🚀 NVDA Massive $249M Calendar Spread Signals Q1 2026 Breakout Bet

📅 December 22, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed a $249M calendar spread on NVIDIA, buying 50,000 March 2026 $160 calls while simultaneously selling 50,000 February 2026 $170 calls. This sophisticated institutional trade expects NVDA to consolidate near current levels through February OpEx before exploding past $170 into the March 20 triple witch expiration - perfectly timed around GTC 2026 conference and Q4 earnings. With the stock at $183, this isn't a directional bet - it's a volatility play banking on major catalysts in Q1 2026.

💰 The Option Flow Breakdown

📊 What Just Happened

Today's massive NVDA option activity shows institutional players making a calculated bet on upcoming catalysts:

🐋 Trade #1: Long March 2026 $160 Calls

- Premium: $152M (50,000 contracts @ $30.40)

- Expiration: March 20, 2026 (88 days out - Quarterly Triple Witch)

- Strike: $160 (12.7% below current price)

- Time: 09:44:39 ET

- Chart: View March $160 Call

🐋 Trade #2: Short February 2026 $170 Calls

- Premium: $97M (50,000 contracts @ $19.35)

- Expiration: February 20, 2026 (60 days out - Monthly OpEx)

- Strike: $170 (7.2% below current price)

- Time: 09:44:39 ET

- Chart: View February $170 Call

Net Debit: $55M for the full calendar spread position

🤓 What This Actually Means

This is a calendar spread - a professional volatility strategy that profits from time decay and volatility expansion. Here's the playbook:

The Short-Term View (February): By selling February $170 calls, the trader collects $97M in premium, betting the stock stays below $170 through February 20 OpEx. This short leg funds more than half the cost of the long position.

The Long-Term Setup (March): The March $160 calls gain value from two sources: (1) time decay working in their favor after February expiration, and (2) volatility expansion around GTC 2026 conference (March 16-19) and any post-earnings momentum.

Why This Works: If NVDA trades sideways or slightly down through mid-February, the short calls expire worthless, leaving the trader with March $160 calls at a massive discount. Then, if major announcements at GTC 2026 or strong Q4 earnings drive the stock higher, those March calls could explode in value.

Translation: Big money expects relative calm through February earnings, followed by significant volatility and upside into March. They're essentially getting paid $97M to wait for the real fireworks at GTC 2026.

