🛡️ ORCL $22M Diagonal Put Spread - Smart Money Bracing for Turbulence on Oracle's AI Transformation!

📅 February 2, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just built a $22M diagonal put spread on Oracle at 09:49 this morning - buying ~18,500 contracts of $160 puts (March 2026) while simultaneously selling ~18,500 contracts of $135 puts (June 2026) for a net debit of roughly $5.6M. With ORCL down ~53% from its September all-time high of $345 and sitting right on the $160 gamma support wall, this is a sophisticated institutional play positioning for continued volatility through Q3 earnings on March 16th and the massive $50B capital raise. Z-scores above 130 mean this kind of size basically never happens.

📊 Company Overview

Oracle Corporation (ORCL) is a legacy software titan rapidly transforming into an AI infrastructure powerhouse:

- Market Cap: $472.9B

- Industry: Prepackaged Software (Enterprise Cloud & AI Infrastructure)

- Current Price: ~$164 (down ~53% from $345.72 ATH in September 2025)

- Primary Business: Enterprise databases, cloud infrastructure (OCI), AI model training, ERP platforms, and healthcare IT (Cerner)

- Employees: 162,000 | Founded: 1977 | HQ: Austin, TX

Oracle is at a crossroads - a company betting everything on AI cloud infrastructure with $50B in planned 2026 capital expenditures, $523B in remaining performance obligations, and a starring role in the $500B Stargate AI project with OpenAI. The stock has been hammered on cash burn concerns but the upside optionality is massive if execution delivers.

💰 The Option Flow Breakdown

📊 What Just Happened

The Tape (February 2, 2026 @ 09:49:04) - 4-Leg Complex Roll / Diagonal Put Spread:

| Time | Symbol | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:49:04 | ORCL | BUY | PUT | 2026-03-20 | $11M | $160 | 19K | 24K | 9,271 | $166.41 | $11.49 | ORCL20260320P160 |

| 09:49:04 | ORCL | BUY | PUT | 2026-03-20 | $11M | $160 | 9.3K | 24K | 9,270 | $166.41 | $11.49 | ORCL20260320P160 |

| 09:49:04 | ORCL | SELL | PUT | 2026-06-18 | $8.2M | $135 | 19K | 2.1K | 9,271 | $166.41 | $8.86 | ORCL20260618P135 |

| 09:49:04 | ORCL | SELL | PUT | 2026-06-18 | $8.2M | $135 | 9.3K | 2.1K | 9,270 | $166.41 | $8.86 | ORCL20260618P135 |

🤓 What This Actually Means

This is a diagonal put spread - one of the more sophisticated multi-leg options strategies out there. Let's break it down in plain English:

The Structure:

- 🛡️ Bought ~18,541 contracts of March 20 $160 puts for ~$22M total - this is near-term downside protection just 4% below the current price

- 💰 Sold ~18,541 contracts of June 18 $135 puts collecting ~$16.4M - this partially finances the hedge by selling insurance at a MUCH lower strike ($135, or ~19% below current price) further out in time

- 📊 Net debit: ~$5.6M ($22M spent - $16.4M collected)

- 🎯 Notional exposure: ~18,500 contracts = 1.85 million shares = roughly $304M worth of ORCL

Why diagonal instead of just buying puts?

- 💸 Buying $22M in puts outright is expensive. By selling the June $135 puts, this trader cut their cost by 75% (from $22M down to $5.6M net)

- ⏰ The March puts give IMMEDIATE protection through Q3 earnings (March 16) and the bond issuance

- 📅 The June short puts collect elevated premium from longer-dated options while the $135 strike is far enough below to provide comfortable room

- 🧠 This structure profits if ORCL drops to $135-160 range by March, or if volatility spikes heading into earnings

Unusual Score: 🔥 OFF THE CHARTS - Z-scores of 12.15, 5.73, 130.96, and 63.91 across the four legs, all rated EXTREMELY_UNUSUAL. The June $135 put leg at 130.96x is staggering - this kind of volume relative to open interest (9,270 contracts traded against just 2,100 OI) happens maybe a handful of times per year across all tickers. This is a serious institutional-size position.

