🔥 PLTR Massive $36M Call Sale - Institutional Profit-Taking on AI Defense Rally! 💰

📅 December 30, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just SOLD $36 MILLION worth of PLTR call options at the $160 strike expiring March 20, 2026! This massive 11,000 contract sale represents institutional profit-taking with PLTR trading at $183.19 - meaning they're locking in gains on calls they likely bought months ago when the stock was much lower. Translation: Smart money is cashing out of their AI defense trade after PLTR's explosive 150%+ YTD run, banking profits before potential volatility in Q1 2026.

📊 Company Overview

Palantir Technologies (PLTR) is the analytical software powerhouse behind government intelligence and enterprise AI transformation:

- Market Cap: $438.98 Billion (Top 10 tech company by valuation!)

- Industry: Prepackaged Software Services

- Current Price: $183.19 (up +150% YTD)

- Primary Business: Foundry platform (commercial AI), Gotham platform (government intelligence), AIP (Artificial Intelligence Platform)

- Founded: 2003 | Public Since: September 2020

- Employees: 4,414

Palantir focuses on leveraging data to create efficiencies for clients, with a selective approach restricting work to Western-allied nations. The company has transformed from government contractor to AI platform leader, with explosive commercial revenue growth and record contract values.

💰 The Option Flow Breakdown

The Tape (December 30, 2025 @ 12:31:59):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:31:59 | PLTR | BID | SELL | CALL $160 | 2026-03-20 | $36M | $160 | 11K | 33K | 11,000 | $183.19 | $32.90 |

🤓 What This Actually Means

This is institutional profit-taking on a massive scale! Here's the real story:

- 💸 Huge premium collected: $36M ($32.90 per contract × 11,000 contracts)

- 🎯 Deep in-the-money calls: $160 strike is $23.19 below current price (12.7% ITM)

- ⏰ Strategic timing: 80 days to March expiration - capturing Q4 earnings (Feb 2026) and any volatility

- 📊 Size matters: 11,000 contracts represents 1.1 million shares worth ~$201M at current prices

- 🏦 Closing position: With Vol/OI ratio of 0.333 and existing 33K open interest, this is likely closing a long position

What's really happening here: This trader likely bought these deep ITM $160 calls back when PLTR was trading in the $160-180 range (probably October-November 2025), paying maybe $15-20 per contract. Now with the stock at $183 and calls worth $32.90, they're SELLING to close for a massive profit. Think about it: buying at $20 and selling at $32.90 = 64% gain in 2-3 months, or they held even longer for bigger gains.

Why sell now instead of holding? With PLTR up +150% YTD at extreme valuations (P/E ~428x), smart money is derisking ahead of Q4 earnings uncertainty, potential profit-taking, and the new year. They're saying "I've won big, time to lock it in."

Unusual Score: 🔥 EXTREMELY UNUSUAL (3.85 Z-Score) - This trade is 33x the normal contract size for PLTR options. This happens only a few times per year. With Vol/OI ratio of 0.333 (moderate activity), this represents concentrated profit-taking by likely 1-2 large institutional players.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

PLTR is on an absolute TEAR - up +150% YTD with current price of $183.19. The chart shows a stunning AI-driven transformation from $63.40 in January to a peak of $207.52 in early November. This isn't a steady climb - it's a moonshot fueled by explosive 121% U.S. commercial growth, the $10 billion Army contract, and AIP platform adoption.

Key observations:

- 🚀 Parabolic rally: Vertical move from $80 in September to $207 in November on Q3 earnings beat

- 📈 All-time highs: Hit $207.52 on November 3rd after Q3 results crushed expectations

- 🎢 Recent pullback: Down ~12% from ATH to $183 - healthy profit-taking after massive run

- 📊 Institutional rotation: Following S&P 500 (Sept 2024) and Nasdaq-100 (Dec 2024) inclusion

- ⚠️ Overbought historically: Trading at 428x P/E and 118x P/S - valuation EXTREME even by tech standards

The chart pattern screams "take profits" - after doubling in just 3 months and trading near all-time highs, smart money is rotating out. This option sale fits perfectly with that narrative.

