🐋 PLTR $23M Call Sweep - Institutional Bull Loading Up Before Earnings!

📅 January 28, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $23 MILLION on PLTR calls at 11:31:38 this morning! This whale bought 15,000 contracts of the $160 strike calls expiring March 20th - a massive bullish bet placed just 5 days before Q4 earnings on February 2nd. With PLTR trading at $162.43 and this call struck near the money, smart money is betting Palantir rips higher through earnings and beyond. Translation: An institutional player is paying $15.45 per share for the right to profit on any rally above $175 by March - and they're putting $23M behind that conviction.

📊 Company Overview

Palantir Technologies (PLTR) is an analytical software powerhouse that builds AI-powered platforms for governments and enterprises worldwide:

- Market Cap: $394.9 Billion

- Industry: Prepackaged Software Services

- Current Price: $162.43

- Primary Business: AI-powered data analytics platforms (Gotham for government, Foundry for commercial, AIP for generative AI)

- Key Clients: U.S. Army, U.S. Navy, major enterprises including Walgreens, AIG, American Airlines

- 52-Week Range: $66.12 - $207.52

💰 The Option Flow Breakdown

The Tape (January 28, 2026 @ 11:31:38):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:31:38 | PLTR | ASK | BUY | CALL $160 | 2026-03-20 | $23M | $160 | 15K | 19K | 15,000 | $162.43 | $15.45 |

🤓 What This Actually Means

This is an aggressive bullish bet on PLTR heading into earnings and beyond. Here's the breakdown:

- 💸 Massive premium paid: $23M ($15.45 per contract x 15,000 contracts)

- 🎯 Near-the-money strike: $160 is just 1.5% below the current price of $162.43 - this trader wants DELTA exposure immediately

- ⏰ Strategic timing: 51 days to expiration captures Q4 earnings (Feb 2), FY 2026 guidance, and any post-earnings momentum

- 📊 Size matters: 15,000 contracts represents 1.5 million shares worth ~$243M in notional exposure

- 🏦 Classified as BTO (Buy to Open): This is a NEW position, not closing an old one - fresh bullish conviction

- 📈 Volume vs OI: Volume of 15K against 19K open interest (Vol/OI ratio 0.789) - this is HIGH ACTIVITY, signaling a major new position

What's really happening here: This trader is making a leveraged bet that PLTR climbs significantly over the next 51 days. At $15.45 per share, the March $160 calls need PLTR above $175.45 to break even. That's roughly 8% higher from here. With earnings in 5 days and the stock already down ~19% from its November all-time high of $207.52, this player sees the pullback as a buying opportunity - not the start of something worse.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-Score: 4.86) - This lands in the "Extremely Unusual" classification with only 2 similar trades in recent history. The sheer dollar size ($23M) and contract count (15,000) on a single strike make this a standout institutional flow event.

📈 Technical Setup / Chart Check-Up

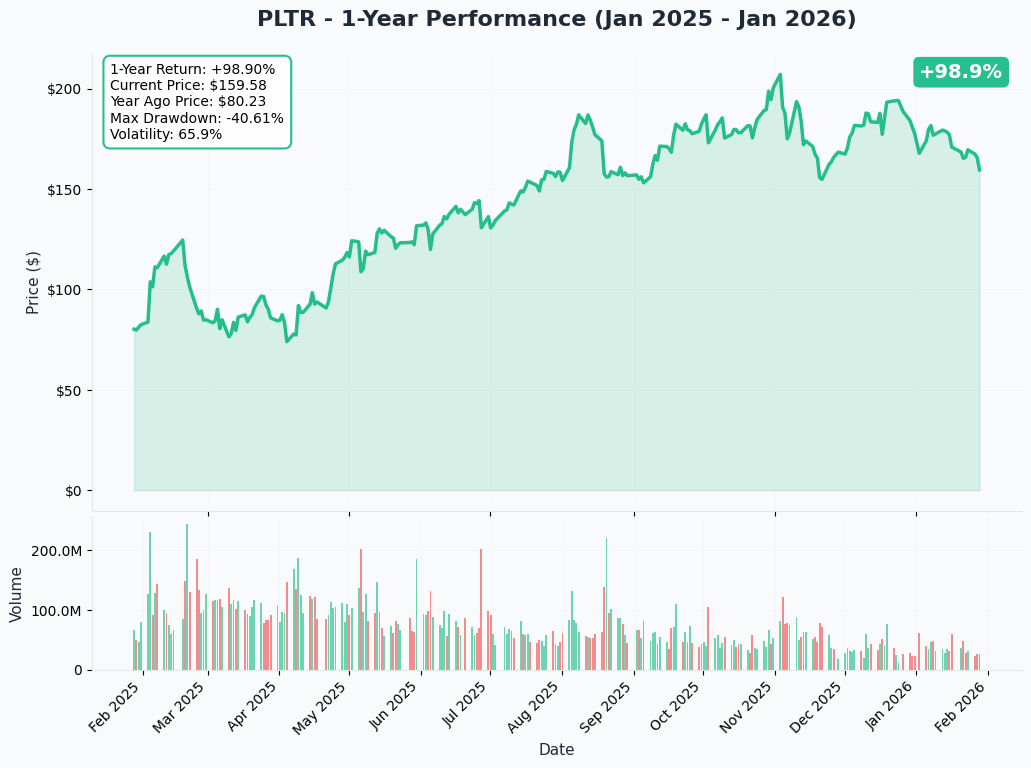

YTD Performance Chart

PLTR has been on an absolute tear over the past year - up +133.97% from $73.07 a year ago to current levels around $162. But the recent picture tells a more nuanced story. After rocketing to an all-time high of $207.52 on November 3, 2025 (the same day Q3 earnings crushed estimates), the stock has pulled back roughly 19-22%.

