🐻 SNPS $2.8M Bearish LEAPS Bet - Institutional Player Bets On Post-Earnings Decline! 📉

📅 December 3, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $2.8 MILLION on SNPS long-dated puts this afternoon! A massive 500-contract position hit the tape at 12:20 PM - targeting the $410 strike (Dec 2026), a full year out. With SNPS trading at $459 and earnings dropping in just 7 DAYS (December 10th), this trader is positioning for a significant decline - either as a bearish speculation or as portfolio insurance ahead of multiple risk factors: conservative FY2026 guidance, Ansys integration stumbles, or renewed China geopolitical concerns. Translation: Smart money is betting SNPS faces serious headwinds over the next 12 months!

📊 Company Overview

Synopsys Inc (SNPS) is the global leader in Electronic Design Automation (EDA) software and semiconductor intellectual property (IP):

- Market Cap: $85.6 Billion

- Industry: Software - Application (EDA Tools)

- Current Price: $459.43 (down 4.89% YTD)

- Market Position: 31% EDA market share (near-duopoly with Cadence at 30%)

- Primary Business:

- EDA Software: Golden signoff tools for advanced chip design (3nm/2nm nodes)

- Semiconductor IP: Pre-verified building blocks for chip designs

- AI-Powered Tools: Synopsys.ai Copilot delivering 30% engineer productivity gains

- Recent Acquisition: $35B Ansys acquisition completed July 2025

Founded in 1986, Synopsys occupies a near-monopoly position in EDA software alongside Cadence - together controlling 61% of the $19B+ global market. The company's tools are essential for designing complex chips at TSMC, Samsung, Intel, and every major semiconductor manufacturer. With 80-85% recurring revenue and near-100% customer retention, SNPS historically trades at premium valuations. However, the stock has declined 29.5% from 52-week highs on integration concerns following the transformational Ansys acquisition.

💰 The Option Flow Breakdown

The Tape (December 3, 2025 @ 12:20:47 PM):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:20:47 | SNPS | ASK | BUY | PUT $410 | 2026-12-18 | $2.8M | $410 | 500 | 19 | 500 | $459.43 | $55.40 | SNPS 410P 12/18/26 |

🤓 What This Actually Means

This is high-conviction bearish positioning OR sophisticated portfolio hedging ahead of critical catalysts! Here's the breakdown:

The Long Put LEAPS Position 🐻

- 💸 Premium paid: $2.8M ($55.40 per contract × 500 contracts)

- 🎯 Strike: $410 puts - 10.8% below current price

- ⏰ Expiration: December 18, 2026 (380 days!) - LEAPS-dated for long-term bearish thesis

- 📊 Size: 500 contracts represents 50,000 shares worth ~$23M notional exposure

- 🎪 Breakeven: $354.60 (22.8% decline required to profit)

- 🔥 Unusual Score: EXTREMELY UNUSUAL (Z-score 96.5, 26.3x vol/OI ratio)

What's really happening here: This trader paid $2.8M for downside protection or bearish speculation extending 380 days into the future. The positioning captures:

- 📅 December 10 Earnings Risk (7 days away) - Conservative FY2026 guidance expected

- 🏢 Ansys Integration Execution (next 6-12 months) - $35B acquisition complexity

- 🌏 China Geopolitical Risk (ongoing) - 16% of revenue exposure to export restrictions

- 📉 Valuation Compression (12-month horizon) - 32x forward P/E vulnerable to multiple contraction

- 🤖 Competitive Pressure (full year) - Cadence gaining ground in verification market

Why LEAPS (380 days)? This isn't a short-term earnings gamble - it's a structural bearish thesis that SNPS faces extended headwinds from integration, valuation, or competitive pressures. The trader needs only a 22.8% decline over 380 days to break even - achievable given the stock already fell 40.5% from peak to November lows.

The timing is surgical: 7 days before earnings when implied volatility is elevated (8.53% expected move through Dec 19 OPEX), maximizing option value while positioning for post-earnings decline. If management guides conservatively or integration concerns surface, this put could gain 50-100% in weeks.

