🚨 ORCL $197M Put Protection - Smart Money Hedging Before Opex! 🛡️

📅 December 17, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $197 MILLION on ORCL puts at 14:33:10 - an absolutely massive two-legged hedge buying 29,000 contracts at the $210 strike and 27,000 contracts at the $220 strike, both expiring in just 2 days on December 19th! With ORCL trading at $179.10, this sophisticated institution is protecting a huge position through monthly/quarterly opex. Translation: Big money wants insurance through Friday's triple witching expiration after the stock's recent pullback.

📊 Company Overview

Oracle Corporation (ORCL) is a global enterprise software and cloud infrastructure giant transforming into an AI powerhouse:

- Market Cap: $542.02 Billion (one of tech's mega-caps)

- Industry: Prepackaged Software (Enterprise Applications & Cloud Infrastructure)

- Current Price: $179.10 (trading near recent lows after December earnings selloff)

- Primary Business: Enterprise databases, cloud infrastructure (OCI), AI infrastructure partnerships with OpenAI, xAI, Meta, and NVIDIA

What they do: Oracle pioneered commercial SQL databases and now provides the cloud infrastructure backbone for AI training through massive partnerships. Think of them as the "picks and shovels" provider for the AI gold rush - building the data centers that power ChatGPT and other frontier AI models.

💰 The Option Flow Breakdown

The Tape (December 17, 2025 @ 14:33:10):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 14:33:10 | ORCL | ASK | BUY | PUT $210 | 2025-12-19 | $88M | $210 | 29K | TBD | 29,000 | $179.10 | $30.35 |

| 14:33:10 | ORCL | ASK | BUY | PUT $220 | 2025-12-19 | $109M | $220 | 27K | TBD | 27,000 | $179.10 | $40.37 |

Total Premium Paid: $197 MILLION 🤯

🤓 What This Actually Means

This is a massive defensive hedge executed as a custom spread! Here's what's really happening:

- 💸 Enormous capital commitment: $197M total premium ($88M + $109M) for just 2-day protection

- 📊 Two-legged structure: 29,000 contracts at $210 + 27,000 contracts at $220 (roughly equal weighting)

- ⏰ Ultra-short expiration: December 19th (2 days!) - this is pure monthly/quarterly opex hedging

- 🎯 Strategic strikes: $210 (17.3% OTM) and $220 (22.8% OTM) - protecting against catastrophic gap moves

- 🏦 Institutional size: 56,000 total contracts represents 5.6 million shares worth ~$1 BILLION

- 🛡️ Cost vs protection: Paying ~17-23% of strike prices for 48-hour insurance shows EXTREME caution

What's really going down:

This trader holds a MASSIVE long position in ORCL stock or calls and is terrified of further downside through Friday's triple witching opex. After ORCL tanked 11% on December 10th earnings (wiping out $70+ billion in market cap), they're not taking ANY chances through this critical expiration window.

Think of it like buying a massive hurricane insurance policy on your beachfront mansion when the storm is 2 days away - incredibly expensive, but necessary if you have hundreds of millions at risk.

Why buy BOTH strikes? The $220 puts provide first-level protection (cap losses if stock drops to $220), while the $210 puts create a floor (protect against catastrophic moves to $200-210). This is a bear put spread sold structure - they own the underlying long position and are buying downside protection at two levels.

Unusual Score: 🔥 EXTREME (69.67x average size for $210s, 28.54x for $220s) - The Z-scores are astronomical, making this one of the largest ORCL option trades of the year. The fact that BOTH trades show "OPEN" volume signals means this is entirely new positioning, not closing existing hedges.

📈 Technical Setup / Chart Check-Up

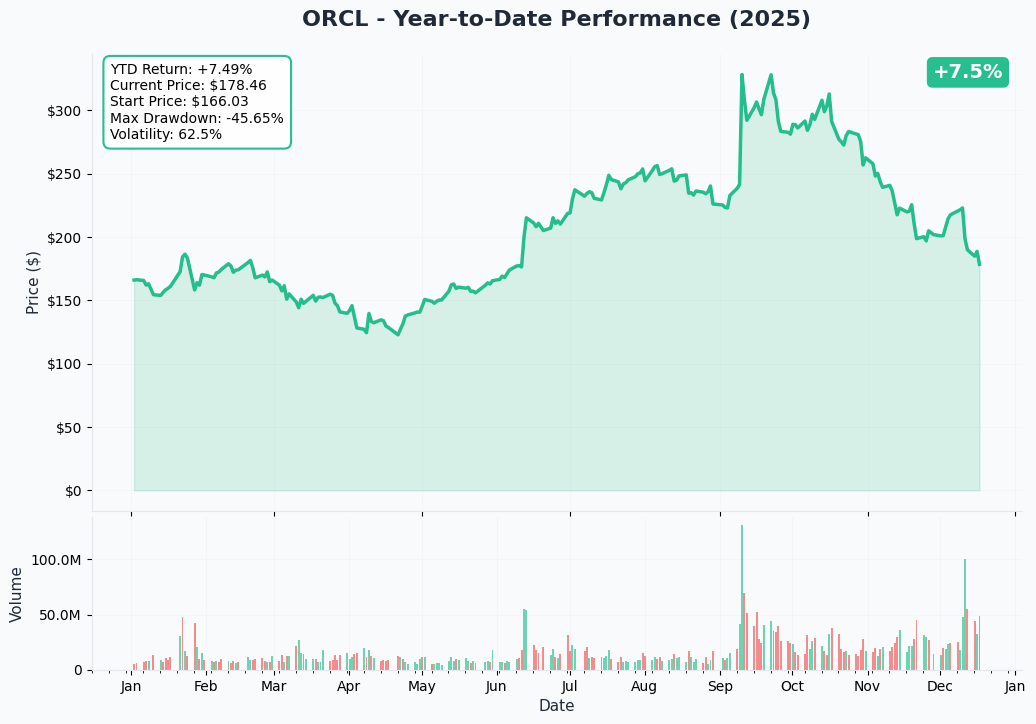

YTD Performance Chart

ORCL had an explosive run through September 2025 before hitting the wall in December. Current price of $179.10 shows the damage from the recent earnings selloff:

Key observations:

- 📈 Strong run to Sept: Rallied hard on AI infrastructure momentum and OpenAI Stargate partnership announcements

- 💔 December disaster: Plunged 11% on Dec 10th earnings despite massive $523B RPO - market worried about capex ($50B FY2026) and debt levels

- 🎢 High volatility: Swings of 10-15% on news show this isn't a stable mega-cap stock anymore

- ⚠️ Broken support: Failed to hold $187-190 support zone from earlier in the year

- 📊 Consolidating: Trading in a tight range around $178-180 after the selloff stabilized

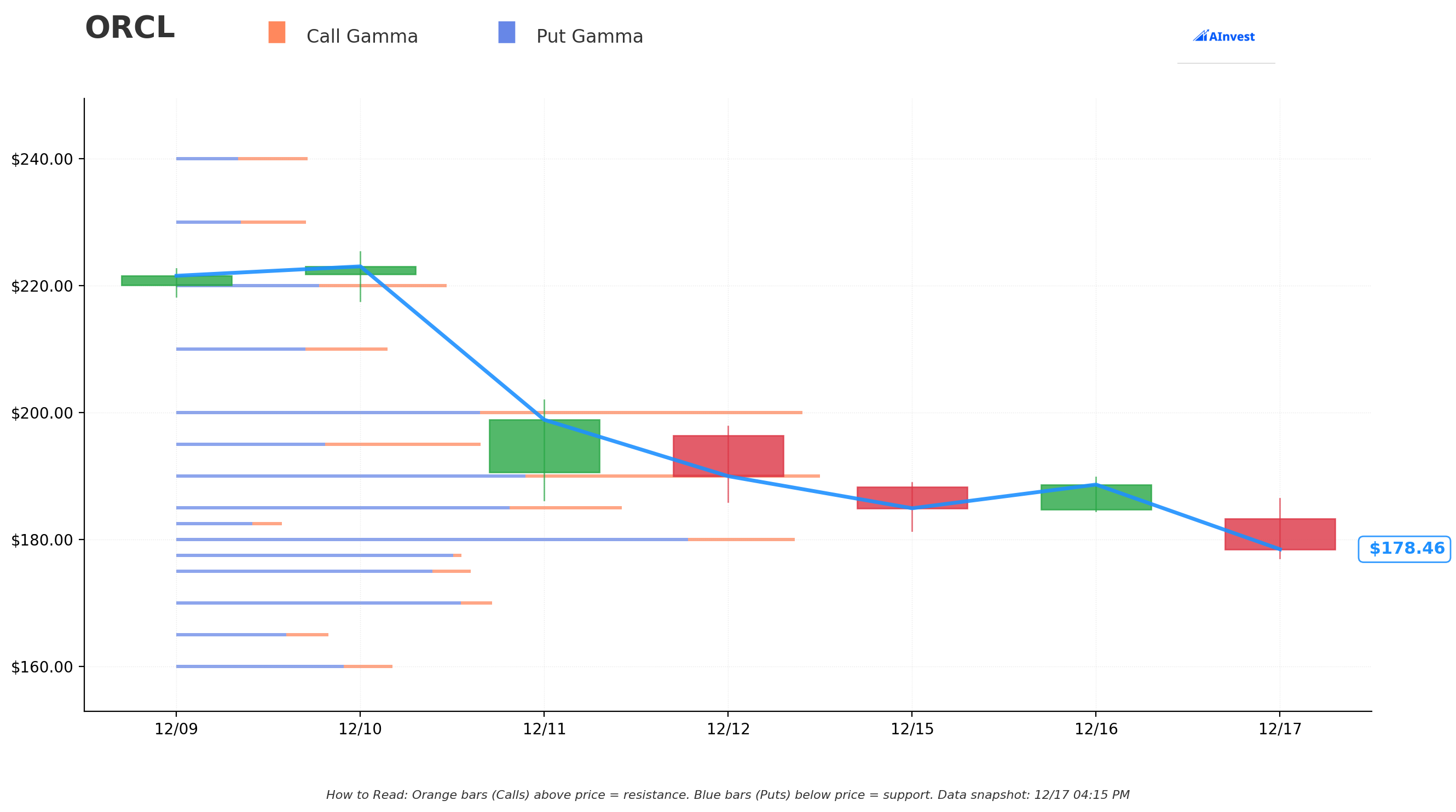

Gamma-Based Support & Resistance Analysis

Current Price: $179.10

The gamma exposure map reveals critical battlegrounds where market makers will defend:

🔵 Support Levels (Put Gamma Below Price):

- $177.50 - STRONGEST nearby support with 11.8B total gamma (11.5B put gamma) - only 0.9% below current price!