📈 Technical Setup

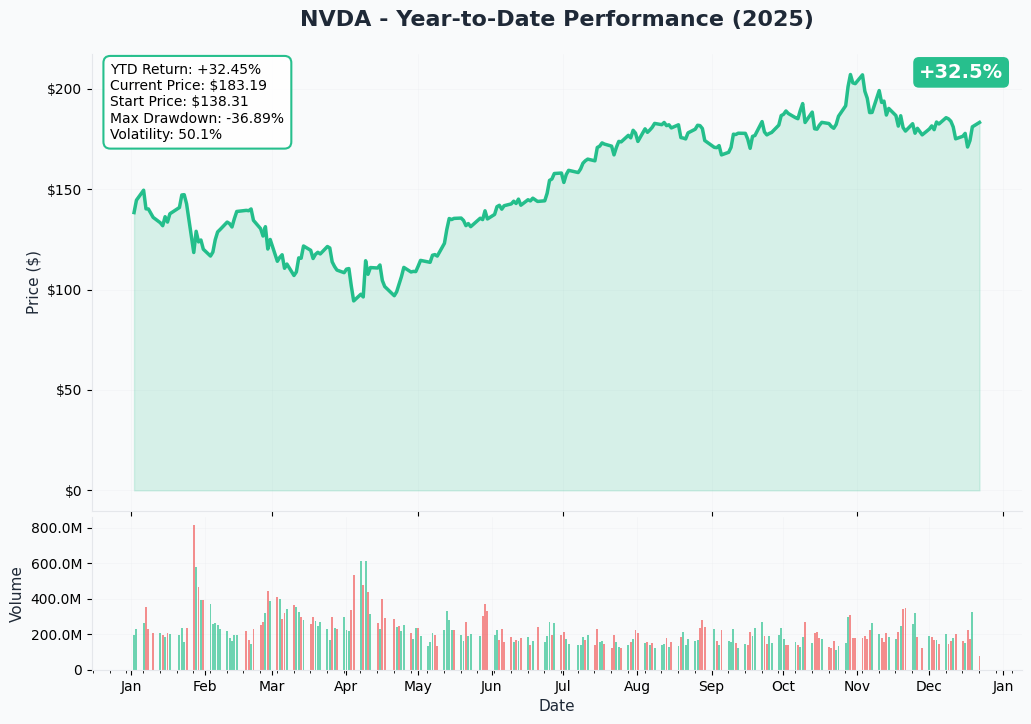

YTD Performance Overview

NVIDIA has had a rollercoaster 2025, hitting an all-time high of $212.19 on October 29 before pulling back to current levels around $183. The stock is down about 14% from those highs, trading in a consolidation pattern that's built strong support in the $175-180 zone. This pullback has come despite stellar fundamentals - Q3 revenue of $57B (up 62% YoY) and "sold out" Blackwell GPU inventory through 2026.

The current technical picture shows NVDA digesting gains after the massive AI-driven rally, with volume declining and implied volatility compressing. This sets up perfectly for the calendar spread strategy - low volatility now with major catalysts ahead that could reignite momentum.

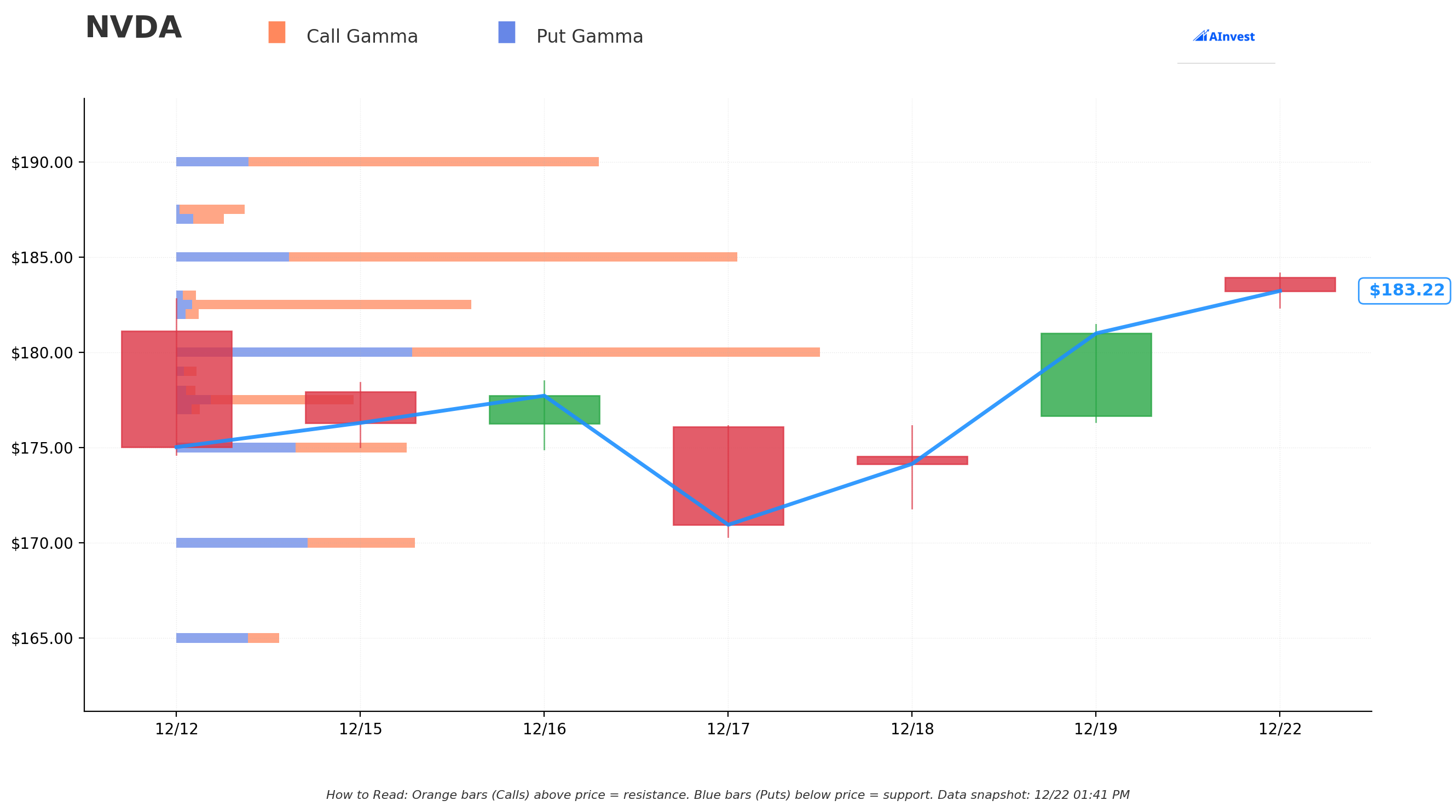

🎯 Gamma-Based Support & Resistance Analysis

Current Price: $183.29

Key Resistance Levels:

- $185 (Strongest Resistance): Net GEX of $125.8M with $167.8M in call gamma creates a strong ceiling just $1.71 above current price (0.9% away). This is where market makers turn from buyers to sellers, creating natural selling pressure.

- $190: Net GEX of $104.5M marks the next major barrier at 3.7% above current levels - a key psychological level that's proven difficult to reclaim.

- $195-$200: Lighter resistance zone with $55.8M-$97.8M net GEX, representing the bull case targets if momentum builds.

Key Support Levels:

- $182.50 (Strongest Support): Net GEX of $98.2M with massive call gamma ($103.9M) creates the immediate floor, just $0.79 below current price (0.4% away).

- $180: Heavy support with $239.4M total GEX (combining $151.6M call and $87.8M put gamma) - this is the line in the sand at 1.8% down.

- $175-$177.50: Deeper support zone with net GEX turning negative, showing put gamma dominance that would trigger dealer buying below these levels.

Net GEX Bias: Bullish - Total call gamma of $1.3B vs. put gamma of $582.3M shows markets are positioned for upside, creating a supportive dealer flow environment.

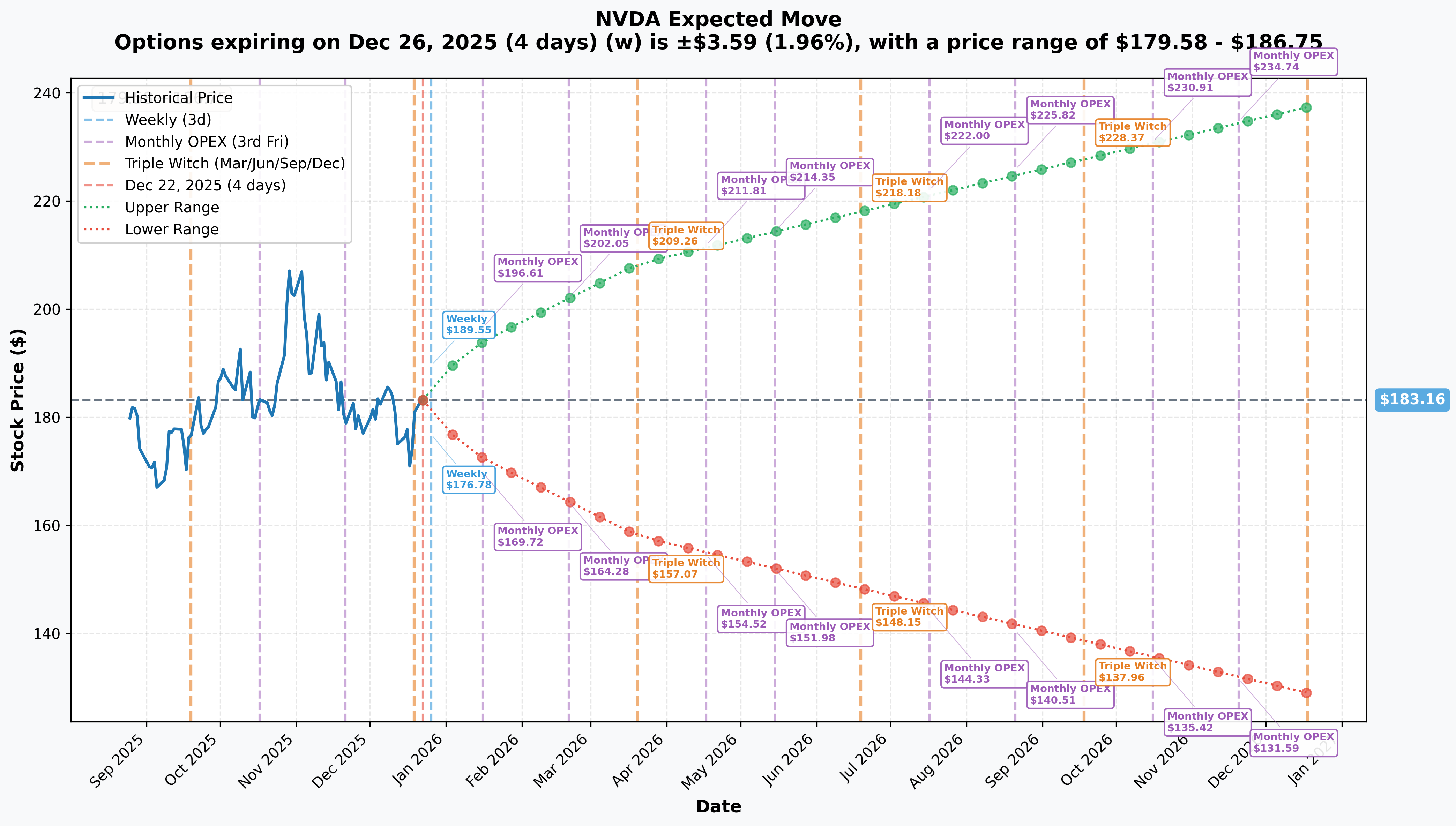

📊 Implied Move Analysis

The options market is pricing in significant movement across all timeframes, with volatility expanding the further out you look:

Weekly (December 26 Expiration - 4 days):

- Implied Move: ±1.96% (±$3.59)

- Range: $179.58 - $186.75

- Analysis: Tight expected range through year-end suggests quiet holiday trading with dealers keeping prices pinned.

Monthly OpEx (January 16, 2026 - 25 days):

- Implied Move: ±5.97% (±$10.94)

- Range: $172.22 - $194.11

- Analysis: Markets expect modest volatility through January, well below recent historical moves. This aligns with the calendar spread thesis of relative calm before storms.

Quarterly Triple Witch (March 20, 2026 - 88 days):

- Implied Move: ±13.78% (±$25.24)

- Range: $157.92 - $208.41