Key observations:

- 📈 Massive rally: From $66 lows to $207 in under a year on AI platform adoption and government mega-contracts

- 📉 Recent pullback: Down ~19% from ATH driven by DOGE spending concerns and profit-taking

- 🎢 High volatility name: PLTR can swing 5-10% on a single headline - this isn't a sleepy blue-chip

- 🐋 Insider selling: CEO Alex Karp and executives sold $205M+ in November 2025 shares (all under pre-planned 10b5-1 plans, but still notable)

- ⚠️ DOGE overhang: Stock slid ~25% on fears that Department of Government Efficiency reviews could cut defense spending

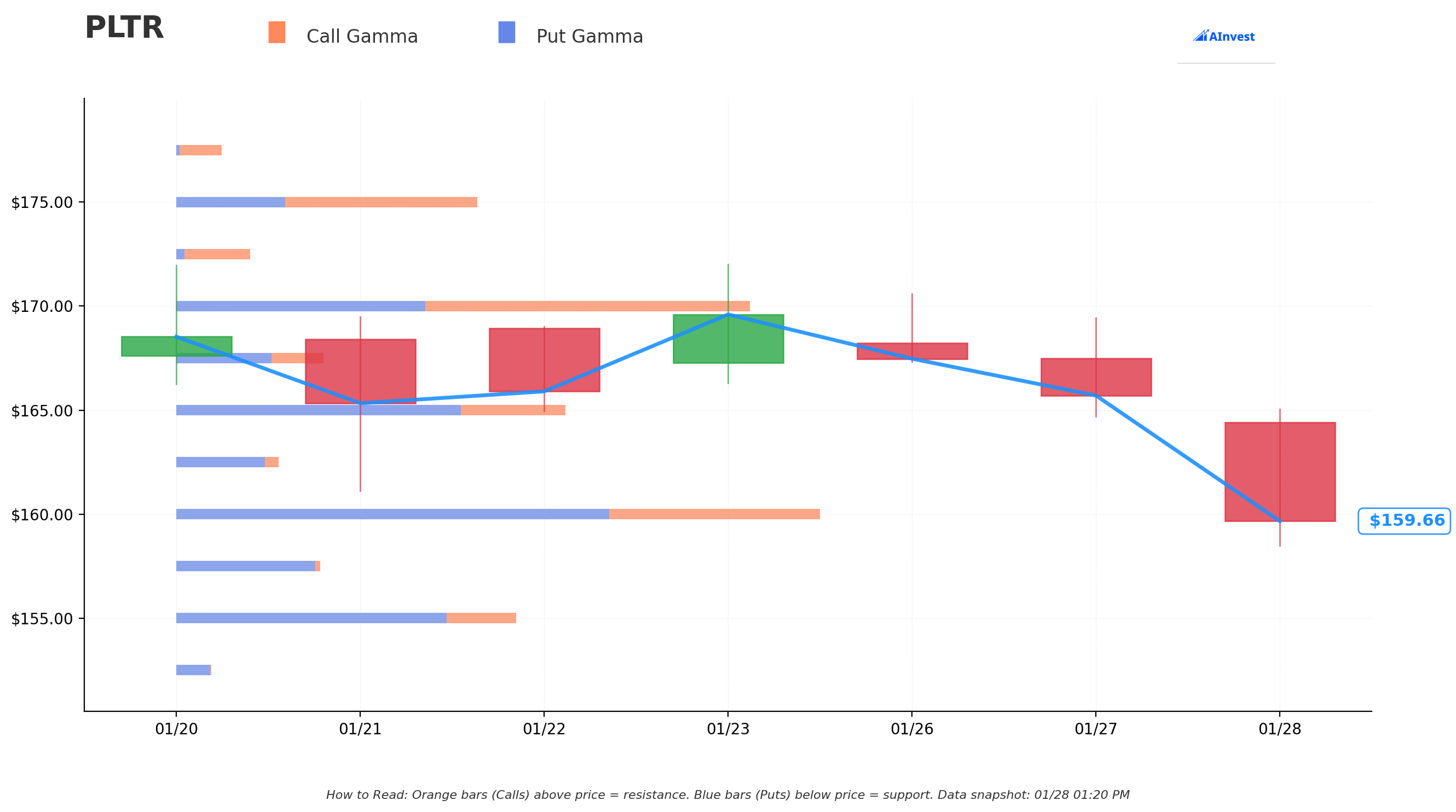

Gamma-Based Support & Resistance Analysis

Current Price: $159.43

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $155 - Strongest nearby support with 17.0B total gamma exposure (immediate floor if stock dips)

- $150 - Major structural support with 22.2B total gamma (highest put gamma below price - this is THE LINE IN THE SAND)

- $145 - Secondary support at 8.6B gamma (9% below current price)

- $140 - Deep support at 7.7B gamma (disaster floor, 12% below current price)

🟠 Resistance Levels (Call Gamma Above Price):

- $160 - Immediate resistance with 31.8B total gamma (STRONGEST SINGLE LEVEL - exactly where this call trade is struck!)