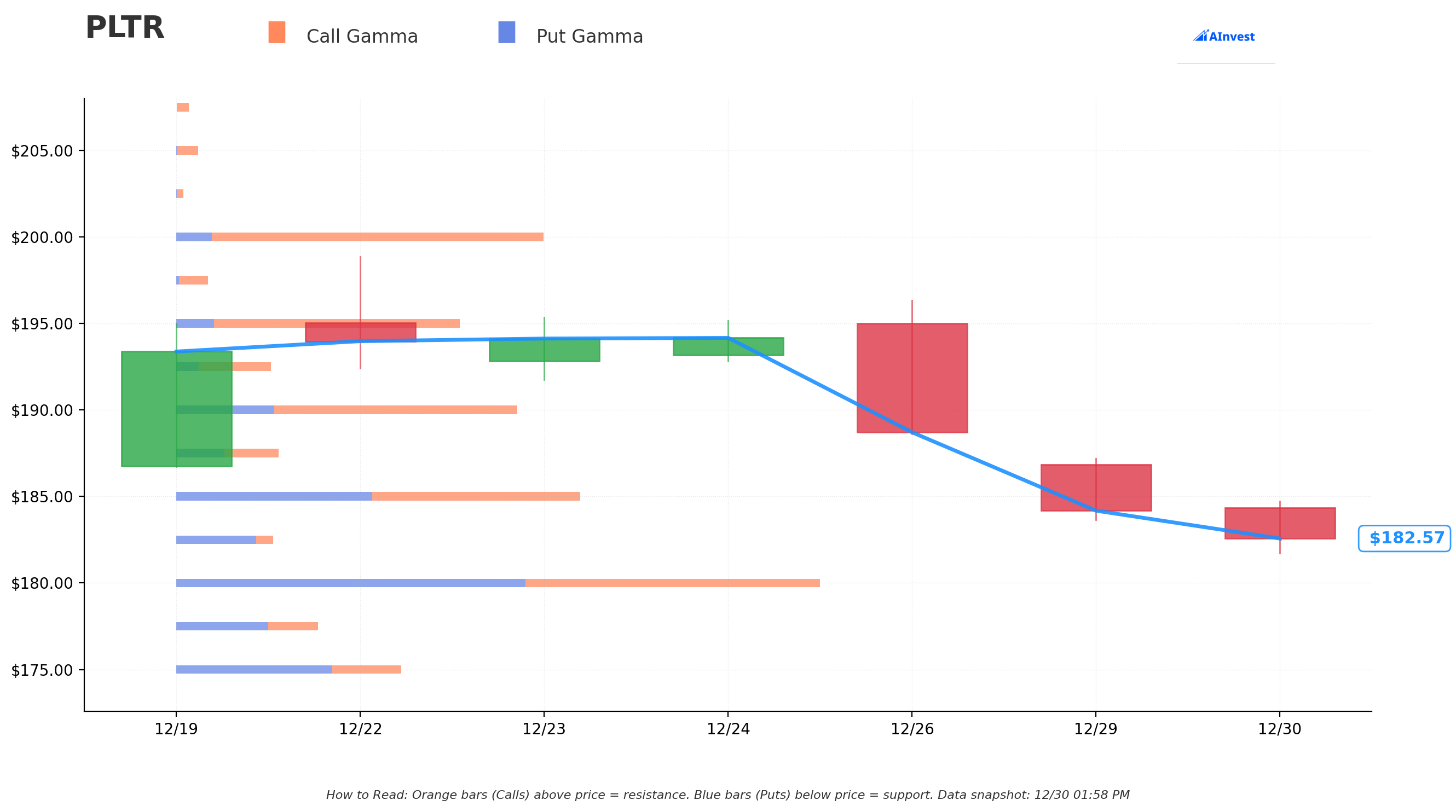

Gamma-Based Support & Resistance Analysis

Current Price: $182.70

The gamma exposure map reveals critical magnetic price levels that will govern near-term action:

🔵 Support Levels (Put Gamma Below Price):

- $180 - MASSIVE support wall with 44.8B total gamma (STRONGEST FLOOR!)

- $177.50 - Secondary support at 9.8B gamma (dealers buying dips here)

- $175 - Major structural floor with 15.6B gamma

- $170 - Deep support at 15.9B gamma (round number psychology)

- $165 - Extended support zone with 7.4B gamma

- $160 - Critical floor at 16.5B gamma (EXACTLY where this call was struck! Not coincidental)

🟠 Resistance Levels (Call Gamma Above Price):

- $185 - Immediate ceiling with 28.3B gamma (strong resistance overhead)

- $187.50 - Secondary resistance at 7.2B gamma

- $190 - Major ceiling zone with 23.9B gamma (psychological barrier)

- $195 - Extended upside resistance at 19.8B gamma

- $200 - Monster resistance at 25.7B gamma (4% above current - tough ceiling)

What this means for traders: PLTR is consolidating between massive $180 support (44.8B - single largest level) and overhead $185-190 resistance. The gamma data shows market makers holding enormous positions at $180 which creates natural buying pressure on dips - this is THE LINE IN THE SAND. Any break above $185-190 resistance could trigger momentum back toward $200, but that 25.7B gamma wall at $200 will be tough to crack.

Notice anything? The call seller struck at $160 where there's 16.5B gamma support. They're positioned well below major support levels, giving themselves a massive cushion. Even if PLTR drops 12% to $160 by March, they still pocket the full premium. That's smart risk management.

Net GEX Bias: Slightly bullish overall but balanced - showing market at equilibrium after the massive rally.

