☕ SBUX $1.2M Bullish Bet - Betting on Turnaround Glory! 🚀

📅 December 23, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up $1.2 MILLION on Starbucks calls this morning at 11:26! This bullish bet bought 1,500 contracts of June 2026 $85 strike calls - betting big that CEO Brian Niccol's turnaround plan delivers over the next 6 months. With SBUX trading at $83.74, these slightly out-of-the-money calls are a pure conviction play that the "Back to Starbucks" strategy succeeds, the China JV removes the overhang, and the stock rebounds to $85+ by June. Translation: Institutional money is betting the coffee giant gets its mojo back!

📊 Company Overview

Starbucks Corporation (SBUX) is the world's largest coffee brand and retail coffeehouse chain:

- Market Cap: $97.98 Billion (down from prior peaks amid turnaround efforts)

- Industry: Retail - Eating & Drinking Places (Coffee retail and beverage services)

- Current Price: $83.74

- Primary Business: 41,000 cafes across 80+ countries, generating revenue through company-operated stores (52%), licensed locations, roasteries, and packaged products

- Geographic Split: North America (74%), International (21%), Channel Development (5%)

💰 The Option Flow Breakdown

The Tape (December 23, 2025 @ 11:26:05):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:26:05 | SBUX | ASK | BUY | CALL $85 | 2026-06-18 | $1.2M | $85 | 1,500 | - | 1,500 | $83.74 | $8.00 |

🤓 What This Actually Means

This is a turnaround conviction play with solid risk/reward! Here's the breakdown:

- 💸 Premium paid: $1.2M ($8.00 per contract × 1,500 contracts)

- 🎯 Strike positioning: $85 is just 1.5% above current price ($83.74) - barely out-of-the-money

- ⏰ Time horizon: 177 days to June expiration captures TWO critical earnings reports (Q1 FY2026 in Feb, Q2 FY2026 in April) plus Investor Day in January

- 📊 Leverage structure: Represents 150,000 shares worth ~$12.6M with only $1.2M at risk

- 🎪 Catalyst-rich period: China JV closure (Q2 FY2026), 1,000 store renovations completion, MI325X product launches

What's really happening here: This trader is betting that Niccol's turnaround gains serious traction over the next 6 months. The $85 strike is positioned just above the current gamma resistance level at $85.0 (0.7893 call gamma), suggesting they expect a breakout above this technical ceiling. If SBUX rallies to $91 (the call wall), these calls would be worth $6.00 intrinsic value ($91-$85) for a 75% gain. At $94 (key resistance), they'd be worth $9.00 for 112% return. This is NOT a defensive hedge - this is an aggressive bullish bet on recovery.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-score 10.78) - This happens only a few times per year! We're talking about 10+ standard deviations above normal SBUX option activity. The massive size (1,500 contracts) coupled with the strategic June expiration (captures full turnaround thesis) shows sophisticated institutional positioning ahead of major catalysts.

📈 Technical Setup / Chart Check-Up

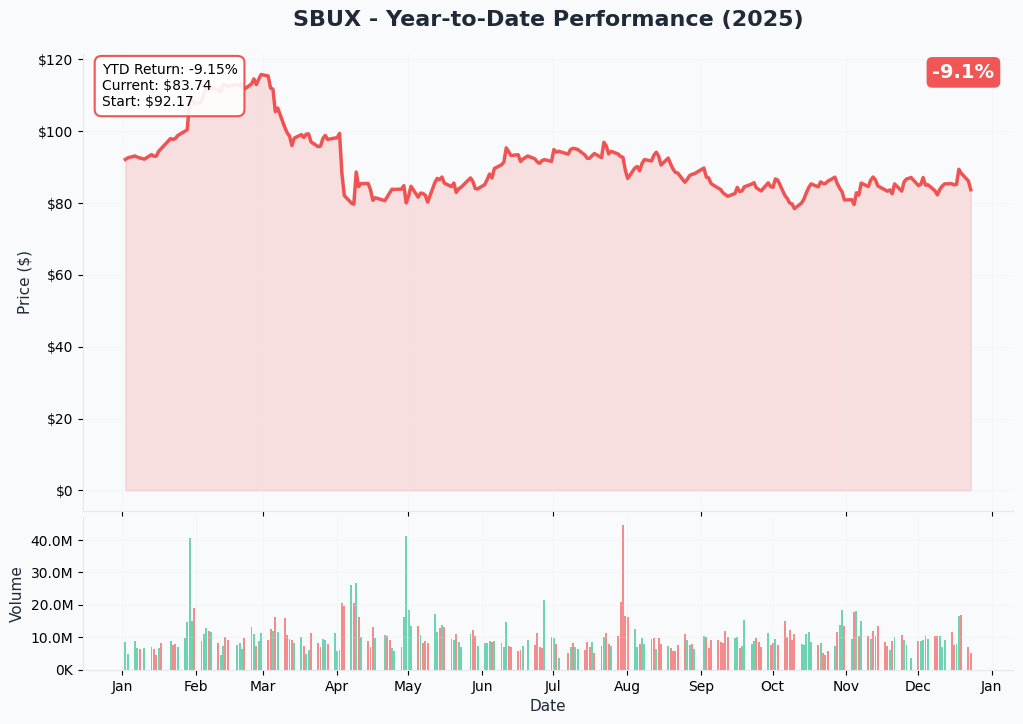

YTD Performance Chart

SBUX has been on a challenging journey this year - down from August highs near $98 to current levels around $83.74. The chart shows a clear narrative: peaked in late July/early August, then sold off sharply through mid-August to the low $70s, followed by recovery attempts that have stalled at the $85-88 range.