- $175 - Secondary floor at 12.2B gamma (10.6B put gamma) - major line in the sand

- $170 - Deep support with 13.1B gamma (11.8B put gamma) - this is the CRITICAL level

- $160 - Extended floor at 9.0B gamma (6.9B put gamma)

🟠 Resistance Levels (Call Gamma Above Price):

- $180 - IMMEDIATE ceiling with 25.7B gamma (21.2B put gamma) - STRONGEST resistance level on the entire chain!

- $185 - Secondary resistance at 18.5B gamma (13.8B put gamma) - 3.3% overhead

- $190 - Major ceiling with 26.7B gamma (14.5B put gamma) - massive options interest here

- $195 - Resistance at 12.6B gamma (6.2B put gamma)

- $200 - Psychological barrier with 26.0B gamma (12.6B put gamma)

- $210 - This put strike! 8.8B gamma (5.3B put gamma) - not coincidental

What this means for traders:

ORCL is trading in a BRUTAL setup - right below massive $180 resistance (25.7B gamma, the single largest level) which creates natural selling pressure. The stock is essentially pinned between $177.50 support and $180 resistance, creating a very narrow range going into opex.

The put buyer positioned at $210 and $220 - WAY out of the money (17-23% above current price) - showing they're protecting against a low-probability but devastating scenario where ORCL gaps higher through opex and their short puts/long calls get destroyed.

Net GEX Bias: Bearish (92.3B call gamma vs 164.6B put gamma) - Overall positioning is heavily defensive with nearly 2:1 put gamma dominance. This creates a "sticky" environment where market makers buy on dips and sell on rallies, keeping the stock rangebound.

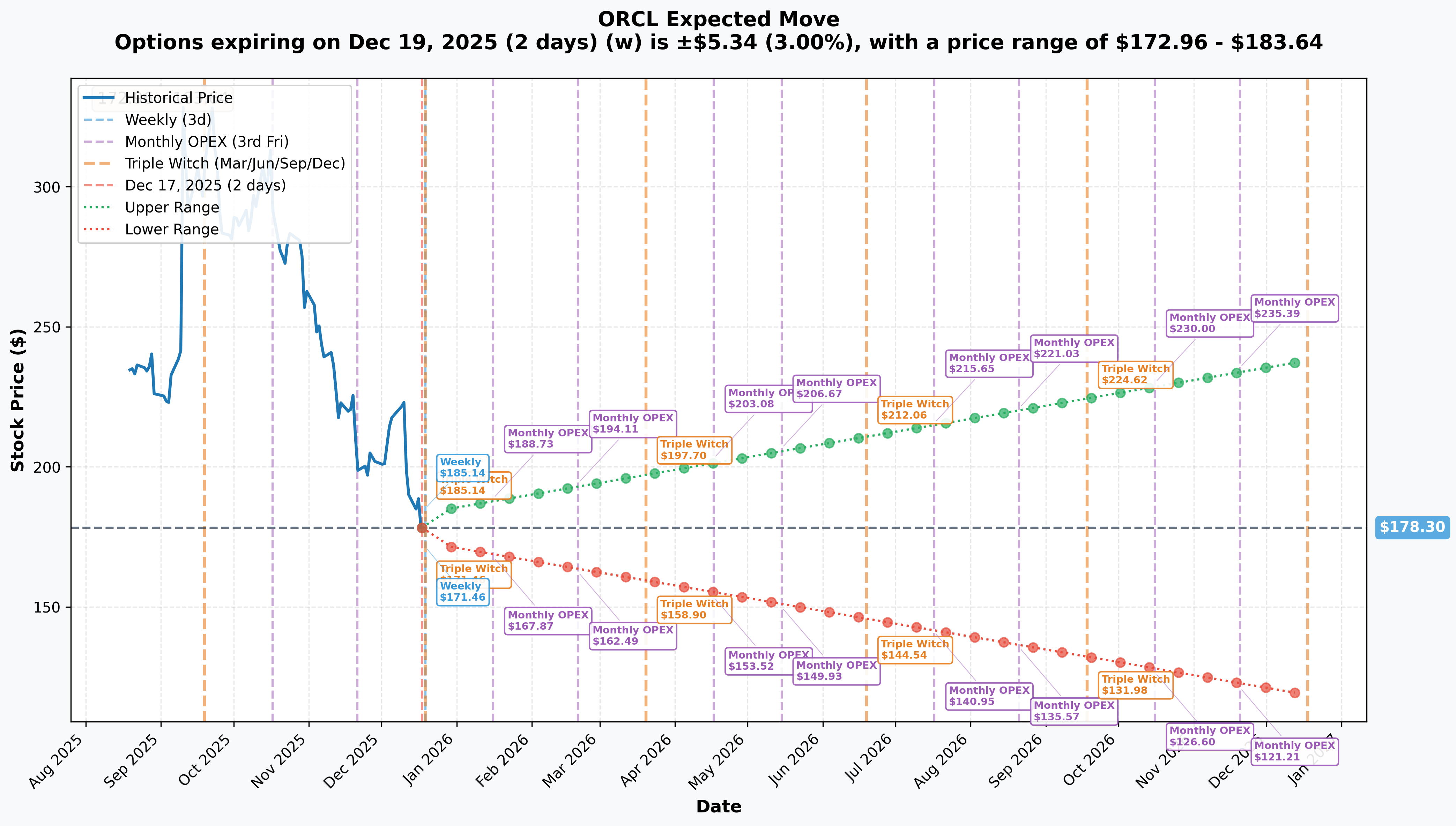

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly/Monthly/Triple Witch (Dec 19 - 2 DAYS - THIS TRADE!): ±$5.34 (±3.0%) → Range: $172.96 - $183.64