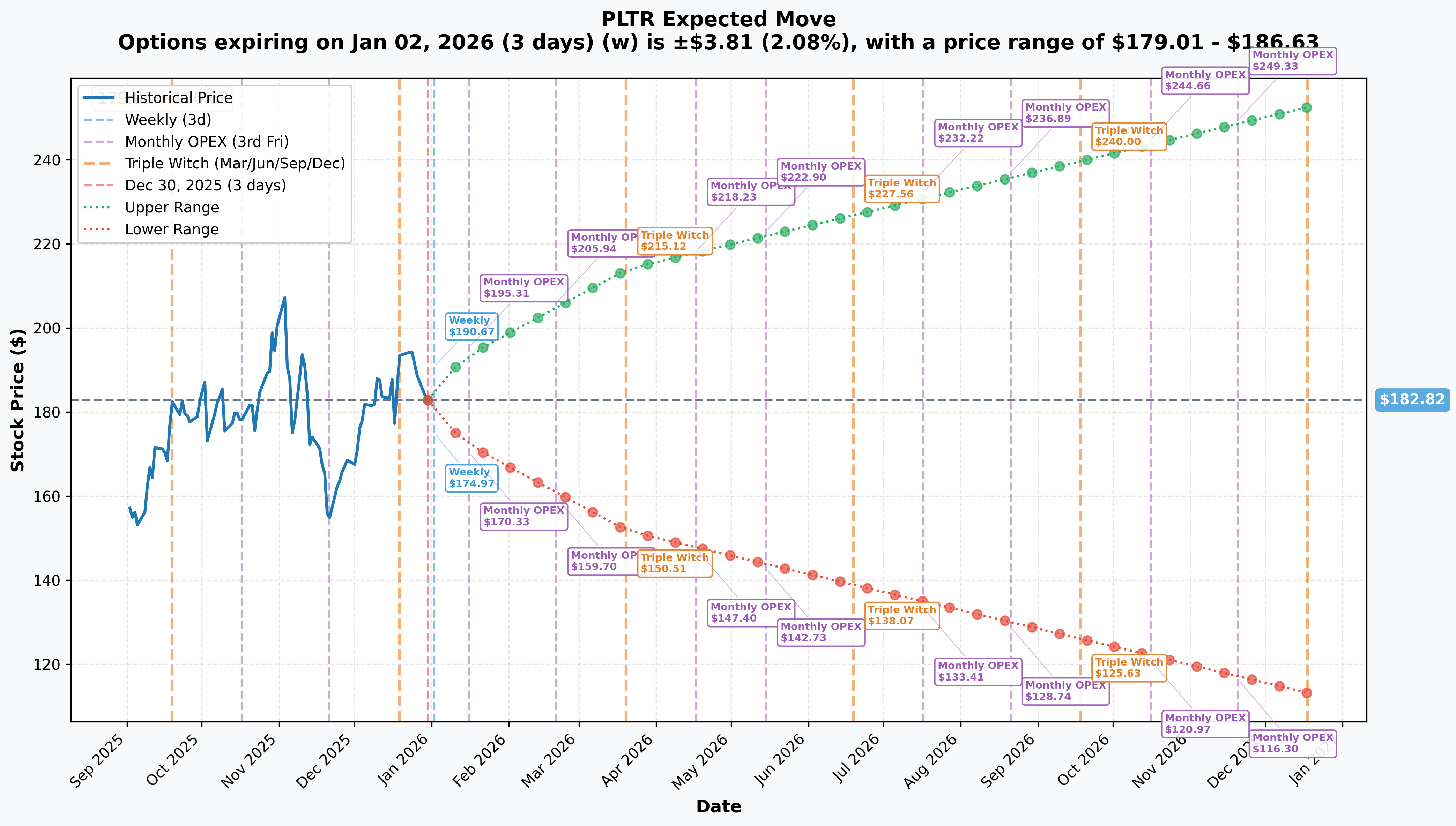

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 2 - 3 days): ±$3.81 (±2.08%) → Range: $179.01 - $186.63

- 📅 Monthly OPEX (Jan 16 - 17 days): ±$10.88 (±5.95%) → Range: $171.94 - $193.70

- 📅 Quarterly Triple Witch (Mar 20 - 80 days - THIS TRADE!): ±$31.17 (±17.05%) → Range: $151.64 - $213.99

- 📅 Yearly LEAPs (Dec 18, 2026 - 353 days): ±$69.76 (±38.16%) → Range: $113.05 - $252.58

Translation for regular folks: Options traders are pricing in a 2% move ($4) by end of week for year-end positioning, but a MUCH larger 6% move ($11) through January OPEX which includes year-end flows. The March 20th expiration (when this $36M trade expires) has an implied range of $151.64-$213.99, meaning the market sees a 17% two-way possibility.

The March expiration range lower bound of $151.64 sits well below the $160 strike - giving the call seller comfortable cushion. For these calls to expire worthless, PLTR would need to drop 13% to $160 or lower. Given the $180 gamma support wall, that seems unlikely unless major negative catalyst emerges.