Key observations:

- 📉 Trading range: Stuck between $75 support and $91 resistance for the past few months

- 🎢 Recent volatility: Multiple failed breakout attempts above $85-88 zone

- 📊 Current position: Trading near the middle of the range at $83.74, just below the $85 strike

- ⚠️ Sentiment shift: Market still digesting the turnaround plan - needs proof of execution

- 🚀 Bullish setup IF: Can break and hold above $85, next target is $91 call wall

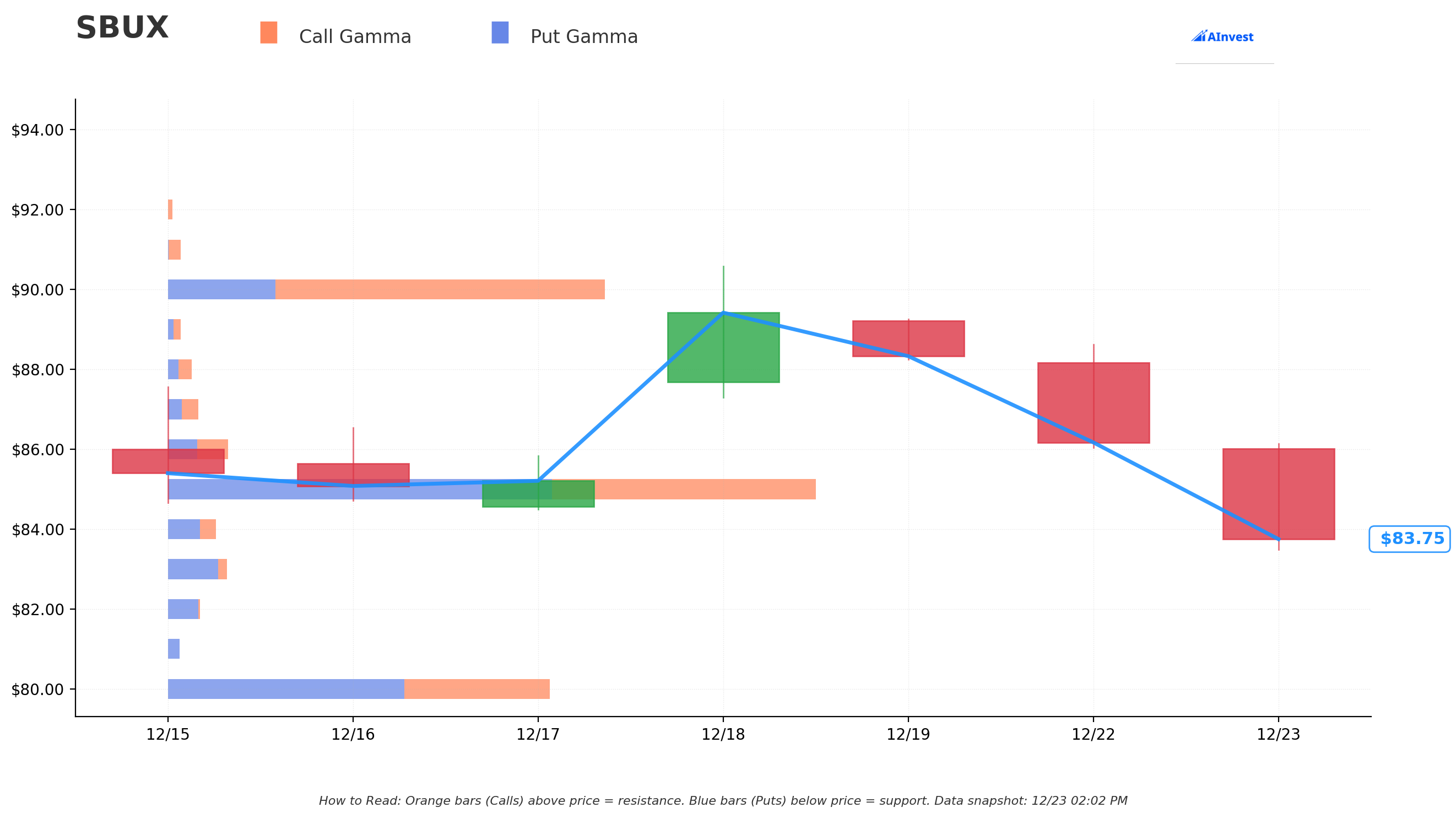

Gamma-Based Support & Resistance Analysis

Current Price: $83.74

The gamma exposure map reveals critical price levels that will govern near-term action:

🟠 Resistance Levels (Call Gamma Above Price):

- $85 - Immediate ceiling with 0.7893 call gamma vs 0.7413 put gamma (net +0.048) - THIS IS WHERE THE TRADE IS STRUCK!

- $91 - MASSIVE resistance at call wall (HVL) with 0.1755 call gamma (highest call level) - major breakout target

- $92 - Secondary ceiling at 0.1474 call gamma (net +0.0563)

- $94 - Extended resistance at 0.1163 call gamma (net +0.0618)

- $97 - Overhead ceiling with unusual put gamma dominance (0.1079 put vs 0.0739 call - net -0.034)

🔵 Support Levels (Put Gamma Below Price):

- $76 - Minor support zone with 0.1313 call gamma vs 0.098 put gamma (net +0.0333)

- $75 - Strong support floor at 0.293 call gamma vs 0.250 put gamma (net +0.0433)

- $55 - Deep put wall with 0.0599 put gamma (extreme downside protection level)

What this means for traders: SBUX is trading right at a critical inflection point. The $85 strike where this call buyer positioned has MASSIVE gamma (0.7893 call + 0.7413 put = 1.53 total gamma) - this is the single largest concentration of option activity on the board! This creates a powerful "pin" effect where the stock gravitates toward $85 as market makers hedge their exposure.

