💎 PRU $2.1M LEAP Put - Smart Money Hedging Insurance Giant! 🛡️

📅 December 10, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $2.1 MILLION on PRU long-dated puts this morning at 10:54:34! This sophisticated hedge bought 3,000 contracts of $100 strike puts expiring January 15, 2027 - a 13+ month LEAP providing downside protection on Prudential Financial while the stock trades at $113.30. With PRU down -10.6% YTD after pulling back from September highs, smart money is locking in insurance at the $100 level (11.7% below current price). Translation: Institutional investors are buying long-term protection as financial sector faces interest rate uncertainty and valuation concerns!

📊 Company Overview

Prudential Financial (PRU) is one of America's largest life insurance and financial services companies:

- Market Cap: $39.1 Billion (major financial services player)

- Industry: Life Insurance, Asset Management

- Current Price: $113.30 (trading mid-range after September pullback)

- Primary Business: Life insurance, annuities, pension risk transfer, PGIM asset management ($1.4T AUM)

- Employees: 38,196 across US, Japan, and emerging markets

💰 The Option Flow Breakdown

The Tape (December 10, 2025 @ 10:54:34):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:54:34 | PRU | ASK | BUY | PUT $100 | 2027-01-15 | $2.1M | $100 | 3K | 273 | 3,000 | $113.30 | $7.05 |

🤓 What This Actually Means

This is a long-term defensive hedge on a significant insurance/financial services position! Here's the breakdown:

- 💸 Premium paid: $2.1M ($7.05 per contract × 3,000 contracts)

- 🛡️ Protection strike: $100 provides 11.7% downside cushion below current $113.30 price

- ⏰ LEAP duration: 401 days to expiration (13+ months) captures Q4 2025 earnings (Feb 10), full 2026 earnings cycle, CIO transition (March 2026), and extended interest rate environment

- 📊 Size matters: 3,000 contracts represents 300,000 shares worth ~$34M at current prices

- 🏦 Institutional insurance: This is sophisticated portfolio hedging on a long-term position, not a short-term bearish bet

What's really happening here: This trader likely holds a SUBSTANTIAL long position in PRU stock accumulated during the rally to $123.88 in September. Now, with PRU down 10% from highs and facing multiple uncertainties (Fed policy, $30.7B unrealized losses, CIO transition, valuation at 15.36x trailing P/E), they're paying $7.05 per share for the Jan 2027 $100 puts for long-term insurance. If PRU drops below $100 over the next 13 months, these puts pay off dollar-for-dollar. Think of it like buying a $2.1M insurance policy to protect a $34M+ long position through 2026's uncertainty.

Unusual Score: 🔥 SIGNIFICANT - While not as extreme as mega-cap tech trades, 3,000 contracts with 11x the existing open interest (273) and $2.1M premium on a 13-month LEAP is highly unusual for PRU. This represents sophisticated institutional positioning, not retail speculation.

📈 Technical Setup / Chart Check-Up

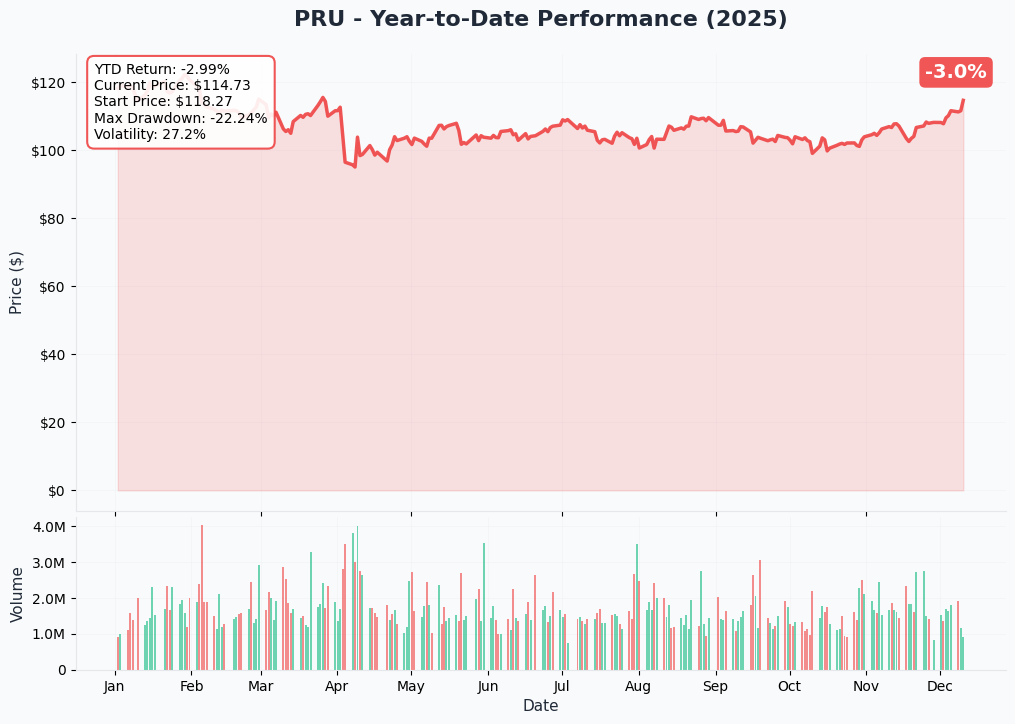

YTD Performance Chart

PRU is struggling - down -10.6% YTD with current price around $113.30 (started the year near $127). The chart tells a story of volatility and consolidation - after hitting a 52-week high of $123.88 in September following strong Q3 earnings, the stock has pulled back sharply over the past three months.