Key insight: The relatively contained 2% weekly implied move suggests market expects consolidation through year-end, but the 17% quarterly move reflects uncertainty around Q4 earnings in February and ongoing AI/defense execution.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened - Driving Current Price)

Q3 2025 Earnings BLOWOUT - November 3, 2025 📊

PLTR absolutely CRUSHED Q3 expectations, triggering the rally to all-time highs:

- 📊 Revenue: $1.181B (up 63% YoY) - Beat by 8.26%

- 💰 EPS: $0.21 (up 250% YoY) - Beat by 40% vs $0.15 expected

- 🚀 U.S. Commercial Revenue: $397M (up 121% YoY) - EXPLOSIVE growth

- 🤖 Total Contract Value (TCV): $2.76B (+151% YoY) - Company record!

- 💪 Rule of 40 Score: 114% (revenue growth + profit margin) - Exceptional efficiency

- 📈 Customer Growth: 45% YoY overall, 49% commercial

Why this matters: This was THE quarter that transformed PLTR from "government contractor" to "enterprise AI leader." The 121% U.S. commercial growth silenced critics who said PLTR couldn't scale beyond defense. This earnings report triggered the run from $155 to $207 - and explains why call buyers made fortunes.

U.S. Army $10 Billion Enterprise Agreement - July 31, 2025 🇺🇸

Game-changing government contract that provides massive revenue visibility:

- 💰 Contract ceiling: Up to $10 billion over 10 years

- 📝 Consolidates 75 existing contracts into single framework

- 🎯 Covers Palantir's commercial products for Army and DoD agencies

- ⚡ Streamlines procurement and removes pass-through fees

This is PLTR's "annuity" - recurring revenue locked in for a decade with the world's most powerful military. Provides stability and cash flow to fund aggressive AIP expansion.

Maven Smart System Contract Expansion - May 2025 🚀

Critical defense AI platform seeing explosive adoption:

- 💰 Contract ceiling increased by $795M to nearly $1.3B through 2029

- 👥 Active user base: 20,000+ across 35+ military tools

- 📈 User base DOUBLED since January 2025 - showing rapid adoption

Maven is becoming the "operating system" for military AI - similar to what AIP is doing commercially.

U.S. Navy ShipOS Contract - December 9, 2025 🚢

Brand new contract announced just weeks ago:

- 💰 Value: $448 million

- 🎯 Platform manages supply chain visibility for Virginia-class and Columbia-class nuclear submarines

- 📊 Signals expansion into naval operations beyond Army/Air Force

Total 2025 Defense Contract Value: Over $2 billion in new defense contracts captured this year alone.

Strategic Partnerships Accelerating Commercial Growth 🤝

- Snowflake Partnership (October 2025): AIP to run directly on Snowflake's Data Cloud - expands addressable market

- Accenture Partnership: Launched Accenture Palantir Business Group for enterprise AI deployment

- Nvidia Partnership: Using Palantir AIP/Ontology with Nvidia CUDA X libraries for AI infrastructure

- xAI Partnership: Collaboration with Elon Musk's AI venture

AIP Platform Success Stories 🌟

The AI Platform is PLTR's commercial growth engine, with impressive customer deployments:

- 🏪 Walgreens: AI workflows deployed to 4,000 stores in 8 months

- 🏦 AIG: Agentic AI ecosystem accelerates underwriting 5X

- ✈️ Notable clients: Airbus, Morgan Stanley, American Airlines, BP, Novartis, Merck KGaA

The "Bootcamp" sales model (deploy first, bill later) is creating unprecedented speed-to-value.

🚀 Upcoming Catalysts (Next 6 Months - Critical for March Options)

Q4 2025 Earnings Release - February 2-18, 2026 📊

THIS IS THE CATALYST that will determine if this call sale looks brilliant or premature:

Expected Date: Early-mid February 2026 (exact date unconfirmed)

Consensus Expectations:

- 📊 Revenue: ~$1.33B (per company guidance) - up 61% YoY

- 💰 EPS: $0.21

- 🚀 U.S. Commercial: Can the 121% growth rate CONTINUE? This is THE question

Key Metrics to Watch:

- 🔥 U.S. commercial revenue sustainability: 121% is unsustainable long-term, but can it hold above 80-100%?

- 🌍 International commercial acceleration: Currently lagging at only 10% YoY - needs improvement

- 📝 Total contract value momentum: Can Q4 match Q3's record $2.76B TCV?

- 💰 Operating margin expansion: How much falls to bottom line as scale increases?

- 👥 Customer count trajectory: 45% YoY customer growth needs to continue

- 🎯 FY 2026 guidance: Street wants $6.2B revenue (+41% YoY) - will management deliver?

Upside surprise potential: Beat-and-raise pattern has been consistent for 12 quarters. AIP momentum shows no signs of slowing. Government contracts provide visibility.

Downside risk factors: ANY disappointment in commercial growth would be catastrophic at current valuation. International weakness persisting would raise questions about TAM. Conservative guidance given stock at $180+ could trigger selloff.

Why this matters for the option trade: The call seller positioned at $160 strike likely expects either (1) choppy consolidation through earnings with stock staying $160-200 range, or (2) profit-taking on any disappointment. By selling in late December, they collect $32.90 premium and let Q4 earnings be someone else's problem. Smart.

