PLTR: $8.2M LEAP Call Sale - Big Money Collecting Premium Through 2028!

January 13, 2026 | Unusual Activity Detected

The Quick Take

Someone just sold $8.2 MILLION worth of PLTR calls expiring in January 2028! This is a massive premium-collecting play on a stock that's up 173% in the past year. With a Z-score of 9.22 (EXTREMELY UNUSUAL), this is institutional-sized activity - likely a covered call strategy or a bet that PLTR won't break $200 over the next two years despite its AI dominance narrative.

Company Overview

Palantir Technologies Inc. (NASDAQ: PLTR) is a Denver-based software company specializing in big data analytics platforms for government and commercial clients. Founded in 2003 and public since September 2020, Palantir operates through two main platforms: Gotham (government) and Foundry (commercial).

| Metric | Value |

|---|---|

| Market Cap | $427.6B |

| Industry | Prepackaged Software |

| Employees | 4,414 |

| Current Price | ~$178.87 |

| P/E Ratio | 415x |

| 52-Week Range | $63.40 - $207.52 |

The company has emerged as a dominant AI infrastructure player, with its Artificial Intelligence Platform (AIP) driving explosive growth. However, that 415x P/E ratio tells you everything about the valuation expectations baked into this stock.

The Option Flow Breakdown

What Just Happened

| Time | Direction | Type | Expiration | Strike | Volume | OI | Premium | Spot | Option |

|---|---|---|---|---|---|---|---|---|---|

| 13:13:40 | SELL | CALL | 2028-01-21 | $200 | 1,500 | 2,400 | $8.2M | $178.87 | PLTR20280121C200 |

Trade Details:

- Option Symbol: PLTR20280121C200

- Option Price: $54.85 per contract

- Vol/OI Ratio: 62.5% (HIGH_ACTIVITY)

- Z-Score: 9.22 (EXTREMELY_UNUSUAL)

- Classification: Sell-to-Open (STO) - Short Call

What This Actually Means

This is a premium selling strategy - specifically a Short Call (STO). Here's what's likely happening:

Scenario 1: Covered Call Strategy The trader likely owns PLTR shares and is selling calls against their position to generate income. At $54.85 per contract on 1,500 contracts, they're collecting $8.2M upfront. If the stock stays below $200 by January 2028, they keep all the premium.

Scenario 2: Naked Call Sale (Higher Risk) If the trader doesn't own shares, this is an extremely bold bet that PLTR won't exceed $200 in the next two years. Given the stock's volatility and AI narrative, this carries significant risk.

Why $200 Strike Makes Sense:

- Current price: $178.87

- Strike price: $200 (11.8% above current)

- All-time high: $207.52

- Breakeven for seller: $254.85 ($200 + $54.85 premium)

The seller is betting that despite PLTR's momentum, the stock won't sustain a move above $254.85 - which represents a 42.5% gain from current levels. Given the extreme valuation (415x P/E), this isn't an unreasonable bet.