Key observations:

- 📉 Post-earnings selloff: Down from $123.88 high in September to current $113 range (8.8% correction)

- 📊 52-week range: $90.38 - $123.88 (significant volatility for insurance stock)

- 💰 Support levels: Trading above $110-112 support zone from mid-year

- ⚠️ Defensive positioning: 5.04% dividend yield attracts income investors but YTD decline suggests fundamental concerns

- 📈 Institutional accumulation: 59.41% institutional ownership with recent adds from CalPERS, Norges Bank, Arrowstreet Capital

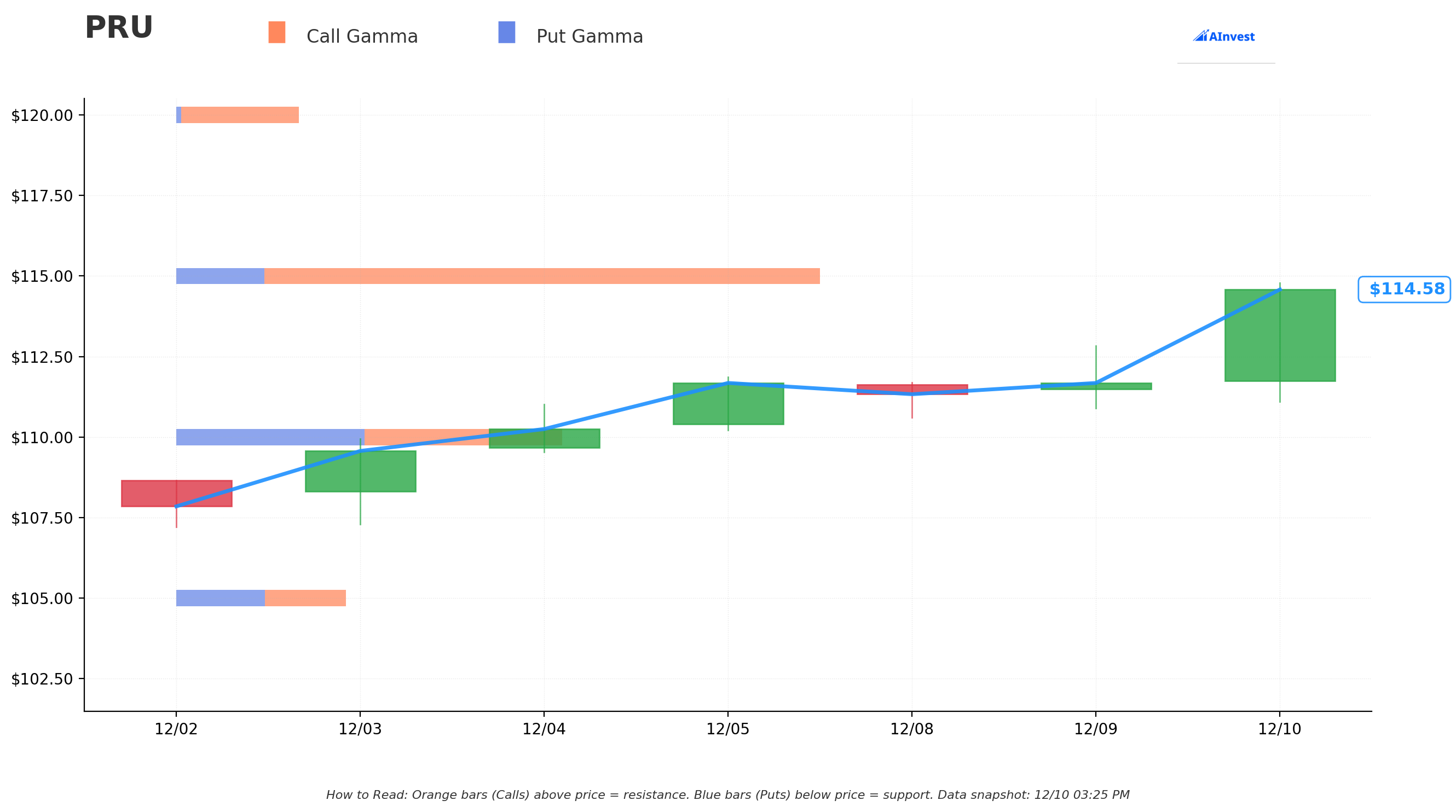

Gamma-Based Support & Resistance Analysis

Current Price: $114.61

The gamma exposure map reveals critical price magnets and barriers governing near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $110 - Immediate major support with 4.59B total gamma (strongest nearby floor - 4.0% below current)

- $105 - Secondary support at 2.02B gamma (dealers will buy dips here)

- $100 - Deep support with 0.72B gamma (exactly where this put trade is struck! Critical psychological level)

- $97.50 - Extended support zone with 0.23B gamma

- $95 - Disaster floor at 0.37B gamma (near 52-week low of $90.38)

🟠 Resistance Levels (Call Gamma Above Price):

- $115 - Immediate ceiling with 7.66B gamma (STRONGEST RESISTANCE - dealers will sell into rallies, only 0.34% overhead)

- $120 - Secondary resistance at 1.46B gamma (4.7% above current)

- $125 - Major ceiling zone with 0.47B gamma (September high area)

- $130 - Extended upside target at 0.18B gamma (13.4% rally required)

- $135 - Long-term resistance at 0.19B gamma (analyst target zone)

What this means for traders: PRU is trading in a TIGHT range just below massive $115 resistance (7.66B - the single largest level). The gamma data shows market makers holding enormous positions at $115 which creates natural selling pressure. This setup screams "capped upside" before the next catalyst. The $110 level with 4.59B gamma is THE critical near-term support - break below that and momentum could accelerate toward $105-100.

Notice anything? The put buyer struck EXACTLY at $100 where there's meaningful gamma support and a major psychological level. They're positioning below the $105-110 support cluster, expecting that if PRU cracks through those levels on negative catalysts (disappointing earnings, interest rate volatility, margin compression), it could flush quickly toward $100.

Net GEX Bias: Bullish (12.8B call gamma vs 6.4B put gamma) - Overall positioning remains moderately bullish, but immediate price action constrained by massive overhead $115 resistance.