- 📅 January OPEX (Jan 16 - 30 days): ±$10.59 (±5.9%) → Range: $167.87 - $188.73

- 📅 February OPEX (Feb 20 - 65 days): ±$15.81 (±8.9%) → Range: $162.49 - $194.11

- 📅 Yearly LEAPS (Dec 18, 2026 - 366 days): ±$59.78 (±33.53%) → Range: $118.52 - $238.08

Translation for regular folks:

Options traders are pricing in a 3.0% move ($5.34) by Friday Dec 19th - relatively modest for a stock that just had an 11% earnings gap. The market expects ORCL to stay in the $173-$184 range through opex.

BUT - the put buyer is positioned at $210-$220, which is OUTSIDE even the January implied move range ($188.73 upper bound). They're protecting against a scenario the market thinks has <5% probability: a massive reversal rally that breaks the stock back above $200.

Key insight: The ultra-short 2-day expiration makes these puts pure opex hedging tools. After Friday's close, the gamma will unwind and the stock could move more freely. The put buyer likely expects volatility AFTER opex, not before.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened - Setting The Stage)

Q2 FY2026 Earnings Disaster - December 10, 2024 📊

ORCL reported Q2 results on Dec 10th that triggered the 11% selloff the stock is still recovering from:

- 💪 The Good: RPO (Remaining Performance Obligations) surged to $523 BILLION (up 438% YoY) - unprecedented backlog including $300B+ from OpenAI Stargate partnership

- 😰 The Bad: Capex guidance exploded to $50 BILLION for FY2026 (up from $35B just 3 months earlier), raising debt and free cash flow concerns

- 💔 Market reaction: Stock plunged 11%, wiping out $70+ billion in market cap on concerns about revenue conversion timeline and negative free cash flow

- ⚠️ Debt worries: Oracle carrying $100B+ in debt with $1B+ quarterly interest expenses, free cash flow deficit widened to -$10B

Analyst downgrades post-earnings: Multiple firms expressed concern about the RPO-to-revenue ratio (3x annual revenue), questioning when/if Oracle can convert the massive backlog into actual cash flow.

Why this matters for the put trade: The stock is still digesting this negative catalyst. The put buyer may be protecting against: (1) further analyst downgrades through year-end, (2) tax-loss selling pressure, or (3) year-end portfolio rebalancing causing institutional selling.

OpenAI / Stargate Partnership ($300+ Billion) 🤝

Oracle's landmark deal announced January 2025 with the White House, OpenAI, and SoftBank:

- 🏭 Scale: $500B joint venture building up to 4.5 gigawatts of AI infrastructure

- 🎯 Oracle's role: $300B+ over 5 years building Stargate capacity on Oracle Cloud Infrastructure

- ✅ Progress: Flagship Abilene, Texas campus operational; began delivering NVIDIA GB200 racks in June 2025

- 📅 Timeline: Five new Stargate sites announced July 2025, total capacity over 5 gigawatts across multiple facilities

The bull case: This is transformational - validates Oracle as THE alternative to AWS/Azure/Google Cloud for AI infrastructure at the highest level (OpenAI chose Oracle for ChatGPT infrastructure expansion).

The bear case: Revenue won't materialize for 12-24 months as data centers take time to build, and the massive capex ($50B/year) is debt-fueled with negative free cash flow.

🚀 Upcoming Catalysts (Next 6 Months)

Q3 FY2026 Earnings - Expected March 10-11, 2026 📊

Oracle's next earnings report is THE major catalyst that will determine if the December selloff was overdone or justified:

Key metrics to watch:

- 💰 Cloud infrastructure revenue growth: Target is 70%+ YoY - need to see strong sequential growth

- 📊 RPO conversion rate: Wall Street wants to see the $523B backlog converting to recognized revenue faster

- 💵 Free cash flow: Critical to show improvement from -$10B deficit - need path back to positive FCF

- 🏭 Capex spending update: Any increase beyond $50B would be disastrous; any reduction would rally stock

- 🤖 OpenAI/Stargate progress: Updates on deployment milestones, revenue recognition timeline

Consensus estimates: Expected revenue ~$14.5-15.0B (16% full-year growth target), with cloud growth driving the beat.

Risk: If Oracle disappoints AGAIN on revenue conversion or raises capex further, the stock could test $160-170 support levels. Conversely, a strong beat showing RPO converting faster than expected could rally the stock back to $200+.

Stargate Phase 2 Completion - Mid-2026 🏗️

Oracle's second phase at Abilene, Texas (six additional buildings, another gigawatt of capacity) began construction March 2025:

- 📅 Expected energization: Mid-2026

- 💰 Revenue impact: Could accelerate billions in quarterly cloud revenue recognition from OpenAI contract

- 🚀 Significance: Physical proof the Stargate partnership is real and scaling

MI325X / MI350 GPU Deployments Throughout 2026

Oracle is one of the largest deployers of NVIDIA Blackwell GPUs globally:

- 🔥 Scale: Deploying 100,000+ NVIDIA Blackwell GPUs in superclusters

- 📈 Historical context: GPU consumption revenue up 336% YoY in Q2 FY2025 - shows AI demand is real

- ⏰ Timeline: Ongoing deployments Q1-Q4 2026 as new data centers come online

- 💡 Implications: Each deployment milestone demonstrates Oracle can monetize the massive capex spend

Multicloud Expansion: Oracle Database@AWS / Azure / Google Cloud

Oracle significantly expanded multicloud partnerships in late 2024:

- 🌐 Oracle Database@Azure: Expanding from 10 to 33+ regions throughout 2025 (24 new regions announced Nov 2024)

- ☁️ Oracle Database@AWS: Launched limited preview December 2, 2024 in US East, expanding 2025

- 📈 Revenue impact: Each new region activation drives incremental customer wins in regulated industries (healthcare, finance, government)

Why this matters: Removes the "cloud lock-in" objection - customers can now use Oracle databases on AWS/Azure/Google Cloud infrastructure, making Oracle's software sticky while expanding addressable market.