Risk/Reward profile: Maximum loss is $2.8M (100% of premium) if SNPS stays above $410 through Dec 2026. Maximum gain is unlimited downside - if SNPS declines to $300 (35% drop), the put would be worth $110/share for 98% gain. If SNPS collapses to $250 on integration failure, the gain would be 186% ($5.2M profit).

Who makes this trade?

- Institutional hedger protecting a large SNPS or EDA/semiconductor long portfolio

- Bearish hedge fund conviction trade expecting Ansys integration disappointment

- Volatility trader betting earnings miss causes IV expansion and put appreciation

- Risk arbitrageur pairing with other positions in a complex spread strategy

Combined bet: This trader is risking $2.8M betting that SNPS declines meaningfully below $410 (or at minimum, remains volatile enough that the put holds value for trading). At current premium levels, they're paying 13.5% time value for 380 days of protection/speculation - reasonable pricing for high-volatility tech stock ahead of earnings catalyst.

📈 Technical Setup / Chart Check-Up

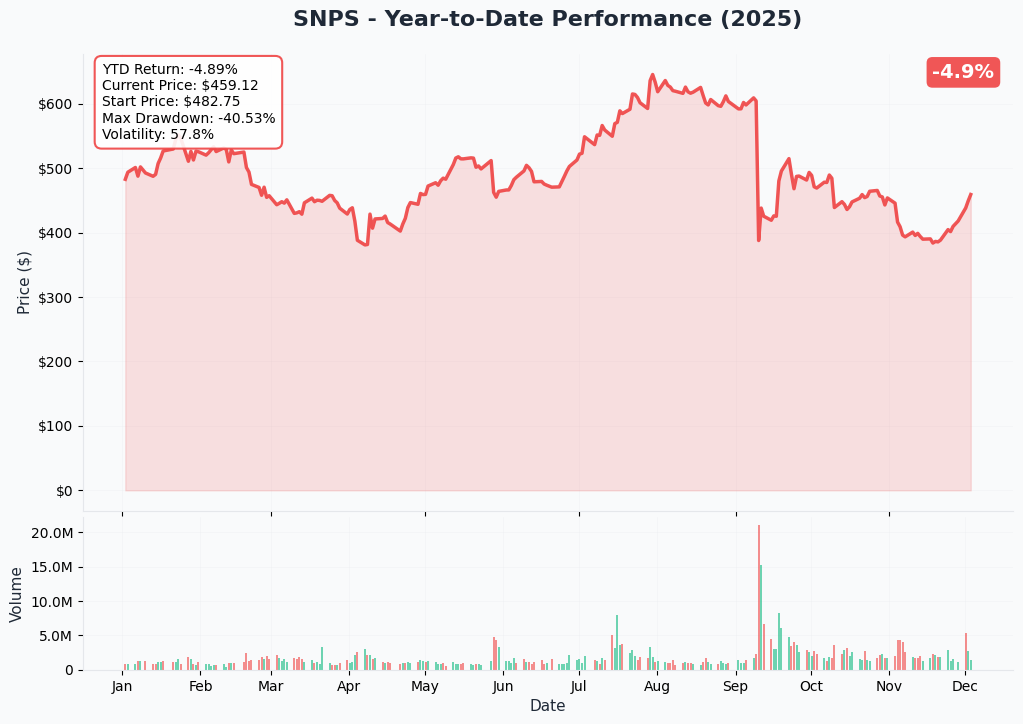

YTD Performance Chart

SNPS is in a DOWNTREND following the Ansys acquisition - down -4.89% YTD with significant volatility throughout 2025. The chart tells the story of a company navigating a transformational $35B deal while facing integration uncertainty and conservative market expectations.

