🚨 NVDA: $27M Synthetic Long - Closing 2028 Calls While Selling Deep OTM Puts!

📅 December 11, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just restructured a $27 MILLION position in NVDA, closing 5,100 deep in-the-money calls at the $250 strike while simultaneously selling 5,000 puts at the $140 strike—both expiring in January 2028! This isn't a simple directional bet; it's a sophisticated synthetic long adjustment by institutional money, likely booking massive profits from their 2028 call position while maintaining bullish exposure through short puts. With NVDA trading at $180, this trader is taking $16M off the table from calls bought when the stock was lower, while selling puts 22% below current price to generate $11M in premium. Translation: They still believe in NVDA long-term but want to lock in gains and reduce position risk.

💼 Company Overview

NVIDIA Corporation (NASDAQ: NVDA)

- Market Cap: $4.47 Trillion (world's most valuable company)

- Sector: Semiconductors - AI Accelerators

- Employees: ~30,000+

- Headquarters: Santa Clara, California

What They Do: NVIDIA designs the GPUs and AI chips that power the artificial intelligence revolution. They command over 90% market share in AI accelerators, with their Blackwell GPU architecture sold out for the next 12 months. Think of them as the arms dealer of the AI gold rush—every major tech company (Google, Microsoft, Meta, Amazon, OpenAI) is buying their chips to train and run AI models. From data centers to autonomous vehicles to gaming, NVIDIA's technology is everywhere.

💰 The Option Flow Breakdown

📊 What Just Happened

Here are the actual trades that crossed the tape:

Trade #1: Closing the Long Call Position

| Date | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Spot Price | Z-Score |

|---|---|---|---|---|---|---|---|---|---|

| 2025-12-11 | NVDA | SELL | CALL | 2028-01-21 | $250 | 5,100 | $16,000,000 | $180.24 | 5.42 |

Trade #2: Opening the Short Put Position

| Date | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Spot Price | Z-Score |

|---|---|---|---|---|---|---|---|---|---|

| 2025-12-11 | NVDA | SELL | PUT | 2028-01-21 | $140 | 5,000 | $11,000,000 | $180.24 | 28.81 |

🔥 Track these options live on Ainvest

🤓 What This Actually Means

Translation for us regular folks:

🐋 Institutional Positioning: This is NOT retail. A $27M combined position represents extreme conviction and sophistication. The Z-Scores tell the story: 5.42 on the call close means this trade is 555 times average size, while 28.81 on the put sell is absolutely off the charts—occurring only a handful of times per year for NVDA options.

💡 The Strategy - Synthetic Long Adjustment: Let's break down what's happening:

Original Position (Established Earlier):

- Owned 5,100 calls at $250 strike (2028 expiration)

- With NVDA at $180, these calls are worth about $16M total

- Assuming they bought these when NVDA was around $200-220, they're sitting on nice profits

New Position (Today's Move):

- Close (Sell) the calls: Take $16M in premium, booking profits

- Sell puts at $140: Generate $11M in premium, 22% below current price

- Net Effect: This creates a synthetic long position - the trader maintains bullish exposure through short puts but with significantly reduced risk and locked-in gains

⏰ Why Now? With NVDA at $180, the stock is consolidating after a massive run. This trader is:

- Taking profits on deep ITM calls that have performed well

- Collecting $11M in put premium at strikes they're comfortable owning NVDA

- Reducing position delta and capital at risk

- Maintaining long-term bullish exposure (short puts = obligation to buy at $140)

📈 Unusualness Analysis:

Call Trade (Z-Score 5.42):

- This is 5.42 standard deviations above normal trading volume

- Translates to a trade occurring maybe 3-5 times per year at this size

- 555x average contract volume - institutional money only

Put Trade (Z-Score 28.81):

- This is absolutely extraordinary - 28.81 standard deviations

- This size of put sale occurs perhaps once or twice per year maximum

- The trader is willing to commit $700 MILLION to buying NVDA at $140 if assigned

- Shows tremendous conviction in NVDA's long-term floor

📈 Technical Setup / Chart Check-Up

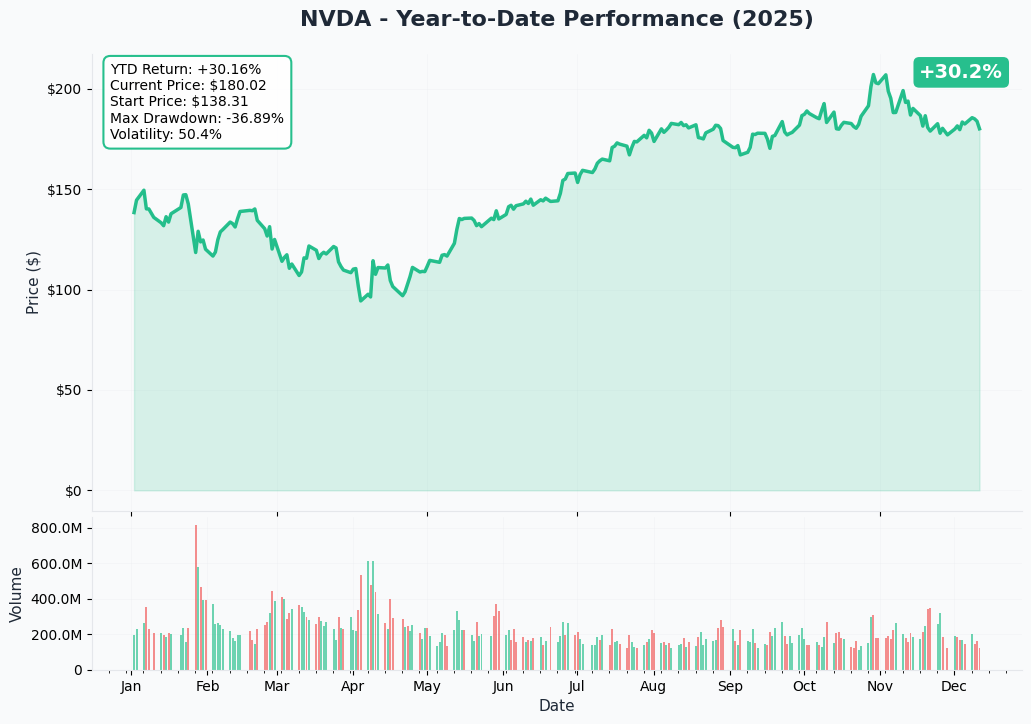

YTD Chart Analysis

What We're Seeing:

NVDA has had a remarkable 2025, but with notable volatility. The stock peaked at $212.19 earlier this year before pulling back to current levels around $180-183. This represents a 15% correction from highs, creating an interesting technical setup.