- $165 - Secondary ceiling at 19.0B gamma (3.5% above current)

- $170 - Major resistance at 27.7B gamma (6.6% above, call gamma begins to dominate)

- $175 - Resistance at 14.7B gamma (roughly the breakeven for this $23M trade)

- $180 - Extended resistance at 19.8B gamma (12.9% above current)

- $190 - Distant target at 9.0B gamma (19.2% above current)

What this means for traders: PLTR is sitting right at the $160 gamma magnet - the single largest gamma level on the board at 31.8B. This creates a tug-of-war zone where market makers hold enormous positions. Below $160, the stock could slide toward $155 and $150 gamma support. Above $160, the path to $170 opens up where call gamma starts dominating.

Notice anything? The call buyer struck EXACTLY at $160 - the highest-gamma strike on the entire board. This isn't coincidental. They're buying right at the inflection point where a breakout above $160 would trigger dealer hedging flows that push the stock HIGHER. Smart positioning.

Net GEX Bias: Bearish (124.1B call gamma vs 157.1B put gamma) - Overall positioning leans bearish, which means dealers are likely short gamma. This creates conditions where moves in EITHER direction get amplified. If earnings are strong and PLTR pushes above $170, the negative gamma positioning could force dealers to buy aggressively, accelerating the rally.

