🏦 NU $41.1M Complex Multi-Leg Strategy - Smart Money Building Advanced Position! 🎯

📅 January 5, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed a $41.1 MILLION sophisticated multi-leg options strategy on NU Holdings (Nubank) this morning at 10:32:17! This institutional player executed FIVE simultaneous trades creating a complex position that combines long-term downside protection, near-term bullish exposure, and premium collection. With NU up +52.65% over the past year at $17.91 and trading near all-time highs ($17.84), smart money is building a nuanced position ahead of Q4 2025 earnings on February 25th and Mexico's banking license activation expected in Q1-Q2 2026. Translation: This isn't a simple bet - it's an architectural position designed for multiple scenarios!

📊 Company Overview

Nu Holdings Ltd (NU) is Latin America's leading digital banking platform revolutionizing financial services across the region:

- Market Cap: $82.47 Billion (largest digital bank in Latin America)

- Industry: Digital Banking & Financial Services

- Current Price: $17.91 (near all-time high of $17.84 hit December 2, 2025)

- Primary Business: Digital banking services including credit cards, personal accounts, investments, personal loans, insurance, mobile payments, business accounts, and rewards across Brazil (110M customers), Mexico (13M), and Colombia (4M)

💰 The Option Flow Breakdown

The Complete Tape (January 5, 2026 @ 10:32:17):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Strategy | Z_Score | Volume_Signal |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-05 | 10:32:17 | NU | BUY | PUT $13 | 2028-01-21 | $13.00 | 50,000 | $6.8M | BTO | Long-Dated Protective Put (LEAP) | 8,278.17 | OPEN |

| 2026-01-05 | 10:32:17 | NU | BUY | CALL $19 | 2026-04-17 | $19.00 | 50,000 | $4.3M | BTO | Long Call | 75.65 | OPEN |

| 2026-01-05 | 10:32:17 | NU | SELL | PUT $14 | 2026-04-17 | $14.00 | 50,000 | $1.1M | STO | Short Put (Cash Secured) | 234.01 | OPEN |

| 2026-01-05 | 10:32:17 | NU | BUY | CALL $12 | 2026-01-16 | $12.00 | 50,000 | $29.0M | BTO | Bull Call Spread (Long Leg) | 78.14 | OPEN |

| 2026-01-05 | 10:32:17 | NU | SELL | CALL $17 | 2026-01-16 | $17.00 | 26,000 | $1.9M | STO | Bull Call Spread (Short Leg) | 16.88 | OPEN |

Total Premium: $41.1 MILLION ($6.8M + $4.3M + $1.1M + $29.0M + $1.9M)

🤓 What This Actually Means - The Strategy Decoded

This is NOT a simple directional bet! This sophisticated trader constructed a multi-layered position across THREE different expirations with FIVE legs working together. Let me break down what's really happening here:

🛡️ Layer 1: Long-Term Insurance (2-Year LEAP Puts)

- 💸 Leg 1: Bought 50,000 Jan 2028 $13 puts for $6.8M

- ⏰ Time horizon: 751 days (2+ years of protection!)

- 🎯 Protection level: $13 strike is 27.4% below current price ($17.91)

- 📊 Purpose: Deep, long-term catastrophe insurance protecting against Brazilian macro crisis, regulatory disaster, or FinTech sector collapse

- 💰 Cost: $1.36 per share for 2 years of protection (7.6% annual premium)

This is the foundation - smart money saying "I'm bullish on NU's growth story, BUT I need protection against tail risks over the next 2 years as they execute Mexico expansion and U.S. charter application."

🚀 Layer 2: Medium-Term Bullish Play (April 2026)

- 💸 Leg 2: Bought 50,000 Apr 2026 $19 calls for $4.3M

- 💸 Leg 3: SOLD 50,000 Apr 2026 $14 puts collecting $1.1M

- ⏰ Time horizon: 102 days (captures Q4 earnings Feb 25 + Mexico bank activation)

- 🎯 Net cost: $3.2M ($4.3M - $1.1M = $0.064 per share net debit)

- 📈 Bullish bet: Expects NU above $19.06 by April (6.4% upside from current levels)

- 🛡️ Downside obligation: If NU drops below $14, must buy stock at $14 (willing to own at 21.8% discount!)

This layer is tactical - positioned for Mexico banking license activation catalyst in Q1-Q2 2026 driving stock toward $19-20. The short $14 puts show they're HAPPY to own NU at $14 if pullback occurs (brilliant use of cash-secured puts to collect premium while setting buy limit).

⚡ Layer 3: Near-Term Income Generator (January 2026 - 11 DAYS!)

- 💸 Leg 4: Bought 50,000 Jan 16 $12 calls for $29.0M (MASSIVE position!)

- 💸 Leg 5: SOLD 26,000 Jan 16 $17 calls collecting $1.9M

- ⏰ Time horizon: 11 days (expires Jan 16)

- 🎯 Net cost: $27.1M for deep in-the-money calls ($29M - $1.9M)

- 📊 Purpose: This is essentially a synthetic long stock position using options leverage

- 💰 Delta exposure: The $12 calls are deep ITM (delta ~0.99), so this behaves like owning 5M shares while capping upside at $17 on half the position

Wait, there's something UNUSUAL here: They bought 50,000 of the $12 calls but only sold 26,000 of the $17 calls. This creates asymmetric exposure - if NU stays below $17, they keep full upside on 24,000 contracts (representing 2.4M shares of leveraged exposure). If NU rallies above $17, they cap gains on only half the position while the other half continues participating.

🔥 The COMPLETE Strategy Picture

When you combine all five legs, here's what this trader has constructed:

NET POSITION ANALYSIS:

- 💰 Total capital deployed: ~$41.1M in premiums paid/collected

- 🎯 Effective leverage: Controlling 5M+ shares worth of exposure (~$89.5M notional) with $41M

- ⏰ Time diversification: Three different expirations (11 days, 102 days, 751 days)

- 📊 Directional stance: Bullish with comprehensive downside protection

- 🛡️ Risk management: Maximum downside protected at $13 (Jan 2028 puts), willing to own stock at $14 (Apr puts), deep leverage at $12 (Jan calls)

SCENARIOS & PAYOFFS:

📈 If NU rallies to $20+ by mid-January:

- ✅ Jan $12 calls worth $8+ each = Huge profit on 5M shares of exposure

- ❌ Jan $17 short calls cap gains on 2.6M shares but still profit

- ⏰ Apr $19 calls and short $14 puts both expire worthless (no harm)

- ⏰ Jan 2028 $13 puts lose value but preserve long-term insurance

- 💰 Estimated P&L: +$15-20M profit

🎯 If NU consolidates $17-19 through February (BASE CASE):

- ✅ Jan $12 calls capture $5-7 of intrinsic value = Solid profit

- ⏰ Jan $17 short calls expire worthless (keep premium)

- ✅ Apr $19 calls gain value as Mexico catalyst approaches

- ✅ Apr $14 short puts expire worthless (keep $1.1M premium)

- ⏰ Jan 2028 $13 puts maintain insurance value

- 💰 Estimated P&L: +$8-12M profit

📉 If NU drops to $15-16 (mild pullback):

- ✅ Jan $12 calls still profitable ($3-4 intrinsic value)

- ✅ Jan $17 short calls expire worthless (keep premium)

- ⚠️ Apr $19 calls lose value but still have time

- ⚠️ Apr $14 short puts at risk (may need to take stock assignment)

- ✅ Jan 2028 $13 puts GAIN value (hedge working)

- 💰 Estimated P&L: -$2-5M loss (protected by LEAP puts)

😱 If NU crashes below $14 (disaster scenario):

- ❌ Jan $12 calls lose most value

- ✅ Jan $17 short calls expire worthless

- ❌ Apr $19 calls worthless

- 💪 Apr $14 short puts assigned → forced to buy 5M shares at $14 (cost: $70M)

- 🚀 Jan 2028 $13 puts EXPLODE in value → protecting the downside!

