🚀 ORCL Massive $18M Long Call - Smart Money Betting on Cloud Comeback! ☁️

📅 January 5, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up on $18 MILLION worth of Oracle call options this morning at 12:01:20! This monster bet bought 5,300 contracts of March 20th $170 strike calls - positioning for a significant rally from current levels around $193. With ORCL down a brutal 40-45% from its September 2025 all-time high of $345.72 after the market freaked out about its $50 billion AI infrastructure spending plan, smart money is swooping in to play the rebound. Translation: Institutional investors smell opportunity in the wreckage!

📊 Company Overview

Oracle Corporation (ORCL) is a global enterprise software and cloud infrastructure giant that's betting big on AI:

- Market Cap: $562.3 Billion (one of tech's largest)

- Industry: Prepackaged Software Services

- Current Price: $193.22 (down from $345.72 all-time high in Sept 2025)

- Primary Business: Enterprise applications, database software, cloud infrastructure optimized for AI workloads

- Employees: 162,000 worldwide

- Headquarters: Austin, Texas

Oracle provides enterprise applications and infrastructure through flexible IT deployment models spanning on-premises, cloud, and hybrid solutions. Established in 1977, the company pioneered commercial SQL-based relational database systems and has expanded into enterprise resource planning platforms and cloud infrastructure supporting AI model development. With massive partnerships including a $300 billion OpenAI deal and $20 billion Meta partnership, Oracle is positioning itself as the backbone for the AI revolution.

💰 The Option Flow Breakdown

The Tape (January 5, 2026 @ 12:01:20):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Z_Score | Z_Classification | Similar_Trades | Volume_Signal |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-05 | 12:01:20 | ORCL | BUY | CALL $170 | 2026-03-20 | $170 | 5,300 | $18M | BTO | 4.07 | EXTREMELY_UNUSUAL | 1 | OPEN |

🤓 What This Actually Means

This is a massive bullish directional bet on Oracle's recovery! Here's the breakdown:

- 💸 Huge premium paid: $18M total ($33.96 per contract × 5,300 contracts)

- 🎯 Strike selection: $170 is actually IN-THE-MONEY by $23.22 (current price $193.22), not out-of-the-money speculation

- ⏰ Strategic timing: 74 days to expiration (March 20th expiration) captures Q3 FY2026 earnings on March 16, TikTok deal closure (Jan 22), and Stargate project milestones

- 📊 Size matters: 5,300 contracts represents 530,000 shares worth ~$102M in stock exposure

- 🏦 Institutional positioning: Deep in-the-money calls suggest leveraged long exposure, not speculative lottery tickets

What's really happening here: This trader is using deep ITM calls as a stock replacement strategy - getting leveraged long exposure to 530,000 shares of ORCL while only putting up $18M instead of $102M. The $170 strike is already $23 in-the-money, meaning this position has high delta (moves nearly 1:1 with the stock) and acts like owning the stock with 5.7x leverage. Think of it as borrowing money to buy stock, but with defined risk if things go south.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-score 4.07) - This trade size is dramatically larger than normal ORCL activity. The classification shows only 1 similar trade in recent history, and the volume signal indicates this is fresh "OPEN" activity, not closing an existing position. We're seeing sophisticated money establishing a new bullish position at depressed levels.

Why buy deep ITM calls instead of just buying stock?

- 🎯 Leverage: Control $102M worth of stock with only $18M capital (5.7x leverage)

- 💰 Defined risk: Maximum loss is $18M vs. potential unlimited downside on stock

- 📅 Time-bound thesis: If ORCL doesn't recover by March 20th, they're out cleanly

- 🎢 Capture specific catalysts: Q3 earnings (March 16), TikTok deal, Stargate milestones all within this timeframe

📈 Technical Setup / Chart Check-Up

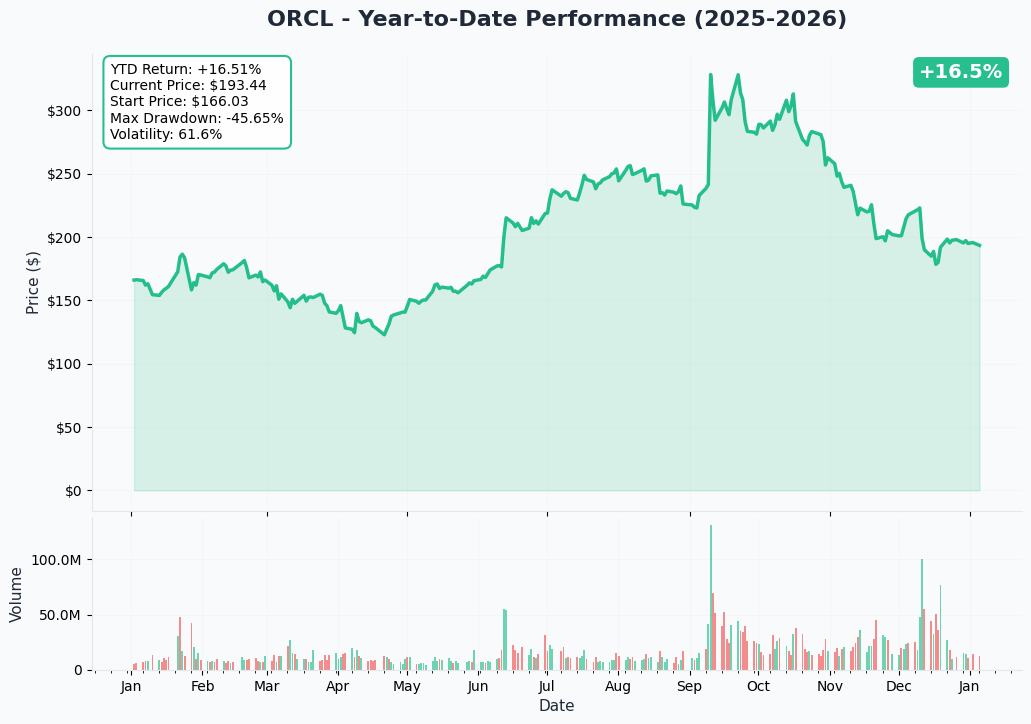

YTD Performance Chart

The chart tells a brutal story of boom and bust - ORCL absolutely exploded to an all-time high of $345.72 on September 10, 2025 after announcing the massive OpenAI Stargate partnership, up from $166.32 at the start of 2025. But the subsequent December earnings report triggered an epic collapse, with the stock now trading at $193.22, down 44% from peak.

