💊 PFE $1.2M Bullish Call Bet - Someone's Loading Up Ahead of Two PDUFA Dates and Earnings!

📅 January 27, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $1.2 MILLION on PFE June $30 calls this morning - buying 28,000 contracts on a stock trading at $26.40. That's a bet that Pfizer rallies ~14% in the next 5 months, and the timing lines up perfectly with Q4 earnings on February 3, the Padcev PDUFA on April 7, and the vepdegestrant PDUFA on June 5. Translation: This trader is betting the patent cliff fears are overdone and Pfizer's pipeline delivers.

📊 Company Overview

Pfizer Inc. (PFE) is one of the world's largest pharmaceutical companies, with annual sales of roughly $60B:

- 💊 Market Cap: $147.2 Billion

- 🏥 Industry: Pharmaceutical Preparations (NYSE)

- 💵 Current Price: $26.40 (near 52-week lows)

- 💰 Dividend Yield: 6.65% ($1.72 annualized)

- 📊 Forward P/E: 8.8x (well below pharma peer average of 12-15x)

- 🧬 Primary Business: Prescription drugs and vaccines across oncology, cardiovascular, COVID-19, inflammation, and obesity therapeutics. Key products include Eliquis, Vyndaqel, Padcev, Paxlovid, and Comirnaty. International markets represent ~40% of revenues.

💰 The Option Flow Breakdown

The Tape (January 27, 2026 @ 10:24:02):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:24:02 | PFE | ASK | BUY | CALL $30 | 2026-06-18 | $1.2M | $30 | 28K | 61K | 26,728 | $26.40 | $0.45 |

🤓 What This Actually Means

This is a straight-up bullish bet on Pfizer's next 5 months. Here's the breakdown:

- 💸 Premium paid: $1.2M ($0.45 per contract x 26,728 contracts)

- 🎯 Strike price: $30 is ~14% above current price - these are out-of-the-money calls

- ⏰ Expiration: June 18, 2026 - captures earnings, BOTH PDUFA dates, and potential obesity pipeline updates

- 📊 Volume vs OI: 28K volume against 61K open interest (Vol/OI ratio of 0.46) - solid activity level

- 🔥 Z-Score: 16.25 (EXTREMELY UNUSUAL) - This level of activity on this contract is something you'd see only a few times a year

- 🏦 Order type: Buy-to-Open (BTO) on the ASK side - aggressive buyer initiating a new position, not closing an old one

What's really happening here: This trader is looking at Pfizer trading near 52-week lows around $25-26 with an RSI recently hitting 21.6 (deeply oversold) and seeing value. At $0.45 per contract, they're getting cheap exposure to a potential recovery through multiple binary catalysts. The June expiration is strategic - it captures Q4 earnings on February 3, the Padcev MIBC PDUFA on April 7, AND the vepdegestrant PDUFA on June 5. If even ONE of these catalysts pops, the stock could rally enough to push these calls into the money.

Think of it this way: $1.2M sounds like a lot, but for an institutional player, it's a relatively cheap lottery ticket on a $147B pharma giant with a 6.65% dividend yield and multiple near-term catalysts. The risk is defined - worst case, they lose $1.2M. Best case, a move to $32-33 would turn this into a 4-5x winner.

