PLTR $18.4M Call Sell - Someone Just Cashed Out Massive Premium 3 Days Before Earnings

January 30, 2026 | Unusual Activity Detected

The Quick Take

Someone just sold $18.4 MILLION worth of PLTR calls in two rapid-fire trades this morning! Two blocks totaling 22,400 contracts of the $150 strike calls expiring March 20th hit the tape within 26 seconds -- both sold on the bid, both Sell to Open (brand new short positions). With Palantir reporting Q4 2025 earnings on Monday February 2nd (just 3 days away), this institutional seller is collecting a mountain of premium while capping their upside right at the $150 resistance wall. The z-score on this activity is extremely elevated -- volume was 2.07x the open interest. This is a high-conviction bet that PLTR stays below $150 through March.

Company Overview

Palantir Technologies Inc (PLTR) is the AI and big data analytics powerhouse serving both government and commercial clients:

- Market Cap: $361.9 Billion

- Industry: Software - Prepackaged Software

- Current Price: ~$147.16

- Primary Business: Three core platforms -- Gotham (defense/intelligence), Foundry (commercial enterprise data integration), and AIP (AI Platform) -- serving the U.S. military, intelligence community, NATO allies, and a rapidly growing roster of commercial enterprises across healthcare, finance, energy, and manufacturing

- CEO: Alex Karp | Founded: 2003 | Employees: ~3,800+

- Index Membership: S&P 500 (added Sept 2024), Nasdaq 100 (added Dec 2024)

The Option Flow Breakdown

The Tape (January 30, 2026):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:39:29 | PLTR | BID | SELL | CALL $150 | 2026-03-20 | $9.2M | $150 | 15K | 5.4K | 7,165 | $149.62 | $12.85 | PLTR20260320C150 |

| 10:39:03 | PLTR | BID | SELL | CALL $150 | 2026-03-20 | $9.2M | $150 | 7.4K | 5.4K | 7,165 | $149.55 | $12.80 | PLTR20260320C150 |

What This Actually Means

This is a bearish-to-neutral income play -- someone opening brand new short call positions to collect premium. Here is what stands out:

- Total premium collected: $18.4M ($12.85 + $12.80 average x 22,400 total contracts)

- Both trades hit the BID: Selling on the bid means the seller wanted to get filled fast -- they were not waiting around for a better price. That is aggressive.

- Sell to Open (STO): These are NEW short positions, not someone closing a long. This seller is opening fresh exposure heading into earnings.

- Strike selection: $150 is right at the stock price ($149.55-$149.62 spot) -- this is an at-the-money call sale

- Breakeven at expiration: $162.83 ($150 strike + $12.83 avg premium) -- PLTR needs to rally 9% past the strike before the seller starts losing money

- Volume vs Open Interest: 22,400 contracts traded against just 5,400 OI -- that is a 2.07x ratio, which is extremely unusual

- Expiration: March 20 quarterly OPEX gives 49 calendar days -- this covers earnings AND the full Q1 2026 trading window

What is really happening here:

There are two likely scenarios for this trade:

Scenario 1 -- Covered Call Writing (Most Likely): A large institutional holder of PLTR stock is writing calls against their position to collect $18.4M in premium ahead of earnings. At 368x P/E and trading at roughly 104x sales, PLTR is priced for perfection. This seller may believe the stock is range-bound or vulnerable to a post-earnings pullback, and they are happy to cap their upside at ~$163 in exchange for $18.4M in cash. If PLTR drops after earnings, the premium cushions the blow. Smart money income generation.

Scenario 2 -- Naked Call Selling (More Aggressive): If this is a naked short, the seller is making a directional bet that PLTR will NOT rally meaningfully above $150 through March. Given the stock is down ~24% from its November highs and insiders have been dumping shares aggressively, this seller may be betting the earnings report -- even if good -- is already priced in at these valuations.

Either way, the message is the same: someone with deep pockets does not think PLTR is going meaningfully higher for the next 49 days.

The BID-side execution on both trades (26 seconds apart) confirms this is institutional. Retail traders do not sell 22,400 contracts in two clips. This is a professional desk executing a planned strategy.

