QCOM: Someone Just Bet $3.3M That Qualcomm Stays Range-Bound!

January 9, 2026 | Unusual Activity Detected

The Quick Take

A whale just collected $3.3 million in premium by selling a massive short strangle on Qualcomm - betting the stock stays between $165 and $200 through March expiration. With 10,000 call contracts at the $200 strike and 3,600 put contracts at $165, this trader is positioning for QCOM to chop sideways despite earnings, the Arm trial, and CES buzz. Translation: They're betting the hype won't move the needle in either direction - a NEUTRAL/RANGE-BOUND bet collecting $3.3M upfront while the rest of the market picks sides!

Company Overview

Qualcomm Inc. (QCOM) is the world's leading fabless semiconductor company specializing in wireless technology:

- Market Cap: $195-198 Billion

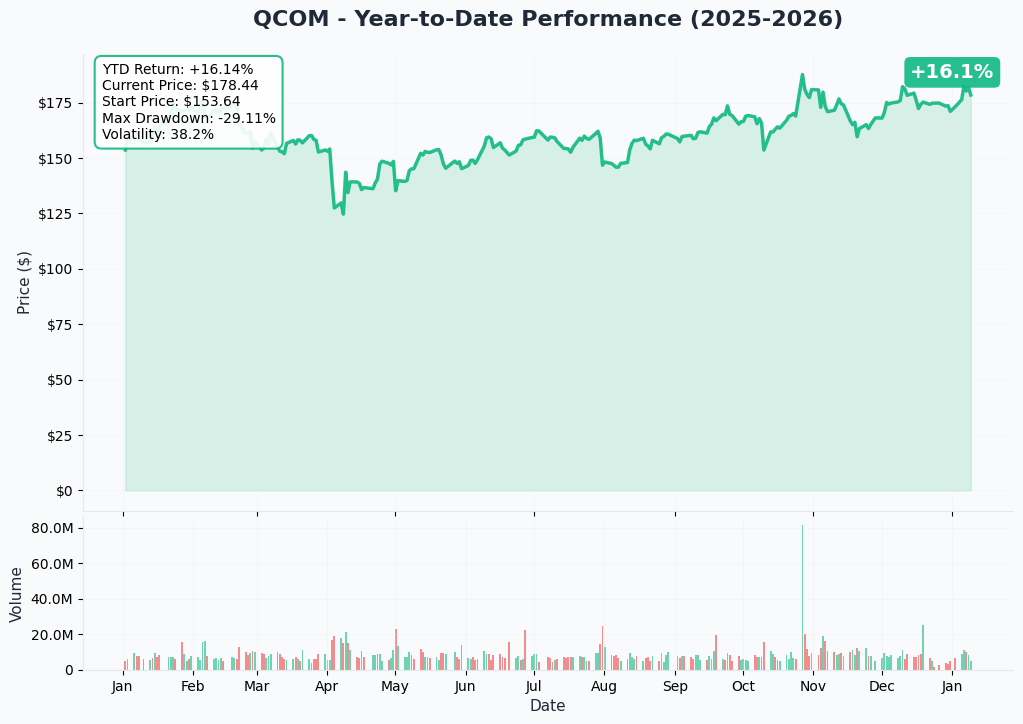

- Current Price: $178.32 (up 13.27% YTD)

- P/E Ratio: 36.38

- Dividend Yield: 1.9%

- 52-Week Range: $120.80 - $205.95

- Core Business: Snapdragon mobile processors, 5G modems, automotive chips, AI PC processors

- Key Holdings: 74-75% institutional ownership, including Norges Bank (Norway Sovereign Fund) new position

Qualcomm is experiencing a transformative period with diversification beyond smartphones into automotive (now exceeding $1B quarterly revenue), AI PCs (Snapdragon X2 series), and data center AI chips (AI200 launching in 2026).

The Option Flow Breakdown

The Tape (January 9, 2026 @ 10:49:14):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Z-Score | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:49:14 | QCOM | ASK | SELL | CALL $200 | 2026-03-20 | $2.1M | $200 | 10K | 6.5K | 1.54 | $178.32 | $2.10 |

| 10:49:14 | QCOM | ASK | SELL | PUT $165 | 2026-03-20 | $1.2M | $165 | 3.6K | 1.2K | 3.0 | $178.32 | $3.33 |

What This Actually Means

This is a textbook short strangle - a premium-collection strategy where the trader is playing the role of the house at the casino! Here's the breakdown:

Short Strangle Structure:

- Short leg (call): Sold 10,000 contracts of March 20, 2026 $200 calls for $2.10 each = $2.1M total

- Short leg (put): Sold 3,600 contracts of March 20, 2026 $165 puts for $3.33 each = $1.2M total

- Total Premium Collected: $3.3M

- Current Price: $178.32

- Risk Profile: UNLIMITED on upside, substantial on downside

What's the trader's thesis?