Implied Move Analysis

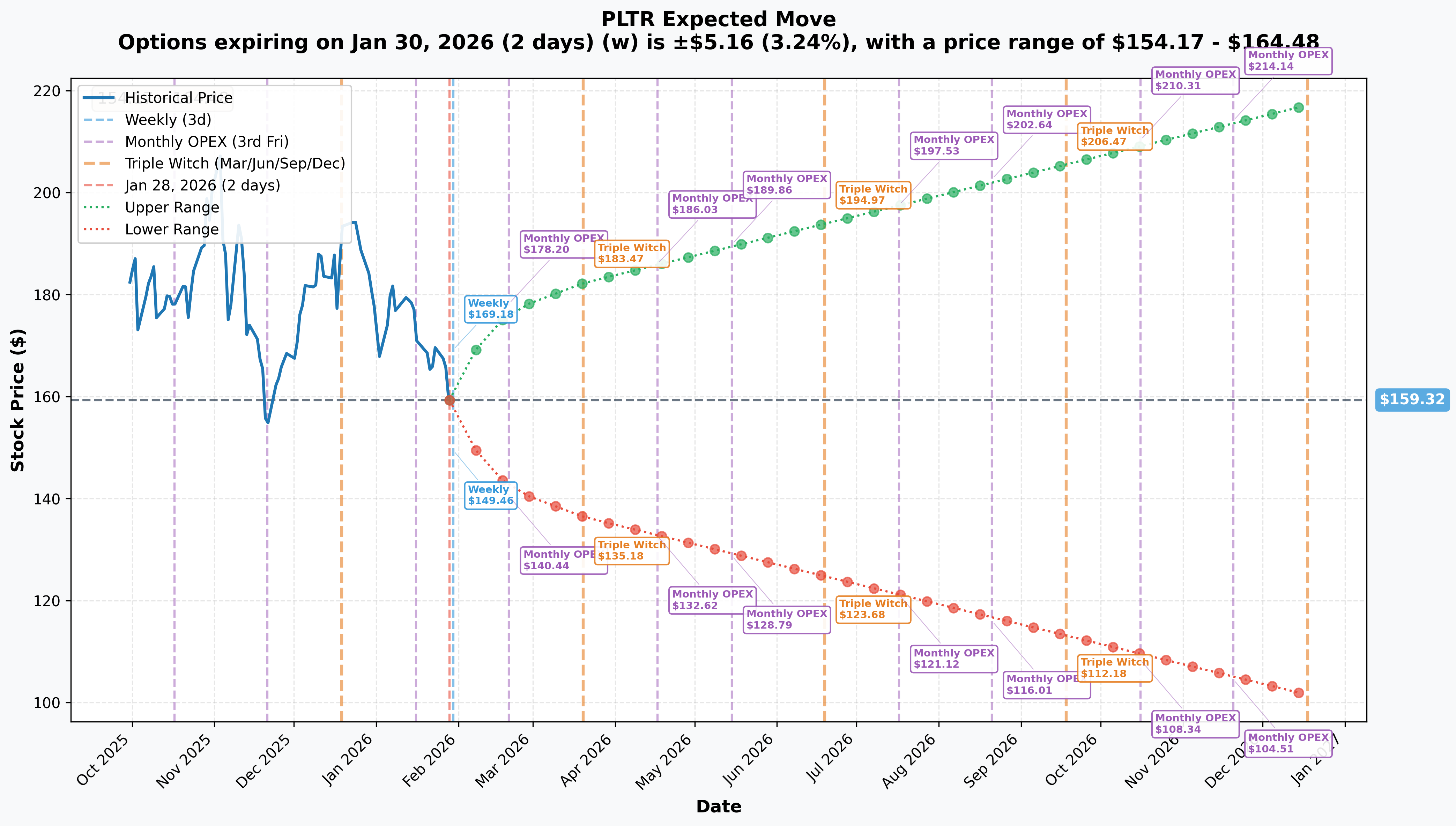

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 30 - 2 days): +/-$5.16 (+/-3.24%) -> Range: $154.17 - $164.48

- 📅 Monthly OPEX (Feb 20 - 23 days): +/-$17.51 (+/-10.99%) -> Range: $141.81 - $176.83

- 📅 Quarterly Triple Witch (Mar 20 - 51 days - THIS TRADE!): +/-$22.99 (+/-14.43%) -> Range: $136.33 - $182.32

- 📅 Yearly LEAPS (Dec 18 - 324 days): +/-$57.88 (+/-36.33%) -> Range: $101.44 - $217.21

Translation for regular folks: Options traders are pricing in a 3.2% move ($5) over the next 2 days, but a HUGE 11% move ($17.50) through February OPEX which includes earnings on February 2nd. The market expects BIG moves around this report - that's a massive implied swing for a nearly $400B company!

The March 20th expiration (when this $23M trade expires) has an upper range of $182.32, meaning the market thinks PLTR could realistically trade up to $182 over the next 51 days. The call buyer's breakeven of $175.45 sits comfortably WITHIN this implied range - the market agrees this target is achievable.

Key insight: The implied move of +/-14.4% through March tells us the options market is pricing in sustained volatility well beyond just the earnings event. The buyer of these calls is positioned to capture the full post-earnings rally AND any additional catalyst from FY 2026 guidance or government contract announcements.

🎪 Catalysts

🔥 Immediate Catalysts (Next 7 Days)

Q4 2025 Earnings - February 2, 2026 (5 DAYS AWAY!) 📊

PLTR reports fiscal Q4 results on Monday, February 2, 2026 after market close. This is THE catalyst that could send these calls to the moon or crush them. Wall Street consensus:

- 📊 Revenue: $1.34B (+62% YoY) - company guided $1.327B-$1.331B

- 💰 Adjusted EPS: $0.23 (+64.3% YoY) vs $0.14 last year

- 💰 GAAP EPS: $0.17 (+1,800% YoY from break-even)

- 🤖 U.S. Commercial Revenue: Can the 121% YoY growth pace from Q3 sustain?

- 📈 Customer Count: 45% YoY growth in Q3 - acceleration or deceleration?

- 🎯 FY 2026 Guidance: THIS IS THE BIG ONE. Analysts project ~35% revenue growth deceleration from 53% in 2025 - any beat here could send stock flying

Upside surprise potential: Citi upgraded PLTR to Buy on January 12 with a $235 price target, with analyst Tyler Radke predicting revenue could increase up to 80% before year-end. The AIP bootcamp conversion rates and remaining deal value ($8.6B in Q3, +91% YoY) could deliver outsized upside if momentum continues.

Downside risk factors: At 391x trailing P/E, even a slight miss or conservative FY 2026 outlook could trigger a violent selloff. The stock has already shown it can drop 25% on sentiment shifts (DOGE fears). Growth deceleration from 63% to sub-40% could spook growth investors.

Historical precedent: Q3 2025 earnings (Nov 3) sent the stock to an ATH of $207.52 - the stock initially surged before giving back gains over the following weeks. PLTR has a pattern of post-earnings volatility that extends well beyond the initial reaction.

🚀 Near-Term Catalysts (Q1-Q2 2026)

DOGE Clarification - POTENTIAL POSITIVE 🇺🇸

The stock dropped ~25% from ATH on fears that Department of Government Efficiency reviews would cut defense spending. But recent developments suggest the opposite:

- 🛡️ Defense Secretary Pete Hegseth clarified DOD's $5.1B DOGE cuts target "ancillary things like consulting" - NOT mission-critical AI platforms like Palantir

- 🤖 Palantir rumored to be a PRIMARY vendor for DOGE's own efficiency initiative, helping automate administrative roles across IRS and State Department

- 💰 Federal contract value nearly doubled from $541.2M (2024) to $970.5M (2025) - trajectory expected to continue

Why this matters for the call trade: If management provides DOGE clarity on the earnings call and reveals Palantir is actually BENEFITING from efficiency reviews, the 19% drawdown from ATH could reverse rapidly. The March $160 calls have 51 days to capture this narrative shift.