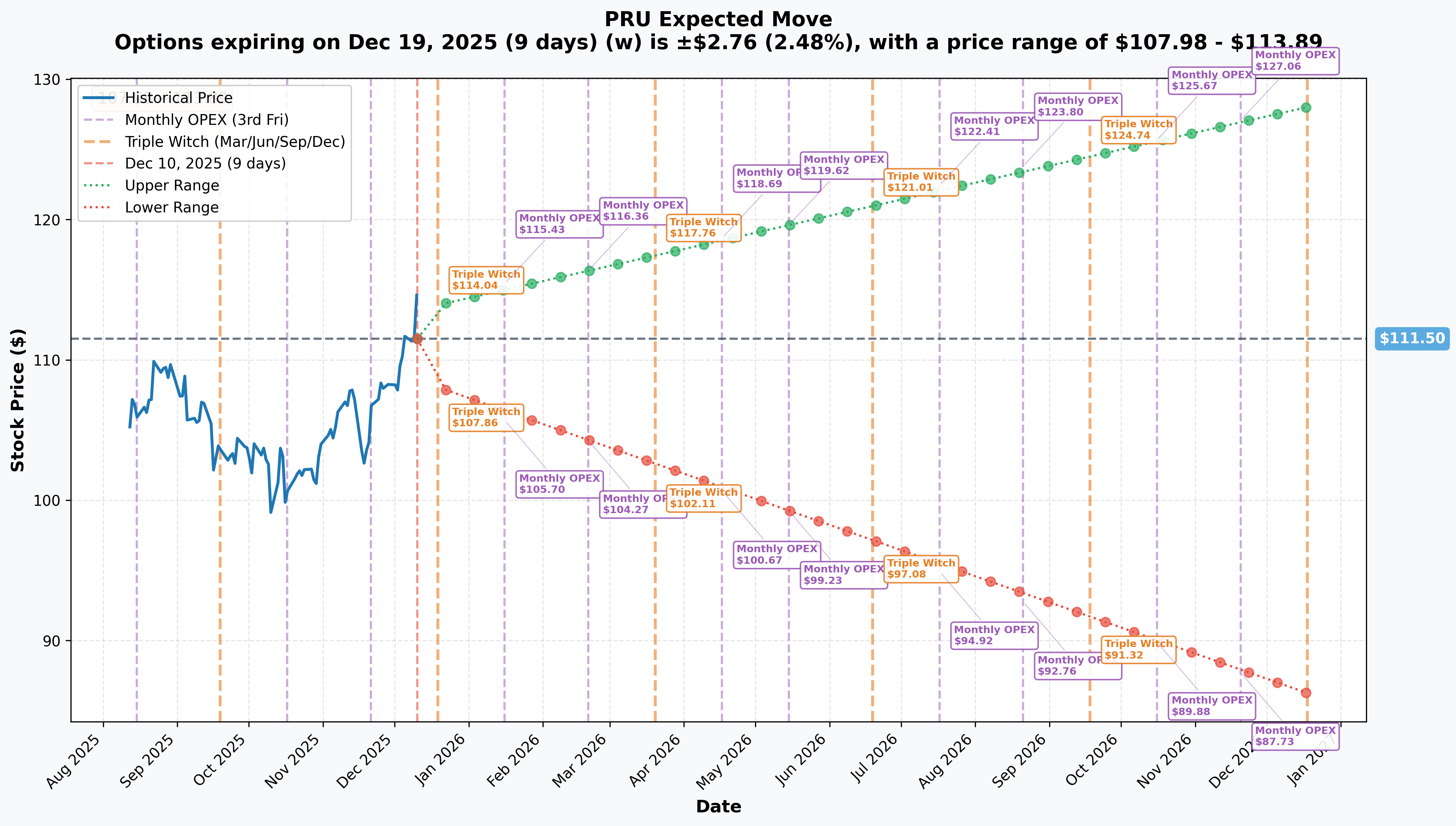

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX (Dec 19 - 9 days): ±$2.76 (±2.48%) → Range: $107.98 - $113.89

- 📅 Quarterly Triple Witch (Dec 19 - 9 days): ±$2.76 (±2.48%) → Range: $108.04 - $113.92

- 📅 Yearly LEAPS (Dec 18, 2026 - 373 days): ±$18.36 (±16.47%) → Range: $86.23 - $128.03

Translation for regular folks: Options traders are pricing in a 2.5% move ($2.76) through December OPEX - relatively modest for near-term action. However, the LEAP market expects a MUCH LARGER 16.5% move ($18.36) over the next year, reflecting uncertainty around interest rates, earnings, and competitive dynamics in the insurance sector.

The December 2026 LEAP expiration (close to this trade's January 2027 expiration) has a lower range of $86.23 - meaning the market thinks there's a meaningful possibility PRU could trade as low as $86 over the next year (24% downside). This aligns with the put buyer's thesis: protect against a 13-24% drawdown over the next 13 months if financial sector headwinds intensify, interest rates remain volatile, or earnings disappoint.

Key insight: The relatively low near-term IV (2.48%) compared to longer-term IV (16.47%) suggests the market sees current consolidation continuing short-term, but expects significant volatility through 2026 earnings cycle and macro events.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

December FOMC Meeting - December 17-18, 2025 (8 DAYS!) 🏦

The Federal Reserve is widely expected to cut interest rates by 25 basis points at its December meeting, with further cuts projected into 2026 based on cooling labor market conditions and inflation approaching the 2% target.