Technical Setup / Chart Check-Up

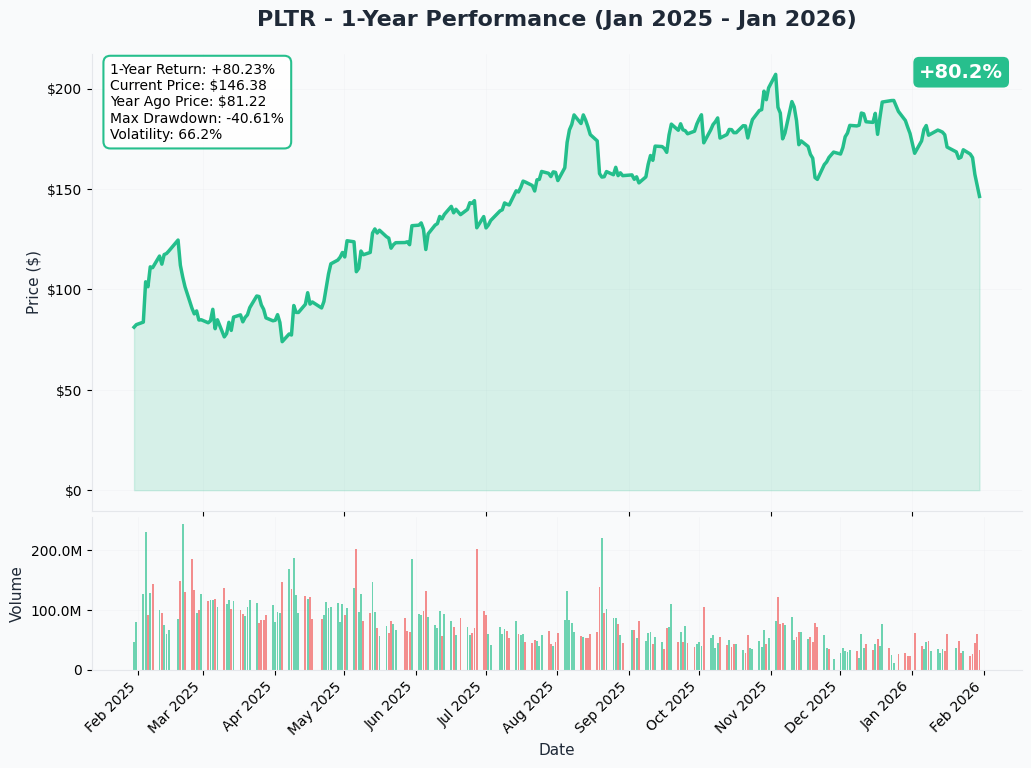

One Calendar Year Chart

PLTR is sitting at ~$147, down roughly 17% YTD from its December 31 close of ~$177.75 and down ~24% from the November 2025 all-time high of $207.52. Despite the recent pullback, the stock is still up massively from its 52-week low of $66.12.

Key observations:

- Massive 2025 rally fading: PLTR surged 135% in 2025 but has given back a significant chunk to start 2026

- 52-week range: $66.12 to $207.52 -- currently trading in the upper-middle of that range

- Below-average volume: 25.41M shares on Jan 29 vs. 36.17M average -- the selling pressure has moderated but buying conviction is also thin heading into earnings

- Key psychological level: $150 is both a round number and the call strike -- expect this level to act as a magnet

- Post-ATH distribution: The pullback from $207 to $147 looks like classic distribution after an extended rally