- 💰 Estimated P&L: Limited loss due to $13 put floor protecting 5M share exposure

Unusual Scores - This is HISTORIC:

- 🔥 LEAP $13 puts: Z-Score 8,278.17 = This size happens maybe once every few YEARS

- 🔥 Jan $12 calls: Z-Score 78.14 = 78x average size

- 🔥 Apr $19 calls: Z-Score 75.65 = 75x average size

- 🔥 Apr $14 short puts: Z-Score 234.01 = 234x average size

Translation: This isn't institutional hedging - this is an architected position built by someone with MASSIVE conviction in NU's 2026 story but sophisticated enough to structure for multiple scenarios. The Z-scores show this is truly unusual activity - the $13 LEAP puts alone are larger than 99.99% of all NU option trades in recent history.

📈 Technical Setup / Chart Check-Up

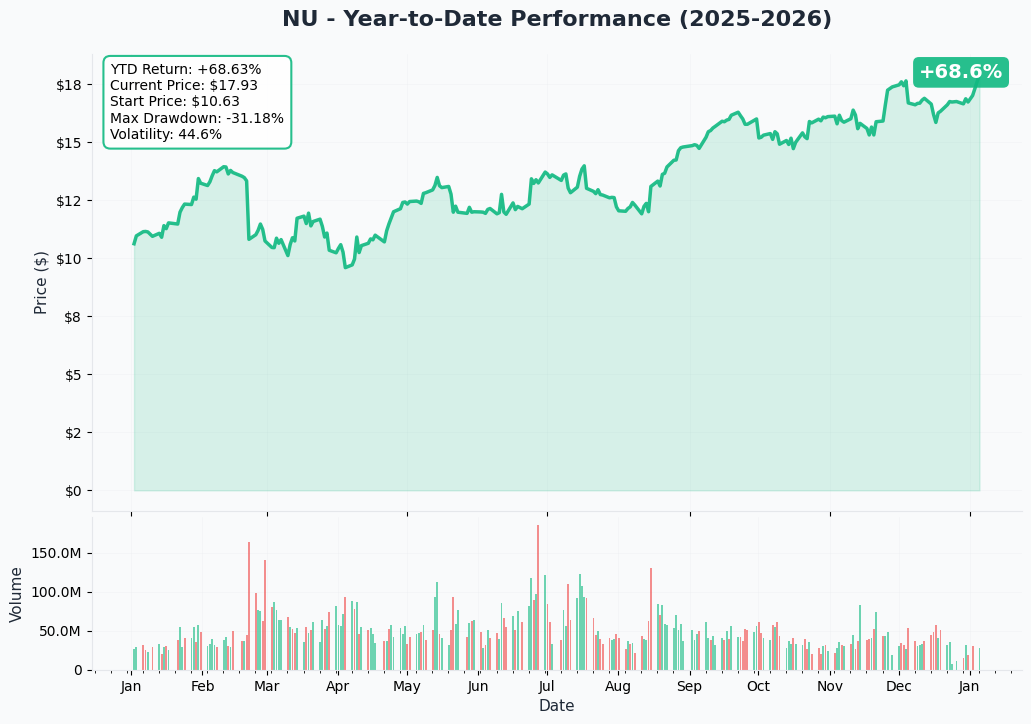

YTD Performance Chart

NU is on an absolute TEAR - up +52.65% over the past year with current price of $17.91 (started January 2025 at $11.75). The chart shows a powerful fintech growth story - after trading in a tight $11-13 range through Q1 2025, NU broke out above $13 in May and never looked back, rallying to all-time highs of $17.84 on December 2, 2025.

Key observations:

- 🚀 Sustained uptrend: Clean rally from $11.75 to $17.91 with higher lows throughout 2025

- 📈 Breakout momentum: Explosive move from $13 to $17+ in October-November on OpenAI partnership and earnings beat

- 📊 All-time highs: Trading just 0.4% below December 2 peak of $17.84

- 🎯 52-week range: $9.01 - $17.84 (current near the high end)

- 💪 Institutional accumulation: Consistent buying pressure with 84% institutional ownership

- ⚠️ Overbought risk: Extended above most moving averages - near-term consolidation likely