📈 Technical Setup / Chart Check-Up

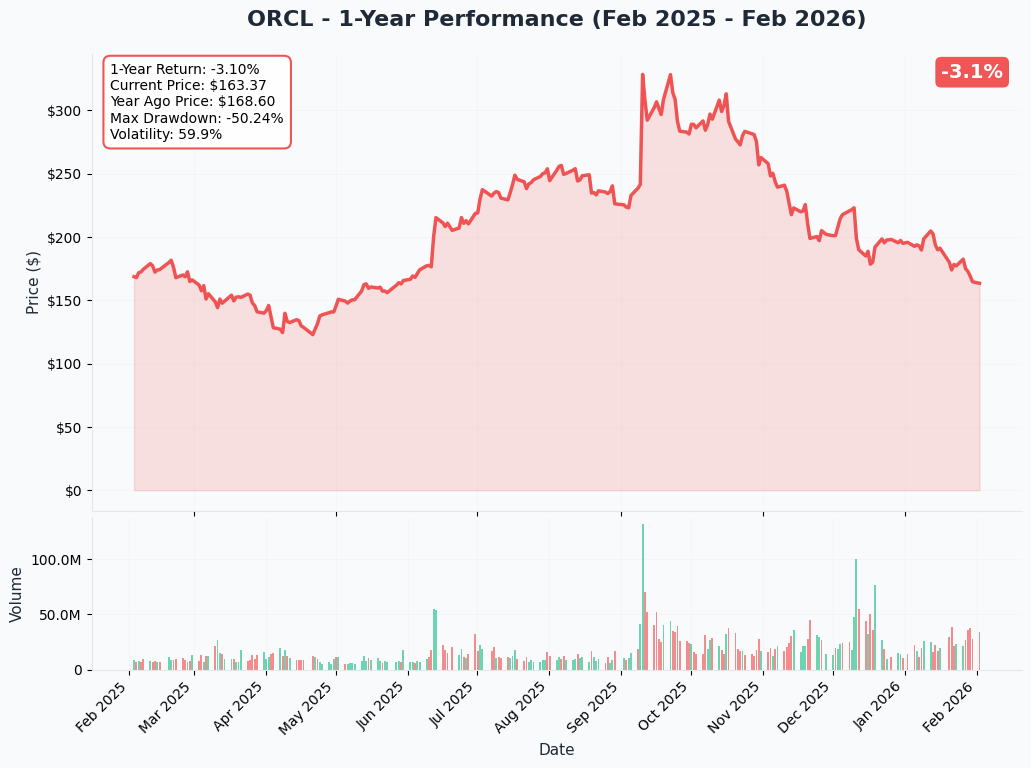

YTD Performance Chart

ORCL has been through the wringer. After reaching a breathtaking all-time high of $345.72 in September 2025, the stock has cratered roughly 53% to the $160s. This is on pace for the sharpest quarterly decline since 2001, driven by fears over $50B in annual capital spending, negative free cash flow, and customer concentration risk on OpenAI.

Key observations:

- 📉 Massive selloff: From $345 to $160 in about 5 months - brutal for a $470B mega-cap

- 🛡️ Finding a floor? Stock bounced off the $150-160 zone multiple times, suggesting institutional buying

- 📊 Gap up today: Jumped on the $50B financing plan announcement - trading in $163-169 range

- ⚠️ Still in a downtrend: Lower highs and lower lows since September - needs to reclaim $180+ to shift momentum