Key observations:

- 📉 Peak-to-trough decline: 40.53% drawdown from $651.73 (mid-2025) to $365.74 (November 2025)

- 🎢 Ansys acquisition impact: Stock peaked on deal announcement, then declined on integration concerns

- 🚨 China export control shock: 9.6% single-day decline (May 29, 2025) on U.S. restrictions

- ✅ Brief recovery: Restrictions lifted July 2, but stock failed to reclaim $500 resistance

- 💪 NVIDIA partnership bounce: 4.85% rally Dec 1 on $2B strategic investment announcement

- ⚠️ Failed breakout: Currently at $459, still 29.5% below 52-week high despite positive catalyst

- 📊 High volatility: 57.8% annualized volatility reflects ongoing uncertainty

The technical picture is CONSTRUCTIVELY BEARISH - lower highs, failed rallies at resistance, elevated volatility. The December 1 NVIDIA partnership provided only temporary relief, suggesting underlying selling pressure. For bears, this is "downtrend intact." For bulls, this is "deep value after correction."

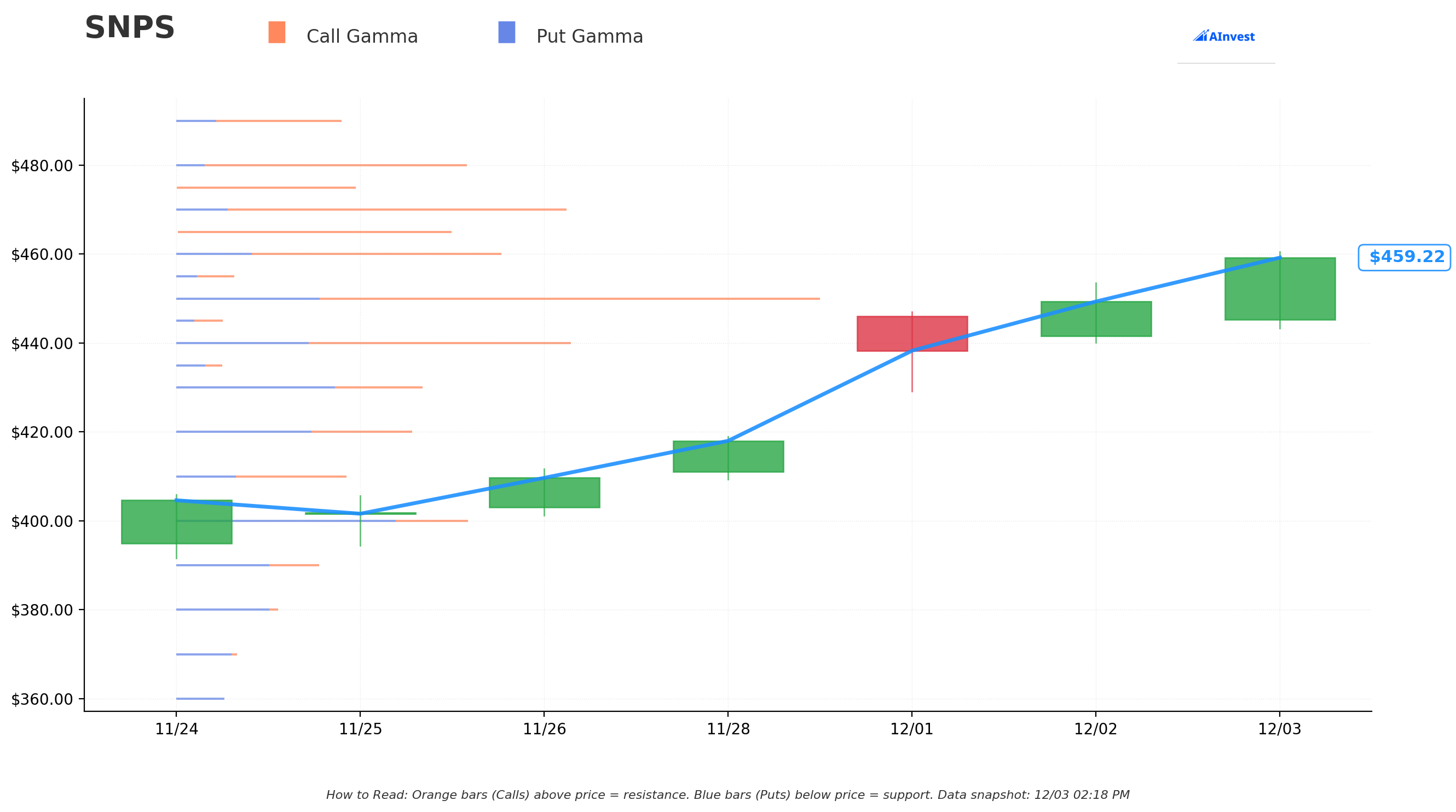

Gamma-Based Support & Resistance Analysis

Current Price: $459.22

The gamma exposure map reveals ZERO gamma exposure across all strikes, indicating limited options market positioning relative to company size or data collection limitations. This suggests the market has not established significant gamma walls that would influence near-term price action.

🔵 Support Levels (Technical, not Gamma-Based):

- $450 - Primary support, round number psychological level (2% below current)

- $440 - Secondary support, near recent bounce zone (4.2% below)

- $430 - Key support from recent volatility cluster (6.4% below)

- $410 - PUT STRIKE TARGET - exactly where the bearish bet is positioned (10.8% below)

- $400 - Major support, crisis-low from November (12.9% below)

- $365 - 52-week low from November 2025 (20.5% below)

🟠 Resistance Levels (Technical):

- $460 - Immediate resistance (at current price)

- $465 - Near-term resistance (1.3% above)

- $470 - Key overhead supply zone (2.3% above)

- $480-$500 - Major resistance band (4.5-8.8% above)

- $550+ - Extended resistance (analyst target zone)

