🛡️ ORCL $10.2M Put Protection After Earnings Miss - Smart Money Hedging AI Infrastructure Bet!

📅 December 15, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $10.2 MILLION on ORCL put protection across three strategic strikes today! This institutional hedging spree includes $5.9M in near-term December 19th $190 puts, $2.6M in March $140 puts, and $1.7M in January $160 puts - all purchased AFTER Oracle's brutal 11% crash on December 9th earnings miss. Translation: Smart money is doubling down on downside protection, betting Oracle's AI infrastructure spending spree ($50B capex!) has further to fall despite already being down from $205 highs.

📊 Company Overview

Oracle Corporation (NYSE: ORCL) is a global enterprise software and cloud infrastructure powerhouse transforming into an AI infrastructure provider:

- Market Cap: $545.8 Billion (top 10 software company)

- Industry: Prepackaged Software / Cloud Infrastructure

- Current Price: $184.25 (down from $205 pre-earnings highs, near 52-week low)

- Primary Business: Oracle provides enterprise applications and infrastructure offerings through various IT deployment models including on-premises, cloud-based, and hybrid solutions. The company is pioneering in relational database systems and cloud infrastructure, with major AI partnerships including the $500B Stargate project with OpenAI.

💰 The Option Flow Breakdown

The Tape (December 15, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:53:36 | ORCL | ASK | BUY | PUT $160 | 2026-01-09 | $1.7M | $160 | 10K | 394 | 10,000 | $182.09 | $1.68 |

| 11:21:02 | ORCL | ASK | BUY | PUT $190 | 2025-12-19 | $5.9M | $190 | 9.2K | 1,000 | 7,500 | $184.25 | $7.85 |

| 11:21:02 | ORCL | ASK | BUY | PUT $140 | 2026-03-20 | $2.6M | $140 | 10K | 2,400 | 7,500 | $184.25 | $3.49 |

🤓 What This Actually Means

This is a LAYERED DEFENSIVE HEDGE across three timeframes showing serious concern about Oracle's trajectory post-earnings disaster. Here's the breakdown:

Trade #1: $190 Dec 19 Puts - $5.9M (LARGEST)

- 🎯 Near-term insurance: Only 4 days to expiration - betting on IMMEDIATE further weakness

- 💸 Expensive premium: Paying $7.85 per share ($785 per contract) for just 4 days of protection!

- 📊 Strike significance: $190 is just 3.2% above current price - this is IN-THE-MONEY protection

- ⚠️ Urgent timing: December 19th is monthly/quarterly OPEX - expects volatility into year-end

- 🔥 Unusual Score: 4.37 Z-score (extremely unusual) - this is 9.2x larger than average ORCL put volume

Trade #2: $140 March 20 Puts - $2.6M (DEEPEST)

- 🛡️ Disaster insurance: $140 strike is 24% below current price - protecting against CATASTROPHIC scenario

- ⏰ Extended timeline: 95 days to expiration captures Q2 FY2026 earnings (March 2026) and Stargate milestones

- 💰 Cheaper premium: Only $3.49 per share for deep protection shows they expect gradual decline, not crash

- 📉 Bearish thesis: Only profitable if ORCL falls below $136.51 by March - implies belief in 25%+ downside

- 🔥 Unusual Score: 95.64 Z-score (EXTREME) - this is 4.17x normal activity and RARELY seen

Trade #3: $160 Jan 9 Puts - $1.7M (MEDIUM-TERM)

- ⚖️ Balanced protection: $160 strike is 12.5% below current - bridges the gap between near/far-term

- ⏰ Strategic timing: 25 days to expiration captures year-end positioning and January momentum

- 📊 Volume surge: 10,000 contracts vs only 394 open interest - BRAND NEW positioning

- 🎯 Technical level: $160 aligns with major support from pre-earnings rally - betting it breaks

- 🔥 Unusual Score: 107.81 Z-score (OFF THE CHARTS) - this is 25.4x average size!

What's REALLY happening here:

This trader is building a PUT LADDER - protection at three strikes across three timeframes to hedge a massive long Oracle position (likely stock or calls accumulated during the +69% YTD rally). The structure reveals their thesis:

- Near-term (Dec 19): Expect immediate weakness as post-earnings selling continues into year-end tax loss harvesting

- Medium-term (Jan 9): Believe stock tests $160 support as AI infrastructure spending concerns mount

- Long-term (March 20): Genuine fear of 25%+ correction if Stargate delays or free cash flow concerns deepen

This is NOT a directional bearish bet - it's sophisticated portfolio insurance by someone who's made HUGE money on Oracle's AI rally and refuses to give it back.

The timing is CRITICAL: They bought AFTER the 11% earnings crash, suggesting they think the selling isn't done. If they believed $182-184 was the bottom, they'd be buying calls, not puts. The combined $10.2M premium represents protection on a position worth $150-200M+ at minimum.

Combined Unusual Score: EXTREME - All three trades show Z-scores above 4.0, indicating this level of put buying happens only a few times per year. The market is pricing serious downside risk despite Oracle's strong long-term AI narrative.

