💎 NVDA $124M Institutional Call Bonanza - Smart Money Loads Up Before 2026! 🚀

📅 December 23, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $124 MILLION on NVDA calls this morning across two massive trades! First, $73M on deep in-the-money $50 calls expiring January 16th (38 days out), then another $51M on $160 calls expiring March 20th (87 days). With NVDA trading at $188.47 and sitting on a $4.46 trillion market cap, institutional players are making their biggest bullish bets of the year right before critical Q4 earnings (Feb 25) and the game-changing GTC 2025 conference in March. Translation: Smart money believes NVDA's AI dominance story accelerates into 2026!

📊 Company Overview

NVIDIA Corporation (NVDA) is the undisputed king of AI infrastructure, powering over 90% of cloud-based AI workloads globally:

- Market Cap: $4.46 Trillion (world's most valuable company)

- Industry: Semiconductors & Related Devices (Graphics Processing Units & AI Computing)

- Current Price: $188.47 (down 11% from October ATH of $207.03, up 33% YTD)

- Primary Business: AI-optimized GPUs (Blackwell, Hopper), CUDA software platform, data center networking solutions

- Key Customers: Microsoft, Google, Meta, Amazon, Tesla, OpenAI, Oracle, xAI

💰 The Option Flow Breakdown

The Tape (December 23, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | Strategy | Z-Score | Spot | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:30:15 | NVDA | ASK | BUY | CALL $50 | 2026-01-16 | $73M | $50 | 10,000 | Long Call | 11.62 | $188.47 | NVDA20260116C50 |

| 10:48:09 | NVDA | ASK | BUY | CALL $160 | 2026-03-20 | $51M | $160 | 16,000 | Long Call | 3.24 | $188.47 | NVDA20260320C160 |

Combined Premium: $124,000,000

🤓 What This Actually Means

These are two distinct institutional strategies targeting different catalysts over the next 3 months:

Trade #1: The $73M Deep ITM Mega-Position (January 16 expiration)

- 💸 Massive capital deployment: $73M for 10,000 contracts of $50 strike calls

- 🎯 Deep in-the-money: Strike at $50 vs. stock at $188.47 = $138.47 intrinsic value per share

- 📊 Leverage with safety: These calls have ~99 delta (move nearly 1:1 with stock) with 38 days until expiration

- ⏰ Strategic timing: Expires 8 days BEFORE Q4 earnings on Feb 25 - locks in position through January monthly OPEX

- 🏦 Institution replicating shares: This is essentially buying 1,000,000 shares ($188M notional) with only $73M capital deployed

- 🔥 Unusualness: Z-score of 11.62 means this is 11.6 standard deviations above normal - happens maybe twice a year

Trade #2: The $51M Strike Selection Play (March 20 expiration)

- 💰 Targeted positioning: $51M for 16,000 contracts at $160 strike

- 🎯 Out-of-the-money bet: Strike $28.47 below current price (15% cushion), betting on rally to $200+ by expiration

- 📈 Catalyst coverage: Expires AFTER Q4 earnings (Feb 25) AND GTC 2025 conference (March 17-21)

- 🚀 Risk-defined speculation: Maximum profit if NVDA explodes to $220+, breakeven around $185-190 depending on entry price

- ⏰ 87 days to expiration: Gives time for Blackwell ramp, sovereign AI deployments, and Rubin architecture announcements at GTC

- 🎢 Gamma exposure: At-the-money-ish strike provides maximum leverage if stock surges above $200

What's really happening here:

This looks like TWO DIFFERENT institutional traders (or desks within the same fund) expressing bullish views with different risk/reward profiles:

-

Conservative long (Trade #1): Deep ITM calls act like leveraged stock ownership - the trader wants full upside exposure with minimal time decay. They're essentially holding a massive long position (1M shares) but only putting up $73M instead of $188M. This position profits from ANY upward movement and holds most intrinsic value even if NVDA trades sideways through January. Think of it as margin-efficient share ownership.

-

Aggressive speculation (Trade #2): OTM calls betting on a 15-20% rally into March driven by earnings beat and GTC announcements. This trader is paying $51M for the RIGHT to explosive gains if NVDA breaks out to new all-time highs above $210. Maximum leverage play - if NVDA hits $220 by March 20, these calls could be worth $90-100M (80%+ gain). This is conviction that Q4 earnings will be a blowout.

Combined thesis: Both trades signal institutions believe NVDA's current $188 level represents a BUYING OPPORTUNITY after the 11% pullback from October highs. The January trade hedges near-term consolidation risk while the March trade swings for the fences on earnings and GTC catalysts.

Unusual Score: 🔥 EXTREME for both trades! The January $50 calls posted a Z-score of 11.62 (occurs less than once per year), while the March $160 calls scored 3.24 (highly unusual, ~97th percentile). We're talking about position sizes 324x and 1,162x their normal averages. Combined $124M premium is among the largest single-day bullish NVDA bets we've tracked in 2025.

📈 Technical Setup / Chart Check-Up

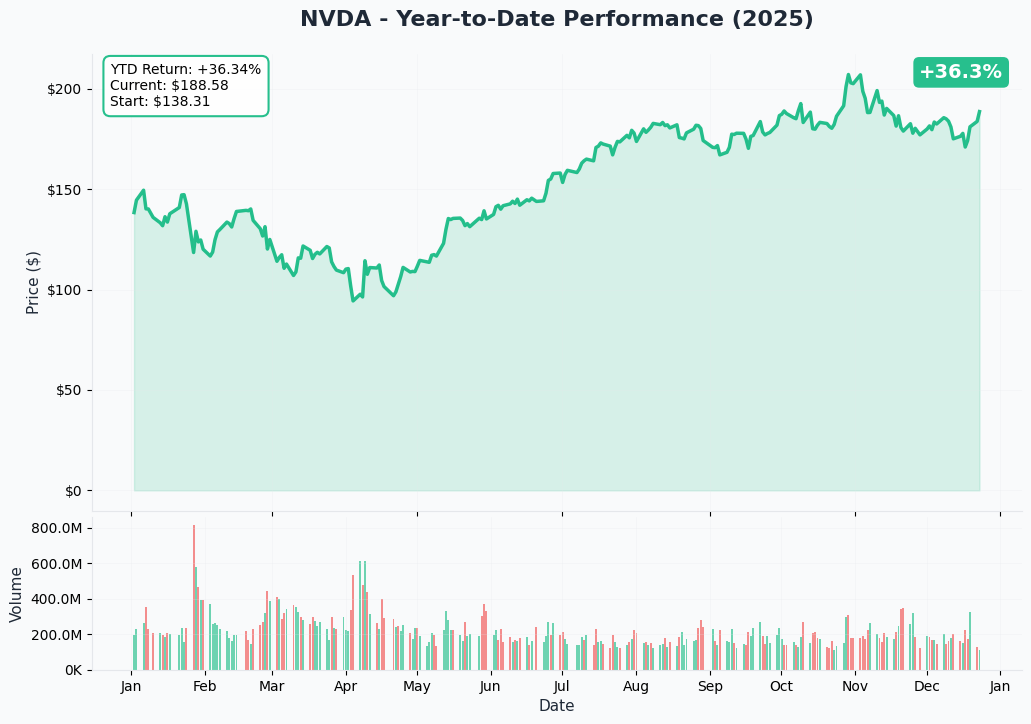

YTD Performance Chart

NVDA is up +33% YTD at $188.47, but don't let that fool you - this stock has been on an absolute rollercoaster. Starting the year at $141.60, NVDA rocketed to an all-time high of $207.03 on October 29th before pulling back 11% to current levels. The chart shows a powerful AI infrastructure buildout story that took a breather in Q4.