Impact on PRU:

- ✅ Positive: Could reduce the $30.7 billion in gross unrealized losses on available-for-sale fixed maturities, improving balance sheet flexibility

- ⚠️ Negative: Lower rates reduce investment income on new fixed-income purchases, pressuring net interest margins

- 📊 Japan exposure: Structural low-rate environment in Japan (40% of earnings) remains challenging regardless of US policy

- 🎯 Watch: Commentary on terminal rate expectations and 2026 trajectory - this drives long-term planning for asset-liability management

Year-End Portfolio Positioning & Tax Loss Harvesting 📊

With PRU down 10.6% YTD, institutional investors may engage in tax loss harvesting before December 31st, creating additional selling pressure. Conversely, value-oriented funds may add exposure to the 5.04% dividend yield heading into 2026.

🚀 Near-Term Catalysts (Q1 2026)

Q4 2025 Earnings - February 10, 2026 (62 DAYS AWAY!) 📊

Prudential reports fiscal Q4 results on February 10, 2026. This is THE major catalyst that could validate or challenge the current positioning. Wall Street consensus and key expectations:

- 📊 Q4 EPS: $3.18 (revised down from $3.30 by Zacks on Nov 19)

- 💰 Full Year 2025 EPS: $14.31-$14.36, representing 11.6%-13.6% growth from $12.62 in 2024

- 🤖 Longevity Risk Transfer: Watch for updates on $4B NN Life deal and new pipeline activity

- 💻 PGIM Asset Flows: Net flows critical for fee income growth (Q3 showed $2.4B total flows)

- 📈 Operating ROE: Target to maintain 17.5% from Q3 record levels

- 🇯🇵 Japan Operations: 40% of earnings - watch for interest rate sensitivity and demographic headwinds

- 💸 Capital Return: Progress on $1 billion share buyback authorization for 2025

Upside surprise potential: Continued strength in longevity risk transfer deals (following $1.5B in Q3), PGIM private credit expansion through Prismic Life's $1.3B capital raise, and reduction in unrealized losses if rates decline.

Downside risk factors: Disappointing advisor network momentum (despite $3B in new assets YTD), margin compression from competitive pricing, higher-than-expected assumption updates (Q2 had $134M charge), or conservative 2026 guidance citing macro uncertainty. JPMorgan already lowered price target to $133 from $136 while CFRA downgraded from Buy to Hold with $110 target.

Chief Investment Officer Transition - March 12, 2026 (92 DAYS AWAY!) 👔

Matthew Armas will take over as Chief Investment Officer, replacing Timothy Schmidt who is retiring after 16 years. This leadership transition introduces execution risk around investment strategy continuity, particularly managing the $1.6 trillion asset portfolio during a volatile rate environment.

Why this matters:

- 🎯 16-year veteran being replaced - significant institutional knowledge loss

- 📊 Occurs during critical period of managing $30.7B unrealized losses

- ⚠️ New CIO may implement strategy shifts that impact near-term performance

- 🏦 Coincides with interest rate normalization and Fed policy pivot

- 📈 Market will scrutinize early decisions for signs of direction change

Dividend Ex-Date Window - February/March 2026 💰

With a 5.04% dividend yield and quarterly payout of $1.35/share, the next ex-dividend date (likely mid-February) typically provides support for the stock as income investors accumulate shares. PRU has paid dividends since 2002 with 5-year average yield of 4.8%.

📊 Medium-Term Catalysts (Q2-Q4 2026)

Continued Longevity Risk Transfer Deal Flow 🏢

Following the $4 billion NN Life & Pensions deal in August 2025 and $1.5B in Q3 transactions, Prudential indicated "increased activity and demand in the Dutch market" with opportunities to help clients manage longevity risk.

Pipeline expectations:

- 💰 Target: Multiple jumbo transactions (>$2B each) through 2026

- 🌍 Geography: Netherlands expansion, potential UK/European opportunities

- 📈 Revenue impact: Each $1B deal generates approximately $15-25M in annual fee income

- 🎯 Competitive advantage: Leading longevity risk transfer capabilities with international reach

- ⚠️ Risk: Capital-intensive business requiring strong balance sheet - $30.7B unrealized losses could constrain deal capacity

PGIM Private Credit Expansion Through Prismic Life 🏦

PGIM manages $341.7 billion in private alternatives as of September 30, 2025. The Prismic Life $1.3 billion capital raise completed November 18 is expected to drive approximately $15 billion in asset allocations throughout 2026.

Growth drivers:

- 📊 AUM expansion: Target $400B+ in private alternatives by end of 2026

- 💼 Fee income: Higher-margin private credit vs traditional fixed income

- 🤝 Partners Group strategic partnership: Multi-asset portfolio solutions launched September 2025

- 🎯 Institutional distribution restructuring: Integrated team under Blalock and Chamieh improves cross-selling

- 📈 Market position: 16th largest money manager globally (out of 369 firms)

LPL Financial Partnership Momentum 🚀

Prudential partnered with LPL Financial in September 2025 to expand retirement security access. By November 2025, Prudential had added advisor teams representing more than $3 billion in client assets, increasing advisor headcount by nearly 9% to over 3,000 advisors nationwide.

2026 targets:

- 👥 Headcount: Continue 9% annual growth trajectory (3,300+ advisors by end of 2026)

- 💰 Assets: Additional $3-5B in client assets through recruits and organic growth

- 🎯 Distribution: Leverage LPL infrastructure for operational efficiency

- 📊 Revenue: Each $1B in advisor-managed assets generates ~$8-12M in annual fees

Potential Alexforbes Stake Sale 💸

Strategic implications:

- 💵 Capital: $627M provides additional capacity for US growth initiatives or share buybacks

- 🌍 Focus: Signals potential reallocation away from emerging markets toward core US/Japan operations

- ⚖️ Valuation: Market reaction depends on use of proceeds (buybacks bullish, debt reduction neutral)

- ⏰ Timing: Likely H1 2026 if proceeds

⚠️ Risk Catalysts (Negative)

Interest Rate Volatility & Unrealized Losses 📉

Prudential reported $30.7 billion in gross unrealized losses on available-for-sale fixed maturities as of June 30, 2025, primarily due to rising interest rates.