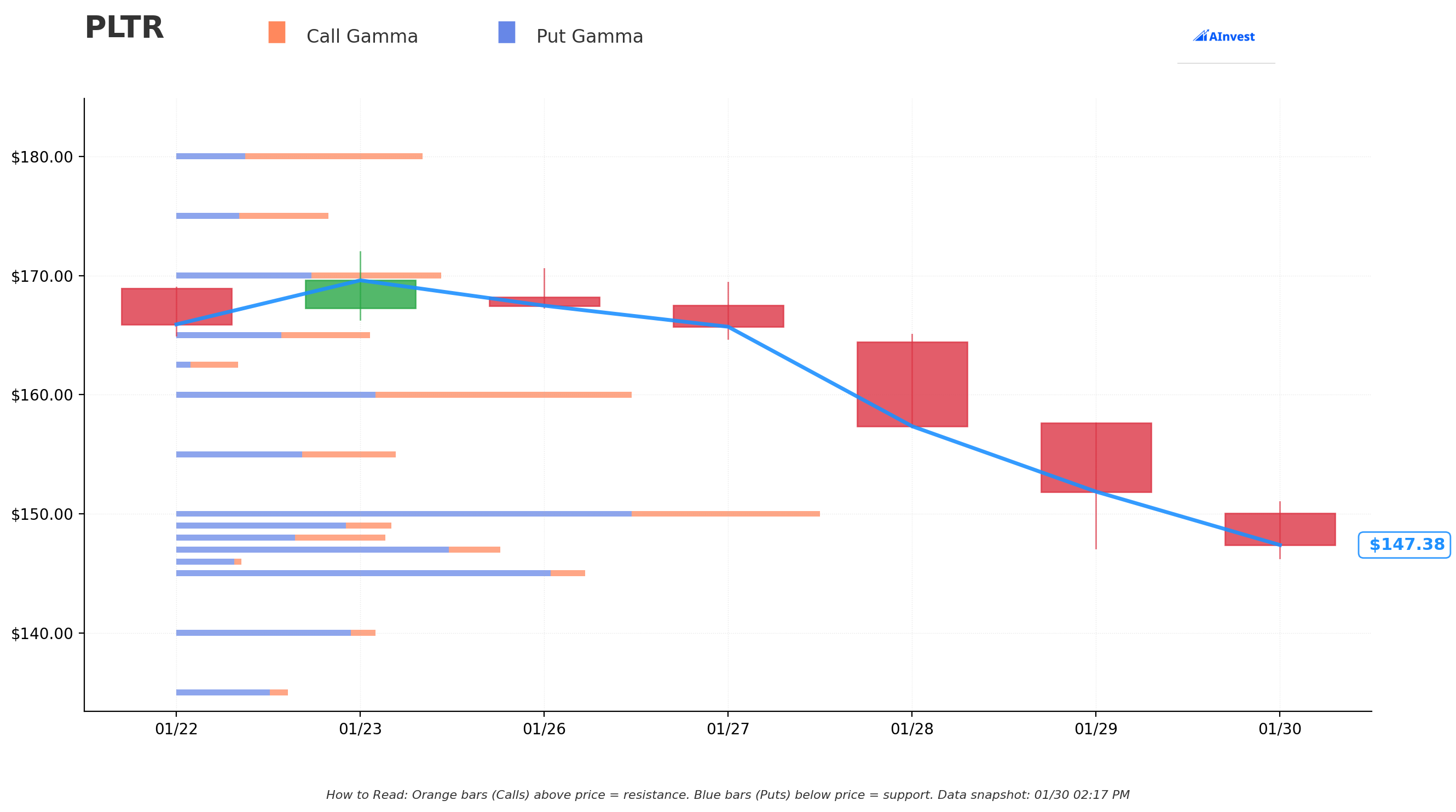

Gamma-Based Support & Resistance Analysis

Current Price: $147.16

The gamma exposure map reveals where market maker hedging flows will create natural price barriers:

Support Levels (Below Price):

- $147 - Immediate support (gamma: 21) -- first line of defense

- $145 - Strongest support level (gamma: 27) -- this is the key floor to watch

- $140 - Secondary support (gamma: 12) -- deeper pullback target

Resistance Levels (Above Price):

- $148 - Near-term resistance (gamma: 12)

- $149 - Additional overhead (gamma: 11)

- $150 - THE STRIKE and strongest resistance (gamma: 35) -- this is a wall

- $155 - Mid-range resistance (gamma: 13)

- $160 - Major resistance (gamma: 27) -- significant overhead supply

What this means for traders: The $150 level is the single most important gamma node on the board -- it has the highest gamma reading (35) and is also the exact strike where $18.4M in new short call open interest just got created. As market makers hedge these new short call positions, they will be selling stock into rallies toward $150, creating a natural ceiling. This is textbook "gamma resistance" -- the call seller picked the strike with the most structural headwind for the bulls.

Notice this: The gap between the strongest support ($145, gamma 27) and strongest resistance ($150, gamma 35) is only $5 wide. That is a tight range, and it suggests PLTR could get pinned in this $145-$150 corridor through the near term. The call seller would love nothing more than this outcome.

Net GEX Bias: Bearish -- dealer positioning favors downside moves being amplified and upside moves being dampened. This aligns perfectly with the call seller's thesis.