- Analysis: This is where it gets interesting. The March expiration (same as the long leg of our whale trade) prices in major two-way risk, with the upside target of $208 representing 13.5% gains from current levels. GTC 2026 conference (March 16-19) falls right before this expiration, explaining the elevated volatility expectations.

Yearly LEAPS (December 2026 - 361 days):

- Implied Move: ±29.61% (±$54.23)

- Range: $128.94 - $237.39

- Analysis: Long-term options price in extraordinary uncertainty, reflecting both the massive AI growth opportunity and significant execution/geopolitical risks. The $237 upside target implies 29% gains, while the $129 downside shows markets haven't forgotten NVDA can correct sharply.

Key Insight: The implied move structure validates the calendar spread strategy - relatively low volatility near-term (5.97% by January OpEx) followed by significant expansion into March (13.78%). This is exactly the volatility term structure that calendar spreads profit from.

🎪 Catalysts

🔜 Upcoming Catalysts

Q4 Fiscal 2026 Earnings (February 25, 2026):

- Timing: After market close, Wednesday

- Guidance: $65B revenue (±2%), exceeding Street consensus of $61.66B by $3.3B

- Gross Margin Guidance: 74.8% GAAP, 75% non-GAAP (±50 bps)

- Why It Matters: This is the first earnings report where Blackwell revenue contribution becomes material. Management has guided for Blackwell to exceed Hopper revenue in Q1 FY2027, making Q4 the critical inflection quarter. Expect intense focus on production ramp progress, supply chain bottlenecks, and China policy impacts.

- Calendar Spread Impact: Falls between the two legs of our whale trade. If results are strong but stock doesn't immediately rally (taking time to digest guidance), the short February $170 calls expire worthless while March calls retain optionality for the post-earnings drift higher.

NVIDIA GTC 2026 Conference (March 16-19, 2026):

- Location: San Jose, California (SAP Center)

- Historical Significance: GTC has been the launchpad for every major NVIDIA architecture announcement for the past decade. Jensen Huang's keynotes routinely move the stock by billions in market cap.