Sovereign Cloud Contract Announcements 🇺🇸🌍

Oracle is winning major sovereign cloud deals globally as governments prioritize data security:

- 🇬🇧 UK Government: 250,000 civil servants using Oracle Cloud for shared services (announced Oct 2024)

- 🇦🇪 Abu Dhabi: 25 government entities with 15,000+ daily users (launched Dec 2024, backed by 13B AED investment)

- 🇺🇸 U.S. Government: GSA partnership announced July 2025 to reduce costs across federal agencies

- 🌍 Expected announcements: EU member states, Japan, India, Middle East countries likely through 2026

Catalyst timing: Each new sovereign cloud win provides positive news flow and validates Oracle's competitive differentiation (162 data centers globally - more than AWS, Azure, and Google Cloud COMBINED).

⚠️ Risk Catalysts (What Could Go Wrong)

Debt and Free Cash Flow Crisis 💸

Oracle's biggest threat heading into 2026:

- 🚨 Debt load: $100B+ in debt with combined debt/lease obligations totaling $111.6B (up from $84.5B in 2024)

- 💰 Interest expense: Over $1B quarterly - eats into profitability

- 📉 Negative FCF: -$10.33B in H1 FY2026 after $20.54B capex spending

- ⚡ Credit concerns: Cost to insure Oracle debt rose to 139 basis points for 5-year CDS - highest since at least Sept 2020

The risk: If Oracle can't convert RPO to revenue quickly enough, credit markets could force them to cut capex dramatically, derailing the AI growth story. Unlike Amazon/Microsoft/Google who generate massive FCF to self-fund AI capex, Oracle must rely on debt markets.

AI Investment Cycle Uncertainty 🎢

- 🎰 AI bubble concerns: Oracle shares tumbled on "gloomy forecasts and higher capex reigniting AI bubble concerns"

- 📊 Customer concentration: RPO heavily concentrated in OpenAI ($300B+), Meta, NVIDIA, xAI - if any delay deployments, revenue trajectory suffers

- ⏰ Long buildout timeline: Data centers take 12-24 months to construct, delaying revenue recognition

Competition from Hyperscalers 🏆

- 📊 Market share: Oracle has only 3% cloud market share vs AWS (31%), Azure (21%), Google Cloud (13%)

- 💪 Ecosystem maturity: AWS has 200+ services, deepest enterprise relationships, and most mature AI/ML tooling

- 🚀 Google acceleration: Google Cloud doubling market share, growing 30% YoY - faster than Oracle

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalysts, here are scenarios through March 2026 (next earnings):

📈 Bull Case (30% probability)

Target: $210-$230 (Exactly where these puts are struck!)

How we get there:

- 💪 Stargate Phase 2 progress announcements show tangible infrastructure coming online

- 📊 Q3 earnings (March) delivers revenue beat with RPO conversion accelerating faster than Street expects

- 💵 Free cash flow shows improvement path (even if still negative, better trajectory)

- 🌐 Multiple sovereign cloud wins announced (EU countries, Japan) - validates differentiation

- ☁️ Oracle Database@AWS and @Azure adoption metrics exceed expectations

- 🤖 Management provides detailed roadmap showing $50B capex converting to $15-20B annual revenue run-rate by late 2026

- 📈 Breakout above $180 resistance triggers short covering rally to $190, then $200 gamma resistance zones

- 🎯 Analysts upgrade on visibility improvement, raise price targets back to $250-300 range

Key metrics needed:

- OCI revenue growth accelerating (70%+ YoY sustained)

- Gross margins holding/expanding (proving pricing power despite massive spending)

- RPO-to-revenue conversion showing progress (ratio declining from 3x toward 2.5x)

Why only 30%? Stock needs to overcome significant fundamental concerns (debt, negative FCF) and the December selloff showed institutions are skeptical. Getting back to $210-220 requires near-perfect execution AND broader market supporting high-multiple growth stocks.

🎯 Base Case (50% probability)

Target: $165-$195 range (CHOPPY RANGE-BOUND ACTION)

Most likely scenario:

- ⚖️ Stock consolidates in broad range through March earnings, digesting December selloff

- 🛡️ Support holds at $165-170 (gamma support zone), resistance caps at $190-200

- 📊 Q3 earnings meets consensus but doesn't wow - solid cloud growth but FCF still negative

- 💰 Capex remains elevated ($50B guidance unchanged) - no relief for debt/FCF concerns

- 🏭 Stargate progress steady but not accelerating - timeline remains 12-24 months for major revenue

- 🌐 Sovereign cloud wins continue but not game-changing in near term

- 📈 Trading within established gamma bands - dealers defend $175-180 support, sell $190-200 resistance

- ⏰ Market in "wait and see" mode until concrete evidence of RPO conversion appears

This is the most realistic outcome: Oracle's long-term AI story intact but near-term fundamentals (debt, FCF, revenue conversion) create uncertainty. Stock trades sideways in wide range as bulls and bears fight it out.