Key observations:

- 💥 Epic rally then crash: Surged 36% to $345.72 intraday high on OpenAI partnership announcement, representing the third-sharpest rally since 1986 IPO

- 📉 Brutal selloff: Down 40-45% in just 3 months, making Q4 2025 potentially worst quarter since 2001

- ⚠️ Cash burn fears: December 2025 earnings showing $50 billion capex guidance and negative $10 billion free cash flow spooked investors

- 📊 Still up YTD: Despite the carnage, ORCL is still +17.68% YTD from $166.32 starting price

- 🎯 Smart money sees value: This $18M call buy suggests institutions think the selloff is overdone

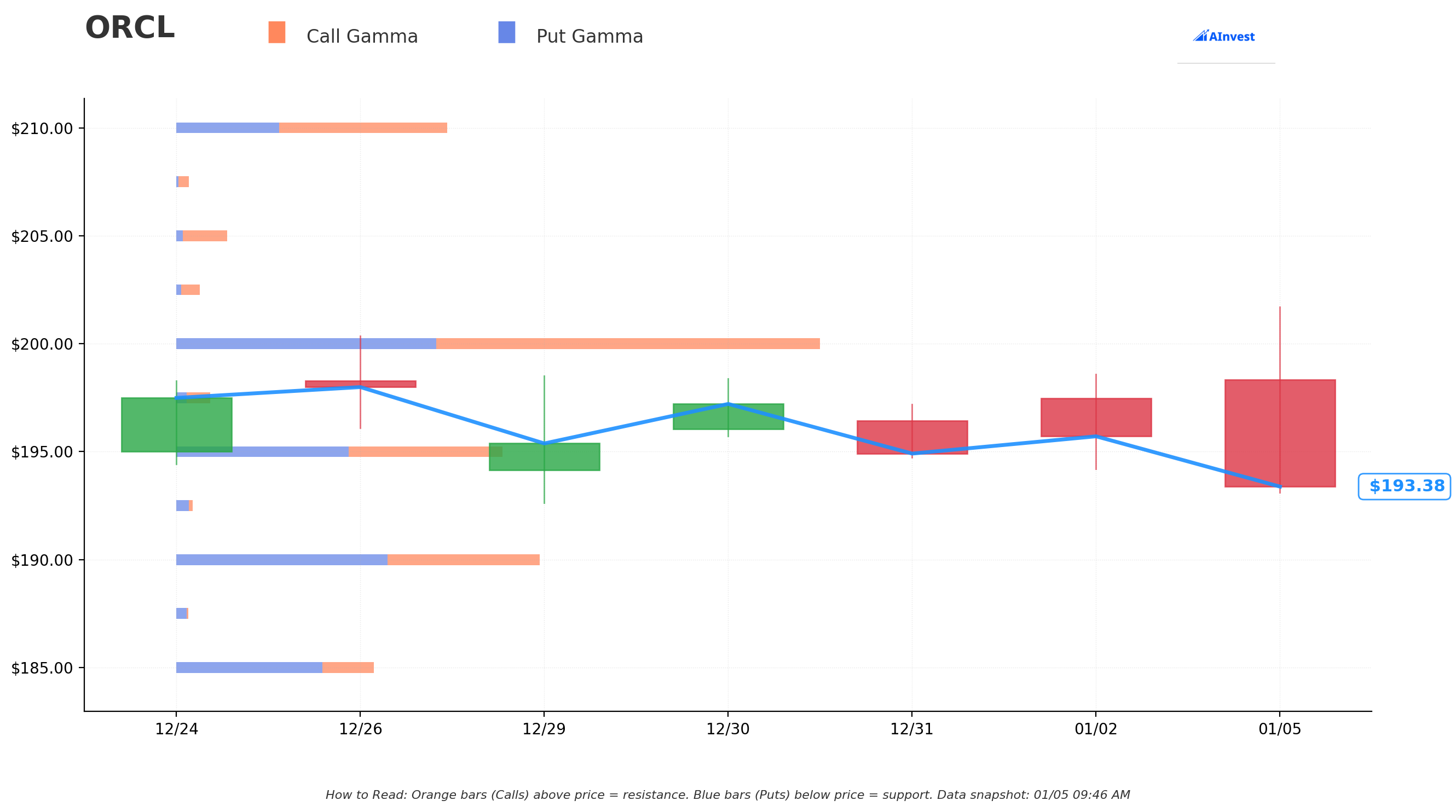

Gamma-Based Support & Resistance Analysis

Current Price: $193.22

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $190 - Immediate support with 20.2B total gamma exposure (strongest nearby floor with put dominance of 11.8B vs 8.4B calls)

- $185 - Secondary support at 11.1B gamma (put-heavy at 8.2B)

- $180 - Major structural floor with 16.1B gamma (12.3B in puts - this is a CRITICAL LINE)

- $170 - Deep support at 8.8B gamma (exactly where this call is struck! Not coincidental)

- $160 - Extended support zone with 5.8B gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $195 - Immediate ceiling with 18.1B gamma (put-heavy at 9.6B - shows lingering bearishness)

- $200 - MAJOR resistance with 35.5B gamma (STRONGEST LEVEL on entire chain - 21.0B calls vs 14.5B puts, first call-dominated strike above current price)

- $210 - Secondary resistance at 14.8B gamma (calls winning 9.1B vs 5.7B puts)

- $220 - Extended ceiling with 16.0B gamma (calls at 9.6B)

- $230 - High-altitude target at 7.8B gamma

What this means for traders: ORCL is trading in a put-dominated zone between $190-$195, showing market makers positioned defensively. However, the MASSIVE $200 strike (35.5B gamma - largest on the board) represents a critical battleground. Notice the shift - below $195, puts dominate; above $200, calls take over. This $195-$200 range is the pivot point where market sentiment flips from bearish to bullish.

