🏛️ ORCL Institutional Covered Call Write - Smart Money Harvesting Premium After Blockbuster Earnings! 💰

📅 March 11, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just sold $11 MILLION worth of ORCL calls the morning after Oracle's strongest earnings quarter in 15 years! A 20,000-contract sale of the March 20 $170 strike calls — with spot at $167.73 — signals an institutional holder is monetizing the post-earnings premium pop with a classic covered call write. This isn't bearish; it's a sophisticated income-harvesting move with only 9 days until expiration and the stock still up double digits from yesterday's $149.40 close.

📊 Company Overview

Oracle Corporation (ORCL) is one of the world's largest enterprise software and cloud infrastructure companies:

- Market Cap: $429.4 Billion

- Industry: Services — Prepackaged Software (Enterprise Applications & Cloud Infrastructure)

- Exchange: NYSE

- Primary Business: Cloud infrastructure (OCI), autonomous databases, enterprise applications, and AI-driven infrastructure services for hyperscalers, governments, and enterprises worldwide

Oracle's OCI has emerged as a differentiated AI infrastructure player, securing landmark contracts with OpenAI, Meta, and NVIDIA while simultaneously winning federal clients like CMS (Medicare/Medicaid) and the US Air Force. Its Q3 FY2026 earnings — reported March 10, 2026 — delivered the company's strongest organic growth in over 15 years.

💰 The Option Flow Breakdown

📊 The Tape (March 11, 2026 @ 10:50:48)

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:50:48 | ORCL | SELL | CALL | 2026-03-20 | $11M | $170 | 29K | 2K | 20,000 | $167.73 | $5.31 | ORCL20260320C170 |

🤓 What This Actually Means

This is a post-earnings covered call write — and the mechanics matter here:

- 💼 The setup: The seller almost certainly owns 2,000,000 shares of ORCL stock (or equivalent long calls). They're selling the right for someone else to buy those shares at $170 by March 20 — just $2.27 above where the stock is trading right now.

- 💸 Premium collected: $5.31/share × 20,000 contracts × 100 shares = $11M in cash, pocketed upfront

- 🎯 Effective exit price if called away: $167.73 (spot) + $5.31 (premium collected) = $175.04 effective sale price per share — a 4.4% buffer above spot

- ⏰ 9 days to expiration: The March 20 expiry is also a quarterly triple witch — elevated options settlement activity is expected

- 📊 Vol/OI ratio of 14.5x: This trade created roughly 14.5x the existing open interest — that's a flood of new contracts, confirming this is fresh positioning, not a close of an existing position

Real talk: why would anyone do this?

Oracle just ripped 10% in after-hours on March 10 earnings. The stock was at $149.40 yesterday and now trades at $167.73 — an institutional holder sitting on a monster unrealized gain is essentially saying: "I'll cap my upside at $170 for the next 9 days and pocket $11M in premium while I decide what to do next." If the stock stays below $170, they keep the premium and all their shares. If it runs past $170 and they get called away, they exit at an effective $175.04 — not a bad outcome from a $149 stock yesterday. This is textbook premium harvesting after an earnings event.

The 14.5x Vol/OI ratio is what makes this extremely unusual — this level of flow shows up a few times a year in ORCL, not every week.