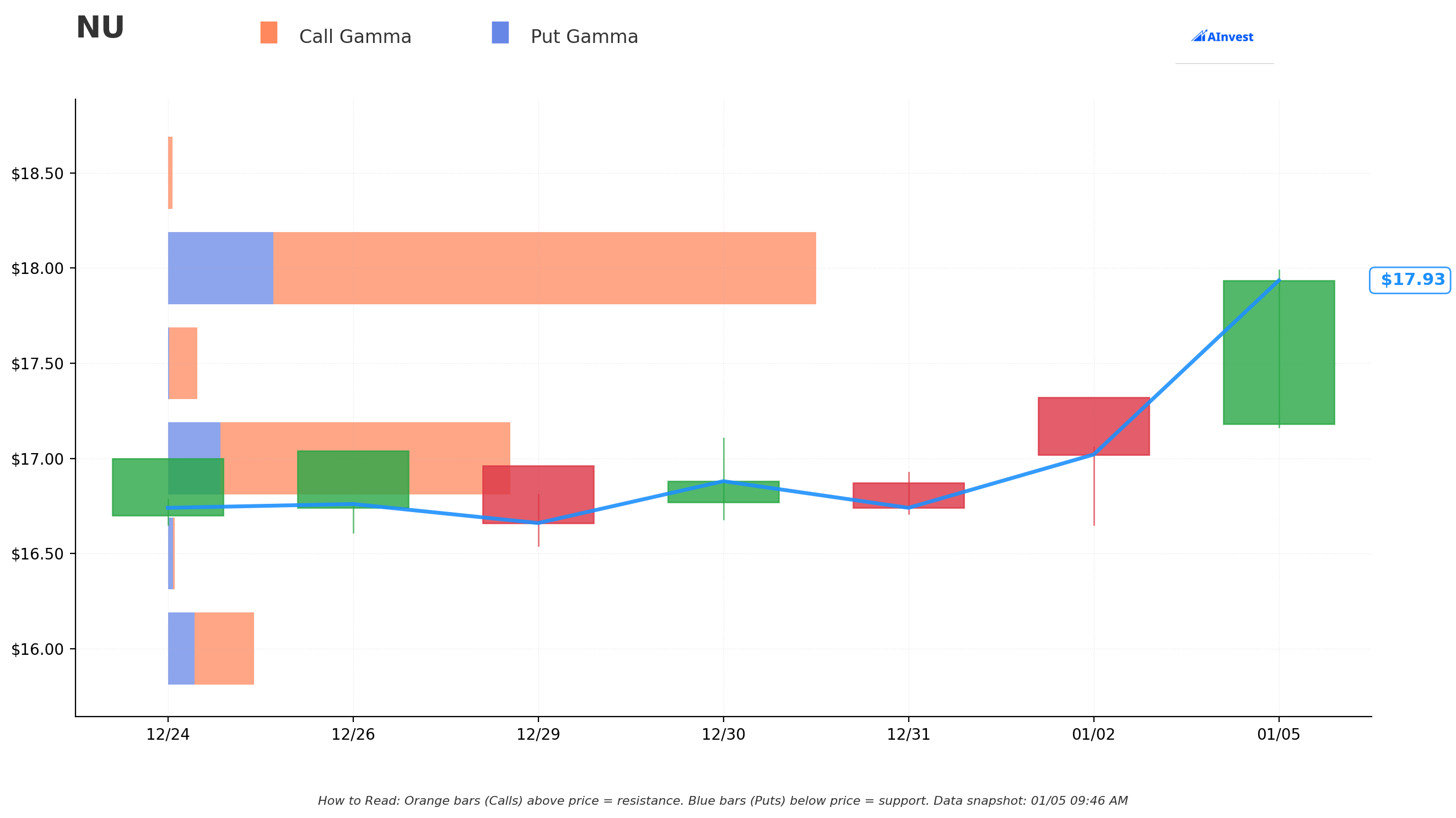

Gamma-Based Support & Resistance Analysis

Current Price: $17.93

The gamma exposure map reveals critical price magnets and barriers for near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $17.50 - Immediate support with 4.94B total gamma exposure (2.42% below current)

- $17.00 - Strong support at 55.54B gamma (5.21% below - MAJOR LEVEL!)

- $16.50 - Secondary floor with 1.06B gamma (7.99% below)

- $16.00 - Deep support at 13.99B gamma (10.78% below)

- $15.00 - Extended support zone with 17.82B gamma (16.36% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $18.00 - Immediate ceiling with 105.07B gamma (STRONGEST RESISTANCE - 0.37% overhead!)

- $18.50 - Secondary resistance at 0.77B gamma (3.16% above)

- $19.00 - Medium-term target with 7.90B gamma (5.94% above - matches Apr $19 calls!)

- $20.00 - Extended upside target at 24.36B gamma (11.52% above)

- $21.00 - Long-term target with 0.55B gamma (17.10% above)

What this means for traders:

NU is trading in a CRITICAL zone just below massive $18.00 resistance (105.07B gamma - the single largest level on the entire chain). This creates enormous selling pressure as market makers hedge their exposure. The stock has tried to break $18 multiple times and gotten rejected - this is THE ceiling that needs to break for continuation to $19-20.

Notice the asymmetry: Resistance at $18 is nearly DOUBLE the total gamma of all support levels combined. This setup screams "consolidation range" or potential pullback before the next leg higher.

But here's the kicker: The options player struck their Apr $19 calls EXACTLY where there's 7.90B gamma resistance at $19. They're positioned for a breakout through $18, consolidation around $19 by April expiration. The short $14 puts sit between the $15.00 support (17.82B) and $16.00 support (13.99B) - showing they're comfortable buying any dip to that zone.

Net GEX Bias: Bullish (201.39B call gamma vs 46.08B put gamma) - Overall positioning remains extremely bullish, but immediate price action constrained by overhead $18 resistance.

The strongest support at $17.00 (55.54B gamma) is the LINE IN THE SAND - this matches the Jan $17 short calls strike. If NU holds above $17, those short calls expire worthless and they keep the premium. Smart positioning!

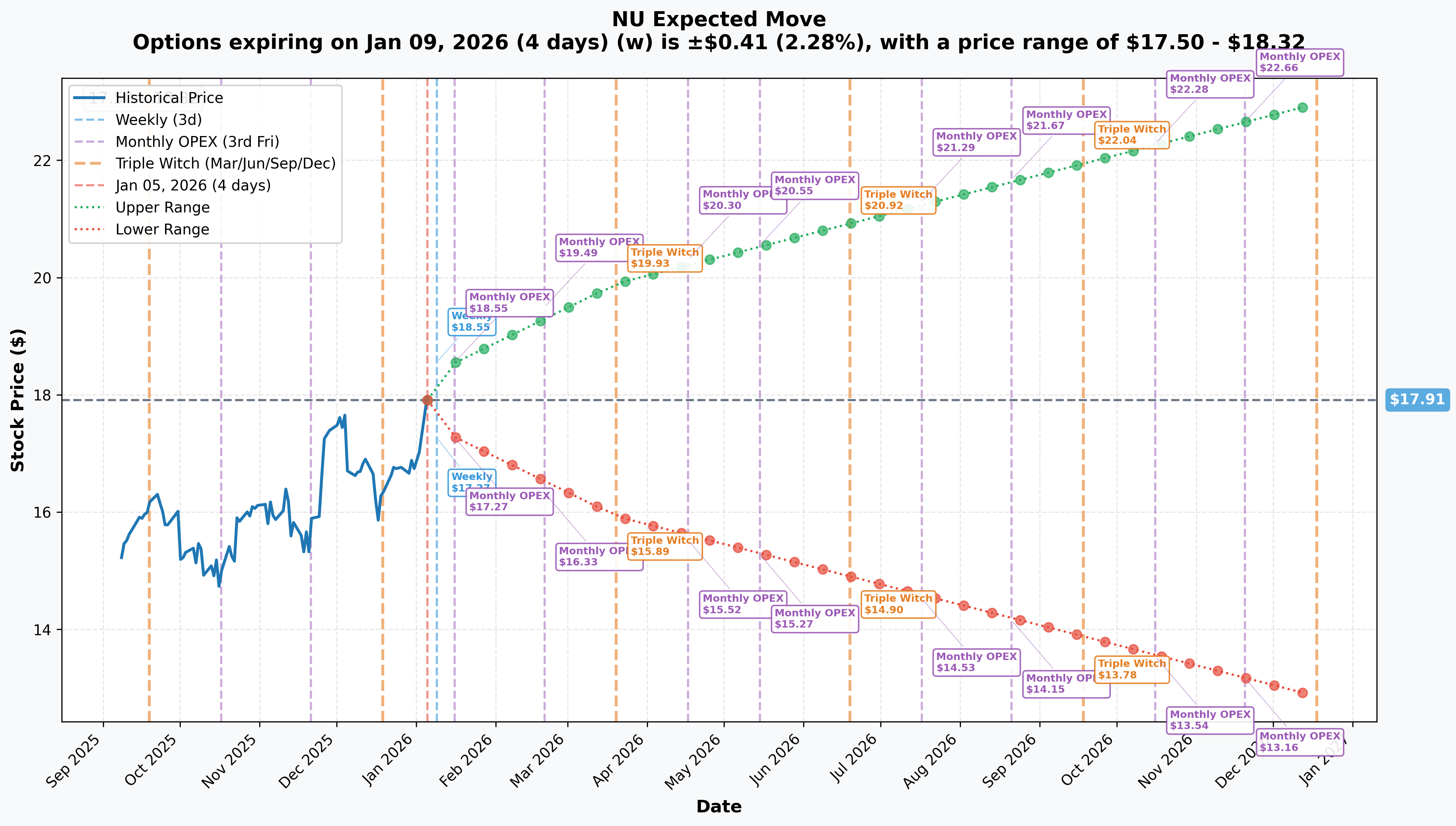

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 4 days): ±$0.41 (±2.28%) → Range: $17.50 - $18.32

