💎 NVDA $16M Call Exit - Smart Money Takes Profits Before CES! 🎯

📅 December 30, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just cashed out $16 MILLION in NVDA call options this morning! A sophisticated trader sold 4,600 contracts of deep in-the-money $160 strike calls expiring March 20th - locking in massive gains with the stock at $187.45. This isn't panic selling - this is profit-taking perfection! After NVDA's incredible run to $4.57 trillion market cap, smart money is taking chips off the table just days before the critical CES 2026 keynote on January 5th. Translation: Institutions are securing triple-digit gains rather than gambling on the next catalyst!

📊 Company Overview

Nvidia Corporation (NVDA) is the undisputed AI infrastructure leader dominating the semiconductor revolution:

- Market Cap: $4.57 Trillion (one of the world's most valuable companies)

- Industry: Semiconductors & Related Devices

- Current Price: $187.45 (down from $212 all-time high in October)

- Primary Business: AI GPUs, data center accelerators, CUDA software ecosystem, gaming graphics, automotive AI

Nvidia controls 90%+ of the AI accelerator market with its Blackwell GPU architecture shipping at record pace, Q3 FY2026 revenue hitting $57 billion (up 62% YoY).

💰 The Option Flow Breakdown

The Tape (December 30, 2025 @ 10:01:46):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:01:46 | NVDA | BID | SELL | CALL $160 | 2026-03-20 | $16M | $160 | 4.6K | 109K | 4,625 | $187.45 | $33.60 |

🤓 What This Actually Means

This is textbook profit-taking on a winning long call position! Here's the full story:

- 💰 Massive exit: $16M ($33.60 per contract × 4,600 contracts) - this is a MAJOR position unwind

- 🎯 Deep ITM calls: $160 strike is $27.45 in-the-money (stock at $187.45) - these have massive intrinsic value

- 📈 Huge gains realized: Assuming entry around $10-15 when stock was $160-170, this trader is booking 120-200%+ returns!

- ⏰ Strategic timing: 80 days to expiration, 6 days before CES keynote, 57 days before Q4 earnings (Feb 25)

- 📊 Position size: 4,600 contracts controls 460,000 shares worth ~$86 million in stock exposure

- 🏦 Professional derisking: This is institutional-grade risk management, not retail panic

What's REALLY happening: This trader accumulated these $160 calls when NVDA was likely trading $160-175 (September-October timeframe). Now with the stock at $187.45, they're sitting on MONSTER profits and facing critical catalysts (CES keynote, Q4 earnings). Rather than risk giving back gains if news disappoints, they're cashing out the entire position for $16M. Think of it like selling your house after it doubled in value - you'd want to lock in the win before the market shifts!

Unusual Score: 🔥 MODERATE (Z-score 0.65, TYPICAL classification) - While the dollar amount is huge, this type of deep ITM exit happens regularly at NVDA's scale. The 4,600 contract size is about 4.2% of open interest (109,000), suggesting institutional rebalancing rather than panic. We see 7 similar-sized trades in recent history, making this notable but not unprecedented.

📈 Technical Setup / Chart Check-Up

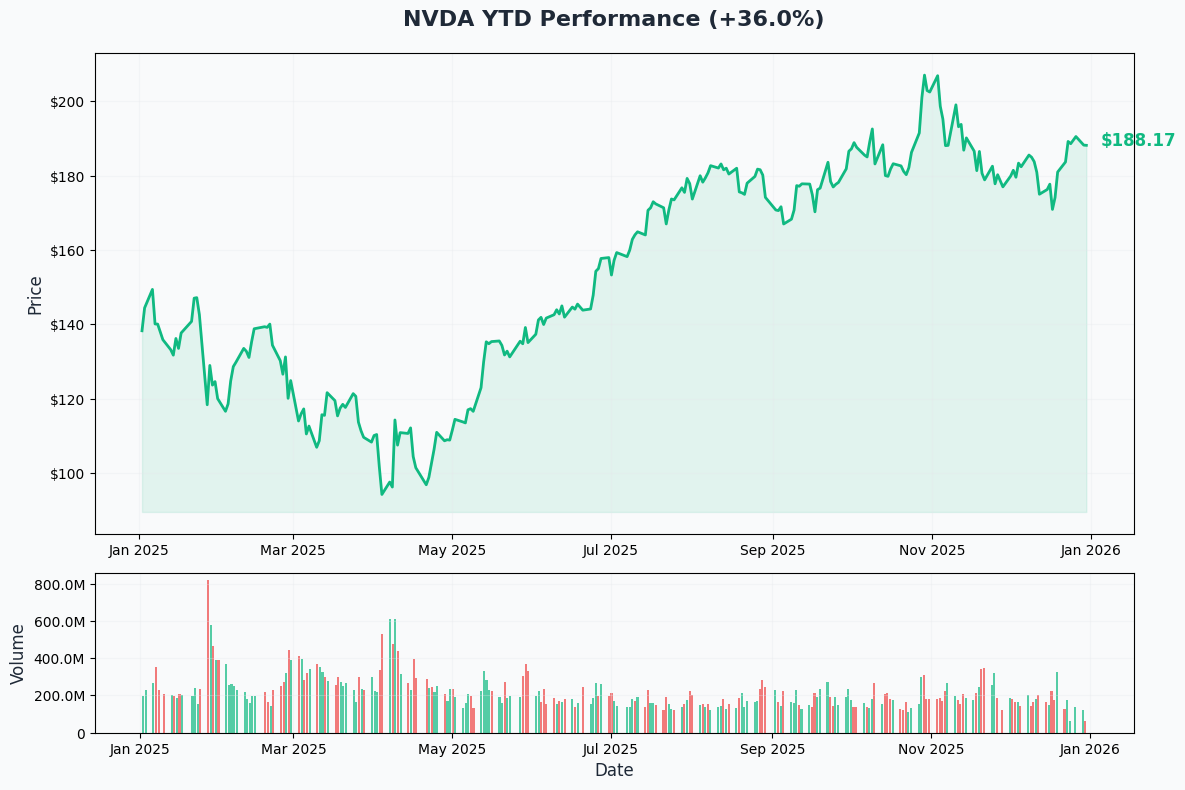

YTD Performance Chart

NVDA is up +41.88% YTD at $188.17, recovering from the brutal April crash to $86.62 on Trump tariff fears. The chart shows NVIDIA's incredible resilience - after falling 59% from highs, the stock more than doubled from April lows, driven by record Blackwell GPU demand and the $20 billion Groq acquisition.