📈 Technical Setup / Chart Check-Up

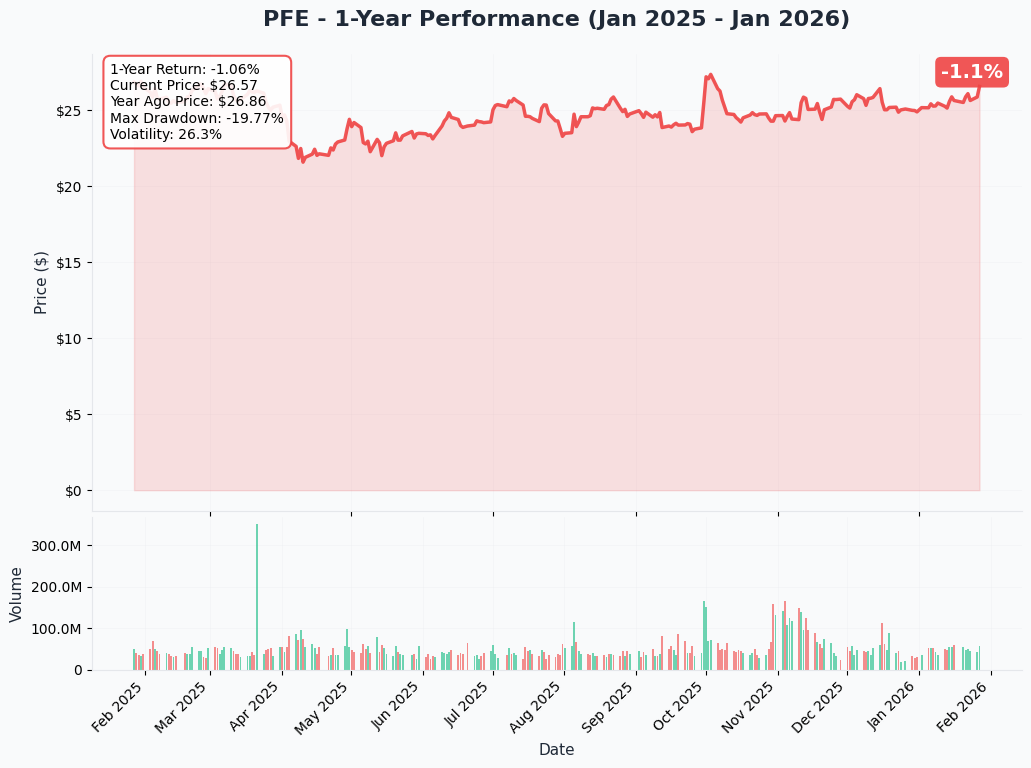

1-Year Performance Chart

PFE has been in a rough spot - currently trading at $26.40 near the bottom of its 52-week range of $20.92-$27.69. The stock got hit hard after disappointing 2026 guidance on December 16 (down 5%) and dropped further after the ViiV Healthcare divestiture news on January 20.

Key observations:

- 📉 Downtrend intact: Stock fell from ~$28 in November to $26.40 today - steady selling pressure

- 😰 Deeply oversold: RSI hit 21.6 recently - that's extreme territory that often precedes at least a short-term bounce

- 💰 Dividend floor: 6.65% yield provides some natural support as income investors step in

- 📊 Volume patterns: Selling has been orderly, not panicked - suggests positioning adjustments rather than capitulation