- 📅 Monthly OPEX (Jan 16 - 11 days - JAN CALLS EXPIRATION!): ±$0.64 (±3.56%) → Range: $17.27 - $18.55

- 📅 Quarterly Triple Witch (Mar 20 - 74 days): ±$1.99 (±11.11%) → Range: $15.92 - $19.90

- 📅 April OPEX (Apr 17 - 102 days - APR CALLS/PUTS EXPIRATION!): ±$2.19 (±12.21%) → Range: $15.72 - $20.10

- 📅 Yearly LEAPS (Dec 18 - 347 days): ±$5.06 (±28.24%) → Range: $12.85 - $22.97

Translation for regular folks:

Options traders are pricing in a 2.3% move ($0.41) by January 9th for weekly expiration, but a larger 3.6% move ($0.64) through January 16th which is when the massive Jan $12 calls and $17 short calls expire. The market expects modest volatility near-term.

The April 17th expiration (when the $19 calls and $14 short puts expire) has an implied range of $15.72 - $20.10. This aligns PERFECTLY with the trader's thesis:

- Upper range $20.10 covers their $19 call strike with room to spare

- Lower range $15.72 sits above their $14 put obligation

- They're positioned for the exact range the market is pricing!

The 2-year LEAP expiration (Dec 2026) shows a massive ±28.24% implied move with a lower range of $12.85 - just below their $13 put protection at $13.00. This suggests the market sees meaningful downside risk over 2 years (Brazilian macro, regulatory changes, competition), which is exactly what those LEAP puts protect against.

Key insight: The sharp increase in implied volatility from 3.6% (monthly) to 12.2% (April) to 28.2% (yearly) reflects growing uncertainty as you move further out. The trader structured each layer to match the risk profile of each timeframe - brilliant position architecture!

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Q4 2025 Earnings - February 25, 2026 (50 DAYS AWAY!) 📊

NU reports fiscal Q4 2025 results on Wednesday, February 25, 2026. This is a CRITICAL catalyst that could validate the bullish thesis. Wall Street consensus and key expectations:

- 📊 Revenue: Expected ~$4.01B (continued 35%+ YoY growth trajectory) per consensus estimates

- 💰 EPS: Expected $0.19 (+12% vs Q3's $0.17)

- 🤖 Customer Growth: Watch for 130M+ total customers (127M in Q3)

- 💻 ARPAC (Revenue per Customer): Target $13.50+ (was $13.40 in Q3, up 20% YoY)

- 📈 Net Interest Margin: Critical metric after 100bps compression in Q3 to 17.3%

- 💚 ROE: Expecting to maintain 30%+ (Q3 was record 31%)

- 🇲🇽 Mexico Update: Commentary on banking license activation timeline and 13M customer monetization plan

Why this matters for the options position:

- ⏰ The Jan $12 calls expire 40 days BEFORE earnings, so near-term move driven by anticipation

- 🎯 The Apr $19 calls expire 51 days AFTER earnings, positioned to capture the full earnings reaction

- 📊 Strong Q4 results + positive Mexico commentary could drive the $17→$19 move this structure needs

Upside surprise potential: If NU announces Mexico banking operations BEGIN during Q4 or early Q1, stock could explode to $19-20 on the transformational revenue opportunity (payroll accounts targeting 36% of Mexican adults without banking).

Downside risk factors: Any disappointment in customer additions, ARPAC growth stalling, or NIM compression continuing would hit the stock. Conservative Q1 2026 guidance citing macro uncertainty in Brazil could also pressure shares.

🚀 Near-Term Catalysts (Q1-Q2 2026)

Mexico Banking Operations Activation - Q1-Q2 2026 (GAME CHANGER!) 🇲🇽

NU Mexico received banking license approval on April 24, 2025 and is currently undergoing regulatory audit before operations begin:

- 🏦 License significance: First Popular Financial Society to transform into full bank in Mexico

- 👥 Customer base ready: 13 million customers waiting for full banking services

- 💰 Revenue opportunity: Payroll accounts targeting 36% of Mexican adults without payroll banking

- 📈 Deposit expansion: Higher deposit limits and 16x increased IPAB deposit insurance from $1,580 to $25,000

- 🎯 ARPAC acceleration: Mexico ARPAC currently lags Brazil - banking license unlocks monetization

- 💵 Investment scale: $1.4B+ already invested in Mexico, $4.5B+ deposits accumulated

- ⏰ Timeline: Activation expected Q1-Q2 2026 (matches April options expiration perfectly!)

Why this is HUGE for the April position:

The trader positioned Apr $19 calls to capture this exact catalyst. If Mexico banking operations launch in March-April 2026 with strong initial metrics (payroll account adoption, deposit growth), NU could easily hit $19-20 by April 17th expiration. This is a known catalyst with a clear timeline - not speculation.

Potential revenue impact: Brazil ARPAC is $13.40 while Mexico is still ramping. If Mexico achieves even 50% of Brazil's ARPAC over 13M customers, that's $1B+ incremental annual revenue opportunity (13M × $6.70 × 12 months). Market will re-rate NU higher when this materializes.

U.S. National Bank Charter Application - Decision Expected 2026 🇺🇸

NU Holdings applied to the OCC on September 30, 2025 for a de novo national bank charter:

- 🏛️ Charter scope: Would enable deposit accounts, credit cards, lending, and digital asset custody in U.S. market

- ⏰ Decision timeline: Typical OCC review takes 12-18 months (decision likely Q3-Q4 2026)

- 🌎 Strategic significance: First major expansion beyond Latin America - validates global ambitions

- 💰 TAM expansion: U.S. retail banking market estimated at $1.5+ trillion in deposits

- ⚠️ Regulatory risk: OCC approval not guaranteed - fintech charter scrutiny has increased

Why this matters for the 2-year LEAP puts:

The $13 LEAP puts expiring Jan 2028 provide protection through the ENTIRE U.S. charter process. If the OCC denies the charter or imposes restrictive conditions, it could crater the stock 20-30% on dashed global expansion dreams. The long-dated puts protect against this binary regulatory risk while allowing full upside participation if charter is approved.