Key observations:

- 🚀 Explosive rally: From $141 in January to $207 in October = 46.2% surge in 10 months on Blackwell momentum

- 📈 Higher lows: Every meaningful dip ($155 in April, $165 in June, $175 in Sept) got bought aggressively - institutions accumulating

- 🎢 Consolidation mode: Trading in $185-195 range since November after pulling back from ATH

- 📊 Volume confirmation: Massive institutional volume in August-October during the breakout to $200+

- ⚠️ Recent pressure: Down 11% from peak despite fundamentals strengthening - suggests positioning for next leg up

The YTD chart screams "healthy pullback in a sustained uptrend" - exactly the type of setup where smart money adds size.

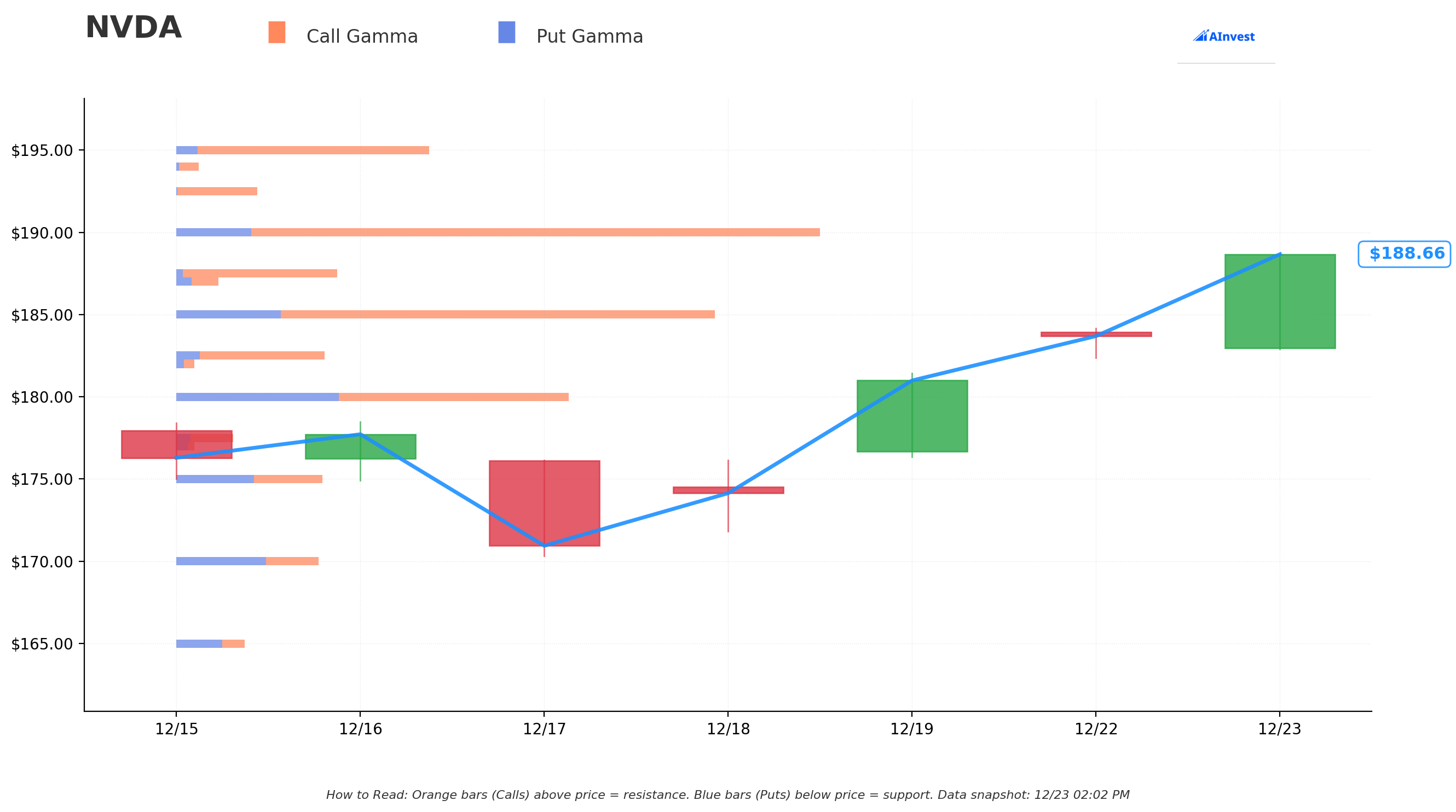

Gamma-Based Support & Resistance Analysis

Current Price: $188.47

The gamma exposure map reveals massive dealer positioning that will govern price action through Q1 2026:

🔵 Support Levels (Put Gamma Below Price):

- $152.50 - MAJOR PUT WALL with 350.0M gamma (this is THE floor - dealers will defend aggressively)

- No significant put gamma between $152.50 and current price - clean air below if $152.50 breaks (unlikely)

🟠 Resistance Levels (Call Gamma Above Price):

- $235 - Strong resistance at 235.0M gamma (24% above current - first major ceiling)

- $320 - Secondary resistance at 320.0M gamma (70% rally required - extended target)

- $330 - Tertiary resistance at 330.0M gamma (75% upside - blow-off scenario)

- $340 - Major ceiling zone at 340.0M gamma (80% gain needed)

- $350 - HIGHEST CALL GAMMA at 350.0M (dealers will systematically sell into rallies here)

What this means for traders:

NVDA has an ASYMMETRIC gamma profile - massive put support at $152.50 (19% below current) but minimal call resistance until $235 (24% above). This creates a "spring-loaded" setup where the path of least resistance is HIGHER. Market makers have huge put exposure at $152.50, meaning they'll BUY shares aggressively on any dip toward that level to hedge their short puts. Conversely, the lack of meaningful call gamma between $188 and $235 means less mechanical selling pressure on rallies.