- Expected Announcements:

- Next-generation architecture preview (potentially "Blackwell Ultra" or successor architecture)

- Major cloud partnership expansions

- New automotive/robotics platform announcements

- VC Alliance networking for NVIDIA Inception startups

- Why It Matters: This is THE catalyst event for NVIDIA. Markets typically begin pricing in GTC announcements 2-3 weeks ahead, with follow-through momentum lasting weeks after. Historical pattern shows elevated volatility surrounding the conference.

- Calendar Spread Impact: Occurs just 4 days before March 20 expiration (the long leg). This is no coincidence - the trade is explicitly positioned for GTC-driven volatility expansion.

China Export Policy Resolution (Mid-January 2026):

- Background: Trump administration announced a 30-day inter-agency review to potentially allow H200 chip sales to China with 25% revenue tax

- Deadline: Approximately January 15-20, 2026

- Potential Impact:

- Bullish scenario: H200 approval adds $3-5B annual revenue opportunity

- Neutral scenario: Status quo maintained, no change

- Bearish scenario: Congressional "Secure and Feasible Exports Act" blocks exports for 30 months

- Why It Matters: China geopolitical risk remains the biggest uncertainty hanging over NVDA. The company already took $5.5B in charges for H20 restrictions. Any resolution removes a major overhang, even if the outcome is negative (certainty is better than uncertainty for options traders).

Q1 Fiscal 2027 Earnings (Expected May 28, 2026):

- Preliminary Consensus: $0.93 EPS, up 52.46% YoY

- Why It Matters: First quarter where Blackwell revenue should exceed Hopper, validating the architecture transition

- Calendar Spread Impact: Falls well after March expiration, but guidance on this call will drive March option values leading into expiration

✅ Already Happened (Context for Current Setup)

Q3 Fiscal 2026 Results (Reported November 19, 2025):

- Revenue: $57.0B, up 62% YoY and 22% QoQ - massive beat

- EPS: $1.30, exceeding consensus of $1.25 by 4%

- Data Center Revenue: Record $51.2B, up 66% YoY

- Market Reaction: Stock rose 4% in after-hours but failed to sustain gains, retreating from October highs

- Key Takeaway: Fundamentals are extraordinary, but stock needs new catalysts to break out of consolidation - exactly what the calendar spread is positioned for

Blackwell Production Ramp:

- Current Status: Production ramped from 250,000-300,000 units in Q4 2024 to projected 750,000-800,000 units in Q1 2025, a 3x increase

- Demand: Entire 2025 production already sold out by November 2024 per Morgan Stanley

- Pricing: B200 chips command 60-70% premium over H200 predecessor

- Latest: RTX PRO 5000 72GB Blackwell GPU became generally available December 18, 2025

GeForce RTX 5000 Series Launch (January 2025):

- Products: RTX 5090 ($1,999) and RTX 5080 ($999) launched January 30, 2025

- Technology: 32GB GDDR7 memory, 21,760 CUDA cores, DLSS 4 with up to 8x frame rate enhancement

- Challenge: Launch faced stock shortages and price gouging due to exceptional demand

🎲 Price Targets & Probabilities

Based on the convergence of gamma levels, implied move ranges, and upcoming catalysts, here's how the next 3 months could play out:

🐂 Bull Case: $200-$208 by March 20 (35% probability)

Path: NVDA consolidates through January around $180-185, then Q4 earnings on February 25 delivers another beat with strong Blackwell commentary. Stock breaks through $185 resistance into the $190s, then GTC 2026 announcements (March 16-19) provide the catalyst to push toward $200+.

Supporting Factors:

- Gamma resistance at $200 ($97.8M net GEX) is lighter than lower levels, suggesting breakout potential if momentum builds

- Implied move for March expiration ($208.41 upper range) aligns with this scenario

- Analyst consensus price target of $252-260 implies significant upside expectations

- 86.67% Strong Buy ratings from 39 of 45 analysts shows Wall Street conviction

- $500B hyperscaler spending visibility over next 14 months provides demand certainty

Calendar Spread Outcome: Maximum profit scenario. February $170 calls expire worthless (stock at $170-185 through Feb OpEx), March $160 calls gain substantial intrinsic value ($40-48 per contract if stock at $200-208), turning the $55M net debit into $145-185M profit.

📊 Base Case: $175-$190 range (45% probability)

Path: Stock trades in a wide range through Q1, respecting strong gamma support at $180 and resistance at $185-190. Q4 earnings are solid but not inspiring enough for immediate breakout. GTC 2026 provides temporary spike but no sustained follow-through.