Key observations:

- 🎢 Extreme volatility: $86 to $212 range (145% spread) shows NVDA isn't for the faint of heart

- 📈 Recovery complete: Bounced from April low of $86.62 to $212.19 all-time high in October

- 📉 Current pullback: Down 11.4% from October peak, trading near $188 support zone

- 💪 Institutional accumulation: 68.98% institutional ownership with Vanguard holding 8.94% ($389B)

- ⚠️ Consolidation phase: Trading sideways $180-190 for past month - waiting for next catalyst

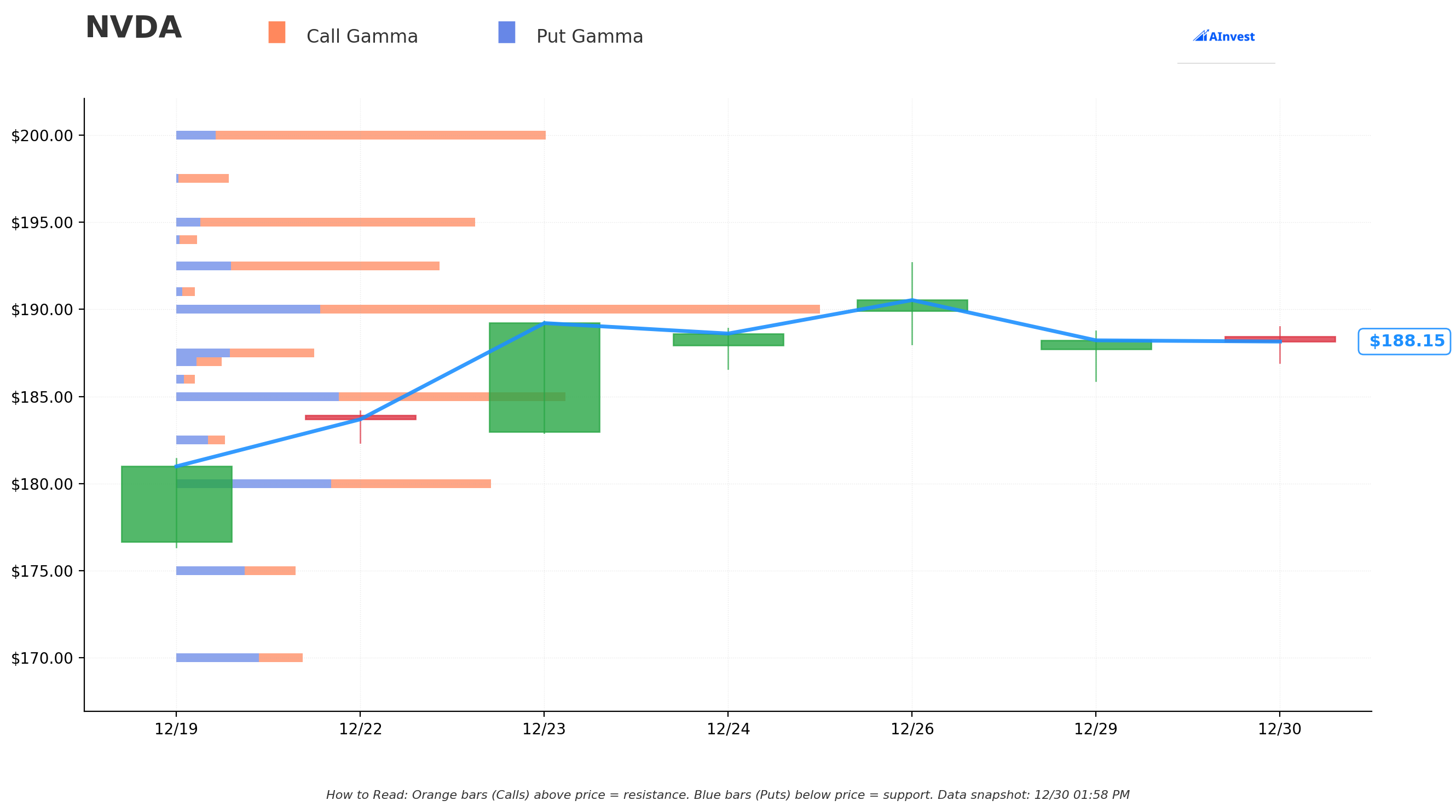

Gamma-Based Support & Resistance Analysis

Current Price: $188.30

The gamma exposure map reveals TIGHT bands that will control near-term price action heading into CES:

🔵 Support Levels (Put Gamma Below Price):

- $185 - STRONGEST immediate support with 191.3B total gamma exposure (this is the floor!)

- $180 - Major structural support at 154.6B gamma (8.6% cushion below)

- $175 - Secondary floor with 58.4B gamma

- $170 - Deep support zone at 62.1B gamma

- $160 - Extended support with 66.2B gamma (exactly where this call was struck! Not coincidental)

🟠 Resistance Levels (Call Gamma Above Price):

- $190 - CRUSHING overhead resistance with 318.7B gamma (STRONGEST LEVEL - massive ceiling!)

