🚀 PLTR Massive $18.5M Bullish Bet - Institutions Loading Up Into Nasdaq-100 Inclusion! 📈

📅 December 2, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $18.5 MILLION on PLTR calls this morning! Two monster trades hit the tape at 10:46 AM - a $1.5M bet on $200 calls (Dec 19) and a whopping $17M position in $180 calls (Jan 16). With PLTR trading at $173 and Nasdaq-100 inclusion happening December 23rd (triggering $7B in passive buying), smart money is positioning for a major breakout. Translation: Institutions are betting big that PLTR explodes higher into year-end!

📊 Company Overview

Palantir Technologies (PLTR) is an analytical software powerhouse dominating the AI platform space for government and commercial clients:

- Market Cap: $399.2 Billion (one of the largest software companies globally)

- Industry: Prepackaged Software

- Current Price: $173.11 (up 343% YTD!)

- Primary Business: AI-powered data analytics through two flagship platforms:

- Gotham: Government/defense clients (CIA, FBI, NSA, DoD)

- Foundry: Commercial enterprises (55% YoY growth in US commercial!)

- AIP (Artificial Intelligence Platform): Revolutionary bootcamp-driven AI deployment

Founded in 2003 by Peter Thiel and Alex Karp, Palantir went public in 2020 and has since become THE dominant player in operational AI - turning raw data into actionable intelligence for the world's most critical organizations.

💰 The Option Flow Breakdown

The Tape (December 2, 2025 @ 10:46:14):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:46:14 | PLTR | ASK | BUY | CALL $200 | 2025-12-19 | $1.5M | $200 | 19K | 33K | 17,257 | $173.11 | $0.89 | PLTR 200C 12/19 |

| 10:46:14 | PLTR | ASK | BUY | CALL $180 | 2026-01-16 | $17M | $180 | 18K | 12K | 17,257 | $173.11 | $9.75 | PLTR 180C 01/16 |

🤓 What This Actually Means

This is aggressive bullish positioning ahead of a MASSIVE catalyst! Here's what went down:

Trade #1: The December Triple Witch Lottery Ticket 🎰

- 💸 Premium paid: $1.5M ($0.89 per contract × 17,257 contracts)

- 🎯 Strike: $200 calls - 15.5% above current price

- ⏰ Expiration: December 19 (17 days!) - expires RIGHT as Nasdaq-100 rebalancing completes

- 📊 Size: 17,257 contracts represents 1.73 million shares worth ~$300M

- 🎪 The bet: PLTR needs to hit $201+ by Dec 19 to profit (16% rally required!)

- 🔥 Unusual Score: EXTREMELY UNUSUAL (Z-score 6.62, 576% vol/OI ratio)

Trade #2: The Mega Position 🐋

- 💰 Premium paid: $17M ($9.75 per contract × 17,257 contracts)

- 🎯 Strike: $180 calls - just 4% above current price

- ⏰ Expiration: January 16 (45 days) - captures full Nasdaq buying wave + Q1 earnings setup

- 📈 Size: MASSIVE - same 17,257 size as the Dec trade (likely same player!)

- 💪 Breakeven: $189.75 (10% rally needed)

- 🔥 Unusual Score: OFF THE CHARTS (Z-score 27.59, 1.5x vol/OI ratio)

What's really happening here: This trader is making a two-pronged assault on PLTR upside. The December $200 calls are a HIGH RISK/HIGH REWARD bet that Nasdaq-100 passive buying ($7B expected!) creates explosive momentum through $200 by triple witch expiration. Meanwhile, the $180 January calls are the core position - paying $9.75 for calls only 4% out of the money with 45 days to work.

Why the EXACT SAME size (17,257)? This screams institutional playbook - they're structuring a defined allocation across two time horizons. The Dec trade is the "moonshot" capturing peak Nasdaq rebalancing, while the Jan trade is the "base case" capturing sustained buying pressure and potential Q1 earnings strength.

Combined bet size: $18.5M represents conviction that PLTR trades SIGNIFICANTLY higher (likely $190-210 range) over the next 45 days. At current premium levels, they're not paying up for crazy implied vol - this is SMART positioning, not panic buying.