Why this is a major overhang:

- 🚨 Flexibility constraints: Limits management's ability to sell assets without realizing losses or reallocate capital

- 📊 Balance sheet pressure: While not impacting credit losses directly, creates optical issues for investors

- ⚠️ Asset-liability mismatch: Rapid rate shifts can create significant P&L impacts through hedging costs

- 🇯🇵 Japan exposure compounding: Low-rate Japanese operations (40% of earnings) facing structural headwinds

If rates rise unexpectedly: Unrealized losses could expand beyond $30.7B, further constraining strategic options and pressuring book value.

MetLife Digital Competitive Advantage 🤖

MetLife's Xcelerator digital platform has reached 4.5 million customers and generated $200 million in adjusted premiums since its 2023 launch, demonstrating superior technology adoption.

Competitive risks:

- 📱 Market share erosion: Prudential's slower digital transformation could lose younger customers to MetLife

- 💰 Margin pressure: Traditional distribution more expensive than digital-first approaches

- 🎯 Innovation gap: MetLife leads in customer experience, potentially commanding premium pricing

- 📊 Market cap differential: MetLife at $53.7B vs PRU at $39.1B reflects investor preference for digital leader

Regulatory & Capital Requirement Changes ⚖️

Specific concerns:

- 🏦 Group-wide supervision: Potential for stricter capital requirements reducing ROE

- 📋 Fiduciary rules: Changes could impact distribution strategies and product sales

- 💼 Tax law changes: Potential changes in tax treatment of insurance products affecting customer demand

- ⭐ Credit rating risk: Downgrade could limit ability to market products, increase policy surrenders

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through January 15, 2027 expiration:

📈 Bull Case (30% probability)

Target: $130-$140

How we get there:

- 💪 Q4 earnings BEAT with EPS $3.30+ and strong 2026 guidance ($15+ EPS)

- 🚀 Longevity risk transfer pipeline accelerates with $8-10B in new deals through 2026

- 🤖 PGIM private credit expansion hits $400B+ AUM, driving fee income growth

- 📊 Interest rates normalize to 3.5-4% range, reducing unrealized losses to $15-20B

- 🇯🇵 Japan operations stabilize with improved profitability despite low rates

- 💰 $1B+ in share buybacks through 2026 supports EPS growth

- 📈 Dividend increases to $5.60-$5.80/share (4% raise), attracting more income investors

- 🎯 Successful CIO transition with no strategic disruptions

- ⚖️ Alexforbes sale provides $627M for opportunistic share repurchases

Key metrics needed:

- Operating ROE sustained above 17% through 2026

- PGIM net flows exceeding $10B annually

- Gross margins on new business expanding

- Capital ratios remaining strong (409% RBC)

Probability assessment: 30% because it requires favorable macro environment (rate stability), flawless execution on multiple growth initiatives, and no competitive pressure from MetLife's digital advantage. Gamma resistance at $115-125 creates technical headwinds.

🎯 Base Case (50% probability)

Target: $105-$120 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Q4 earnings meet consensus ($3.15-3.20 EPS) with in-line guidance

- 📱 Longevity risk transfer deals continue steadily ($3-5B annually) but not spectacular

- ⚖️ PGIM growth progresses but private credit competition intensifies

- 🤖 Interest rates volatile but trend toward 3.75-4.25% by end of 2026

- 🇯🇵 Japan remains structural drag (40% of earnings in low-growth market)

- 🔄 Trading within gamma support ($110) and resistance ($115-120) for extended periods

- 💤 Multiple compression from 15.36x to 13-14x trailing P/E on macro uncertainty

- 📊 Dividend maintained at $5.40/share (5% yield at $110 provides floor)

- 👔 CIO transition smooth but no major strategic pivots announced

This is the put buyer's BASE scenario: Stock consolidates in $105-115 range through 2026, puts expire worthless or with minimal value around $5-10, but downside protection served its purpose during uncertain Fed policy and earnings volatility. The $2.1M is simply the "insurance premium" they're willing to pay for peace of mind on a $34M+ long position.

Why 50% probability: Stock at fair valuation (15.36x P/E vs industry average), solid fundamentals (17.5% ROE, 5% dividend yield) but facing multiple headwinds (unrealized losses, Japan exposure, digital transformation lag). Most likely path is range-bound consolidation waiting for catalysts.

📉 Bear Case (20% probability)

Target: $90-$105 (TEST THE PUT STRIKE!)

What could go wrong:

- 😰 Q4 earnings miss with EPS $2.90-3.00 and conservative 2026 guidance ($13-13.50 EPS)

- 🚨 Longevity risk transfer pipeline slows due to capital constraints from unrealized losses

- ⏰ PGIM faces massive outflows ($5B+) as competitors offer better terms

- 🇨🇳 Interest rates spike unexpectedly to 5%+, expanding unrealized losses to $40B+

- 💸 Broader financial sector selloff drags all insurers lower (recession fears, credit concerns)

- 📊 MetLife continues taking market share with digital platform, PRU loses pricing power

- 🤖 CIO transition creates strategy confusion, asset allocation missteps

- 💰 Dividend cut to $1.20-1.25/share to preserve capital (yield no longer defensive)

- 🔨 Break below $110 gamma support triggers cascade to $105, then $100

- ⚖️ New regulatory capital requirements force dilutive equity raise

Critical support levels:

- 🛡️ $110: Major gamma floor (4.59B) - MUST HOLD or momentum shifts bearish

- 🛡️ $105: Secondary support (2.02B gamma) - institutions likely buy dips here

- 🛡️ $100: Deep support (0.72B gamma) + this put strike - psychological level and hedge strike

- 🛡️ $95: Extended floor near 52-week low of $90.38

Probability assessment: 20% because it requires multiple negative catalysts to align. PRU's fundamentals remain solid (strong capital ratios, diversified revenue, 5% yield), but execution risk is real and valuation offers limited upside. The put buyer clearly thinks this scenario has >20% odds or they wouldn't pay $2.1M for 13-month protection.