$10B U.S. Army Enterprise Agreement Ramp 🏛️

PLTR's $10 billion Army software and data contract, secured in August 2025, is beginning to generate incremental revenue:

- 🎯 10-year contract term creates massive revenue visibility and switching cost barrier

- 💪 Validates PLTR as THE enterprise AI platform for U.S. defense

- 📈 Q4 call should provide first substantive update on deployment progress and revenue recognition

- 🔒 Creates institutional lock-in: once the Army is on Palantir, they're not switching

U.S. Navy ShipOS Program ($448M) 🚢

Authorized up to $448M to deploy Palantir Foundry and AIP across the Maritime Industrial Base:

- 🏭 Initial rollout targeting the Submarine Industrial Base

- ⚡ Pilot results: submarine schedule planning reduced from 160 manual hours to under 10 minutes

- 🚀 Expected to scale beyond submarines - could become much larger than initial $448M scope

Accenture Partnership & AIP Expansion 🤝

- 🤝 Accenture formed the Accenture Palantir Business Group for advanced AI and data solutions

- 💼 PwC UK multi-year, multi-million-pound investment combining Foundry/AIP with PwC sector expertise

- 📊 Over 1,300 AIP bootcamps completed with accelerating conversion rates

- 🔗 AIP now runs natively on Snowflake's Data Cloud - expanding addressable market

AIPCon 9 (Expected H1 2026) 📣

Palantir has held AIPCon events roughly quarterly, with AIPCon 8 in September 2025. The next event is expected H1 2026 and typically features 70+ new customer use cases - historically a stock-moving catalyst.

⚠️ Risk Catalysts (Negative)

Extreme Valuation Leaves Zero Room for Error 📊

At 391x trailing P/E and ~102x P/S, PLTR trades at multiples that dwarf even the most aggressive growth names:

- ⚖️ Snowflake trades at ~20x P/S, CrowdStrike at ~29x P/S - PLTR at ~102x is in a league of its own

- 💸 Priced for a DECADE of flawless execution

- 📉 Any growth deceleration below expectations could trigger violent multiple compression

- 🐻 Michael Burry has disclosed a bearish position worth $912M against PLTR

Insider Selling Continues 💼

CEO Alex Karp: 41 sells, 0 buys over past 5 years. In November 2025 alone, 5 senior officers filed to sell 1.26M+ shares worth $205M+. While all under pre-planned 10b5-1 trading plans, the persistent one-directional flow is hard to ignore.

Growth Deceleration Expected 📉

Analysts project deceleration from 53% (2025) to ~35% (2026). The law of large numbers is real - sustaining 60%+ growth on a $4.4B revenue base becomes increasingly difficult. If deceleration exceeds expectations, the momentum premium could evaporate.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20th expiration:

📈 Bull Case (30% probability)

Target: $180-$200

How we get there:

- 💪 Q4 earnings CRUSH expectations with revenue above $1.35B and FY 2026 guidance showing 45%+ growth (beating the ~35% consensus)

- 🇺🇸 Management reveals PLTR is a DOGE vendor, flipping the narrative from headwind to tailwind

- 🤖 U.S. commercial revenue growth sustains above 100% YoY - AIP bootcamp conversions accelerating

- 📊 Remaining deal value surges past $10B (was $8.6B in Q3) confirming enterprise adoption

- 🚀 Breakout above $170 gamma resistance triggers dealer hedging flows, pushing stock toward $180 (implied move upper range: $182.32)

- 📈 Citi's $235 target gains consensus support as more analysts upgrade

Key metrics needed:

- Revenue beat of 3%+ above consensus ($1.38B+)

- FY 2026 guidance at 40%+ growth (vs ~35% consensus)

- U.S. commercial growth sustaining 100%+ pace

- DOGE commentary definitively positive

Call P&L in Bull Case:

- Stock at $180 by Mar 20: Calls worth $20.00, profit = $4.55/share x 15,000 = $6.8M gain (30% ROI)

- Stock at $190 by Mar 20: Calls worth $30.00, profit = $14.55/share x 15,000 = $21.8M gain (95% ROI)

- Stock at $200 by Mar 20: Calls worth $40.00, profit = $24.55/share x 15,000 = $36.8M gain (160% ROI!)

Probability assessment: 30% because PLTR has a PROVEN history of crushing earnings estimates (Q3 beat revenue consensus by 8.3%, EPS by 23.5%), and the 19% pullback from ATH provides room for a snap-back rally. The negative gamma positioning means moves higher would be amplified.

🎯 Base Case (45% probability)

Target: $155-$175 range (POST-EARNINGS CHOP)

Most likely scenario:

- ✅ Solid Q4 earnings meeting or slightly beating consensus (~$1.33-1.35B revenue, $0.22-0.24 EPS)

- 📱 FY 2026 guidance in-line with expectations (~35% growth) - neither exciting nor disappointing

- ⚖️ DOGE commentary cautiously optimistic but no bombshell revelations

- 🤖 AIP momentum continues but growth rate naturally decelerating from 121% pace

- 🔄 Stock trades between $155 gamma support and $170 gamma resistance for weeks

- 💤 Volatility crush post-earnings as implied vol drops from elevated levels

- 📊 Market digests the 19% pullback, waits for next catalyst (AIPCon 9 or Q1 2026 results)

This is the call buyer's acceptable scenario: Stock consolidates in $160-175 range, calls retain some value from time premium and any slight upside move. Not a home run, but not a total loss either.