Technical Setup / Chart Check-Up

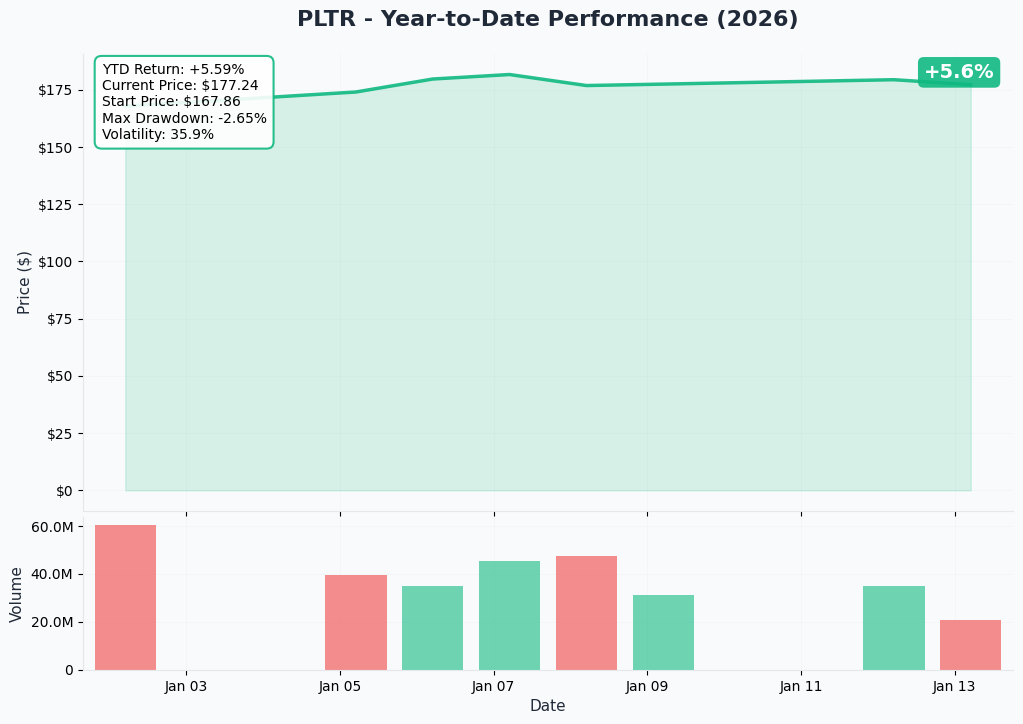

YTD Chart Analysis

PLTR has been on an absolute tear, with the stock up +173% over the past year and +1,829% since its October 2020 IPO. The chart shows a strong uptrend but also reveals the stock is currently trading about 24.8% below its all-time high of $207.52.

The pullback from highs creates an interesting dynamic - the LEAP call seller may be betting that this represents a near-term top in the AI hype cycle.

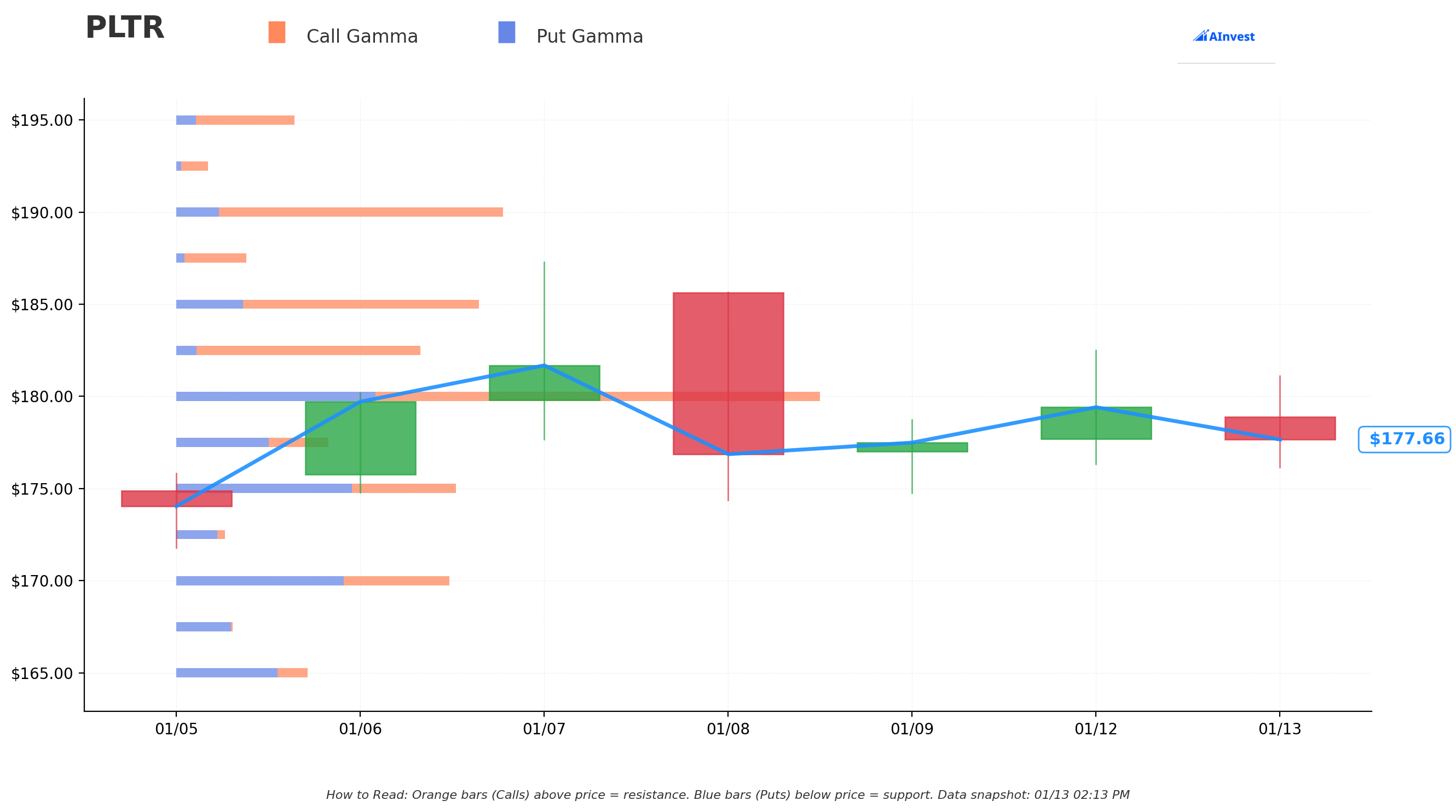

Gamma-Based Support & Resistance Analysis

Key Gamma Levels:

| Level | Strike | Net GEX | Distance from Price |

|---|---|---|---|

| Strongest Resistance | $180 | +22.33 | +1.3% |

| Resistance | $182.50 | +18.50 | +2.7% |

| Resistance | $185 | +15.44 | +4.1% |

| Resistance | $190 | +22.05 | +6.9% |

| Major Resistance | $200 | +11.00 | +12.5% |

| Strongest Support | $177.50 | -2.99 | -0.2% |

| Support | $175 | -6.35 | -1.6% |

| Support | $170 | -5.53 | -4.4% |

| Support | $165 | -6.30 | -7.2% |

| Support | $160 | -2.14 | -10% |

Translation for Retail Traders:

The $180 strike is a major resistance level with the highest net gamma exposure. Market makers are heavily positioned here, which means the stock may face headwinds pushing through $180. The $200 strike (our LEAP trade strike) has significant gamma, suggesting it's a key psychological and technical level.

On the downside, $175-$177.50 acts as immediate support. If we break below $170, the next major support is at $165.

Net GEX Bias: Bullish - Total call gamma ($210.9M) exceeds put gamma ($138.7M), suggesting market makers will need to buy as the stock rises (gamma squeeze potential) and sell as it falls (amplifying moves).

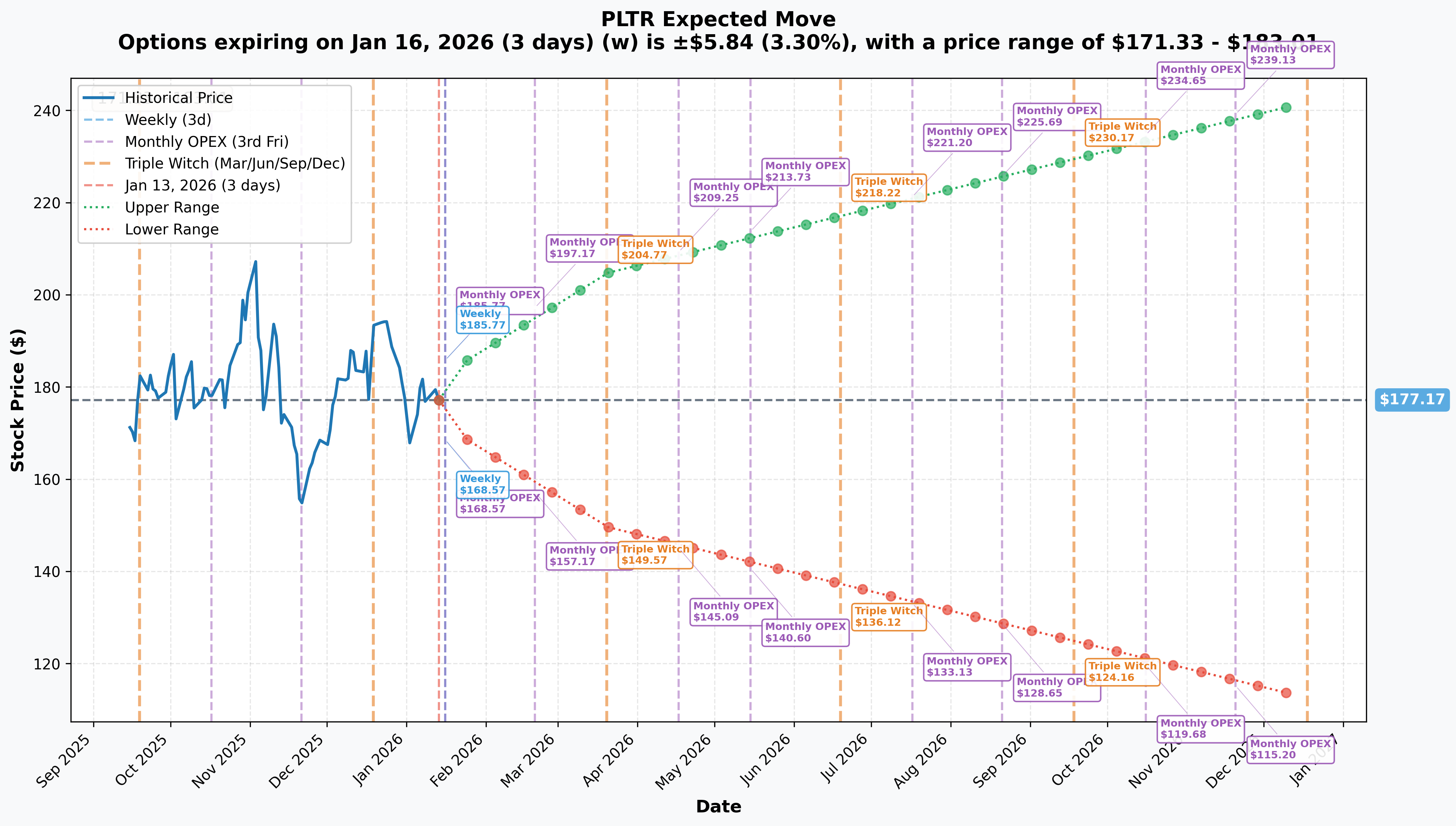

Implied Move Analysis

Current Implied Volatility Expectations:

| Timeframe | Expiry | Implied Move | Price Range |

|---|---|---|---|

| Weekly | 2026-01-16 | 3.3% | $171.33 - $183.01 |

| Quarterly (Triple Witch) | 2026-03-20 | 15.6% | $149.57 - $204.77 |

| Yearly LEAPS | 2026-12-18 | 36.5% | $112.48 - $241.85 |

Key Insight: The market is pricing in massive volatility for PLTR. A 36.5% annual implied move means options traders expect the stock could be anywhere from $112 to $242 by year-end. This explains the fat $54.85 premium on that $200 LEAP call - volatility = expensive options = opportunity for premium sellers.

The $200 Strike in Context:

- Quarterly Triple Witch upper range: $204.77 (above strike)