Net GEX Bias: Bearish (112.3B put gamma vs 107.6B call gamma) - Overall positioning remains defensive despite this bullish trade, but the bias is nearly balanced. This suggests the market is at an inflection point.

Call buyer's thesis validation: The $170 strike sits at deep support with 8.8B gamma. If ORCL holds above $170, those calls stay in-the-money with full intrinsic value. The buyer is essentially saying: "I think ORCL bottoms at $170 worst case, and has clear path to $200+ over next 74 days."

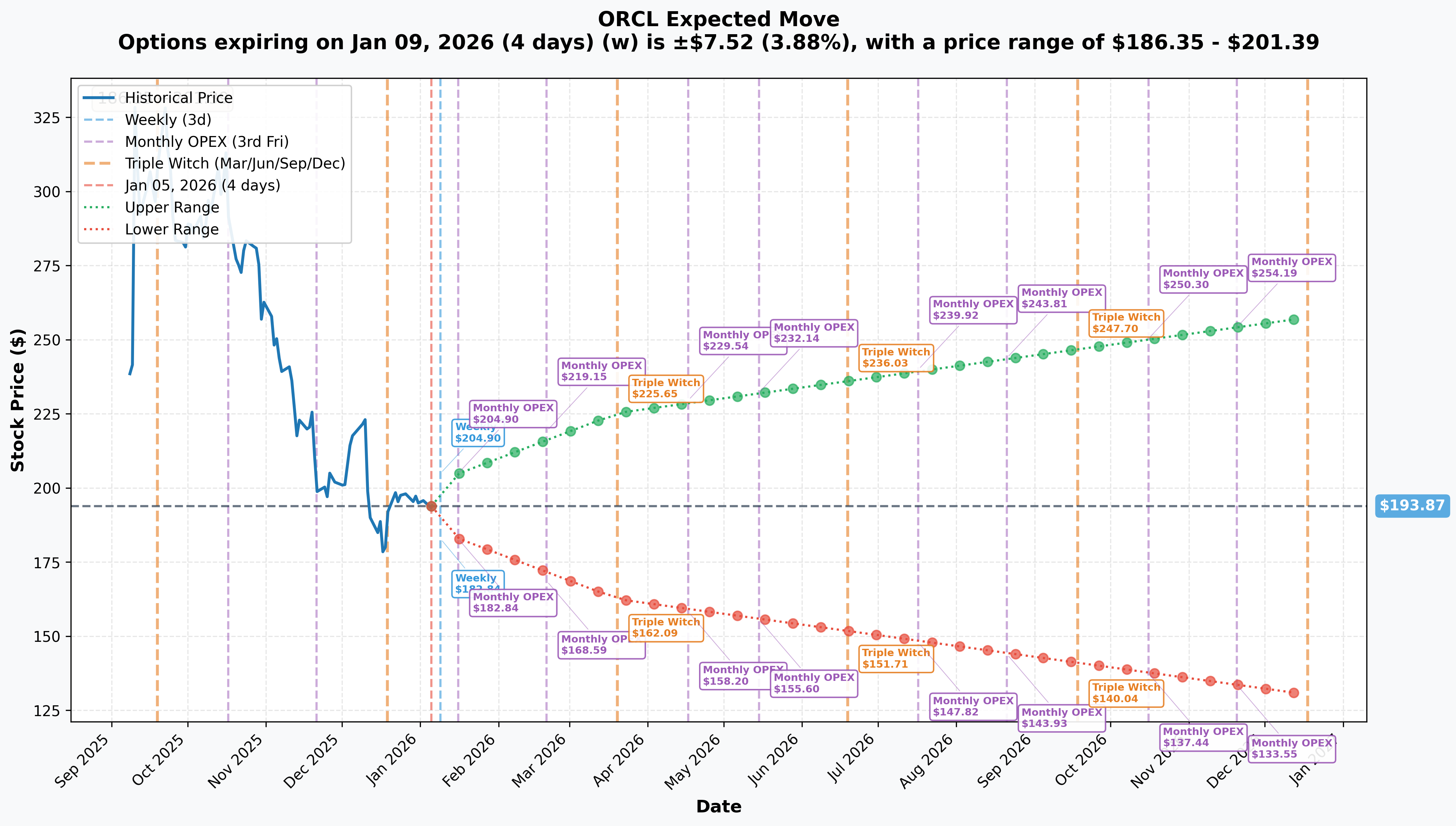

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 4 days): ±$7.52 (±3.88%) → Range: $186.35 - $201.39

- 📅 Monthly OPEX (Jan 16 - 11 days): ±$11.03 (±5.69%) → Range: $182.84 - $204.90

- 📅 Quarterly Triple Witch (Mar 20 - 74 days - THIS TRADE!): ±$31.43 (±16.21%) → Range: $162.44 - $225.30

- 📅 Yearly LEAPS (Dec 18 - 347 days): ±$63.62 (±32.82%) → Range: $130.25 - $257.49

Translation for regular folks: Options traders are pricing in a 3.9% move ($7.52) by this Friday for weekly expiration, but a MASSIVE 16.2% move ($31.43) through March 20th which includes the critical Q3 earnings on March 16th. The market expects VOLATILITY around earnings - that's huge for a $562B mega-cap stock!