Stablecoin Credit Card Integration - Testing Phase 2026 💳

Former Brazilian Central Bank Governor Roberto Campos Neto (now NU Vice-Chairman) disclosed plans at Meridian 2025 to integrate stablecoins with credit card transactions:

- 🔗 Technology: Testing stablecoin payments linked to existing credit card infrastructure

- 🎯 Vision: Combining blockchain/tokenization with mainstream fintech products

- ⏰ Timeline: Testing underway in 2026, broader rollout TBD

- 🌐 Strategic alignment: Positions NU as innovator at intersection of crypto and traditional banking

- ⚠️ Regulatory uncertainty: Brazil and Mexico crypto regulations still evolving

Market Impact: This is more "option value" than near-term catalyst - could become meaningful by 2027-2028 timeframe, well within the LEAP protection window.

📊 Strategic Developments

AI-First Strategy with Proprietary nuFormer Model 🤖

CEO David Velez announced "AI-first" strategy focusing on agentic workflows:

- 🧠 nuFormer: Proprietary AI model for customer behavior analysis and credit decisioning

- 💳 Credit optimization: Used AI to adjust credit card limit policies in Brazil, expanding credit access without increasing risk

- 🤝 OpenAI partnership: Signed enterprise deal in March 2025 for search and productivity tools

- 💰 Cost leadership: Maintains $0.90 cost to serve per customer (below $1.00 target) through AI automation

- 📈 Competitive advantage: AI enables superior unit economics vs traditional banks

Institutional Ownership Surge 🏦

NU has 84.02% institutional ownership with 1,246 institutional holders:

Recent institutional activity (Q3 2025):

- Voya Investment Management: Increased position by 573% to 2.95M shares ($47.3M)

- Ariose Capital Management: New position of 113,200 shares ($1.8M) on January 4, 2026

- Itau Unibanco: New $39.8M position (major Brazilian bank investing in digital competitor!)

- Global Retirement Partners: Increased 517%

- Top holders: BlackRock, Baillie Gifford, Capital Research, Morgan Stanley, JPMorgan

This smart money activity VALIDATES the bullish thesis - institutions are aggressively accumulating NU heading into 2026 catalysts.

⚠️ Risk Catalysts (Negative)

Brazilian Real Currency Weakness & Macro Uncertainty 🇧🇷

- 💱 USD/BRL at 5.42 (January 2, 2026) and weakened 2.06% in past month

- 📉 Projection: USD/BRL between 5.01-5.22 by December 2026 per Trading Economics forecasts

- ⚠️ Impact: Real weakness impacts USD-reported revenue and earnings (NU reports in USD but earns in BRL/MXN/COP)

- 🗳️ Pre-Q4 2026 election: Brazilian election spending could drive fiscal uncertainty and further Real pressure

- 📊 Historical volatility: NU took $800M charges from currency-driven impacts historically

This is EXACTLY what the $13 LEAP puts protect against - if Brazilian macro deteriorates significantly (recession, Real collapse, political crisis), those puts could increase 5-10x in value to offset losses.

Mexico Interchange Fee Cap Proposal 🇲🇽

Mexican government consulting on capping credit/debit card interchange fees:

- ⚖️ Regulatory risk: Fee caps could reduce unit economics for new-to-credit customers in Mexico

- 💰 Revenue impact: Interchange fees are meaningful revenue stream for card products

- 🎯 Strategic concern: Could inhibit financial inclusion strategy and credit deepening

- ⏰ Timeline: Consultation ongoing, implementation could occur 2026

Net Interest Margin Compression Trend 📉

- 📊 Q3 NIM: 17.3% (down 100bps YoY) per NU's Q3 2025 earnings

- ⚠️ Funding cost pressure: Rising deposit rates to attract and retain customers

- 💳 Brazil rate environment: Selic rate projected around 11.50% end-2026

- 📉 Profitability risk: Continued NIM compression could pressure ROE and margins

Valuation Stretched at Premium Multiples 💰

- 🎯 P/E valuation: ~30x trailing vs banking industry average ~11x per Simply Wall St analysis

- 📈 Forward P/E: 23.83x

- ⚠️ Premium pricing: Stock up 52.65% YTD and trades at 180-210% premium to bank peers

- 💸 Limited margin: Any execution misstep could trigger 15-20% correction

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through the strategy's timeframes:

📈 Bull Case (35% probability)

Target: $19-$21 by April 2026

How we get there:

- 💪 Q4 earnings BEAT with revenue toward $4.2B+ and EPS $0.20+ (vs $0.19 consensus)

- 🇲🇽 Mexico banking activation announced for March 2026 with strong payroll account adoption metrics

- 📊 ARPAC expansion accelerates to $14+ (from $13.40) showing monetization momentum

- 🏦 Customer growth surprises at 132M+ total (vs 127M in Q3)

- 💚 ROE maintains 30%+ and NIM stabilizes (no further compression)

- 📈 Institutional accumulation continues - more Voya-style position increases

- 🔨 Technical breakout above $18 gamma resistance triggers momentum rally to $19-20

- 🌐 Analyst upgrades citing Mexico catalyst and raising price targets to $20-23 range

Key gamma levels supporting bull case:

- Break $18.00 resistance (105.07B gamma) - THE key level

- Consolidate at $19.00 resistance (7.90B gamma) - matches April call strike

- Target $20.00 (24.36B gamma) if momentum continues

Options position P&L in bull case:

- ✅ Jan $12 calls: Massive profit on 5M share equivalent (stock at $19+ = $7+ intrinsic value = $35M gain)

- ❌ Jan $17 short calls: Capped at $17 on 2.6M shares but still profitable overall

- ✅ Apr $19 calls: In-the-money with profit (stock at $20 = $1+ profit = $5M gain)

- ✅ Apr $14 short puts: Expire worthless, keep $1.1M premium

- ⏰ Jan 2028 $13 puts: Lose some time value but maintain catastrophe insurance

- 💰 Total estimated P&L: +$25-35M profit (60-85% ROI on $41M deployed)

Probability assessment: 35% because it requires multiple catalysts firing correctly (earnings beat + Mexico activation + NIM stabilization + macro cooperation). Achievable but not guaranteed.

🎯 Base Case (45% probability)

Target: $17-$19 range (CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q4 earnings meeting consensus (~$4.0B revenue, $0.19 EPS)

- 📅 Mexico banking activation confirmed for Q2 2026 (April-June) but not immediate

- 📊 ARPAC steady at $13.50-$13.80 range (solid but not spectacular)

- 👥 Customer growth in-line at 129-130M

- ⚖️ NIM stabilizes at 16.5-17.5% range (no major compression but no expansion)

- 💱 Brazilian Real volatility continues but no crisis

- 🔄 Trading within gamma bands - respecting $17 support and $18-19 resistance

- 📊 Analyst targets remain $17-19 range with Hold/Buy ratings

- ⏰ Market waits for Mexico activation proof points before next major move

This is the "position works as designed" scenario:

Options position P&L in base case:

- ✅ Jan $12 calls: Good profit (stock at $17-18 = $5-6 intrinsic = $25-30M gain)

- ✅ Jan $17 short calls: Expire worthless or small loss, keep most premium

- 📊 Apr $19 calls: Break-even to small loss (stock at $18 = $1 out of money)

- ✅ Apr $14 short puts: Expire worthless, keep full $1.1M premium

- ⏰ Jan 2028 $13 puts: Maintain value as insurance

- 💰 Total estimated P&L: +$15-20M profit (35-50% ROI)

Why 45% probability: This aligns with implied move expectations ($17.27-$18.55 for Jan, $15.72-$20.10 for April). Fundamentals support consolidation while waiting for Mexico catalyst. The structure is DESIGNED for this scenario - profit on Jan calls, collect premium on short positions, maintain long-term protection.