This institutional player believes QCOM stays range-bound between $165 and $200 through March 20th expiration. They're collecting $3.3M upfront and betting that:

- Earnings (Feb 4) won't cause a breakout move

- The Arm trial (March 2026) won't swing sentiment dramatically

- CES momentum is already priced in

- Volatility is overpriced - time to sell premium, not buy it

Here's the math:

- Profit Zone: QCOM stays between ~$161.70 and ~$203.30 (breakeven levels after adding premium)

- Sweet Spot: Stock pins between $165-$200 at March expiration = max profit

- Max Gain: $3.3M (if both options expire worthless)

- Max Risk: UNLIMITED on the upside if QCOM rockets, substantial on the downside if it crashes

Unusual Score: HIGHLY UNUSUAL

The put leg shows 3.0 standard deviations above average activity - this happens a few times per year at most. The call leg at 1.54x Vol/OI ratio signals institutional size, not retail speculation. Combined with the $3.3M commitment, this is sophisticated premium-selling, not directional betting.

Technical Setup / Chart Check-Up

YTD Performance

QCOM is currently trading at $178.32, up +13.27% YTD. The stock is sitting comfortably above all major moving averages:

- 50-Day SMA: $169.86 (price is 5% above)

- 100-Day SMA: $163.80 (price is 8.9% above)

- 200-Day SMA: $156.21 (price is 14.2% above)

Technical signals are flashing Strong Buy with 10 buy signals vs. only 2 sells according to TipRanks' technical analysis.