Why 45% probability: PLTR's fundamentals remain strong (63% growth, $4B cash, expanding margins), but the extreme valuation and growth deceleration narrative create a ceiling on multiple expansion. Post-earnings chop is the most common outcome for high-multiple growth stocks.

📉 Bear Case (25% probability)

Target: $130-$150 (VALUATION RECKONING)

What could go wrong:

- 😰 Earnings miss or FY 2026 guidance disappoints - even guiding 30% growth (vs 35% consensus) could trigger -15% gap down at this valuation

- 🚨 DOGE actually DOES cut Palantir contracts or creates uncertainty around government revenue pipeline

- 💼 More insider selling announced, spooking retail investors who are heavy in the name

- 🇨🇳 Broader tech selloff on macro fears drags high-multiple names lower

- 📊 Growth deceleration sharper than expected - U.S. commercial growth falls below 80% YoY

- 🐻 Michael Burry's $912M bearish position proves prescient

- 🔨 Break below $150 gamma support triggers cascade to $145, then $140

Critical support levels:

- 🛡️ $155: Strongest nearby gamma floor (17.0B) - first line of defense

- 🛡️ $150: Major gamma wall (22.2B) - MUST HOLD or momentum goes negative

- 🛡️ $145: Secondary floor (8.6B gamma)

- 🛡️ $140: Deep support (7.7B gamma) - break here and implied move targets $136

Probability assessment: 25% because it requires meaningful negative catalysts. PLTR's business momentum is genuinely strong (Q3 crushed estimates), but the extreme valuation means even minor disappointments get punished harshly. The implied move lower range of $136.33 by March 20th shows the market sees this as a real possibility.

Call P&L in Bear Case:

- Stock at $150 by Mar 20: Calls worth ~$3-5, loss = $10-12/share x 15,000 = $15-18M loss (65-78%)

- Stock at $140 by Mar 20: Calls worth ~$0.50-1, loss = ~$14.50/share x 15,000 = $21.7M loss (94%)

- Stock at $130 by Mar 20: Calls essentially worthless, loss = ~$23M (100% loss)

💡 Trading Ideas

🛡️ Conservative: Wait for Earnings, Buy the Dip

Play: Stay on the sidelines until after February 2nd earnings, then look for entry on pullback to $150-155 gamma support

Why this works:

- ⏰ Earnings in 5 days creates binary event risk with +/-11% implied move - too unpredictable

- 💸 Implied volatility elevated pre-earnings - options are EXPENSIVE right now

- 📊 At 391x trailing P/E, even a solid beat might get "sell the news" treatment

- 🎯 $150-155 gamma support zone offers 5-8% margin of safety vs current price

- 📉 Stock already dropped 19% from ATH - could easily dip further before finding a floor

- 🤔 The 19% pullback suggests market is already nervous - why rush in?

Action plan:

- 👀 Watch Monday's earnings closely for revenue ($1.34B+ needed), FY 2026 guidance (40%+ growth would be bullish), and DOGE commentary

- 🎯 If stock pulls back to $150-155 post-earnings, consider buying shares or March/April calls

- ✅ Need to see: FY 2026 guidance, AIP conversion metrics, DOGE clarity before committing capital

- 📊 Monitor unusual options activity after earnings - if institutions add MORE calls, follow the flow

- ⏰ If earnings are strong and stock gaps above $170, wait for consolidation before chasing

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -10-20% drawdown if earnings disappoint. Get better entry at gamma support levels. Maintain optionality.

⚖️ Balanced: Post-Earnings Bull Call Spread

Play: After earnings settle, buy a call spread targeting the implied move upper range

Structure: Buy $170 calls, Sell $190 calls (March 20 expiration - SAME as the $23M trade)

Why this works:

- 🎢 IV crush after earnings makes call spreads much cheaper - buy AFTER volatility drops

- 📊 Defined risk spread ($20 wide = $2,000 max risk per spread)

- 🎯 Targets $170-$190 gamma resistance zone where the breakout would generate momentum

- 🤝 Aligns with the institutional call buyer's thesis but at better post-IV-crush prices

- ⏰ 49 days to expiration (post-earnings entry) gives time for catalysts to play out

- 🛡️ Capped risk means you know your max loss going in

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Pay ~$5-7 net debit per spread post-earnings

- 📈 Max profit: $13-15 if PLTR above $190 at March expiration

- 📉 Max loss: $5-7 (your debit paid)

- 🎯 Breakeven: ~$175-177

- 📊 Risk/Reward: ~2:1 which is attractive for defined-risk bullish play

Entry timing:

- ⏰ Wait 1-2 days post-earnings (by Feb 3-4) for IV to settle

- 🎯 Only enter if earnings are solid AND stock holds above $155 support

- ❌ Skip if stock drops below $150 (thesis broken, gamma support failed)

- ✅ Best entry: Stock pulls back to $158-165 range post-earnings with strong guidance

Position sizing: Risk only 3-5% of portfolio (this is directional speculation with binary earnings risk behind you)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Pre-Earnings Momentum Play (ADVANCED ONLY!)