Put P&L in Bear Case:

- Stock at $90 on Jan 15, 2027: Puts worth $10.00, profit = $2.95/share × 3,000 = $885K gain (42% ROI)

- Stock at $85 on Jan 15, 2027: Puts worth $15.00, profit = $7.95/share × 3,000 = $2.385M gain (114% ROI!)

- Stock at $100 on Jan 15, 2027: Puts worth $0 (at-the-money), loss = -$7.05/share × 3,000 = -$2.115M (100% loss)

💡 Trading Ideas

🛡️ Conservative: Income-Focused Dividend Accumulation

Play: Dollar-cost average into PRU for 5%+ dividend yield on any pullback to $105-110

Why this works:

- 💰 Attractive yield: 5.04% dividend yield (85% higher than Financial Services sector average of 2.84%)

- ⏰ Dividend safety: Payout ratio of 73.37% is sustainable, paid dividends since 2002

- 📊 Valuation support: 15.36x trailing P/E below 52-week high suggests limited downside

- 🎯 Gamma support at $110: Strong technical floor from 4.59B gamma exposure

- 📉 Contrarian opportunity: Down 10.6% YTD creates entry point for long-term holders

- 🤔 Institutional backing: 59.41% institutional ownership with recent adds from CalPERS, Norges Bank

- 🏦 Capital return program: $1B buyback authorization provides additional support

Action plan:

- 👀 Wait for pullback to $108-110 range (gamma support zone)

- 🎯 Accumulate 100-300 shares in 2-3 tranches over 1-2 months

- ✅ Collect quarterly $1.35/share dividends ($135-405/quarter depending on position size)

- 📊 Re-invest dividends if stock remains below $115, take cash if above $120

- ⏰ Hold minimum 2-3 years for dividend compounding and potential valuation rerating

Expected outcome: Generate 5%+ annual income while waiting for interest rate normalization, longevity deal flow, and PGIM growth to drive stock back to $120-130 range (15-20% capital appreciation + dividends = 8-10% annual total return).

Risk level: Low (defensive dividend play) | Skill level: Beginner-friendly

⚖️ Balanced: Post-Earnings Covered Call Strategy

Play: After February 10 earnings, sell covered calls to generate income on existing PRU shares

Structure: Own 100 shares of PRU, Sell 1 contract of $120 calls (March or April expiration)

Why this works:

- 🎢 Earnings volatility creates elevated IV - sell calls AFTER earnings when IV is still elevated but declining

- 📊 Strong gamma resistance at $115 and $120 makes upside above $120 unlikely near-term

- 🎯 Generate 2-3% additional income per month on top of 5% dividend yield

- 🤝 Willing to sell shares at $120 (6% above current price) represents acceptable profit target

- ⏰ 45-60 days to expiration gives time decay advantage

- 🛡️ Dividend collection while covered calls outstanding

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Collect ~$2.00-3.00 per contract monthly ($200-300 income per 100 shares)

- 📈 If PRU stays below $120: Keep premium + shares + dividends = 8-10% annualized return

- 📉 If PRU rises above $120: Shares called away at $120 = 6% gain + premium + dividends = 10-12% total return

- 🎯 Downside: Stock drops below $110 - keep premium but shares decline (mitigated by $110 gamma support)

Entry timing:

- ⏰ Wait until 2-3 days after February 10 earnings for IV to settle

- 🎯 Only sell calls if stock is $112-116 range (not too close to strike)

- ❌ Skip if stock already above $118 (too close to $120 strike)

Position sizing: Use only on existing long PRU shares, not naked calls

Risk level: Low-Moderate (requires stock ownership) | Skill level: Intermediate

🚀 Aggressive: Copy The Smart Money - Long-Term Put Protection (ADVANCED ONLY!)

Play: Buy smaller version of the institutional trade - long-dated $100 puts for portfolio protection

Structure: Buy $100 puts (January 15, 2027 expiration - SAME as the $2.1M trade)

Why this could work:

- 💥 Smart money validation: Institutional player paid $2.1M for this exact structure

- 🎰 Tail risk hedge: Protects against financial sector meltdown, recession, or PRU-specific disaster

- 📊 13-month duration: Captures Q4 2025 earnings, full 2026 earnings cycle, CIO transition, Fed policy evolution

- 🚀 Defined risk: Maximum loss is premium paid ($7.05 per contract = $705 per put)

- ⚡ Asymmetric payoff: If PRU drops to $85-90 (bear case), puts worth $10-15 = 42-113% return

- 📈 Portfolio insurance: Hedge against broader financial sector exposure

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Each put costs $705 ($7.05 × 100), need meaningful PRU position to justify

- ⏰ TIME DECAY: Theta burns -$1.50/month ($150 per contract) with acceleration in final 6 months

- 😱 Out-of-the-money: Stock needs to drop 11.7% to $100 just to break even at expiration

- 📊 Base case = total loss: If PRU stays $105-120 range (50% probability), entire premium lost

- 🎢 Opportunity cost: $705 could generate $35/year in dividends if used to buy PRU shares instead

- ⚠️ Requires disaster: Only profitable if PRU drops below $92.95 (18% decline) - low probability

Estimated P&L:

- 💰 Cost: $705 per put contract

- 📈 Profit scenario: PRU drops to $90 by Jan 2027 = put worth $1,000, gain = $295 (42% ROI)

- 🚀 Home run: PRU drops to $80 = put worth $2,000, gain = $1,295 (184% ROI)

- 📉 Loss scenario: PRU stays above $105 = lose $400-600 (60-85% loss)

- 💀 Total loss: PRU above $100 at expiration = lose entire $705 (100% loss)

Breakeven: Stock must be below $92.95 at January 15, 2027 expiration (18% decline from current $113.30)

Position sizing guidelines:

- ✅ Hedge ratio: Buy 1 put per 100 shares of PRU owned (1% portfolio insurance cost)

- ✅ Speculation: Only risk 1-2% of portfolio ($700-1,400 = 1-2 contracts max)

- ❌ Never: Don't buy more puts than you can afford to lose entirely

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Own substantial PRU position (300+ shares minimum) and need long-term downside protection

- ✅ Understand you're paying $705 for 13 months of insurance that likely expires worthless

- ✅ Can afford to lose ENTIRE premium (60-80% probability)

- ✅ Believe bear case (financial crisis, recession, PRU-specific disaster) has >25% probability

- ✅ Accept that even if stock drops to $105-108, you still lose money on this hedge

- ⏰ Plan to hold to expiration or sell if PRU breaks below $100 (don't try to trade in/out)

Risk level: HIGH (likely lose 60-100% of premium) | Skill level: Advanced only

Probability of profit: ~25% (requires 18% decline over 13 months - below base case)

When this makes sense: You own 500+ shares of PRU (worth $56,650 at $113.30), bought near the highs ($120-124), and want to protect against extended bear market in financials. Paying $705-$1,410 (1-2 puts) for $10,000-$20,000 of downside protection could be worthwhile insurance if you believe macro risks are elevated.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ $30.7B unrealized losses overhang: Gross unrealized losses on available-for-sale fixed maturities create massive balance sheet uncertainty. While not impacting credit losses directly, these losses severely limit management's flexibility to sell assets without crystallizing losses or reallocate capital. Any forced asset sales in a rising rate environment would compound the problem. This is a STRUCTURAL issue that won't resolve quickly even if rates decline.

-

💸 Q4 earnings binary event in 62 days: Results February 10, 2026 create significant volatility risk. Consensus expects $3.18 EPS but Zacks revised down from $3.30, suggesting earnings estimate risk is to the downside. Key watch items: longevity deal pipeline, PGIM flows, Japan profitability, and 2026 guidance quality. Stock could gap 5-8% either direction based on guidance tone.

-

🇯🇵 Japan structural headwinds (40% of earnings): With Japan contributing 90% of international revenue (40% of total earnings), structural low interest rates and demographic decline create long-term headwinds that are nearly impossible to offset. This isn't a cyclical issue - Japan's aging population and deflationary pressures are multi-decade challenges. Limited growth prospects in a market generating 40% of profits is a major strategic constraint.

-

⚖️ MetLife's digital competitive advantage widening: MetLife's Xcelerator platform reaching 4.5 million customers with $200M in premiums demonstrates PRU is LOSING the digital transformation race. Younger customers prefer digital-first experiences, and PRU's traditional distribution model is more expensive and less scalable. This gap will only widen through 2026 unless PRU invests aggressively (which would pressure near-term margins).

-

👔 CIO transition risk in volatile environment: Timothy Schmidt retiring after 16 years and being replaced by Matthew Armas on March 12, 2026 introduces execution risk at the WORST possible time. Managing $1.6T in assets with $30.7B in unrealized losses during Fed rate normalization requires expert judgment. Any missteps in asset allocation, hedging, or risk management could be catastrophic. Market will scrutinize every decision.

-

📊 Valuation offers limited margin of safety: At 15.36x trailing P/E (above 10-year average of ~12-14x) after a -10.6% YTD decline, PRU is not "cheap" despite the pullback. The market is pricing in modest growth, but requires flawless execution on longevity deals, PGIM expansion, and Japan stabilization. Any disappointment magnified 2-3x at this valuation. Downside to $100-105 (13-15x P/E) if growth stalls.

-

🚨 Regulatory capital requirement wildcards: 2024 Annual Report highlights risks from group-wide supervision and capital requirement changes. If regulators impose stricter capital requirements on systemically important insurers, PRU could be forced to raise equity (dilutive) or reduce shareholder returns (dividend cut/buyback suspension). This risk is BINARY - you don't know when/if it hits, but the impact would be severe.

-

💰 Private credit competition intensifying: While PGIM's $341.7B in private alternatives is impressive, EVERY asset manager is flooding into private credit (Blackstone, Apollo, KKR, Ares). Competition for deal flow will compress spreads and reduce returns, pressuring the 10% of earnings from asset management. If PGIM can't maintain performance, outflows accelerate and fee income collapses.

-

🐋 Smart money buying $2.1M insurance at $100 strike: This institutional put purchase signals sophisticated players are WORRIED about downside below $100 despite reasonable fundamentals. When funds pay $7.05/share ($2.1M total) for 13-month protection rather than staying fully long, it's a major caution flag. The 11x open interest increase shows this isn't normal hedging - this is concern about tail risk.

-

📈 Gamma ceiling at $115 creates natural resistance: Massive 7.66B call gamma at $115 (strongest single level) means market makers will systematically SELL into rallies to hedge their exposure. This creates mechanical selling pressure making breakouts extremely difficult. Would need sustained institutional buying or major positive catalyst (rate cuts, huge longevity deal) to overcome. Current price around $114 sitting right under this ceiling.

-

🎢 Analyst downgrades accelerating: JPMorgan lowered price target to $133 from $136, CFRA downgraded from Buy to Hold with $110 target. These aren't aggressive bear calls - they're NEUTRAL calls suggesting limited upside. When consensus shifts from "Buy" to "Hold", it signals the easy money has been made. 71% of analysts now rate Hold - that's not a bullish setup.

-

💸 Dividend sustainability questions if earnings disappoint: While payout ratio of 73.37% appears sustainable, it's creeping higher (was 65-70% historically). If 2026 EPS disappoints at $13-13.50 (vs consensus $14.95), payout ratio could exceed 80%, forcing difficult choice: cut dividend (stock craters) or maintain and constrain capital flexibility (limits buybacks/growth investment).