The March 20th expiration (when this $18M trade expires) has an upper range of $225.30 - meaning the market thinks there's a real possibility ORCL could rally 16.6% over the next 74 days if AI momentum returns. This aligns perfectly with the call buyer's thesis: positioned for $170 floor with upside to $225+ if execution delivers.

Key insight: The sharp increase in implied volatility from 3.9% (weekly) to 16.2% (quarterly) reflects massive earnings uncertainty. The call buyer is paying for time through this binary event, betting that positive catalysts (TikTok deal, earnings beat, Stargate progress) overcome the negative cash flow narrative.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

TikTok U.S. Deal Closure - January 22, 2026 (17 DAYS AWAY!) 🎯

Oracle joined an investor group alongside Silver Lake and Abu Dhabi-based MGX to lead TikTok's U.S. operations. The deal is expected to close on January 22, 2026, providing Oracle with ongoing cloud services and data hosting revenue from one of the world's largest social platforms.

What's at stake:

- 📱 TikTok has 170+ million U.S. users generating massive data/compute requirements

- 💰 Oracle already provides cloud infrastructure for TikTok - deal formalizes and expands relationship

- 🚀 Stock jumped 7% when deal was announced in December 2025

- 🎯 Potential multi-billion dollar long-term revenue stream from content delivery, data storage, AI recommendations

Why this matters for the call trade: The January 22nd deal closure falls perfectly within the March 20th option expiration window. If the deal completes successfully and Oracle announces the financial terms or expanded scope, it could be the catalyst that breaks the stock out of the $190-$200 range and validates the turnaround thesis.

🚀 Near-Term Catalysts (Q1 2026)

Q3 FY2026 Earnings - March 16, 2026 (70 DAYS AWAY, 4 DAYS BEFORE EXPIRATION!) 📊

Oracle reports fiscal Q3 results on Monday, March 16, 2026 after market close. This is THE catalyst that will make or break this options trade - the call expires March 20th, just 4 days after earnings! Wall Street consensus and key expectations:

Company Guidance:

- 📊 Revenue: 19%-21% growth in USD (16%-18% constant currency) from Q2's $16.1B

- 💰 Non-GAAP EPS: $1.70-$1.74 guidance range

- 🤖 Cloud Revenue: 40%-44% growth expected

- ☁️ Cloud Infrastructure (IaaS): Following Q2's 68% YoY growth pace

Street Consensus:

- 📈 Revenue estimate: $16.91 billion

- 💵 EPS estimate: $1.71

Critical metrics to watch:

- 🏭 Cloud infrastructure revenue trajectory: Can they sustain 60-70%+ growth rates?

- 📊 Remaining Performance Obligations (RPO): Q2 showed $523 billion RPO, up 438% YoY - any sequential growth validates pipeline

- 💸 Free cash flow: Most critical metric! Was negative $10B in Q2, needs to show improvement or path to positive

- 🏢 OpenAI/Meta contract updates: Progress on Stargate deployment, any new major deals

- 🔢 Multicloud database growth: Q2 showed 817% YoY growth, proving AWS/Azure partnerships working

Upside surprise potential: Analysts see potential for cloud revenue to exceed guidance if multicloud database continues growing at 1,529% pace and OpenAI/Meta deployments accelerate faster than expected.

Downside risk factors: Any further deterioration in free cash flow, delays in Stargate data center construction, or conservative guidance citing macro uncertainty could trigger another leg down. Stock already down 44% from highs - high expectations for stabilization.

This is a HUGE BINARY EVENT for the call trade: With expiration on March 20th (4 days post-earnings), the call buyer is making a concentrated bet that Q3 earnings will be the TURNING POINT that validates Oracle's AI infrastructure thesis and reverses the negative sentiment. There's no time to recover if earnings disappoint - this is all-or-nothing.

🏗️ Strategic Catalysts (2026)

OpenAI Stargate Partnership: The $300 Billion Game-Changer 🤝

Oracle's landmark $300 billion, 5-year cloud computing agreement with OpenAI announced September 2025 represents the largest cloud deal in history:

Deal specifics:

- 🏭 4.5 gigawatts of data center capacity committed

- 🗺️ New data center campuses in Wyoming, Pennsylvania, Texas, Michigan, and New Mexico

- ⏰ Oracle confirmed project remains on schedule despite Bloomberg reports of delays

- 💪 First deployments expected H2 2026

Why this is transformational:

- ✅ Validates Oracle's technology at HIGHEST level - OpenAI chose ORCL to compete with their existing infrastructure

- 📊 $523 billion RPO provides exceptional multi-year revenue visibility

- 🎯 Positions Oracle as critical backbone for AI era, not just legacy database company

- 🚀 Potential to generate tens of billions in annual recurring revenue

The investor concern that caused the selloff: The $50 billion capital expenditure plan to build this infrastructure triggered negative $10 billion free cash flow in Q2, spooking investors about near-term cash burn. The call buyer is betting this is SHORT-TERM pain for LONG-TERM gain.