Notice the trade structure? The call buyer struck EXACTLY at $85 where there's maximum gamma concentration. They're betting on a breakout ABOVE this level to $91 (the call wall and HVL). If SBUX can clear $85 resistance and momentum accelerates, the path to $91-94 opens up quickly (8-12% upside from current levels).

Net GEX Bias: Moderately Bullish - Most key levels above current price show positive net gamma (call dominance), but the massive $85 level acts as current equilibrium. Downside protection solid at $75 floor.

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 26 - 3 days): ±$1.10 (±1.31%) → Range: $82.64 - $84.84

- 📅 Monthly OPEX (Jan 16 - 24 days): ±$3.77 (±4.50%) → Range: $79.97 - $87.51

- 📅 Quarterly Triple Witch (Mar 20 - 87 days): ±$9.29 (±11.09%) → Range: $74.45 - $93.03

- 📅 June OPEX (Jun 18 - 177 days - THIS TRADE!): Expected between quarterly and yearly (estimate ±14-16%) → Range: ~$72-96

Translation for regular folks: Options traders are pricing in a relatively quiet week ahead (only 1.3% move through Dec 26), but a MUCH larger move by January OPEX (4.5% move) which captures Q1 FY2026 earnings on February 3rd and the critical Investor Day in January. The market expects the real fireworks in Q1 2026 as the turnaround thesis gets tested.

The June 18th expiration (when this $1.2M call trade expires) sits in a HIGH catalyst density zone. Based on the quarterly implied move of 11% and yearly of 22%, a 6-month horizon suggests ~14-16% potential move, putting the upper range around $95-97. This aligns perfectly with the gamma resistance levels at $91-94! The call buyer needs SBUX to break above $85 and rally toward the $90-95 zone over the next 6 months to generate serious profits.

Key insight: The January OPEX upper range of $87.51 sits comfortably above the $85 strike, while the March upper range of $93.03 reaches the major resistance cluster. This trade is betting the company delivers positive surprises in Q1/Q2 that drive the stock steadily higher.

🎪 Catalysts

🔥 Immediate & Near-Term Catalysts (Next 90 Days)

Investor Day - January 2026 (CRITICAL!) 📊

SBUX will host an Investor Day in Q2 fiscal year 2026 (January 2026) where management will provide comprehensive long-term guidance:

- 🎯 Full fiscal 2026 financial guidance and long-term targets for first time under Niccol1

- 💰 Capital allocation philosophy details including dividend policy and buyback plans2

- 🏗️ 1,000 café renovation timeline and expected ROI from the $500M+ investment3

- 🚀 2026 innovation pipeline including improved bakery, customizable matcha menu, app enhancements4

- 💼 Green Apron Service scaling plans and margin recovery roadmap5

- 📈 Multi-year recovery trajectory - management has cautioned "turnarounds are not always linear"6

Why this matters: This is THE moment of truth for the turnaround thesis. After suspending guidance in Q4 FY2025 to allow Niccol time for assessment, the market desperately needs a concrete roadmap. Strong, credible guidance could catalyze a breakout above $85-88 resistance toward the $91-94 targets. Weak or overly conservative guidance would likely send the stock back to $75-76 support.

Q1 Fiscal 2026 Earnings - February 3, 2026 (After Market Close) 💰

SBUX reports fiscal Q1 results on February 3, 2026 after market close7 covering the critical October-December 2025 holiday season:

Key metrics to watch:

- 📊 U.S. comparable store sales: Continuation of positive trend from September-October crucial

- 🇨🇳 China comparable sales: Impact of Boyu JV announcement and ongoing competition

- 🎁 Holiday performance: Gift card sales, seasonal beverage success, traffic patterns

- 💰 Operating margin trajectory: Post-restructuring efficiency gains vs wage/tariff pressures

- 👷 Union strike impact: November strikes during peak season could disrupt results

- ⚡ Green Apron progress: Update on service time improvements (80%+ stores under 4 minutes targeted)

Consensus expectations: Not yet established as company suspended guidance. Analysts watching for continued momentum from late FY2025 quarter when comp sales turned positive for first time in seven quarters.

Risk factors: Union strikes affecting 3,800+ partners hit during November-December peak season. Coffee tariff costs beginning to materialize. Any disappointment sends stock back to $75-76 support zone.

China Joint Venture Regulatory Approval - Q2 Fiscal 2026 (Jan-Mar 2026) 🇨🇳

The $4 billion sale of 60% controlling stake to Boyu Capital8 is expected to close in Q2 FY2026:

- 💵 Cash proceeds: Approximately $4 billion to Starbucks strengthens balance sheet for U.S. reinvestment

- 🤝 Strategic partnership: Boyu's local expertise and commercial real estate capabilities9 (controls SKP luxury malls, Jinke Smart Services)

- 🌏 Expansion pathway: Long-term plan to grow from current 8,000 to 20,000+ China stores8

- ✅ Regulatory hurdle: Requires Chinese government approval; Boyu's connections (cofounder is grandson of former President Jiang Zemin)9 likely advantageous

- 📈 Overhang removal: Could eliminate China weakness concerns, allow management focus on North America recovery

Market impact: Successful closure removes a major overhang. SBUX retains 40% upside exposure plus ongoing licensing fees while partnering with local experts who can navigate intense competition from Luckin Coffee (26,000+ stores) and tea chains1011.