📉 Bear Case (20% probability)

Target: $14-$16 (TEST THE SHORT PUTS!)

What could go wrong:

- 😰 Q4 earnings miss or weak guidance disappoints - even small miss triggers selloff at 30x P/E

- 🇲🇽 Mexico activation delayed to Q3 2026 or later - removes near-term catalyst

- 📉 NIM compression accelerates below 16% - profitability concerns emerge

- 🇧🇷 Brazilian macro deteriorates - Real crashes below 6.00, recession fears

- 🇺🇸 U.S. charter denied or delayed - global expansion thesis questioned

- ⚖️ Mexico interchange fee caps implemented - hurts unit economics

- 💸 Broader fintech selloff drags all Latin American digital banks lower

- 📊 Competition intensifies - Mercado Pago, PagBank, PicPay gaining share

- 🔨 Break below $17 gamma support triggers cascade to $16, then $15

Critical support levels:

- 🛡️ $17.00: Major gamma floor (55.54B) - MUST HOLD or momentum shifts bearish

- 🛡️ $16.00: Deep support (13.99B gamma)

- 🛡️ $15.00: Extended floor (17.82B gamma)

- 🛡️ $14.00: Apr short put strike - forced to buy stock here

Options position P&L in bear case:

- ❌ Jan $12 calls: Reduced profit (stock at $15 = $3 intrinsic = $15M gain, less than hoped)

- ✅ Jan $17 short calls: Expire worthless, keep premium

- ❌ Apr $19 calls: Total loss (-$4.3M)

- 💰 Apr $14 short puts: ASSIGNED → buy 5M shares at $14 (cost: $70M but willing!)

- 🚀 Jan 2028 $13 puts: GAIN significant value as hedge (stock at $15 = puts worth $2+ = value increase)

- 💰 Total estimated P&L: -$5-10M loss BUT protected by put floor and gets to own stock at $14

The beauty of this scenario: Even in the bear case, the trader is PROTECTED. They're forced to buy 5M shares at $14 (21.8% below current price), which they view as excellent value. The $13 LEAP puts limit catastrophic risk below $13. This is intelligent risk management - the downside is structured and acceptable.

Probability assessment: Only 20% because NU's fundamentals remain strong (127M customers, 39% revenue growth, 31% ROE, Mexico catalyst pending). Would require multiple negative catalysts to align. The trader clearly thinks this scenario has <20% odds or they wouldn't structure with so much upside exposure.

💡 Trading Ideas

🛡️ Conservative: Cash-Secured Put at $15 (Copy The Pros!)

Play: Sell cash-secured puts at strikes below current support, willing to own NU at a discount

Structure: Sell Mar 2026 $15 puts (triple witch expiration)

Why this works:

- 📊 Copying smart money: Institutional player is WILLING to own NU at $14, so $15 is even safer

- 🎯 Gamma support: $15.00 has 17.82B put gamma - strong technical floor

- 💰 Premium income: Collect $0.40-0.60 per share (~3-4% return in 74 days)

- 🛡️ Margin of safety: 16.36% below current price ($17.91 → $15.00)

- ⏰ Timeline: Captures Q4 earnings reaction and any early Mexico activation news

- 🏦 Fundamentals support: NU growing 39% YoY with 31% ROE - $15 is CHEAP if pullback occurs

- 📈 Upside: Keep premium if NU stays above $15 (high probability given support levels)

Entry mechanics:

- 💸 Sell 1 contract = collect $40-60 premium, commit to buy 100 shares at $15

- 🏦 Capital required: $1,500 cash held in account (you're promising to buy stock if assigned)

- ⏰ Time to work: 74 days (nearly 2.5 months)

Three scenarios:

- NU above $15 at March 20: Keep full premium, puts expire worthless → 3-4% return in 2.5 months (15-18% annualized!)

- NU at $14-15 at March 20: Assigned stock at $15 net $0.40-0.60 premium → effective basis $14.40-14.60 (better than institutional $14 strike!)

- NU below $14 at March 20: Assigned stock at $15 but underwater temporarily - HOLD for recovery (fundamentals support $17-19 value)

Position sizing: Only sell puts on stock quantities you're HAPPY to own long-term. If you want to own 500 shares of NU, sell 5 contracts.

Risk management:

- ✅ Only use this strategy if you WANT to own NU at $15 (don't sell puts on stocks you don't like!)

- ⏰ Set calendar reminder for February 25 earnings - close position if results disappoint

- 📊 If NU breaks below $16 before expiration, consider rolling puts down to $14 or buying back to avoid assignment

Risk level: Low-Moderate (must hold capital, stock ownership risk) | Skill level: Beginner-Intermediate

Expected outcome: 70% probability keep premium without assignment, 30% get assigned and own quality fintech stock at 16% discount

⚖️ Balanced: April Call Spread (Targeting Mexico Catalyst)

Play: Bull call spread positioned for Mexico banking activation catalyst

Structure: Buy Apr $18 calls, Sell Apr $20 calls

Why this works:

- 🎯 Catalyst timing: April 17 expiration captures Q4 earnings (Feb 25) AND Mexico bank activation (Q1-Q2 2026)

- 📊 Defined risk: $2 wide spread = $200 max risk per spread

- 💰 Favorable risk/reward: Pay ~$0.70-0.90 for spread with $2.00 max value (2:1 to 3:1 reward)

- 🔨 Technical setup: Targets breakout above $18 resistance (105.07B gamma) to $20 (24.36B gamma)

- 📈 Copying institutional: Smart money has Apr $19 calls - we're bracketing their strike

- ⏰ Time value: 102 days allows Mexico catalyst to develop and materialize

Estimated P&L:

- 💰 Cost: $0.70-0.90 per spread (mid-estimate $0.80)

- 📈 Max profit: $1.20-1.30 if NU above $20 at expiration (150-180% ROI)

- 📊 Breakeven: ~$18.70-18.90

- 💀 Max loss: $0.70-0.90 if NU below $18 (100% loss but defined)

- 🎯 Profit zone: NU above $18.70 (4.4% above current price)

Three scenarios:

- NU at $20+ on Apr 17 (bull case): Spread worth full $2.00 → profit $1.10-1.30 per spread (155% ROI)

- NU at $18.50-19.50 (base case): Spread worth $0.50-1.50 → breakeven to solid profit

- NU below $18 (bear case): Spread expires worthless → lose $0.70-0.90 (capped loss)

Entry timing:

- ⏰ Ideal entry: Wait 2-3 days to see if NU pulls back toward $17.50 support (better entry)

- ❌ Don't chase: If NU already above $18.50, spread becomes less attractive (lower reward)

- ✅ Best scenario: Enter on any dip to $17.50-17.80 range for maximum upside

Position sizing: Risk only 2-5% of options trading capital (this is directional speculation)

Exit strategy:

- 🎯 Take profit at 100% gain (spread doubles to $1.60) - don't get greedy waiting for max value

- ⏰ Close 1 week before earnings (Feb 18) if you want to derisk binary event - lock in gains

- 📊 Or hold through earnings if you're comfortable with volatility - catalyst could drive $18→$20 move

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

🚀 Aggressive: Replicate the Jan Call Spread (ADVANCED!)