📈 Technical Setup / Chart Check-Up

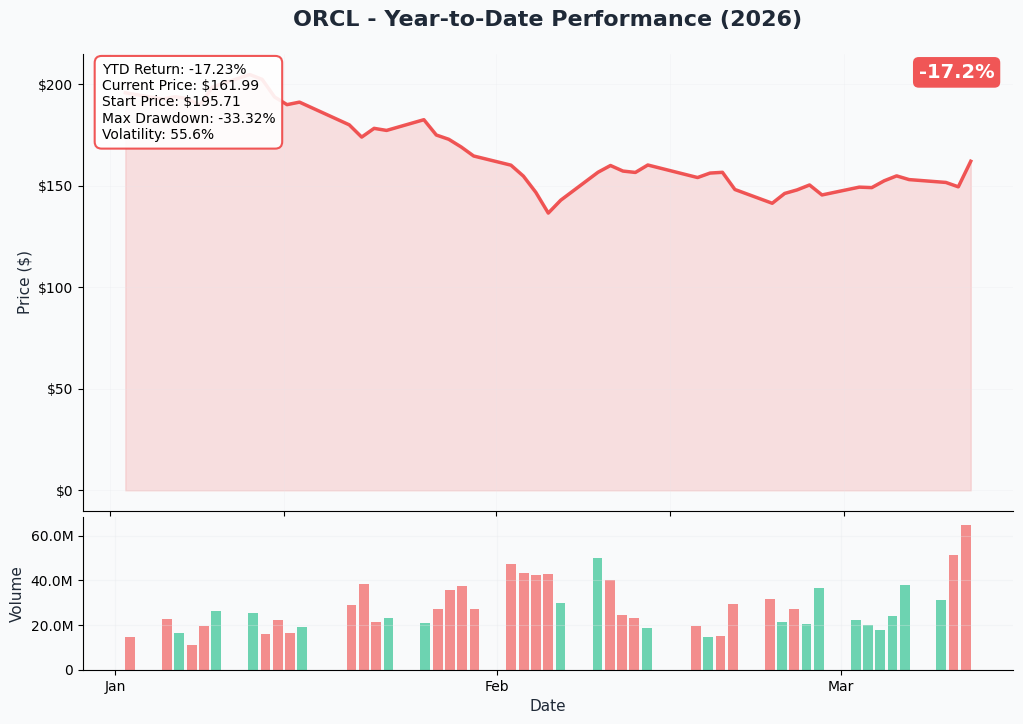

YTD Performance

ORCL's 2026 has been a tale of two chapters. The stock entered the year off its $345.72 all-time high and spent January through early March grinding lower — down roughly 23% YTD from year-end 2025 levels — as the market digested the December Q2 miss and rising capex concerns. Then March 10 happened: Oracle crushed Q3 FY2026 estimates with $17.2B in revenue (+22% YoY) and cloud revenue of $8.9B (+44% YoY), sending the stock surging from $149.40 to current levels around $167-168.

Key observations:

- 📈 Earnings gap-up: Stock surged ~12% from March 10 close to current trading — the post-earnings move is still live

- 🔻 YTD context: Despite the earnings rip, ORCL remains well below its 52-week high of $345.72, down roughly 52% from peak

- 🎢 Volatility environment: Elevated IV post-earnings creates rich premium for covered call writers — exactly why this trade makes sense today

- 📊 $149.40 close yesterday to $167.73 today = $18.33 one-day move; the options market is still pricing in meaningful near-term volatility

🔵🟠 Gamma-Based Support & Resistance

Current Price: ~$162-168 (intraday)

The gamma exposure map reveals exactly where market makers are loaded up — and it explains why $170 is the perfect covered call strike:

🔵 Support Levels (Put Gamma Below Price):

- $160 — Strongest nearby support with 33.9B total gamma exposure. This is the immediate floor — market makers will aggressively buy dips here

- $155 — Secondary support at 12.7B gamma; roughly balanced call/put GEX (net: near-zero), suggesting a transition zone

- $150 — Structural floor at 16.9B total gamma with put gamma dominant (-3.2B net) — dealer hedging turns supportive here; also the prior day's closing price

- $140 — Deep support at 9.2B gamma with strong put dominance (-7.0B net); disaster scenario floor

🟠 Resistance Levels (Call Gamma Above Price):

- $165 — Nearest resistance at 23.9B gamma with call gamma dominant (+11.3B net). This is the IMMEDIATE ceiling — market makers have large call exposure here and will sell rallies

- $170 — Major resistance at 32.7B total gamma (+15.4B net call dominated). This is precisely the strike the covered call seller chose — and it's not random. Gamma data shows this is the strongest call gamma wall above price. The seller is essentially leaning on the options market's own gravitational pull

- $175 — Secondary resistance at 14.6B gamma; a breakout above $170 would next face this ceiling

- $180 — Extended resistance at 25.4B gamma (+8.6B net) — the next major cap if stock gaps above $175

- $190 — Outer resistance at 10.1B gamma; deep upside target

What this means for traders: The gamma map is essentially telling the same story as the covered call trade: $170 is where the market concentrates its largest call gamma mass above current price. The seller picked the level with the highest gravitational pull — a place where the stock is likely to approach but be capped by mechanical dealer hedging pressure. Smart positioning.