- $195 - Secondary resistance at 148.5B gamma (3.5% overhead)

- $197.50 - Micro resistance with 25.7B gamma

- $200 - Psychological and gamma barrier at 182.9B gamma (6.2% above)

- $210 - Extended upside target at 58.1B gamma

What this means for traders: NVDA is trapped in a NARROW $185-$190 range with the STRONGEST gamma level at $190 (318.7B) acting as an iron ceiling. Market makers holding massive call positions at $190 will sell into any rally attempts, creating natural resistance. This setup screams "range-bound until catalyst" - the stock needs a major event (like CES announcement) to break free. The $185 support at 191.3B gamma is critical - hold this level and bulls stay in control, break below and momentum shifts bearish toward $180.

Notice anything? The call seller's $160 strike sits at a significant gamma support level (66.2B). They accumulated calls at a strike that has become a technical floor, rode the rally to $187, and now exit into resistance at $190. Textbook technical trading.

Net GEX Bias: Mixed - while more call gamma above price suggests bullish positioning long-term, the massive $190 wall creates near-term headwinds. Stock will likely chop in this range until CES breaks the technical deadlock.

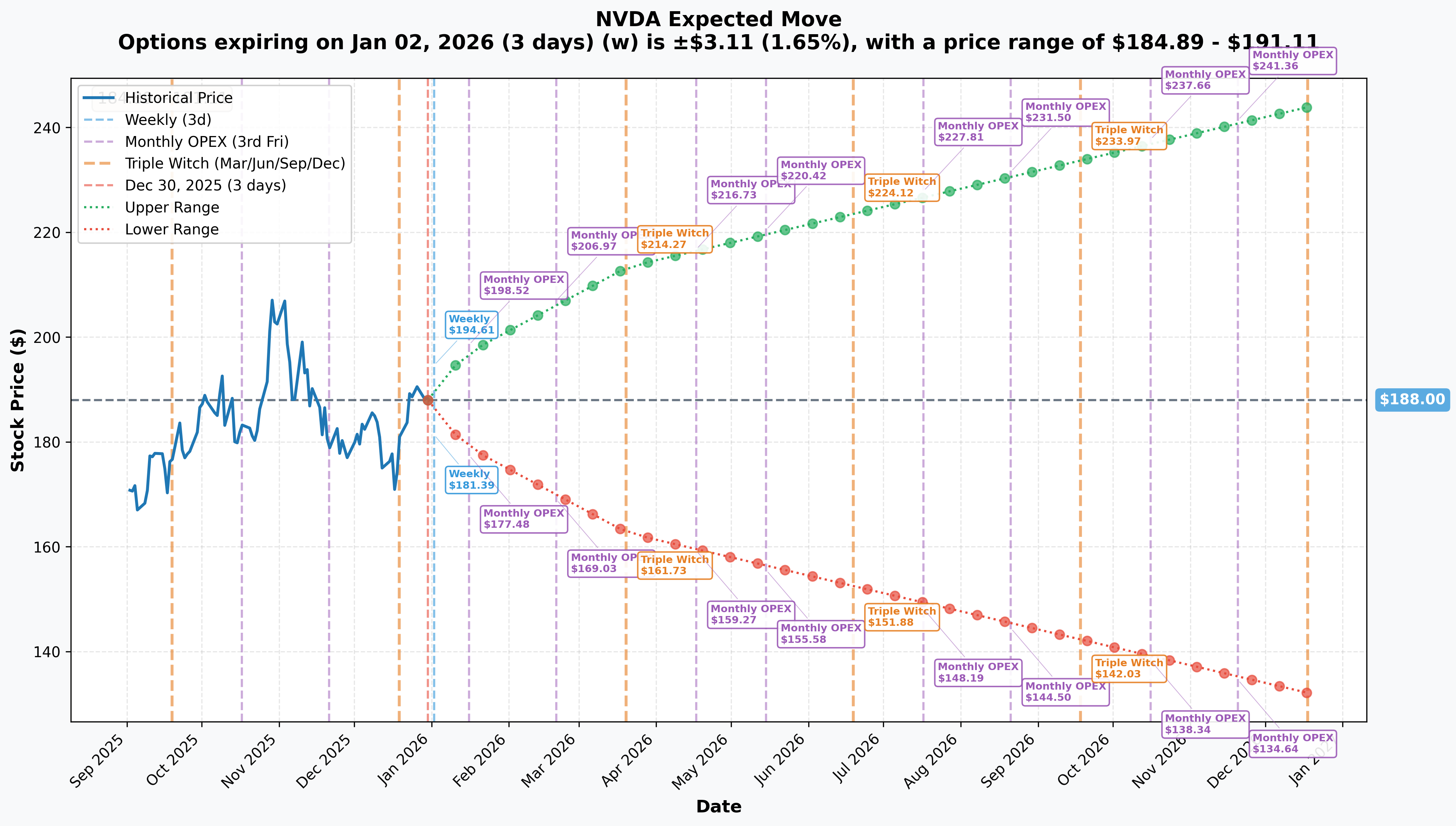

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 2 - 3 days): ±$3.11 (±1.65%) → Range: $184.89 - $191.11

- 📅 Monthly OPEX (Jan 16 - 17 days): ±$9.24 (±4.92%) → Range: $178.76 - $197.24

- 📅 Quarterly Triple Witch (Mar 20 - 80 days - THIS TRADE!): ±$25.37 (±13.5%) → Range: $162.63 - $213.37

- 📅 LEAPS (Dec 18, 2026 - 353 days): ±$55.93 (±29.75%) → Range: $132.07 - $243.93

Translation for regular folks: Options traders are pricing in a 1.7% move ($3) through New Year's weekend but a MUCH LARGER 4.9% move ($9) through January OPEX which includes the CES 2026 keynote on January 5th. The market expects modest volatility short-term but real fireworks around CES!

The March 20th expiration (when this $16M trade expires) has an upper range of $213.37 - meaning the market thinks NVDA could rally 14% to retest all-time highs over the next 80 days through Q4 earnings (Feb 25) and GTC 2026 conference (Mar 16-19). This aligns with the call seller's thesis: they've captured most of the move from $160 to $187 and don't want to risk the final leg given upcoming binary events.

Key insight: The jump in implied volatility from 1.7% (weekly) to 4.9% (monthly) reflects CES uncertainty. Smart money is derisking BEFORE the keynote rather than gambling on product announcements.