-

📉 Broader financial sector rotation risk: If equity markets rotate OUT of financials into growth/tech (as happened in 2024), PRU could suffer despite solid fundamentals. Insurance stocks are rate-sensitive and economically sensitive - a recession or prolonged rate uncertainty could trigger 15-20% sector-wide selloff regardless of company-specific performance.

🎯 The Bottom Line

Real talk: Someone just spent $2.1 MILLION on long-dated put protection 62 days before Prudential's critical Q4 earnings report. This isn't bearish on PRU's long-term viability - it's sophisticated risk management by institutions who want to protect a substantial position against financial sector volatility, interest rate uncertainty, and company-specific execution risks through the entire 2026 earnings cycle.

What this trade tells us:

- 🎯 Sophisticated player expects UNCERTAINTY through 2026 (not necessarily crash, but protecting against 13-24% downside scenario)

- 💰 They're worried enough about $113→$100 move (11.7% decline) to pay $7.05/share for 13-month insurance (6.2% of stock price)

- ⚖️ The LEAP duration (401 days) shows they see extended risk - not just earnings, but full 2026 cycle including CIO transition, Fed policy, Japan headwinds

- 📊 They structured at $100 strike (11.7% below current) which sits at a major psychological level - expects that IF stock breaks $105-110 support, it could flush to $100 quickly

- ⏰ January 15, 2027 expiration captures Q4 2025 earnings (Feb 10), all four 2026 quarterly reports, CIO transition (March 12), Alexforbes sale proceeds, and full Fed policy evolution

This is NOT a "sell everything" signal - it's a "protect your gains and manage downside risk" signal for long-term holders.

If you own PRU:

- ✅ Consider your cost basis - if you bought above $120, this hedge makes sense to protect against further decline

- 📊 If holding for dividend income (5% yield), ensure you can stomach potential 10-15% volatility through 2026

- ⏰ Set MENTAL STOP at $108-110 (gamma support) if you're trading position rather than long-term hold

- 🎯 Consider trimming 20-30% if stock rallies to $118-120 (gamma resistance) to reduce exposure

- 🛡️ For large positions (500+ shares), buying 1-2 protective $100 puts at $7.05 each = 1.2% insurance cost on $56K+ position

If you're watching from sidelines:

- ⏰ February 10, 2026 after close is the moment of truth - DO NOT enter before Q4 earnings clarity!

- 🎯 Post-earnings pullback to $105-110 would be EXCELLENT entry (7-11% off current price with strong gamma support + 5.4-5.7% dividend yield)

- 📈 Looking for confirmation of: Strong longevity deal pipeline ($5B+ annual run rate), PGIM flows positive, Japan stabilization, 2026 EPS guidance $15+

- 🚀 Longer-term (12-18 months), successful PGIM private credit expansion ($400B AUM), LPL partnership momentum (3,500+ advisors), and interest rate normalization are legitimate catalysts for $125-135

- ⚠️ Current valuation (15.36x P/E) is FAIR not CHEAP - requires growth delivery to justify, downside to $100-105 (13-14x) if execution falters

If you're income-focused:

- 💰 5.04% dividend yield is ATTRACTIVE vs 2.84% sector average and 10-year Treasury at ~4.2%

- ✅ PRU's dividend safety appears solid (73% payout ratio, paid since 2002, $1B buyback authorization)

- 📊 Dollar-cost averaging into $108-112 range builds position with margin of safety

- ⏰ Quarterly $1.35/share payments provide steady income while waiting for stock appreciation

- 🎯 Target entry below $110 for 5.5%+ yield on cost with potential 15-20% capital appreciation to $125-130 over 18-24 months

Mark your calendar - Key dates:

- 📅 December 17-18 (7-8 days) - FOMC meeting, expected 25bp rate cut (impacts unrealized losses)

- 📅 December 19 - Monthly/Quarterly OPEX (±2.5% implied move window)

- 📅 December 31 - Year-end (tax loss harvesting pressure possible)

- 📅 February 10, 2026 (62 days) - Q4 2025 earnings report (MAJOR CATALYST)

- 📅 February 2026 - Likely ex-dividend date for Q1 2026 dividend ($1.35/share)

- 📅 March 12, 2026 (92 days) - CIO transition, Matthew Armas takes over from Timothy Schmidt

- 📅 Mid-2026 - Potential Alexforbes stake sale ($627M proceeds)

- 📅 January 15, 2027 (401 days) - Expiration of this $2.1M put trade

Final verdict: PRU's fundamentals remain SOLID - strong capital ratios (409% RBC), growing longevity risk transfer business ($4B NN Life deal, strong pipeline), PGIM private credit expansion ($341.7B and growing), and attractive 5% dividend yield. BUT, with $30.7B in unrealized losses constraining flexibility, 40% earnings exposure to structurally challenged Japan market, digital transformation lag vs MetLife, and CIO transition risk, the path to significant upside is UNCERTAIN through 2026. The $2.1M institutional put buy at $100 is a CLEAR signal: smart money is protecting downside risk, not betting on dramatic upside.

Be patient. Wait for Q4 earnings clarity February 10. Look for entry points $105-110 for dividend income story. The 5% yield will still be there in 2 months, and you'll have much better visibility on 2026 earnings trajectory, Fed policy path, and management's strategic priorities.

This is a show-me story for 2026. Protect capital, collect dividends, wait for catalysts. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Long-dated put purchases like this represent portfolio insurance strategies that typically expire worthless (60-80% of the time) - the premium paid is the cost of downside protection. Always do your own research and consider consulting a licensed financial advisor before trading. Insurance and financial services stocks are sensitive to interest rate changes, regulatory developments, and economic cycles, creating significant volatility risk.

About Prudential Financial: Prudential Financial is one of the largest US life insurers, offering annuities, life insurance, pension risk transfer solutions, and asset-management products through its PGIM division ($1.4 trillion AUM), with a market cap of $39.1 billion in the Life Insurance industry.