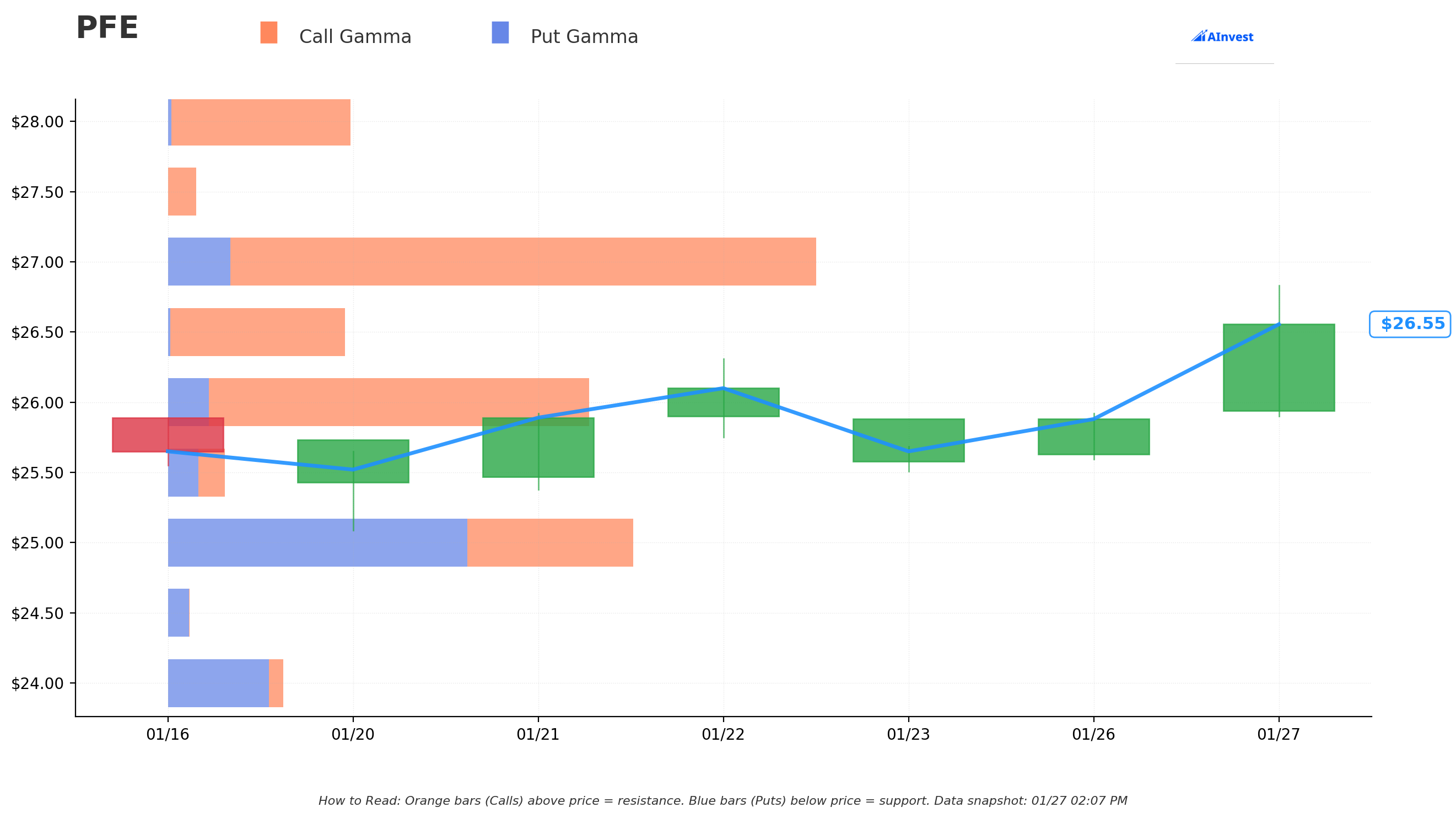

Gamma-Based Support & Resistance Analysis

Current Price: $26.56

The gamma exposure map shows where market makers have the biggest positions, which creates natural price magnets and barriers:

🔵 Support Levels (Where Buyers Step In):

- $26.50 - Immediate support with 34.0B total gamma (closest floor below current price)

- $26.00 - Strong secondary support with 80.2B total gamma (dealers will buy dips aggressively here)

- $25.50 - Moderate support with 8.8B gamma

- $25.00 - MAJOR structural floor with 86.8B gamma (highest total gamma level - this is the line in the sand)

- $24.00 - Deep support at 21.4B gamma

- $23.00 - Extended floor at 27.2B gamma (disaster scenario)

🟠 Resistance Levels (Where Sellers Show Up):

- $27.00 - STRONGEST resistance with 123.4B total gamma (100.0B net GEX - massive dealer selling pressure here!)

- $28.00 - Secondary ceiling at 34.6B gamma (5.4% above current)

- $29.00 - Upper resistance at 27.9B gamma

- $30.00 - Extended ceiling at 56.7B gamma (this is THE STRIKE of the $1.2M call trade! 13% above current)

What this means for traders: PFE is sandwiched between solid $26.00-$26.50 support and a massive $27.00 resistance wall. The $27 level has the largest single gamma concentration (123.4B total) which means market makers will be selling into any rally toward that level. Getting past $27 requires a genuine catalyst - which is exactly what the call buyer is betting on with earnings and PDUFA dates.