Key Observations:

- 📊 Consolidation Zone: Trading in a $175-185 range for the past several weeks

- 🎯 Support Holding: The $175-180 zone has been tested multiple times and held

- 💪 Major Support: $160 level represents strong institutional buying

- ⚡ Resistance: $190 and $200 are key levels to reclaim for bulls

- 📉 Pullback From Highs: Down from $212 peak, giving latecomers entry opportunity

Risk Note: The stock is consolidating after a massive AI infrastructure run. This positioning makes sense - taking profits up here while maintaining exposure at significantly lower prices.

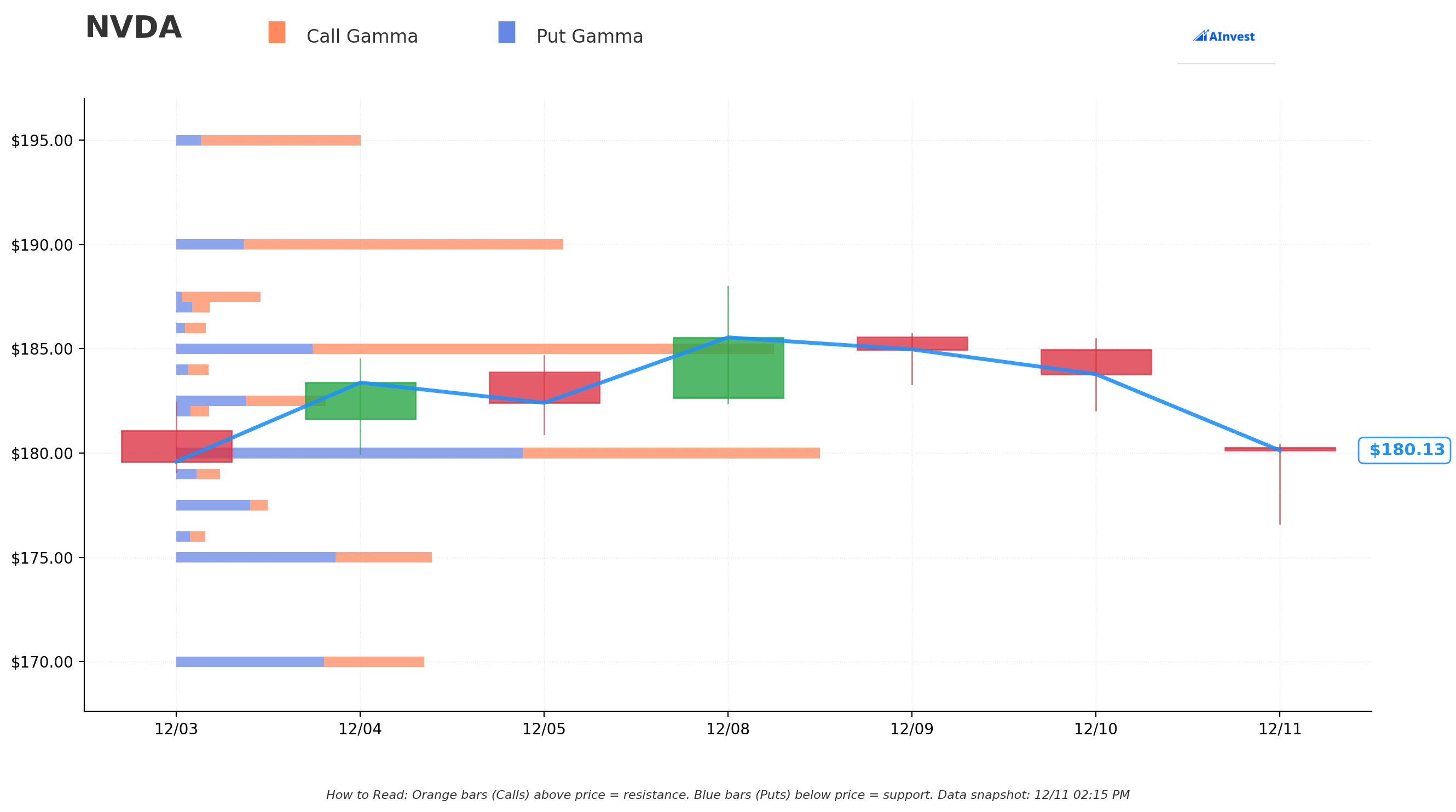

🎯 Gamma-Based Support & Resistance Analysis

What Are Gamma Levels? These are price zones where options dealers have massive exposure. Think of them as invisible force fields - the stock tends to get "sticky" at these levels because market makers have to buy/sell tons of shares to hedge their options positions.

Current Gamma Setup (as of December 11):

🔴 Resistance Levels (Call Gamma Above Price):

| Strike | Net GEX | Distance from Current | Strength |

|---|---|---|---|

| $182.5 | $66.17 | +1.3% | 🔥 Immediate Resistance |

| $185 | $263.67 | +2.6% | 🔥🔥 Very Strong Resistance |

| $190 | $169.88 | +5.4% | 🔥 Strong |

| $195 | $80.18 | +8.2% | Moderate |

| $200 | $131.94 | +10.9% | Strong |

| $210 | $51.67 | +16.5% | Moderate |

🟢 Support Levels (Put Gamma Below Price):

| Strike | Net GEX | Distance from Current | Strength |

|---|---|---|---|

| $180.0 | $280.27 | -0.1% | 🔥🔥🔥 Strongest Support |

| $175 | $110.91 | -2.9% | 🔥 Strong |

| $170 | $107.70 | -5.7% | 🔥 Strong |

| $160 | $74.86 | -11.2% | Moderate |

What This Tells Us:

🎯 Bullish Gamma Bias: Net gamma exposure is $1,326 in calls vs $860 in puts - that's a 54% bullish tilt. Options dealers are positioned for upside, which creates natural buying support as the stock rises.