The put buyer's best scenario: Stock stays rangebound below their $210-220 strikes, puts expire worthless, but the hedging served its purpose protecting against unexpected volatility through year-end/opex.

📉 Bear Case (20% probability)

Target: $140-$165 (Test Major Support)

What could go wrong:

- 😰 Q3 earnings disappoints - revenue miss or weak guidance as RPO conversion slower than expected

- 💸 Credit rating agencies downgrade Oracle debt on FCF concerns - triggers selloff in bonds AND stock

- 🚨 Management announces ANOTHER capex increase beyond $50B - market loses confidence completely

- ⏰ Stargate deployment delays announced - infrastructure buildout taking longer than planned

- 🤖 OpenAI or other major customer reduces commitment or pushes out timeline

- 📉 Broader tech selloff / recession fears hit high-debt growth stocks hardest

- 🔨 Break below $170 gamma support triggers cascade to $160, then $150 levels

- 💔 Analyst downgrades pile on - price targets cut to $150-180 range

Critical support levels:

- 🛡️ $177.50: Immediate support (11.8B gamma) - must hold or momentum shifts

- 🛡️ $175: Secondary floor (12.2B gamma) - major line in the sand

- 🛡️ $170: Deep support (13.1B gamma) - break here opens door to $160

- 🛡️ $160: Extended floor (9.0B gamma) - disaster scenario

Why only 20%? Oracle's fundamentals are actually solid (massive backlog, real AI partnerships, multicloud traction) - the concerns are about TIMING and FINANCING, not viability. Would require multiple negative catalysts to align.

Put buyer's nightmare scenario: They're protecting against a LOW-probability event where stock rallies ABOVE $210-220 by Friday opex, forcing them to cover short puts/protect long positions at huge losses. This is <5% probability, but with $1B+ at risk, the $197M insurance premium makes sense.

💡 Trading Ideas

🛡️ Conservative: Stay Sidelined Until March Earnings

Play: Wait for Q3 earnings clarity before establishing positions

Why this works:

- ⏰ Only 2 days until opex - gamma unwind Friday could create volatility

- 📊 December earnings selloff still being digested - no clear direction established

- 💸 Options extremely expensive with 3% implied move for 2-day window (high IV environment)

- 🎯 March earnings (3 months away) provides next major catalyst for direction

- 🤔 The $197M institutional put buy signals smart money is UNCERTAIN - why fight that?

- 💵 Better to wait for $165-170 pullback with higher margin of safety OR $200+ breakout with confirmed momentum

Action plan:

- 👀 Watch Friday Dec 19th opex closely - how does stock trade as $180 resistance gamma unwinds?

- 📈 Look for either: (1) Pullback to $165-170 gamma support for long entry with 8-10% cushion, OR (2) Breakout above $190 with volume confirming institutional accumulation

- ✅ Need to see Q3 earnings in March showing RPO conversion progress and FCF improving

- 🌐 Monitor sovereign cloud wins and multicloud adoption metrics

- ⏰ Revisit mid-2026 when Stargate Phase 2 completion provides tangible revenue proof

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid whipsaw action through opex and holidays. Get better entry point with clearer catalyst visibility after March earnings.

⚖️ Balanced: Post-Opex Bull Put Spread (Fade The Fear)

Play: After opex gamma unwind, sell bull put spread betting stock holds support

Structure: Buy $170 puts, Sell $177.50 puts (January 16 expiration - 30 days)

Why this works:

- 🎯 Targets strongest gamma support levels ($177.50 and $170) where institutions are positioned

- 📊 Defined risk spread ($7.50 wide = $750 max risk per spread)

- 💰 After Friday opex, IV should drop as near-term gamma unwinds - sell premium at better levels

- 🛡️ Oracle's fundamentals solid (massive backlog, real partnerships) - market likely overreacted to December earnings

- ⏰ 30 days to expiration gives time for year-end tax-loss selling to finish and new year buying to begin

- 📈 Betting that December selloff was overdone and stock consolidates $175-185 range

Estimated P&L (adjust after seeing post-opex IV):

- 💰 Collect ~$2.50-3.00 credit per spread (sell $177.50 put for ~$5, buy $170 put for ~$2.50)

- 📈 Max profit: $250-300 if ORCL above $177.50 at January expiration (keep full credit)

- 📉 Max loss: $450-500 if ORCL below $170 (spread width minus credit)

- 🎯 Breakeven: ~$174.50-175.00

- 📊 Risk/Reward: ~1.5:1 (risking $500 to make $300)

Entry timing:

- ⏰ Wait until Monday Dec 23rd or later (after opex gamma fully unwinds)

- 🎯 Only enter if stock trading $178-182 range (gives room to work)

- ❌ Skip if stock already below $175 (too close to short strike)

Position sizing: Risk only 2-3% of portfolio (this is credit spread speculation)

Risk level: Moderate (defined risk, bullish bias) | Skill level: Intermediate

🚀 Aggressive: March Call Spread - Bet On Earnings Beat (ADVANCED!)