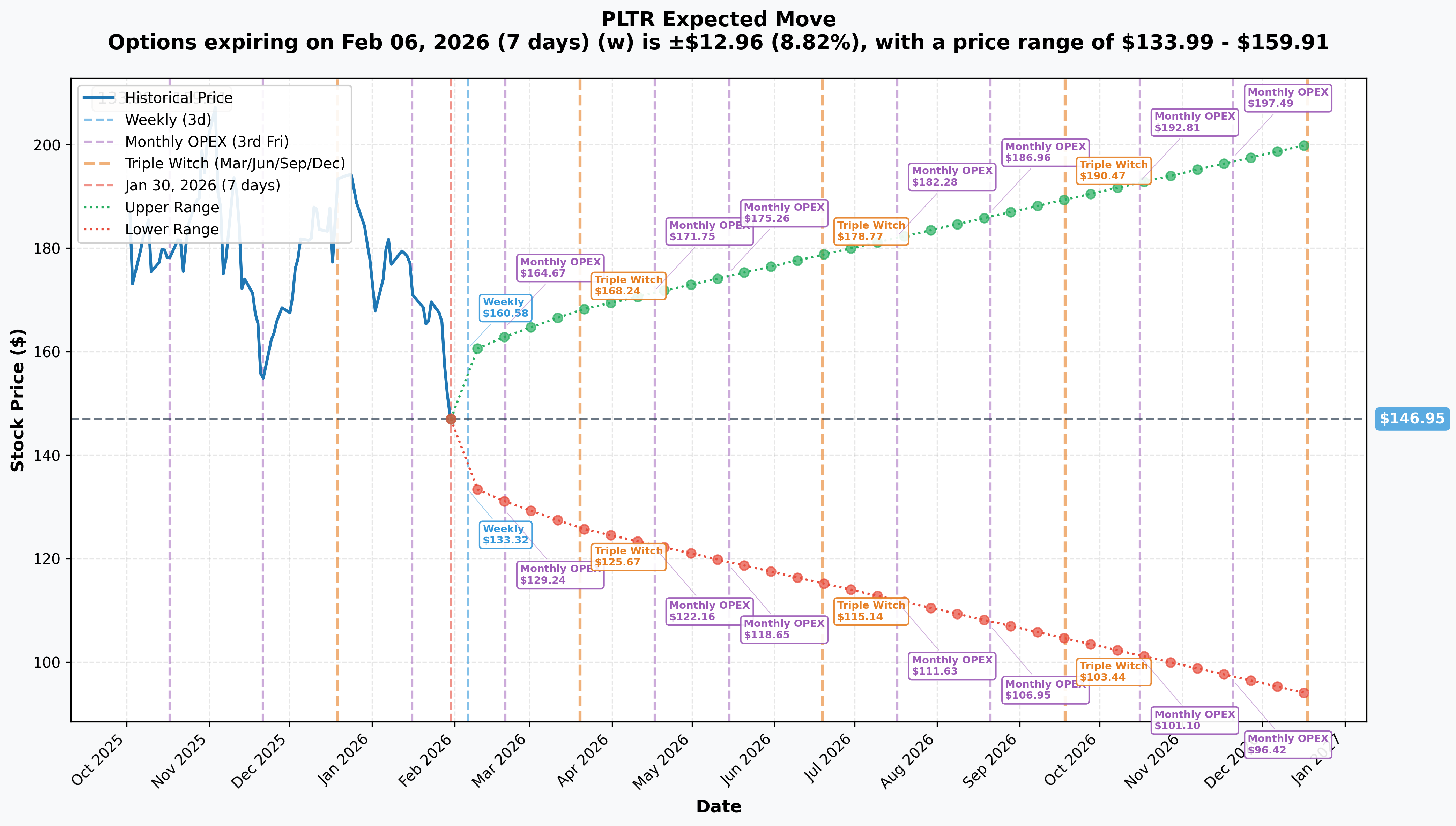

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Feb 6 - includes earnings!): +/-$12.96 (8.8%) -- Range: $133.99 - $159.91

- Monthly OPEX (Feb 20): +/-$16.09 (10.9%) -- Range: $130.87 - $163.04

- Quarterly OPEX (Mar 20 - THIS TRADE!): +/-$21.16 (14.4%) -- Range: $125.79 - $168.12

- Yearly LEAPs (Dec 18): +/-$53.10 (36.1%) -- Range: $93.85 - $200.06

Translation for regular folks: The options market expects PLTR to swing roughly $13 (8.8%) around earnings next week, and about $21 in either direction by the March 20 expiration. The call seller's breakeven of ~$163 is right at the upper end of the monthly implied move range -- meaning the market is saying there is only about a 15-20% chance PLTR trades above the seller's breakeven by March.