What this means for traders: SNPS is trading in a FRAGILE zone just above $450 support with limited options market structure to provide price stability. The lack of gamma walls means dealer hedging flows won't moderate volatility - the stock can move violently in either direction based purely on fundamental news flow.

Notice the pattern? The put buyer struck at $410, which represents:

- 10.8% decline from current $459

- First major support below the recent $400 crisis low

- Logical technical target if $450 support breaks

If SNPS breaks below $450: The next stops are $440, then $430, then $410 (the put strike). Absence of call gamma overhead means rallies face limited dealer resistance.

If SNPS breaks above $465: Watch for tests of $470, then $480-500 band. However, the December 1 NVIDIA catalyst failed to drive sustained breakout, suggesting weak buying pressure.

Net GEX Bias: NEUTRAL/UNKNOWN (zero gamma data) - Market positioning unclear, heightening risk of explosive moves on earnings news.

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 2 days): ±$10.29 (±2.24%) → Range: $448.33 - $468.90

- 📅 Monthly OPEX (Dec 19 - 16 days - CAPTURES EARNINGS!): ±$39.14 (±8.53%) → Range: $419.47 - $497.76

- 📅 Yearly LEAPS (Dec 18 2026 - 380 days - PUT STRIKE EXPIRATION!): ±$148.66 (±32.42%) → Range: $309.95 - $607.28

Translation for regular folks: Options traders are pricing in a modest 2.24% move ($10) by Friday, but a MUCH LARGER 8.53% move ($39) through December 19 OPEX which brackets the December 10 earnings announcement. The market expects SERIOUS volatility around the catalyst!

KEY INSIGHT for this trade:

- The December 2026 $410 puts are positioned within the ±32.42% implied range ($310-607)

- Breakeven at $354.60 sits in the lower third of the 1-year expected range

- The 8.53% December OPEX implied move suggests $420-498 range - the $410 strike is just below

- If earnings disappoints and stock gaps to $420 range, the put gains significant value immediately

The sharp increase in implied volatility from 2.24% (weekly) to 8.53% (Dec 19) reflects massive earnings uncertainty. The put buyer is betting the actual move EXCEEDS the 8.53% downside expectation - they see $410-420 as a realistic near-term outcome with further downside over 12 months.