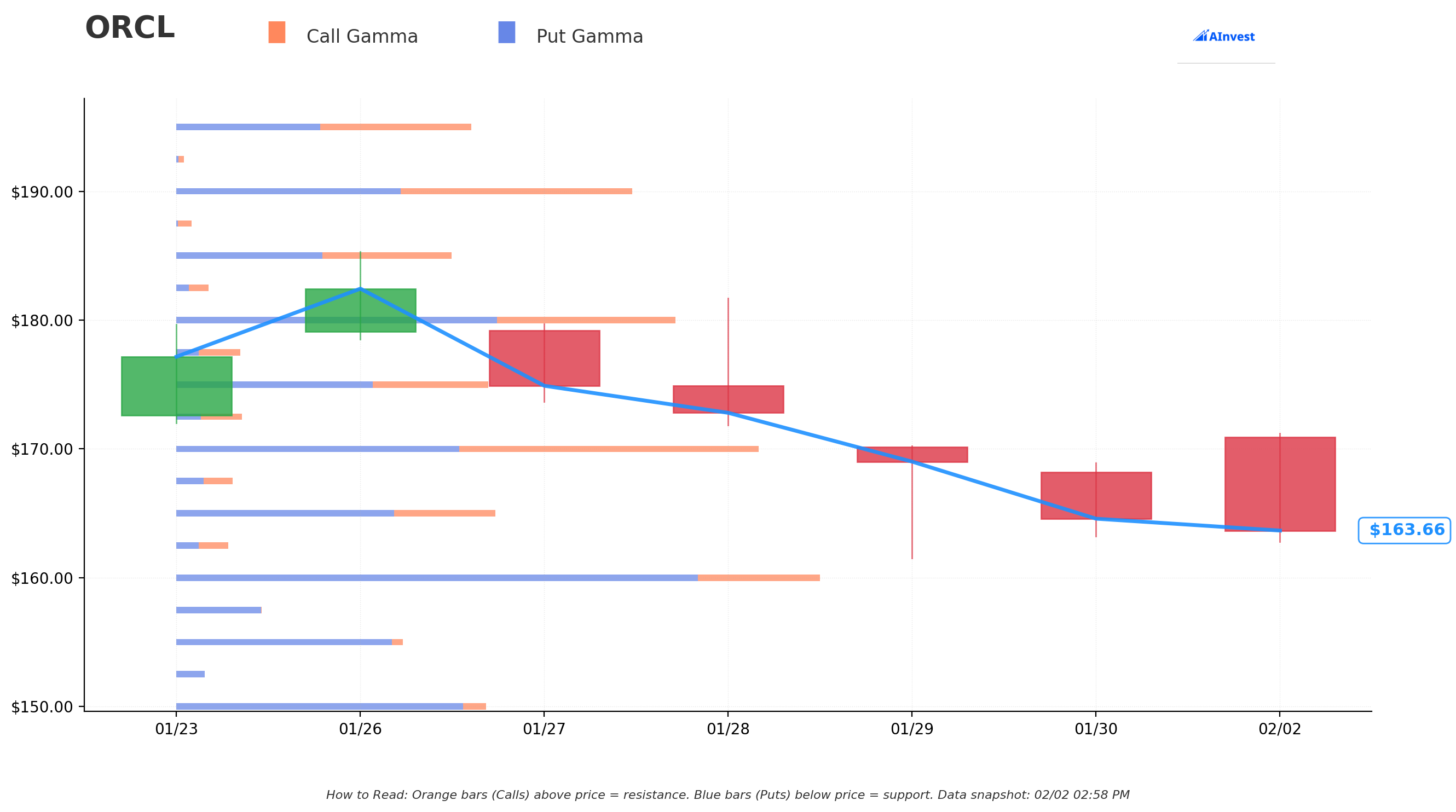

Gamma-Based Support & Resistance Analysis

Current Price: $163.95

The gamma exposure map reveals where the big players have positioned and where price is likely to stick or bounce:

🔵 Support Levels (Put Gamma Below Price):

- $160 - STRONGEST support with 18.8B total gamma (put gamma of 15.2B!) - THIS IS EXACTLY WHERE THE PUT BUYER STRUCK. Not a coincidence. Market makers will aggressively buy dips at this level.

- $150 - Secondary floor with 9.0B gamma (9.2% below current price)

- $145 - Deep support at 7.7B gamma (11.6% below current)

🟠 Resistance Levels (Call Gamma Above Price):

- $165 - Immediate ceiling at 9.3B gamma (just 0.6% overhead - practically on top of it)

- $170 - Major resistance at 17.0B gamma (3.7% above) - need to clear this for trend reversal

- $175 - Secondary resistance at 9.1B gamma

- $180 - Heavy ceiling at 14.6B gamma (9.8% above)

- $185 - 8.0B gamma

- $190 - Strong resistance at 13.3B gamma (15.9% above)

What this means for traders: ORCL is sandwiched between massive $160 support (18.8B gamma) and $170 resistance (17.0B gamma). The $160 level is THE line in the sand - it has the highest gamma exposure of any nearby strike, meaning market makers will fight to keep the stock above that level. If $160 breaks, look out below toward $150 and $145.

The put buyer knows this. They bought the $160 strike March puts right at the gamma support wall. If ORCL loses $160, those puts go from slightly out-of-the-money to deep in-the-money fast. This is precision institutional positioning.

Net GEX Bias: Bearish (82.7B call gamma vs 122.2B put gamma) - Put gamma dominates across the board, indicating dealers are short puts and will need to sell stock as price declines (accelerating downside moves).