Supporting Factors:

- Strongest gamma levels create $180-185 "pin zone" where dealers keep prices stable

- Implied move for January OpEx ($172-194 range) suggests this is market's base expectation

- Historical pattern shows NVDA consolidates after major earnings beats to digest gains

- Supply chain bottlenecks (GDDR7 shortages could cut RTX production 40%, GB200 delays) create execution uncertainty

- China policy resolution provides clarity but no material upside

Calendar Spread Outcome: Moderate profit. February $170 calls expire worthless (stock below $170 at Feb OpEx), leaving March $160 calls purchased at effective cost of $11 per contract ($55M net debit / 50,000 contracts). If stock at $180-190 in March, calls worth $20-30, generating $45-95M profit on the $55M investment.

🐻 Bear Case: $160-$175 (20% probability)

Path: Broader market correction or NVDA-specific negative catalyst (China export ban, earnings disappointment, AMD competitive threat) drives stock down to test deep support levels. Gamma support at $180, $175, and $170 slow the decline but don't stop it.

Supporting Factors:

- At $4.46T market cap, NVDA is world's most valuable company, priced for perfection with limited margin for error

- Congressional opposition to H200 exports could trigger 30-month ban, removing $3-5B revenue opportunity

- Gaming segment already showing weakness (down 1% sequentially in Q3) despite RTX 5000 launch

- AMD's OpenAI deal for 6 gigawatts of MI300 GPUs signals viable competition emerging

- Broader tech multiple compression could hit high-flyer valuations hardest

Calendar Spread Outcome: Limited profit or small loss. Both legs could end in-the-money if stock declines sharply. However, the $160 strike provides strong downside protection - even at $165, the March calls retain $5 intrinsic value ($250M), well above the $55M net debit. The spread structure limits losses compared to outright calls.

💡 Trading Ideas

🛡️ Conservative: Ride the Gamma Range (Sleep Well Strategy)

Strategy: Sell put spreads at strong gamma support levels to collect premium while NVDA consolidates.

Specific Trade:

- Sell Jan 16, 2026 $175 Put @ $3.50

- Buy Jan 16, 2026 $170 Put @ $2.20

- Net Credit: $1.30 per spread ($130 per contract)

- Max Risk: $3.70 per spread ($370 per contract)

- Risk/Reward: 2.8:1

Why This Works:

- $175 strike sits right at strong gamma support ($85.3M total GEX) and matches lower end of January implied move range ($172.22)

- Need stock to stay above $175 (4.5% below current price) over next 25 days - high probability given technical support

- January expiration comes before Q4 earnings (Feb 25), avoiding event risk

- Even if stock dips to $170, you're protected by the long put leg

Probability of Success: ~75% (based on current price $183 with strong support at $180 and $175)

Best For: Traders who believe NVDA stays range-bound through January and want steady income without directional risk.

⚖️ Balanced: Mini Calendar Spread (YOLO with Training Wheels)

Strategy: Replicate the whale trade structure on a smaller scale, positioning for post-earnings volatility expansion.

Specific Trade:

- Buy 10x March 20, 2026 $170 Calls @ $22.00 = $22,000

- Sell 10x February 20, 2026 $180 Calls @ $12.50 = $12,500

- Net Debit: $9,500

Why This Works:

- Same calendar spread logic as the $249M whale trade, just with strikes closer to current price for more delta exposure

- February $180 calls (~2% away) likely expire worthless if stock consolidates post-earnings

- March $170 calls (~7.2% below current) gain value from time decay advantage + GTC 2026 volatility

- Breakeven on full spread: Stock above $179.50 at March expiration

- Maximum profit zone: Stock at $180-190 at Feb expiration, then rallies to $190-210 by March

Probability of Success: ~55% (requires stock above $179.50 by March 20, with optimal outcome if it moves higher after February OpEx)

Best For: Swing traders who want exposure to GTC 2026 catalysts while funding half the cost through near-term premium collection.

🚀 Aggressive: Leveraged Call Ratio Spread (Shoot for the Moon)

Strategy: Express strong conviction in March volatility expansion with asymmetric risk/reward.