📈 Technical Setup / Chart Check-Up

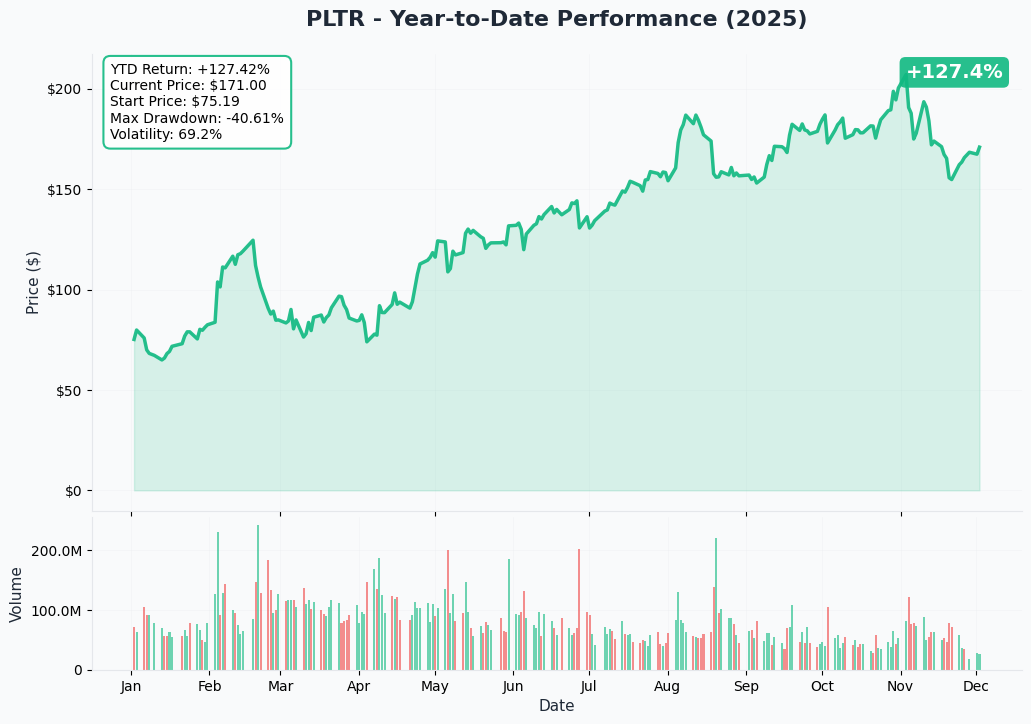

YTD Performance Chart

PLTR is in an absolute MONSTER rally - up +283% in 2024 alone, continuing explosive momentum into 2025! The chart tells the story of a company that's gone from "niche defense contractor" to "AI mega-cap" in record time.

Key observations:

- 🚀 Parabolic acceleration: Vertical move from $120 to $180+ since September on index inclusion announcements

- 📈 S&P 500 inclusion pop: Stock surged 14% on September 9 when S&P announced addition

- 🎢 Nasdaq-100 catalyst pending: December 13 announcement drove another leg higher toward $170s

- 📊 Volume explosion: Institutional accumulation ramping as passive funds prepare to buy

- ⚠️ Never looked back: Zero meaningful pullbacks in Q4 - pure buying pressure

- 💪 Momentum sustained: Even at $170+, bulls keep pushing - this is rotation INTO megacap tech

The technical picture is TEXTBOOK bullish momentum - higher highs, higher lows, sustained volume, no resistance overhead (all-time highs territory). For bulls, this is "buy and hold on tight." For bears, this is "don't fight the tape or you'll get steamrolled."

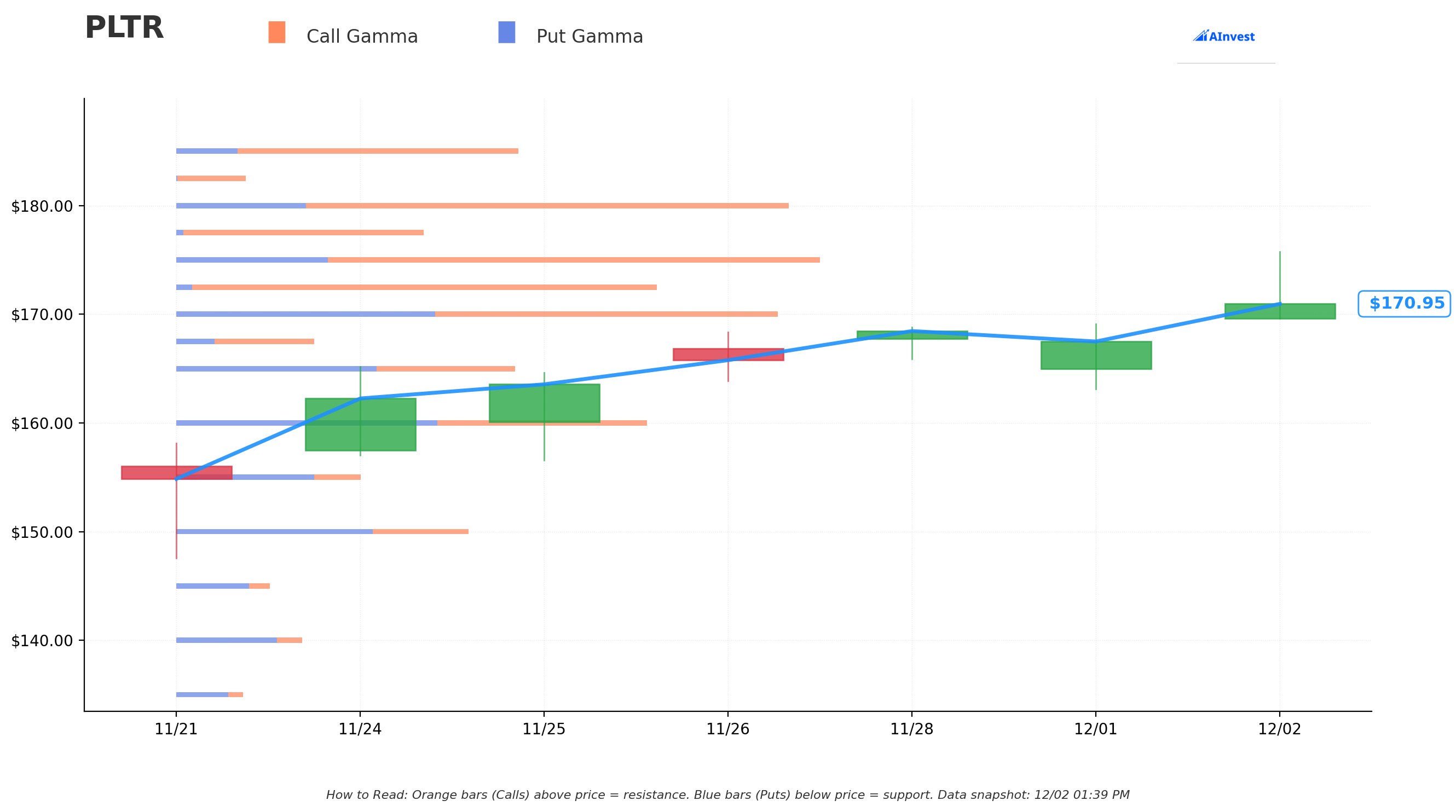

Gamma-Based Support & Resistance Analysis

Current Price: $170.97

The gamma exposure map reveals critical price magnets where market makers have HUGE positions that will influence near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $170 - STRONGEST nearby support with 31.9B total gamma (line in the sand!)