Notice this: The $30 strike where this trader bought calls has 56.7B in gamma with 52.1B net GEX. That level acts as a significant gamma wall. For the stock to reach $30, it would need sustained institutional buying through multiple resistance levels. The call buyer is essentially betting that pipeline catalysts will be strong enough to blow through all overhead resistance.

Net GEX Bias: Bullish (395.2B call gamma vs 166.3B put gamma) - Overall dealer positioning favors upside, which is encouraging for the bullish thesis.

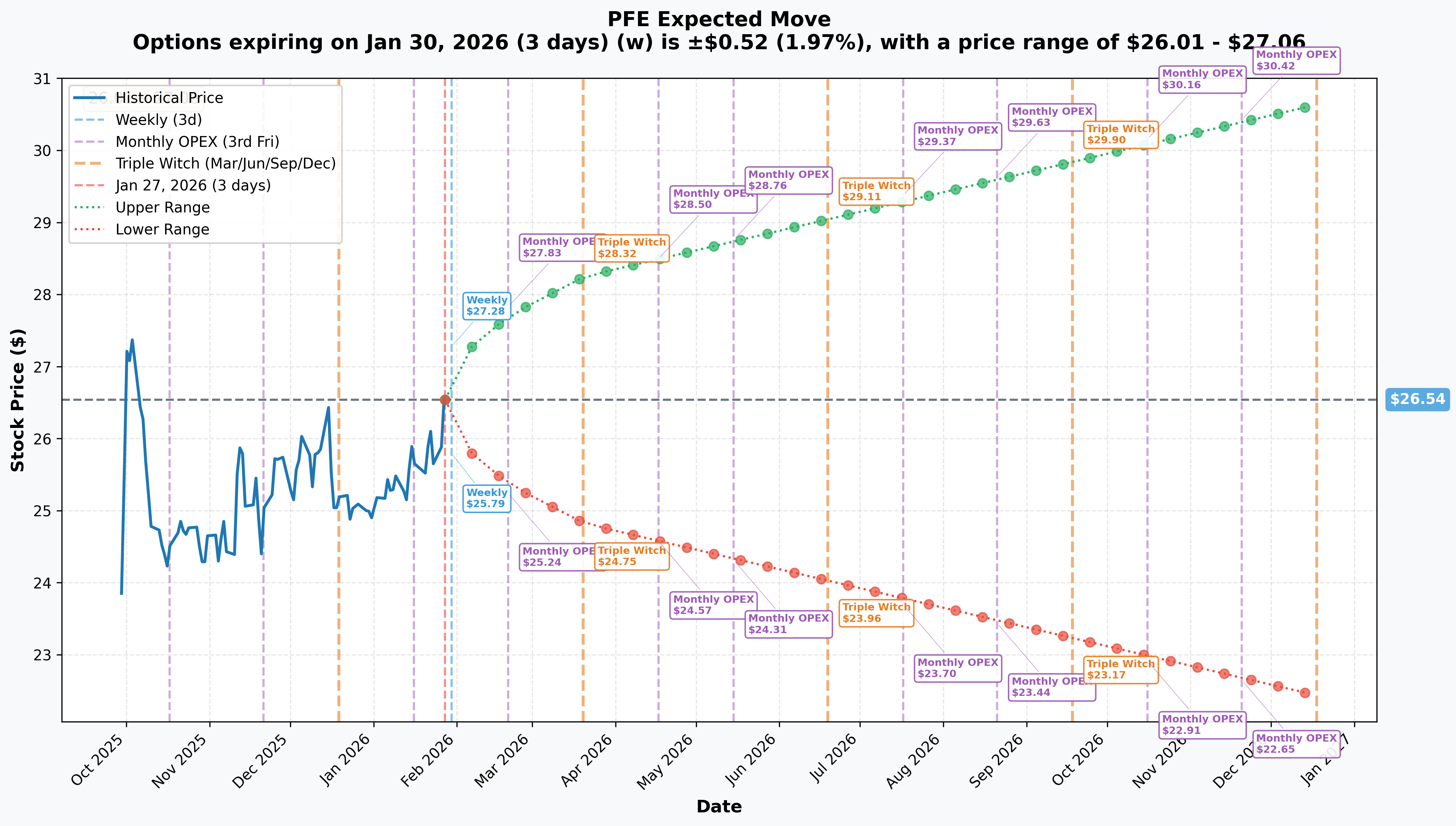

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 30 - 3 days): +/-$0.52 (+/-1.97%) --> Range: $26.01 - $27.06

- 📅 Monthly OPEX (Feb 20 - 24 days): +/-$1.17 (+/-4.42%) --> Range: $25.36 - $27.71

- 📅 Quarterly Triple Witch (Mar 20 - 52 days): +/-$1.71 (+/-6.45%) --> Range: $24.82 - $28.25

- 📅 Yearly LEAPS (Dec 18 - 325 days): +/-$4.10 (+/-15.46%) --> Range: $22.43 - $30.64

Translation for regular folks: The options market is pricing in about a 4.4% move by February OPEX - which includes the February 3 Q4 earnings. That's roughly a $1.17 swing either way. By the quarterly Triple Witch in March, the expected range widens to $24.82 - $28.25.

Key insight for this trade: The LEAPS implied move shows an upper range of $30.64 by year-end - meaning the market considers a move to $30 as within the realm of possibility but right at the edge. The call buyer's $30 strike by June 18 is ambitious but not crazy. The June Triple Witch implied range is $23.96 - $29.11, which means the $30 strike sits just outside the 1-standard-deviation expected move. This is a bet that catalysts push the stock beyond what the market currently expects.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 5 Months)