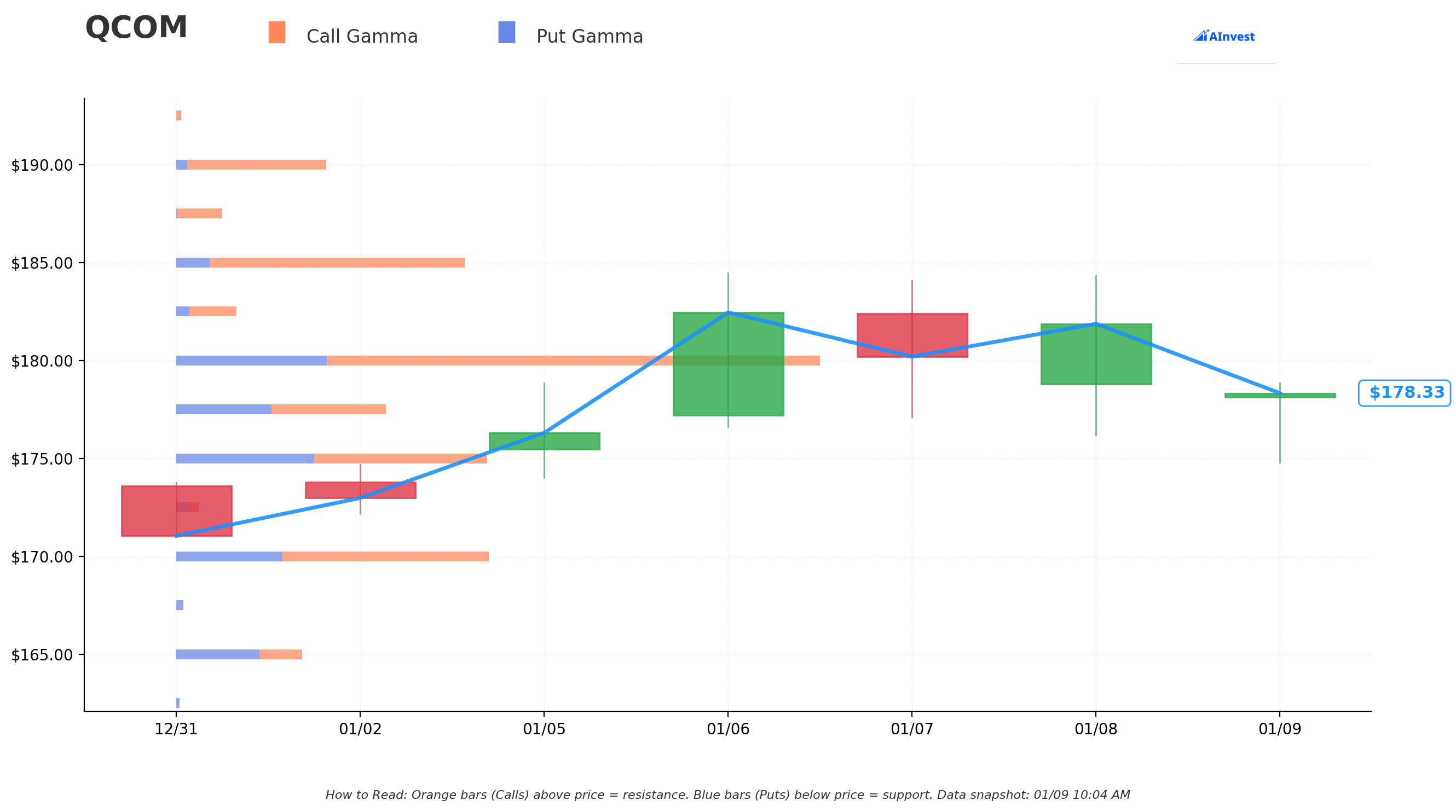

Gamma-Based Support & Resistance Analysis

Current Price: $178.32

The gamma exposure map reveals the magnetic price levels where market makers hold massive positions:

Resistance (Orange Bars):

- $180 - MASSIVE resistance wall (Net GEX: 13.48, Total: 25.26) - Only 0.9% away!

- $185 - Secondary resistance (Net GEX: 8.67)

- $190 - Moderate resistance (Net GEX: 5.04)

- $200 - The call strike target (Net GEX: 5.68) - 12.2% OTM

Support (Blue Bars):

- $177.50 - Immediate support (Net GEX: 0.75) - Just 0.5% below

- $175 - Key support (Net GEX: 1.36)

- $170 - Strong support (Net GEX: 3.94)

- $165 - The put strike target (Net GEX: -1.60) - 7.5% OTM

What this means for the short strangle:

The trader perfectly structured their strangle around gamma dynamics! Notice:

- $180 resistance (25.26M) is the FIRST hurdle - massive call gamma wall caps upside

- $200 strike (6.12M gamma) sits well above all major resistance - trader betting we don't get there

- $175-$177 support provides floor - stock has buyers at these levels

- $165 strike (4.93M gamma) sits below major support - trader betting we don't crash there

Net GEX Bias: Bullish (80.43M call gamma vs 38.68M put gamma = 41.75M net bullish)

Overall positioning remains bullish with significantly more call gamma than put gamma. This creates natural headwinds for downward moves (market makers buy dips) while the $180 level caps immediate upside. The strangle seller is betting this gamma structure keeps QCOM range-bound.