📈 Technical Setup / Chart Check-Up

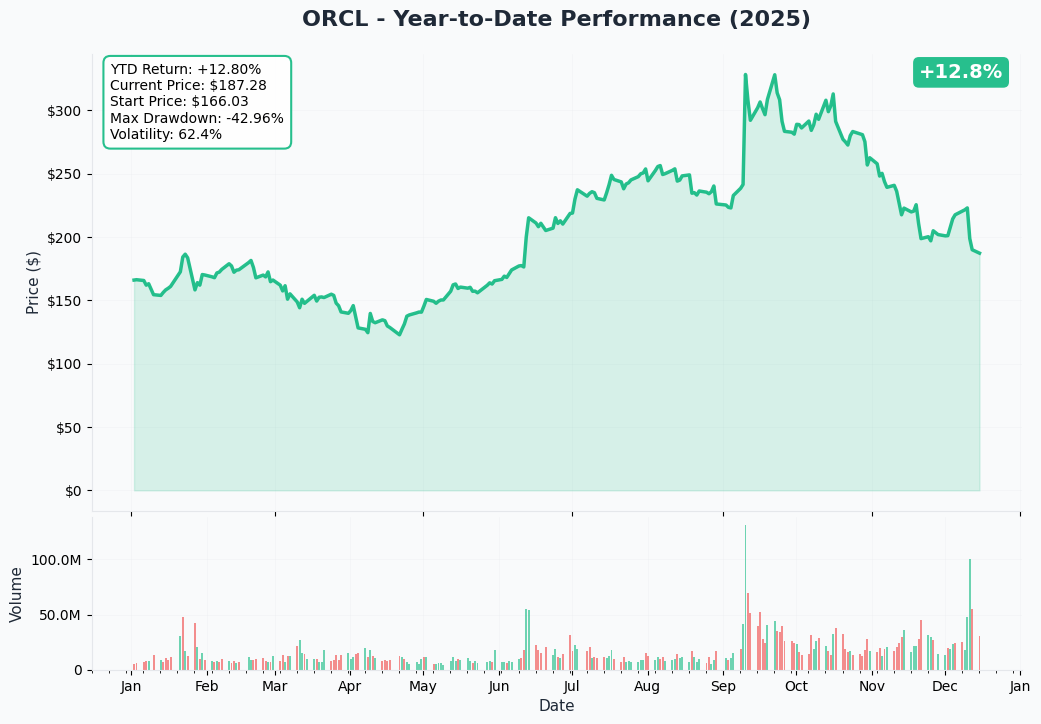

YTD Performance Chart

Oracle had an EXPLOSIVE year - up +69% YTD through December 2024 from $110 to highs of $205 - before the brutal December 9th earnings crash knocked it down 11% in a single day to $183. The chart tells a dramatic transformation story from database dinosaur to AI infrastructure powerhouse.

Key observations:

- 🚀 Parabolic rally: Vertical move from $140 in September to $205 in early December on Stargate project euphoria

- 💥 Earnings disaster: December 9th gap down from $205 to $183 on revenue/EPS miss and weak guidance

- 📈 Support holding (barely): Currently testing $180-185 zone which was resistance in November - needs to hold!

- 🎢 High volatility regime: Stock moved from $110 to $205 to $183 in 12 months - this is NOT a stable utility stock

- ⚠️ Volume spike: Massive selling volume on Dec 9th suggests institutional distribution - not retail panic

The chart shows Oracle at a CRITICAL juncture: Will the $180-185 support (former resistance) hold and lead to a bounce back toward $200? Or will it break down toward $170 and eventually test the $160 level where the medium-term put buyer is positioned?

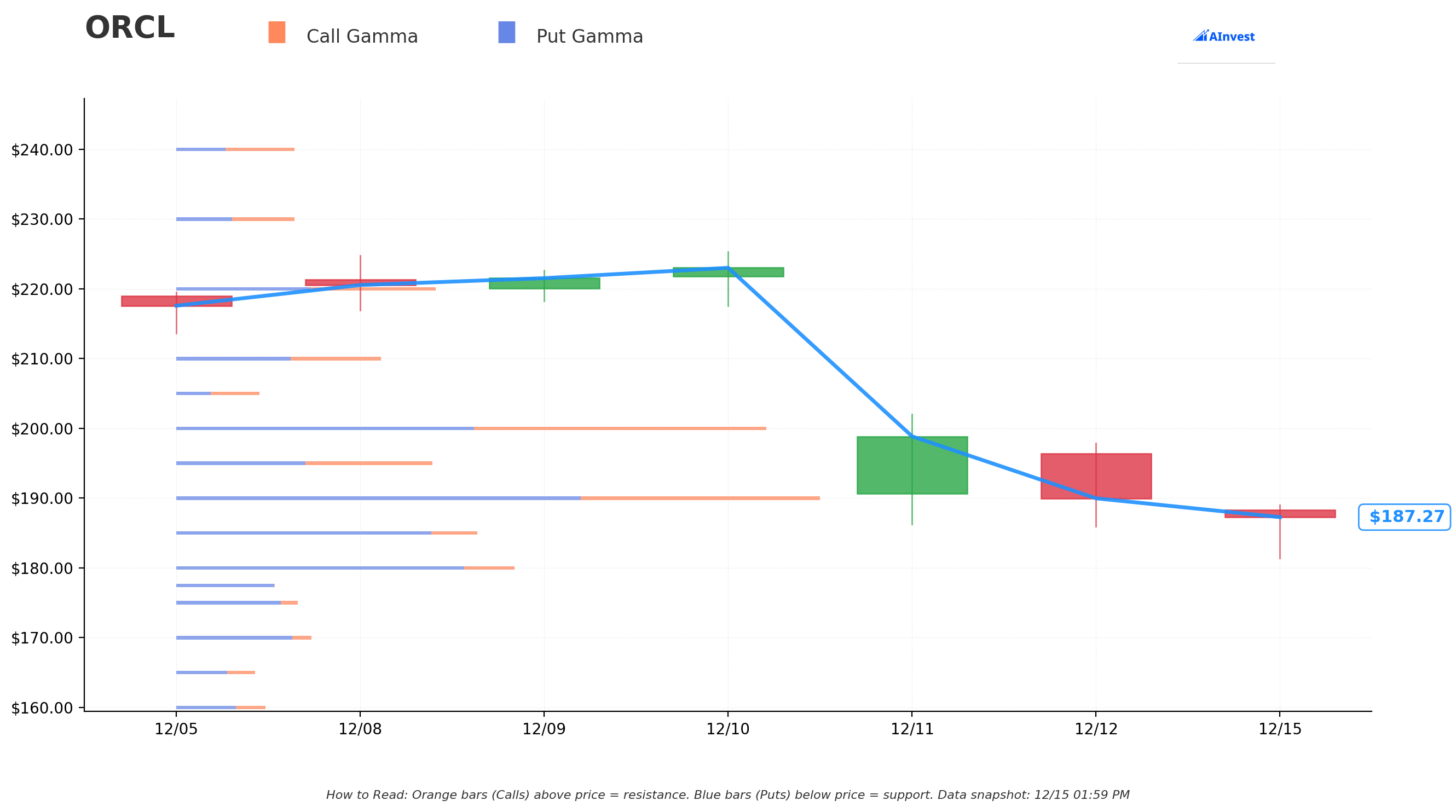

Gamma-Based Support & Resistance Analysis

Current Price: $187.16

The gamma exposure map reveals where options dealers will provide liquidity and create price magnets:

🔵 Support Levels (Put Gamma Below Price):

- $185 - Immediate support with 16.7B total gamma (strongest nearby floor!)