| Date | Event | Why It Matters |

|---|---|---|

| February 3, 2026 | Q4 2025 Earnings Release | Consensus EPS $0.57-$0.58. Pre-market release, 10 AM ET call. Any upside surprise could spark a relief rally from oversold levels. |

| Q1 2026 | ViiV Healthcare Exit Closing | ~$1.88B cash proceeds upon regulatory approval. Provides liquidity amid patent cliff transition. |

| April 7, 2026 | PDUFA: Padcev + Keytruda (MIBC) | Priority Review for cisplatin-ineligible bladder cancer. Strong Phase 3 data (60% reduction in recurrence risk). Approval looks likely. |

| June 5, 2026 | PDUFA: Vepdegestrant | First-ever PROTAC protein degrader - a novel mechanism for ESR1-mutant breast cancer. 43% reduction in progression/death in target population. |

| H1 2026 | Metsera Phase 3 Trials (MET-097i) | Multiple Phase 3 obesity trial initiations throughout 2026 (targeting 10 by year-end). GLP-1 receptor agonist entering the red-hot obesity market. |

| H1 2026 | Etrasimod (Velsipity) Crohn's Data | Phase 3 readout could expand Velsipity's commercial opportunity beyond ulcerative colitis. |

📜 Recent Catalysts (Already Happened)

- 📉 December 16, 2025: FY2026 guidance disappointed - revenue $59.5-$62.5B and EPS $2.80-$3.00, both below consensus. Stock fell 5%.

- 💰 January 20, 2026: Sold entire 11.7% ViiV Healthcare stake for $1.88B - provides cash but removes future HIV revenue stream.

- 🤝 January 20, 2026: Licensed Novavax Matrix-M adjuvant - $30M upfront, up to $500M in milestones for vaccine development.

- ✅ Q3 2025 Earnings (November 4): Beat EPS consensus by 34% ($0.87 vs $0.65 expected). Raised FY2025 EPS guidance.

- 🏥 October 2025: Padcev Phase 3 EV-303 success - 60% recurrence reduction, 50% death risk reduction in bladder cancer.