Play: Buy short-dated calls betting on pre-earnings run-up and post-earnings pop

Structure: Buy $165 calls (March 20 expiration - mirroring the whale)

Why this could work:

- 🐋 A $23M institutional call buyer just showed their hand - big money is bullish into earnings

- 💥 PLTR crushed Q3 by 8.3% on revenue and 23.5% on EPS - history of beats

- 📊 Stock down 19% from ATH creates "buy the dip" setup if earnings confirm the growth story

- 🇺🇸 DOGE narrative could flip from negative to positive overnight with one management comment

- ⚡ Negative gamma positioning means a rally above $170 could ACCELERATE as dealers chase

- 📈 Citi's $235 target represents 45% upside from current levels

- 🎯 Implied move upper range of $182 makes $165 calls attractive with room to run

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: IV is elevated pre-earnings - you're paying a premium for premium

- ⏰ BINARY EVENT: Earnings could gap stock -15% on any miss or weak guidance

- 😱 IV CRUSH: Even if stock moves up 5-7%, IV collapse could still reduce call value

- 📊 391x P/E: This is the most expensive large-cap stock in the market - priced for perfection

- 💼 Insider selling: Management has sold $200M+ recently - what do they know?

- 🐻 Michael Burry is short: The "Big Short" guy has a $912M bearish position

Estimated P&L:

- 💰 Cost: ~$13-15 per call (March 20 $165 strikes)

- 📈 Profit scenario: Stock rallies to $185 post-earnings = call worth ~$20-22 (40-50% gain)

- 🚀 Home run: Stock reclaims $200+ on blowout guidance = call worth $35+ (140%+ gain)

- 📉 Loss scenario: Stock flat to slightly down at $155-160 = call worth $5-8 (40-60% loss)

- 💀 Total loss: Stock crashes to $140 = call nearly worthless (90-100% loss)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded options through earnings before and understand IV crush

- ✅ Can afford to lose the ENTIRE premium

- ✅ Understand you're betting on the most expensive stock in the market by P/E

- ✅ Can monitor position Tuesday morning post-earnings and act quickly

- ✅ Accept that 391x P/E means the bar for a positive reaction is EXTREMELY high

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35-40% (earnings binary risk + IV crush make this a high-risk play)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Earnings binary event in 5 days: Results Monday February 2nd after close create MASSIVE volatility risk. Stock could gap 10-15% either direction. At 391x trailing P/E, the bar for a positive reaction is astronomically high. Even a GOOD quarter might get "sell the news" treatment given the stock's run from $66 to $207 in under a year. Options pricing +/-11% implied move through February OPEX.

-

💸 Most expensive large-cap in the market: At 391x trailing P/E and ~102x price-to-sales, PLTR trades at multiples that make even the most optimistic analyst uncomfortable. For context, Snowflake trades at ~20x P/S and CrowdStrike at ~29x P/S. PLTR is priced for a decade of flawless 40%+ growth execution. Any stumble gets punished HARD at these multiples.

-

🇺🇸 DOGE is a double-edged sword: While Palantir may benefit as a DOGE vendor, the program has already caused a 25% drop from ATH on defense spending fears. Over 50% of PLTR's revenue comes from U.S. government contracts. Any actual cuts to defense AI budgets would be catastrophic. The clarification from Defense Secretary Hegseth helps, but uncertainty persists.

-

💼 Insider selling at unprecedented scale: CEO Alex Karp has made 41 transactions over 5 years: 0 buys, 41 sells. In November 2025, 5 executives filed to sell $205M+ combined. Karp sold $1.88B in 2024 alone. All under pre-planned 10b5-1 plans, but the sheer volume of one-directional selling raises questions about management's confidence in current valuation.

-

📉 Growth deceleration is coming: Analysts project deceleration from 53% (2025) to ~35% (2026) to 25-30% (2027). The law of large numbers makes sustaining 60%+ growth on $4.4B revenue increasingly difficult. If FY 2026 guidance shows sharper deceleration than expected, the momentum premium could collapse overnight.

-

🐻 Michael Burry has a $912M short: The "Big Short" investor who called the 2008 housing crisis has disclosed a massive bearish position against PLTR. While being short a momentum stock is dangerous, Burry's track record on valuation calls is noteworthy. His thesis likely centers on the extreme multiple eventually compressing.

-

⚖️ Hyperscaler competition intensifying: Microsoft Azure AI, AWS, and Google Cloud are building comparable capabilities with larger R&D budgets. Salesforce launched Missionforce targeting government as a cheaper alternative. While Palantir's Ontology layer and government clearances provide differentiation, the moat is narrowing as Big Tech pours billions into enterprise AI.