Play: Copy the institutional Jan 16 call strategy (leveraged synthetic long position)

Structure: Buy Jan 16 $12 calls, Sell Jan 16 $17 calls (ratio 2:1 like the institutional trade)

Why this could work:

- 📊 Copying smart money: Institutions deployed $27.1M net on this exact structure - they see edge

- ⚡ High leverage: Deep ITM $12 calls (delta ~0.99) act like synthetic stock with less capital

- 🎯 Asymmetric payoff: 2:1 ratio means half your position has unlimited upside, half capped at $17

- 💰 Defined max loss: If NU drops hard, loss limited to premium paid (vs owning stock outright)

- ⏰ Near-term catalyst: 11 days captures pre-earnings positioning momentum

- 🔨 Gamma support at $17: Strong 55.54B gamma floor at short call strike - likely to hold

Why this is RISKY (READ THIS CAREFULLY!):

- 💸 EXPENSIVE: $12 calls cost ~$5.80 each, $17 calls worth ~$0.73 → net $5.07 per 2:1 spread

- ⏰ TIME DECAY KILLER: Only 11 days left - theta burns -$0.15-0.25/day per contract

- 📉 Needs immediate move: Stock must stay above $17.07 to profit (only 4.5% downside cushion)

- 😱 Wrong if consolidation: If NU chops $17-18, you lose time value daily and end barely profitable

- 🎢 Pre-earnings risk: Positioning into Feb 25 earnings could see profit-taking/consolidation

- ⚠️ Execution critical: Need to close within days of profitable move - can't hold to expiration or theta eats gains

Estimated P&L (per 2:1 ratio spread):

- 💰 Cost: Buy 2x $12 calls ($11.60) - Sell 1x $17 call ($0.73) = $10.87 net debit

- 📈 Max profit: UNLIMITED if NU rallies past $17 (1 uncapped long call keeps going)

- 📊 Breakeven: ~$17.44 (need 2.6% move in 11 days to breakeven!)

- 💀 Max loss: $10.87 if NU crashes below $12 (unlikely but possible)

- 🎯 Target profit: NU at $19 = ~$3.50 profit per spread (32% ROI in 11 days!)

Scenarios:

- NU rallies to $19 by Jan 16: Each $12 call worth $7.00 (2x = $14.00), short $17 call costs -$2.00 → net $12.00 vs $10.87 cost = $1.13 profit (10% ROI)

- NU stays at $17.90 (flat): Each $12 call worth $5.90 (2x = $11.80), short $17 call worth -$0.90 → net $10.90 vs $10.87 cost = $0.03 profit (0% ROI after commissions)

- NU drops to $16: Each $12 call worth $4.00 (2x = $8.00), short $17 call expires worthless → net $8.00 vs $10.87 cost = -$2.87 loss (26% loss)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded deep ITM call spreads before and understand delta/theta dynamics

- ✅ Can afford to lose ENTIRE premium ($1,087 per spread minimum position)

- ✅ Can monitor position DAILY (this needs active management, not set-and-forget)

- ✅ Understand you're betting on immediate directional move within 11 days

- ✅ Are comfortable with complexity of unbalanced ratios

- ⏰ Plan to close position within 3-5 days if profitable (don't hold to expiration letting theta decay eat gains)

Better alternative for most traders: Just buy Jan 16 $17 calls outright (~$1.20) betting on move to $18.50-19 for simpler 50-100% gain potential

Risk level: EXTREME (high premium, short time, needs immediate move) | Skill level: Advanced only

Probability of profit: ~35-40% (need 2.6%+ move in just 11 days to breakeven, plus fighting time decay)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📅 Q4 earnings in 50 days (Feb 25): Results create binary volatility risk. NU could gap 10-15% either direction based on ARPAC growth ($13.40 vs $14 makes huge difference), NIM trends (compression continuing vs stabilizing), customer additions (127M → 130M+ vs disappointment), and Mexico banking commentary. At 30x P/E with stock near all-time highs, market has priced in strong execution - any miss amplified.

-

💱 Brazilian Real at 5.42 and volatile: Real weakened 2.06% in past month and projections show USD/BRL 5.01-5.22 by December 2026. NU reports in USD but earns revenue in BRL (Brazil 87% of customers), MXN (Mexico), and COP (Colombia). Significant Real weakness directly impacts reported revenue/earnings. Pre-election 2026 fiscal uncertainty in Brazil could drive further currency pressure. This is EXACTLY what the $13 LEAP puts protect against.

-

🇲🇽 Mexico banking activation delay risk: While license approved April 2025, regulatory audit timeline uncertain. Any delay past Q2 2026 removes key catalyst for April $19 calls. Worse, if regulatory issues emerge or license conditions prove restrictive, it could tank the entire Mexico growth thesis (13M customers, $4.5B deposits, $1.4B invested).

-

⚖️ Mexico interchange fee cap proposal: Government consulting on capping credit/debit card fees which could reduce unit economics for new-to-credit customers. If implemented in 2026, would pressure Mexico ARPAC growth trajectory just as banking operations activate. Could force NU to choose between growth (lower fees, more customers) vs profitability (maintain fees, slower adoption).

-

📉 Net interest margin compression accelerating: NIM fell 100bps in Q3 to 17.3% due to rising deposit rates. If this trend continues (NIM below 16%), threatens the 30%+ ROE that justifies premium valuation. Watch Q4 earnings for NIM guidance - any forecast for further compression could trigger 15-20% selloff even if other metrics beat.

-

🇺🇸 U.S. charter approval uncertain: OCC application filed Sept 30, 2025 but approval NOT guaranteed. Regulatory scrutiny on fintech charters has increased significantly. If denied or delayed past 2027, damages global expansion narrative and questions whether NU can scale beyond Latin America. This binary risk extends through 2026-2027, which is why the 2-year LEAP puts make sense.

-

💰 Valuation at 30x P/E vs 11x industry: NU trades at ~30x trailing P/E vs banking industry average ~11x per Simply Wall St. This 180-210% premium requires PERFECT execution on Mexico activation, ARPAC growth, customer expansion, and margin maintenance. Stock has ZERO margin for error - one quarter of disappointment could trigger reversion toward 20-25x multiple (15-20% downside to $15 range).