Net GEX Bias: Bullish (168.5B call gamma vs 112.3B put gamma) — overall dealer positioning skews bullish, but the call wall at $165-$170 creates near-term resistance that aligns perfectly with this trade's strike.

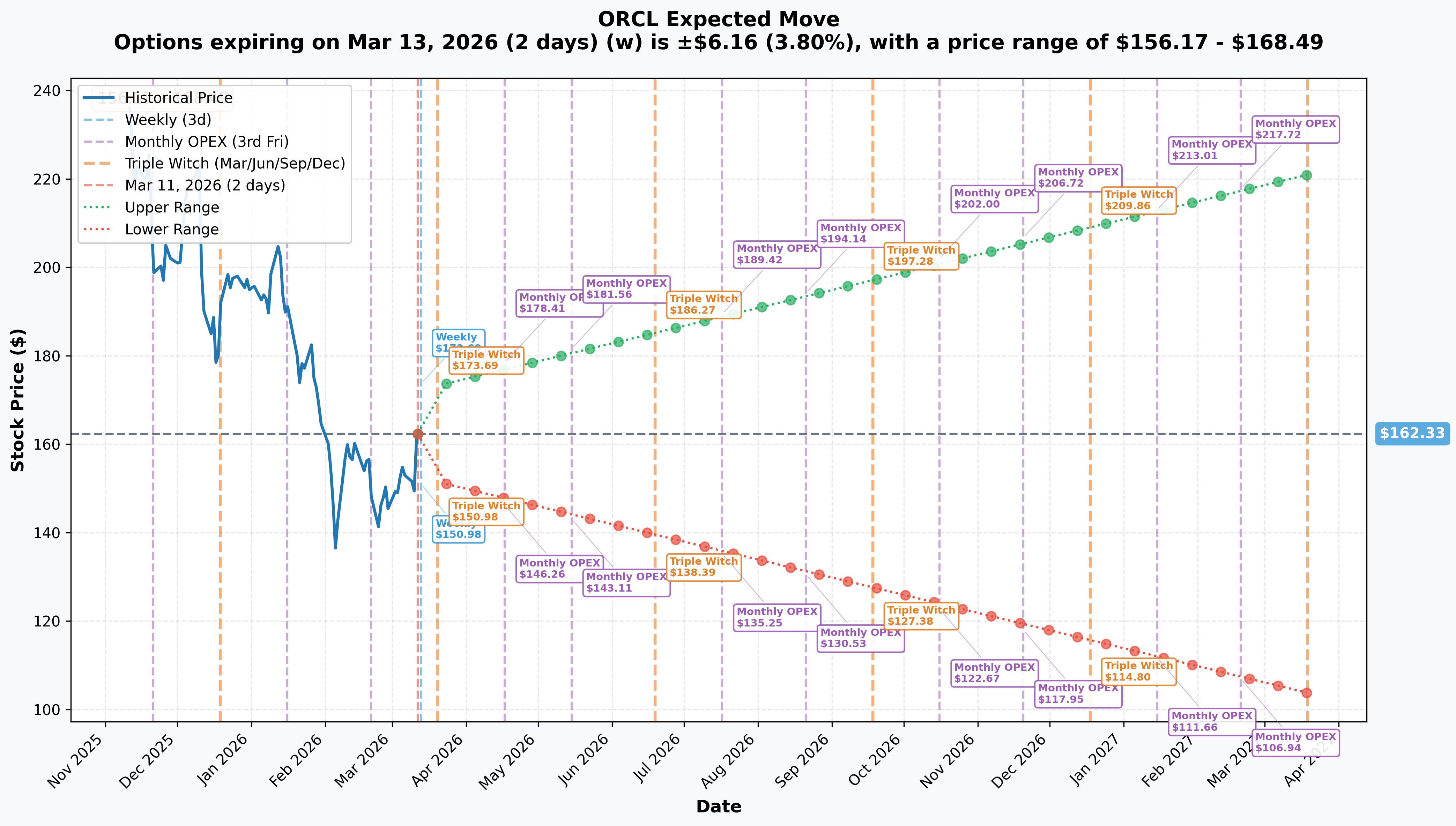

📉 Implied Move Analysis

Options market pricing for upcoming expirations:

| Timeframe | Expiry | Days | Implied Move | Range |

|---|---|---|---|---|

| 📅 Weekly | 2026-03-13 | 2 | ±3.8% (±$6.16) | $156.17 — $168.49 |

| 📅 Monthly OPEX / Triple Witch | 2026-03-20 | 9 | ±6.75% (±$10.96) | $151.37 — $173.30 |

| 📅 Yearly LEAPS | 2027-03-19 | 373 | ±36.1% (±$58.67) | $103.66 — $221.00 |

Translation for regular folks:

The options market is pricing a ±6.75% move ($10.96) through March 20 OPEX — the exact expiration this $11M covered call trade targets. The implied upper range is $173.30, sitting just above the $170 strike. That means the market is essentially saying there's a reasonable probability the stock could test $170-$173 range by expiration — which is exactly the scenario this covered call seller is comfortable with.

The $170 strike sits inside the implied upper bound of $173.30, which tells us the seller chose a strike where the stock is statistically likely to approach but potentially not blow through. If the stock hits $170 at expiration, the seller has maximized their premium income while keeping all shares. If it gaps to $175, they still exit at an effective $175.04 (spot + premium) — well within the implied range upper bound.

Key insight: This trade is constructed with precision relative to the implied move. The seller collected premium right at the edge of the market's expected range.

🎪 Catalysts

✅ Already Happened (Completed Catalysts)

🔥 Q3 FY2026 Earnings Beat — March 10, 2026

Oracle delivered its strongest organic growth quarter in over 15 years:

| Metric | Q3 FY2026 | YoY Change | vs. Consensus |

|---|---|---|---|

| Total Revenue | $17.2B | +22% | Beat ($16.9B expected) |

| Cloud Revenue | $8.9B | +44% | Beat |

| GAAP EPS | $1.27 | +24% | Beat |

| Non-GAAP EPS | $1.79 | +21% | Beat ($1.74 expected) |

| RPO | $553B | +325% | Expanded $30B sequentially |

- Cloud crossed 52% of total revenues for the first time ever

- RPO of $553B — backed by AI contracts with OpenAI, Meta, and NVIDIA — gives Oracle unprecedented backlog visibility

- JP Morgan upgraded ORCL to Overweight; Barclays raised target to $240

💰 $45-$50B Equity and Debt Financing Plan — February 1, 2026

Oracle announced a comprehensive capital raise plan, including ~$20-25B in investment-grade debt and ~$20-25B via equity instruments. The order book was oversubscribed, raising $30B within days and pushing 5-year credit default swaps down 17%.

🏥 CMS Medicare/Medicaid Cloud Contract — February 11, 2026

Oracle won a landmark federal healthcare contract to migrate CMS workloads serving 150+ million Americans to OCI over 36 months — one of the largest government cloud awards in history.

✈️ US Air Force Cloud One — February 2026

$88M contract for cloud infrastructure services — reinforcing Oracle's position in federal cloud.

⚠️ Stargate Abilene Expansion Cancellation — March 6, 2026

Oracle and OpenAI scrapped plans to expand the Abilene, TX data center from 1.2 GW to ~2.0 GW over financing disputes and OpenAI's shifting capacity projections. Oracle pushed back publicly, calling reports "incorrect" and affirming the broader 4.5 GW agreement remains intact. Risk: still a real overhang.

🚀 Upcoming Catalysts (Next 6 Months)

📅 Q4 FY2026 Earnings — June 16, 2026 (after close)

This is the single most important near-term catalyst. Management guided:

- Total revenue growth: 18-20% CC

- Cloud revenue growth: ~44-48% CC

- Full-year FY2026 revenue: $67B

- FY2027 target raised to $90B (~34% YoY implied growth)

🏗️ Stargate Abilene Campus Completion — Mid-2026

Buildings 3-8 are expected to complete mid-2026, with full campus deploying 450,000+ NVIDIA GB200 GPUs under a 15-year lease.

🏥 VA Cerner EHR Rollout — April 2026

4 Michigan VA medical centers go live with Oracle Health/Cerner EHR in April 2026 — a high-stakes execution event that could generate either positive or negative headlines.

☁️ Multi-Cloud Region Expansion

Oracle targeting 22 AWS regions for Oracle Database@AWS by end of Q4 FY2026. Larry Ellison projects multi-cloud could drive Oracle Database to $20B in revenue within five years.