-

🎢 Retail investor concentration amplifies moves: Heavy retail participation means sentiment drives price more than fundamentals. This creates explosive moves in both directions - great when momentum is positive, devastating when it turns. The 19% drawdown from ATH shows how quickly retail can panic.

-

📊 Negative gamma means amplified moves: With net GEX bias bearish (put gamma exceeding call gamma by 33B), dealers are positioned to amplify moves in BOTH directions. If earnings disappoint, the downside move could be sharper than expected as dealers sell into weakness to hedge.

🎯 The Bottom Line

Real talk: Someone just bet $23 MILLION that PLTR rallies through earnings and beyond, buying 15,000 March $160 calls five days before the most important earnings report of the year. This isn't a hedge - it's a CONVICTION BUY. They're paying $15.45/share for 51 days of upside exposure, needing PLTR above $175.45 to break even. That's an 8% rally from here.

What this trade tells us:

- 🎯 An institutional player sees the 19% pullback from ATH as a buying opportunity, not a warning sign

- 💰 They're willing to risk $23M that Q4 earnings and FY 2026 guidance will be strong enough to reverse the DOGE-driven selloff

- ⚖️ Struck at $160 - RIGHT at the highest gamma level on the board - positioning for a breakout where dealer hedging flows accelerate the move higher

- ⏰ March 20th expiration gives 51 days to capture earnings reaction, guidance revision cycle, and any DOGE clarification

- 📊 The Z-score of 4.86 (Extremely Unusual) with only 2 similar trades recently means this is serious institutional conviction, not routine positioning

This IS a strong bullish signal - but at 391x P/E, conviction alone doesn't make it safe.

If you own PLTR:

- ✅ This trade validates your thesis - institutional money is buying the dip alongside you

- 📊 Key levels to watch: $155 support (if broken, consider trimming) and $170 resistance (if cleared, momentum accelerates)

- ⏰ Earnings on Feb 2 is make-or-break - have a plan BEFORE results drop

- 🛡️ Consider trimming 15-25% if you're sitting on massive gains from below $100 - locking in profits is smart, not bearish

- 🎯 If earnings beat AND stock breaks $170, hold tight - next stop could be $180-190

If you're watching from sidelines:

- ⏰ Monday February 2nd after close is the moment of truth - exercise extreme caution entering before earnings

- 🎯 Post-earnings pullback to $150-155 gamma support would be a SOLID entry point (5-8% below current)

- 📈 Looking for confirmation of: FY 2026 guidance at 40%+ growth, DOGE clarity, U.S. commercial acceleration

- 🚀 The $23M call buy gives you confidence that smart money sees upside - but wait for earnings to reduce binary risk

- ⚠️ At 391x P/E, you MUST be comfortable with 20-30% drawdowns as part of owning this name

If you're bearish:

- 🎯 DO NOT short into a $23M institutional call buy 5 days before earnings - fighting this flow is dangerous

- 📊 If earnings disappoint, watch for break below $150 gamma wall - that's your confirmation to play downside

- ⚠️ Post-earnings put spreads ($155/$140 or $150/$135) offer defined-risk way to play bearish thesis after IV crush

- 📉 Break below $150 could trigger cascade to $140, then implied move target of $136

- ⏰ Let earnings play out first - premature bearish positioning risks getting steamrolled by a blowout quarter

Mark your calendar - Key dates:

- 📅 January 30 (Friday) - Weekly OPEX, +/-3.24% implied move window

- 📅 February 2 (Monday) after market close - Q4 FY2025 earnings report (5 DAYS!)

- 📅 February 3 (Tuesday) - Post-earnings price action and analyst reactions

- 📅 February 20 - Monthly OPEX (+/-11% implied move window closes)

- 📅 March 20 - Quarterly Triple Witch - EXPIRATION of this $23M call trade (+/-14.4% implied move)

- 📅 H1 2026 (TBD) - AIPCon 9 expected

- 📅 May 2026 (Est.) - Q1 2026 earnings report

Final verdict: PLTR's business momentum is undeniably strong - 63% revenue growth, 121% U.S. commercial growth, a $10B Army contract, and expanding commercial partnerships. The $23M institutional call buy confirms smart money sees the 19% pullback as opportunity. BUT, at 391x P/E, this is the most valuation-sensitive stock in the market. Earnings need to be EXCEPTIONAL, not just good. The Citi upgrade to $235 provides a bull case framework, but analyst consensus at $184-193 suggests limited near-term upside at current prices.

The smart play: Let earnings clear, watch the reaction, and position accordingly. If PLTR delivers AND the stock holds above $160, the March calls could pay off handsomely. If it stumbles, $150 gamma support gives you a much better entry. Either way, having a plan beats hoping for the best.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 4.86 reflects this specific trade's unusual size relative to recent PLTR history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 10-15% gaps either direction. At 391x trailing P/E, PLTR carries extreme valuation risk that could result in significant losses even on fundamentally sound results.

About Palantir Technologies: Palantir Technologies is an analytical software company that builds AI-powered platforms for governments and commercial enterprises, helping organizations integrate, manage, and analyze data to make better operational decisions, with a market cap of $394.9 billion in the Prepackaged Software Services industry.