Specific Trade:

- Buy 20x March 20, 2026 $180 Calls @ $18.00 = $36,000

- Sell 10x March 20, 2026 $195 Calls @ $9.50 = $9,500

- Net Debit: $26,500

Why This Works:

- 2:1 ratio spread gives you double the upside participation up to $195

- $180 strike sits at major gamma support - if stock is here, it's likely to move higher

- Maximum profit at $195 at expiration:

- Long calls worth: 20 × $15 = $30,000

- Short calls worthless

- Total profit: $3,500 on $26,500 risk = 13% gain

- But real profit potential is if stock lands $185-193 at expiration:

- At $190: Long calls worth $20,000, short calls worth zero = $6,500 loss

- At $188: Long calls worth $16,000, short calls worth zero = $10,500 loss

Wait, this doesn't look aggressive enough - let me recalculate for moon-shot scenario:

Aggressive Trade (Revised):

- Buy 30x February 20, 2026 $190 Calls @ $8.50 = $25,500

- Max Loss: $25,500 (if stock below $190 at Feb OpEx)

- Max Gain: Unlimited above $190

- Breakeven: $198.50

Why THIS Works:

- All-in bet that Q4 earnings (Feb 25) + pre-GTC momentum drives stock through $190 resistance

- If news breaks early on China policy approval or Blackwell production acceleration, could see explosive move

- 30x leverage means every $1 above $198.50 = $3,000 profit

- At $200: $11,500 profit (45% gain)

- At $210: $41,500 profit (163% gain)

- Risk is total loss if stock stays below $190 through earnings - but you've got strong technical support below to limit downside to stock itself

Probability of Success: ~35% (needs 3.7% rally to $190 by Feb 20, or 8.5% to breakeven at $198.50)

Best For: Risk-tolerant traders who believe Q4 earnings will be a blowout catalyst and want maximum leverage on that outcome.

⚠️ Risk Factors

Let's be real about what could derail this trade:

🌊 Execution Risks

Supply Chain Bottlenecks Keep Getting Worse: The most immediate threat isn't market sentiment - it's NVIDIA's ability to deliver products. GB200 NVL72 production has been repeatedly delayed, now pushed to Q2 2025 with shipment estimates cut from 50,000-80,000 racks down to 25,000-35,000. Meanwhile, GDDR7 memory shortages could force a 40% cut in RTX 50-series production during H1 2026.

What This Means: If Q4 earnings reveal that Blackwell revenue contribution is lower than expected due to production constraints, the stock could sell off despite strong demand. Markets are forward-looking - constrained supply means leaving money on the table.

Impact on Calendar Spread: Both legs could lose value if volatility crashes on disappointing guidance. The $55M net debit could turn into a total loss if NVDA drops below $160 and stays there.

🌏 Geopolitical Landmines

China Policy Uncertainty Isn't Priced In: The Trump administration's 30-day review of H200 exports to China creates a binary outcome in mid-January. If Congressional legislation blocks exports for 30 months, NVDA loses a potential $3-5B annual revenue opportunity. Worse, China is already evaluating ways to restrict H200 chip access even if U.S. approves sales, and mandated state-funded datacenters to eliminate foreign AI chips by 2027.

What This Means: The calendar spread expires March 20 - right when the full implications of China policy become clear. A negative resolution could cap upside momentum heading into GTC 2026.

TSMC Geopolitical Risk: NVIDIA's entire supply chain runs through TSMC facilities located ~100 miles from mainland China. Any escalation in Taiwan tensions could trigger violent moves in either direction.

🏢 Competitive Threats

AMD Is No Longer a Joke: AMD signed a deal with OpenAI to deploy 6 gigawatts of MI300 GPUs, with first gigawatt going live H2 2026. This is the first time a tier-1 AI company has meaningfully committed to non-NVIDIA silicon. AMD's Q3 revenue grew 36% YoY to $9.2B, and they're pricing MI300 aggressively below NVIDIA's Blackwell.

Hyperscalers Building Custom Silicon: NVIDIA's biggest customers are simultaneously becoming competitors. Amazon's Trainium and Inferentia, Google's TPU, and Microsoft's Maia chips are designed specifically to reduce NVIDIA dependency for inference workloads. While NVIDIA still dominates training, the inference market could fragment rapidly.

What This Means: If Q4 or Q1 guidance shows any indication that datacenter revenue growth is decelerating due to competitive pressure, the multiple could compress violently. At 76x forward P/E (rough estimate based on current levels), there's no margin for error.