Key insight: The weekly implied move of 8.8% is slightly below the historical average post-earnings move of 9.28%. The options market is pricing this earnings as roughly "normal" volatility for PLTR. But with the stock down 24% from highs and analysts split 6 Buy / 10 Hold / 2 Sell, there is room for a surprise in either direction.

For the call seller: Even if PLTR rallies 14.4% to the upper bound of the quarterly implied move ($168.12), the seller still loses only modestly after accounting for the $12.83 premium collected. The math is tilted in their favor unless PLTR absolutely rips.

Catalysts

Immediate Catalyst -- Q4 2025 Earnings (February 2, 2026 -- THIS MONDAY)

This is the single most important near-term event and it is just 3 days away. The call seller is positioning ahead of this report. Consensus estimates:

| Metric | Consensus Estimate | YoY Growth | Company Guide |

|---|---|---|---|

| Revenue | $1.34B | +62% | $1.327B-$1.331B |

| Adj. EPS | $0.23 | +64.3% | -- |

| Government Revenue | $707.24M | +55.4% | -- |

| Commercial Revenue | $646.25M | +73.5% | -- |

Key metrics to watch:

- FY 2026 guidance -- this is the make-or-break number. Any softening combined with the lofty valuation could trigger significant volatility

- U.S. commercial revenue growth trajectory -- can 121% YoY be sustained?

- AIP bootcamp conversion rates and customer additions (911 clients in Q3)

- Net dollar retention rate (134% in Q3)

- Options market implied move: +/-10.70% vs. historical average of 9.28%

Why the call seller likes this setup: Even a strong beat might not push PLTR through $150 resistance given the current valuation. And if the numbers disappoint or guidance is soft, the stock could drop 10%+ easily -- making those $12.83 calls worth pennies. Heads I win, tails I win more.

Recent Catalysts (Last 3 Months)

Q3 2025 Blowout Earnings (November 3, 2025) Palantir crushed expectations with $1.181B revenue (+63% YoY), $0.21 EPS (+50% beat), Rule of 40 score of 114%, and record TCV of $2.76B (+151% YoY). U.S. commercial revenue surged 121% YoY. Despite the blowout, the stock has pulled back 24% from post-earnings highs.

$10 Billion U.S. Army Enterprise Agreement (August 2025) The single largest contract in company history -- consolidating 75 contracts into one 10-year deal. However, procurement data shows only ~$10M billable immediately, with billions deferred over the decade.

Navy ShipOS / Warp Speed ($448M) Deployed Palantir Foundry and AIP across the Maritime Industrial Base, reducing submarine schedule planning from 160 hours to under 10 minutes.

NATO Adoption NATO officially adopted Palantir's Maven Smart System -- the first alliance-wide AI warfighting platform in history.

HD Hyundai Expansion (January 2026) Palantir expanded its partnership with HD Hyundai to cover the entire group, including robotics and electric systems -- their largest and most comprehensive partnership in Korea.

Citi Upgrade to Buy (January 12, 2026) Tyler Radke at Citi upgraded PLTR and raised the price target to $235, a notable shift for one of the more cautious Street voices.

Risk Catalysts

Aggressive Insider Selling CEO Alex Karp and other insiders dumped more than $250M in stock in November 2025. Over 18 months, net insider activity shows 87.3M shares sold vs. only 10,000 bought. Karp has sold over $2B in stock cumulatively.

Extreme Valuation At 368x P/E and ~104x sales, PLTR is the most expensive stock on the S&P 500. Some analyst models put fair value as low as $13.96/share. RBC's price target is $50 -- a 66% haircut from current levels.

DOGE Sunset (July 4, 2026) The DOGE initiative is set to conclude by July 4, 2026. Palantir has been viewed as a key DOGE beneficiary -- any uncertainty around lasting government AI modernization could weigh on sentiment.

International Growth Weakness International commercial revenue grew only 10% YoY in Q3 vs. 121% for U.S. commercial. The growth story remains heavily U.S.-dependent.