💪 Massive Support at $180: The $180 strike has the strongest support with $280.27 in total GEX. This is EXACTLY where the stock is trading, creating a powerful anchoring effect. Market makers will defend this level aggressively.

🚀 Resistance Ladder: If NVDA breaks above $182.50, it faces significant resistance at $185 (the strongest resistance level with $263.67 GEX). Clear that level and we have runway to $190 and potentially $200.

😰 Downside Protection: Below $180, we have solid support layers at $175 and $170. Our whale's short put at $140 sits well below these levels - they're protected by multiple gamma support zones.

The Whale's Perspective: Selling puts at $140 makes perfect sense given this gamma structure. The stock would need to crash through FOUR major gamma support levels ($180, $175, $170, $160) before even approaching their short put strike. That's a 22% decline with massive institutional support zones in the way.

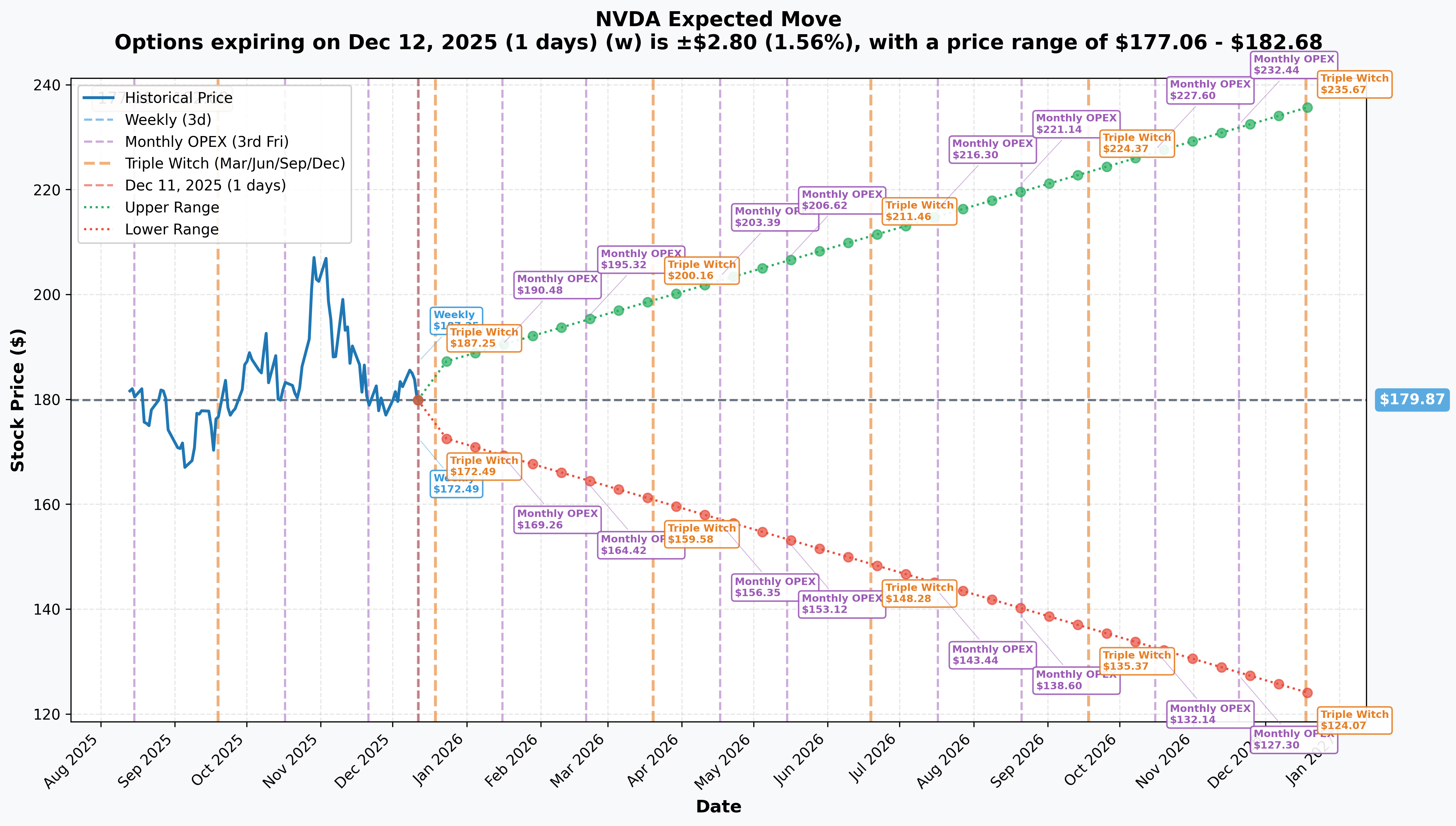

📊 Implied Move Analysis

What Is Implied Move? This shows how much the options market expects the stock to move by various expiration dates. It's basically the market's "best guess" baked into option prices.

Current Implied Moves (Based on $180.24 Stock Price):

📅 Weekly (December 12 Expiry - Tomorrow!):

- Implied Move: ±1.56% or ±$2.81

- Expected Range: $177.06 to $182.68

- Translation: The market expects NVDA to stay in a tight range this week, consistent with the current consolidation pattern.

📅 Monthly OPEX (December 19 - Next Week):

- Implied Move: ±3.8% or ±$6.84

- Expected Range: $173.03 to $186.71

- Translation: By next Friday's option expiration, the market prices in a $7 range - still relatively contained given NVDA's recent volatility.

📅 December 2026 LEAPS (1-Year Out):

- Implied Move: ±31.02% or ±$55.91

- Expected Range: $124.07 to $235.67

- Translation: Over the next year, options price in potential moves to either $236 (bull case) or $124 (bear case) - a massive range reflecting AI uncertainty.

📅 January 2028 LEAPS (Our Whale's Expiration!):

- Implied Move: Based on volatility modeling, approximately ±45-50%

- Expected Range: Roughly $90 to $270

- Translation: Over 3 years to expiration, the market anticipates enormous uncertainty. The $140 put strike sits comfortably within the lower boundary, while still 55% below current price.