🎪 Catalysts

🔥 Immediate Catalysts (Next 7 Days - THE BIG ONE!)

Q4 FY2025 Earnings - December 10, 2025 📊 (THIS IS THE CATALYST!)

SNPS will report fiscal Q4 and full-year FY2025 results on December 10, just 7 DAYS from now:

Consensus Expectations:

- 💰 FY2025 Full Year EPS: $10.64-$10.70 (+3.8-4.4% YoY)

- 📈 FY2026 Guidance: ~$9.7B revenue, ~$14.00 EPS expected

- 🎯 Key Metrics: Ansys integration progress, IP business recovery, backlog trends

- 📊 Critical Questions: Cost synergies timeline, restructuring charges, customer retention

Why this is HUGE for the put trade:

The December 10 earnings call will be management's first comprehensive update on:

- Ansys Integration Status - Progress on combining 6,500 employees and product lines

- FY2026 Outlook - Critical guidance for revenue, margins, and restructuring costs

- IP Business Recovery - Q3 saw weakness from China restrictions and foundry issues

- Restructuring Timeline - 10% workforce reduction (2,650 jobs) execution details

- NVIDIA Partnership Benefits - Quantification of $2B investment impact

Earnings Risk Factors - SETUP FOR DISAPPOINTMENT:

Six major analyst downgrades in Q4 2025:

- 🔻 Bank of America: Downgraded to Underperform

- 🔻 BNP Paribas Exane: Initiated Underperform, $425 target (lowest on Street, -7.5% downside)

- 🔻 Wells Fargo: Cut to $445 target (-3.1%), citing 29x P/E valuation concerns

- 🔻 Rosenblatt: Cut to Neutral from Buy

- 🔻 KeyBanc: Lowered target on NVIDIA dilution concerns

- 🔻 Multiple firms: Expressing caution on conservative FY2026 outlook expectations

Specific risk factors:

- Conservative FY2026 Guidance Expected: Analysts expect management to guide cautiously to rebuild credibility after integration announcement

- IP Business Weakness: Q3 underperformance from China export controls (May-July 2025) and foundry customer issues

- Restructuring Charges: $300-350M in pre-tax costs starting fiscal 2026 will pressure reported earnings

- Integration Costs: Ansys deal closed July 2025 - only 5 months of execution visibility

- Margin Pressure: Integration and restructuring costs could compress near-term margins

Historical precedent: SNPS declined 9.6% in a single day (May 29, 2025) on China export control news. A guidance miss, integration concern, or renewed geopolitical issue could trigger similar 10-15% decline - exactly what this put position is betting on.

Timeline for put trade:

- ✅ Dec 3 (TODAY): Put position established at elevated IV (8.53% expected move)

- 📅 Dec 5-9: Pre-earnings uncertainty - put holds time value, may gain if anxiety builds

- 💥 Dec 10: EARNINGS ANNOUNCED - binary catalyst determines near-term fate

- 📊 Dec 11-19: Post-earnings adjustment - if stock gaps down, put gains 50-100% immediately

- ⏰ Dec 19 - Dec 2026: Long time horizon allows multiple additional catalysts to play out

The put buyer's thesis: Management guides FY2026 conservatively (below consensus $9.7B revenue), highlights integration challenges, or reveals unexpected headwinds. Stock gaps down 10-15% to $390-410 range, putting the $410 strike at-the-money within days. From there, sustained weakness over 12 months drives stock below $355 breakeven.

🚀 Near-Term Catalysts (Next 30-90 Days)

NVIDIA Partnership Implementation 🤖

Announced December 1, 2025 (2 DAYS AGO):

- 💰 Investment: $2B at $414.79/share (9.7% discount to current $459!)