🖥️ AMD MI450 GPU Deployments on OCI — Q3 2026

Oracle committed to deploying 50,000 AMD Instinct MI450 GPUs on OCI, diversifying GPU supply beyond NVIDIA.

🎲 Price Targets & Probabilities

Using the gamma levels, implied move data, and the current catalyst backdrop, here are three scenarios through the March 20 expiration and beyond:

📈 Bull Case — $173-$180 (30% probability by March 20)

How we get there:

- 🚀 Post-earnings momentum carries ORCL through the $165 gamma wall and challenges $170

- 📊 Continued analyst upgrades post-earnings (consensus PT ~$274-293) attract fresh buyers

- 🌐 Multi-cloud expansion news flow (AWS region additions) acts as incremental catalyst

- 📈 Breakout above $170 — against the gamma ceiling — could run to the $173.30 implied upper range and potentially the $175-$180 resistance zone

For the covered call seller: Stock gets called away at $170. Net effective exit = $175.04/share. Still a strong outcome.

🎯 Base Case — $160-$170 (50% probability by March 20)

Most likely scenario:

- ✅ Stock consolidates post-earnings gap in the $160-$170 range as buyers and sellers find equilibrium

- 🧲 The $170 call gamma wall ($32.7B exposure) acts as a natural ceiling — mechanical selling from dealer hedging caps the rally near the strike

- 📊 Implied move upper range is $173.30 — consolidation below $170 is well within statistical expectations

- 💤 Theta decay works rapidly with only 9 days to expiration — the covered call seller collects essentially all the $5.31 premium

- 🔵 $160 gamma support ($33.9B) provides a floor

For the covered call seller: Calls expire worthless, seller keeps $11M premium and all 2 million shares.

📉 Bear Case — $150-$160 (20% probability by March 20)

What could go wrong:

- 😰 Post-earnings euphoria fades, profit-taking from the 12% overnight surge drags stock back toward $155-$160 support

- 🚨 Stargate expansion cancellation concerns resurface or OpenAI relationship commentary disappoints

- 📉 Broader macro selloff drags tech lower; ORCL reverts toward the $150 pre-earnings close

- ⚠️ Break of $160 gamma support could see $155, then $150 tested

For the covered call seller: Premium is fully pocketed. Loss is on the stock itself (shares fall from $167.73), but the $5.31/share collected provides a partial buffer — their effective cost basis on any recent shares is $5.31 lower. This is where the beauty of the covered call shows: the premium partially offsets downside.

💡 Trading Ideas

🛡️ Conservative: Ride the Earnings Momentum with Defined Risk

Play: Buy ORCL shares or a call spread and hold through April OPEX

Why this works:

- 📊 Oracle's fundamentals post-Q3 are genuinely strong: $17.2B revenue (+22%), $553B RPO, cloud majority for the first time

- 📈 Analyst consensus target of $274-$293 implies 63-75% upside from current $167 levels — the stock remains deeply discounted from its 52-week high

- 🎯 Bull spread: Buy the April 17 $170/$185 call spread — costs roughly $4-5, max profit $15 if stock is above $185 at April OPEX

- 🔵 $160 gamma support gives a natural stop level; risk is defined

Structure: April 2026-04-17 $170/$185 call spread Max risk: ~$4-5 per spread (paid upfront) Max reward: ~$10-11 per spread if ORCL reaches $185 Breakeven: ~$174-175 at April expiration Why not just buy stock: The post-earnings gap means you're chasing; the spread lets you participate in upside while limiting downside to the premium paid

Risk level: Moderate | Skill level: Intermediate

⚖️ Balanced: Copy the Institutional Playbook — Your Own Covered Call

Play: If you own ORCL shares (or buy shares now), sell the March 20 $170 calls against your position — the exact same structure the institution just executed

Why this works:

- 💰 $5.31/share premium collected upfront — that's 3.2% return in 9 days, or roughly 130% annualized if you repeat it monthly

- 🧲 The $170 strike sits right at the gamma wall — statistically likely to be near where the stock pins at expiration

- 🛡️ The $5.31 collected lowers your effective cost basis; if ORCL falls back to $162, you're still profitable on a net basis