🎪 Catalysts

🔥 Immediate Catalysts (Next 7 Days)

CES 2026 Keynote - January 5, 2026 (6 DAYS AWAY!) 🎤

Jensen Huang's keynote at CES 2026 on January 5th at 4:00 PM ET is THE near-term catalyst that could move the stock:

- 🎮 RTX 5000 Super Series Expected: Rumors suggest RTX 5080 Super with 24GB VRAM, RTX 5070 Ti Super with 24GB, RTX 5070 Super with 18GB using new 24 Gbit GDDR7 memory

- 🤖 AI Demonstrations: 90-minute keynote with live demos at Fontainebleau hotel showcasing AI capabilities

- 🏢 Data Center Updates: Potential Blackwell production metrics, customer wins, deployment timelines

- 📊 Product Roadmap Hints: Could preview Vera Rubin architecture or new AI services

- ⚠️ Alternative View: Some analysts expect NO consumer GPU launches at CES, with Super SKUs delayed to Q3 2026 - could disappoint if true

Upside potential: Surprise RTX 5000 Super announcement with aggressive pricing could ignite gaming bulls. Major enterprise AI partnership reveals would validate Blackwell momentum. Stock could pop 5-8% to $195-200 on strong content.

Downside risk: If Jensen focuses only on automotive/robotics with no gaming news or data center metrics, stock could sell off 3-5% on disappointment. Market expectations are HIGH after Q3's record $57B revenue beat.

🚀 Near-Term Catalysts (Q1 2026)

Groq Acquisition Integration (Just Completed December 28, 2025) 🤝

NVIDIA's $20 billion "licensing agreement" for Groq (really an acquisition) announced December 24th represents a MAJOR strategic move:

- 💰 Largest deal ever for NVIDIA ($20B vs. previous record $7B for Mellanox in 2019)

- 🏭 ~90% of Groq staff moving to NVIDIA including CEO Jonathan Ross

- 🎯 Eliminates inference competitor, acquires LPU (Language Processing Unit) technology

- 📈 Groq valued at $6.9B in September 2025, paid $20B premium (190% markup!)

- 🚀 Strengthens NVIDIA's inference capabilities where AMD and startups were gaining ground

Why this matters for the call trade: Integration execution over next 90 days will be critical. If Groq technology accelerates NVIDIA's inference roadmap (announced at CES or GTC), it justifies the $20B premium. But if integration drags or talent leaves, it's overpay risk. The March expiration gives this trade time to see early signals.

Blackwell GPU Production Ramp (Ongoing) 🏭

NVIDIA achieved full-scale Blackwell production with record shipments:

- 📦 ~1,000 GB200 NVL72 racks shipping per week

- 🎯 Q1 2026 target: ~800,000 Blackwell units

- 💰 Q4 2025 Blackwell revenue estimated at $11B (80% of total mix)

- 🔥 CEO Jensen Huang: Demand "insane," will exceed supply for "several quarters"

- 🏢 Customers: Microsoft Azure ND GB200 V6 series, Google Cloud A4 VMs, Amazon AWS

Q4 FY2026 Earnings - February 25, 2026 (57 DAYS) 📊

NVIDIA reports Q4 FY2026 earnings on February 25, 2026 after market close:

- 📊 Revenue Consensus: $65.41 billion (up 15% from Q3's $57B)

- 💰 EPS Consensus: $1.52 (up 17% from Q3's $1.30)

- 🎯 Q3 provided guidance: $65B revenue (+/- 2%), 75% gross margin

- 🔑 Key metrics to watch:

- Blackwell revenue ramp rate (was $11B in Q4, could be $15-20B in Q1)

- Data center segment growth trajectory

- China revenue contribution post-H200 export waiver

- Q1 FY2027 guidance quality

Historical precedent: NVIDIA has beaten estimates consistently but stock reaction depends on guidance. Q3 beat by 4% on EPS but stock initially sold off on supply concerns before rallying. Market expects PERFECTION at 47x P/E valuation.

GTC 2026 Conference - March 16-19, 2026 🏟️

NVIDIA's premier annual event at San Jose SAP Center with Jensen Huang keynote on March 16th:

- 🔬 Vera Rubin Architecture: Expected updates on next-gen platform (scheduled Q3 2026 launch, 50 petaflops FP4 vs. 20 for Blackwell)

- 🤖 Robotics & Autonomous Driving: DRIVE platform advances for automotive AI

- 🏭 AI Factories & Digital Twins: Industrial applications showcase

- 📚 CUDA Library Announcements: Software ecosystem enhancements

- 💼 Enterprise Partnerships: Major customer deployments revealed

Significance: GTC is where NVIDIA makes BIG roadmap announcements. This is the last major catalyst before the March 20th option expiration. Stock historically moves 5-10% around GTC based on content quality.

📊 Medium-Term Catalysts (2026)

H200 China Shipments - February 2026 📦

Trump administration granted one-year waiver for H200 exports to China with 25% levy per transaction:

- 🚢 NVIDIA preparing ~80,000 H200 chips for mid-February delivery

- 💰 Potential multi-billion dollar revenue contribution (80K units @ ~$30K each = $2.4B)

- ⚖️ Requires inter-agency approval per deal, subject to geopolitical changes

- 🇨🇳 China may impose domestic chip bundling requirements

- 🚨 Risk: Policy could reverse if U.S.-China tensions escalate

Vera Rubin Architecture Launch - Q3 2026 🚀

Next-generation platform already taped out, scheduled for Q3 2026 release:

- 🔬 Process: TSMC 3nm technology

- 💾 Memory: HBM4 with 13 TB/s bandwidth (up from 8 TB/s in Blackwell)

- 💥 Performance: 50 petaflops FP4 (2.5x improvement over Blackwell's 20 petaflops)

- 📊 System Config: NVL144 with 144 VR200 GPUs delivers 3.6 EFLOPS FP4 (3.3x vs. B300 NVL72)