- $180 - Major structural support at 18.8B gamma (dealers will defend this aggressively)

- $177.50 - Secondary floor with 5.5B gamma

- $175 - Deep support at 6.7B gamma (psychological round number + options interest)

- $170 - Extended floor with 7.5B gamma (critical long-term support from September levels)

🟠 Resistance Levels (Call Gamma Above Price):

- $190 - IMMEDIATE CEILING with 35.6B gamma (STRONGEST LEVEL - this is where the near-term put is struck!)

- $195 - Secondary resistance at 14.1B gamma (3% overhead)

- $200 - Psychological barrier with 32.5B gamma (pre-earnings high zone)

- $210 - Extended resistance at 11.2B gamma

- $220 - Major ceiling with 13.3B gamma (14% rally required)

What this means for traders:

Oracle is trading in a TIGHT range between $185 support (16.7B gamma) and crushing $190 resistance (35.6B gamma - the SINGLE LARGEST LEVEL on the entire gamma map). The put buyer who struck the $190 December puts knew EXACTLY what they were doing - that's a brick wall of call gamma that will prevent rallies.

Notice anything? The near-term put strike of $190 is positioned at the STRONGEST resistance level (35.6B gamma), the medium-term $160 put is positioned just below major support zones, and the long-term $140 put is deep out-of-the-money disaster insurance. This is textbook professional hedging - strike selection based on gamma concentrations, not random numbers.

Net GEX Bias: Bearish (143.7B put gamma vs 99.3B call gamma) - Overall positioning heavily favors downside, with put gamma dominating. This creates a "sticky" environment where rallies will be capped by dealer selling and dips will be cushioned by dealer buying at support levels.

The gamma structure suggests Oracle is STUCK in a $180-190 range until a major catalyst (Stargate news, next earnings, macro shift) provides enough force to break out either direction. The put buyers are betting on a breakdown below $180 which would accelerate momentum toward $175, then $170, and eventually test the $160 level.

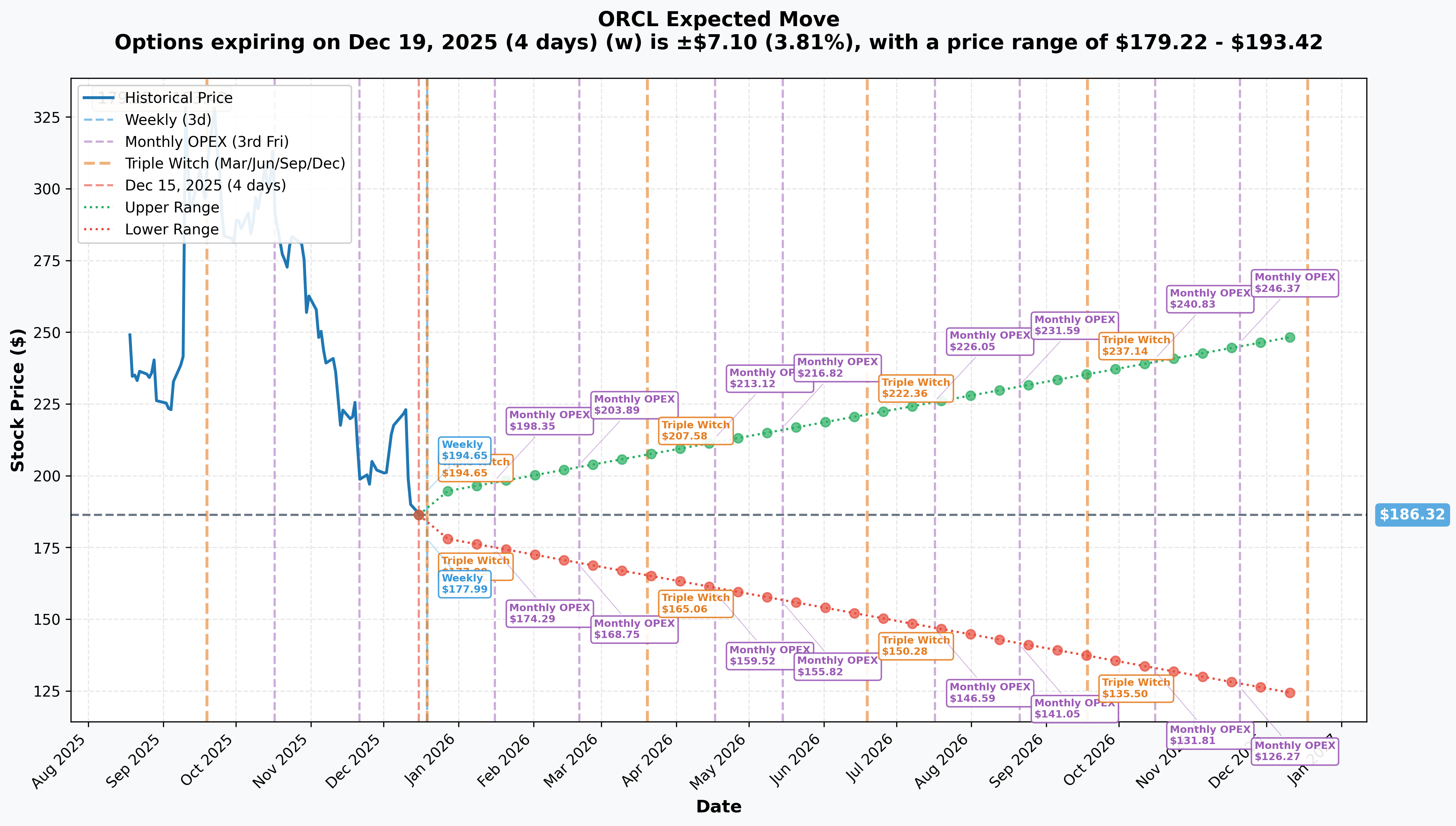

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly/Monthly/Triple Witch (Dec 19 - 4 days!): ±$7.10 (±3.81%) → Range: $179.22 - $193.42

- 📅 Monthly OPEX (Jan 16 - 32 days): ±$11.99 (±6.48%) → Range: $174.29 - $198.35

- 📅 Quarterly Triple Witch (March 20 - 95 days): ±$21.52 (±11.54%) → Range: $165.06 - $207.58

- 📅 LEAPS (Dec 18, 2026 - 368 days): ±$63.13 (±33.88%) → Range: $123.19 - $249.45

Translation for regular folks:

Options traders are pricing a 3.8% move ($7) by Friday's December 19th expiration - which means the $190 put buyer paid $5.9M for protection that's barely in-the-money! The upper range of $193.42 suggests the market thinks Oracle struggles to reclaim $190+ by Friday - exactly what the put buyer is betting on.