- $165 - Secondary floor at 17.9B gamma (dealers will buy any dip here)

- $160 - Major structural support at 24.9B gamma (3.5% below current)

- $150 - Deep support zone with 15.5B gamma (extended downside floor)

🟠 Resistance Levels (Call Gamma Above Price):

- $172.50 - Immediate ceiling with 25.4B gamma (just $1.50 overhead!)

- $175 - Secondary resistance at 34.0B gamma (STRONGEST RESISTANCE - dealers will sell rallies)

- $180 - Major ceiling zone with 32.3B gamma (exactly where the big call trade is struck! 5.3% above)

- $185 - Extended resistance at 18.0B gamma

- $190 - Upper ceiling with 14.7B gamma

- $200 - MASSIVE target level with 18.5B gamma (exactly where the Dec call strike is!)

What this means for traders: PLTR is trading in a TIGHT consolidation between $170 support (31.9B gamma wall) and $175 resistance (34.0B - the single largest gamma level!). This setup is COILED - whichever direction breaks will likely see explosive follow-through.

Notice the pattern? The call buyer struck EXACTLY at $180 (32.3B gamma) and $200 (18.5B gamma) - both MAJOR gamma levels where options market makers have enormous exposure. Smart positioning targeting natural price magnets.

If PLTR breaks above $175: The next stops are $180 (first call strike target), then $185, then $190. Massive call gamma overhead creates natural resistance, but Nasdaq buying pressure could overwhelm dealer hedging.

If PLTR breaks below $170: Watch for quick flush to $165 support, then potentially $160. However, with $7B Nasdaq buying incoming, downside seems limited.

Net GEX Bias: BULLISH (223.8B call gamma vs 119.5B put gamma = 1.87:1 ratio) - Market positioning is HEAVILY skewed bullish, supporting upside breakout thesis.

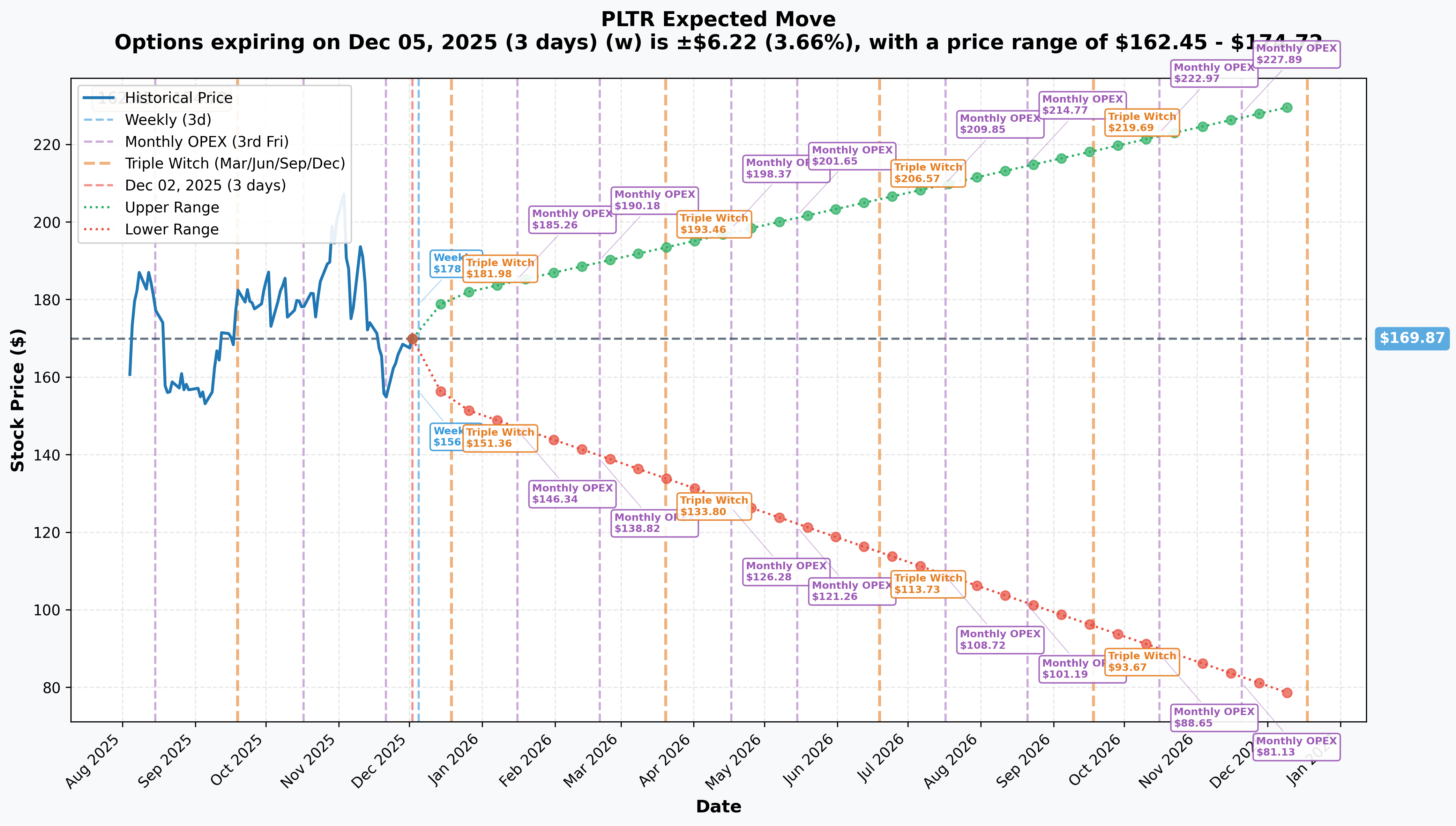

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 3 days): ±$6.22 (±3.66%) → Range: $162.45 - $174.72