- 🌐 NVLink 6.0: 3.6 TB/s bandwidth for multi-GPU scaling

⚠️ Risk Catalysts (Negative)

DOJ Antitrust Investigation 🚨

NVIDIA faces active DOJ investigation with subpoenas issued to company and third parties:

- 📋 Focus: Bundling/tying arrangements, switching costs for customers, RunAI acquisition concerns

- ⚖️ Potential violations: Illegal tying agreements, anti-competitive mergers

- 💸 Market impact: Contributed to $279 billion single-day market cap loss when first announced

- ⏰ Timeline: Investigation ongoing, no resolution timeline provided

- 🎯 Risk: Could force structural changes to business model or block future acquisitions

Custom Silicon Competition 🏭

Hyperscalers developing in-house alternatives to NVIDIA chips:

- 🔷 Google TPU: Growing self-supply, estimated ~10% of internal needs

- 🟠 Amazon Trainium: Increasing adoption for training workloads

- 🔶 Broadcom ASICs: Custom accelerators for major cloud providers

- 📊 Market share risk: While NVIDIA maintains 90%+ share, any erosion threatens premium valuation

- 💰 2025-2027 hyperscaler CapEx: Goldman Sachs projects $1.15 trillion - more competition for this spend

AI ROI Concerns 💔

MIT study found 95% of organizations report no measurable ROI from GenAI deployments:

- 📉 Spending bubble: Hyperscalers added $121 billion in debt over past year (300%+ increase)

- ⏰ Timeline risk: If ROI doesn't materialize in 2026-2027, CapEx could moderate sharply

- 💸 NVDA exposure: ~90% of revenue from data center segment - hyper-concentrated risk

- 🎯 Stock impact: Any signs of hyperscaler spending slowdown could trigger 20-30% correction

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timing, here are the scenarios through March 20th expiration:

📈 Bull Case (30% probability)

Target: $205-$215

How we get there:

- 🎤 CES keynote (Jan 5) delivers MAJOR positive surprise (RTX 5000 Super launch + data center wins announced)

- 💰 Q4 earnings (Feb 25) CRUSH with $67-68B revenue (high-end of guidance) and Q1 guide of $70B+

- 🚀 Blackwell revenue ramps to $15-20B in Q1 calendar 2026, validating "insane demand" narrative

- 🇨🇳 H200 China shipments (Feb) complete successfully, adding $2-3B upside

- 🏟️ GTC 2026 (Mar 16-19) reveals Vera Rubin on track for Q3 launch, major enterprise partnerships

- 📈 Break above $190 gamma resistance triggers technical rally to $200, then retest $212 all-time high

- ⚖️ DOJ antitrust concerns fade or case dismissed

Key metrics needed:

- Data center revenue growth >20% QoQ in Q4

- Gross margins sustain 75%+ (proving pricing power intact)

- Hyperscaler CapEx guidance remains robust for 2026

- No China export policy reversals

Probability assessment: 30% because it requires PERFECT execution across multiple fronts. NVDA already up 42% YTD with 47x P/E - high expectations baked in. Gamma resistance at $190 (318.7B) creates significant technical headwind. Needs strong catalysts to break free.

🎯 Base Case (50% probability)

Target: $180-$195 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ CES keynote delivers solid content but no fireworks - incremental gaming news, reaffirms Blackwell momentum

- 📊 Q4 earnings meet consensus ($65B revenue, $1.50-1.55 EPS) with in-line Q1 guidance

- 🏭 Blackwell production progressing well but not spectacular - steady ramp without supply surprises

- 🇨🇳 China H200 exports proceed but volumes come in lower than hoped (~40-50K units vs. 80K)

- 🤝 Groq integration on track but no immediate product announcements

- 🔄 Trading within gamma support ($185) and resistance ($190) bands for weeks

- 💤 Volatility moderates post-earnings as market digests record results and awaits next growth leg

- 📊 GTC 2026 provides roadmap confidence but no surprises

This is where the call seller wins: They cashed out at $187 with $33.60 in option value. If stock consolidates in $180-190 range through March, they captured 95%+ of the available gains and avoided the risk of catalysts disappointing. The $16M exit was optimal timing - book profits before uncertainty rather than gamble for the last 5-10%.

Why 50% probability: Stock at technical equilibrium with major catalysts ahead. Fundamentals remain EXTREMELY strong (Blackwell selling out, $500B backlog through 2026) but valuation rich (47x P/E). Most likely outcome is sideways consolidation while market waits for next growth catalyst in H2 2026 (Vera Rubin). Institutions will hold and accumulate on dips rather than chase at $190+ resistance.

📉 Bear Case (20% probability)

Target: $160-$180 (RETEST SUPPORT)

What could go wrong:

- 😰 CES keynote disappoints - no RTX 5000 Super launch, weak data center commentary triggers -5-8% sell-off

- 🚨 Q4 earnings miss or soft guidance - even small revenue miss ($63-64B vs. $65B) could gap stock down 10-15%

- 📉 Blackwell yield issues or supply constraints disclosed, pushing revenue recognition into later quarters

- 🇨🇳 China export waiver revoked or significantly restricted - removes $2-5B revenue opportunity

- ⚖️ DOJ antitrust investigation escalates with formal charges filed

- 💸 Hyperscaler spending signals start showing caution - Microsoft, Amazon, Google indicate CapEx moderation

- 🏭 Custom silicon competition accelerates - Google or Amazon announce significant internal chip deployments

- 🎢 Broader tech/semiconductor selloff drags NVDA lower despite solid fundamentals

- 🔨 Break below $185 gamma support triggers cascade to $180, then $175

Critical support levels:

- 🛡️ $185: Immediate floor (191.3B gamma) - MUST HOLD or technical damage

- 🛡️ $180: Major support (154.6B gamma) - likely heavy buying here

- 🛡️ $175-170: Deep support zone (58-62B gamma) - bear case target

- 🛡️ $160: Extended floor (66.2B gamma) + this call strike - extreme scenario

Probability assessment: Only 20% because NVIDIA's fundamentals remain exceptional (Q3 revenue $57B up 62% YoY, $500B backlog through 2026, dominant market position). Would require multiple negative catalysts aligning. However, at 47x P/E with stock down 11% from highs, any execution stumble gets magnified. The call seller clearly didn't assign high probability to this scenario or they would've exited earlier.