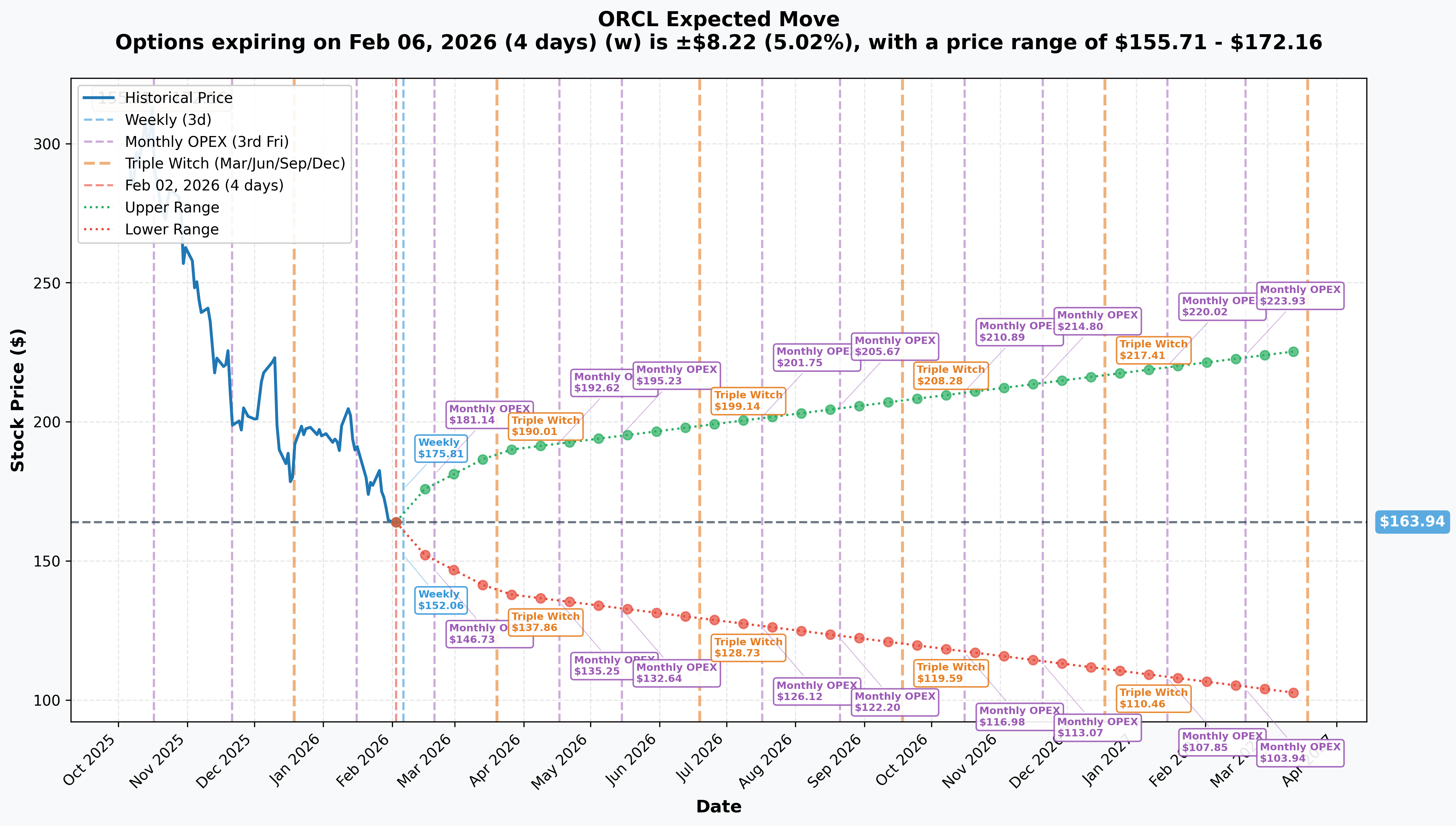

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Feb 6 - 4 days): +/-$8.22 (+/-5.02%) --> Range: $155.71 - $172.16

- 📅 Monthly OPEX (Feb 20 - 18 days): +/-$13.90 (+/-8.48%) --> Range: $150.04 - $177.83

- 📅 Triple Witch (Mar 20 - 46 days - BOUGHT PUT EXPIRATION!): +/-$25.48 (+/-15.54%) --> Range: $138.46 - $189.41

- 📅 LEAPS (Mar 2027 - 410 days): +/-$62.01 (+/-37.82%) --> Range: $101.93 - $225.94

Translation for regular folks: Options traders are pricing in a HUGE amount of uncertainty. The market expects ORCL could move +/-15.5% ($25.48) by the March 20th Triple Witch - that's a range from $138 to $189. The bought $160 puts sit comfortably in the middle of that expected range, meaning the options market thinks there's a real possibility ORCL trades below $160 before March.