Notice the March call buyer's positioning? The $160 strike calls sit comfortably ABOVE the $152.50 put wall, suggesting they believe that level is rock-solid support. If NVDA rallies to $235 by March expiration, those $160 calls would be worth $75 each ($120M value on a $51M bet - 135% gain!).

Net GEX Bias: BEARISH on paper (negative net gamma), but this is misleading. The concentration of puts at $152.50 vs. spread-out calls from $235-$350 actually creates bullish dealer hedging dynamics. As long as NVDA stays above $170, dealers are net buyers of rallies.

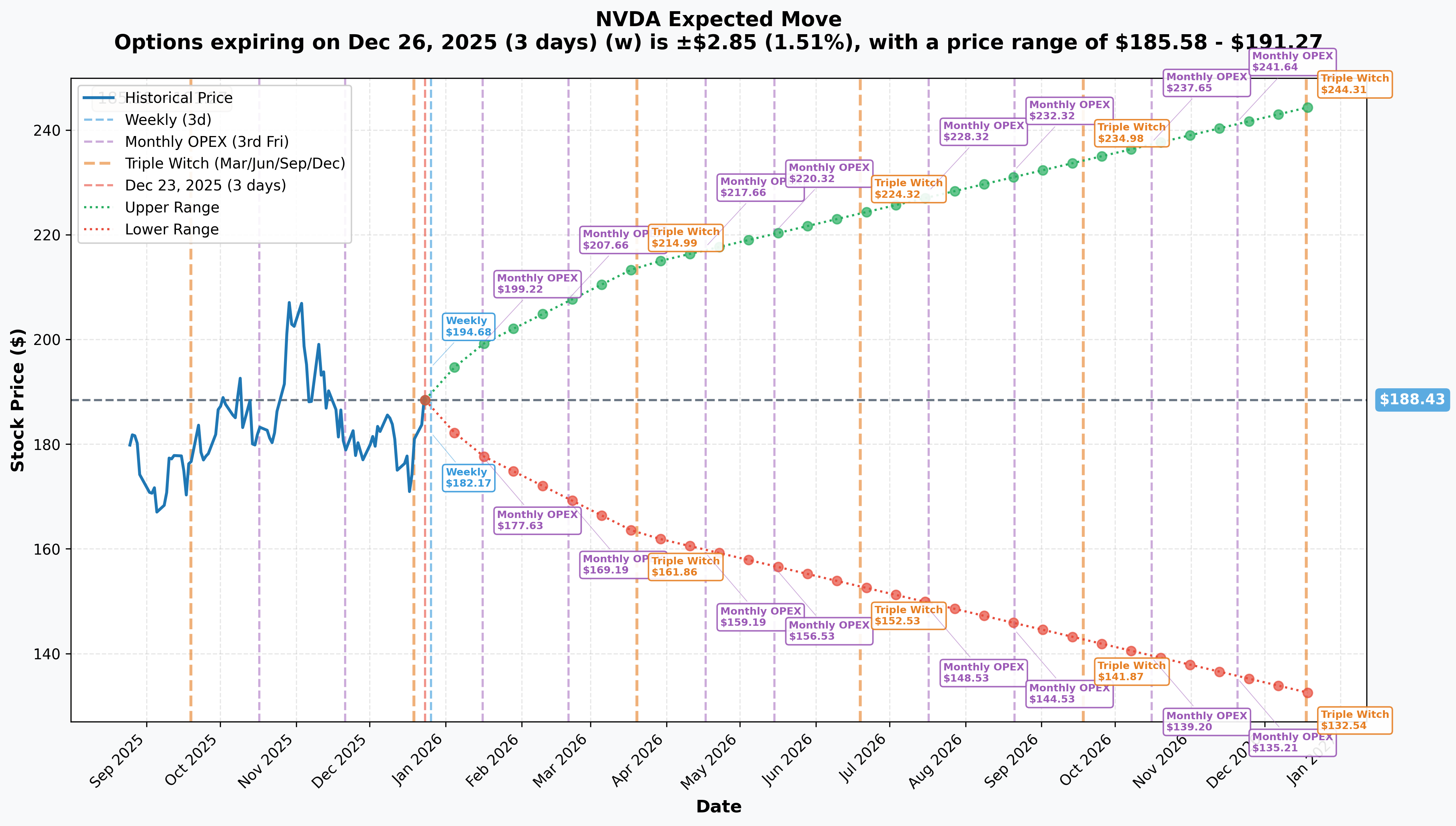

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 26 - 3 days): ±$2.85 (±1.51%) → Range: $185.58 - $191.27

- 📅 January OPEX (Jan 16 - 24 days - TRADE #1!): ±$10.79 (±5.73%) → Range: $177.63 - $199.22

- 📅 Quarterly (March 20 - 87 days - TRADE #2!): ±$25.56 (±13.57%) → Range: $162.86 - $213.99

Translation for regular folks:

Options traders are pricing in a tiny 1.5% move ($3) by Christmas for weekly expiration, but a MUCH BIGGER 5.7% move ($11) through January OPEX and a MASSIVE 13.6% move ($26) through March. The market expects fireworks around Q4 earnings on Feb 25th - that's a huge implied move for a $4.46 TRILLION mega-cap stock!

The January 16th expiration (when Trade #1 expires) has an upper range of $199.22 - meaning the market thinks there's decent probability NVDA pushes toward $200 in the next 24 days. The deep ITM $50 call buyer would make ~$11/share on that move (from $138 intrinsic to $149 intrinsic) - that's $11M profit on a $73M position (15% gain in less than a month).

The March 20th expiration (when Trade #2 expires) has an upper range of $213.99 - aligning PERFECTLY with the $160 call buyer's thesis. If NVDA hits the top of the implied move range by March, those $160 calls would be worth $54 each (current intrinsic $28.47 + time value), representing a potential 70-100% gain depending on entry price.

Key insight: The sharp increase in implied volatility from 1.5% (weekly) to 5.7% (monthly) to 13.6% (quarterly) reflects STACKING CATALYSTS - Q4 earnings, potential export rule changes, GTC announcements, Rubin architecture unveiling, and sovereign AI deployment updates all hit within this window.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Blackwell Sold Out Through Mid-2026 🏭

NVIDIA's Blackwell architecture entered full production in 2025 and demand is OFF THE CHARTS:

- 📊 Q3 FY2026 Results: "Several billion dollars" of Blackwell revenue in Q4 FY2026 (reported Nov 19)

- 🚀 Production Scale: Over 800,000 units produced by Q2 2025, scaling rapidly

- 💰 Sold Out: CEO Jensen Huang confirmed Blackwell chips are effectively sold out through mid-2026

- 🎯 Performance: 40x improvement over Hopper architecture

- 🏦 Full Utilization: NVIDIA stated its GPU installed base including Blackwell, Hopper and Ampere is "fully utilized" and "the clouds are sold out"

Why this matters for the call trades: If Blackwell is sold out through mid-2026, NVDA has effectively pre-sold $100+ billion in revenue with near-term upside driven purely by production scaling. The January call buyer benefits from any Q4 production beat, while the March buyer gets exposure to full Blackwell ramp visibility post-earnings.