Call seller's P&L:

- Current profit: Collected $33.60 on likely $10-15 entry = 120-236% ROI ($6-10M gain on $16M position)

- If held to March 20 at $190 (base case): Option worth ~$30-31, additional $2-3 potential upside (~6-9% gain)

- Risk of holding: If bear case unfolds to $170, option drops to $10-11, LOSING $23-24 per contract (-70% from current) = ~$10M loss from peak value

- Decision: Lock in $6-10M gain NOW rather than risk $10M loss for $2M additional upside. Smart money math!

💡 Trading Ideas

🛡️ Conservative: Hold Cash Through CES, Buy Dip Post-Earnings

Play: Wait for volatility to settle after January-February catalysts

Why this works:

- ⏰ CES (Jan 5) and earnings (Feb 25) create binary event risk with 5-10% move potential each direction

- 💸 Implied volatility elevated pre-CES (5% implied move) - options expensive for protection

- 📊 Stock consolidating $180-190 with massive $190 gamma wall - range-bound likely continues

- 🎯 Better entry after earnings IV crush drops option premiums 40-50%

- 📉 If stock pulls back to $175-180 support on any disappointment, that's 10-15% discount from current

- 🤔 $16M institutional call exit signals smart money taking risk OFF table - why fight the trend?

Action plan:

- 👀 Watch CES keynote for product announcements and Jensen's tone on demand/supply

- 🎯 If stock dips to $180-185 support zone (gamma floor), start building position in tranches

- ✅ Look for $175-178 area if broader weakness - that's compelling risk/reward

- 📊 After earnings, assess Q1 guidance quality and Blackwell revenue trajectory

- ⏰ Re-evaluate before GTC 2026 (Mar 16-19) when next major catalyst provides clarity

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -10% drawdown if catalysts disappoint. Capture better entry if consolidation continues. Maintain optionality for when Vera Rubin catalyst emerges in Q2-Q3 2026.

⚖️ Balanced: Cash-Secured Put Selling (Copy The Exit Strategy)

Play: Sell cash-secured puts at gamma support to get paid while waiting

Structure: Sell $180 puts (January 16 expiration)

Why this works:

- 💰 Collect premium income (~$3-4 per contract) while waiting for entry

- 🎯 $180 strike sits at major gamma support (154.6B) - strong technical floor

- 🛡️ If assigned, you own NVDA at effective $176-177 cost basis (4.1% discount from current)

- 📊 Obligation to buy a stock you WANT to own anyway at a price you find attractive

- ⏰ January 16 expiration captures CES catalyst and earnings pre-announcement period

- 🤝 Essentially getting paid to "copy" the institutional positioning at key support

Estimated P&L (adjust for current prices):

- 💰 Premium collected: ~$3.50-4.00 per put (check current bid/ask)

- 📈 Max profit: Keep full premium if NVDA stays above $180 (time decay works for you)

- 📉 Assignment risk: If NVDA below $180 at Jan 16 expiry, you buy at $180 (effective cost $176-177)

- 🎯 Breakeven: $180 - $3.50 = ~$176.50 (5.3% below current price)

Mechanics:

- 💵 Capital required: $18,000 cash per put contract (must have full cash to cover assignment)

- 📊 Position sizing: Only commit capital you're willing to deploy into NVDA long-term

- ⚠️ Risk: If NVDA crashes to $160-170, you're obligated to buy at $180 (paper loss of $10-20/share initially)

- ✅ Reward: Premium income if stock stays above $180 + you establish position at good price if assigned

Entry timing:

- ⏰ Wait until 2-3 days before CES (Jan 2-3) when IV spikes and put premiums inflate

- 🎯 Target selling $180 puts for $4-5 premium when fear is highest

- ❌ Skip if premium drops below $3 (not enough reward for risk)

Risk level: Moderate (must accept stock ownership) | Skill level: Intermediate

🚀 Aggressive: Diagonal Call Spread - Play The Rebound (ADVANCED ONLY!)

Play: Buy time, sell uncertainty - capitalize if NVDA breaks $190 resistance

Structure:

- Buy March 20 $185 calls (longer dated, near the money)

- Sell January 16 $195 calls (shorter dated, out of the money)

Why this could work:

- 📊 Captures theta decay from short Jan calls while maintaining March upside exposure

- 🎯 $185 long call strike sits at major gamma support - good delta exposure

- 💰 $195 short call strike just above $190 resistance wall - low probability of assignment pre-Jan expiry

- ⏰ If CES disappoints and stock stays $185-190, short calls expire worthless, roll new short calls

- 🚀 If stock BREAKS $190 and rallies to $200+, March calls gain more than short calls lose (positive gamma)

- 📈 MAX profit scenario: Stock at $193-194 at Jan expiry (short calls expire worthless, long calls have huge value)

Why this could blow up (SERIOUS RISKS):

- 💸 CAPITAL INTENSIVE: March $185 calls cost ~$8-10 each ($800-1,000 per spread)

- ⏰ TIMING RISK: If stock doesn't move until March, you're bleeding theta on long calls

- 😱 ASSIGNMENT RISK: If NVDA gaps above $195 on CES news, short calls get assigned (must buy stock to deliver)

- 📉 BREAK-EVEN CHALLENGE: Need stock above $193-195 at March expiry to profit after spread cost

- 🎢 GAMMA RISK: If implied volatility collapses post-earnings, both legs lose value

- ⚠️ Need precise timing - early assignment on short calls before March expiry creates complications

Estimated P&L:

- 💰 Net cost: ~$5-6 debit per spread (buy March $185 call ~$10, sell Jan $195 call ~$4)

- 📈 Max profit: ~$4-5 per spread if stock at $193-195 at Jan 16 expiry (75-100% ROI)

- 🚀 Breakout profit: If stock rallies to $205+ by March, March calls worth $20+, profit ~$10-15/spread

- 📉 Max loss: Full $5-6 debit if stock below $185 at March expiry (100% loss)

- ⚠️ Early assignment: If stock above $195 before Jan 16, forced to manage short call (buy back or deliver shares)

CRITICAL WARNINGS - DO NOT attempt unless you:

- ✅ Understand diagonal spread mechanics and assignment risks

- ✅ Have buying power to handle assignment if short calls exercised

- ✅ Can actively manage position daily through CES and earnings

- ✅ Accept that even if direction correct, timing wrong = loss

- ✅ Comfortable with 100% loss of capital if thesis fails

- ⏰ Plan to roll short calls monthly (sell Feb, then Mar calls against long position)

Management plan:

- 📅 Jan 13-15: If stock below $190, let Jan short calls expire worthless, sell Feb $195 calls

- 📅 If stock above $195: Buy back Jan short calls on Jan 10-12 (before expiry), re-assess

- 📅 Post-earnings (Feb 26): Decide whether to hold March long calls through GTC or take profits

Risk level: EXTREME (can lose 100% of capital + assignment complications) | Skill level: Advanced only

Probability of profit: ~40% (requires stock to move into narrow profitable range $188-195 and proper timing)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎤 CES binary event in 6 days: Jensen Huang keynote on January 5th at 4:00 PM ET could move stock 5-10% either direction. If no RTX 5000 Super launch as some analysts expect, stock could sell off despite strong fundamentals. Conversely, major product announcements or enterprise partnership reveals could ignite rally. Options pricing 5% implied move - expect volatility spike around event.

-

💰 Valuation stretched despite pullback: Trading at 47x forward P/E after 42% YTD gain near $4.57 trillion market cap. While below October high of $212, current $187 still reflects aggressive growth expectations. Requires $65B+ quarterly revenue sustainably and Blackwell ramp to $20B+ run rate to justify multiple. Any guide-down or demand softness would trigger 15-20% correction. Zero margin of safety at this valuation - stock is priced for PERFECT execution.

-

📊 Q4 earnings execution risk (Feb 25): Consensus expects $65.41B revenue and $1.52 EPS - high bar after Q3 beat. Market will scrutinize: 1) Blackwell revenue mix (needs to be $15B+ in Q4 to validate ramp), 2) Gross margin sustainability (needs to hold 75%+ despite Blackwell transition costs), 3) Q1 FY2027 guidance quality (needs to show continued 20%+ QoQ growth), 4) China revenue contribution post-H200 waiver. Even a BEAT could sell off if guidance conservative or margins compress. Historical pattern shows NVDA often dips post-earnings even on beats as traders take profits.

-

🚨 DOJ antitrust investigation overhang: Active investigation with subpoenas issued examining bundling practices, switching costs, and RunAI acquisition. Already contributed to $279 billion single-day market cap loss when first disclosed. Potential outcomes: 1) Structural remedies forcing business model changes, 2) Fines/penalties, 3) Blocked future acquisitions (impacts M&A strategy like Groq), 4) Negative headlines creating volatility. No resolution timeline - uncertainty persists through 2026.

-

🏭 Custom silicon competitive threat accelerating: Hyperscalers (Google TPU, Amazon Trainium, Broadcom ASICs) developing in-house alternatives. While NVDA maintains 90%+ AI GPU share today, any erosion threatens premium valuation. Google already self-supplies ~10% of compute needs. If this trend accelerates to 20-30% by 2027, removes tens of billions in TAM from NVDA. Goldman Sachs projects $1.15 trillion hyperscaler CapEx through 2027 - but more competition for this spend than ever before.

-

💔 AI ROI concerns bubbling up: MIT study: 95% of organizations report NO measurable ROI from GenAI deployments. Hyperscalers added $121 billion in debt (300%+ increase) to fund AI infrastructure buildout. If ROI doesn't materialize in 2026-2027, CapEx spending could moderate sharply. NVDA derives ~90% of revenue from data center - hyper-concentrated exposure. This is THE existential risk: what if AI infrastructure spending is a bubble? Even 20-30% slowdown would crater stock.

-

🇨🇳 China export policy remains fragile: Trump administration's one-year H200 waiver with 25% levy is subject to change with geopolitical winds. NVIDIA preparing ~80,000 H200 chips for February shipment worth $2-3B, but China may impose domestic chip bundling requirements that complicate deals. Any policy reversal or escalation removes meaningful revenue opportunity (China historically 15-20% of sales). Taiwan geopolitical risk (TSMC manufacturing) adds tail risk. Chinese competitors (Huawei, Cambricon) developing domestic alternatives with government backing.

-

💸 Institutional profit-taking signal: This $16M call exit isn't isolated - CEO Jensen Huang sold $1+ billion in stock throughout 2025 under Rule 10b5-1 plan, Vanguard and BlackRock (top holders with combined 16%+ ownership) have been rebalancing. When insiders and sophisticated funds take profits at these levels rather than accumulating, it signals caution. Not bearish on long-term story, but risk/reward at $187 less favorable than $160-170 support levels.

-

📈 Gamma ceiling at $190 creates mechanical resistance: Massive 318.7B call gamma at $190 (STRONGEST single level in entire options complex) means market makers will systematically SELL stock into any rally above this level to hedge their exposure. This isn't bullish enthusiasm - it's mechanical headwind. Would need sustained institutional buying or major catalyst (blockbuster CES/earnings) to overcome. Current price at $188 sitting RIGHT under this ceiling. Technical breakout requires clearing $195-200 decisively.