🚀 Medium-Term Catalysts (Q2-Q4 2026)

1,000 Store Renovations Completion - Through End of 2026 🏗️

SBUX is renovating 1,000 cafés with improved lighting, seating, and welcoming aesthetic3:

- 💰 Investment: Over $500 million in labor and renovations through 2025-2026

- 🎯 Expected benefits: Improved customer experience, higher dwell time, premium positioning reinforcement

- 📅 Timeline: On track for completion by end of calendar 2026

- 📈 Revenue impact: Management expects gradual margin improvements as renovations complete

Green Apron Service Model Scaling 💚

The $500 million investment in additional labor hours12 aims to improve speed, hospitality, and accuracy:

- ⏱️ Service time target: More than 80% of stores achieving under 4 minutes average13

- ☕ Coffeehouse experience: Handwritten cup notes, macchiato art, ceramic mugs, unlimited free refills, condiment bar restoration1415

- 📊 Early results: Model contributed to first positive comparable sales in seven quarters in Q4 FY2025

Coffee Tariff Cost Impact - Peak Expected 2026 ☕

50% U.S. tariff on Brazilian coffee imports16 implemented August 2025 creates margin pressure:

- 🇧🇷 Brazil sourcing: Approximately 22% of Starbucks beans from Brazil17 (33% of total U.S. coffee supply)

- 💸 Cost impact: 0.5% increase in North American COGS; $0.02 EPS impact from 3.5% cost increase in ready-to-drink division18

- ⏰ Timing: Long-term contracts delay impact; costs expected to peak in 202619

- 🌍 Mitigation: Expanding Central American sourcing, diversifying across 30 countries globally20

- 💵 Pricing: Holding prices steady through remainder of fiscal 2025 despite pressures21

Risk: U.S. ground coffee prices hit record $8.41/lb in July 2025, up 33% year-over-year22. Despite "unavailable natural resource" designation potentially exempting coffee from reciprocal tariffs23, policy requires ongoing negotiations and could change.

Q2-Q3 Fiscal 2026 Earnings - April and July 2026

- Q2 FY2026 (April 2026): Covers January-March period including Investor Day impact and China JV closure

- Q3 FY2026 (July 2026): First full quarter under new China JV structure; critical summer season performance

- Before June expiration: Both earnings reports occur BEFORE the $85 calls expire, providing two more binary catalysts

⚠️ Past Catalysts (Already Happened)

Q4 Fiscal 2025 Earnings - Reported October 30, 2025

The Q4 FY2025 results showed early turnaround signs24:

- 💵 Revenue: $9.1 billion (down 3% YoY)

- 💰 EPS: $0.80 GAAP and Non-GAAP (down 25% vs prior year)

- 📈 Comparable sales: Increased 1% - FIRST POSITIVE in seven quarters25

- 🇺🇸 U.S. trend: Flat for quarter but turned positive in September, remained positive through October2627

- 🇨🇳 China sales: Increased 2% driven by 9% transaction increase offset by 7% ticket decline

- 📊 Operating margin: 14.4%, contracted 380 basis points YoY due to wage investments and promotional activity

Strategic Developments:

- $1 billion restructuring plan28: 400 store closures in North America, 900 nonretail employee layoffs in December 2025

- Menu streamlining29: Cutting 30% of food/beverage offerings to improve operational efficiency

- Union negotiations stalemate30: Over 3,800 unionized baristas (4% of workforce) participated in strikes after 92% strike authorization vote

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through June 18th expiration:

📈 Bull Case (40% probability)

Target: $91-$97 (Call Wall to Extended Resistance)

How we get there:

- 💪 Investor Day delivers: Comprehensive long-term guidance shows credible path to margin recovery and sustainable comp sales growth

- 📊 Q1 earnings beat expectations: Holiday season strong, U.S. comp sales accelerating (3-4%+ growth), China stabilizing

- 🇨🇳 China JV closes smoothly: Removes overhang, allows management to focus on North America, $4B cash infusion

- ☕ Green Apron Service wins: 90%+ stores hitting sub-4-minute service times, customer satisfaction scores improving

- 🏗️ Renovation ROI validates: Completed stores showing measurable sales lift and traffic improvement

- 💰 Q2 earnings surprise: March quarter shows continued momentum, guidance raised for full year

- 🎯 Break above $85 gamma resistance: Triggers technical rally to $91 call wall, then potential push to $94-97 zone

- 📈 Multiple expansion: Market re-rates SBUX as turnaround success story, P/E multiple expands from compressed levels

Call option P&L in Bull Case:

- Stock at $91 by June: Calls worth $6.00 intrinsic ($91-$85), profit = $3.00/share × 1,500 = $450K gain (37.5% ROI)

- Stock at $95 by June: Calls worth $10.00 intrinsic ($95-$85), profit = $2.00/share × 1,500 = $300K gain (25% ROI) - WAIT, this is $10 value minus $8 cost = +$2!

- Stock at $97 by June: Calls worth $12.00 intrinsic ($97-$85), profit = $4.00/share × 1,500 = $600K gain (50% ROI)

Probability assessment: 40% because early turnaround signs are positive (Q4 comp sales turned positive, September-October momentum continued), Niccol has proven track record (Chipotle success), and multiple catalysts align favorably over 6-month window. Requires solid but achievable execution.

🎯 Base Case (45% probability)

Target: $82-$88 Range (Choppy Consolidation)

Most likely scenario:

- ✅ Investor Day meets expectations: Guidance credible but not spectacular, market "buys" the plan but wants to see execution

- 📱 Q1 earnings in-line: Meets lowered expectations, shows progress but nothing transformational

- 🇨🇳 China JV closes as planned: Neither major positive nor negative, execution phase begins

- ⚖️ Gradual improvement: U.S. business slowly improving but labor/tariff costs offset margin gains

- 📊 Trading in range: Stock oscillates between $82-88 for several months as market digests progress

- 💤 Waiting for proof: Investors need to see 2-3 quarters of sustained comp sales growth before conviction builds

- ⏰ Time decay hurts: Calls lose extrinsic value as expiration approaches without decisive breakout

Call option P&L in Base Case:

- Stock at $85 by June: Calls worth $0 (at-the-money), loss = -$8.00/share × 1,500 = -$1.2M (100% loss)

- Stock at $87 by June: Calls worth $2.00 intrinsic ($87-$85), loss = -$6.00/share × 1,500 = -$900K (75% loss)

- Stock at $88 by June: Calls worth $3.00 intrinsic ($88-$85), loss = -$5.00/share × 1,500 = -$750K (62.5% loss)

This is the call buyer's risk scenario: Stock grinds modestly higher but not enough to overcome the $8.00 premium paid. Even if fundamentals improve, insufficient price appreciation by June expiration results in significant losses. Time decay accelerates in final 90 days.