- 📅 Monthly OPEX (Dec 19 - 17 days - FIRST CALL STRIKE!): ±$13.11 (±7.72%) → Range: $152.82 - $181.02

- 📅 Triple Witch (Dec 19 - same as monthly): ±$13.11 (±7.72%) → Range: $152.82 - $181.02

- 📅 January OPEX (Jan 16 - 45 days - SECOND CALL STRIKE!): ±$18.85 (±11.1%) → Range: $146.34 - $185.26

- 📅 Yearly LEAPS (Dec 18 2026 - 381 days): ±$67.66 (±39.8%) → Range: $76.74 - $230.76

Translation for regular folks: Options traders are pricing in a 3.7% move ($6) by this Friday, but a MUCH LARGER 7.7% move ($13) through December 19 which captures the Nasdaq-100 rebalancing implementation on December 23rd. The market expects some SERIOUS action around that catalyst!

KEY INSIGHT for these trades:

- The December 19 $200 calls need PLTR to hit $181+ (upper end of implied range) just to breakeven at $200.89. This is betting on a move BEYOND what options market expects - classic "convexity bet"

- The January 16 $180 calls are positioned PERFECTLY within the $146-$185 implied range, with $180 sitting right at the expected upper boundary. Much more reasonable risk/reward

The sharp increase in implied volatility from 3.7% (weekly) to 7.7% (Dec 19) reflects massive Nasdaq inclusion uncertainty. Smart money is betting the actual move EXCEEDS the 7.7% implied - they see $190+ as realistic outcome.

🎪 Catalysts

🔥 Immediate Catalysts (Already Happened)

Q3 2024 Earnings BEAT - November 4, 2024 📊

PLTR crushed Q3 earnings, triggering a 20% single-day pop:

- 💰 Revenue: $726M (beat $701M estimate) - up 30% YoY

- 📈 US Commercial Revenue: Up 54% YoY (EXPLOSIVE growth!)

- 🏢 Customer Count: Up 39% YoY, 6% QoQ

- 💵 Adjusted EPS: $0.10 (beat by $0.01)

- 🎯 Adjusted Operating Margin: 38% (eighth consecutive quarter of expansion)

- 🔥 Rule of 40 Score: 68 (among best in enterprise software!)

Why this matters NOW: Momentum from this beat carried PLTR from $145 to $170+ into year-end. The growth trajectory validates the AI platform story.

Q4 2024 Earnings DEMOLITION - February 3, 2025 🚀

PLTR obliterated Q4 expectations, driving another massive rally:

- 📊 Revenue: Up 36% YoY (vs 30% in Q3 - accelerating!)

- 🇺🇸 US Revenue: Up 52% YoY

- 💼 US Commercial Revenue: $214M, up 64% YoY and 20% QoQ

- 🏛️ US Government Revenue: $343M, up 45% YoY

- 💵 Adjusted EPS: $0.14 (beat estimates by 27%!)

- 🎯 Q1 2025 Guidance: $858-862M vs $799M consensus (+7.4% beat)

- 🚀 FY 2025 Guidance: $3.74-3.76B vs $3.52B consensus (+6-7% beat)

Why this is HUGE: The guidance raises ALONE justify higher valuations. PLTR isn't slowing down - it's ACCELERATING.

S&P 500 Inclusion - September 23, 2024 📈

PLTR joined the S&P 500 on September 23, 2024:

- ✅ Announcement on September 6 triggered 14% surge

- 💰 Replaced American Airlines in the index

- 📊 Brought billions in passive fund buying

- 🎯 Historical precedent: New S&P additions see 10-13% returns in first 12 months

Major Government Contracts - Q4 2024 🏛️

PLTR secured MASSIVE government wins validating their defense/intel dominance:

- Army Vantage Program (December 2024): $619M four-year contract for AI-enabled capabilities

- Navy Contract (November 2024): Nearly $1B software contract

- Maven Smart System (September 2024): $100M five-year contract expanding across all military branches

- Anduril Partnership (December 2024): New consortium merging platforms for national security

Why this matters: Government contracts account for 55% of revenue - these wins secure multi-year revenue visibility.

🚀 Near-Term Catalysts (Next 30 Days - THE BIG ONE!)

Nasdaq-100 Inclusion - December 23, 2024 💥 (THIS IS THE CATALYST!)

PLTR will be added to the Nasdaq-100 index on December 23, 2024:

- 📅 Announcement: December 13, 2024 (already happened - stock jumped!)

- ⏰ Implementation: December 23, 2024 (21 DAYS AWAY!)

- 🤝 Added Alongside: MicroStrategy and Axon Enterprise

- 💰 Estimated Buying Pressure: $6.96 BILLION worth of shares (~98M shares!)