2026 Full Year Catalysts 📅

Financial Expectations:

Product & Platform Evolution:

- 🎤 AIPCon 9 (Expected H1 2026): Annual flagship event showcasing customer wins (historically Q1-Q2)

- 🔋 Chain Reaction Deployment: Full-scale rollout of AI infrastructure initiative with Nvidia/CenterPoint

- 🚢 ShipOS Expansion: Potential additional Navy contracts following December 2025 win

- 🧠 Ontology Platform Enhancements: Continued R&D investment in proprietary data layer

Government Pipeline:

- 🇺🇸 Army Enterprise Agreement task orders (up to $10B ceiling being drawn down)

- 🚀 Potential Maven Smart System expansions beyond $1.3B ceiling

- 🌍 NATO partnership expansions

- 🛡️ Additional defense agency adoptions

Commercial AI Expansion:

- Dan Ives (Wedbush): "Palantir will expand its commercial AI success with AIP and be one of the leaders of the software being front and center in the AI Revolution" in 2026

- Continued enterprise customer acquisition via "Bootcamp" model

- International commercial acceleration (closing the gap vs. U.S. 121% growth)

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timing, here are scenarios through March 20th expiration:

📈 Bull Case (30% probability)

Target: $210-$230

How we get there:

- 💪 Q4 earnings CRUSH again with commercial growth holding above 100% YoY

- 📝 Q4 TCV exceeds $3B on major enterprise wins

- 🚀 FY 2026 guidance surprises to UPSIDE ($6.5B+ revenue vs $6.2B consensus)

- 🌍 International commercial finally accelerates (30%+ growth) showing TAM expansion

- 🎯 Major new government contracts announced (Pentagon, NATO expansion)

- 📈 Breakout above $200 gamma resistance triggers momentum to $220-230

- 🤖 AIPCon 9 showcases game-changing new customer deployments

- ⚡ Street raises price targets en masse - Dan Ives goes to $250+

Key metrics needed:

- U.S. commercial >100% growth (not decelerating)

- International commercial >30% growth (proving global scalability)

- Operating margins expanding 200+ bps (proving leverage)

- Customer count >60% YoY (accelerating adoption)

Probability assessment: Only 30% because it requires PERFECT execution with stock already up 150% YTD at extreme valuation (428x P/E). Gamma resistance at $185-200 creates natural ceiling. Would need spectacular Q4 surprise to break higher.

Call seller P&L: At $220, their $160 calls worth $60 intrinsic - but they collected $32.90, so effective sale at $192.90. With stock at $220, they "miss out" on $27.10/share × 11,000 = $29.8M in additional gains. But they already banked $36M profit closing the position!

🎯 Base Case (50% probability)

Target: $170-$195 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q4 earnings meeting/slightly beating consensus

- 📊 Commercial growth still strong but decelerating to 80-100% YoY (still excellent!)

- ⚖️ Guidance conservative/in-line ($6.0-6.3B for FY2026) due to tough comps

- 🤖 AIP traction continuing but not accelerating dramatically

- 🇨🇳 International remains mixed - some progress but not breakthrough

- 🎪 No major new catalyst surprises in Q1 2026

- 🔄 Trading between $180 gamma support and $190-195 resistance for weeks

- 💤 Post-earnings consolidation as market digests massive YTD gains

- 📉 Volatility crush - IV drops from elevated levels back to 40-50% range

This is exactly what the call seller wants: Stock consolidates in $170-195 range, their $160 calls remain deep ITM but they already extracted $32.90 in extrinsic value + locked in their intrinsic gains by selling at $183. March expiration passes with stock at $185 - they captured 80-90% of potential gains without taking tail risk.

Why 50% probability: After 150% YTD rally, consolidation is NORMAL and HEALTHY. Fundamentals remain strong but valuation stretched. Most institutional players will hold and wait for next leg higher after digesting gains. The $180 gamma support (44.8B) should hold barring major negative surprise.

Call seller P&L: At $185 in March, they sold at $183 with $32.90 premium, missing only small additional gains. They WIN by avoiding volatility risk and locking in massive profits early.

📉 Bear Case (20% probability)

Target: $150-$170 (TEST THE SUPPORT LEVELS)

What could go wrong:

- 😰 Q4 earnings disappoint or guide conservative - commercial growth decelerates to <80%

- 🚨 International weakness persists - raises questions about TAM limitations

- ⚠️ Insider selling accelerates - CEO Karp already sold $2B in 2024, filing for $250M+ more in Nov 2025

- 💰 Broader tech selloff drags high-multiple AI names lower

- 📊 Analyst downgrades citing valuation (428x P/E, 118x P/S)

- 🌍 Government contract delays or budget cuts impact pipeline

- 🔨 Break below $180 gamma support triggers cascade to $170, then $160

- 💸 JPMorgan cut position by 32%, T. Rowe Price by 24% - institutional rotation continues

Critical support levels:

- 🛡️ $180: Major gamma floor (44.8B) - MUST HOLD or momentum shifts bearish

- 🛡️ $175: Secondary support (15.6B gamma)

- 🛡️ $170: Deep support (15.9B gamma) - psychological round number

- 🛡️ $160: Ultimate floor (16.5B gamma) + where call was struck - likely strong buying

Probability assessment: Only 20% because fundamentals remain VERY strong (121% commercial growth, $10B Army contract, record TCV). Would require multiple negative catalysts to break $180 support. But valuation offers ZERO cushion - any stumble magnified 3-4x.