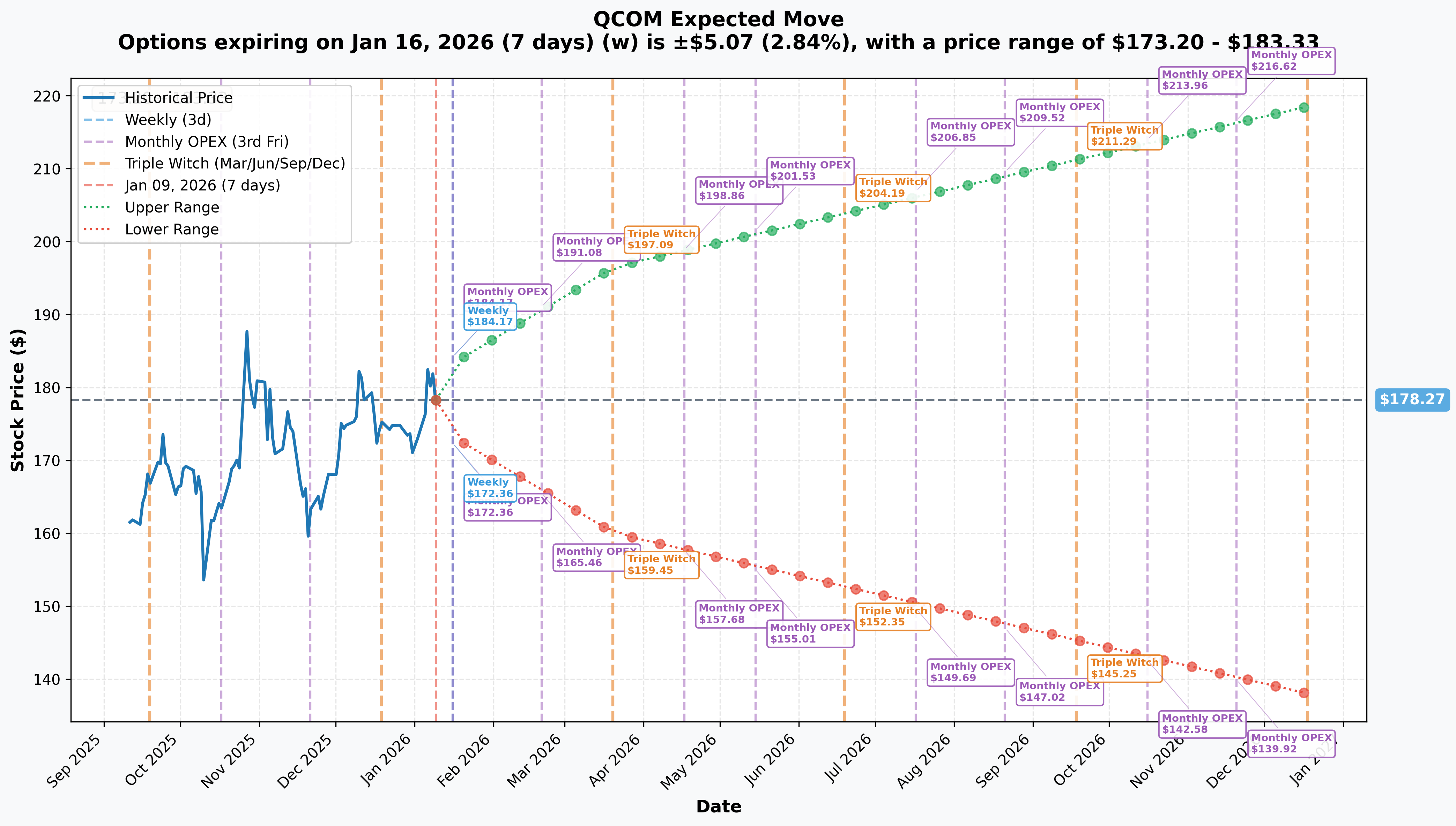

Implied Move Analysis

What the options market is pricing in:

| Timeframe | Expiry | Implied Move | Range |

|---|---|---|---|

| Weekly | Jan 16 | +/- 2.84% | $173.20 - $183.33 |

| Monthly | Feb 20 | +/- 7.2% | $165.46 - $191.08 |

| Mar Triple Witch | Mar 20 | +/- 10.24% | $160.02 - $196.52 |

| LEAPS | Dec 18 | +/- 22.6% | $137.98 - $218.56 |

Translation for regular folks:

The strangle seller's range ($165-$200) is WIDER than the implied move range ($160-$196.52). This means they're betting volatility comes in lower than expected - a classic premium-selling thesis. The market prices a ~10% move by March expiration; the strangle seller says "nope, we stay inside a ~20% range centered at $178."

Key insight: The short strangle is positioned EXACTLY outside the March implied range boundaries, showing sophisticated understanding of options pricing. The trader isn't making a wild lottery ticket bet - they're positioning as the house, collecting premium from speculators who think QCOM will make a big move.

Catalysts

Recent (Already Happened)

Q4 FY2025 Earnings Beat (November 5, 2025): Revenue of $11.27B crushed estimates by 4.8%. EPS of $3.00 beat by 4.5%. Automotive hit record $1B+ quarterly revenue.

Data Center AI Chip Announcement (October 27, 2025): Stock surged 20% in one day - biggest rally since 2019 - on AI200/AI250 chip reveal. First customer Humain signed for 200 megawatt deployment.

Arm Litigation Victory (September 2025): Complete victory over Arm in licensing dispute. Removed near-term legal uncertainty for PC chip roadmap.

CES 2026 (January 6-9, 2026): Snapdragon X2 Plus/Elite launch with 80 TOPS NPU. Samsung 2nm manufacturing talks confirmed by CEO at CES.

Upcoming (Before Expiration)

Q1 FY2026 Earnings - February 4, 2026: Guidance of $11.8-$12.6B revenue and $3.30-$3.50 EPS. Consensus expects another beat. Key metrics: automotive sustainability and AI PC traction.

Qualcomm vs. Arm Trial - March 2026: Qualcomm has sued Arm for breach of contract. Trial scheduled during the expiration window. Outcome could impact IP position and PC chip roadmap.

Samsung 2nm Decision - H1 2026: Final manufacturing deal expected. 33% cost savings vs. TSMC could be material.