What This Tells Us:

⚡ Low Near-Term Volatility: The weekly and monthly implied moves are surprisingly small for NVDA - just 1.56% and 3.8%. This suggests the market expects consolidation, not fireworks.

🎯 Our Trade Makes Sense: The whale's $140 put is 22% below current price and would require NVDA to:

- Fall below the 1-year lower boundary ($124)

- Decline 55% from current levels

- Break through multiple gamma support zones

- Violate the entire AI infrastructure thesis

💰 Premium Collection Strategy: By selling 3-year puts at $140, this trader is collecting $11M in premium for taking on risk at a level they're clearly comfortable with. If NVDA never touches $140 (likely scenario), they keep the entire premium.

📊 Asymmetric Risk/Reward: The trader took $16M off the table from calls (booking profits) and collected $11M from puts. Even if assigned at $140, their effective cost basis is $140 - $2.20 (premium per share) = $137.80 for a stock currently trading at $180. That's a 23% discount.

🎪 Catalysts

🔥 Recent Developments (Last 3 Months)

Q3 FY2026 Earnings Blowout (November 20, 2025):

The catalyst backdrop for NVDA is exceptional. Here's what's driving the story:

📊 Record-Breaking Results:

- Revenue: $57.0 billion (+62% YoY, +22% QoQ) - per NVIDIA Investor Relations

- EPS: $1.30 (beat estimates by 4%, exceeding $1.25 consensus) - per Captide

- Data Center Revenue: $51.2 billion (89.8% of total revenue, up 66% YoY)

- Gross Margins: 73.4% (GAAP), maintaining exceptional profitability

🚀 Q4 FY2026 Guidance:

- Revenue expected: $65.0 billion (±2%) - per NVIDIA Investor Relations

- Gross margins expected: 75.0% (non-GAAP, improving)

- Stock rose 2.85% aftermarket on announcement

💬 CEO Commentary: "Blackwell sales are off the charts, and cloud GPUs are sold out. Compute demand keeps accelerating and compounding across training and inference — each growing exponentially. We've entered the virtuous cycle of AI." - Jensen Huang, per NVIDIA Investor Relations

🤝 Strategic Developments

Synopsys Partnership (December 1, 2025):

- NVIDIA announced $2 billion investment in Synopsys common stock - per NVIDIA Newsroom

- Integration of AI and accelerated computing with chip-design software

- Enables faster, more precise chip design at lower cost

AWS Partnership Expansion (December 2, 2025):

- Full-stack partnership integrating NVIDIA NVLink Fusion and Blackwell architecture - per TS2 Space

- Deepens relationship with largest cloud provider

Microsoft and Anthropic Partnership (December 2025):

- Anthropic scaling Claude AI model on Microsoft Azure, powered by NVIDIA - per NVIDIA Newsroom

- Expands enterprise AI capabilities across Azure customer base

Toyota Automotive Partnership (January 2025 - CES):

- Toyota building next-gen vehicles on NVIDIA DRIVE AGX Orin - per TechCrunch

- Automotive revenue expected to grow to ~$5 billion in FY2026 - per NVIDIA Newsroom

🇨🇳 China Export Policy Developments

H200 Export Approval (December 8-9, 2025):

- U.S. government reversed course on AI chip export restrictions - per TechCrunch

- Department of Commerce approved H200 chip exports to China under 25% fee regime

- H200 is NVIDIA's second-best AI chip, significantly more advanced than H20

- Only H200 chips approximately 18 months old allowed for export

Congressional Opposition:

- Senators introduced Secure and Feasible Exports Act on December 4, 2025 - per Bloomberg

- Bill would block advanced AI chip exports to China for 30+ months

- Creates ongoing regulatory uncertainty

China's Counter-Response:

- Beijing set to limit access to H200 chips despite Trump approval - per Yahoo Finance

- Leading Chinese AI firms (ByteDance, Alibaba) sought immediate orders when window opened - per StartupHub AI

Blackwell Chips Remain Banned:

- U.S. maintains ban on Blackwell chip exports to China - per CNBC

- Smuggling efforts exposed in "Operation Gatekeeper" - per CNBC

📅 Upcoming Catalysts (Next 6 Months)

Q4 FY2026 Earnings Report (Expected Late February 2026):

- Based on historical schedule, likely February 23-27, 2026 - per Wall Street Horizon

- Company Guidance: $65 billion revenue target

- Analyst Consensus: $61.66 billion revenue, $1.43 EPS (prior to guidance raise)

- Key Metrics to Watch:

- Blackwell production ramp and revenue contribution

- Data center revenue growth trajectory

- China revenue impact from H200 export approval

- Q1 FY2027 guidance and full-year outlook

Blackwell Production Scaling (Q1-Q2 2026):

- Production ramping with 350 plants manufacturing 1.5 million components - per Manufacturing Dive

- Current status: Blackwell sold out for next 12 months - per Tom's Hardware

- Expected volume: 750,000-800,000 units by Q1 2025 - per TweakTown

- Revenue potential: FY2026 datacenter compute revenue projected at $154.7 billion, with 80% from Blackwell - per IFP

GeForce RTX 50 Series Rollout (January-February 2025):

- RTX 5090 and 5080 launch January 30, 2025 - per CES

- RTX 5070 Ti and 5070 launch February 2025

- Built on Blackwell architecture, up to 2x performance improvement - per TechFundingNews

- Gaming revenue expected to benefit from upgrade cycle

Project DIGITS Launch (May 2025):

- Personal AI supercomputer with GB10 Grace Blackwell - per Techloy

- $3,000 price point targeting 4+ million CUDA developers

- Enables running AI models with up to 200 billion parameters

- Potential to expand developer ecosystem and CUDA moat

Automotive Revenue Acceleration (Throughout 2025):

- Toyota partnership vehicle production ramp

- Aurora commercial driverless truck launch April 2025 - per NVIDIA Investor Relations

- Automotive revenue target: ~$5 billion for FY2026 (vs. $1.7B in FY2025)

📊 Analyst Activity

Current Consensus:

- Average 12-month price target: $250.93 (range: $140-$352) - per MacroTrends

- Alternative consensus: $255.86 (range: $139.38-$454.42) - per GuruFocus

- StockAnalysis consensus: $242.43 representing +32.80% upside - per Stock Analysis

- 60 of 64 analysts recommend buying shares, 11 with Strong Buy ratings - per MarketBeat

Recent Upgrades:

- Citigroup, J.P. Morgan, Morgan Stanley maintained Buy-equivalent ratings - per Benzinga

- Evercore ISI holds street-high target, citing accelerating revenue growth and Blackwell demand

- Last upgrade: HSBC raised price target to $320 on October 15, 2025 - per Zacks

Post-Earnings Analysis:

- Bank of America analyst Vivek Arya expects FY2026 EPS of $4.56 - per Nasdaq

- Increased FY2027 EPS guidance to $7.02 (from $6.26) and FY2028 to $9.15 (from $8.03)

- NVIDIA has exceeded consensus in 19 of past 21 quarters - per Kiplinger

🎲 Price Targets & Probabilities

Based on gamma levels, implied move analysis, catalyst timing, and analyst targets, here are the likely scenarios:

🚀 Bull Case: $210-225 (16-25% Upside)

Timeline: 3-6 months Probability: 35%

What Needs to Happen:

- ✅ Q4 earnings beat $65B revenue target with strong Blackwell commentary

- ✅ Blackwell production scales successfully through Q1-Q2 2026

- ✅ China H200 export approval generates incremental $5-10B revenue

- ✅ FY2027 guidance raises Street estimates toward BofA's $7.02 EPS target

- ✅ Clear $185 gamma resistance and reclaim $190-200 levels

Why This Works: NVIDIA is executing flawlessly with Blackwell sold out 12 months in advance and data center revenue up 66% YoY. The AI infrastructure buildout is real—management expects $3-4 trillion in spending over next 5 years with NVIDIA commanding 90%+ market share.

Strategic partnerships with Synopsys ($2B investment), Toyota (automotive ramp to $5B), and AWS/Microsoft provide diversification. The recent H200 China export approval could recover $50B in long-term revenue.

Key Levels:

- First target: $195 (analyst support zone)

- Primary target: $210-215 (reclaim YTD highs)

- Stretch target: $225 (toward $251 consensus)

⚖️ Base Case: $175-190 (Range-Bound)

Timeline: 1-3 months Probability: 45%

What Needs to Happen:

- ✅ Earnings meet $65B guidance but don't blow it out

- ✅ Stock oscillates between $180 support and $185-190 resistance

- ✅ Continued consolidation as market digests the recent run

- ✅ Blackwell production meets expectations without major surprises

- ✅ China export situation remains in flux

Why This Makes Sense: NVDA is sitting right at the $180 gamma support level ($280.27 total GEX), with strong resistance at $185 ($263.67 GEX). The weekly implied move of just 1.56% and monthly move of 3.8% suggest the market expects consolidation, not fireworks.

The stock is down 15% from the $212 peak, creating a healthy consolidation zone. With 68.98% institutional ownership and massive positions from Vanguard, BlackRock, and State Street, large holders are likely fine with stabilization here before the next leg higher.

Regulatory uncertainty around China exports and competitive pressure from AMD (now powering 30% of new cloud AI deployments) keep some investors cautious.

Trading Strategy: This scenario favors the whale's approach—selling puts at strikes you're comfortable owning. The $140 put (22% below current price) represents excellent risk/reward if you believe in NVDA long-term.

Key Levels:

- Support: $180 (strongest gamma support)

- Midpoint: $182.50 (immediate resistance)

- Resistance: $185-190 (major gamma resistance zone)

😰 Bear Case: $140-165 (13-22% Downside)

Timeline: 2-6 months Probability: 20%

What Needs to Happen:

- ❌ Earnings disappoint or Blackwell production delays materialize

- ❌ China export restrictions tighten further (Blackwell ban extended, H200 approval reversed)

- ❌ Major hyperscaler announces AI capex cuts or shift to competitors

- ❌ Broader tech sector correction on Fed policy or recession fears

- ❌ AMD/Intel competition accelerates faster than expected

What Could Go Wrong: The GB200 NVL72 production delays could impact revenue through Q2 2025. Blackwell thermal management flaws forced hyperscalers to consider rivals, and memory supply constraints (LPDDR pivot) create "seismic shift" in supply chain.

Geopolitically, the U.S.-China trade war cost NVIDIA $5.5B in inventory write-downs and risks $50B in long-term China revenue (10-15% of data center segment). If the bipartisan bill blocking exports for 30+ months passes, that revenue is gone.

Competitively, AMD's MI300X now powers 30% of new cloud AI deployments, Intel's Gaudi3 offers 30% cost advantage, and hyperscalers developing in-house chips could erode NVIDIA's 92-94% market share.

Notable bearish view: Renowned investor Michael Burry is bearish on NVIDIA, citing regulatory headwinds and China uncertainty.

Key Levels:

- First support: $175 (gamma support #2)

- Critical support: $170 (gamma support #3)

- Major support: $160 (historical strong level)

- Ultimate support: $140 (our whale's put strike, 22% below current)

The Whale's Protection: Notice that the $140 put strike sits well below the 1-year implied move lower boundary ($124). Even in a severe bear scenario, NVDA would need to fall 22% to reach this level, breaking through four major gamma support zones ($180, $175, $170, $160). That's a catastrophic scenario, not a correction.

💡 Trading Ideas

🛡️ Conservative: The "China Hedge" Put Spread

For traders worried about geopolitical risks

Strategy: Buy Jan 2026 $170 Put / Sell Jan 2026 $160 Put

The Setup:

- Buy protection at $170 (just below current gamma support)

- Sell the $160 put to finance the hedge

- Protects against China export reversal or earnings disappointment

- Max profit if NVDA falls to $160 or below

Cost/Risk:

- Net debit: ~$3.50-4.00 per contract ($350-400 total)

- Max loss: $350-400 per contract (if NVDA stays above $170)

- Max profit: ~$600-650 per contract (if NVDA at $160 or below)

- Breakeven: ~$166 (lower strike + debit paid)

Why This Works: You're hedging against the binary risks (China export ban reversal, Blackwell production delays, earnings miss) without paying for expensive at-the-money puts. The $170-160 zone represents strong gamma support—if NVDA breaks below $170, it could accelerate to $160.