Michigan Stargate Facility Progress (Q1 2026):

- 📍 Saline Township facility construction commencing Q1 2026

- ⚡ 1.4 gigawatt capacity (one of world's largest data center projects)

- 👷 Estimated 450 on-site jobs, 1,500 across Washtenaw County

- 🔌 DTE Energy approved to power the facility

Meta Cloud Deal - $20 Billion Partnership 🏢

Oracle's $20 billion multi-year cloud computing deal with Meta confirmed October 2025 provides compute power for AI training and deployment:

- 💰 Part of $65 billion in cloud deals Oracle secured in 30 days

- 🤖 Focused on AI infrastructure for Meta's Llama models and other AI initiatives

- 📈 Diversifies customer concentration beyond just OpenAI

- ✅ Validates Oracle's competitive positioning vs AWS/Azure/Google Cloud

Multicloud Database Expansion (Through 2026) 🌐

Oracle's unique strategy of running Oracle Database on competitors' clouds is showing explosive growth:

Current status:

- 📊 Multicloud database business up 817% YoY in Q2 (fastest-growing segment)

- 🟠 Oracle Database@AWS: Currently 2 U.S. regions, 20+ more planned globally

- 🔵 Oracle Database@Azure: 10 regions live, 23 additional regions planned by end of 2025

- 🎯 Larry Ellison's target: $20 billion in database revenue within 5 years

Why this matters: Multicloud strategy unlocks the MASSIVE AWS/Azure/Google Cloud customer bases who previously wouldn't consider Oracle. It's like Apple Music being available on Android - suddenly your addressable market 10x's overnight. The 1,529% multicloud revenue growth rate shows this strategy is working.

⚠️ Past Catalysts (What Already Happened)

Q2 FY2026 Earnings - December 10, 2025 (THE CATALYST THAT CRASHED THE STOCK) 📉

While Oracle beat on most metrics, the market focused entirely on the negative cash flow and massive capex:

What went right:

- ✅ Revenue: $16.1B, up 14% YoY

- ✅ Non-GAAP EPS: $2.26, beating $1.64 consensus by 38%

- ✅ Cloud revenue: $8.0B, up 34% YoY (now 50% of total revenue)

- ✅ Cloud Infrastructure (IaaS): $4.1B, up 68% YoY

- ✅ RPO: $523B, up 438% YoY (exceptional backlog)

What spooked investors:

- ⚠️ Free cash flow: Negative $10 billion (vs consensus negative $5.2B)

- ⚠️ Capex guidance raised to $50 billion for FY2026 (from $35B)

- ⚠️ Total debt: $124 billion, up 39% YoY

- 😱 Stock dropped 11% in single session post-earnings

The debate: Bulls say this is infrastructure investment for long-term AI dominance. Bears say Oracle is burning cash to chase deals it may not be able to execute. The $18M call buyer is clearly in the bull camp, betting Q3 shows improvement.

Ampere Divestiture - November 2025 ✅

Oracle sold its stake in Ampere Computing to SoftBank for $6.5 billion, generating $2.7 billion pre-tax gain. This provides some cash to fund the massive capex program, though not nearly enough to cover the $50B commitment.

Larry Ellison announced "chip neutrality" policy, stating Oracle will work with all CPU and GPU suppliers while continuing to use Ampere chips in new A4 Standard instances with 35% higher performance.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20th expiration:

📈 Bull Case (30% probability)

Target: $220-$230

How we get there:

- 🎯 TikTok deal closes successfully on Jan 22 with positive terms, adding $1-2B annual revenue

- 💪 Q3 earnings CRUSH expectations with revenue at high-end of guidance ($19.4-19.6B), cloud growth 43%+

- 📊 Critical: Free cash flow improves materially or Oracle provides path to positive FCF by Q4

- 🏭 Stargate Michigan facility construction visibly progressing, validating $300B OpenAI deal execution

- 🌐 Multicloud database wins accelerate - major customer announcements from AWS/Azure partnerships

- 💰 RPO grows sequentially to $540-550B range, proving pipeline remains robust

- 🤖 AI/cloud infrastructure revenue mix expanding as planned

- 📈 Breakout above $200 gamma resistance (35.5B wall) triggers technical rally to $220-230 (implied move upper range)

Key metrics needed:

- Free cash flow better than negative $10B (ideally negative $5-7B with clear Q4 positive trajectory)

- Cloud infrastructure revenue growth sustained at 60%+ YoY

- Gross margins stable or expanding (proving pricing power despite capex)

- No further delays or execution concerns on Stargate

Probability assessment: 30% because it requires strong execution across multiple fronts AND investor sentiment shift from "cash burn concern" to "investing for growth" narrative. The $200 gamma wall (35.5B - largest strike) creates mechanical headwind that needs sustained buying to overcome.

Call P&L in Bull Case:

- Stock at $225 on March 20: Calls worth $55.00 intrinsic, profit = $21.04/share × 5,300 = $11.2M gain (62% ROI)

- Stock at $230 on March 20: Calls worth $60.00 intrinsic, profit = $26.04/share × 5,300 = $13.8M gain (77% ROI)

🎯 Base Case (45% probability)

Target: $185-$205 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ TikTok deal closes but terms underwhelm - no major stock catalyst

- 📱 Q3 earnings meet consensus (~$16.9B revenue, $1.70-1.72 EPS) without fireworks

- ⚖️ Free cash flow still negative but modestly better than Q2 (negative $8-9B range)

- 🤖 Cloud growth solid but not accelerating - steady 40-42% within guidance range

- 🏗️ Stargate progress steady but no major milestones before March 20

- 🇨🇳 No major positive or negative news on debt levels or execution risks

- 🔄 Trading within gamma support ($185-$190) and resistance ($200-$210) bands

- 💤 Volatility normalizes post-earnings back to 20-25% range from current 32%+

This is fair value scenario: Stock consolidates as investors wait for FREE CASH FLOW INFLECTION - the one metric that will determine if this is smart investment or reckless spending. Until Oracle proves it can generate positive FCF while maintaining cloud growth, stock stays range-bound.

Call P&L in Base Case:

- Stock at $190 on March 20: Calls worth $20.00 intrinsic, loss = $13.96/share × 5,300 = -$7.4M (41% loss)

- Stock at $195 on March 20: Calls worth $25.00 intrinsic, loss = $8.96/share × 5,300 = -$4.7M (26% loss)

- Stock at $200 on March 20: Calls worth $30.00 intrinsic, loss = $3.96/share × 5,300 = -$2.1M (12% loss)

- Stock at $205 on March 20: Calls worth $35.00 intrinsic, profit = $1.04/share × 5,300 = +$550K (3% gain)

Why 45% probability: This is the path of least resistance - stock has fallen far enough to find natural buyers (analysts still have $324.93 average price target, 45%+ upside), but negative FCF narrative prevents breakout. Most institutional players hold and wait for FCF proof point.