Why 45% probability: Most turnarounds take time to gain traction. Management cautioned "recoveries are not always linear"6. Likely sees gradual progress but not explosive rally needed for these calls to profit materially.

📉 Bear Case (15% probability)

Target: $75-$79 (Test Support Zone)

What could go wrong:

- 😰 Investor Day disappoints: Guidance too conservative or lacks credibility, market loses faith in turnaround timeline

- 🚨 Q1 earnings miss: Holiday season weaker than expected, comp sales momentum stalls, margins compressed

- ⏰ China JV delays: Regulatory approval issues or complications in transition planning

- 👷 Labor issues escalate: Union strikes expand beyond 4% of stores, additional unfair labor practice complaints

- ☕ Coffee tariff impact worse than expected: Margin compression forces price increases, hurting traffic

- 🇨🇳 China competition intensifies: Luckin Coffee and tea chains continue taking share despite JV partnership

- 💸 Recession fears: Macro environment weakens, premium coffee spending most vulnerable in downturn

- 📉 Break below $82 support: Triggers cascade back to $75-76 gamma support zone

Critical support levels:

- 🛡️ $76: Minor support (0.1313 call gamma) - first test if breakdown occurs

- 🛡️ $75: Major support floor (0.293 call + 0.250 put gamma) - must hold or sentiment shifts very bearish

Call option P&L in Bear Case:

- Stock at $79 by June: Calls worth $0 (out-of-the-money), loss = -$8.00/share × 1,500 = -$1.2M (100% loss)

- Stock at $75 by June: Calls worth $0 (out-of-the-money), loss = -$8.00/share × 1,500 = -$1.2M (100% loss)

Probability assessment: Only 15% because fundamentals showing early improvement (first positive comp sales in seven quarters25, September-October momentum), Niccol's track record strong31, and multiple positive catalysts ahead. Would require multiple negative surprises to reach this scenario.

💡 Trading Ideas

🛡️ Conservative: Wait for Investor Day Clarity

Play: Stay on sidelines until after January Investor Day provides concrete guidance

Why this works:

- ⏰ Catalyst clarity: Investor Day in January will reveal management's actual long-term plan and targets

- 💸 Better visibility: Will know if guidance credible and market reaction before committing capital

- 🎯 Entry timing: Post-Investor Day pullback (if any) or breakout confirmation above $85-88 provides better risk/reward

- 📊 Avoid premium decay: Not paying inflated option premiums before major binary event

- 🤔 Niccol track record: While proven at Chipotle, Starbucks turnaround more complex - need to see execution proof

Action plan:

- 👀 Watch January Investor Day closely for FY2026 guidance quality, margin recovery timeline, comp sales targets

- 🎯 If guidance strong and stock breaks above $85-88 with conviction, consider stock position or longer-dated calls

- ✅ If guidance disappoints and stock pulls back to $75-76 support, that's the buying opportunity with margin of safety

- 📊 Monitor Q1 earnings (Feb 3) for validation of Investor Day promises

- ⏰ Re-evaluate in March/April after seeing Q1 results and China JV closure impact

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Preserve capital during uncertain period. Get better entry after key catalysts clear. Maintain flexibility.

⚖️ Balanced: Defined-Risk Bull Spread (Copy Smart Money Structure)

Play: After Investor Day, sell call spread mirroring institutional positioning but with defined risk

Structure: Buy $85 calls, Sell $91 calls (June 18 expiration - SAME as the $1.2M trade)

Why this works:

- 🎯 Defined risk: $6 wide spread ($600 max risk per spread) vs unlimited exposure of naked long calls

- 📊 Lower cost: Selling the $91 calls (call wall resistance) reduces net debit significantly

- 🎪 Same thesis: Betting on turnaround success driving stock from current $83.74 to $85-91 range

- ⏰ Still 177 days: Plenty of time for two earnings reports and catalyst development

- 💰 Better risk/reward: Capped upside but dramatically reduced cost basis improves probability of profit

- 🛡️ Takes advantage of gamma levels: Long at $85 (massive gamma concentration), short at $91 (call wall resistance)

Estimated P&L (current market prices - adjust based on entry timing):

- 💰 Net debit: ~$5.00-6.00 per spread (buying $8 calls, selling $3-4 calls)

- 📈 Max profit: $1.00-2.00 if SBUX at/above $91 at expiration (17-33% ROI)

- 📉 Max loss: $5.00-6.00 if SBUX below $85 (defined and limited)

- 🎯 Breakeven: ~$90-91 depending on entry prices

- 📊 Risk/Reward: ~1:1 to 1:1.5 which is reasonable for defined-risk bullish play

Entry timing:

- ⏰ Wait for Investor Day (January) to pass and assess guidance quality

- 🎯 Only enter if guidance credible and stock holding $82+ (gives spread room to work)

- ❌ Skip if stock already above $88 (spread too tight, limited profit potential)

- ✅ Best entry: Stock at $83-86, post-Investor Day if reaction positive

Position sizing: Risk only 3-5% of portfolio (directional play with turnaround execution risk)

Risk level: Moderate (defined risk, directional bullish) | Skill level: Intermediate

Probability of profit: ~35-40% (need stock to reach $90-91, which is call wall resistance but achievable on strong execution)

🚀 Aggressive: Replicate the Whale Trade (CONVICTION PLAY!)