The June expiration (where the $135 puts were sold) implies an even wider range. At $135, the sold puts are ~18% below current price - sitting near the outer edge of the expected move. The trader is essentially saying: "I need protection to $160 near-term, but I don't think ORCL drops below $135 by June."

Key insight: The 5% weekly implied move reflects extreme short-term uncertainty around the $50B capital raise announcement. This is NOT a calm stock right now.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 6 Months)

Q3 FY2026 Earnings - March 16, 2026 (6 WEEKS AWAY!) 📊

This is THE catalyst the bought puts are positioned for. Oracle reports fiscal Q3 on March 16th:

- 📊 Revenue consensus: ~$16.91B (16-18% growth in constant currency)

- 💰 EPS guidance: $1.70-$1.74 non-GAAP

- 🔥 Cloud revenue growth expected: 37-41% (must deliver to maintain narrative)

- ⚠️ Key risk metrics: Free cash flow trajectory, capex run rate, debt levels, RPO growth

- 📈 Full-year FY2026 EPS consensus: $5.97 (up 35.7% from FY2025)

$45-$50B Capital Raise - Imminent 💸

Oracle just announced plans to raise $45-$50B in calendar 2026 via balanced debt and equity:

- 📊 Debt side: Single large investment-grade bond offering expected any day now

- 💰 Equity side: Mandatory convertible preferred + at-the-market program up to $20B

- ⚠️ Dilution risk: Equity issuance at these depressed prices means MORE shares for LESS capital

- 🎯 Funds earmarked for OCI capacity to serve AMD, Meta, NVIDIA, OpenAI, TikTok, xAI

Potential 20,000-30,000 Job Cuts 🔪

TD Cowen reported Oracle is considering massive layoffs to free up $8-$10B in cash flow, plus a potential sale of the Cerner health-care unit ($28.3B acquisition in 2022). Not confirmed by Oracle yet, but would be a significant restructuring signal.

Stargate Data Center Buildout - Ongoing 🏗️

Oracle is building out multiple Stargate sites across the U.S. (Michigan, Ohio, Wisconsin, Texas) as part of the $500B joint venture with OpenAI, SoftBank, and MGX. Over $100B in capital already deployed as of January 9, 2026.

OpenAI GPT-6 Release - Expected Q1 2026 🤖

Could drive a step-change in AI demand and validate Oracle's infrastructure thesis. OpenAI's planned 2026 IPO would also significantly de-risk Oracle's largest customer relationship.

📰 Recent Catalysts (Already Happened)

Q2 FY2026 Results (December 10, 2025):

- Revenue of $16.1B slightly missed consensus of $16.2B despite 14% YoY growth

- EPS of $2.26 (up 54% YoY) crushed estimates

- OCI revenue up 66% YoY, GPU revenue up 177%

- RPO surged to $523B (up 438% YoY)

- Stock FELL 6%+ after-hours on revenue miss and capex fears

TikTok U.S. Joint Venture Closed (January 22, 2026):

- Oracle holds 15% stake alongside Silver Lake and MGX

- Oracle serves as "trusted security partner" hosting all U.S. user data on OCI

- TikTok U.S. ad revenue projected at $17B+ in 2026

Bondholder Lawsuit (January 14, 2026):

- Bondholders sued Oracle alleging the company concealed how much debt would be needed for the AI infrastructure buildout

Analyst Downgrades Wave:

- Morgan Stanley cut to $213 (from $320) on January 23

- UBS cut target to $280 (from $325) on January 5

- KeyCorp cut to $300, Bernstein cut to $339, RBC cut to $250

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and the catalyst landscape, here are the scenarios through the March 20th put expiration and beyond to the June 18th short put expiration:

📈 Bull Case (25% probability)

Target: $180-$190 by March 20 / $190-$200 by June 18

How we get there:

- 💪 Q3 earnings on March 16 CRUSH expectations - cloud revenue growth >44%, positive free cash flow trajectory visible