- 🏛️ October 2025: Trump administration MFN pricing deal - discounted drug prices in exchange for 3-year tariff grace period and $70B domestic manufacturing commitment.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through the June 18 expiration:

📈 Bull Case (20% probability)

Target: $30-$33

How we get there:

- ✅ Q4 earnings on February 3 beat expectations and management provides encouraging 2026 pipeline commentary

- 💊 Padcev MIBC approval on April 7 expands Padcev's addressable market significantly

- 🧬 Vepdegestrant approval on June 5 as first PROTAC generates excitement about novel oncology mechanism

- 🏋️ Metsera Phase 3 trial updates show promising early data, validating obesity strategy

- 📊 Multiple analyst upgrades from current consensus (only 8 of 25 analysts at Buy) as pipeline de-risks

- 💰 Stock re-rates from 8.8x to 10-11x forward P/E on improved sentiment

Call trade P&L at $30: Breakeven at $30.45. At $33, calls worth $3.00, profit = $2.55/contract x 26,728 = ~$68K per contract, total ~$6.8M (5.7x return).

Why only 20%: Requires ALL catalysts to land favorably AND market to re-rate the stock through heavy $27-$30 gamma resistance. The patent cliff concerns ($17B revenue at risk by 2030) and no expected revenue growth until 2029 are real headwinds that keep the multiple compressed.

🎯 Base Case (55% probability)

Target: $25.50-$28.50 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- 📊 Earnings are fine but not spectacular - in-line with consensus EPS of $0.57-$0.58

- 💊 Padcev approval expected and mostly priced in - modest positive reaction

- ⚖️ Vepdegestrant gets approved but narrow ESR1-mutant label limits commercial excitement

- 📈 Stock bounces from oversold levels toward $27-28, tests gamma resistance, consolidates

- 💤 Market digests patent cliff fears gradually; dividend yield provides income floor

- 🔄 Trading range bound between $25 gamma support and $27-28 resistance

Call trade P&L in base case: Stock ends $25.50-$28.50 by June 18 - calls expire worthless. Full $1.2M loss. This is the most likely outcome for this specific trade.

📉 Bear Case (25% probability)

Target: $22-$25

What could go wrong:

- 😰 Q4 earnings disappoint with continued COVID revenue declines and margin compression from MFN pricing

- ❌ Vepdegestrant gets a CRL or delay - overall ITT population missed statistical significance, creating regulatory uncertainty

- 💸 Eliquis EU patent expiry in H2 2026 accelerates patent cliff fears earlier than expected

- 📉 Broader pharma sector weakness from IRA drug pricing negotiations

- 🔨 Break below $25 gamma support (86.8B wall) triggers momentum selling to $23-$24

Call trade P&L: Calls expire worthless. Full $1.2M loss.

Critical support levels:

- 🛡️ $26.00-$26.50: Immediate gamma floor (80.2B + 34.0B gamma)

- 🛡️ $25.00: Major structural support (86.8B gamma - MUST HOLD)

- 🛡️ $24.00: Deep support (21.4B gamma)

- 🛡️ $23.00: Extended floor (27.2B gamma)

💡 Trading Ideas

🛡️ Conservative: Own the Stock for the Dividend

Play: Buy PFE shares at $26.40 and collect the 6.65% dividend while you wait for catalysts

Why this works:

- 💰 6.65% yield means you're getting PAID $1.72/year per share while waiting for pipeline catalysts

- 📉 Stock is deeply oversold (RSI 21.6) near 52-week lows - not the time to sell, historically

- 🛡️ Forward P/E of 8.8x provides valuation cushion - a lot of bad news already priced in

- 📊 Multiple catalysts in next 5 months could drive re-rating

- ⏰ Patient approach - collect dividends, wait for pipeline readouts

Position sizing: 3-5% of portfolio. Add on dips to $25 (major gamma support).