China Export Policy Shift (December 2025) 🇨🇳

On December 8, 2025, the Trump administration approved a framework allowing NVIDIA to resume H200 exports to China:

- 🚀 H200 Export Approval: Most powerful AI chip ever approved for export to China

- 💰 Revenue Share: 25% of H200 sales proceeds go to U.S. government (NVDA keeps 75%)

- 📅 Shipment Timeline: Mid-February 2026 start date

- 📦 Initial Volume: 5,000-10,000 chip modules (40,000-80,000 H200 chips)

- ⚖️ Vetting Requirement: Commerce Department licensing for approved commercial customers only

- ⚠️ Blackwell Restricted: Newer Blackwell and Rubin architectures remain blocked from China

Upside potential: China historically represented 15-20% of NVDA's revenue. Even with 25% revenue sharing with the government, H200 exports could add $3-5 billion in incremental revenue through 2026. Congressional opposition via the SAFE Chips Act could block this, but the framework is currently approved.

Downside risk: China holding "emergency meetings" with Alibaba, ByteDance, and Tencent to assess H200 demand and potential import restrictions. If China imposes caps or retaliates, this catalyst evaporates.

🚀 Near-Term Catalysts (Q1 2026 - Next 90 Days)

Q4 Fiscal 2026 Earnings - February 25, 2026 (64 DAYS!) 📊

NVDA reports Q4 results on Wednesday, February 25, 2026 after market close. This is THE catalyst both call trades are positioning for:

Company Guidance for Q4 FY2026 (ending January 2026):

- 💰 Revenue: $65.0 billion ± 2% (consensus: $65.41B) vs. $57.0B in Q3

- 📈 Gross Margin: 74.8% GAAP, 75.0% non-GAAP ± 50 bps

- 🚀 Blackwell Contribution: Significant ramp expected (company hinted at "several billion" minimum)

Wall Street consensus and beat potential:

- 🎯 Revenue: Bulls see upside to $67-68B if Blackwell ramp exceeds guidance

- 💎 EPS: Expecting $1.40-1.50 (up from $1.30 in Q3) on operating leverage

- 🏭 Data Center Revenue: Expected to exceed $55 billion (up from $51.2B in Q3)

- 🖥️ Gaming Segment: RTX 5000 series contribution likely minimal (launched Jan 30) but positive commentary key

Key metrics to watch:

- Blackwell revenue breakdown and customer adoption rates (Microsoft, Google, Meta deployments)

- H200 shipment volumes and gross margin impact (China exports starting mid-Feb)

- Data center revenue trajectory toward $60B quarterly run rate

- Automotive revenue growth (targeting $5 billion annual run rate)

- Most importantly: Guidance for fiscal 2027 and Rubin architecture timeline

Historical context: NVDA crushed Q3 earnings on Nov 19 with $57B revenue (up 62% YoY), beating $33.2B consensus. CEO Jensen Huang stated: "The age of AI is in full steam, propelling a global shift to NVIDIA computing." If Q4 beats by a similar magnitude (15-20% above consensus), we're looking at $75B+ revenue - which would send the stock to new all-time highs.

Why the January call buyer expires BEFORE earnings: The $50 strike calls expire Jan 16, avoiding earnings binary risk on Feb 25. This trader wants to capture any pre-earnings rally (stock typically runs into NVDA earnings) without the overnight gap risk. They can sell the position for intrinsic value + time premium into Jan 16 OPEX, or roll forward to March if bullish.

Why the March call buyer is swinging through earnings: The $160 strike calls expire 23 days AFTER earnings, giving time for post-earnings consolidation and the next leg higher. This trader is BETTING on an earnings beat that propels NVDA to $200-220 by March expiration.

GTC 2025 Conference - March 17-21, 2025 (84-88 DAYS!) 🎤

NVIDIA's flagship GPU Technology Conference in San Jose is historically where the company unveils its most important product roadmap updates:

Expected Announcements:

- 🚀 Blackwell Ultra: Second-half 2025 launch announcement - next evolution of Blackwell platform

- 💎 Vera Rubin Architecture: Next-generation GPU series with "big, big, huge step up" in performance (already taped out!)

- 📅 Annual Rhythm Confirmation: Yearly GPU, CPU, and accelerated computing advancements

- 🤖 AI Infrastructure Updates: Robotics, sovereign AI, AI agents, automotive partnerships

- 🌌 Quantum Day: March 20, 2025 with D-Wave Systems, IonQ, and Rigetti Computing

- 💰 $1 Trillion Inflection Point: Jensen Huang's vision for AI computing transformation

Attendance: 25,000 in-person, 300,000 virtual attendees expected - this is the Super Bowl of AI

Why this matters for the March call trade: The $160 calls expire March 20 - the EXACT DAY as Quantum Day at GTC! If Jensen Huang unveils Rubin specs, Blackwell Ultra timeline, and sovereign AI deployment numbers that blow away expectations, the stock could gap to $210-220 during the conference. This positioning suggests the trader has insider knowledge of potential announcement magnitude OR is simply betting that GTC historically moves the stock 10-15%.

OpenAI Partnership ($100 Billion Deployment) 🤝

NVIDIA and OpenAI announced a strategic partnership for at least 10 gigawatts of NVIDIA systems deployment:

- 💰 Investment: NVIDIA intends to invest up to $100 billion in OpenAI

- 🏭 Deployment Scale: First systems deployment planned for 2026 (timing TBD)

- ⚠️ Status: Still at letter-of-intent stage, no definitive agreement signed as of December 2, 2025

Upside potential: If the partnership is finalized and deployment begins in H1 2026, this could add $20-30 billion in annual revenue starting 2027. The scale is unprecedented - 10 gigawatts of compute is equivalent to the entire hyperscaler buildout in 2024.

Risk factor: Fortune reported in December that the deal is "still unsigned", raising questions about whether terms could change. Any announcement of a SIGNED agreement would be a major catalyst; conversely, a deal collapse would hurt sentiment.