- 🚀 Bond offering prices at tight spreads, signaling credit market confidence in Oracle's AI bet

- 🤖 GPT-6 launch validates Oracle's infrastructure spend with visible demand pull-through

- 📊 Analyst upgrades flood in as "worst is priced in" narrative takes hold

- 🎯 Stock reclaims $170 gamma resistance, then pushes toward $180 (14.6B gamma) and $190 (13.3B gamma)

- 💰 Potential Cerner divestiture announced, generating $20B+ cash to address FCF concerns

Put spread P&L in bull case: Near total loss. Bought $160 puts expire worthless = -$22M. Sold $135 puts collected $16.4M. Net loss: ~$5.6M (the initial debit). This is simply the "insurance cost" the trader was willing to pay.

🎯 Base Case (45% probability)

Target: $150-$170 range by March 20 / $140-$165 by June 18

Most likely scenario:

- ✅ Q3 earnings meet guidance ($16.9B revenue, $1.70-$1.74 EPS) but no upside surprise

- 📊 Bond offering completes but at wider spreads, confirming credit concerns

- ⚖️ Stock bounces around the $160 gamma support and $170 resistance - classic range-bound

- 🔄 Market digests the $50B capital raise and dilution with modest selling pressure

- 💤 No major positive surprises - just execution on the buildout

- ⏰ By June, stock still trading $140-$165 as market waits for FY2027 proof points

Put spread P&L in base case: Modest gain to modest loss depending on exact price at March expiration. If ORCL at $155 in March, bought puts worth ~$5 each = $92.7M revenue on $22M cost, minus $16.4M collected on short puts (which still have time value). Net could be +$2-5M.

📉 Bear Case (30% probability)

Target: $135-$150 by March 20 / $110-$135 by June 18

What could go wrong:

- 😰 Q3 earnings disappoint - revenue misses, FCF deeply negative, capex even higher than feared

- 🚨 Bond offering struggles or prices at junk-like spreads - Barclays warned Oracle may run out of cash by November 2026

- 💸 Credit downgrade from Moody's or S&P (currently Baa2/BBB - just two notches above junk)

- 🇨🇳 OpenAI delays or scales back Stargate commitment - Bloomberg reported some data centers already pushed from 2027 to 2028

- 📉 Equity issuance at $150-160 creates dilution spiral

- 🔨 Break below $160 gamma support triggers cascade to $150, then $145, potentially $135

Put spread P&L in bear case: This is the payday. If ORCL at $140 by March 20: Bought $160 puts worth $20 each = $370M on $22M cost, minus ongoing short put obligation. If $135 by June: short puts at-the-money, maximum value extracted from both legs. The $5.6M net debit could generate $20-40M+ in profit.

Why 30% probability? Oracle's financial situation is genuinely concerning. Negative $10B free cash flow in Q2 alone, Morgan Stanley projects EPS of just $10.02 by 2030 vs management's $21 target, bonds trading at junk-like spreads despite investment-grade ratings, and a bondholder lawsuit. The fundamental bear case is real.

💡 Trading Ideas

🛡️ Conservative: "The Patience Play" - Wait for Q3 Earnings Clarity

Play: Sit on your hands until after March 16th earnings report

Why this works:

- ⏰ Q3 earnings in 6 weeks creates binary event risk with +/-15.5% implied move through March OPEX

- 💸 Options are EXPENSIVE right now - elevated IV means you're paying a premium for any directional bet

- 📊 Stock at critical $160 gamma support - could bounce hard OR break down, impossible to predict

- 🎯 Post-earnings IV crush will make options 30-50% cheaper for the SAME underlying exposure

- 🤔 When a $5.6M institutional diagonal put spread shows up, it means smart money sees REAL risk ahead

Action plan:

- 👀 Watch March 16 earnings: Revenue ($16.9B target), free cash flow (MUST show improvement), bond market reception

- 🎯 If stock drops to $145-150 post-earnings with gamma support, that's your buy zone with 40-50% upside to analyst consensus

- ✅ If stock rallies above $170 on earnings beat, wait for first pullback before chasing

- 📊 Monitor the bond offering pricing - tight spreads = buy signal, wide spreads = stay away

Risk level: Minimal (cash) | Skill level: Beginner-friendly

⚖️ Balanced: "The Copycat" - Simplified Put Spread

Play: Buy a scaled-down version of the institutional diagonal spread targeting March earnings