Risk Management:

- Size this as portfolio insurance (2-5% of long NVDA position)

- Exit if NVDA breaks convincingly above $190 (hedge no longer needed)

- Consider rolling to lower strikes if NVDA approaches $170

Best For: Existing NVDA shareholders who want cheap protection against tail risks, or traders expecting consolidation but worried about downside catalysts.

⚖️ Balanced: The "Whale Lite" Short Put

For traders who want to copy the institutional strategy with smaller size

Strategy: Sell Jan 2026 $160 Put (naked or cash-secured)

The Setup:

- Similar thesis to whale's $140 put, but shorter duration and closer strike

- Collect premium for obligation to buy NVDA at $160 (11% below current)

- If assigned, you own NVDA at an effective cost basis of ~$154-156 (after premium)

Cost/Risk:

- Premium collected: ~$4.50-5.50 per contract ($450-550 per put)

- Max loss: Substantial (if NVDA goes to zero, theoretically $16,000 per contract)

- Obligation: Must buy 100 shares at $160 if assigned (requires $16,000 cash or margin)

- Breakeven: ~$154.50-155.50 (strike - premium collected)

Why This Works: You're getting paid $450-550 to commit to buying NVDA at $160, which is:

- 11% below current price ($180)

- Sitting right at the $160 gamma support level

- 13% below the $185 consensus analyst target

- 36% below the $251 average price target

If NVDA never hits $160, you keep the entire premium (3-3.4% return in 5 weeks). If you do get assigned, you own a world-class company at a significant discount during a temporary pullback.

Profit Scenarios:

- NVDA stays above $160 by Jan 16 = Keep full $450-550 premium (3-3.4% return)

- NVDA at $165 by Jan 16 = Keep full premium

- NVDA at $155 by Jan 16 = Assigned at $160, effective cost ~$155 (still 14% below current)

- NVDA at $140 by Jan 16 = Assigned at $160, effective cost ~$155 (unrealized loss ~10%)

Risk Management:

- CRITICAL: Only do this if you WANT to own NVDA at $160

- Must have $16,000 cash per contract (for cash-secured puts)

- Or adequate margin if selling naked (not recommended for most traders)

- Exit/roll if NVDA approaches $170 and shows weakness

- Consider taking profits at 50% max gain (~$225-275)

Best For: Bullish traders with capital who want to either collect premium or own NVDA at a discount. You must be comfortable holding 100 shares per contract.

🚀 Aggressive: The "Blackwell Breakout" Call Spread

For traders betting on Q4 earnings catalyst and Blackwell momentum

Strategy: Buy Jan 2026 $185 Call / Sell Jan 2026 $205 Call

The Setup:

- Targets the $185 gamma resistance breakout

- Spread caps max profit at $205 but reduces cost significantly

- January expiration gives 5+ weeks for thesis to develop

- Profits if NVDA reclaims $190-200 levels post-earnings

Cost/Risk:

- Net debit: ~$6.50-7.50 per contract ($650-750 total)

- Max loss: $650-750 per contract (if NVDA below $185 at expiration)

- Max profit: ~$1,250-1,350 per contract (if NVDA at $205+)

- Breakeven: ~$191.50-192.50 (lower strike + debit paid)

- Probability of profit: ~40%

Why This Is Aggressive But Smart: You're betting on NVDA breaking through the $185 gamma resistance (strongest call wall) and heading toward the $210-215 zone where it traded earlier this year. The catalyst is clear:

- Q4 Earnings (Late Feb 2026): $65B revenue guidance, Blackwell commentary

- Analyst Support: Average target of $251, with BofA projecting $7.02 FY2027 EPS

- Technical Setup: Stock has consolidated for weeks at $180, setting up for breakout

- Blackwell Ramp: Production scaling in Q1-Q2 could provide positive surprises

If NVDA beats earnings, confirms Blackwell is ramping smoothly, and provides strong FY2027 guidance, the stock could easily hit $195-205 by January expiration. You're risking $650-750 to make $1,250-1,350 - that's a 1.7x to 2x return.

Profit Scenarios:

- NVDA at $205+ by Jan 16 = +67% to 108% gain (max profit ~$1,300)

- NVDA at $200 by Jan 16 = +35% to 65% gain (~$500-900 profit)

- NVDA at $195 by Jan 16 = +10% to 30% gain (~$150-400 profit)

- NVDA at $190 by Jan 16 = -20% to -40% loss

- NVDA at $180 by Jan 16 = -100% loss (full debit)

Risk Management:

- Only risk capital you can afford to lose completely

- Exit at 50-75% profit (don't get greedy waiting for max profit)

- Cut losses if NVDA breaks below $175 and stays there

- Consider taking partial profits at $195 and letting runners go to $205

Best For: Bullish traders with high conviction in the AI infrastructure thesis who believe Q4 earnings will be a positive catalyst. You're making a directional bet on upside momentum, not just "NVDA goes up eventually."

⚠️ Risk Factors

Let's keep it real - here's what could derail the bullish thesis:

📉 Execution Risks

1. Blackwell Production Delays (MODERATE-HIGH RISK) The GB200 NVL72 production delays could extend into Q2 2025, impacting revenue recognition. Blackwell thermal management flaws forced Microsoft and Meta to evaluate alternatives. While NVIDIA claims these are resolved, any further hiccups would be devastating.

Why It Matters: Blackwell represents 80% of FY2026 datacenter revenue ($154.7B projected). A 1-quarter delay in 10% of shipments = ~$12B revenue miss. At 47x forward P/E, that's a potential 15-20% stock correction.

2. Supply Chain Bottlenecks (MODERATE RISK) CoWoS packaging capacity constraints and memory supply issues (LPDDR pivot creates "seismic shift") limit production scale. Reliance on external foundries (TSMC) means NVIDIA doesn't control its destiny.

The Risk: Suppliers worried about overbuilding expensive capacity - adding capacity takes 2-3 years. If demand surges beyond expectations (good problem) but supply can't keep up, NVIDIA loses sales to competitors.