Price Targets & Probabilities

Using gamma levels, implied move data, and the pre-earnings setup, here are the scenarios through the March 20th expiration:

Bull Case (25% probability)

Target: $165-$185

How we get there:

- Q4 earnings blow past expectations with FY 2026 guidance pointing to $6B+ revenue

- AIP adoption inflects even faster than expected -- new large deal announcements

- Analyst upgrades cascade (Bank of America already at $255 target)

- AI spending narrative strengthens broadly, lifting all AI names

- Short covering and FOMO push stock through the $150 gamma wall

- DOGE-related government contract wins provide additional catalysts

Call trade P&L in Bull Case (for the SELLER):

- PLTR at $165 on Mar 20: Calls worth $15.00, seller loses ~$2.17/contract x 22,400 = $4.9M loss

- PLTR at $185 on Mar 20: Calls worth $35.00, seller loses ~$22.17/contract x 22,400 = $49.7M loss

This is where the trade gets painful for the seller. If PLTR truly rips through earnings, losses are theoretically unlimited on naked calls.

Base Case (50% probability)

Target: $135-$155 range (CHOP AND RANGE)

Most likely scenario:

- Q4 earnings meet or modestly beat expectations -- stock pops 5-8% then fades

- $150 gamma resistance caps rallies, $145 support catches dips

- FY 2026 guidance is solid but not spectacular enough to justify 368x P/E

- Analyst consensus remains split (6 Buy / 10 Hold / 2 Sell)

- Post-earnings volatility crush destroys call premium rapidly

- Stock settles into a $140-$155 range as market digests valuation

Call trade P&L in Base Case (for the SELLER):

- PLTR at $150 on Mar 20: Calls expire at the money (near-zero value), seller keeps ~$12.83/contract x 22,400 = $18.4M profit (nearly all of it)

- PLTR at $145 on Mar 20: Calls expire worthless, seller keeps full $18.4M premium

This is the sweet spot for the call seller. Range-bound price action plus time decay equals maximum profit.

Bear Case (25% probability)

Target: $110-$135

What could go wrong (for longs):

- Q4 earnings disappoint on any metric -- guidance soft, growth decelerating

- Valuation reckoning: market decides 368x P/E is simply unsustainable

- Insider selling accelerates heading into lock-up expirations

- Broader AI spending concerns (Microsoft's recent capex-driven sell-off spreads to PLTR)

- DOGE budget cuts unexpectedly hit Palantir government contracts

- Break below $145 support triggers momentum selling toward $130-$140

- International weakness continues to drag on overall growth narrative

Call trade P&L in Bear Case (for the SELLER):

- PLTR at $130 on Mar 20: Calls expire worthless, seller keeps full $18.4M premium

- PLTR at $110 on Mar 20: Calls expire worthless, seller keeps full $18.4M premium

This is a home run for the call seller. If PLTR drops, the premium collected is pure profit.

Trading Ideas

Conservative: Sell Covered Calls Into Earnings Strength

Play: If you already own PLTR shares, sell the March 20 $160 or $165 calls against your position to collect premium heading into earnings

Why this works:

- This is essentially what the institutional seller may be doing -- monetizing volatility

- You keep the premium regardless of direction, providing a cushion if earnings disappoint

- $160-$165 strike gives room for a post-earnings pop while still collecting meaningful premium

- Pre-earnings implied volatility is elevated (10.70% implied move) -- this is when you WANT to sell options

- If PLTR rallies past your strike, you still profit on the stock appreciation plus the premium

Action plan:

- Sell calls BEFORE earnings (today or Monday morning) to capture peak IV

- Choose $160 strike for more premium or $165 for more upside room

- Do NOT sell more calls than you have shares to cover (100 shares per contract)

- Be prepared to have shares called away if PLTR surges past your strike

Risk level: Low-Moderate (hedged by stock ownership) | Skill level: Intermediate

Balanced: Iron Condor Around Earnings

Play: Sell the March 20 $130/$135 put spread AND the $160/$165 call spread to collect premium from both sides

Why this works:

- Profits if PLTR stays in the $135-$160 range through March -- the most likely outcome based on gamma levels

- Collects premium from elevated pre-earnings IV on both sides

- Defined risk on both directions (capped loss on the wings)