Risk level: Low-Moderate | Skill level: Beginner-friendly

⚖️ Balanced: Bull Call Spread Targeting $28-$30

Play: Buy the June $27 call, sell the June $30 call - cheaper way to play the bullish thesis with defined risk

Structure: Buy June $27 call ($1.20) / Sell June $30 call ($0.45) = ~$0.75 net debit per spread

Why this works:

- 💸 Much cheaper than buying the $30 calls outright ($75 per spread vs $45 for the naked call but with better probability)

- 🎯 Captures the most likely bullish outcome ($27-$30 range) rather than needing a home run to $30+

- 📊 Max profit $2.25 per spread if PFE reaches $30 by June (3x return on risk)

- 🛡️ Defined risk - can only lose the $0.75 debit

- ⏰ Benefits from ANY catalyst that pushes stock through $27 gamma resistance

Estimated P&L:

- 📈 Max profit: $2.25 per spread at $30+ (3x return)

- 📉 Max loss: $0.75 per spread below $27 (defined)

- 🎯 Breakeven: $27.75

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Copy the Whale - Buy June $30 Calls

Play: Buy PFE June $30 calls at $0.45 per contract, mirroring the institutional trade

Why this could work:

- 🎰 Cheap entry ($45 per contract) gives massive leverage to a $147B company with multiple catalysts

- 💊 Two PDUFA dates (April 7 Padcev, June 5 vepdegestrant) create binary upside events

- 📊 An institution just put $1.2M behind this exact thesis - they clearly see something

- 🏋️ Metsera obesity pipeline updates could be a wildcard catalyst if early Phase 3 data impresses

Why this could blow up (SERIOUS RISKS):

- ⚠️ 14% OTM: Stock needs to rally from $26.40 to $30.45 just to BREAK EVEN - that's a big ask

- 📉 Heavy gamma resistance at $27 and $30: Market makers will sell into rallies at these levels

- 💀 Time decay: At $0.45, these calls have minimal intrinsic value - pure time value that bleeds every day

- 📊 Base case = total loss: 55% probability the stock stays below $30 and calls expire worthless

- 🏔️ Patent cliff is structural: No revenue growth expected until 2029 - hard to see sustained re-rating

Position sizing: SMALL. Risk only what you can afford to lose completely. 1-2% of portfolio MAX.

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🏔️ Patent cliff is real and imminent: Pfizer faces ~$17B in annual revenue at risk by 2030. LOE impact starts at $1.5B in 2026, accelerating to $3B+ in 2027 and $6B+ in 2028. Eliquis EU patent expires H2 2026 with U.S. generics expected April 2028. Management acknowledged no revenue growth until 2029. This isn't a temporary headwind - it's a multi-year structural challenge.

-

📉 Below-consensus 2026 guidance already set a negative tone: Revenue guidance of $59.5-$62.5B and EPS of $2.80-$3.00 came in below Street expectations. COVID products declining ~$1.5B YoY, elevated R&D spending ($10.5-$11.5B), and higher tax rate (15% vs 11%) all compress earnings. The bar was already lowered.

-

💊 Vepdegestrant's narrow efficacy is a concern: While it showed a 43% PFS improvement in ESR1-mutant patients, the overall ITT population did NOT meet statistical significance. A narrow label could significantly limit the commercial opportunity vs. broader breast cancer therapies.

-

🏋️ Obesity pipeline is years from revenue: Metsera's MET-097i is just entering Phase 3 with potential approval not until 2028+. Pfizer is a LATE entrant competing against Novo Nordisk and Eli Lilly who already have blockbuster products on market. Plus, Pfizer's prior oral GLP-1 (danuglipron) was discontinued after liver injury concerns.

-

💸 Drug pricing pressure from multiple angles: The Trump MFN pricing deal introduces margin compression. Eliquis likely subject to IRA negotiated pricing in 2026. Despite deals, Pfizer raised list prices on 72-80 products in January 2026, creating political risk.