The January 16th expiration (32 days) has a lower range of $174.29, meaning there's real possibility Oracle trades to $174 over the next month. This aligns with the $160 January put buyer's thesis - if the stock breaks $175, momentum could carry it to $160.

Most telling: The March 20th lower range of $165.06 validates the $140 March put position - while extreme, a move to $140 (24% decline) falls within the options market's expected range of outcomes over the next 95 days.

Key insight: The sharp increase in implied moves from 3.8% (weekly) to 6.5% (monthly) to 11.5% (quarterly) reflects escalating uncertainty around Oracle's AI infrastructure spending payoff timeline. Market expects volatility to INCREASE, not decrease, in coming months.

🎪 Catalysts

💥 Recent Catalysts (Already Happened)

Q2 FY2025 Earnings Miss - December 9, 2024 (6 DAYS AGO!) 📊

Oracle's most recent earnings triggered an 11% single-day crash - the worst day for the stock in 2024 - as the company missed on both revenue and EPS while guiding conservatively (CNBC):

- 📊 Revenue Miss: $14.06B actual vs $14.1B consensus (small but meaningful at this valuation)

- 💰 EPS Miss: $1.47 actual vs $1.48 consensus (CNBC)

- 🔥 Cloud Infrastructure (OCI) Growth: +52% YoY to $2.4B (strong, but not enough) (Oracle Press Release)

- 💸 Free Cash Flow DISASTER: Negative $10.33 billion in H1 FY2025 due to massive $20.54B capex (The Motley Fool)

- 📉 Q3 Guidance Disappointing: Revenue growth of only 7-9% vs higher analyst expectations (CNBC)

- 🏦 Debt Explosion: Total debt (including leases) exceeded $124 billion, up from $89B a year earlier (The Motley Fool)

Why this matters for the put trades: The earnings miss revealed that Oracle's aggressive $50B capex strategy is creating MASSIVE cash flow and debt burdens with uncertain payback timelines. Revenue grew only 9% YoY while debt grew 40%+ - that's an unsustainable trajectory. The put buyers are betting the market hasn't fully digested the implications of negative $10B free cash flow and $124B debt load.

Analyst reactions were mixed - KeyBank maintained buy rating calling it "a bit of a stumble," while Bank of America cut price target from $368 to $300 (TipRanks). The stock dropped from $205 to $183 (11%) but hasn't bounced meaningfully, suggesting institutional investors remain cautious.

🚀 Upcoming Catalysts (Next 6 Months)

Stargate Project Progress - $500B AI Infrastructure Joint Venture 🌟

Oracle's landmark partnership with OpenAI and SoftBank announced January 21, 2025 represents potentially the most transformative catalyst in company history:

- 🏭 Unprecedented scale: $500 billion investment over multiple years to build 10 gigawatts of AI data center capacity

- 📍 First site operational: Abilene, Texas facility expected Q1-Q2 2026 (CRITICAL MILESTONE!)

- 🌐 Five new sites announced: September 23, 2025 expansion brought total to nearly 7 gigawatts planned (OpenAI)

- 💰 Revenue visibility: Oracle's $455 billion Remaining Performance Obligations (RPO) backlog includes massive Stargate contracts (Oracle Investor Relations)

- 🎯 GPU purchases: Oracle will buy approximately 400,000 NVIDIA GB200 GPUs at $40B cost, then lease computing to OpenAI under 15-year agreement (Network World)

Why this is CRITICAL for put buyers: If Stargate encounters ANY delays, cost overruns, or scope reductions, Oracle's entire growth narrative collapses. The first Abilene site going operational in Q1-Q2 2026 is THE proof point that this isn't vaporware. The March 20th $140 puts expire RIGHT before this milestone - the put buyer may be positioning for pre-Stargate disappointment or delays.

Q3 FY2025 Earnings - March 10, 2025 (85 DAYS AWAY) 📊

Oracle's next earnings report in March will be CRUCIAL for validating whether Q2's miss was a one-time hiccup or start of a trend:

- 📊 Consensus expectations: Revenue $14.13B vs $14.39B expected (another potential miss!) (CNBC)

- 💰 EPS expectations: $1.47 adjusted vs $1.49 expected

- 🔥 OCI growth target: Wall Street watching for sustained 50%+ growth to justify AI premium valuation

- 💸 Free cash flow: Must show improvement from negative $10B H1 position or debt concerns escalate

- 🏗️ Stargate updates: Any commentary on construction progress, timeline, or customer commitments will move stock 10-15%

- 📈 RPO growth: Expecting continued growth toward $500B milestone

This falls EXACTLY in the window of the $140 March 20 puts! If Oracle misses AGAIN in March or guides conservatively due to macro uncertainty, the stock could cascade from $180s to $160s, then test $140s as debt/cash flow concerns dominate.

Oracle Database@AWS General Availability - 2025 🤝

Oracle's multicloud database partnerships expanded significantly in 2024 with preview launch of Oracle Database@AWS in late 2024, with general availability expected in 2025:

- 💻 Early customers: Best Buy, State Street, Vodafone, Fidelity Investments already testing

- 📈 Growth rate: Multicloud database revenue grew 115% from Q3 to Q4 FY2025 - validating product-market fit (Oracle Press Release)

- 🌐 Strategic significance: Proves Oracle can win on competitors' platforms without vendor lock-in

- 💰 Revenue upside: Could become multi-billion dollar segment by late 2026 if adoption accelerates

Why this matters: Multicloud revenue growth of 115% quarter-over-quarter is ONE OF THE FEW bright spots in Oracle's story. If AWS general availability drives another step-function increase, it could partially offset Stargate execution concerns. Conversely, if adoption slows or AWS prioritizes its own database offerings, Oracle's "Switzerland of cloud" strategy fails.

NVIDIA Blackwell Platform Deployment - H1 2026 🎮

Oracle announced it will be first cloud provider to offer NVIDIA Blackwell-based AI supercomputers, with orders for up to 131,072 NVIDIA Blackwell GPUs:

- 🔬 OCI Zettascale10: Connecting hundreds of thousands of GPUs across multiple data centers for 16 zettaFLOPS peak performance (Oracle Press Release)

- ⏰ Timeline: H1 2026 delivery expected (aligned with Stargate first site operational)

- 💪 Competitive positioning: Blackwell offers 5x performance vs current H100 generation

- 💸 Supply risk: NVIDIA facing global demand - any GPU delivery delays push Oracle's data center ramps to the right

This is a double-edged sword: Successful Blackwell deployment validates Oracle's AI infrastructure leadership and could drive stock to $220+. Delays or performance issues crater the AI growth story and stock tests $140-160 support levels - exactly where the put buyers are positioned.