Price Targets & Probabilities

Based on gamma levels, implied move data, and catalyst timing:

Bull Case: $190-$200 (25% probability)

- Needs: Strong Q1 earnings beat + favorable Arm trial developments

- Resistance at $185 and $190 creates friction

- The $200 call strike acts as a ceiling (call sellers will defend)

- Implied move upper bound is $196.52 - aligns with $200 resistance

Base Case: $170-$185 (55% probability)

- Stock gravitates toward high gamma zones ($175-$180)

- Earnings priced in, no major surprises

- Range-bound chop as market digests CES news

- This is exactly what the strangle seller is betting on

Bear Case: $160-$165 (20% probability)

- Needs: Earnings miss + negative Arm trial news

- Strong support at $170 and $165

- Implied move lower bound is $160.02

- The $165 put strike should hold as floor

Trading Ideas

Conservative: The "Sleep Well" Iron Condor

Strategy: Sell Mar 20 $160P / Buy $150P / Sell $205C / Buy $215C Credit: ~$3.50 (estimate) Max Risk: $6.50 per spread Win Rate: ~70% based on implied move

Why this works: You're betting on the same thesis as the whale but with defined risk. Your breakevens ($156.50 and $208.50) are wider than implied move. Earnings and trial are wildcards, but gamma structure supports range-bound action.

Balanced: The "Volatility Crush" Play

Strategy: Buy shares at $178 + Sell Mar 20 $190C covered call Premium: ~$4.50 (estimate) Breakeven: $173.50 Max Gain: $16.50 if called away at $190

Why this works: You own the stock with downside protection from premium. If QCOM pops on earnings, you participate up to $190. If it chops, you keep the premium. Worst case: stock tanks, but you have $4.50 cushion.

Aggressive: The "Fade the Strangle" Straddle

Strategy: Buy Mar 20 $180 straddle Cost: ~$18.00 (estimate) Breakevens: $162 and $198 Thesis: Earnings + trial = bigger move than priced in

Why this works: You're betting the whale is wrong. If Q1 earnings surprise big (either way) or the Arm trial drops a bombshell, you profit. Risk: time decay eats you alive if QCOM pins near $180.

Risk Factors

For the Short Strangle (What Could Go Wrong):

- Unlimited upside risk: If QCOM rips above $200 on blowout earnings or surprise acquisition, losses are theoretically unlimited

- Substantial downside risk: A crash below $165 on earnings miss or adverse trial ruling = major losses

- Earnings volatility: February 4 earnings is a binary event - could easily move stock 5-10%

- Arm trial uncertainty: March trial is during expiration window - unknown outcome

- Sector rotation: Semiconductors can swing violently on macro news

- China exposure: Significant revenue from Chinese smartphone OEMs - tariff risk remains

For Retail Following This Trade:

- Short strangles require significant margin and capital

- 70 days to expiration = lots of time for things to go wrong

- Two major catalysts (earnings + trial) within the window

- The whale can afford to be wrong - can you?

The Bottom Line

Real talk: A sophisticated trader just collected $3.3M betting that Qualcomm stays boring through March. With the stock at $178, they're saying it won't break below $165 (7.5% drop) or above $200 (12.2% jump) - even with Q1 earnings and the Arm trial on deck.

What this trade tells us:

- Neutral on direction - trader doesn't care if QCOM goes up or down slightly, just that it stays range-bound

- Bearish on volatility - betting implied volatility is too high and will collapse

- Confident in gamma structure - $165-$200 range aligns with support/resistance levels

- Risk tolerance - willing to take unlimited risk for $3.3M premium

The case for the whale being right:

- Gamma structure supports $175-$185 range

- Implied move of 10.24% keeps stock within their profit zone

- CES news already digested, earnings likely priced in

- Net GEX is bullish but capped at $180 resistance

The case for the whale being wrong:

- Earnings can surprise (Q4 beat by 4.8%!)

- Arm trial is a wildcard with material IP implications

- Samsung 2nm decision could be catalyst

- 70 days is a long time in semiconductor land

Action Plan:

If you're bullish: Consider the covered call strategy - you get upside to $190 with premium protection.

If you're neutral: The iron condor lets you fade the extremes with defined risk.

If you think volatility is underpriced: The straddle is your play, but earnings had better deliver fireworks.

Mark your calendars: February 4 (earnings) and March 2026 (trial) are the dates that make or break this trade.

Options Links:

About Qualcomm Inc. (QCOM): Qualcomm is a global leader in wireless technology, designing and licensing semiconductor products and services for mobile devices, automotive, IoT, and emerging AI applications. With $44 billion in FY2025 revenue and a $195B+ market cap, the company is diversifying beyond its smartphone dominance into automotive ($1B+ quarterly), AI PCs (Snapdragon X2), and data center AI chips (AI200/AI250).

Disclaimer: This analysis is for educational purposes only and does not constitute investment advice. Options trading involves significant risk and is not suitable for all investors. The short strangle strategy described carries unlimited risk on the upside and substantial risk on the downside. Always do your own research and consult with a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.