3. Demand Normalization (LOW-MODERATE RISK) AI infrastructure buildout is unprecedented, but what if it slows? Market cap has cooled from $5T peak as AI sentiment became more volatile. If hyperscaler capex moderates or AI monetization disappoints, demand could normalize faster than Street expects.

🤺 Competitive Threats

1. AMD Gaining Market Share (MODERATE RISK) AMD's MI300X now powers 30% of new cloud AI deployments, up from negligible share 2 years ago. They've more than doubled total customers in first 9 months of 2025 and are on track for 40% server CPU market share by year-end.

The Competitive Wedge: AMD offers 30% cost advantage for LLM training vs H100. For cost-conscious customers, "good enough" performance at 70% of the price is compelling. AMD outperformed NVDA in 2025 stock performance, signaling shifting sentiment.

2. Hyperscaler In-House Development (MODERATE-LONG TERM RISK) Cloud providers developing custom AI chips to reduce NVIDIA dependence. Google TPUs, AWS Trainium, Microsoft Maia all represent threats. If internal chips reach 80-90% of NVIDIA performance, why pay NVIDIA's premium?

Mitigation: NVIDIA's CUDA ecosystem with 4+ million developers creates massive switching costs. But over 3-5 years, hyperscalers could make the investment.

3. Intel's Gaudi3 and Emerging Competitors (LOW-MODERATE RISK) Intel's Gaudi3 offers 30% cost advantage, though performance lags. More concerning: Tenstorrent raised $700M at $2.6B+ valuation, OpenAI exploring own chips, and Huawei Ascend 910C claims 60% of H100 inference performance.

⚖️ Geopolitical & Regulatory Landmines

1. U.S.-China Trade War Escalation (HIGH RISK) This is the elephant in the room. NVIDIA has already suffered:

- $5.5B inventory write-down from H20 export ban

- Potential $50B long-term revenue loss from China (10-15% of data center)

- U.S. AI Diffusion Rule banned H20 exports (effective May 15, 2025)

Recent Developments:

- ✅ POSITIVE: H200 export approval with 25% fee

- ❌ NEGATIVE: Beijing limiting H200 access despite U.S. approval

- ❌ NEGATIVE: Bipartisan bill seeking 30+ month export block

- ❌ NEGATIVE: Blackwell chips remain banned

The Risk: If the Secure and Feasible Exports Act passes, NVIDIA loses China for 30+ months. That's $10-15B annual revenue GONE. Even worse: China could retaliate by banning NVIDIA entirely, accelerating Huawei/domestic alternatives.

2. China Antitrust Probe (LOW-MODERATE RISK) China's antitrust investigation doesn't block market access but creates operational uncertainty and potential fines. Signals risk of regulatory pushback and price volatility.

3. Congressional Scrutiny (MODERATE RISK) Smuggling operations like "Operation Gatekeeper" ($160M worth of H100/H200 GPUs to China) trigger Congressional hearings. Increased compliance costs and reputational risk.

📊 Valuation & Macro Risks

1. Premium Valuation Compression (MODERATE-HIGH RISK) At 45.37x forward P/E, NVDA trades at significant premium to semiconductor peers (20-30x). The stock is priced for flawless execution of 60%+ AI growth. Any miss triggers violent multiple compression.

Historical Context: NVDA has corrected 20-30% multiple times during bull markets when growth expectations weren't met. Current $4.47T market cap (world's largest company) creates "too big to sustain" narrative.

2. Interest Rate Sensitivity (MODERATE RISK) High-growth tech valuations compress when rates rise. If Fed holds rates higher for longer or inflation re-accelerates, NVDA's premium multiple won't hold. A 100-200 bps rate increase could drive 15-25% decline purely from valuation reset, independent of fundamentals.

3. AI Bubble Fears (LOW-MODERATE RISK) Market increasingly questioning AI ROI. If enterprises don't adopt AI fast enough or monetization disappoints, infrastructure spending decelerates sharply. The market cap cooling from $5T peak reflects this skepticism.

The Scary Scenario: AI bubble pops, hyperscalers cut capex 40%, NVDA's revenue growth crashes from 60% to 10-15%, and we find out how much of the $4.47T valuation was hype vs. fundamentals. Stock could realistically trade back to $100-120 (where it was in early 2023).

4. Insider Selling Signals (LOW RISK, BUT NOTABLE) CEO Jensen Huang sold 200,000+ shares at $175.91-$182.70 in July 2025. While insiders receive RSUs and sell regularly, the timing raises eyebrows. Are they taking profits at peak?

🎯 Binary Event Risk

Q4 FY2026 Earnings (Late February 2026):

This is make-or-break for the bull thesis. NVIDIA has beat estimates in 19 of past 21 quarters, but the bar keeps rising.

Bull Case Triggers:

- Blackwell revenue exceeds $10B (implies strong ramp)

- FY2027 guidance confirms $7+ EPS trajectory

- China H200 revenue contribution mentioned positively

- No production delay commentary

Bear Case Triggers:

- Revenue misses $65B target or guidance is cautious

- Blackwell delays mentioned explicitly

- Hyperscaler demand moderation hinted

- Margin pressure from competition

The Bottom Line on Risk: The $140 put strike makes sense because it assumes NVDA could fall 22% in worst-case scenario while still maintaining long-term value. That's realistic—NVDA has corrected 15-25% multiple times during bull runs. But it also assumes the company's fundamental dominance (90%+ market share, Blackwell ramp, CUDA moat) remains intact. If the AI thesis breaks entirely, even $140 might not hold.

🎯 The Bottom Line

Real talk: This $27M position restructuring is one of the most sophisticated trades I've seen in NVDA options. The trader isn't gambling—they're managing a massive winner while maintaining long-term exposure.