⚠️ Risk Catalysts (Negative)

Data Center Construction Delays 🏗️

Oracle is building/expanding 166 data centers simultaneously - an unprecedented construction program requiring multi-gigawatt power allocations, specialized cooling, and massive GPU deliveries (CIO Dive):

- ⚡ Power constraints: Securing multi-gigawatt power in Texas, Ohio, New Mexico increasingly difficult

- 🏭 Permitting risk: Government approvals for large-scale facilities can take 12-24 months

- 📦 Supply chain: Cooling systems, networking equipment, construction materials all facing inflation

- ⏰ Timeline pressure: Any delays in Stargate first site (Q1-Q2 2026) would be CATASTROPHIC for stock

If the first Abilene site slips to H2 2026 or later, Oracle's stock could test the $140 March put strike as the $455B RPO thesis gets questioned.

Debt and Free Cash Flow Crisis 💸

Oracle's aggressive AI buildout created a financial powder keg:

- 🔴 Negative $10.33B free cash flow in H1 FY2025 (The Motley Fool)

- 💰 $124 billion total debt (including leases) up from $89B a year ago

- 📈 Interest expense: Over $1 billion per quarter (WebProNews)

- 📉 $18 billion debt raise in September 2024 alone

If interest rates remain elevated or credit markets tighten, Oracle's cost of capital could spike, forcing capex cuts or Stargate delays. The put buyers are clearly pricing this scenario - $10B negative cash flow is NOT sustainable indefinitely.

Revenue Recognition Timing Gap 📊

Oracle's $455 billion RPO must convert to revenue over time - approximately 33% within 12 months, but the remainder stretches over many years (Sherwood News). Key concerns:

- 🕐 First Stargate revenue: Not until Q1-Q2 2026 when facilities go operational

- 🤔 Customer deployment delays: If OpenAI/xAI/Meta slow workload migrations, revenue lags bookings

- 📉 Wall Street impatience: Market may not tolerate quarters of capex pain before revenue materialize

- ⚖️ Valuation compression: If revenue recognition slows, Oracle's 7.5x sales multiple (vs 5.2x historical average) compresses

This timing gap is EXACTLY what the put buyers are exploiting - betting Oracle can't sustain investor confidence during the 12-18 month "valley of death" between massive capex spend and revenue realization.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, catalyst timing, and the put trade structure, here are the scenarios through March 20th (longest put expiration):

📈 Bull Case (20% probability)

Target: $210-$220

How we get there:

- 💪 Q3 earnings (March 10) BEAT on both revenue ($14.5B vs $14.4B expected) and EPS ($1.52 vs $1.49)

- 🏗️ Stargate first site construction AHEAD of schedule - operational timeline pulled in to Q1 2026

- 📊 Free cash flow improves to only -$2-3B in Q3 (vs -$10B H1) as data centers begin operations

- 🌐 Multicloud database revenue accelerates to $1B+ quarterly run rate on AWS GA success

- 🤖 OpenAI announces EXPANSION of Stargate partnership to 12 gigawatts (from 10 GW)

- 📈 OCI revenue guidance raised to 80%+ growth for FY2026 (from 70% target)

- 🇨🇳 China export clarity removes overhang, adds upside optionality

- 📊 Breakout above $190 gamma resistance triggers technical rally to $200, then $210-220

Key metrics needed:

- RPO growth toward $500B milestone in Q3 report

- Debt stabilization (no new massive raises)

- Operating margins expanding despite capex drag

- Blackwell GPU delivery confirmation for H1 2026

Why only 20% probability: Requires PERFECT execution across multiple fronts while stock already up 69% YTD before the earnings crash. The gamma ceiling at $190 (35.6B) creates enormous headwinds. Oracle needs to prove it can convert $455B RPO to actual revenue while managing $124B debt and negative cash flow - that's an incredibly high bar.

All three put trades expire WORTHLESS in this scenario - the $10.2M is simply insurance premium lost.

🎯 Base Case (55% probability)

Target: $170-$190 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Q3 earnings meet or slightly miss conservative consensus (~$14.0-14.2B revenue, $1.45-1.48 EPS)

- 🏗️ Stargate construction progressing but no major updates - timeline remains Q1-Q2 2026 (no acceleration)

- 💸 Free cash flow remains deeply negative (-$5-7B in Q3) but narrative shifts to "investment phase"

- ⚖️ OCI growth solid (45-55% range) but not accelerating enough to expand valuation multiple

- 🤝 Multicloud revenue steady but not spectacular - AWS GA sees moderate adoption

- 🇨🇳 China remains question mark - neither major positive nor catastrophic negative

- 📊 Stock trades within gamma support ($175-180) and resistance ($190-195) bands for weeks

- 💤 Volatility stabilizes as market digests the shift from "growth story" to "show me the revenue"

This is the sweet spot for put sellers / covered call writers: Stock consolidates in $170-190 range, implied volatility remains elevated (great premium collection), but no catastrophic breakdown. The put buyers' insurance expires with minimal value, but downside protection served its purpose during uncertain period.

Put P&L in Base Case:

- $190 Dec 19 puts: Expire worthless if stock above $190 Friday (-$5.9M loss)

- $160 Jan 9 puts: Worth $5-10 if stock at $170-175, loss of $0.8-1.2M

- $140 March 20 puts: Worth $5-15 if stock at $170-180, loss of $1.1-2.0M

- Total loss: $7.8-9.1M out of $10.2M (76-89% loss on hedges)

Why 55% probability: This is the PATH OF LEAST RESISTANCE given current setup. Oracle's fundamentals remain solid (data center growth, OpenAI partnership, product roadmap) but valuation offers no cushion after 69% YTD gain. Most institutions will hold and wait for Stargate operational proof in mid-2026. Neither bulls nor bears have conviction to force breakout/breakdown.

📉 Bear Case (25% probability)

Target: $140-$160 (TEST THE PUT STRIKES!)