- 🎯 Strategic Value: GPU-accelerated EDA tools achieving 30x circuit simulation speedup

- 🤝 Technology: Access to NVIDIA CUDA, Omniverse platform, cloud infrastructure

- 📊 Dilution: 2.6% share count increase

Bear Case Concerns (Supporting Put Trade):

- Price Signal: NVIDIA paid $414.79 - exactly where this put is struck ($410)! Suggests strategic partner saw fair value 10% below current market price

- Dilution Without Immediate Benefit: 2.6% share count increase with no near-term revenue contribution

- Dependency Risk: Tighter NVIDIA coupling reduces SNPS pricing power and strategic flexibility

- Competitive Response: Cadence may accelerate partnerships with AMD, Intel, other GPU providers

Bull Case (Risk to Put Trade):

- Validates SNPS' AI strategy and provides technological edge

- 30x performance gains could drive market share expansion

- Access to NVIDIA ecosystem enhances competitive moat

Workforce Reduction Execution 🏢

Announced November 9, 2025:

- 👥 Scale: 10% of 26,500 employees (~2,650 jobs)

- 💰 Charges: $300-350M in restructuring costs starting fiscal 2026

- 📅 Timeline: Most layoffs in fiscal 2026, completion by late FY2027

- 🌍 California: 175 layoffs at Sunnyvale HQ effective January 2026

Execution Risks (Supporting Put Trade):

- Knowledge Loss: Experienced engineers departing during critical integration period

- Customer Service: Degradation during organizational upheaval could hurt renewals

- Employee Morale: Integration + layoffs = cultural challenges

- Timing: Cutting 10% while absorbing 6,500 Ansys employees = chaos risk

Bull Case (Risk to Put Trade):

- Cost synergies from workforce optimization ($300-350M annual savings potential)

- Elimination of redundancies from Ansys overlap

- Margin improvement in FY2027 once complete

📅 Medium-Term Catalysts (3-12 Months)

Ansys Integration Milestones (Q1-Q4 FY2026) 🔧

Key Integration Targets:

- Revenue Synergies: Cross-selling EDA to Ansys customers, simulation to SNPS customers

- Product Integration: Combined silicon-to-system design platform for digital twins

- Cost Synergies: Workforce consolidation, facility optimization, platform consolidation

- Customer Retention: Maintaining 95%+ retention through organizational changes

Risk Factors (Supporting Put Trade):

- Integration Complexity: Merging 6,500 Ansys employees while cutting 10% of combined workforce

- Cultural Clash: Different corporate cultures, product philosophies, customer relationships

- Execution Delays: M&A integrations frequently miss synergy targets and timelines

- Customer Churn: Competitive poaching during transition period (Cadence, Siemens)

- Product Delays: Development roadmap disruptions from organizational restructuring

Historical M&A Context: Large tech integrations frequently disappoint:

- Knowledge loss from layoffs interrupts product development

- Customer service degradation leads to competitive losses

- Synergy realization takes 2-3x longer than initially projected

- Cultural integration challenges persist for years

If integration stumbles, the $35B acquisition price becomes an albatross, pressuring valuation toward the $410 strike or below.

Geopolitical Risk - China Exposure (Ongoing) 🌏

Timeline of China Risk:

- May 29, 2025: U.S. export restrictions imposed - stock -9.6% single day

- July 2, 2025: Restrictions lifted under trade framework

- Current Status: Fragile detente with ongoing uncertainty

- Revenue at Risk: $1B annually (16% of total revenue)

Bear Case (Supporting Put Trade):

- 30-40% probability of renewed export restrictions within 12-18 months

- U.S.-China tech decoupling accelerating (AI chips, EDA software, semiconductor equipment)

- China developing domestic EDA alternatives (Huawei, X-Epic, government-funded startups)

- Potential permanent loss of $1B revenue stream with limited recourse

Historical Impact: The May 29 export control announcement caused immediate 9.6% decline. A renewed, comprehensive ban could trigger 15-25% decline - directly validating this put trade's thesis.