Play: Buy call spread betting Q3 earnings shows RPO conversion progress

Structure: Buy $185 calls, Sell $200 calls (March 20 expiration - 93 days, captures Q3 earnings)

Why this could work:

- 📊 March expiration captures Q3 earnings (expected March 10-11) - THE major catalyst

- 🎯 Targets realistic rally zone ($185-200) if earnings deliver strong RPO conversion story

- 💰 Spread caps risk vs buying naked calls (limits upside but also limits cost)

- 🚀 If Oracle shows FCF improving and Stargate progress, analysts could re-rate stock back to $220+ longer term

- ⏰ 93 days gives time for: (1) year-end selling to clear, (2) Stargate progress updates, (3) sovereign cloud wins

- 🤝 Multicloud adoption (Oracle@AWS/Azure) likely showing strong metrics by March

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Call spread costs ~$5-7 ($500-700 per spread)

- 😱 Earnings risk: If Q3 disappoints AGAIN, stock could tank to $160-165 and you lose entire premium

- 📊 Resistance overhead: Massive gamma at $180 (25.7B), $190 (26.7B), $200 (26.0B) creates selling pressure

- 💵 Debt overhang: Any credit rating downgrade or FCF deterioration torpedoes thesis

- 🎢 Stock needs to rally 10-15% just to reach spread's profit zone

- ⚠️ Q3 earnings could be "good but not great" - stock stays $180-190 and spread expires with minimal value

Estimated P&L:

- 💰 Cost: ~$5-7 per spread

- 📈 Max profit: $8-10 if ORCL above $200 at March expiration ($15 spread width minus $5-7 cost) = 115-143% ROI

- 🚀 Partial profit: If ORCL at $190-195 at expiration = $3-5 gain = 43-71% ROI

- 📉 Total loss: If ORCL below $185 = lose entire $5-7 premium = -100%

- 🎯 Breakeven: ~$190-192

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium ($500-700 per spread is real money!)

- ✅ Understand earnings create binary risk - stock could gap $15-20 either direction

- ✅ Have conviction Oracle's RPO ($523B) will show conversion progress by Q3

- ✅ Can monitor position through earnings and take profits quickly if you get the move

- ⏰ Plan to close position 1-2 weeks post-earnings (don't wait until March expiration)

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35% (needs both earnings beat AND stock to rally through resistance)

⚠️ Risk Factors

Don't get caught by these landmines:

-

💸 Debt and negative free cash flow crisis: Oracle carrying $100B+ in debt with $1B+ quarterly interest expenses. Free cash flow deficit of -$10.33B in H1 FY2026 is SEVERE for a mature software company. Credit default swap spreads widened to 139 basis points (highest since Sept 2020) showing bond investors are worried. Unlike AWS/Azure/Google Cloud which generate massive FCF to self-fund AI capex, Oracle is betting the farm on debt-fueled infrastructure buildout. If credit markets lose confidence and rates stay elevated, Oracle may be forced to cut capex dramatically - killing the AI growth story.

-

⏰ RPO-to-revenue conversion timeline uncertainty: The RPO hit $523 BILLION (438% YoY growth, 3x annual revenue) but that's BACKLOG, not actual revenue. Data centers take 12-24 months to build and energize. OpenAI's $300B+ commitment phases in over 5 years. The market's December selloff showed Wall Street is skeptical about WHEN this converts to cash. Management projects OCI growing to $144B by FY2030 - that requires near-perfect execution for 5 YEARS STRAIGHT. Any stumble and the stock gets murdered.

-

🤖 Customer concentration in mega-tech platforms: RPO heavily concentrated in OpenAI, Meta, NVIDIA, xAI. If ANY of these relationships sour, deployment timelines slip, or customers reduce commitments, Oracle's revenue trajectory collapses. You're betting on OpenAI's continued hypergrowth, Meta's AI infrastructure expansion, and NVIDIA's ecosystem remaining dominant. That's a LOT of external dependencies.

-

🏗️ Infrastructure buildout execution risk: Stargate Phase 2 in Abilene, Texas expected mid-2026 - but what if construction delays, permitting issues, power grid constraints, or NVIDIA GPU supply shortages push timeline out? Five additional Stargate sites announced with no concrete timelines. Each delay pushes revenue recognition further out while capex spending and interest expenses continue.

-

🎢 AI investment cycle bubble concerns: Oracle shares "reignited AI bubble concerns" with $50B capex guidance in December. If broader market sentiment shifts against AI infrastructure spending (recession fears, AI hype cooling, competing technologies emerging), high-capex AI plays like Oracle will be first to get crushed. Stock down 11% on December earnings shows how quickly sentiment can reverse.

-

📊 Valuation offers zero margin of safety: Even after December selloff, Oracle trades at premium valuation requiring flawless execution. The December 11% drop wiped $70B+ in market cap in ONE DAY. Current $542B market cap assumes everything goes RIGHT for 5 years. Any disappointment magnified.

-

🔨 Gamma resistance creates mechanical selling pressure: The $180 level has 25.7B gamma (STRONGEST on the entire chain), $190 has 26.7B, $200 has 26.0B. Market makers must systematically SELL into rallies to hedge their massive gamma exposure at these strikes. This creates natural ceiling effects making breakouts very difficult. Stock has failed at $180 multiple times post-December earnings.

-

🌐 Competitive threats from hyperscalers: Oracle has only 3% cloud market share vs AWS (31%), Azure (21%), Google Cloud (13%). The Big Three generate positive FCF to self-fund AI investments AND have more mature ecosystems. Google Cloud growing 30% YoY - faster than Oracle. Microsoft leads AI race through OpenAI partnership. AWS has most mature enterprise relationships. Oracle is winning deals but from a TINY base - maintaining hyper-growth gets harder each quarter.