Play: Copy the exact trade - buy June 2026 $85 calls for turnaround conviction

Structure: Buy $85 calls (June 18, 2026 expiration)

Why this could work:

- 💪 Leverage to recovery: Niccol's "Back to Starbucks" plan showing early results (positive comp sales in Q4)

- 📊 Multiple catalysts: Investor Day guidance (Jan), Q1 earnings (Feb), China JV closure (Q2), Q2 earnings (Apr)

- 🎯 Strike positioning: $85 just 1.5% OTM - betting on modest recovery, not moon shot

- ⏰ Sufficient time: 177 days allows turnaround thesis to develop through two earnings cycles

- 🤝 Following smart money: Institutional player betting $1.2M on this exact structure

- 🚀 Upside potential: If turnaround delivers and stock reaches $91-97 targets, 50-150% returns possible

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Calls cost ~$8.00 ($800 per contract)

- ⏰ TIME DECAY KILLER: Theta accelerates in final 90 days - need stock movement SOON

- 😱 BINARY EXECUTION RISK: Turnarounds are messy - one bad quarter and these go to zero

- 📊 Stuck in range: Stock could chop between $80-88 for months, calls expire worthless

- 🎢 Need $93+ to profit meaningfully: Breakeven at $93 ($85 strike + $8 cost), need rally to $94-97 for solid returns

- ⚠️ Guidance disappointment risk: Investor Day or Q1 earnings disappoint, stock drops to $75-79, 100% loss

Estimated P&L:

- 💰 Cost: ~$8.00 per call (current pricing)

- 📈 Profit scenario: Stock at $95 by June = $10.00 intrinsic value = $2.00 gain (25% ROI)

- 🚀 Home run: Stock at $100 by June = $15.00 intrinsic value = $7.00 gain (87.5% ROI)

- 📉 Loss scenario: Stock ends $80-85 range = lose $5-8 (62-100% loss)

- 💀 Total loss: Stock below $85 = lose entire $8.00 (100% loss)

Breakeven point: ~$93 (need 11% rally from current $83.74)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Believe deeply in Niccol's turnaround ability (Chipotle track record)

- ✅ Can afford to lose ENTIRE premium (real possibility!)

- ✅ Understand turnaround plays are high-risk/high-reward

- ✅ Have conviction in U.S. business recovery offsetting China/margin headwinds

- ✅ Accept that even if RIGHT on thesis, timing matters - stock needs to move by June

- ⏰ Willing to actively manage position - take profits on rallies to $90+, cut losses if breaks below $80

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~30-35% (need stock at $93+ to profit, which requires strong execution across multiple catalysts)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎢 Turnaround execution uncertainty: Management themselves cautioned "turnarounds are not always linear" and "recoveries are not always linear"6. Even with early positive signs in Q4 FY202525 (first positive comp sales in seven quarters), sustaining momentum through Q1-Q2 2026 is NOT guaranteed. One analyst already warned "turnaround is far less straightforward than improving investor sentiment implies"32.

-

☕ Coffee tariff costs peaking in 2026: 50% Brazil tariffs16 hitting Starbucks' 22% Brazil sourcing. While long-term contracts delay impact, $0.02 EPS hit and 0.5% COGS increase expected to peak in 20261819 - exactly when these calls expire! Record $8.41/lb coffee prices (up 33% YoY)22 squeeze margins just as company tries to avoid price increases to rebuild customer loyalty. Catch-22: raise prices and hurt traffic, or absorb costs and compress margins.

-

👷 Labor union strikes during peak season: Over 3,800 unionized baristas (4% of workforce) struck in November30 during critical holiday period with 92% strike authorization vote33. Talks stalled since December 2024 with 700+ unfair labor practice complaints outstanding3435. If strikes expand or continue through Q1 2026, could disrupt operations and Q1 earnings just as turnaround needs validation. Four years after first Buffalo unionization with no contract36 - resolution timeline completely uncertain.

-

🇨🇳 China competition remains brutal despite JV: While Boyu Capital partnership removes operational burden8, competitive reality unchanged. Starbucks market share plunged to 14% in 2024 from 34% in 201910. Luckin Coffee operates 26,000+ stores with 47% YoY revenue growth and 21% operating margins3738 on low-price model. Tea chains offer drinks for $0.30-$1.2039. JV doesn't magically fix competitive disadvantage - execution risk transfers to Boyu.

-

💰 Margin compression from wage investments: $500M Green Apron Service investment and $500M+ renovation spending123 pressures near-term margins. Q1 FY2025 operating margin contracted 390 basis points, Q4 FY2025 contracted 380 bps4024. Improving customer experience is expensive - revenue growth needs to accelerate significantly to offset these investments. If comp sales don't reach 3-4%+ growth, margin targets won't be hit.

-

📊 Analyst skepticism and wide price target dispersion: Price targets range from $59 (Jefferies) to $125 (Deutsche Bank)4142 - massive 111% spread reflects deep uncertainty. Consensus "Moderate Buy" with average target $97.8743, but this represents only 16.9% upside from current $83.74. For $85 calls to profit, need stock at $93+ (20%+ rally). Street is cautious - not pricing in explosive recovery.

-

🎯 Massive $85 gamma concentration creates pin risk: The $85 strike has 0.7893 call gamma + 0.7413 put gamma = 1.53 total gamma - BY FAR the largest concentration on the board. This creates powerful gravitational pull toward $85 as market makers hedge. Stock could get "pinned" at $85 for extended periods, causing these calls to expire exactly at-the-money (zero profit after paying $8 premium). High gamma concentration works AGAINST breakout moves.

-

🏦 Institutional ownership creates overhang: 78% institutional ownership with top holders Vanguard (9.8%)4445. Any loss of patience from large holders creates selling pressure. Elliott Management and Starboard Value took activist stakes4647 - if turnaround disappoints, activists could push for more dramatic action (further cost cuts, CEO change, etc.) creating uncertainty.