-

📊 $30 strike is 14% OTM with heavy gamma resistance: The gamma map shows massive resistance at $27 (123.4B gamma) and $30 (56.7B gamma). Breaking through multiple resistance walls requires sustained buying pressure that only comes from truly transformative catalysts.

-

💼 Analyst sentiment is lukewarm: Only 8 of 25 analysts rate PFE as Buy. Average price target is $27.18-$28.26 - well below the $30 strike. UBS initiated with Neutral at $25. The Street doesn't share this trader's optimism.

-

🏦 Zero insider buying signal: No insider transactions in the past 90 days. If management believed in a recovery to $30, you'd expect to see some buying at these levels.

🎯 The Bottom Line

Real talk: Someone just put $1.2M on the line betting Pfizer rallies 14% by June. It's a bold call on a beaten-down pharma giant with a loaded catalyst calendar. The thesis makes sense on paper - deeply oversold stock, 6.65% dividend yield, two PDUFA dates, and forward P/E at 8.8x. But $30 is a stretch when the average analyst target is $27-$28 and the company itself says no revenue growth until 2029.

What this trade tells us:

- 🎯 Someone sees value in PFE at these levels - cheap calls as a leveraged bet on pipeline execution

- 💊 The June expiration is no accident - it captures Q4 earnings (Feb 3), Padcev PDUFA (Apr 7), AND vepdegestrant PDUFA (Jun 5)

- 📊 At $0.45/contract, this is a defined-risk bet with asymmetric upside if things break right

- ⚠️ But the probability is against them - base case (55%) is these expire worthless

If you like the Pfizer story:

- ✅ Consider owning the STOCK at $26.40 with the 6.65% dividend as your safety net

- 📊 Look at the bull call spread ($27/$30) for a more balanced risk/reward than naked calls

- ⏰ February 3 earnings is the FIRST real test - watch for revenue beat and pipeline commentary

- 🎯 $27 is the first gamma resistance to clear - if stock can't get past there, $30 calls are in trouble

If you're on the sidelines:

- 👀 Watch February 3 earnings reaction closely - a beat AND rally through $27 would validate the bullish thesis

- 📊 $25 is the floor to watch (86.8B gamma support) - a break below that gets ugly fast

- 💊 April 7 Padcev PDUFA is the highest-probability positive catalyst - the Phase 3 data was strong

If you're bearish:

- 📉 Patent cliff headwinds are structural and multi-year - this isn't going away

- 🎯 $25 is the critical support level - break below opens path to $23-$24

- ⚠️ BUT be careful shorting a stock with 6.65% dividend yield at 52-week lows - short squeeze + dividend risk

Mark your calendar - Key dates:

- 📅 February 3 - Q4 2025 earnings (7 DAYS!)

- 📅 February 20 - Monthly OPEX (+/-4.4% implied move)

- 📅 March 20 - Quarterly Triple Witch (+/-6.5% implied move)

- 📅 April 7 - Padcev MIBC PDUFA (Priority Review)

- 📅 June 5 - Vepdegestrant PDUFA (first PROTAC approval?)

- 📅 June 18 - This $1.2M call trade expires

Final verdict: This is a cheap, speculative bet on a pharma turnaround story. The catalysts are real, the stock is oversold, and the risk is defined at $1.2M. But reaching $30 requires breaking through heavy gamma resistance and overcoming legitimate structural concerns about the patent cliff. For most retail traders, owning the stock for the dividend while waiting for catalysts is the smarter play. Let the institutional player take the OTM call risk - you collect 6.65% while you wait.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 16.25 reflects this specific trade's unusual size relative to recent PFE history - it does not imply the trade will be profitable. OTM calls have a high probability of expiring worthless. Always do your own research and consider consulting a licensed financial advisor before trading.

About Pfizer Inc.: Pfizer is one of the world's largest pharmaceutical companies with annual sales of roughly $60 billion, focusing on prescription drugs and vaccines across oncology, cardiovascular, inflammation, and infectious disease therapeutics, with a market cap of $147.2 billion in the Pharmaceutical Preparations industry.