📉 Valuation Reality Check

NVDA Is the Most Valuable Company in the World: At $4.46 trillion market cap, NVIDIA is priced for absolute perfection. The company is on track to report more net income this year than AMD and Intel's combined sales. That's extraordinary - but it also means any stumble gets punished severely.

The Gaming Segment Is Already Cracking: Q3 gaming revenue was $4.265B, down 1% sequentially despite the RTX 5000 launch. This suggests that segment has peaked, which is fine when datacenter is growing 66% YoY - but what happens when that growth inevitably slows?

🎢 Volatility Collapse Risk

The Calendar Spread Needs Volatility Expansion: This trade is built on the assumption that implied volatility expands into March (GTC 2026). But if the conference is a dud, or if Q4 earnings are so good that all uncertainty disappears, implied volatility could collapse. Calendar spreads lose money when vol crashes across the board.

What Could Cause Vol Collapse:

- Q4 earnings so strong that the bull case is validated and uncertainty evaporates

- China policy resolution (even negative outcome) removes overhang

- Broader market rally that lifts all boats, reducing single-stock vol

Impact: Both legs lose value, and the time decay advantage of owning March vs. selling February disappears.

🎯 The Bottom Line

Real talk: This $249M calendar spread is one of the most sophisticated option trades we've seen on NVDA this year. It's not a directional bet - it's a volatility and timing play that recognizes where NVDA is in its catalyst cycle.

Here's the deal: The stock has pulled back 14% from October highs despite reporting a blowout Q3 ($57B revenue, up 62% YoY) with entire 2025 GPU production already sold out. That's textbook consolidation before the next leg higher. The calendar spread structure tells you that big money expects:

- Relative calm through February → Stock stays below $170 through Feb 20 OpEx, short calls expire worthless

- Catalyst-driven breakout into March → GTC 2026 (March 16-19) or strong Q4 earnings momentum drives stock toward $190-200+, March $160 calls become deeply ITM

Three scenarios for your playbook:

📈 If You Own NVDA Stock: The gamma support levels at $182.50 and $180 (combined $338M in GEX) should hold during normal market conditions. Use them as your stop-loss guide. If we break below $180 on volume, next support isn't until $175-177.50. But above $180, path of least resistance is toward $185 resistance. Consider selling covered calls against your shares at the $190 or $195 strikes for February expiration to collect premium during the consolidation phase.

👀 If You're Watching from Sidelines: Mark your calendar for three key dates:

- Mid-January 2026: China export policy decision (30-day review deadline)

- February 25, 2026: Q4 FY2026 earnings after close

- March 16-19, 2026: GTC 2026 conference

Any one of these could be the catalyst that breaks NVDA out of its current $175-190 range. The implied move for March ($157.92-$208.41 range) tells you options market is pricing in significant two-way risk.

🐻 If You're Bearish: The calendar spread structure actually shows you where smart money thinks downside is limited - they're comfortable owning $160 calls because they don't expect NVDA to trade much below that level even in a correction. Combine that with $252-260 average analyst price targets and 86.67% Strong Buy ratings, and you're fighting against significant institutional conviction. If you're bearish, you better have a strong fundamental thesis (supply chain collapse, China export ban, competitive share loss, AI spending pullback) - because technical and sentiment aren't on your side.

The Play: For retail traders, the balanced calendar spread strategy (buy March $170 calls, sell February $180 calls for $9,500 net debit on 10 contracts) offers the best risk/reward. You get to play the same thesis as the whale trade without needing $55M in capital, and your strikes are closer to current price for better delta exposure.

Final Warning: Options are leveraged instruments that can go to zero. The calendar spread mitigates some risk through the short leg, but you can still lose 100% of your investment if NVDA craters below $160 or if volatility collapses across the board. Size your position accordingly - this shouldn't be more than 5-10% of your options portfolio.

⚠️ Disclaimer: This analysis is for educational purposes only and not financial advice. Options trading involves substantial risk and may not be suitable for all investors. Past performance does not guarantee future results. Always conduct your own due diligence and consider consulting a financial advisor before making investment decisions.

🔗 Learn More:

- NVIDIA Stock Analysis

- NVIDIA Interactive Chart

- Understanding Calendar Spreads - Investopedia

- Options Greeks Explained - CBOE

Analysis Date: December 22, 2025 | NVDA Stock Price: $183.29 Total Option Premium: $249M | Number of Trades: 2 Market Cap: $4.46T | 52-Week Range: $86.62 - $212.19