- 📈 Market Cap at Inclusion: ~$161.5B (now $399B!)

- 🎯 YTD Performance Through Inclusion: +343%

Why this is THE catalyst for these calls:

The December 23rd implementation means passive funds tracking QQQ and Nasdaq-100 (TRILLIONS in AUM) MUST buy PLTR shares to match index weights. This creates MECHANICAL buying pressure that has NOTHING to do with fundamentals - funds literally HAVE to buy regardless of price.

Historical pattern alert: New Nasdaq-100 additions typically underperform in first 21 trading days post-inclusion, BUT the run-up INTO implementation can be explosive as speculators frontrun the passive flows.

Timeline breakdown:

- ✅ Dec 13: Announcement made (stock jumped to $170s)

- 📅 Dec 13-23: Speculators position ahead of passive buying (THIS IS WHERE WE ARE NOW!)

- 💥 Dec 23: Actual rebalancing - $7B hits the tape

- 📊 Dec 23-Jan 16: Post-inclusion dynamics play out (second call expiration window)

The call buyer's thesis: PLTR continues rallying through Dec 19 on Nasdaq anticipation (targeting $200 with Dec calls), then sustains gains through January on actual buying pressure and momentum (Jan $180 calls capture this).

📅 Upcoming Catalysts (Q1 2025)

Q1 2025 Earnings - Expected Early May 2025 📊

PLTR's next earnings report will be CRITICAL:

- 🎯 Guided Revenue: $858-862M (vs $799M consensus - already guided +7.4% beat!)

- 📈 Expected Metrics:

- US Commercial Revenue growth >68% YoY (guidance implied)

- Customer count additions and net retention rate

- AIP bootcamp conversion metrics (running ~5 bootcamps per day in 2024)

- Government contract backlog and new wins

- Q2 guidance (critical for sustained growth narrative)

Why this matters for Jan calls: The January 16 expiration expires BEFORE Q1 earnings, so the call buyer is NOT betting on earnings beat. They're betting on Nasdaq buying + setup INTO earnings creating momentum to $180-190 range.

AIP Platform Acceleration 🤖

PLTR's Artificial Intelligence Platform (AIP) is seeing EXPLOSIVE adoption:

- 🏭 Conducting ~5 bootcamps per day in 2024 (vs 500 total in 2023!)

- 📊 Projected 3,000 bootcamps in 2024 (vs 92 in 2022)

- 💰 80 deals closed in Q3 including 12 worth $10M+

- 📈 US Commercial TCV deals jumped 134% to $803M

- 🎯 Net Retention Rate: 120% in Q4 (up from 107% trough)

The bootcamp model is a GAME CHANGER - hands-on 5-day proof-of-value demonstrations converting enterprises at unprecedented rates.

FY 2025 Full Year Trajectory 🚀

PLTR's full-year guidance implies sustained acceleration:

- 💰 Revenue Guidance: $3.74-3.76B (+31% YoY)

- 🇺🇸 US Commercial Revenue: Expected to exceed $687M (+50% minimum)

- 💵 Adjusted Free Cash Flow: Excess of $1 billion

- 📊 Margin Expansion: Continuing trend toward 40%+ adjusted operating margins

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, Nasdaq-100 catalyst, and earnings momentum, here are the scenarios through January 16th expiration:

📈 Bull Case (40% probability)

Target: $190-$210

How we get there:

- 💥 Nasdaq-100 buying pressure EXCEEDS $7B estimates as active managers also chase momentum

- 🚀 PLTR becomes "consensus crowded long" as retail/momentum traders pile in

- 📊 Breaks through $175 gamma resistance (34.0B), triggering cascade to $180, then $185, then $190

- 🤖 Additional major AIP bootcamp deal announcements (Fortune 500 wins)

- 🏛️ New government contract wins announced (DoD, intelligence agencies)

- 🌊 Short squeeze dynamics as bears capitulate on index buying reality

- 📈 Technical breakout above $180 triggers systematic buying from quant/CTA funds

- 🎯 December $200 calls go ITM by triple witch expiration

- 💪 January $180 calls finish deep ITM at $190-200

Key metrics needed:

- Sustained daily volume >50M shares (vs ~30M recent average)

- Break above $175 with conviction (close above, not just intraday spike)

- Nasdaq-100 weighting announced at upper end of estimates

- No negative news on valuation concerns, insider selling, or competitive threats

Probability assessment: 40% because Nasdaq buying is REAL and MECHANICAL (not discretionary). The $7B has to flow in - question is timing and price impact. Gamma resistance at $175-$180 creates headwinds, but passive flows can overwhelm market maker hedging. Historical precedent shows new index additions often see 5-10% pops into implementation.

Call P&L in Bull Case:

- Dec $200 calls at $210: Profit = $9.11/share × 17,257 = $157M gain (10,457% ROI on $1.5M!)

- Jan $180 calls at $200: Profit = $10.25/share × 17,257 = $177M gain (1,041% ROI on $17M!)

- Combined: $334M profit on $18.5M invested = 18x return!

🎯 Base Case (45% probability)

Target: $175-$190 range (CHOPPY RALLY)

Most likely scenario:

- ✅ Nasdaq-100 buying occurs as expected (~$7B over Dec 23-Jan timeframe)

- 📊 Stock grinds higher from $170 to $180-185 range but encounters resistance

- 🎢 Volatility around implementation date (Dec 23) - gap up then consolidation

- 📈 Breaks $175 resistance but struggles at $180 gamma ceiling (32.3B)

- 💰 Some profit-taking by early bulls who bought $120-150 range

- ⚖️ Valuation concerns prevent parabolic blowoff (430x P/E is RICH)

- 🐳 Insider selling headlines create periodic selling pressure

- 📊 Trading within $175-$190 band through January expiration

- 🤔 Market digests 343% YTD gain, waits for Q1 earnings proof

- 💤 Implied volatility crush post-Dec 23 (IV drops from 7.7% to 5-6% range)

This is the "slow grind higher" scenario: Stock benefits from Nasdaq buying but doesn't explode vertically. Reaches $180-185 by mid-January, satisfying the $180 call buyers but leaving the $200 calls worthless.