📉 Bear Case (25% probability)

Target: $165-$175 (TEST THE CALL STRIKE SUPPORT)

What could go wrong:

- 😰 Q3 earnings disappoint - revenue at low-end of guidance or miss, margins compress

- 🚨 Free cash flow WORSENS to negative $12-15B range - debt concerns intensify

- ⏰ Stargate project delays announced or Blue Owl financing issues resurface

- 🇨🇳 Moody's downgrades debt citing customer concentration risk (OpenAI/Meta)

- 💸 Broader tech selloff drags cloud stocks lower (AWS/Azure weakness, macro recession fears)

- 📊 OpenAI or Meta scales back deployment plans or timeline

- 🤖 Competitive pressure: AWS/Azure/Google Cloud respond aggressively on pricing

- 💰 TikTok deal falls through or terms disappointing

- 🔨 Break below $180 gamma support triggers cascade toward $170 call strike

Critical support levels:

- 🛡️ $185: Secondary support (11.1B gamma) - initial test likely

- 🛡️ $180: Major gamma floor (16.1B) - MUST HOLD or momentum shifts very bearish

- 🛡️ $170: Deep support (8.8B gamma) + this call strike - likely strong buying here from institutions

- 🛡️ $160: Disaster scenario (5.8B gamma) - breaks the entire AI thesis

Probability assessment: 25% because it requires Q3 earnings to actively DISAPPOINT after stock already down 44% from highs. Most negative news (high capex, negative FCF, debt concerns) is already known and priced in. However, execution risk on $300B+ contracts is real and any further deterioration could trigger capitulation.

Call P&L in Bear Case:

- Stock at $175 on March 20: Calls worth $5.00 intrinsic, loss = $28.96/share × 5,300 = -$15.3M (85% loss)

- Stock at $170 on March 20: Calls worth $0 (at-the-money), loss = $33.96/share × 5,300 = -$18M (100% loss)

- Stock at $165 on March 20: Calls expire worthless, loss = $33.96/share × 5,300 = -$18M (100% loss)

💡 Trading Ideas

🛡️ Conservative: Wait for Post-Earnings Clarity

Play: Stay on sidelines until after March 16th earnings, then reassess

Why this works:

- ⏰ Earnings on March 16th (4 days before option expiration) creates MASSIVE binary risk

- 💸 This $18M institutional call is essentially a 74-day EARNINGS BET - too concentrated for most retail

- 📊 Stock still digesting 44% decline from highs - needs time to find sustainable bottom

- 🎯 Better risk/reward waiting for Q3 to prove free cash flow improvement

- 📉 If earnings disappoint, could enter stock at $170-180 with much better margin of safety

- 🤔 Negative $10B FCF in Q2 is a REAL concern - want to see proof of improvement before committing

Action plan:

- 👀 Watch March 16th earnings closely for FCF trajectory, RPO growth, Stargate updates

- 🎯 If earnings beat AND FCF improves, look for post-earnings dip (IV crush) to enter stock $195-205

- ✅ Need to see: FCF better than negative $10B, cloud growth 40%+, positive Q4 guidance

- 📊 If earnings miss, wait for $170-180 test (deep value zone with gamma support)

- ⏰ Long-term (6-12 months), OpenAI/Meta deals are legitimate if Oracle can execute

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -15-25% drawdown if earnings disappoint and stock tests $170. Get better entry if stock consolidates post-earnings. Maintain optionality without risking capital into binary event.

⚖️ Balanced: Bull Put Spread on Earnings Strength

Play: After positive earnings reaction, sell bull put spread capturing gamma support

Structure: Sell $185 puts, Buy $175 puts (March 20 expiration - SAME as the $18M call trade)

Why this works:

- 🎢 Only enter AFTER March 16 earnings if results are positive and stock holds $195+

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Targets gamma support zone at $175-$185 where market makers positioned

- 🛡️ Essentially betting Oracle holds above $185 into March 20 expiration (just 4 days post-earnings)

- 💰 Collect premium from elevated IV, then benefits from time decay in final days

- 🤝 Aligns with institutional bullish positioning but with much better risk profile

Estimated P&L (enter day after positive earnings):

- 💰 Collect ~$2.50-3.50 credit per spread (adjust based on post-earnings IV)

- 📈 Max profit: $250-350 if ORCL above $185 at March 20 expiration (keep entire credit)

- 📉 Max loss: $650-750 if ORCL below $175 (spread width minus credit)

- 🎯 Breakeven: ~$182-182.50

- 📊 Risk/Reward: ~2.5:1 (collect $300 vs risk $700) - favorable for defined-risk bullish play

Entry criteria (ALL must be met):

- ✅ Q3 earnings beat on revenue AND show FCF improvement

- ✅ Stock trading above $195 day after earnings (March 17)

- ✅ Implied volatility elevated (can collect $2.50+ credit on $10-wide spread)

- ✅ Guidance for Q4 positive or in-line

Position sizing: Risk only 3-5% of portfolio per spread (this is short-dated directional play)

Risk level: Moderate (defined risk, bullish) | Skill level: Intermediate

🚀 Aggressive: Long Call Diagonal - Ride the Wave (ADVANCED ONLY!)