Structure: Buy ORCL March 20 $160 put, Sell ORCL March 20 $145 put (vertical put spread for simplicity)

Why this works:

- 🎯 $160 strike sits right on gamma support - if it breaks, profits accelerate

- 📊 Defined risk: $15-wide spread = max risk ~$800-1,000 per spread after credit from short leg

- ⏰ March 20 captures Q3 earnings (March 16) and any post-earnings follow-through

- 🤝 Essentially "copying" the institutional thesis but with defined risk and smaller capital

- 🛡️ Even if wrong, you know EXACTLY what you can lose

Estimated P&L (per spread):

- 💰 Net debit:

$6-8 per spread ($600-800 risk per contract) - 📈 Max profit: ~$7-9 if ORCL below $145 at March expiration ($700-900)

- 📉 Max loss: Premium paid if ORCL above $160

- 🎯 Breakeven: ~$152-154

- 📊 Risk/reward: roughly 1:1

Position sizing: Risk only 2-3% of portfolio. This is a directional bearish bet with a specific catalyst (earnings).

Risk level: Moderate | Skill level: Intermediate

🚀 Aggressive: "The Recovery Bet" - Selling Cash-Secured Puts for Entry

Play: Sell cash-secured puts to get paid to wait for a cheaper entry on ORCL's AI turnaround story

Structure: Sell ORCL June 18 $135 put at ~$8.86 per contract

Why this works:

- 💰 Collect $886 per contract in premium (6.6% return on $13,500 capital in 4.5 months)

- 🎯 $135 strike is ~18% below current price AND below every gamma support level - very comfortable cushion

- 📊 Analyst consensus averages $300+ (62-93% upside) - if you get assigned at $135, you own ORCL at an effective cost of ~$126 ($135 - $8.86 premium)

- 🤖 At $126, you'd be buying Oracle's $523B RPO backlog, 66% OCI growth, Stargate partnership, and TikTok JV at a massive discount

- ⏰ June expiration gives time for Q3 earnings, bond offering, and potential catalysts to play out

CRITICAL WARNINGS:

- ❗ You MUST have $13,500 per contract in cash ready if assigned (this is a capital-intensive strategy)

- ⚠️ If Oracle's credit situation deteriorates or OpenAI deal unravels, $135 could be IN-the-money fast

- 📉 Worst case: ORCL drops to $100-110 and you own it at $126 effective cost (20-25% underwater)

- 🎰 This is essentially saying "I'd happily own ORCL at $126 for the long-term AI buildout thesis"

Risk level: HIGH (large capital requirement, uncapped downside on stock ownership) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💸 Negative free cash flow is ALARMING: Oracle burned through $10B in negative free cash flow in Q2 alone (operating cash flow $2.1B vs $12B capex). At this rate, Barclays warned Oracle could run out of cash by November 2026. The $50B capital raise is a necessity, not a choice.

-

📊 Customer concentration risk on OpenAI: The $300B five-year deal with OpenAI could represent one-third of total revenues by FY2028. OpenAI is NOT currently profitable. If OpenAI defaults, renegotiates, or diversifies away (they already have $250B Azure deal and $38B AWS deal), it's catastrophic for Oracle.

-

🏦 Debt levels approaching danger zone: Total gross debt has ballooned past $130B with bonds trading at junk-like spreads despite investment-grade ratings (Baa2/BBB). Adding $45-50B more in 2026 could push leverage past 5x. A credit downgrade to junk would trigger massive forced selling.

-

⚖️ $50B dilution at depressed prices: Raising equity capital at $160 instead of $345 means Oracle must issue roughly 2x as many shares for the same capital. The mandatory convertible preferred and at-the-market program could meaningfully dilute existing shareholders.

-

🔨 Bondholder lawsuit creates legal overhang: Filed January 14, 2026, alleging Oracle concealed debt requirements. Legal uncertainty never helps a stock trading at distressed levels.

-

🏗️ Data center construction delays: Bloomberg reported some U.S. data centers for OpenAI pushed from 2027 to 2028 due to labor and material shortages. Delays mean deferred revenue but ongoing costs.

-

📉 Bearish gamma positioning amplifies downside: With net GEX bias bearish (122.2B put gamma vs 82.7B call gamma), market maker hedging will ACCELERATE selling pressure if $160 support breaks. The gamma structure works AGAINST bulls right now.