📊 Medium-Term Catalysts (Q2-Q3 2026)

Rubin Architecture Deployment (Q3-Q4 2026) 🔬

Timeline: Second half of 2026 enterprise deployment

Key Specifications:

- 🧬 Process: TSMC 3nm (vs. 4nm for Blackwell)

- 💾 Memory: HBM4 (288GB per GPU, 13 TB/s bandwidth vs. 8 TB/s for Blackwell)

- 🚀 Performance: 50 petaflops FP4 (2.5x improvement over Blackwell's 20 petaflops)

- 📈 System Performance: Rubin NVL144 offers 3.6 EFLOPS dense FP4 vs. 1.1 EFLOPS for B300 NVL72 (3.3x improvement!)

- ⚡ Training: 1.2 ExaFLOPS FP8 vs. 0.36 ExaFLOPS for B300

- ✅ Already Taped Out: Production-ready design completed

Rubin CPX: New specialized GPU for massive-context processing (million-token coding, generative video) with 30 petaflops NVFP4 compute

Rubin Ultra: 2027 launch with 100 petaflops (2x Rubin performance)

Revenue Visibility: NVIDIA has "visibility to a half trillion dollars in Blackwell and Rubin revenue" from early 2025 through end of 2026. This is INSANE forward visibility for a semiconductor company - essentially guarantees $500B in revenue over 24 months.

Sovereign AI Deployments (Q1-Q2 2026) 🌍

Multi-billion dollar infrastructure projects creating geopolitical demand floor:

Europe (3,000+ exaflops of Blackwell compute):

- France, Italy, Spain, UK building domestic AI infrastructure

- Enables secure development of agentic and physical AI applications

Saudi Arabia:

- 600,000 GPU deployment (incremental to prior orders)

- Low-double-digit billions in sovereign AI revenue forecast

United Kingdom (£11 billion investment):

- 120,000 NVIDIA Blackwell GPUs

- Largest AI infrastructure rollout in UK history

- Partners: CoreWeave, Microsoft, Nscale

Japan, Germany: Major sovereign AI initiatives underway

Strategic Importance: National security budgets are less sensitive to interest rate fluctuations than corporate CapEx, creating demand stability even if economy softens.

⚠️ Risk Catalysts (Negative)

AMD Competition Intensifying 🔴

AMD signed a deal with OpenAI for 6 gigawatts of AMD GPUs (first gigawatt in H2 2025), representing a major strategic win:

- 🎯 Instinct MI350 series launched mid-2025 with 4x AI compute improvement over prior gen

- 📊 Market Share: AMD growing from <5% to targeting 10%+ by 2027

- 💰 2025 AI GPU Revenue: $7-10 billion vs. NVIDIA's $150+ billion (still tiny but growing fast)

- ⚖️ Different approach: AMD positioning as "NVIDIA alternative" for cost-conscious hyperscalers

Why this matters: If AMD can deliver competitive performance at lower cost with better availability, hyperscalers may diversify away from 100% NVDA dependence. Even losing 5-10% share to AMD could impact NVDA's premium valuation multiple.

Hyperscaler Custom Silicon (Broadcom) 📉

Broadcom designing custom AI ASICs for hyperscalers:

- 💎 $60+ billion opportunity with three furthest-along ASIC customers in fiscal 2027 (Alphabet's TPUs)

- 🚨 Surprise $10 billion order from fourth unnamed customer for H2 2025 delivery

- 🔧 Different approach: Custom chips vs. NVIDIA's general-purpose GPUs

- 📊 Long-term threat: If Google, Amazon, Microsoft develop in-house accelerators, could erode 10-20% of NVDA's TAM by 2030

GDDR7 Memory Shortages 🛑

NVIDIA plans to cut RTX 5000 gaming GPU production by 30-40% in H1 2026 due to GDDR7 memory shortages:

- ⚠️ Supply Constraints: Rising VRAM prices impacting margins

- 💸 Prioritization: NVIDIA choosing to allocate memory to higher-margin AI GPUs over consumer gaming

- 😰 Reputation Risk: Alienating gaming customer base (NVIDIA's core constituency historically)

- 🎮 AMD/Intel Opportunity: Competitors could gain gaming GPU share while NVDA focuses on AI

Power Infrastructure Bottlenecks ⚡

U.S. data center construction takes ~3 years from groundbreaking to operation:

- 🚨 Power Grid Constraints: Shortages threatening AI boom

- 🏗️ Jensen Huang Response: Hosting "power summit" with utilities and policymakers

- ⏰ Timeline Impact: Even with GPU supply, data centers can't scale without power infrastructure

- 📉 Demand Ceiling: Could cap AI infrastructure buildout pace through 2027

Valuation at Premium Levels 💰

- 📊 Current Valuation: P/E of 45.50, $4.46 trillion market cap

- 📈 YTD Performance: +33% suggests positive catalysts partially priced in

- 🎯 Analyst Targets: Average $253-264 implies only 35-45% upside from current $188

- ⚠️ Limited Margin for Error: Any execution stumble could trigger 20-30% correction

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20th expiration:

📈 Bull Case (40% probability)

Target: $220-$240

How we get there:

- 💪 Earnings CRUSH: Q4 revenue beats to $67-70B (vs. $65B guidance) on Blackwell production surge

- 🚀 Blackwell Ramp Exceeds: Management guides Q1 FY2027 revenue to $75B+ on full Blackwell capacity utilization

- 🇨🇳 China Exports Confirmed: Mid-February H200 shipments begin as planned, adding $1-2B quarterly revenue

- 🤝 OpenAI Deal Signed: Definitive agreement announced with deployment timeline confirmed for H1 2026

- 🎤 GTC Blowout: Rubin architecture unveiling shows 3-4x performance improvement, Blackwell Ultra timeline aggressive

- 📊 Sovereign AI Accelerates: UK, Saudi, European deployments begin in Q1 with additional country wins announced

- 🎯 Margin Expansion: Gross margins sustain 75%+ as Blackwell pricing power remains strong

- 📈 Technical Breakout: Stock reclaims $200, then gamma squeeze through $235 resistance to $240+

Key metrics needed:

- Data center revenue growth >20% QoQ in Q4 (to $62B+)

- Blackwell revenue contribution $8-10B in Q4 vs. "several billion" guidance

- Fiscal 2027 full-year guidance toward $280-300B (up from ~$240B in FY2026)

- Automotive and gaming segments showing strength (diversified growth story)

Call option P&L in Bull Case:

- Trade #1 ($50 calls): If NVDA at $200 by Jan 16, calls worth $150 intrinsic (up from ~$138 entry) = $12M gain on $73M position (16% ROI in 24 days)

- Trade #2 ($160 calls): If NVDA at $230 by Mar 20, calls worth $70 intrinsic (up from ~$32 entry) = $60.8M gain on $51M position (119% ROI!)

Probability assessment: 40% because it requires strong but NOT perfect execution. NVDA has beaten earnings consistently, Blackwell is sold out, and GTC historically moves stock 10-15%. The gamma setup (clean air to $235) favors upside. Main risk is valuation already reflecting much of this optimism.