Why 45% probability: This balances the bullish Nasdaq catalyst against stretched valuation (430x P/E!), massive YTD gains (hard to sustain vertical momentum), and historical pattern of index additions consolidating post-implementation. Fundamentals are strong but price is ahead of fundamentals.

Call P&L in Base Case:

- Dec $200 calls at $185: Expire worthless = -$1.5M loss (100% loss)

- Jan $180 calls at $185: Profit = $0.25/share × 17,257 = $4.3M gain (25% ROI - minimal)

- Combined: $2.8M gain on $18.5M invested (15% return - underwhelming for the risk)

📉 Bear Case (15% probability)

Target: $150-$170 (SELL THE NEWS)

What could go wrong:

- 😰 Classic "sell the news" dynamic - Nasdaq inclusion ALREADY priced in from Dec 13 announcement

- 🚨 Historical pattern plays out: Additions underperform in 21 days post-inclusion

- 💸 Valuation concerns finally matter - 430x P/E called out by analysts as "most overvalued company ever"

- 📉 Insider selling accelerates - CEO Karp's $2B in sales and Peter Thiel's $1.5B spook retail

- 🇨🇳 Geopolitical tensions or export restrictions limit international growth

- 🤖 Competitor announcements (Databricks, Snowflake, Microsoft) threaten market share

- 💰 Broader tech selloff drags high-multiple stocks lower

- 📊 Break below $170 gamma support triggers cascade to $165, then $160

- 🔨 Profit-taking overwhelms passive buying as early investors cash out

Critical support levels:

- 🛡️ $170: Major gamma floor (31.9B) - MUST HOLD or momentum shifts

- 🛡️ $165: Secondary support (17.9B gamma)

- 🛡️ $160: Deep support (24.9B gamma) - disaster scenario

Probability assessment: Only 15% because it requires Nasdaq buying pressure to be FULLY offset by selling, which seems unlikely given the mechanical nature of index flows. However, valuation is EXTREME and insider selling is REAL. The "sell the news" pattern is well-documented for index additions.

Call P&L in Bear Case:

- Dec $200 calls at $165: Expire worthless = -$1.5M loss (100% loss)

- Jan $180 calls at $165: Expire worthless = -$17M loss (100% loss)

- Combined: -$18.5M loss (100% wipeout!)

💡 Trading Ideas

🛡️ Conservative: Wait for Post-Nasdaq Implementation Pullback

Play: Stay on sidelines until AFTER December 23rd Nasdaq implementation settles

Why this works:

- ⏰ Nasdaq buying creates binary event risk with unpredictable short-term price action

- 📊 Historical pattern: New additions often pull back 5-10% in 21 days POST-implementation

- 💸 Valuation at 430x P/E offers zero margin of safety at current $170 levels

- 🎯 Better entry likely post-Dec 23 after passive flows complete and volatility settles

- 📉 Even if stock goes higher short-term, patient capital can enter on inevitable consolidation

- 🤔 The $18.5M institutional bet signals FOMO, not careful analysis - why chase?

Action plan:

- 👀 Watch December 23rd rebalancing action closely - track volume and price behavior

- 🎯 Look for pullback to $160-165 gamma support (6-9% correction) for stock entry with margin of safety

- ✅ Need to see Nasdaq buying COMPLETE before committing capital (avoid getting front-run)

- 📊 Monitor post-implementation flow data - did funds buy more or less than expected?

- ⏰ Revisit late January for Q1 earnings setup with cleaner technical picture

Expected outcome: Avoid potential -10-15% drawdown if "sell the news" plays out. Get better entry on consolidation. Maintain optionality for Q1 catalyst.

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: Bull Put Spread - Play the Support Levels

Play: After Dec 23 implementation, sell bull put spread targeting gamma support

Structure: Sell $165 puts, Buy $160 puts (January 16 expiration - SAME as the call trade)

Why this works:

- 📊 Defined risk spread ($5 wide = $500 max risk per spread)

- 🎯 Targets major gamma support zone at $160-$165 (24.9B and 17.9B gamma)

- 💰 Collect premium betting PLTR stays above $165 through Jan 16

- 🛡️ Thesis: Nasdaq buying + strong fundamentals prevent sustained breakdown below support

- ⏰ 45 days to expiration gives time for Nasdaq flows to provide floor

- 📈 Even in bear case, $160 support likely holds (10% below current price)

Estimated P&L (adjust after seeing post-Dec 23 IV):

- 💰 Collect ~$1.50-2.00 credit per spread

- 📈 Max profit: $150-200 if PLTR above $165 at January expiration (keep full credit)

- 📉 Max loss: $300-350 if PLTR below $160 (defined and limited)

- 🎯 Breakeven: ~$163-163.50

- 📊 Risk/Reward: ~1.5:1 to 2:1 (favorable for defined-risk bullish play)

Entry timing:

- ⏰ Enter after Dec 23 once Nasdaq buying complete and IV stabilizes

- 🎯 Only enter if stock trading $170+ (gives cushion to support)

- ❌ Skip if stock already below $167 (too close to short strike)

Position sizing: Risk only 3-5% of portfolio (this is defined-risk premium collection)

Risk level: Moderate (defined risk, mildly bullish) | Skill level: Intermediate

🚀 Aggressive: Copy The Whale - Buy Jan $180 Calls (SPECULATIVE!)