-

🎯 Morgan Stanley's bear case is sobering: Analyst projects Oracle cash capex of ~$275B between FY2026-2028 (far above consensus), and slashed 2030 EPS estimate to $10.02 vs management's $21 goal. That's a 52% miss on long-term earnings targets.

🎯 The Bottom Line

Real talk: A sophisticated institutional player just built a $5.6M net diagonal put spread on Oracle - buying near-term downside protection at the $160 gamma support wall while financing it by selling longer-dated puts at $135. This is NOT a panic trade. This is calculated risk management by someone managing a very large ORCL position through one of the most uncertain periods in Oracle's history.

What this trade tells us:

- 🎯 They see SIGNIFICANT downside risk through March 16th earnings - enough to pay $22M for puts (even after collecting $16.4M from the short leg)

- 💰 They DON'T think ORCL goes below $135 by June - that's where they're comfortable selling insurance

- ⚖️ The $160 strike on the gamma support wall shows precision - they know exactly where the floor is and they're protecting right at it

- 📊 Z-scores above 130 mean this trade is in the top 0.01% of all ORCL options activity - someone is taking this VERY seriously

- ⏰ The diagonal structure suggests they're playing for a MOVE, not just directional - they want to profit from near-term volatility while staying positioned longer-term

If you own ORCL:

- 🛡️ Consider protective puts or reducing position size ahead of March 16 earnings

- 📊 Set a mental floor at $160 - if it breaks, the gamma structure suggests accelerated selling toward $150

- ✅ Long-term thesis (Stargate, $523B RPO, OCI growth) remains intact, but short-term pain possible

- 🎯 If you believe in the AI buildout story, any pullback to $135-145 is a generational buying opportunity

If you're watching from sidelines:

- ⏰ March 16 Q3 earnings is the next major inflection point - wait for it

- 📊 Watch the bond offering pricing closely - it's a better signal than earnings for Oracle's financial health

- 🎯 Best entry zones: $145-150 (gamma support) for moderate risk, $135 (short put strike) for aggressive accumulation

- 🤔 The analyst consensus target of $300+ represents 62-93% upside from current levels - IF execution delivers

If you're bearish:

- 📉 Put spreads through March 20 expiration capture earnings catalyst with defined risk

- 🎯 Watch $160 support - a break below triggers gamma cascade

- ⚠️ Don't short into the $50B financing announcement momentum - wait for the dust to settle

- 📊 The implied move of +/-15.5% through March suggests the options market agrees volatility is coming

Mark your calendar - Key dates:

- 📅 February 2026 (imminent) - Bond offering pricing (credit market verdict on Oracle)

- 📅 March 16, 2026 - Q3 FY2026 earnings report (46 DAYS!)

- 📅 March 20, 2026 - Triple Witch / Bought put expiration

- 📅 June 2026 - Q4 FY2026 earnings + Sold put expiration (June 18)

- 📅 H2 2026 - Stargate capacity ramp and OpenAI deployment milestones

Final verdict: Oracle is the most polarizing mega-cap stock in the market right now. The bull case ($523B RPO, 66% OCI growth, Stargate, TikTok) and the bear case ($10B quarterly cash burn, $130B+ debt, customer concentration, dilution) are BOTH compelling. This institutional diagonal put spread says: "I'm protecting for the worst while staying positioned for the long-term." That's a smart approach. Follow their lead - manage your risk, keep your position sizes reasonable, and let March earnings provide clarity.

The AI infrastructure buildout is real. The question is whether Oracle can finance it without breaking. We'll know a lot more in 46 days.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The extreme Z-scores (up to 130.96x) reflect this specific trade's size relative to recent ORCL option history - it does not imply the trade will be profitable or that you should follow it. Diagonal put spreads are complex multi-leg strategies with multiple expiration dates and risk profiles - ensure you fully understand the mechanics before trading. Always do your own research and consider consulting a licensed financial advisor before trading. Oracle's financial situation involves significant credit risk and potential for large price moves in either direction.

About Oracle Corporation: Oracle Corporation specializes in enterprise applications and cloud infrastructure, offering flexible deployment options including on-premises, cloud, and hybrid solutions. The company pioneered commercial SQL-based relational databases in 1977 and now provides enterprise resource planning platforms and cloud infrastructure used in AI model training, with a market cap of $472.9 billion in the Prepackaged Software industry.