🎯 Base Case (45% probability)

Target: $185-$210 range (CHOPPY BUT HIGHER)

Most likely scenario:

- ✅ Solid earnings meeting/slightly beating: Q4 revenue $65-67B, in-line with consensus or modest beat

- 📱 Blackwell ramp progressing: Production scaling as expected, no major surprises up or down

- ⚖️ Guidance conservative: Management guides Q1 FY2027 to $68-70B (modest sequential growth) citing normal seasonality

- 🤖 China exports proceed: H200 shipments begin mid-Feb but volumes limited initially, Congressional pushback continues

- 🇨🇳 OpenAI deal unsigned: Partnership remains at letter-of-intent stage, no new updates at GTC

- 🔄 GTC solid but expected: Rubin specs meet expectations, Blackwell Ultra timeline confirmed for H2 2025, no major surprises

- 📊 Market digests gains: Stock consolidates in $190-210 range post-earnings, waiting for next catalyst

- 💤 Volatility crush: IV drops from 13% (pre-earnings) to 8-10% post-earnings as binary risk passes

This is "steady state NVDA" - fundamentals strong, execution solid, but no fireworks to justify explosive rally:

The stock trades up modestly on earnings beat, pulls back slightly on profit-taking, then grinds higher toward $200-210 by March as Blackwell revenue contribution becomes more visible. $50 call buyers capture $5-10/share intrinsic value gain by January OPEX. $160 call buyers see stock at $200-210 by March, making 50-70% on the position.

Call option P&L in Base Case:

- Trade #1: If NVDA at $195 by Jan 16, calls worth $145 intrinsic = $7M gain (9.6% ROI)

- Trade #2: If NVDA at $205 by Mar 20, calls worth $45 intrinsic = $20.8M profit (41% ROI)

Why 45% probability: This is the "default" scenario for a well-run company with strong fundamentals executing a known product roadmap. No major positive surprises needed, but also no major stumbles. Market already expects NVDA to grow 50-60% in FY2027, so meeting that bar keeps stock range-bound to modestly higher.

📉 Bear Case (15% probability)

Target: $160-$175 (TEST THE GAMMA FLOOR!)

What could go wrong:

- 😰 Earnings miss or weak guidance: Q4 revenue $63-64B (below $65B guidance) or Q1 FY2027 guide disappoints at $62-65B

- 🚨 Blackwell production issues: Manufacturing constraints or yield problems slow ramp, revenue contribution below expectations

- ⏰ Rubin timeline delay: GTC announcement pushes Rubin from H2 2026 to 2027, losing competitive advantage window

- 🇨🇳 China export reversal: Congressional SAFE Chips Act passes, blocking H200 exports for 30 months

- 💸 OpenAI deal collapse: Partnership fails to materialize, raising questions about Blackwell demand sustainability

- 📊 AMD wins major customer: Hyperscaler announces large-scale AMD MI350 deployment, validating competition

- 💰 Margin compression: Gross margins dip to 72-73% on product mix shift or competitive pricing pressure

- 🤖 Hyperscaler CapEx cuts: Microsoft, Google, or Amazon signal slower AI infrastructure spending on macro concerns

- 🔨 Technical breakdown: Break below $180 triggers cascade toward $160-165 gamma floor area

Critical support levels:

- 🛡️ $180: Psychological support and recent consolidation lows - MUST HOLD or momentum shifts bearish

- 🛡️ $165: Midpoint between current price and $152.50 put wall - likely strong buying here

- 🛡️ $152.50: MAJOR GAMMA FLOOR (350M put gamma) - dealers will defend this aggressively, massive institutional stop-loss likely set just below

Probability assessment: Only 15% because it requires MULTIPLE negative catalysts to align. NVDA's fundamentals remain dominant (90% cloud AI market share, Blackwell sold out, $500B revenue visibility). Even if earnings miss slightly or guidance disappoints, the long-term AI thesis remains intact. The put wall at $152.50 creates a technical floor 19% below current - very hard to break without catastrophic news.

Call option P&L in Bear Case:

- Trade #1 ($50 calls): If NVDA at $170 by Jan 16, calls worth $120 intrinsic = -$18M loss (-24.7%)

- Trade #2 ($160 calls): If NVDA at $165 by Mar 20, calls worth $5 intrinsic = -$43.2M loss (-84.7%!)

The deep ITM January calls have natural downside protection (still $120 intrinsic at $170), but the OTM March calls would get crushed in a bear scenario.

💡 Trading Ideas

🛡️ Conservative: Buy The Dip Strategy (January Gamma Floor Play)

Play: Wait for any pre-earnings pullback to $180-185 range, then buy shares or sell cash-secured puts

Why this works:

- ⏰ Timing is everything: Earnings not until Feb 25 (64 days away) - plenty of time to scale in if stock dips

- 📊 Gamma support at $152.50: Massive 350M put wall creates rock-solid floor 19% below current - extreme downside limited

- 🎯 Risk/Reward: Buying at $180-185 offers 8-15% downside to gamma floor vs. 25-35% upside to $235-250 targets

- 💸 Implied move lower bound: Jan 16 implied move goes down to $177.63 - buying near that level captures full statistical edge

- 🤔 Institutions loading up: If smart money is deploying $124M in calls, why fight the tape?

- 📈 Pre-earnings rally: NVDA historically runs 5-10% into earnings as momentum builds

Action plan:

- 👀 Watch for any macro selloff or sector rotation that drags NVDA to $180-185

- 🎯 Buy 50% position at $183, remaining 50% at $178 if it gets there (dollar-cost average)

- ⏰ Hold through Jan 16 OPEX to capture any pre-earnings rally

- 📊 Alternative: Sell Feb $175 cash-secured puts for $5-7 premium (collect income while waiting)

- ✅ Stop-loss: If NVDA breaks below $172, exit and reassess (signal gamma floor might not hold)

Expected outcome: Either stock never gets to $180 (you miss the trade but avoid chasing), or you buy near implied move lower bound with excellent risk/reward. Worst case, you're buying the world's best AI company at 19% discount to current levels with $500B revenue visibility.