- Yearly LEAPS upper range: $241.85 (well above strike)

The option market thinks there's a real chance PLTR hits $200 within the year, making this short call position a calculated bet against the options market's expectations.

Catalysts

Upcoming Catalysts

| Date | Event | Impact |

|---|---|---|

| February 2, 2026 | Q4 2025 Earnings | Expected revenue $1.33B (+61% YoY), EPS $0.17-$0.18 |

| Q1-Q2 2026 | Army Enterprise Agreement task orders | $10B contract ceiling, major task orders expected |

| Mid-2026 | AIPCon Customer Event | New product reveals and customer announcements |

| Ongoing | DOGE Initiative Expansion | IRS database API, immigration enforcement platform |

Nasdaq's earnings calendar shows consensus expecting continued strong growth, with FY 2026 revenue growth projected at ~35% YoY.

Recent Catalysts (Already Happened)

Q3 2025 Results (November 3, 2025):

- Revenue: $1.181B (+63% YoY, beat by 8.3%)

- EPS: $0.21 (beat by 23.5%)

- U.S. Commercial Revenue: +121% YoY

- Raised FY 2025 guidance to $4.398B (Palantir IR)

Major Contracts:

- $10B U.S. Army Enterprise Agreement (July 2025) - consolidated 75 contracts into single 10-year deal (Breaking Defense)

- $448M Navy ShipOS Contract (December 2025)

- Maven Contract Expansion - ceiling raised by $795M to exceed $1B total

Recent Analyst Action:

- Citi upgraded to Buy with $235 target (+31% upside) on January 12, 2026

- Consensus remains "Hold" with average target $174-$190

Price Targets & Probabilities

Based on gamma levels, implied moves, and catalyst analysis:

Bull Case: $200-$210 (25% probability)

Triggers:

- Q4 earnings beat + aggressive FY 2026 guidance (40%+ growth)

- Major Army Enterprise task orders announced

- Broader AI market rally

Key Levels: Break above $180 gamma wall, then $185, $190 before testing $200

Risk to LEAP Seller: This is the scenario where the short call trade loses. Breakeven at $254.85 provides buffer.