What could go wrong:

- 😰 Q3 earnings MISS again with revenue below $14B and EPS below $1.45 - "Houston, we have a pattern"

- 🚨 Stargate timeline DELAYS announced - first site pushed from Q1-Q2 to H2 2026 or later

- 💸 Free cash flow DETERIORATES to -$12-15B in Q3 as capex accelerates without revenue offset

- 🏦 Debt rating DOWNGRADE by Moody's or S&P due to unsustainable cash burn

- 📉 Q4 guidance extremely conservative (revenue growth only 5-7%) citing macro uncertainty

- 🤖 OpenAI REDUCES Stargate scope or spreads deployment over longer timeframe

- 🇨🇳 New China export restrictions hit MI325X or other products without warning

- 💰 Margin compression from aggressive infrastructure pricing to win customers

- 📊 Broader tech selloff drags software stocks lower (recession fears, Fed policy error)

- 🔨 Break below $180 gamma support triggers cascade to $170, then $160, potentially $140

Critical support levels:

- 🛡️ $185: Current support (16.7B gamma) - already tested, must hold!

- 🛡️ $180: Major floor (18.8B gamma) - MUST HOLD or momentum shifts decisively bearish

- 🛡️ $175: Secondary floor (6.7B gamma) - psychological support

- 🛡️ $170: Deep support (7.5B gamma) - September rally levels

- 🛡️ $160: Critical level ($160 Jan put strike) - major institutional protection here

- 🛡️ $140: Disaster floor ($140 March put strike) - 25% down from current

Probability assessment: 25% because it requires MULTIPLE negative catalysts to align simultaneously. However, Oracle's current setup creates asymmetric downside risk - the combination of $124B debt, -$10B free cash flow, stretched valuation, and execution-dependent AI thesis means ONE major disappointment could trigger cascade.

The put buyers clearly think this scenario has 25-30%+ odds or they wouldn't pay $10.2M across three strikes for this protection.

Put P&L in Bear Case:

- Stock at $160 by Jan 9: $160 puts worth $0 (at-the-money), loss = -$1.7M

- Stock at $150 by Jan 9: $160 puts worth $10.00, profit = $8.32/share × 10,000 = $83.2M gain (+$81.5M profit!)

- Stock at $175 by Dec 19: $190 puts worth $15.00, profit = $7.15/share × 7,500 = $53.6M (+$47.7M profit!)

- Stock at $140 by March 20: $140 puts worth $0 (at-the-money), loss = -$2.6M

- Stock at $120 by March 20: $140 puts worth $20.00, profit = $16.51/share × 7,500 = $123.8M (+$121.2M profit!)

Total profit in severe bear case (stock to $140-150): $150-200M+ on $10.2M investment (15-20x return!)

💡 Trading Ideas

🛡️ Conservative: Sell Covered Calls or Cash-Secured Puts (Income Strategy)

Play: Use Oracle's elevated volatility to collect premium while staying neutral

Structure Options:

Option A - Own the stock? Sell covered calls:

- 📞 Sell $195 calls against every 100 shares (January 16 expiration)

- 💰 Collect $5-6 per share ($500-600 per contract)

- 🎯 Keeps you in the trade if stock rallies to $195 (5% upside from current $187)

- ⏰ 32 days to collect premium while waiting for Q3 earnings clarity

Option B - Want to own ORCL? Sell cash-secured puts:

- 📉 Sell $175 puts (January 16 expiration)

- 💰 Collect $4-5 per share ($400-500 per contract)

- 🎯 Get assigned at $175 (6.5% below current) if stock drops - gives you margin of safety

- 🛡️ $175 is just below major gamma support at $180 - good technical level

Why this works:

- ⚡ Implied volatility elevated post-earnings (option premiums JUICY!)

- 📊 Stock in consolidation range $180-190 - perfect for theta decay strategies

- 💸 Collect income while market digests Oracle's debt/cash flow concerns

- ⏰ 30-45 day timeframes capture premium decay without major earnings risk (Q3 not until March)

- 🤝 Essentially betting on the BASE CASE scenario (choppy range-bound trading)

Risk level: Low (defined risk, keep stock/cash) | Skill level: Beginner-friendly

Expected outcome: Collect 2.5-3.5% monthly returns on capital while Oracle consolidates. May get assigned on puts if stock breaks down to $170s, but that's an acceptable entry point for long-term holders.

⚖️ Balanced: Post-Holiday Put Spread (Copy the Pros - DEFERRED ENTRY)

Play: After December 19th OPEX, mirror institutional put structure at better prices

Structure: Wait until December 20-23, then buy $180 puts, sell $160 puts (March 20 expiration - SAME as the $2.6M institutional trade)

Why WAIT until after Dec 19:

- 🎢 IV crush after December OPEX makes put spreads 30-40% cheaper

- 📊 Year-end tax loss selling creates opportunities if stock dips to $175-180

- ⏰ Removes near-term gamma pin risk around December 19th expiration

- 💰 Better risk/reward entering AFTER the $190 Dec puts expire

Estimated P&L (post-IV crush pricing):

- 💰 Pay ~$7-9 net debit per spread (vs $12-14 now)

- 📈 Max profit: $1,100-1,300 if ORCL below $160 at March expiration (stock down 15%)

- 📉 Max loss: $700-900 if ORCL above $180 (defined and limited)

- 🎯 Breakeven: ~$171-173

- 📊 Risk/Reward: ~1.3:1 to 1.5:1 (acceptable for defined-risk bearish play)

Entry timing:

- ⏰ Wait until December 20-27 (post-OPEX, post-holiday)

- 🎯 Only enter if stock still trading $182-188 range (gives room to work)

- ❌ Skip if stock already below $175 (spread too close to profit zone)

- ✅ Need to see continued weakness or bad news flow to justify bearish bet

Position sizing: Risk only 3-5% of portfolio (this is directional speculation on debt/cash flow concerns)

Why this works:

- 🎯 Targets gamma support zone at $160-180 where institutions clearly positioned

- 📊 March 20 expiration captures Q3 earnings (March 10) and Stargate updates

- 🤝 Essentially "copying" the $2.6M smart money trade at better entry after IV drops

- 🛡️ Defined $2,000 max risk per spread - can sleep at night

- ⚖️ Betting on BASE CASE (consolidation $170-190) to BEAR CASE (breakdown to $160) transition

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

🚀 Aggressive: Short-Term Directional Bet on Break Below $180 (ADVANCED ONLY!)