Risk level: Low (buying stock, not options) | Skill level: Beginner-friendly

⚖️ Balanced: Bull Put Spread (Copy The Gamma Floor)

Play: Sell bull put spread targeting the massive $152.50 gamma support

Structure: Sell $165 puts, Buy $150 puts (January 16 expiration)

Why this works:

- 🎯 Aligned with institutions: $152.50 gamma floor means dealers will BUY aggressively on dips toward $165

- 📊 Defined risk: $15 spread width = $1,500 max risk per spread

- 💰 Premium collection: Collect ~$3-4 credit per spread (20-25% ROI if stock stays above $165)

- ⏰ Before earnings: Expires 40 days before Feb 25 earnings, avoiding binary event risk

- 🛡️ Margin of safety: NVDA needs to drop 12.5% (to $165) before position starts losing money

- 📈 Probability of profit: ~70-75% based on delta (stock has to drop significantly to lose)

Estimated P&L:

- 💰 Max profit: $300-400 per spread if NVDA above $165 at Jan 16 expiration (20-27% ROI)

- 📉 Max loss: $1,100-1,200 per spread if NVDA below $150 (assignment risk)

- 🎯 Breakeven: ~$161-162 (12-14% drop from current)

Entry timing:

- ⏰ Best entry: Sell spread when NVDA rallies to $195-200 (maximum premium collection)

- ❌ Skip if: Stock already below $180 (spread too close to at-the-money, risk/reward deteriorates)

Position sizing: Risk only 3-5% of portfolio (sell 3-5 spreads max on $100K account)

Risk level: Moderate (defined risk, high probability) | Skill level: Intermediate

🚀 Aggressive: Earnings Volatility Straddle (ADVANCED ONLY!)

Play: Buy straddle on Feb monthly expiration (Feb 21), hold through earnings on Feb 25

Structure: Buy $190 calls + Buy $190 puts (Feb 21 expiration)

Why this could work:

- 💥 Implied move potentially underpriced: Historical NVDA earnings moves have been 12-18%, current implied ~13%

- 🎰 Binary catalyst: Q4 earnings could send stock to $220+ on beat or $165 on miss - huge two-way potential

- 📊 At current levels: Stock at $188 makes $190 strikes near-the-money with maximum gamma

- 🚀 Blackwell visibility: Earnings will provide FIRST FULL QUARTER of Blackwell production data

- ⚡ Need 14-15% move either direction to profit after IV crush

- 📈 Maximum leverage: If stock gaps to $230 or $165, straddle could double (100%+ ROI)

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Straddle costs ~$25-30 ($2,500-3,000 per straddle)

- ⏰ TIME DECAY KILLER: Theta burns -$100-150/day as earnings approaches

- 😱 IV CRUSH: Even if stock moves 10%, IV collapse could still result in LOSS on both legs

- 📊 Earnings "in-line" scenario: Stock gaps to $195-200 (only 5-7% move) and straddle loses 30-50%

- 🎢 Need to be RIGHT on magnitude: Direction matters less than SIZE of move

- ⚠️ Feb 21 expiration: Only 4 days BEFORE earnings - need to time entry perfectly

Estimated P&L:

- 💰 Cost: ~$25-30 per straddle

- 📈 Profit scenario: Stock moves to $230 or $165 (20-22% move) = $35-40 gain (40-60% ROI)

- 🚀 Home run: Stock moves to $250 or $150 (30%+ move) = $60+ gain (120%+ ROI)

- 📉 Loss scenario: Stock ends $180-200 range = lose $15-25 (50-80% loss)

- 💀 Total loss: Stock flat at $190 = lose entire $25-30 (100% loss)

Breakeven points:

- 📈 Upside breakeven: ~$215-220 (need 15-17% rally)

- 📉 Downside breakeven: ~$160-165 (need 13-15% drop)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded straddles through earnings 5+ times and understand IV crush mechanics

- ✅ Can afford to lose ENTIRE premium (real possibility!)

- ✅ Understand you're betting AGAINST the options market's implied probability

- ✅ Can monitor position Wednesday Feb 25 post-earnings and take profits within MINUTES

- ✅ Accept that even if you're RIGHT on direction, timing IV crush wrong causes loss

- ⏰ Plan to close position within 1-4 hours post-earnings (don't hold overnight - IV collapses instantly)

Alternative (safer): Buy March straddle instead (expires March 20), which gives 23 days post-earnings for stock to make its move. Costs more (~$35-40) but avoids brutal Feb expiration IV crush.

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35-40% (lower than 50% due to IV crush and need for outsized move)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💰 Valuation at $4.46T market cap: Trading at 45.5x P/E after 33% YTD gain with $188 price near analyst consensus targets ($253-264 implies 35-45% upside but much already priced in). Stock is priced for PERFECTION - requires sustained 50-60% annual growth through 2027 to justify current multiple. Any execution stumble magnified by premium valuation. Zero margin of safety.

-

⏰ Q4 Earnings binary risk (Feb 25): Results 64 days away create MASSIVE volatility potential. Market expecting $65B revenue vs. $57B in Q3 - even small misses could trigger 10-15% gap down. Blackwell production commentary will be scrutinized intensely. Guidance for Q1 FY2027 matters MORE than Q4 results. Historical precedent shows NVDA can move 15-20% overnight on earnings surprises. Options pricing ±13% implied move quarterly but actual moves have been larger.

-

🇨🇳 China export policy uncertainty: H200 exports approved but Congressional pushback strong. SAFE Chips Act could block exports for 30 months. China holding "emergency meetings" with Alibaba, ByteDance, Tencent to assess potential import caps. 25% revenue share with U.S. government reduces profitability. Blackwell and Rubin completely blocked from China. Geopolitical tensions could escalate rapidly, removing $5-10B annual revenue opportunity overnight.

-

📊 AMD competition accelerating: OpenAI partnership with AMD for 6 gigawatts represents major strategic win for competitor. MI350 series showing competitive performance at lower cost. AMD targeting 10%+ market share by 2027 vs. current <5%. Even losing 5-10% share to AMD could compress NVDA's premium valuation multiple from 45x to 35-40x (stock reprices to $160-170).

-

🏭 Hyperscaler custom silicon threat: Broadcom designing $60+ billion in custom AI ASICs for Google, Amazon, Microsoft. If hyperscalers develop in-house accelerators and reduce NVDA dependence from 90% to 70-80%, could erase $30-50B in TAM by 2030. OpenAI also developing first AI chip with Broadcom/TSMC (3nm, mass production 2026). Long-term structural threat to NVDA's monopoly.

-

⚡ Power infrastructure bottlenecks: U.S. data center construction takes ~3 years, power grid constraints threatening AI boom. Even with GPU supply, data centers can't scale without electricity. Jensen Huang hosting "power summit" with utilities - signals this is a REAL bottleneck. Could cap AI infrastructure buildout pace through 2027, limiting NVDA's addressable market growth.

-

🎮 Gaming segment production cuts: NVIDIA cutting RTX 5000 production by 30-40% in H1 2026 due to GDDR7 memory shortages. Prioritizing AI GPUs over gaming alienates core customer base. AMD/Intel could gain gaming GPU share while NVDA focuses on data center. Reputation risk with enthusiast community.