-

💵 $1B restructuring costs near-term headwind: 400 store closures and 900 employee layoffs28 with $1B total restructuring costs including $150M severance, $400M asset disposal, $450M lease expenses48 hit near-term earnings. These are one-time costs but impact FY2026 results during critical turnaround validation period.

-

📉 Macro recession risk kills premium coffee spending: At 54.23x P/E ratio trading near $8449, Starbucks has zero recession protection. Premium $5-8 coffee purchases are first to get cut in economic downturn. If 2026 sees recession, even perfect execution won't save the stock from 25-30% correction. These calls would be worthless.

-

🎪 Mobile order concept sunset creates transition risk: Plans to sunset mobile order and pick-up only format in fiscal 202650 deemed "overly transactional". While philosophically aligned with coffeehouse repositioning, operationally complex - could disrupt near-term performance during transition.

🎯 The Bottom Line

Real talk: Someone just bet $1.2 MILLION that Brian Niccol's turnaround plan delivers over the next 6 months31. This isn't a hedge - this is pure bullish conviction that the "Back to Starbucks" strategy works, early momentum continues, and the stock breaks out above $85 resistance toward $91-97 targets by June 2026.

What this trade tells us:

- 🎯 Smart money believes in Niccol: Track record at Chipotle proved his turnaround ability - now applying to Starbucks

- 💰 Betting on catalyst delivery: January Investor Day guidance, Q1 earnings (Feb), China JV closure, Q2 earnings all occur BEFORE expiration

- 📊 Strike positioning strategic: $85 at massive gamma concentration - slightly OTM bet on breakout above current consolidation

- ⏰ Time horizon sufficient: 177 days gives turnaround thesis time to develop through two full quarters

- 🚀 Upside target $91-97: If execution delivers, call wall at $91 first target, then extended resistance $94-97

This is NOT a "buy blindly" signal - it's a "turnaround conviction with catalyst convergence" signal.

If you own SBUX stock:

- ✅ Hold your position: Early turnaround signs positive (first positive comp sales in seven quarters25)

- 📊 Watch January Investor Day closely: Quality of long-term guidance will determine if rally sustainable

- 🎯 Consider adding on pullbacks to $80-82: If Investor Day strong but stock consolidates, that's opportunity

- ⏰ Stop loss at $76-77: If breaks below 2024 support zone, turnaround thesis in question

- 💰 Take some profits at $91-94: If stock rallies to call wall/resistance, trim and lock in gains

If you're watching from sidelines:

- ⏰ January Investor Day is THE catalyst - wait for this before making major commitments

- 🎯 Two good entry points: Pullback to $80-82 (support) OR breakout above $88-90 (confirmation)

- 📈 Looking for confirmation: Need to see credible long-term guidance, U.S. comp sales accelerating to 3-4%+, margin recovery path

- 🚀 If turnaround validates: Rally to $95-100 over 12-18 months is achievable (20-25% upside)

- ⚠️ Current valuation fair but not cheap: Stock at $83.74 pricing in moderate turnaround success - need execution to avoid disappointment

If you're considering options:

- 🎯 June $85 calls viable but aggressive: Need stock at $93+ to profit (11% rally) - achievable but requires strong execution

- 📊 Better risk/reward with call spreads: Buy $85 calls, sell $91 calls for defined risk and lower cost basis

- ⚠️ Wait until post-Investor Day: Entering before January guidance is gambling on unknown outcome

- ⏰ Time decay is real: These calls lose value daily - need stock movement sooner rather than later

- 💸 Position size appropriately: Maximum 3-5% of portfolio given binary execution risk

Mark your calendar - Key dates:

- 📅 January 2026 - Investor Day with full FY2026 guidance and long-term targets (CRITICAL!)

- 📅 February 3, 2026 (Monday) after close - Q1 FY2026 earnings (includes holiday season)

- 📅 Q2 Fiscal 2026 (Jan-Mar) - China JV with Boyu Capital expected to close

- 📅 April 2026 - Q2 FY2026 earnings (first full quarter under China JV, spring season performance)

- 📅 June 18, 2026 - Expiration of this $1.2M call trade

- 📅 End of 2026 - 1,000 café renovations targeted for completion

Final verdict: Starbucks turnaround thesis has real merit - Niccol's proven track record31, early momentum in Q4 FY202525, massive investments in service/renovations12, and China JV removing overhang8 all support recovery. BUT execution risk remains HIGH - labor strikes30, coffee tariffs peaking16, margin compression40, and China competition10 are real headwinds.

The $1.2M call buyer is making a calculated bet: More things will go RIGHT than WRONG over the next 6 months. They're willing to risk $1.2M for potential $600K-$1.8M gains if stock reaches $91-97 targets (50-150% ROI).

For most investors: Wait for January Investor Day to provide clarity. If guidance strong, stock becomes more attractive. If weak, you avoided a potential trap. Patience will be rewarded - the coffee isn't going anywhere. ☕

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. The Z-score of 10.78 reflects this trade's unusual size relative to recent SBUX history - it does not guarantee profitability. Turnarounds are inherently risky and outcomes uncertain. Past performance doesn't guarantee future results. Always do your own research and consider consulting a licensed financial advisor before trading.

About Starbucks Corporation: Starbucks is the world's largest coffee brand operating approximately 41,000 cafes across 80+ countries, with a market cap of $97.98 billion in the Retail - Eating & Drinking Places industry.