- 📅 Effective exit if called away: $175.04 — you're selling at a price above today's spot while getting paid to wait

What to watch:

- ✅ If stock stays below $170 at March 20 close: keep premium + keep shares, possibly sell again for April expiration

- 🎯 If stock rallies above $170: shares get called away at an effective $175.04 — book the gain and re-evaluate

- ❌ If stock tanks to $155-$160: you keep the premium but hold a losing stock position — ensure you're comfortable owning ORCL at these levels

Risk level: Low-Moderate (requires stock ownership) | Skill level: Intermediate | Best for: Existing ORCL holders who want income

🚀 Aggressive: Triple Witch + Earnings Momentum Play

Play: Buy the March 20 $170/$175 call spread, betting ORCL breaks through the gamma wall into triple witch

Why this could work:

- 🎢 March 20 is both monthly OPEX and a quarterly triple witch — settlement day volatility can create outsized moves

- 📊 Implied upper range for March 20 is $173.30 — the $175 short strike sits just outside the implied move, making this a cheap way to bet on an overshoot

- 🚀 Post-earnings momentum + JP Morgan Overweight upgrade + Barclays $240 target could attract momentum buyers this week

- 💥 Only need 1.4% additional upside from spot ($167.73 → $170) to start making money on the spread

Structure: Buy March 20 $170/$175 call spread (2026-03-20)

Estimated cost: ~$1.50-$2.50 per spread (narrow window, time decay aggressive)

Max reward: $5.00 per spread if ORCL above $175 at expiration (100-200% return)

Max risk: Full premium paid ($1.50-$2.50)

Breakeven: ~$171.50-$172.50

Serious warnings:

- ⚠️ 9 days to expiration means theta burns fast — you need ORCL to move NOW, not next week

- ❌ If stock stays flat at $168, this spread likely loses 60-80% of value by expiration

- 🎰 This is a directional bet with a tight window — size accordingly (no more than 1-2% of portfolio)

Risk level: High (full premium at risk) | Skill level: Advanced | Best for: Traders who believe post-earnings momentum continues this week

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Only 9 days to expiration — theta is ruthless: Any options position you put on today faces aggressive daily time decay. ORCL needs to move materially and quickly for directional bets to work. The covered call seller has theta working FOR them; you would have it working against you on long positions.

-

🚨 Stargate Abilene expansion cancellation overhang: Oracle and OpenAI scrapped the Abilene expansion plans just 5 days before earnings. Oracle pushed back, but the underlying tension about financing terms and OpenAI's shifting capacity needs is real. Any negative development on the broader 4.5 GW Stargate relationship could cause a sharp reversal.

-

💸 $50B capex with negative free cash flow through 2030: Oracle's massive infrastructure buildout is debt-funded. Long-term debt sits around $100B. Rising interest rates increase carrying costs. The financing plan reduces near-term liquidity risk, but the company is not self-funding its AI ambitions the way AWS or Azure are.

-

🐋 OpenAI concentration risk: TD Cowen has flagged that Oracle could face serious pressure if OpenAI delays or cancels commitments. The $553B RPO sounds massive, but concentration in a single counterparty (OpenAI) that is not yet profitably scaling at its own level is a legitimate tail risk.

-

🏥 Cerner / VA execution risk: Lawmakers are questioning the VA Oracle EHR rollout and GAO found most recommendations remain unimplemented. A high-profile failure at the VA in April could generate significant negative headlines. Additionally, Oracle may potentially sell Cerner at a write-down to fund AI infrastructure — a potential one-time hit.

-

📊 Stock still down 52% from 52-week high of $345.72: Despite the earnings rip, ORCL at $167 is still deeply underwater from its peak. Bulls need sustained execution over multiple quarters to rebuild confidence. Bears argue the AI capex cycle is overleveraged and the stock was overvalued at $345 — not $167.

-

💰 Potential 30,000 job cuts: Reports suggest Oracle may slash up to 30,000 jobs to redirect resources toward data center expansion. This could hit morale, product quality, and customer support — a slow-burn risk that doesn't show up in a single quarter.

-

🎢 Post-earnings gap = elevated near-term IV: The stock just moved $18+ in one day. Implied volatility is elevated, meaning options are priced richly. Buying premium here costs more than normal — one reason the institution is SELLING premium rather than buying it.