Call seller P&L: Even at $160, their calls still have $0 extrinsic value (at-the-money). But they collected $32.90 selling at $183, so they've already banked massive profits and avoided the drawdown. If they bought these calls at $20 originally, they booked 64% gain versus riding to $160 for minimal additional upside. SMART.

💡 Trading Ideas

🛡️ Conservative: The "Thank You, Next" Strategy

Play: If you own PLTR, trim 30-50% here and lock in triple-digit gains

Why this works:

- ✅ You've WON - up 150% YTD is AMAZING. Protecting profits is smart trading

- 📊 At 428x P/E and 118x P/S, valuation has ZERO margin for error

- 🐋 Institutions are derisking ($36M call sale, $250M+ insider selling) - why fight smart money?

- 📅 Q4 earnings in ~6 weeks creates binary risk - better to lock in gains before volatility

- 🎯 Can always re-enter at $170-180 if consolidation creates better entry

- 💰 Tax considerations: Realize gains in early 2026, have full year for portfolio management

Action plan:

- 🎯 Sell 30-50% of position at current $180-185 levels

- 📊 Set MENTAL STOP at $175 (below gamma support) to protect remaining shares

- 👀 Watch Q4 earnings closely - if they crush again AND stock breaks $200, consider re-entering trimmed shares

- ⏰ Don't chase - be patient for $170-175 pullback which offers better risk/reward

- 💵 Redeploy proceeds into diversified positions (don't stay in cash earning nothing)

Risk level: Minimal (taking profits) | Skill level: Beginner-friendly

Expected outcome: Lock in generational gains, reduce concentration risk, sleep better at night. If PLTR continues higher, you still have 50-70% working. If it consolidates/pulls back, you sold the top.

⚖️ Balanced: Post-Earnings Bull Put Spread (Copy The Pros' Safety Net)

Play: After Q4 earnings, sell put spread using the gamma support levels

Structure: Sell $180 puts, Buy $170 puts (March 20 expiration - SAME as the $36M trade)

Why this works:

- 🎢 IV crush after earnings makes put spreads much cheaper to sell

- 📊 Defined risk spread ($10 wide = $1,000 max loss per spread)

- 🎯 Targets massive 44.8B gamma support at $180 - this is THE floor

- 💰 Collect premium betting PLTR stays above $180 (where institutions are positioned)

- ⏰ ~45 days to expiration post-earnings gives time for consolidation

- 🛡️ Essentially getting paid to buy PLTR at $180 if assigned (not terrible outcome!)

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Collect ~$2.50-3.50 credit per spread post-earnings

- 📈 Max profit: $250-350 if PLTR above $180 at March expiration (keep full credit)

- 📉 Max loss: $650-750 if PLTR below $170 (defined and limited)

- 🎯 Breakeven: ~$177-177.50

- 📊 Win rate: ~65-70% if $180 support holds

Entry timing:

- ⏰ Wait 2-3 days post-earnings (mid-February) for full IV collapse

- 🎯 Only enter if stock above $185 (gives cushion to $180 floor)

- ❌ Skip if stock already testing $180 (spread too risky)

Position sizing: Risk only 5-10% of portfolio (this is premium collection with defined risk)

Risk level: Moderate (defined risk, neutral-to-bullish) | Skill level: Intermediate

🚀 Aggressive: The "Ride or Die" Long Call Calendar (ADVANCED ONLY!)

Play: Bet on consolidation into Q4 earnings, then explosive move after

Structure:

- SELL: January 16 $190 calls (near-term)

- BUY: March 20 $190 calls (same expiration as the $36M trade)

Why this could work:

- ⏰ Betting on choppy consolidation through January, then earnings catalyst in February

- 💰 Sell expensive near-term premium (high IV), buy cheaper back-month (lower IV)

- 📊 Max profit if PLTR consolidates $185-195 through January 16, then breaks out after earnings

- 🎯 $190 strike sits just above current price and below $195 resistance

- ⚡ Calendar spreads profit from time decay AND IV expansion into earnings

- 🔥 If PLTR stays $185-190 by Jan 16, short calls expire worthless, keep long March calls with earnings catalyst ahead

Why this could blow up (SERIOUS RISKS):

- 💸 COMPLEXITY: Calendar spreads are tricky - need to manage both legs carefully

- ⚠️ Early assignment risk: If PLTR rallies hard above $190 before Jan 16, short calls get exercised

- 📉 Whipsaw risk: Big move either direction before Jan 16 hurts calendar spread value

- ⏰ Timing dependent: Need PLTR to cooperate with consolidation thesis (market doesn't care what you want!)