- The $145-$150 gamma corridor suggests the stock wants to stay in this zone

- Post-earnings IV crush benefits short premium strategies

Estimated P&L:

- Net credit: ~$2.00-$2.50 per iron condor ($200-$250 per contract)

- Max profit: Full credit if PLTR between $135-$160 at expiration

- Max loss: $2.50-$3.00 per spread minus credit received (if PLTR moves outside $130-$165)

- Best case: PLTR chops sideways, both spreads expire worthless, you keep everything

Entry timing:

- Enter today or Monday BEFORE earnings to capture maximum IV

- Skip if PLTR moves more than 15% on earnings -- the range assumptions change

Position sizing: Risk 2-4% of portfolio maximum

Risk level: Moderate (defined risk, range-bound thesis) | Skill level: Intermediate-Advanced

Aggressive: Pre-Earnings Put Spread (Fade the Hype)

Play: Buy the February 20 $140/$130 put spread to bet on a post-earnings fade

Why this works:

- At 368x P/E, even a strong beat may not sustain a rally -- "buy the rumor, sell the news"

- Insiders have dumped $250M+ in stock -- they know the business better than anyone

- The $18.4M call sell confirms at least one large player expects downside or range

- Bearish gamma positioning amplifies downside moves

- $145 support, if broken, opens a fast path to $140 and below

- Historical average post-earnings move is 9.28% -- a downside move to $134 is within 1 standard deviation

Estimated P&L:

- Cost: ~$2.50-$3.50 per spread ($250-$350 per contract)

- Max profit: $7.50-$6.50 per spread if PLTR below $130 at February 20 expiration

- Risk/Reward: ~2:1 to 2.5:1

- Breakeven: ~$137-$138

Why this could go wrong:

- PLTR has a history of massive post-earnings rallies when they beat big

- AIP adoption could be accelerating faster than anyone expects

- Government contract wins could provide upside surprises

- If PLTR gaps above $155 on earnings, put spreads are worthless

Position sizing: Risk 1-3% of portfolio MAXIMUM

Risk level: HIGH (directional bet against a momentum name) | Skill level: Advanced

Risk Factors

Do not overlook these potential headwinds:

-

Earnings in 3 days is a coin flip on steroids: PLTR reports Monday after close. The options market is pricing a 10.70% move -- that is roughly $15.75 in either direction from current levels. At 368x P/E, any miss on revenue, guidance, or growth metrics could easily trigger a 15-20% sell-off. Conversely, a blowout beat could send the stock ripping through the $150 gamma wall. Earnings on high-multiple names are genuinely binary events.

-

Valuation requires perfection for decades: Palantir must grow revenue at approximately 35% annually for 25 years to justify its current valuation. That is an extraordinarily high bar. The company trades at ~104x sales while the enterprise software industry average is 10-15x. Even bulls acknowledge the valuation is "rich" -- the question is whether AIP changes the math. RBC's price target of $50 implies 66% downside.

-

Insiders are aggressively selling: Over $250M in insider sales in November 2025 alone. CEO Karp has sold over $2B cumulatively. Net insider activity over 18 months: 87.3M shares sold, 10,000 shares bought. When the people running the company are selling hand over fist, pay attention.

-

$10B Army contract is headline, not reality (yet): The contract has a $10 billion ceiling over 10 years, but only ~$10M is immediately billable. The gap between the headline number and near-term revenue contribution is enormous. Do not confuse contract ceilings with guaranteed revenue.

-

International growth is lagging badly: U.S. commercial revenue grew 121% YoY in Q3, but international commercial grew only 10%. For a company valued at $362B, that kind of geographic concentration is a risk. If U.S. growth slows and international does not pick up the slack, the growth narrative unravels.

-

Bearish gamma positioning adds structural headwinds: Net GEX bias is bearish, meaning market maker hedging will amplify downside moves and dampen rallies. The $150 level now has even more call gamma stacked on top from the $18.4M trade, making it an even harder ceiling to break through.

-

Competition is intensifying: Microsoft Azure AI, AWS, Databricks, and Snowflake are all competing for enterprise AI budgets. Several consulting firms have partnered with PLTR, but hyperscalers have massive distribution advantages that could erode Palantir's pricing power over time.

-

DOGE uncertainty cuts both ways: While Palantir is positioned as a DOGE beneficiary, government spending cuts could also reduce overall federal IT budgets. The DOGE initiative sunsets July 4, 2026 -- any signals of reduced government AI modernization would be a headwind.