-

🏦 Competition intensifying in key markets: Mercado Pago leads in Argentina, Mexico, Chile and is #2 in Brazil. PagBank named "highlight of the year" in Brazil rankings. PicPay "tied with Nubank" in recent rankings. Customer acquisition costs could rise as competition heats up. Market share gains in Brazil slowing (already 60%+ penetration) - future growth depends on Mexico/Colombia execution.

-

🔨 Gamma resistance at $18 creates mechanical ceiling: Massive 105.07B call gamma at $18.00 (more than DOUBLE any other level) means market makers systematically SELL into rallies to hedge exposure. Stock has tried breaking $18 multiple times and gotten rejected. Would need massive institutional buying or major catalyst to overcome this technical barrier. Until $18 breaks decisively, upside limited.

-

📊 Institutional position could be hedging, not directional bet: While this analysis assumes bullish positioning, there's possibility this is a sophisticated HEDGE for an even larger underlying stock position. If the institution owns 20M+ shares of NU, this $41M position could be defensive portfolio management (protecting gains from $11→$18 rally) rather than new bullish bet. We don't know their full book!

-

⏰ Time decay on near-term calls brutal: The Jan $12 calls (11 days) and Apr $19 calls (102 days) both lose value DAILY from theta decay. Jan calls burning $0.15-0.25/day, Apr calls losing $0.03-0.05/day. If NU consolidates $17-18 without catalyst, option values erode even if stock flat. Retail traders copying this position need to understand time decay risk.

🎯 The Bottom Line

Real talk: Someone just architected a $41.1 MILLION multi-layer options position that's bullish on NU's 2026 story while intelligently protecting against tail risks. This isn't a YOLO bet - it's sophisticated portfolio construction by an institution with deep conviction in NU's growth trajectory (Mexico banking, U.S. expansion, ARPAC scaling) but smart enough to hedge Brazilian macro risk, regulatory uncertainty, and execution risk.

What this position tells us:

🎯 Near-term (11 days to Jan 16):

- Positioned for consolidation/modest rally to $17-18 range

- The massive $12 call position (50K contracts = 5M shares) is leveraged synthetic long, capturing upside with less capital than buying stock

- Short $17 calls on half the position show they're comfortable capping gains at $17 on 2.6M shares - expecting consolidation not explosion

- Translation: They want exposure but not betting on immediate breakout

📊 Medium-term (102 days to Apr 17):

- THIS is where the conviction shows - $19 calls positioned for Mexico banking catalyst

- Short $14 puts show they're EAGER to own NU at $14 (21.8% below current) if pullback occurs

- Timeline perfectly captures Q4 earnings (Feb 25) + Mexico activation (Q1-Q2 2026)

- Translation: Bullish on 6.4% rally to $19+ by April, willing to buy dips to $14

🛡️ Long-term (751 days to Jan 2028):

- $13 LEAP puts are CATASTROPHE insurance (Z-score 8,278 = maybe once every few years size)

- Protects against Brazilian macro crisis, U.S. charter denial, regulatory disaster, FinTech sector collapse

- $6.8M premium for 2+ years of protection = 7.6% annual cost - expensive but worth it for large position

- Translation: Very bullish BUT protecting against tail risks that could crater stock to $10-13

This is NOT a "sell everything" signal - it's a "smart positioning ahead of catalysts while managing risk" signal.

If you own NU:

- ✅ HOLD through Mexico catalyst (Q1-Q2 2026) - this is the key value unlock

- 📊 Consider trimming 20-30% at $18+ if breakout occurs - lock in gains, reduce risk

- 🛡️ If holding large position (500+ shares), consider buying protective puts - copy the LEAP insurance strategy at smaller scale

- ⏰ Watch Feb 25 earnings CLOSELY - ARPAC, NIM, and Mexico commentary will set direction for next 6 months

- 🎯 Set mental stop at $16 (below this, support weakens and $14-15 likely)

If you're watching from sidelines:

- ⏰ Best entry: $14-15 range if pullback occurs (institutions willing to buy there, so should you!)

- 📈 Alternative entry: Breakout above $18.50 confirmed (momentum trade to $19-20)

- 🚫 DON'T chase at $17.90 - wait for better setup either direction

- 🎯 Ideal: Sell cash-secured puts at $15 and get paid to wait for pullback (copy conservative trade idea)

- ⏰ Watch Mexico banking activation news - when announced, stock likely gaps $1-2 immediately

If you're bearish:

- ⚠️ Fighting 52% YTD momentum and 84% institutional ownership - dangerous to short

- 📊 First support $17.00 (55.54B gamma) - don't get aggressive until this breaks

- 🎯 Better play: Wait for failed breakout at $18 then short with tight stop at $18.50

- ⏰ Post-earnings (after Feb 25) could offer better risk/reward for bearish positioning if results disappoint

Mark your calendar - Key dates:

- 📅 January 9 (Weekly OPEX) - Minor expiration but watch for $17-18 pin

- 📅 January 16 (Monthly OPEX - JAN CALLS EXPIRE!) - $41M of this position expires, watch for repositioning

- 📅 February 25 (Tuesday) - Q4 2025 Earnings Release - THE catalyst for next major move

- 📅 March 20 (Triple Witch) - Quarterly expiration

- 📅 April 17 (Monthly OPEX - APR CALLS/PUTS EXPIRE!) - Medium-term position layer expires, Mexico catalyst window

- 📅 Q1-Q2 2026 (March-June) - Mexico banking operations activation expected

- 📅 Q3-Q4 2026 - U.S. OCC charter decision window

- 📅 January 21, 2028 - Long-term LEAP puts expiration (2+ years out)

Final verdict: NU's growth story is COMPELLING - 127M customers, 39% revenue growth, 31% ROE, Mexico banking catalyst pending, U.S. expansion planned. The institutional player deploying $41.1M sees significant upside potential to $19-21 by April 2026 driven by Mexico activation, while protecting against catastrophic downside with $13 LEAP puts. The structure shows CONVICTION but also CAUTION - they want exposure but aren't betting the farm without hedges.

For retail traders, the takeaway is clear: NU is a QUALITY fintech stock at a critical inflection point. Wait for Mexico banking activation to materialize (Q1-Q2 2026) before making huge bets. Use pullbacks to $14-15 to build positions at institutional buy levels. Don't chase at all-time highs without protection.

This is a marathon, not a sprint. Let the catalysts develop. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-scores reflect this specific trade's size relative to recent NU history - they do not imply the trade will be profitable or that you should follow it. The institutional trader may have complex portfolio hedging needs, access to information, or risk tolerance not applicable to retail traders. Multi-leg strategies like this carry significant complexity, execution risk, and margin requirements. Always do your own research and consider consulting a licensed financial advisor before trading. NU operates in emerging markets with currency, regulatory, and political risks. The 2-year LEAP puts represent a 7.6% annual cost for protection - expensive insurance that may expire worthless if tail risks don't materialize.

About Nu Holdings Ltd: Nu Holdings Ltd provides digital banking services across Latin America, offering credit cards, personal accounts, investments, personal loans, insurance, mobile payments, business accounts, and rewards to 127 million customers in Brazil, Mexico, and Colombia, with a market cap of $82.47 billion in the digital banking industry.