Play: Buy the SAME January $180 calls this institutional player purchased

Structure: Buy $180 calls (January 16 expiration)

Why this could work:

- 🐋 "Following smart money" - someone with $18.5M sees value here

- 💥 Nasdaq-100 buying is REAL and MECHANICAL ($7B has to flow in)

- 📊 $180 strike only 4% out of the money - not crazy lotto ticket

- 🎯 Implied move upper range ($185) suggests options market sees $180 as achievable

- ⏰ 45 days to expiration captures full Nasdaq buying wave + potential Q1 setup

- 📈 Gamma levels show $180 as natural price magnet (32.3B gamma resistance)

- 🎢 High implied vol (7.7% for Dec 19) means big moves expected

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Calls cost ~$9.75 ($975 per contract)

- 🤯 Valuation insanity: 430x P/E is STRETCHED - no room for error

- ⏰ Time decay: Theta burns ~$25-30 per contract per day

- 😱 IV crush risk: After Dec 23, IV could collapse 30-40%, hurting option value even if stock flat

- 📊 One-way risk: Stock could easily consolidate $165-175 and calls expire worthless

- ⚠️ Insider selling: Karp and Thiel dumping $4B in stock sends bad signal

- 💀 Historical pattern: Index additions often disappoint post-implementation

Estimated P&L:

- 💰 Cost: ~$9.75 per call ($975 per contract)

- 📈 Profit scenario: Stock at $190 by Jan 16 = $5.25 profit (54% ROI)

- 🚀 Home run: Stock at $200 by Jan 16 = $10.25 profit (105% ROI)

- 📉 Loss scenario: Stock at $175 by Jan 16 = -$4.75 loss (49% loss)

- 💀 Total loss: Stock below $180 by Jan 16 = -$9.75 loss (100% wipeout)

Breakeven point: $189.75 (10% rally from current $173)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand options pricing and can monitor position daily

- ✅ Can afford to lose ENTIRE premium (real 100% loss possibility!)

- ✅ Accept that even if directionally correct, timing and IV crush can cause losses

- ✅ Plan exit strategy BEFORE entering (don't hold to expiration hoping for miracle)

- ⏰ Consider taking profits at 50-100% gain rather than holding for max profit

- 📊 Size position at 2-5% of portfolio MAX (this is speculation, not investment)

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35-40% (need 10% rally in 45 days during volatile period)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💰 Extreme valuation offers zero cushion: Trading at 430x P/E and 153x forward earnings (vs sector average 31x) near all-time highs after 343% YTD gain. Stock is priced for ABSOLUTE PERFECTION. Requires 1,500% revenue growth over 25 years to justify current price (50%+ annual growth through 2035). Any execution stumble could trigger 50-70% multiple compression. Base case intrinsic value: $18.51 per share implies 89% overvaluation. This is nosebleed territory.

-

🐳 Massive insider selling signals peak: Insiders dumped $4B+ in stock over 2024 - CEO Karp sold $2B, Peter Thiel sold $1.5B (33% of holdings). When founders are DUMPING at these levels while making bullish public statements, that's a RED FLAG. Karp plans to sell up to $1B more in 2025. Classic peak valuation behavior.

-

📉 Historical pattern: Index additions often disappoint: New additions typically underperform in first 21 trading days post-inclusion. The "buy the rumor, sell the news" dynamic is REAL. Speculators who frontran Nasdaq buying will likely take profits Dec 23-Jan timeframe. Even S&P 500 inclusion (Sept 23) was followed by consolidation despite initial pop.

-

🤖 Competition intensifying from well-funded rivals: Databricks raised $10B at $62B valuation (December 2024) and added $5.25B debt financing for aggressive expansion. Microsoft's unlimited capital for Azure AI, Snowflake's data platform dominance, and open-source alternatives all threaten PLTR's "premium platform" positioning. Market share battle heating up with Databricks at $3B revenue run-rate vs PLTR's $3.8B.

-

🚨 Government concentration creates policy risk: 55% of revenue from government contracts makes PLTR vulnerable to budget cuts, administration changes, or AI ethics concerns. One major contract loss or renewal failure could crater the stock 20-30%. Dependence on CIA, NSA, DoD creates single-customer concentration within government segment.

-

💸 "Black box" perception limits adoption: PLTR's proprietary platform approach faces resistance from enterprises preferring open, flexible solutions from Databricks/Snowflake. The closed ecosystem creates switching costs but also limits addressable market. Some customers cite lack of transparency vs open-source alternatives.

-

⚡ Execution risk on commercial growth: Must maintain [50%+ US commercial growth](https://investors.palantir.com/files/Palantir Q3 2024 Business Update.pdf) to meet expectations. Bootcamp model requires scaling from 500 to 3,000+ annually. Customer acquisition costs trending higher as easier enterprise wins captured. Any slowdown in commercial momentum would be devastating to growth narrative.

-

🌍 Geopolitical and regulatory risks: AI ethics concerns around defense/surveillance applications could trigger restrictions. Privacy regulations (GDPR, CCPA) impact data platform capabilities. Export controls on AI technology create compliance overhead. Growing market dominance in government AI could attract antitrust scrutiny.