-

🎢 Volatility whipsaw risk: NVDA's 2025 range of $86 to $212 (145% spread) shows this stock can move VIOLENTLY on sentiment shifts. 41% YTD gain impressive but masks the -59% drawdown from highs to April low on Trump tariff fears. Stock can gap 5-10% overnight on macro headlines, Fed policy, semiconductor sector rotation, or no news at all. Not for weak stomachs. Max historical drawdown of 59% shows how fast sentiment can turn even for quality companies.

-

🕐 Catalyst density = execution risk: Three major binary events in 80 days (CES Jan 5, earnings Feb 25, GTC Mar 16-19) means heightened volatility through March option expiration. Each event could move stock 5-10%. Probability of navigating ALL THREE perfectly without stumble is low. One disappointing catalyst could erase gains from the others. This is why smart money (like this $16M call seller) is derisking BEFORE the gauntlet rather than gambling through it.

🎯 The Bottom Line

Real talk: Someone just locked in $6-10 MILLION in profits by exiting a winning NVDA call position ahead of three massive catalysts. This isn't fear - this is professional risk management. They rode NVDA from ~$160-170 (when they likely bought these $160 calls) all the way to $187, capturing 120-200%+ returns. Now with CES in 6 days, earnings in 57 days, and GTC in 76 days, they're taking risk OFF the table rather than gambling for the last 5-10% of upside.

What this trade tells us:

- 💰 Sophisticated player prefers LOCKING IN $6-10M gain over risking it for additional $2-3M potential profit

- ⚖️ They're worried enough about near-term volatility to exit 80 days BEFORE expiration (March 20) rather than hold

- 🎯 The timing (6 days before CES, 2 months before earnings) shows they see binary risk - catalysts could go either way

- 📊 They accumulated at $160 strike when stock was likely $160-175, rode the rally, and EXIT into $190 resistance - textbook technical trading

- ⏰ March 20 expiration would capture all three catalysts but they don't want the stress - profit-taking WINS

This is NOT a "sell everything and run" signal - it's a "mission accomplished, secure the gains" signal.

If you own NVDA:

- ✅ Consider trimming 20-30% at $185-190 levels if you've got nice gains - lock in some profits, reduce exposure

- 📊 If holding through catalysts, set MENTAL STOP at $180 (major gamma support) to protect capital

- ⏰ Don't get greedy - up 42% YTD is FANTASTIC. Protecting profits is smart, not cowardly.

- 🎯 If CES and earnings both beat AND stock clears $200, you can re-enter trimmed shares

- 🛡️ Consider buying 1-2 protective puts at $180 strike per 100 shares if holding large position (portfolio insurance)

If you're watching from sidelines:

- ⏰ DO NOT chase above $185-190 - you're buying at resistance with immediate catalysts ahead

- 🎯 Wait for post-CES or post-earnings pullback to $175-180 support (gamma floor) for quality entry

- 📈 Looking for confirmation of: Blackwell revenue $15B+ in Q4, gross margins 75%+, Q1 guide $70B+, Vera Rubin on track for Q3

- 🚀 Longer-term (6-12 months), Vera Rubin launch (Q3 2026) and $20B Groq integration are legitimate catalysts for $200-220 if execution delivers

- ⚠️ Current valuation (47x P/E) requires flawless execution - one stumble and it's back to $160-170 support

If you're considering options strategies:

- 🛡️ Cash-secured put selling at $180 strike (January 16 expiry) offers premium income + entry at support

- ⚠️ Avoid buying calls before CES - implied volatility elevated, theta decay brutal, IV crush post-event

- 📊 Diagonal spreads (buy March calls, sell January calls) for advanced traders who can manage assignment risk

- ❌ AVOID naked put selling or aggressive bullish bets before catalysts - downside gaps can be 10%+

Mark your calendar - Key dates:

- 📅 January 5, 2026 (Sunday) 4:00 PM ET - CES 2026 keynote with Jensen Huang (6 DAYS!)

- 📅 January 6-7 - Post-CES price action and analyst reactions

- 📅 January 16 - Monthly OPEX (5% implied move window closes)

- 📅 Mid-February - H200 China shipments (~80K units)

- 📅 February 25, 2026 (after close) - Q4 FY2026 earnings report

- 📅 February 26 - Post-earnings volatility and guidance assessment

- 📅 March 16-19, 2026 - GTC 2026 conference in San Jose

- 📅 March 20, 2026 - Quarterly triple witch, expiration of this $16M call trade

- 📅 Q3 2026 (July-Sept) - Vera Rubin architecture launch expected

Final verdict: NVIDIA's long-term AI dominance thesis remains INCREDIBLY compelling - 90%+ market share, Blackwell selling out with "insane" demand, $500B backlog through 2026, $20B Groq acquisition, Vera Rubin roadmap positioning company for continued dominance. BUT, at 47x P/E after 42% YTD gain with THREE major catalysts in next 80 days, the risk/reward is NO LONGER favorable for aggressive positioning at $187-190 resistance. The $16M call exit is a CLEAR signal: smart money is securing gains rather than gambling through volatility.

Be patient. Let catalysts play out. Look for $175-180 support entries. The AI revolution isn't going anywhere - NVDA will still be the leader in 3-6 months, and you'll sleep better owning it at $175 than chasing at $190.

Winners secure profits. Losers hope for more. Be a winner. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 0.65 (TYPICAL classification) reflects this trade's size relative to recent NVDA history - it represents a large institutional position exit but not unprecedented activity. Always do your own research and consider consulting a licensed financial advisor before trading. CES, earnings, and GTC create binary event risks with potential for 5-10% gaps either direction. The call seller may have complex portfolio hedging needs not applicable to retail traders. Profit-taking at $187 after entry around $160-170 represents sound risk management, not a bearish signal on NVIDIA's long-term prospects.

About Nvidia Corporation: Nvidia is a leading developer of graphics processing units with expanding focus on AI infrastructure, providing GPUs for artificial intelligence applications, CUDA software for model development, and data center networking solutions to integrate multiple GPUs for complex computational workloads, with a market cap of $4.57 trillion in the Semiconductors & Related Devices industry.