, $775 target) suggests mounting competitive/execution risks

- ⏰ Earnings risk: Q4 results Jan 28 could move stock 10-15% either direction - spread already captured most value, why risk it?

This is NOT a "sell everything" signal - it's a "take profits and manage risk intelligently" signal.

If you own NOW:

- ✅ Consider trimming 20-30% at $760-780 levels (lock in gains, reduce concentration risk)

- 🛡️ If holding through catalysts, set mental stop at $740 (major gamma support)

- 📊 Don't get greedy - stock up from $600s to $1000+ in past year, protecting capital is smart

- 🎯 If earnings beat AND Armis praised, can re-enter trimmed shares on momentum break above $820

- ⏰ Split on Dec 18 is technical event - don't over-trade it, focus on fundamentals

If you're watching from sidelines:

- ⏰ Wait for post-split clarity (Dec 18) and post-earnings volatility (Jan 28) before entering

- 🎯 Ideal entry: Pullback to $720-740 (gamma support + spread's long call strike) on any Armis integration concerns

- 📈 Looking for confirmation of: Now Assist sustaining $500M+ quarterly ACV adds, 2026 revenue guide $14B+, operating margins holding 30%+, Armis revenue synergies visible

- 🚀 Longer-term (6-12 months), AI monetization and federal contract expansion are legitimate bull catalysts

- ⚠️ Current $762 lacks attractive risk/reward - need 10-15% margin of safety given execution risks

If you're bearish:

- 🎯 Don't fight the fundamentals - NOW still growing 21%, 79% gross margins, industry leader

- 📊 Wait for technical breakdown below $740 before initiating shorts

- ⏰ Post-earnings put spreads (Feb expiration) offer defined-risk way to play downside if Q4 disappoints

- ⚠️ KeyBanc $775 target only 2% below current - not enough edge for aggressive short positioning

Mark your calendar - Key dates:

- 📅 December 16 (Monday) - Stock split record date

- 📅 December 18 (Wednesday) - 5-for-1 stock split effective, trading begins on split-adjusted basis

- 📅 December 19 (Thursday) - Weekly/Monthly/Quarterly OPEX (triple witch!) - ±2.9% implied move

- 📅 Late December 2025 - Armis acquisition expected to close

- 📅 January 16, 2026 - Monthly OPEX

- 📅 January 28, 2026 (Tuesday after close) - Q4 FY2025 earnings report - THE CATALYST

- 📅 January 29, 2026 - Post-earnings price action and analyst reactions

Final verdict:

ServiceNow's long-term story remains compelling - AI-powered Now Assist on track for $1B ACV by 2026, growing federal presence, industry-leading margins, and expanding TAM beyond ITSM into workflow automation across all enterprise functions. The Armis acquisition is strategically logical (cybersecurity complements workflow security), but execution risk is REAL at $7B price tag.

BUT, at $762 with KeyBanc downgrade fresh, stock split in 3 days, Armis integration uncertainty, and earnings in 44 days, the risk/reward is NOT favorable for aggressive new positioning. The $7.6M institutional spread close is a CLEAR signal: smart money is taking profits at $779, not adding exposure.

Be patient. Let the split clear. Watch Armis integration updates. Wait for earnings. The SaaS revolution will still be here in 2-3 months, and you'll sleep better paying $730 instead of $779.

This is a marathon, not a sprint. Protect your capital, wait for better entries, and let catalysts resolve before committing. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The "extremely unusual" classification reflects this specific trade's size relative to recent NOW history - it does not imply the trade will be profitable or that you should follow it. Stock splits create mechanical adjustments to options contracts which may affect liquidity and pricing. Earnings create binary event risk with potential for 10-15% moves either direction. The spread trader may have complex portfolio hedging needs or tax considerations not applicable to retail traders. Always do your own research and consider consulting a licensed financial advisor before trading.

About ServiceNow, Inc.: ServiceNow Inc provides software solutions to structure and automate various business processes via a SaaS delivery model, specializing in IT service management, workflow automation, and AI-powered enterprise applications, with a market cap of $179.48 billion in the Prepackaged Software industry.