Base Case: $165-$185 (50% probability)

Triggers:

- In-line earnings, guidance maintained at 35% growth

- Gradual contract awards without major surprises

- Market consolidation after massive 2025 gains

Key Levels: Stock oscillates between $175 support and $180 resistance

LEAP Seller Outcome: Premium decays, trade is profitable

Bear Case: $130-$160 (25% probability)

Triggers:

- Earnings miss or guidance cut

- Multiple compression as growth slows to 35%

- Broader tech selloff on valuation concerns

- Competition from hyperscalers (Microsoft, AWS)

Key Levels: Break below $170, $165, with $160 as major support

Risk Factors:

- Michael Burry's $912M bearish position signals institutional skepticism

- $250M+ insider selling by executives including CEO Alex Karp

- Extreme 415x P/E valuation leaves no margin for error

LEAP Seller Outcome: Big win - premium collected + stock declines = maximum profit

Trading Ideas

Conservative: Cash-Secured Put Selling

Strategy: Sell PLTR 2026-03-20 $160 Put @ ~$8.00 Max Risk: $15,200 per contract (if assigned) Max Profit: $800 per contract Breakeven: $152

Why This Works: You get paid to wait for a pullback. If PLTR drops to $160, you own shares at an effective cost basis of $152 - a 15% discount from current prices. Implied move lower range is $149.57, so this strike is near the bottom of expected range.

Balanced: Covered Call on Existing Position

Strategy: If you own 100+ PLTR shares, sell PLTR 2026-06-19 $200 Call @ $18-20

Max Profit: $200 strike + premium ($218-220 effective sale price)

Risk: Give up upside above $200

Why This Works: Mirrors the institutional trade we spotted. You collect premium while still participating in upside to $200. If the stock rockets past, you still profit - just with a cap.

Aggressive: Bull Call Spread (Contrarian to the Flow)

Strategy: Buy PLTR 2026-03-20 $180 Call, Sell PLTR 2026-03-20 $200 Call Cost: ~$8-10 spread Max Profit: $20 - cost = ~$10-12 per spread (100-120% ROI) Max Risk: Premium paid

Why This Works: If you think the LEAP seller is wrong and PLTR breaks out, this captures the move from $180 to $200. You're betting with the momentum and against the premium seller.

Risk Factors

For PLTR Bulls:

- Extreme Valuation: 415x P/E leaves zero room for error. Any miss = pain.

- Growth Deceleration: 2026 growth expected to slow to 35% from 53%

- Insider Selling: CEO Alex Karp has sold ~$2B in stock over two years

- Competition: Microsoft, AWS, Google all pushing enterprise AI hard

- Government Concentration: 55% of revenue from government - budget risk

For the LEAP Call Seller (Short Position):

- Breakout Risk: If AI narrative intensifies, $200 could fall fast

- Time Value: Two years is a long time - many catalysts ahead

- Assignment Risk: If stock surges, early assignment possible

- Unlimited Risk: If naked call, losses theoretically unlimited

Broader Market Risks:

- Interest rate uncertainty

- AI sector rotation

- Geopolitical events impacting defense spending

- Regulatory scrutiny on data/AI companies

The Bottom Line

Real talk: This $8.2M LEAP call sale tells us that at least one institutional player thinks PLTR's run is getting long in the tooth. They're collecting a massive premium betting the stock won't break $255 (strike + premium) over the next two years.

Here's the deal:

If You Own PLTR: Consider following this institutional playbook. Selling covered calls against your position generates income and provides some downside cushion. The $200 strike gives you plenty of room for upside while collecting premium.

If You're Watching PLTR: The $175-$180 range is the battleground. A break above $180 with volume could signal the next leg higher. A break below $175 opens the door to $165-$170. Q4 earnings on February 2nd will be the next major catalyst.

If You're Bearish: The premium seller is on your side. The extreme valuation, insider selling, and growth deceleration narrative all support the thesis that PLTR may consolidate here. But be warned - betting against momentum stocks can be painful.

Mark Your Calendar:

- February 2, 2026: Q4 Earnings - the next major volatility event

- March 20, 2026: Triple Witch - watch implied move levels

The Unusual Activity Verdict: This trade has a Z-score of 9.22 - meaning it's approximately 9 standard deviations above normal trading activity. For context, we see trades this size only a handful of times per year in PLTR. The institutional desk trade classification ($8.2M in a single order) confirms this is big money making a deliberate play.

Whether it's a sophisticated covered call strategy or a bold naked call sale, the message is the same: someone with deep pockets thinks the easy money in PLTR has been made.

Track PLTR: Ainvest PLTR Page

Monitor This Option: PLTR 2028-01-21 $200 Call Chart

Disclaimer: This analysis is for educational purposes only and does not constitute investment advice. Options trading involves significant risk and is not suitable for all investors. The unusual activity described represents institutional trading behavior that may not be appropriate for retail traders to replicate. Always do your own research and consider your risk tolerance before trading.