-

🤝 OpenAI deal still unsigned: Fortune reported deal remains at letter-of-intent stage as of Dec 2. No definitive agreement signed for $100 billion partnership. Terms could change, deployment timeline could slip, or deal could collapse entirely. Market pricing in this partnership as high-probability event - if it fails to materialize, stock could drop 10-15% on sentiment shift.

-

📉 Gross margin pressure emerging: Q4 guidance of 74.8% GAAP margin down from 75%+ recently. Product mix shift toward lower-margin solutions or competitive pricing pressure from AMD. H200 China exports with 25% revenue sharing further pressures margins. If margins compress to 72-73% range, earnings miss even if revenue beats.

-

🎢 Extreme beta to tech sector: NVDA moves 2-3x the Nasdaq. If broader market sells off on Fed policy, recession fears, or geopolitical events, NVDA will get hit disproportionately hard. Current $188 price offers NO fundamental support levels until $165-170 range (12% drop). Technicals matter less than macro for a $4.46T mega-cap.

-

🔨 Institutional call buyers could be hedging: The $124M in call purchases COULD be part of a complex hedge (e.g., long stock, short upside calls, buying downside puts, then buying deep ITM calls to create synthetic position). We don't know the full portfolio context. Don't blindly follow "smart money" without understanding their complete book.

🎯 The Bottom Line

Real talk: Two institutional players just bet $124 MILLION that NVDA explodes higher over the next 1-3 months. This isn't retail FOMO - this is sophisticated capital deploying $73M on deep in-the-money calls (acting like leveraged shares) and $51M on out-of-the-money calls (betting on a 15-20% rally into March). The size, timing, and strike selection tell us everything we need to know: smart money believes the current $188 level is a GIFT.

What these trades tell us:

- 🎯 January trader wants safe leverage: $50 calls expire before earnings, avoiding binary risk - they're playing the pre-earnings rally

- 💰 March trader swinging for the fences: $160 calls positioned for earnings beat + GTC blowout combo - betting on $200-220 move

- ⚖️ Combined conviction: $124M represents ~400-500x normal daily call volume at these strikes - this is NOT a hedge, this is DIRECTIONAL

- 📊 Timing is surgical: January expires at monthly OPEX (max liquidity), March expires DURING GTC conference (Quantum Day March 20)

- ⏰ Catalyst density: Both trades capture Blackwell ramp acceleration, China export clarity, sovereign AI deployments, and potential OpenAI deal signing

This is NOT a "buy blindly" signal - but it IS a "pay very close attention" signal.

If you own NVDA:

- ✅ HOLD through at least Feb earnings - fundamentals have never been stronger (Blackwell sold out, $500B revenue visibility)

- 📊 Consider selling calls against shares: If you own 100+ shares, sell Feb $210 or $220 calls for $8-12 premium (income while waiting)

- ⏰ Don't panic on dips to $180-185 - that's the BUY ZONE, not the sell zone

- 🎯 If earnings beat, take profits on 25-30% of position at $210-220 to lock in gains, let rest run toward $235 gamma resistance

- 🛡️ Mental stop at $172 - if NVDA breaks below that, something fundamentally broken (reassess thesis)

If you're watching from sidelines:

- ⏰ Wait for pullback to $180-185 before entering - don't chase at $188 after 33% YTD gain

- 🎯 Best entry: Any macro selloff that drags NVDA to implied move lower bound ($177-180)

- 📈 Alternative entry: Scale in 25% at $190, 25% at $185, 25% at $180, 25% at $175 (dollar-cost average into strength)

- 🚀 Long-term (6-12 months): Blackwell sold out through mid-2026, Rubin launching H2 2026, and sovereign AI creating geopolitical demand floor justify $250-300 targets by end of 2026

- ⚠️ Current valuation (45x P/E) requires flawless execution - one stumble and it's back to $160-170

If you're bearish:

- 🎯 Don't fight this tape - $124M institutional buying + Blackwell sold out + $500B revenue visibility = uptrend remains intact

- 📊 Wait for earnings before initiating shorts - fighting into a binary catalyst is suicide

- ⚠️ If earnings disappoint AND stock breaks $180, THEN consider put spreads targeting $165-170 range

- 📉 Watch for breaks below $175 - that's the trigger for cascade toward $160-165, then $152.50 gamma floor

- ⏰ Timing is EVERYTHING: Premature bearish positioning risks getting steamrolled by earnings beat

Mark your calendar - Key dates:

- 📅 January 16, 2026 - Monthly OPEX, expiration of Trade #1 ($73M deep ITM calls)

- 📅 January 30, 2026 - RTX 5090/5080 launch (gaming segment data point)

- 📅 Mid-February 2026 - H200 China exports begin (if approved)

- 📅 February 25, 2026 (Tuesday after close) - Q4 FY2026 earnings report (THE CATALYST!)

- 📅 March 17-21, 2026 - GTC 2025 conference (Rubin unveiling expected)

- 📅 March 20, 2026 - Expiration of Trade #2 ($51M OTM calls) + Quantum Day at GTC

- 📅 H2 2026 - Rubin architecture enterprise deployment begins

Final verdict: NVDA's AI infrastructure dominance story remains the most compelling secular growth thesis in public markets. Blackwell sold out through mid-2026, $500B revenue visibility through end of 2026, 90% cloud AI market share, and annual product cadence maintaining technological leadership ALL remain intact.

BUT, at 45x P/E with $4.46T market cap after 33% YTD gain, the risk/reward is NO LONGER heavily skewed to upside for aggressive new positioning. The $124M institutional call buying suggests smart money believes the 11% pullback from October highs ($207 to $188) has created a tactical entry point into Q4 earnings and GTC 2025.

The trade: If you don't own it, wait for $180-185 pullback to enter (6-10% margin of safety). If you own it, HOLD through Feb 25 earnings with conviction. If you're aggressive, the bull put spread strategy (sell $165/$150 spread) offers 70% probability of 20-25% ROI by mid-January with defined risk.

This is a sprint to the next two catalysts (earnings + GTC), not a marathon. Position accordingly. Manage risk. And remember: institutions deploying $124M in calls are playing with house money after riding NVDA from $30 in 2020 to $188 today. Don't bet the farm chasing their moves - but don't ignore them either. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-scores of 11.62 and 3.24 reflect these specific trades' sizes relative to recent NVDA history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 15-20% gaps either direction. The institutional call buyers may have complex portfolio hedging needs, access to non-public information, or risk tolerances not applicable to retail traders. The $124M combined premium represents extreme conviction, but institutions have been wrong before.

About NVIDIA Corporation: NVIDIA is a leading developer of graphics processing units (GPUs) and AI computing infrastructure, offering AI-optimized GPUs alongside its CUDA software platform for model development. The company provides data center networking solutions to connect GPUs for complex computational workloads, with a market cap of $4.46 trillion in the Semiconductors & Related Devices industry.