Play: IF AND ONLY IF stock breaks below $180 support with volume, buy puts for quick 10-15% move

Structure: Wait for technical breakdown, then buy $170 puts (January 16 expiration - 30 days out)

Trigger conditions (ALL must occur):

- 📉 Stock closes below $180 on heavy volume (2x average)

- 📊 Gamma support at $180 (18.8B) fails to hold on retest

- 📰 Negative catalyst: Stargate delay news, analyst downgrade, or macro weakness

- 🎯 Enter ONLY if stock at $176-179 (gives 2-3% cushion from $180 break)

Why this could work:

- 🔨 Breaking major gamma support at $180 triggers dealer de-hedging (momentum accelerates)

- 📊 Next support not until $175 then $170 - could get fast 5-10% move in days

- 💸 Put buyers already positioned at $160 - institutions smell blood

- ⏰ January OPEX means 30 days for thesis to play out (captures Q3 earnings preview period)

- 📈 If right, stock could cascade to $165-170 quickly for 50-100% gain on puts

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: $170 puts cost $8-12 ($800-1,200 per contract) depending on entry timing

- ⏰ TIME DECAY: Theta burns -$40-60/day - need immediate follow-through

- 😱 False breakdown risk: Stock could fail at $178, rally back to $185-190, puts crushed

- 🛡️ Gamma support: Even if $180 breaks, $175 support (6.7B gamma) could halt decline

- ⚠️ Year-end games: December has low volume, market makers can manipulate into OPEX

Estimated P&L:

- 💰 Cost: ~$10-11 per put (using entry at $177-178 post-breakdown)

- 📈 Profit scenario: Stock drops to $165-170 in 7-10 days = $15-20 gain (50-100% ROI)

- 🚀 Home run: Stock cascades to $160 on Stargate delay = $25-30 gain (150-200% ROI)

- 📉 Loss scenario: Stock bounces back above $180 = lose $6-9 (60-80% loss)

- 💀 Total loss: Stock rallies to $190+ = lose entire premium (100% loss)

Breakeven: Stock needs to reach ~$159-160 for breakeven after premium paid

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can watch the position DAILY and take profits at 40-60% quickly

- ✅ Have traded technical breakdowns before and understand false breakdown risk

- ✅ Can afford to lose ENTIRE premium (realistic 40-50% probability)

- ✅ Will WAIT for confirmed breakdown (don't try to predict it!)

- ✅ Accept that even if direction is right, timing could be off

- ⏰ Plan to close within 10-14 days (don't hold to expiration for theta bleed)

Risk level: EXTREME (can lose 100% of premium easily) | Skill level: Advanced only

Probability of profit: ~35-40% (this is a low-probability, high-reward speculation)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💸 Free cash flow crisis deepening: Oracle burned -$10.33 billion in H1 FY2025 due to $20.54B capex (The Motley Fool). This is UNSUSTAINABLE - the company is literally borrowing to fund growth with no immediate cash payback. If free cash flow stays deeply negative through Q3/Q4, credit rating agencies could downgrade Oracle's debt, spiking borrowing costs and forcing capex cuts that delay Stargate.

-

🏦 Debt spiral accelerating: Total debt (including leases) hit $124 billion in November 2024, up from $89B just one year earlier - that's 40% growth in debt load (The Motley Fool). Oracle is paying $1B+ per quarter in interest expenses - if rates stay elevated or another crisis hits, Oracle could face liquidity constraints. September 2024 alone saw $18B in new debt issuance.

-

🏗️ Stargate execution risk at unprecedented scale: Building 166 data centers simultaneously while securing multi-gigawatt power allocations in competitive markets is INSANELY difficult (CIO Dive). Construction delays, permitting issues, power constraints, or supply chain disruptions (cooling systems, GPUs, networking equipment) could push the first Abilene site operational date from Q1-Q2 2026 to H2 2026 or later - devastating for the thesis.

-

⏰ Revenue recognition timing gap: Oracle's $455 billion RPO sounds impressive, but only ~33% converts to revenue within 12 months (Sherwood News). The remainder stretches over MANY YEARS. This creates an 18-24 month "valley of death" where Oracle burns cash on capex but can't recognize Stargate revenue until data centers go operational. Wall Street may lose patience during this period.

-

🤖 Stargate dependency concentration risk: The $500 billion Stargate project represents MASSIVE customer concentration in OpenAI/SoftBank (OpenAI). If OpenAI scales back commitments, delays deployments, encounters financial stress, or pivots back to Microsoft Azure, Oracle's entire growth story collapses. The 15-year partnership timeline also exposes Oracle to long-term execution risk - what if OpenAI's business model changes?

-

📊 Q3 earnings potential repeat miss (March 10): Wall Street expects $14.13B revenue vs $14.39B consensus - Oracle is ALREADY positioned to miss again (CNBC)! If the company reports below $14B or guides conservatively for Q4, it confirms Q2 wasn't a one-time hiccup but start of a TREND. Stock could gap down 10-15% to $160-165 overnight.

-

⚖️ Valuation stretched with zero margin for error: At 7.5x sales vs 5-year average of 5.2x, Oracle is trading at a PREMIUM multiple despite negative cash flow and execution uncertainty. This pricing assumes PERFECT Stargate execution, sustained OCI growth above 50%, and successful multicloud expansion. ONE major disappointment and the multiple compresses 20-30% back to historical norms - that's $140-160 stock price.

-

🎯 $190 gamma resistance ceiling impossible to break: The single largest gamma concentration on the entire options chain is at $190 (35.6B call gamma) - this creates MECHANICAL selling pressure as market makers hedge their exposure. Stock has tried $190 three times since the earnings crash and gotten rejected each time. Would need sustained institutional buying wave to overcome - unlikely until Stargate operational proof.

-

🇨🇳 China export restriction wildcard: Oracle already took $800M charge in Q2 2025 from MI308 export restrictions (later lifted). U.S.-China tech tensions create ongoing risk of NEW restrictions on cloud infrastructure or AI services without warning. China historically represented 15-20% of Oracle's revenue - loss of this market would offset Stargate gains.

-

💰 Hyperscaler competition intensifying: Oracle faces AWS, Azure, and Google Cloud - all with MASSIVE capital resources, established customer bases, and lower debt loads. If hyperscalers enter price wars for AI infrastructure (already happening), Oracle must match pricing which compresses margins on low-margin infrastructure revenue. Traditional high-margin software becoming smaller mix of business.