🎯 The Bottom Line

Real talk: This $11M covered call write is one of the cleaner reads you'll see in option flow. An institutional holder sitting on a massive ORCL position — suddenly up 12% overnight after Oracle's blockbuster Q3 FY2026 earnings — is doing exactly what sophisticated income investors do after a big move: harvest the premium spike.

Here's the math they're running:

- 🔵 Stock at $167.73 → they sell the $170 calls for $5.31 each

- 💰 Collect $11M upfront, in cash, today

- 🎯 If ORCL stays below $170 by March 20: keep $11M + keep all 2 million shares → rinse and repeat

- 📤 If ORCL runs above $170 and they get called away: effective exit at $175.04/share — not bad for a stock trading at $149 yesterday

The 14.5x Vol/OI ratio tells you this was a major fresh position, not a routine hedge. The choice of $170 as the strike — right at the heaviest call gamma wall above price — shows disciplined, technically-informed positioning.

If you own ORCL:

- ✅ Consider the covered call strategy yourself — selling the $170 or $175 call against your shares for income during a period of likely near-term consolidation

- 📊 The $160 gamma support is your key level; hold above that and the post-earnings thesis stays intact

- ⏰ Mark June 16, 2026 as the next major catalyst — Q4 FY2026 earnings will show whether the $553B RPO starts converting to recognized revenue at the pace bulls need

If you're watching from the sidelines:

- ⏰ Let the post-earnings dust settle this week before adding exposure — the 12% gap-up means you're chasing

- 🎯 A pullback to $160 (strongest gamma support) would be a cleaner entry with meaningful risk/reward

- 📈 Analysts averaging $274-$293 price targets means if Oracle executes on its $90B FY2027 guidance, there's significant upside from $167

- 🚀 The multi-cloud expansion across AWS, Azure, and Google Cloud regions is a real, durable growth driver that doesn't disappear in one quarter

If you're bearish:

- 🛡️ The covered call writer is already partially hedged — don't fight an institution that just spent $11M to monetize their position at $170

- 📉 Below $160 (the $33.9B gamma support), momentum could shift to $155, then $150

- ⚠️ Stargate execution risk + $100B debt + negative FCF through 2030 are legitimate longer-term bearish arguments

Mark your calendar — Key dates:

- 📅 March 13, 2026 — Weekly OPEX; implied ±3.8% move

- 📅 March 20, 2026 — Triple Witch / OPEX; this $11M covered call expires; implied ±6.75% move

- 📅 April 2026 — First VA Michigan EHR go-live; high execution risk

- 📅 Mid-2026 — Stargate Abilene campus buildings 3-8 completion milestone

- 📅 June 16, 2026 — Q4 FY2026 earnings (the next major inflection point)

Final verdict: Oracle's Q3 FY2026 was a genuine inflection — the fastest organic growth in 15 years, cloud crossing 50% of revenue, and a $553B RPO that gives unprecedented forward visibility. But the stock has already moved hard on this news, and the covered call writer just told you with $11M of their own money that $170 is their near-term ceiling. Respect the gamma wall. Let the post-earnings consolidation settle. Then assess whether the June earnings trajectory — and the $90B FY2027 guide — deserves a fresh commitment.

The $11M premium harvest is smart money saying: "We crushed it on earnings. Now we get paid to wait."

⚠️ Disclaimer: Options trading involves substantial risk of loss and is not appropriate for all investors. This analysis is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past unusual options activity does not guarantee future price performance. The covered call strategy described requires owning the underlying stock and carries the risk of capped upside if the stock rallies significantly above the strike price. All options positions carry the risk of total loss of premium paid. Near-term options with 9 days to expiration experience accelerated time decay. The Vol/OI ratio and Z-Score described reflect unusual activity relative to historical norms for this ticker and do not predict outcome. Always conduct your own due diligence and consider consulting a licensed financial advisor before making investment decisions.

About Oracle Corporation: Oracle Corporation provides enterprise applications and infrastructure offerings through cloud, on-premises, and hybrid deployment models. With a market cap of approximately $429.4 billion, Oracle operates as one of the world's largest enterprise software and cloud infrastructure companies, competing with AWS, Azure, and Google Cloud in the AI infrastructure space through its Oracle Cloud Infrastructure (OCI) platform.