The Bottom Line

Straight talk: An institutional player just collected $18.4 million in premium by selling PLTR calls at the $150 strike -- right at the stock's strongest gamma resistance level -- with earnings just 3 days away. This is a high-conviction income play that says: Palantir is not going meaningfully above $150 through March, and the elevated pre-earnings volatility is something to sell, not buy.

What this trade tells us:

- The seller chose the exact strike with the highest gamma resistance (35) -- they know the gamma map

- Selling ahead of earnings captures maximum implied volatility -- the premium will decay sharply post-earnings regardless of direction

- The 2.07x volume-to-OI ratio signals this is a fresh, large, and unusual position

- Two trades 26 seconds apart, both on the bid, totaling $18.4M -- this is methodical execution, not a casual trade

- Breakeven at ~$163 gives a significant cushion -- PLTR needs to rally 9%+ past the strike before the seller loses

If you own PLTR:

- Consider writing covered calls against your position to generate income -- this institutional seller is doing exactly that (probably)

- Be aware that $150 is a hard ceiling reinforced by gamma and now by $18.4M in new short call open interest

- If you are nervous about earnings, the covered call premium provides a meaningful cushion (8-9% worth)

- Set a mental floor at $130-$135 -- below that level, the pullback from $207 becomes a trend reversal

- Remember: the business is executing well (63% revenue growth, 114% Rule of 40) even if the valuation is extreme

If you are watching from the sidelines:

- PLTR at 368x earnings is not a stock you buy casually -- the margin of safety is essentially zero

- If earnings disappoint, a 15-20% drop to $125-$130 is within the range of outcomes

- If earnings crush, the stock may rally but face heavy resistance at $150-$155 from gamma and the new call wall

- The best risk/reward entry may come AFTER earnings -- wait for the binary event to pass, then assess

- Analyst consensus average target of $189.94 (25% upside) is notable but the range is enormous ($50 to $255)

If you are bearish:

- The $18.4M call sell validates the bearish-to-neutral thesis at these levels

- Bearish gamma positioning + $150 call wall = structural resistance overhead

- Insider selling of $250M+ is a flashing amber light

- At 104x sales, even a modest growth deceleration could trigger 30-50% downside

- Put spreads into earnings offer defined-risk bearish exposure without unlimited downside risk

Key dates to watch:

- February 2 (Monday!) - Q4 2025 earnings after market close -- the main event

- February 3 - Post-earnings market reaction (expect 10%+ move)

- February 6 - Weekly OPEX (+/-8.8% implied move window)

- February 20 - Monthly OPEX (+/-10.9% implied move window)

- March 20 - Quarterly OPEX and expiration of the $18.4M call trade

- May 2026 - Q1 2026 earnings (next fundamental catalyst)

- July 4, 2026 - DOGE sunset deadline

Final take: The $18.4M institutional call sell on PLTR is a statement trade: collect premium, cap upside, and bet that the stock's best days for the near term are behind it. At 368x P/E with insiders rushing for the exits, earnings in 3 days, and the strongest gamma resistance sitting right at $150, the setup favors the seller. The business itself is impressive -- 63% revenue growth, $10B Army contract, AIP adoption inflecting -- but the stock price already reflects years of perfection. The call seller is betting that perfection is priced in, and anything less means the premium is theirs to keep.

For most traders, this is a "wait for earnings" situation. The binary event on Monday will determine the next major move. If you must take a position, selling premium (covered calls, iron condors) aligns with both the institutional flow and the gamma structure. Buying calls into this setup is fighting the flow, the gamma, and the valuation -- possible but high-risk.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. The $18.4M call trade reflects one institution's view and does not imply the trade will be profitable or that you should replicate it. Always do your own research and consider consulting a licensed financial advisor before trading. Pre-earnings positioning carries extreme risk -- stocks can move 10%+ in either direction on earnings reports. The call seller may have portfolio context (hedging long stock, portfolio overlay) that makes the trade rational for them but inappropriate for retail investors.

About Palantir Technologies Inc: Palantir develops analytical software platforms leveraging data integration and AI for client organizations. Known for Gotham (government), Foundry (commercial), and AIP (AI Platform), with a market cap of $361.9 billion in the Software - Prepackaged Software industry.