- 😱 Vol collapse: If IV drops across all months, spread loses value even if price right

- 🎢 Earnings binary: Could go either way - calendar benefits from consolidation, NOT volatility

Estimated P&L:

- 💰 Cost: ~$5-7 net debit per calendar spread

- 📈 Max profit scenario: PLTR at $190 on Jan 16 = short calls expire worthless, March calls worth $10-15 = $3-8 profit (50-100%+ ROI)

- 🚀 Post-earnings explosion: If PLTR rallies to $220 after Feb earnings, March calls could be worth $30+ = $23-25 profit (300%+ ROI!)

- 📉 Loss scenario: PLTR at $210 on Jan 16 = short calls ITM ($20 loss), long calls worth $20 = net loss $5-7 (100% loss)

- 💀 Disaster: PLTR drops to $160 = both legs near worthless (100% loss)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded calendar spreads before and understand mechanics

- ✅ Can monitor position daily and adjust/roll as needed

- ✅ Understand early assignment risk and have capital to cover

- ✅ Accept that timing needs to work PERFECTLY for max profit

- ✅ Can afford to lose entire debit (real possibility if wrong)

- ⏰ Plan to actively manage - this is NOT set-and-forget

Risk level: EXTREME (complex mechanics, multiple ways to lose) | Skill level: Advanced only

Probability of profit: ~45% (need consolidation AND subsequent rally - tough combo)

⚠️ Risk Factors

Don't get blindsided by these potential landmines:

-

⏰ Q4 earnings binary event (~Feb 10-15, 2026): Results will determine if $180+ levels hold or if profit-taking accelerates. Stock could gap 10-15% either direction based on commercial growth trajectory (need >100% to maintain narrative), international progress, and FY2026 guidance quality. Historical precedent shows PLTR can have violent moves on earnings surprises - both directions.

-

💸 Valuation at stratospheric levels: Trading at 428x trailing P/E and 118x price-to-sales - literally the most expensive stock on P/S basis ever for a company of its market cap. This is EXTREME pricing for perfection. Requires sustained 40-50% revenue growth with margin expansion for YEARS to justify current multiple. Any deceleration magnified 4-5x. Zero margin of safety.

-

🚨 Massive insider selling continues: CEO Alex Karp sold $2B in 2024, plans up to $1B in 2025. In November 2025, Karp + 4 executives filed to sell $250M+ combined. While using 10b5-1 plans (pre-scheduled), the SCALE and TIMING (at all-time highs) signals even management sees current levels as rich. When insiders aggressively sell, retail should pay attention.

-

📊 Institutional rotation accelerating: JPMorgan reduced position by 32%, T. Rowe Price by 24%. Smart money taking profits after massive run. The $36M call sale analyzed here is PART of this broader derisking trend. When the biggest asset managers trim, it's a warning sign even if fundamentals remain strong.

-

🌍 International commercial growth lagging dramatically: U.S. commercial up 121% YoY while international only up 10% - this is a MAJOR red flag for TAM sustainability. If PLTR can't crack international markets (data sovereignty issues, regulatory friction, competitive dynamics), the addressable market shrinks considerably. Bulls assume international will "catch up" - not guaranteed.

-

⚖️ Competitive pressure intensifying: Microsoft, AWS, Databricks investing BILLIONS in enterprise AI. Databricks hit ~$3B ARR by end of 2025. PLTR's "Ontology" moat is real but competitors are narrowing gap. Enterprise customers increasingly have alternatives - pricing power could erode.

-

🔒 Regulatory/Legal friction building: UK MPs questioning Palantir contracts after Swiss security concerns. Data sovereignty issues in Europe. U.S. scrutiny over immigration-related system involvement. Political and regulatory friction can slow contract awards and create reputational risk limiting commercial TAM.

-

🔐 Cybersecurity/Reputational risks: U.S. Army flagged security flaws in battlefield communications system co-developed with Anduril. Privacy/surveillance concerns could deter commercial clients hesitant about association. Any major security breach would be catastrophic for company built on trust.

-

💰 Government concentration and budget risk: Despite commercial growth, government still represents 50%+ of revenue. Federal budget cuts, political transitions, or program cancellations could impact revenue significantly. While $10B Army contract provides visibility, it's a ceiling not a guarantee - actual spend depends on annual appropriations.

-

📉 Gamma resistance at $185-$200 creates ceiling: Massive call gamma at $185 (28.3B) and $200 (25.7B) means market makers will systematically SELL into rallies to hedge. This creates mechanical selling pressure making breakouts difficult without massive catalyst. Current price pinned just under $185 resistance.

-

🎢 Tech sector rotation risk: If market rotates from high-growth tech to value/cyclicals (recession fears, rate changes, AI sentiment shift), PLTR as a 428x P/E stock gets hit FIRST and HARDEST. Recent examples: growth stocks down 30-40% in weeks during 2022 tech selloff. PLTR offers no dividend, no buybacks, just growth story - highly vulnerable to sentiment shifts.