Here's what I think is happening:

👀 The Whale's Thesis: This institutional trader likely bought the $250 calls when NVDA was trading around $200-220 (early-to-mid 2024). With the stock now at $180, those calls are worth substantially more than paid (intrinsic value alone). Rather than hold the entire position through potential volatility, they're:

- Booking Profits: Taking $16M off the table from the calls (profit realization)

- Generating Income: Collecting $11M in put premium at strikes 22% below current price

- Maintaining Exposure: The short $140 puts keep them long NVDA via synthetic position

- Reducing Risk: If NVDA corrects to $140-160, they're obligated to buy at a massive discount

- Increasing Flexibility: With $27M in premium collected, they can redeploy capital elsewhere

The Z-Scores Tell the Story:

- Call close: 5.42 = 555x average size, occurring a few times per year

- Put sale: 28.81 = absolutely extraordinary, maybe once or twice annually

- Combined: This is institutional-grade capital allocation, not speculation

📊 What The Charts Say:

NVDA is sitting right at $180 gamma support (strongest level with $280.27 GEX), having pulled back 15% from the $212 peak. This consolidation is healthy after massive run. The gamma structure shows:

- Clear support: $180, $175, $170, $160 (four major levels before $140)

- Resistance: $185 (strongest), $190, $200 (need to reclaim)

- Bullish bias: $1,326 call GEX vs $860 put GEX = 54% bullish tilt

The $140 put sits 22% below current price and would require breaking through ALL major gamma support levels. That's a catastrophic scenario, not a correction.

🎪 Catalyst Calendar:

The setup for bulls is exceptional:

- ✅ Q4 Earnings (Late Feb 2026): $65B revenue target, Blackwell commentary

- ✅ Blackwell Ramp (Q1-Q2 2026): 750k-800k units/quarter, sold out 12 months

- ✅ GeForce RTX 50 (Jan-Feb): Gaming revenue boost from Blackwell launch

- ✅ Project DIGITS (May): $3k supercomputer expands CUDA ecosystem

- ✅ China H200 Exports: Potential $5-10B incremental revenue recovery

- ✅ Analyst Support: $251 average target, 60 of 64 analysts Buy-rated

⚠️ But Here's The Rub:

The risks are real and material:

- Execution Risk: Blackwell delays, thermal issues, memory constraints

- Geopolitical Risk: $50B China revenue at stake, Congressional export bans

- Competitive Risk: AMD at 30% of new cloud deployments, hyperscaler in-house chips

- Valuation Risk: 45x forward P/E prices in perfection, AI bubble fears

- Macro Risk: Fed policy, recession fears, tech sector correction

My Take:

🚀 If You're Bullish (35% conviction): The AI infrastructure buildout is real, NVIDIA's 90%+ market share is defensible via CUDA moat, and Blackwell ramp provides 2-year visibility. Play it with defined-risk spreads (Aggressive strategy) targeting $195-210. Don't buy naked calls—use spreads to cap risk.

😐 If You're Neutral (45% conviction - BASE CASE): Expect consolidation between $175-190 for next 1-3 months as market digests recent run and awaits earnings clarity. The gamma trap at $180 support / $185 resistance creates range-bound trading. Consider selling puts at $160-165 (Balanced strategy) to collect premium, or iron condors at $175-190 range for theta decay.

😰 If You're Bearish (20% conviction): NVDA is priced for perfection after massive run. Any earnings miss, Blackwell delay, or China export reversal triggers 15-25% correction to $140-155. Buy protective puts at $170-175 (Conservative strategy) or wait for better entry after volatility.

What I'm Watching:

- Q4 earnings (late Feb): Must hit $65B revenue, confirm Blackwell ramp

- Blackwell production updates: Any delay commentary is red flag

- China export policy: H200 sales momentum, Congressional bill progress

- AMD market share: If they cross 35-40% of new deployments, narrative shifts

- Hyperscaler capex guidance: Microsoft, Google, Meta Q1 guidance (Jan-Feb)

- Gamma levels: Watch for $180 support break or $185 resistance breakout

Mark Your Calendar:

- January 30, 2025: GeForce RTX 5090/5080 launch (gaming catalyst)

- February 2025: RTX 5070 Ti/5070 launch

- Late February 2026: Q4 FY2026 earnings (CRITICAL)

- May 2025: Project DIGITS launch

- Q1-Q2 2026: Blackwell production scaling

- January 21, 2028: Expiration of whale's $27M trade

Final Thought:

The whale who repositioned this $27M isn't panicking—they're being prudent. They've locked in $16M in gains from calls while collecting $11M in put premium at strikes they're comfortable owning. You can play a similar thesis with smaller size:

- Conservative: Buy put spreads at $170-160 as hedge ($350-400 risk)

- Balanced: Sell puts at $160 to collect premium ($450-550 income)

- Aggressive: Buy call spreads at $185-205 targeting breakout ($650-750 risk)

But respect the risks. NVDA trades at $4.47 trillion market cap with 45x forward P/E. This isn't a deep value play—it's a growth stock priced for AI dominance. If fundamentals crack, the downside is swift and severe.

The beauty of this trade: Even if NVDA falls to $140 (22% decline), the whale gets to buy a world-class company at a massive discount with an effective cost basis of ~$137-138 after premium collected. That's 24% below current price for a stock analysts target at $251.

This is how institutional money thinks: probabilities, risk management, and asymmetric payoffs. Not "will NVDA go up?" but "what's my risk-adjusted return across multiple scenarios?"

Trade smart, not big. 🎯

⚖️ Disclaimer

Options trading involves substantial risk and is not suitable for all investors. The value of options can fluctuate rapidly, and you can lose your entire investment. Selling puts creates obligation to buy stock at strike price, which can result in substantial capital requirements and losses if stock declines significantly.

This analysis is for informational and educational purposes only - it is NOT financial advice. The author may hold positions in securities mentioned. Always conduct your own research and consult with a licensed financial advisor before making investment decisions.

Key Risks:

- Options can expire worthless, resulting in total loss of premium paid

- Short puts create obligation to buy stock, requiring substantial capital

- NVDA is highly volatile and can gap up/down significantly on news

- Gamma exposure levels change throughout the day - they are not static

- Implied moves are estimates, not guarantees - actual moves can be larger or smaller

- Geopolitical, competitive, and regulatory risks could materially impact stock price

- Past performance (19 of 21 quarters beating) does not guarantee future results

Do your own due diligence. Never risk more than you can afford to lose. Understand the obligations and capital requirements of short puts before trading. 🎯