Play: Copy institutional positioning but with longer timeframe and lower cost

Structure:

- Buy $180 calls, June 2026 expiration (further out in time)

- Sell $200 calls, March 2026 expiration (near-term, against the gamma wall)

Why this could work:

- 🎯 Lower cost than buying March calls outright (sell premium against position)

- ⏰ June expiration gives more time for thesis to play out beyond single earnings print

- 💪 If ORCL rallies to $200 by March expiration, short calls get exercised but you keep June $180 calls for continued upside

- 📊 Benefits from time decay on short calls while maintaining long delta exposure

- 🚀 Breakeven much lower than buying March calls outright

- 🎢 Captures Q3 earnings (March 16) with room for Q4 earnings catalyst (late May)

Why this could blow up (SERIOUS RISKS):

- 💸 Still expensive: Diagonal costs $15-18 per spread ($1,500-1,800 capital)

- ⏰ Assignment risk: If stock rallies past $200 before March expiry, short calls assigned early

- 😱 Earnings risk: If March earnings crater stock below $180, both legs lose value

- 📊 Complexity: Requires managing two expirations and potential roll decisions

- ⚠️ Negative FCF: Core thesis of cash flow improvement could take longer than expected

- 🎰 Max profit capped: If stock goes to $250, you only make ($200-$180-cost) vs unlimited on long call

Estimated P&L:

- 💰 Cost: ~$15-18 net debit (June $180 call ~$25, March $200 call ~$7-10 credit)

- 📈 Max profit: $2-5 per spread if stock exactly at $200 at March expiration

- 🚀 Extended upside: Keep June $180 calls if assigned on March $200 - can ride to $220-250 by June

- 📉 Max loss: $15-18 (entire debit) if stock below $180 at March expiration

- 🎯 Breakeven: ~$195-198 at March expiration

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand diagonal spreads and early assignment mechanics

- ✅ Have capital to handle potential early assignment of short calls

- ✅ Can afford to lose entire premium (possible if earnings catastrophically bad)

- ✅ Comfortable with multi-leg options and rolling strategies

- ✅ Accept capped upside in exchange for lower cost basis

- ⏰ Have plan for what to do at March expiration (roll, close, exercise, etc.)

Risk level: HIGH (complex multi-leg, assignment risk) | Skill level: Advanced only

Probability of profit: ~50% (stock needs to stay above $195 by March, then has June runway)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💸 Massive cash burn with no end in sight: Negative $10 billion free cash flow in Q2 is EXTREMELY concerning. Oracle is literally hemorrhaging cash to build out AI infrastructure on $50 billion capex plan. While bulls say this is "investment for future," bears rightly point out Oracle needs to PROVE it can generate positive FCF while maintaining growth. Q3 earnings is the test - if FCF worsens or timeline to positive FCF extends, stock could retest lows.

-

📊 Customer concentration risk is EXTREME: Oracle's entire AI thesis rests on TWO customers - OpenAI ($300B deal) and Meta ($20B deal). That's $320B of the $523B RPO (61%!) tied to just two contracts. If EITHER customer scales back deployment, renegotiates terms, or experiences technical issues with Oracle's infrastructure, the entire investment thesis collapses. Moody's already flagged this concentration risk.

-

🏗️ Stargate execution risk at unprecedented scale: Building 4.5 gigawatts of data center capacity across multiple states is MASSIVE undertaking. For context, that's enough power for ~3 million homes. Oracle has NEVER built infrastructure at this scale. Blue Owl Capital already withdrew from Michigan project, forcing Oracle to seek alternative financing. Construction delays, permitting issues, power grid constraints, or cost overruns could derail timeline and burn even more cash.

-

💰 Debt load at $124 billion and climbing: Total debt up 39% YoY to $124 billion including operating lease liabilities. While Oracle has strong credit rating, rising interest rates make this debt MORE expensive to service. If negative FCF persists into 2026, Oracle may need to raise MORE debt or equity to fund capex, diluting shareholders. Goldman Sachs warned about rotation away from debt-funded capex names.

-

⚔️ Competing against hyperscalers with WAY deeper pockets: AWS, Azure, and Google Cloud have combined $527 billion in capex planned for 2026 per Goldman Sachs. Oracle's $50B is DWARFED by competition. These giants can afford to price aggressively, outspend on R&D, and wait longer for returns. Oracle is distant fourth with 4.5-5.1% cloud market share vs AWS (32%), Azure (23%), Google Cloud (11%). If hyperscalers view Oracle as threat, they could crush margins with pricing war.

-

⏰ Earnings binary event with call expiring 4 days later: This $18M call trade expires March 20, just 4 days after March 16 earnings. This is MAXIMUM concentration risk - entire position lives or dies on single earnings print. If Oracle guides conservatively or shows ANY weakness, stock could gap down 10-15% and these calls lose massive value overnight. Zero room for error or time to recover.

-

🌍 Macro headwinds if recession hits: At current valuation, Oracle is pricing in PERFECT execution. But if economy weakens in 2026 and enterprise IT budgets get cut, even OpenAI/Meta might slow deployments. Cloud spending is highly cyclical - Oracle's 68% IaaS growth rate would crater in recession. Stock could fall to $150-160 (back to early 2025 levels) if macro turns.

-

📉 Stock already had third-largest rally in company history, then crashed 44%: Oracle surged 36% to $345.72 on September 10, 2025 - the third-sharpest rally since 1986 IPO. Then crashed 44% in three months making Q4 2025 potentially worst quarter since 2001. This EXTREME volatility shows investor sentiment can shift violently. Technical damage from crash could take months/quarters to repair even if fundamentals improve.

-

🎯 Analysts still bullish but lowering targets: Post-Q2 earnings, Citi lowered target to $370 from $375 and Bank of America cut to $300 (18.5% reduction). While consensus $324.93 target implies 45%+ upside, the DIRECTION is concerning - analysts are reducing conviction. If Q3 disappoints, expect another wave of downgrades.

-

🔒 Valuation no longer cheap after 44% decline: At 34.63x trailing P/E with EPS of $5.33, Oracle still isn't "cheap" despite the selloff. Stock is up +17.68% YTD from $166.32, suggesting $193 level is closer to fair value than distressed pricing. For call to pay off meaningfully, need stock at $210+ (11% higher, 39x+ P/E) - requires multiple expansion which needs PROOF of FCF improvement.