-

⚠️ AIP platform execution risk: The 121% commercial growth is PRIMARILY driven by AIP adoption. If AIP platform encounters technical issues, slower deployment times, or customer dissatisfaction, the entire commercial growth thesis unravels. This is still relatively NEW platform (launched mid-2023) - early innings of proving sustained value.

🎯 The Bottom Line

Real talk: Someone just cashed out $36 MILLION worth of PLTR call options after riding them from who-knows-where to a $32.90 sale price with the stock at $183. This isn't bearish on PLTR's long-term story - it's brilliant profit-taking by institutions who've captured the 150% YTD rally and are now derisking before Q4 earnings volatility.

What this trade tells us:

- 💰 Sophisticated player is TAKING CHIPS OFF THE TABLE at all-time highs after massive run

- 🎯 They positioned at $160 strike giving huge cushion - shows they expect consolidation in $160-200 range through March

- ⚖️ The timing (late December, before Q4 earnings) shows they're not interested in holding through the next binary event

- 📊 With Vol/OI ratio of 0.333, this is likely 1-2 large players closing positions, not opening them

- ⏰ They're booking gains NOW rather than risking Q4 earnings surprise, institutional rotation, or valuation multiple compression

This is NOT a "sell everything immediately" signal - it's a "the easy money has been made, time to be selective" signal.

If you own PLTR:

- ✅ Strongly consider trimming 30-50% at $180-185 levels (LOCK IN triple-digit gains!)

- 📊 Set mental stop at $175 (below major gamma support) to protect remaining position

- ⏰ Don't get greedy - you've already WON massively. Protecting profits is champion-level trading

- 🎯 If Q4 earnings CRUSH expectations AND stock breaks $200, can consider re-entering trimmed shares on momentum

- 🛡️ Consider protective puts (maybe $180 or $175 strikes) if holding concentrated position through earnings

- 💵 Remember: CEO Karp, insiders, and JPMorgan are ALL selling - you're in good company taking profits

If you're watching from sidelines:

- ⏰ DO NOT CHASE at $180+ - risk/reward terrible at 428x P/E after 150% YTD run

- 🎯 Wait for Q4 earnings clarity (early-mid February) and subsequent consolidation

- 📈 Best entry would be pullback to $165-175 (gamma support levels) which offers 10-15% margin of safety

- 🚀 Looking for confirmation of: Commercial growth >100% YoY, international acceleration >20%, FY2026 guidance $6.3B+, operating margin expansion

- ⚠️ Longer-term (12+ months), PLTR's AI platform story and government moat are legitimate - but current valuation prices in YEARS of perfect execution with zero room for error

- 💡 Better to miss the first 10% of a new rally than catch the last 10% of an old one

If you're bearish:

- 🎯 Don't short into institutional selling - let the consolidation/decline come to you

- 📊 First test will be $180 support (44.8B gamma) - if that breaks, cascade to $170-175 likely

- ⚠️ Post-Q4 earnings put spreads offer defined-risk way to play downside after IV crush

- 📉 Watch for break below $175 - that's the trigger for momentum shift toward $160

- ⏰ Most vulnerable scenario: Q4 earnings merely "good" (not spectacular), causing valuation-based selloff even without fundamental disappointment

Mark your calendar - Key dates:

- 📅 January 16, 2026 - Monthly OPEX (first potential volatility event)

- 📅 February 2-18, 2026 - Q4 FY2025 earnings report (THE CATALYST!)

- 📅 February post-earnings - Price action and guidance will set tone for Q1-Q2

- 📅 March 20, 2026 - Expiration of this $36M call trade and quarterly triple witch

- 📅 H1 2026 - Expected AIPCon 9 customer showcase event

- 📅 Mid-2026 - Chain Reaction AI infrastructure deployment milestones

Final verdict: PLTR's transformation from "government contractor" to "enterprise AI platform leader" is REAL - the 121% U.S. commercial growth, $10B Army contract, record $2.76B TCV, and AIP platform momentum validate the long-term bull case. BUT, at 428x trailing P/E and 118x P/S after 150% YTD gain, the risk/reward is NO LONGER favorable for aggressive new positioning. The $36M institutional call sale, CEO selling $2B+, and major funds trimming positions are CLEAR signals: smart money is derisking at the peak.

Be patient. Let Q4 earnings clear. Look for better entry points at $165-175 with margin of safety. The AI revolution will still be here in 3 months, and you'll sleep better buying on consolidation than chasing all-time highs.

This is a marathon, not a sprint. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 3.85 Z-score reflects this specific trade's size relative to recent PLTR history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. PLTR trades at extreme valuations (428x P/E) with high volatility - suitable only for risk-tolerant investors. The call seller may have complex portfolio needs not applicable to retail traders.

About Palantir Technologies: Palantir Technologies is an analytical software company focusing on leveraging data to create efficiencies for clients through its Foundry (commercial) and Gotham (government) platforms, with a market cap of $438.98 billion in the Prepackaged Software Services industry.