References

Footnotes

-

https://www.marketscreener.com/quote/stock/STARBUCKS-CORPORATION-4905/calendar/ ↩

-

https://investor.starbucks.com/news/financial-releases/news-details/2025/Starbucks-Announces-Increase-in-Quarterly-Cash-Dividend/default.aspx ↩

-

https://www.nrn.com/quick-service/starbucks-plans-1-000-store-renovations-by-end-of-2026-and-tests-out-new-budget-prototype ↩ ↩2 ↩3

-

https://www.merca20.com/goodbye-to-the-starbucks-you-knew-this-is-what-its-new-stores-will-look-like-in-2026/ ↩

-

https://finance.yahoo.com/news/starbucks-plans-1-000-renovations-155037103.html ↩

-

https://s203.q4cdn.com/326826266/files/doc_financials/2025/q3/SBUX-3Q25-Corrected-Transcript.pdf ↩ ↩2 ↩3

-

https://www.cnbc.com/2025/11/03/starbucks-boyu-capital-china.html ↩ ↩2 ↩3 ↩4

-

https://finance.yahoo.com/news/starbucks-sells-60-stake-china-220649336.html ↩ ↩2

-

https://us.cnn.com/2025/11/04/business/starbucks-china-divestment-intl-hnk ↩ ↩2 ↩3

-

https://247wallst.com/companies-and-brands/2025/08/03/starbucks-vs-luckin-u-s-icon-slows-as-chinese-company-surges-with-119-new-drinks-and-24000-stores/ ↩

-

https://www.emarketer.com/content/brian-niccols-starbucks-turnaround-q1-2025 ↩ ↩2 ↩3

-

https://www.fastcasual.com/articles/starbucks-ceo-reveals-5-step-recovery-plan/ ↩

-

https://about.starbucks.com/stories/2025/how-back-to-starbucks-is-reshaping-every-aspect-of-the-coffeehouse-experience/ ↩

-

https://www.restaurantdive.com/news/starbucks-2025-investor-day-labor-union-investment/742354/ ↩

-

https://www.cnbc.com/2025/07/10/trump-brazil-tariffs-could-raise-coffee-prices.html ↩ ↩2 ↩3

-

https://www.nasdaq.com/articles/starbucks-faces-looming-brazil-coffee-tariffs-can-it-absorb-hit ↩

-

https://mr-bean.coffee/uncategorized/starbucks-faces-pressure-as-u-s-tariffs-on-brazilian-coffee-drive-up-costs/ ↩ ↩2

-

https://247wallst.com/investing/2025/07/14/starbucks-faces-huge-surge-in-coffee-prices-earnings-trouble/ ↩ ↩2

-

https://www.cnbc.com/2025/09/04/why-coffee-prices-are-so-high-and-where-theyre-headed-next.html ↩

-

https://fortune.com/2025/08/06/starbucks-stock-trump-coffee-tariffs/ ↩

-

https://intelligence.coffee/2025/10/whats-new-with-tariffs-on-coffee/ ↩

-

https://investor.starbucks.com/news/financial-releases/news-details/2024/Starbucks-Reports-Q4-and-Full-Fiscal-Year-2024-Results/default.aspx ↩ ↩2

-

https://www.comunicaffe.com/starbucks-comparable-sales-are-back-in-the-black-after-seven-quarters-1-but-higher-coffee-prices-and-the-cost-of-the-revamp-squeeze-profits/ ↩ ↩2 ↩3 ↩4 ↩5

-

https://www.restaurantdive.com/news/starbucks-stanches-the-same-store-sales-bleeding/803927/ ↩

-

https://www.verdictfoodservice.com/news/starbucks-same‑store-sales-growth/ ↩

-

https://www.restaurantdive.com/news/starbucks-closes-400-stores-lays-off-900-staff/761102/ ↩ ↩2

-

https://www.newsweek.com/starbucks-plans-major-menu-changes-2133262 ↩

-

https://www.cnn.com/2025/12/09/business/starbucks-workers-union-four-years-without-contract ↩ ↩2 ↩3

-

https://www.cnbc.com/2025/09/09/starbucks-ceo-brian-niccol-starbucks-turnaround-plan-one-year.html ↩ ↩2 ↩3

-

https://www.benzinga.com/analyst-stock-ratings/analyst-color/25/12/49147051/starbucks-turnaround-isnt-as-simple-as-it-looks-analyst-warns ↩

-

https://atlantaciviccircle.org/2025/12/17/union-doings-republic-services-starbucks/ ↩

-

https://www.realchangenews.org/news/2025/12/05/starbucks-baristas-go-nationwide-strike-bargaining-stalls ↩

-

https://sbworkersunited.org/statement-on-starbucks-announcement-of-store-closures-layoffs/ ↩

-

https://www.cnn.com/2025/12/09/business/starbucks-workers-union-four-years-without-contract ↩

-

https://qahwaworld.com/coffee-community/luckin-coffee-expansion-outperforms-starbucks/ ↩

-

https://amworldgroup.com/blog/luckin-coffees-tech-driven-model-is-starbucks-rival ↩

-

https://www.cnbc.com/2025/02/26/starbucks-is-struggling-to-grow-sales-in-china-heres-why.html ↩

-

https://investor.starbucks.com/news/financial-releases/news-details/2025/Starbucks-Reports-Q1-Fiscal-Year-2025-Results/default.aspx ↩ ↩2

-

https://finance.yahoo.com/news/78-institutional-ownership-starbucks-corporation-120010607.html ↩

-

https://finance.yahoo.com/news/starbucks-corporation-sbux-faces-activist-122558999.html ↩

-

https://www.cnbc.com/2024/07/19/elliott-starbucks-sbux-stake.html ↩

-

https://www.indmoney.com/blog/us-stocks/starbucks-closing-stores-announces-layoffs-1b-restructuring-plan ↩

-

https://www.nrn.com/quick-service/starbucks-plans-1-000-store-renovations-by-end-of-2026-and-tests-out-new-budget-prototype ↩