-

📊 Quadruple witching volatility (Dec 19-23): Nasdaq implementation coincides with options expiration, creating explosive volatility potential. Large option positions (like this $18.5M trade!) can create gamma squeezes or volatility spikes in either direction. Unpredictable short-term price action during this window.

-

💔 Macroeconomic headwinds: Recession fears could pause AI platform investments. CFOs scrutinizing ROI on expensive AI deployments. PLTR's premium pricing vulnerable in cost-cutting environment. High-growth, high-multiple stocks historically underperform during economic slowdowns or rate increases.

🎯 The Bottom Line

Real talk: Someone just bet $18.5 MILLION that PLTR explodes higher into year-end, positioning across two time horizons (Dec 19 and Jan 16) to capture the Nasdaq-100 implementation catalyst. This isn't a hedge or collar - this is PURE BULLISH CONVICTION betting on $180-$200 range by January.

What this trade tells us:

- 🎯 Sophisticated player expects Nasdaq buying pressure to drive significant upside (not just drift higher)

- 💥 The TWO-PRONGED structure (Dec $200 calls + Jan $180 calls) shows they're playing both "moonshot" and "base case" scenarios

- 📊 Identical 17,257 size suggests institutional allocation model, not retail FOMO

- ⏰ Timing around Nasdaq-100 implementation (Dec 23) is NOT coincidental - they're positioning for mechanical buying wave

- 💰 $18.5M commitment shows strong conviction despite already being up 343% YTD

This is NOT a "guaranteed winner" - it's a HIGH RISK/HIGH REWARD bet on a binary catalyst.

If you own PLTR:

- ✅ Consider trimming 15-25% at $170+ levels if you bought <$120 (lock in triple-digit gains)

- 📊 Set mental stop at $165 (major gamma support) to protect remaining position

- ⏰ Watch Dec 23 Nasdaq implementation closely - if stock gaps up 10%+ and you're sitting on huge gains, TAKE SOME PROFITS

- 🎯 If holding through year-end, be prepared for volatility and potential "sell the news" after Dec 23

- 🛡️ Consider selling covered calls at $180-$185 strikes to generate income if you're long-term bullish but want downside protection

If you're watching from sidelines:

- ⏰ December 23rd Nasdaq implementation is the catalyst to watch - don't chase before then!

- 🎯 Post-implementation pullback to $160-165 would be EXCELLENT entry (with 6-10% margin of safety)

- 📈 Looking for confirmation: Sustained volume >50M shares, break above $175 resistance, Nasdaq buying completion

- 🚀 Longer-term (Q1 2025), earnings catalyst and AIP bootcamp momentum could drive another leg to $200+

- ⚠️ Current valuation (430x P/E) is EXTREME - only enter if you believe in multi-year AI platform story

If you're considering the call trade:

- 🎯 The Jan $180 calls are the "smarter" play (only 4% OTM, captures full Nasdaq wave)

- 💀 The Dec $200 calls are LOTTERY TICKETS (15.5% OTM, 17 days to expiration - high risk!)

- ⚠️ Only allocate 2-5% of portfolio to either trade - this is SPECULATION, not investment

- 📊 Have exit plan BEFORE entering: Take profits at 50-100% gain rather than holding for max

- ⏰ Monitor daily - options can swing wildly during Nasdaq implementation window

If you're bearish:

- 🎯 Wait until AFTER Dec 23 Nasdaq buying completes before initiating short positions

- 📊 First support at $170, major support at $165, deep support at $160

- ⚠️ Bull put spreads (sell $165/buy $160) post-Dec 23 offer defined-risk way to bet on support holding

- 📉 Watch for break below $170 - that's the trigger for potential cascade to $165, then $160

- ⏰ Fighting $7B mechanical buying pressure is DANGEROUS - timing is everything

Mark your calendar - Key dates:

- 📅 December 19 (Thursday) - Monthly OPEX and Triple Witch (first call expiration!)

- 📅 December 23 (Monday) - Nasdaq-100 rebalancing implementation ($7B buying!)

- 📅 January 16, 2026 (Friday) - Monthly OPEX (second call expiration)

- 📅 Early May 2025 - Q1 2025 earnings report (guided $858-862M revenue)

- 📅 Full Year 2025 - Target $3.74-3.76B revenue (+31% YoY)

Final verdict: PLTR's fundamental story is INCREDIBLY strong - government contract dominance, [explosive commercial growth](https://investors.palantir.com/files/Palantir Q3 2024 Business Update.pdf), revolutionary AIP platform, and Nasdaq-100 inclusion creating $7B buying wave. BUT at 430x P/E after 343% YTD gain with $4B insider selling, the risk/reward is NO LONGER favorable for aggressive new positioning.

The $18.5M call buyer believes Nasdaq implementation overwhelms all concerns and drives explosive rally to $180-200. They might be right. But they're also risking $18.5M on a binary catalyst with potential 100% loss.

Be smart. Size appropriately. Use defined risk. Take profits. The AI revolution will still be here in Q1 2025, and you'll sleep better at night with a disciplined approach.

Stay sharp, manage risk, and may the gamma be with you. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-scores and unusual classifications reflect statistical analysis of recent trading patterns - they do not imply the trades will be profitable or that you should follow them. Index inclusion creates mechanical buying but also "sell the news" risk. Always do your own research and consider consulting a licensed financial advisor before trading. The call buyer may have complex portfolio needs not applicable to retail traders.

About Palantir Technologies: Palantir Technologies is an analytical software company that leverages data to create efficiencies in its clients' organizations through its Gotham (government) and Foundry (commercial) platforms, with a market cap of $399.2 billion in the Prepackaged Software industry.