-

🇨🇳 Geopolitical and regulatory risks: Export restrictions already hit Oracle with $800M charges in Q2 2025 (though later lifted). Future export controls could impact new products. China revenue historically 15-20% of sales. Sovereign cloud strategy means building dedicated infrastructure in each country - multiplies capex without economies of scale. Subject to political changes and budget constraints.

-

🛡️ Smart money buying $197M insurance through opex: This MASSIVE institutional put purchase (69.67x and 28.54x unusual scores) signals sophisticated players are WORRIED about near-term volatility. When institutions managing billions pay $197M for 2-DAY protection rather than staying fully long, it's a major caution flag. They positioned at $210-220 strikes (17-23% OTM) showing fear of low-probability but catastrophic scenarios.

🎯 The Bottom Line

Real talk: Someone just spent $197 MILLION on 2-day put protection through Friday's opex - that's not bearish on Oracle's long-term AI story, it's sophisticated risk management heading into a known volatility event. With ORCL down 11% from December earnings and still digesting debt/FCF concerns despite the $523B RPO, smart money wants insurance through triple witching.

What this trade tells us:

- 🎯 Institutions expect VOLATILITY through opex (not necessarily down, but protecting against unexpected gaps)

- 💰 They positioned at $210-220 strikes WAY out of the money - protecting against low-probability rally that breaks them

- ⚖️ The 2-day expiration shows this is pure opex hedging - gamma unwind Friday could move stock

- 📊 $197M premium for 48 hours of protection shows institution has hundreds of millions (likely $1B+) at risk

- ⏰ After opex, positioning resets and stock could move more freely

This is NOT a "sell everything" signal - it's a "volatility ahead through year-end" signal.

If you own ORCL:

- ✅ Consider trimming 20-30% at $180-185 if stock rallies post-opex (take some chips off table after rough December)

- 📊 If holding core position, set MENTAL STOP at $170 (major gamma support) to protect against further leg down

- ⏰ December selloff may have been overdone BUT Oracle needs to prove RPO conversion in Q3 earnings (March)

- 🎯 Long-term (12-24 months), Stargate partnership and multicloud expansion are compelling - but TIMING and FINANCING are real concerns

- 🛡️ Could buy 1-2 protective puts per 200 shares if nervous about Q1 2026 volatility

If you're watching from sidelines:

- ⏰ Friday December 19th opex is key inflection - watch how stock trades as near-term gamma unwinds

- 🎯 Best entry likely AFTER opex at $165-175 support (8-12% pullback provides margin of safety) OR above $190 with confirmed breakout

- 📈 Looking for Q3 earnings (March) confirmation: RPO conversion accelerating, FCF improving, capex controlled at $50B

- 🚀 Longer-term (6-12 months), Stargate Phase 2 completion and sovereign cloud momentum are legitimate catalysts for $220-250 IF execution delivers

- ⚠️ Current $179 price offers poor risk/reward - too much uncertainty, too little margin of safety

If you're bearish:

- 🎯 Wait for post-opex to establish bearish positions - fighting through Friday's gamma could be painful

- 📊 First resistance at $180 (25.7B gamma), major resistance at $190 (26.7B)

- ⚠️ Put spreads ($185/$175 or $180/$170 in Feb/March) offer defined-risk way to play downside

- 📉 Watch for break below $175 - that triggers cascade to $170, then potentially $160-165

- ⏰ Q3 earnings (March) biggest risk event - if Oracle disappoints again, $150-160 possible

Mark your calendar - Key dates:

- 📅 December 19 (Friday) - Monthly/Quarterly Triple Witching Opex (THIS WEEK!) - massive gamma unwind

- 📅 December 20-31 - Holiday/year-end period (lower volume, potential tax-loss selling)

- 📅 January 16 - Monthly OPEX (±5.9% implied move)

- 📅 March 10-11, 2026 - Q3 FY2026 earnings report (THE major catalyst)

- 📅 Mid-2026 (May-July) - Stargate Phase 2 expected completion at Abilene, Texas

- 📅 Throughout 2026 - Oracle Database@Azure expansion to 24 new regions, sovereign cloud announcements

Final verdict: Oracle's long-term AI infrastructure story is INCREDIBLY compelling - the $523B RPO, Stargate partnership, multicloud expansion, and sovereign cloud momentum are all real. BUT, at $179 post-selloff with debt/FCF concerns and opex volatility ahead, the risk/reward is NOT attractive for new aggressive positioning. The $197M put purchase is a CLEAR signal: smart money managing risk into uncertainty.

Be patient. Let opex clear. Wait for Q3 earnings visibility. The AI revolution will still be here in 3 months, and you'll have much better entry points and clarity. ⏰

This is a marathon, not a sprint. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual scores (69.67x and 28.54x) reflect these trades' size relative to recent ORCL history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. Opex creates volatility risk with potential for significant gaps either direction. The put buyers may have complex portfolio hedging needs not applicable to retail traders. The extremely short 2-day expiration makes these pure hedging instruments that will expire worthless if the stock stays below the strikes.

About Oracle Corporation: Oracle provides enterprise applications and cloud infrastructure through flexible IT deployment models. The company pioneered commercial SQL-based relational database management systems and now offers cloud infrastructure increasingly utilized in AI model training and deployment, with a market cap of $542.02 billion in the Prepackaged Software industry.