🎯 The Bottom Line

Real talk: Someone just bet $18 MILLION that Oracle's AI infrastructure story is real and the 44% decline from all-time highs is a GIFT. This isn't a lottery ticket - it's a sophisticated institutional player using deep in-the-money calls to get 5.7x leveraged exposure to Oracle stock through the March 16th Q3 earnings catalyst.

What this trade tells us:

- 🎯 Smart money thinks $170 is the FLOOR - that's where they struck the calls and where major gamma support sits (8.8B)

- 💰 They're bullish enough to put up $18M instead of just buying stock - they want LEVERAGE on the rebound

- ⚖️ The March 20 expiration (4 days post-earnings) shows this is 100% an EARNINGS PLAY - bet on Q3 showing FCF improvement

- 📊 They believe negative $10B free cash flow narrative is TEMPORARY pain for long-term AI infrastructure gain

- ⏰ TikTok deal (Jan 22) and potential Stargate milestones provide near-term catalysts before main event (earnings)

This is NOT a "buy blindly" signal - it's a "the selloff may have gone too far" signal from institutions who did the homework.

The bull case is compelling:

- ✅ $523 billion RPO provides multi-year revenue visibility that's UNPRECEDENTED

- ✅ OpenAI partnership validates Oracle as credible AI infrastructure player, not legacy database company

- ✅ Multicloud strategy growing at 817-1,529% unlocking AWS/Azure customer bases

- ✅ Stock down 44% has removed a LOT of froth - analysts see 45%+ upside to $324.93 target

- ✅ If Oracle executes on Stargate, this $193 price will look CHEAP in 2027-2028

But the bear case is REAL:

- ⚠️ Negative $10B free cash flow with no clear timeline to positive is SCARY

- ⚠️ $124B debt and rising rates create financial stress

- ⚠️ Customer concentration (61% of RPO from OpenAI/Meta) is EXTREME risk

- ⚠️ Execution on gigawatt-scale data centers unproven - Blue Owl withdrawal concerning

- ⚠️ Hyperscalers have 10x Oracle's resources and could bury ORCL with pricing war

If you own ORCL:

- ✅ March 16th earnings is THE moment of truth - mark your calendar

- 📊 If holding through earnings, watch for: FCF improvement, RPO sequential growth, Stargate updates, Q4 guidance

- ⏰ Consider trimming position ahead of earnings and re-entering on weakness if you're nervous about binary risk

- 🎯 $170 is the LINE IN THE SAND per this institutional trade - if stock breaks below, thesis in serious trouble

- 🛡️ Long-term believers (12+ months) can weather volatility if they believe in AI infrastructure story

If you're watching from sidelines:

- ⏰ DO NOT chase before March 16 earnings - too much binary risk

- 🎯 Post-earnings pullback to $175-185 would be EXCELLENT entry with gamma support and post-FCF-clarity

- 📈 Looking for confirmation of: FCF improvement trajectory, RPO growth, cloud revenue 40%+ growth, positive guidance

- 🚀 Longer-term (6-12 months), if Oracle proves it can execute Stargate AND generate positive FCF by mid-2026, $250-300 is achievable

- ⚠️ Current $193 level is NOT distressed - it's closer to fair value. Need PROOF before paying up.

If you're bearish:

- 🎯 Wait for earnings - shorting into massive institutional call buying is dangerous

- 📊 Key breakdown level is $170 (call strike + gamma support) - below that opens $160 then $150

- ⚠️ Put spreads post-earnings offer better risk/reward than outright shorts given high borrow costs

- 📉 Watch for Q3 guidance cut, FCF deterioration, or Stargate delays as triggers

- ⏰ If earnings beat but stock can't hold $200 gamma wall, that's a SHORT signal (failed breakout)

Mark your calendar - Key dates:

- 📅 January 22, 2026 - TikTok U.S. deal expected to close

- 📅 March 16, 2026 (Monday) after market close - Q3 FY2026 earnings report (THE BIG ONE!)

- 📅 March 17, 2026 (Tuesday) - Post-earnings price action and analyst reactions

- 📅 March 20, 2026 - Monthly OPEX, $18M call trade expiration

- 📅 Q1 2026 - Michigan Stargate facility construction begins

- 📅 Mid-2026 - First OpenAI Stargate deployments expected

- 📅 Late May 2026 - Q4 FY2026 earnings (critical for full-year FCF assessment)

Final verdict: Oracle's AI infrastructure thesis is LEGITIMATE - the $300B OpenAI partnership and multicloud explosion are game-changing. BUT execution risk is REAL and near-term free cash flow remains deeply negative. The $18M institutional call purchase suggests smart money believes Q3 earnings will be the TURNING POINT that validates the investment thesis.

For most retail traders, the smart play is PATIENCE. Let March 16 earnings clear the air. If Oracle proves FCF is improving and Stargate is on track, you can buy stock at $195-205 with MUCH more confidence than speculating now. If earnings disappoint, you get a gift at $170-180.

The AI infrastructure buildout will take YEARS. There's no rush. Protect your capital and wait for proof. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 4.07 Z-score reflects this specific trade's unusual size relative to recent ORCL history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 10-20% gaps either direction. Deep in-the-money call strategies involve significant capital at risk and may not be suitable for all investors. The call buyer may have complex portfolio strategies or hedging needs not applicable to retail traders.

About Oracle Corporation: Oracle Corporation provides enterprise applications and infrastructure offerings through flexible IT deployment models spanning on-premises, cloud, and hybrid solutions. Established in 1977, the company pioneered commercial SQL-based relational database systems and has expanded into enterprise resource planning platforms and cloud infrastructure supporting AI model development, with a market cap of $562.3 billion in the Prepackaged Software Services industry.