-

🎢 Smart money hedging at peak with $10.2M protection: The TIMING of these put purchases is critical - they bought AFTER the 11% earnings crash, not before. This suggests institutions see MORE downside despite already being down 10% from highs. When sophisticated players managing hundreds of millions deploy $10.2M for downside protection rather than bottom-fishing, it's a MAJOR caution flag.

-

📉 Macroeconomic recession risk: At current valuation, Oracle has ZERO recession protection. Enterprise IT budgets get cut first in economic downturns. If recession emerges in 2025-2026, data center spending contracts sharply regardless of AI hype. Stargate deployments could be delayed or reduced in scope if OpenAI faces funding constraints.

🎯 The Bottom Line

Real talk: Three separate institutions just spent $10.2 MILLION building a PUT LADDER across December, January, and March expirations - six days AFTER Oracle crashed 11% on earnings. This isn't panic selling or directional bearishness - this is sophisticated risk management by players who understand Oracle's AI infrastructure bet carries SERIOUS execution risk over the next 3-6 months.

What these trades tell us:

Trade #1 - $5.9M in Dec 19 $190 puts:

- 🎯 Betting stock CAN'T reclaim $190 by Friday (4 days!) despite being only 3% away

- 💰 Willing to pay $785 per contract for just 4 days of protection - that's EXTREME urgency

- 📊 The $190 strike is positioned at STRONGEST gamma resistance (35.6B) - they know the ceiling

Trade #2 - $1.7M in Jan 9 $160 puts:

- 📉 Positioning for 12.5% decline to $160 by early January (25 days out)

- ⏰ Expects year-end tax loss selling and Q3 earnings preview to drive weakness

- 🛡️ Medium-term insurance bridging near-term and long-term protection

Trade #3 - $2.6M in March 20 $140 puts:

- 😰 Genuine DISASTER scenario positioning (24% downside)

- 📅 Captures Q3 earnings (March 10) and early Stargate construction updates

- 💸 Cheap premium ($3.49) suggests they see this as tail risk insurance, not base case

The composite message: "We believe Oracle faces a difficult 3-6 months navigating debt concerns, cash flow pressure, and Stargate execution uncertainty. Even after the 11% crash, further downside to $160-170 is realistic, with tail risk to $140 if multiple things go wrong."

This is NOT a "sell everything and run" signal - it's a "reduce exposure, take profits, and protect remaining positions" signal.

If you own ORCL:

- ✅ Consider trimming 30-50% at current $183-187 levels if you bought below $140 (lock in 30-40% gains)

- 📊 If holding through Q3 earnings, set MENTAL STOP at $175 (below major gamma support at $180)

- ⏰ You've already survived an 11% earnings crash - don't get greedy chasing the last 5-10%

- 🛡️ Consider buying 1-2 $175 or $170 protective puts per 100 shares if holding large position

- 🎯 If you're REALLY bullish on Stargate long-term, sell covered calls at $195-200 to collect premium during consolidation

If you're watching from sidelines:

- ⏰ DO NOT CHASE at current levels - wait for better entry

- 🎯 Post-holiday pullback to $170-175 would be EXCELLENT long-term entry (10-12% off current price with gamma support)

- 📈 Looking for these confirmations before buying: 1) Free cash flow improvement in Q3, 2) Stargate timeline updates showing progress, 3) Multicloud revenue acceleration, 4) Debt stabilization

- 📅 Mark calendar for March 10 Q3 earnings - this is THE moment of truth

- 🚀 If Oracle BEATS in Q3 and raises guidance, stock could rocket to $200-210 quickly

- ⚠️ If Oracle MISSES again or guides weak, $160 becomes realistic target by April

If you're bearish:

- 🎯 Wait for technical breakdown below $180 before initiating shorts or puts

- 📊 Major support levels: $180 (18.8B gamma), $175 (6.7B gamma), $170 (7.5B gamma), $160 (institutional put strike)

- ⏰ Best risk/reward is POST-December OPEX put spreads when IV crushes (cheaper entry)

- ⚠️ Watch for break below $180 on volume - that's the trigger for cascade to $170 then $160

- 📉 Alternative: Sell call spreads (e.g., sell $195 calls, buy $205 calls) to bet on range-bound action

Mark your calendar - Key dates:

- 📅 December 19 (Friday - THIS WEEK!) - Monthly/Quarterly OPEX, $5.9M put trade expires

- 📅 December 20-27 - Post-OPEX, year-end positioning (good entry window if stock weak)

- 📅 January 9, 2026 - $1.7M put trade expires

- 📅 January 16 - Monthly OPEX

- 📅 March 10, 2026 - Q3 FY2025 earnings report (CRITICAL CATALYST!)

- 📅 March 20 - Quarterly triple witch, $2.6M put trade expires

- 📅 Q1-Q2 2026 (April-June) - Stargate first site (Abilene, Texas) expected operational

- 📅 H2 2026 - NVIDIA Blackwell GPU deliveries and deployment

Final verdict: Oracle's long-term AI infrastructure story remains COMPELLING - the Stargate $500B partnership, multicloud database growth of 115% Q/Q, $455B RPO backlog, and government contracts are all real catalysts. BUT, the near-term setup is TREACHEROUS: $124B debt, -$10B free cash flow, 18-24 month revenue recognition gap, and execution risk on 166 simultaneous data center builds create asymmetric downside.

The $10.2M institutional put ladder is a CLEAR signal: The easy money has been made (up 69% YTD through Dec 9). From here, it's a show-me story - Oracle must PROVE it can convert massive capex into profitable revenue while managing a debt/cash flow crisis.

Be patient. Let Oracle prove the Stargate thesis. The AI infrastructure revolution will still be here in 6-12 months, and you'll sleep better entering at $170-175 after Q3 earnings clarity than at $185 today gambling on hope.

This is about capital preservation and risk management. The institutions paying $10.2M for protection understand something the optimists don't: Hope is not a strategy. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual Z-scores (107.81, 95.64, 4.37) reflect these specific trades' sizes relative to recent ORCL history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. Oracle faces significant execution risk on Stargate project, debt burden of $124B, and negative $10B free cash flow creating material downside risk. The put buyers may have complex portfolio hedging needs not applicable to retail traders. Oracle's business model transformation from software to infrastructure is unproven at current scale.

About Oracle Corporation: Oracle provides enterprise applications and infrastructure offerings through a variety of flexible IT deployment models, including on-premises, cloud-based, and hybrid. The company is a pioneer in relational database systems and also offers enterprise resource planning and cloud infrastructure solutions, with a market cap of $545.8 billion in the Prepackaged Software industry.