Q1 FY2026 Earnings - Expected March 2026 📊

Critical Update Points:

- Ansys integration progress after first full quarter

- FY2026 guidance refresh based on Q1 execution

- Customer retention metrics

- Backlog and bookings trends

- Competitive dynamics commentary

This represents the second major catalyst within the put's time horizon - another opportunity for disappointment if integration struggles or guidance disappoints.

Competitive Dynamics - Cadence Momentum 🥊

Cadence Market Share Gains:

- Verification market share: 30% → 35.1% (taking share from SNPS)

- Aggressive cloud and AI investments

- Strong customer momentum in advanced nodes

- Risk of key design wins at TSMC 3nm/2nm

Emerging Threats:

- Chinese domestic EDA tools (5-10 year timeline to competitiveness)

- Vertical integration by large customers (Samsung, Intel developing internal tools)

- Open-source alternatives reducing switching costs

If Cadence continues gaining ground, SNPS' premium valuation becomes harder to justify.

🚀 Long-Term Catalysts (6-12 Months)

Valuation Compression Risk (32x Forward P/E) 💸

Current Valuation:

- P/E: 32x forward earnings (vs. historical 25-28x range)

- Premium: 14-28% above historical average

- Peer Comparison: Cadence at 35x P/E (SNPS trading at slight discount)

- Assumption: Flawless Ansys integration, AI tailwinds sustained, no China disruption

Downside Scenarios:

| P/E Multiple | FY2026 EPS | Implied Price | Downside |

|---|---|---|---|

| 32x (current) | $14.00 | $448 | -2.5% |

| 29x (Wells Fargo) | $14.00 | $406 | -11.6% |

| 25x (historical low) | $14.00 | $350 | -23.8% |

| 25x (conservative) | $12.00 | $300 | -34.7% |

Bear Case: If management guides FY2026 conservatively ($9.5B revenue, $12-13 EPS) and the market applies a 25x multiple due to execution concerns, the stock could decline 25-35% toward the put's breakeven zone of $354.60.

Multiple compression catalysts:

- Integration execution disappointment

- China revenue loss

- Competitive market share losses

- Broader tech valuation reset in higher-rate environment

EDA Market Growth Trajectory 📈

Market Projections:

- 2025: $19.22 billion

- 2030: $28.85 billion (8.5% CAGR)

- Key Drivers: AI chip complexity, advanced nodes, multi-die systems, automotive electrification

SNPS Position:

- 31% market share (vs. Cadence 30%, Siemens 13%)

- 61% combined duopoly share with Cadence

- 80-85% recurring revenue model

- Near-100% customer retention (switching costs prohibitive)

Bull Case (Risk to Put Trade): If AI investment cycle continues unabated and SNPS executes flawlessly, the 8.5% market CAGR supports premium valuation. However, this requires perfect execution on Ansys integration and no major disruptions.

🎲 Price Targets & Probabilities

Using technical levels, implied move data, earnings catalyst, and integration risk, here are the scenarios through December 2026 expiration:

📉 Bear Case (30% probability) - PUT TRADE WINS BIG

Target: $300-$355 (Breakeven Zone)

How we get there:

- 💥 December 10 earnings disappoint with FY2026 guidance below consensus ($9.5B vs $9.7B expected)

- 🚨 Ansys integration challenges surface - customer churn, product delays, or cost overruns

- 🌏 China geopolitical risk resurfaces - renewed export restrictions announced

- 📊 Valuation compression from 32x to 25x P/E on execution concerns

- 💰 IP business recovery slower than expected

- 🥊 Cadence competitive wins at major customers (NVIDIA, AMD, hyperscalers)

- 📉 Technical breakdown below $450 triggers cascade: $440 → $430 → $410 → $400

- 🔨 Broader tech selloff pressures high-valuation software stocks

- 💸 NVIDIA partnership fails to deliver near-term benefits, highlights dependency

Key metrics needed:

- Break below $450 support with conviction (triggers technical cascade)

- Earnings guidance 5-10% below consensus

- Negative commentary on Ansys integration timeline or customer retention

- Analyst downgrades to $400-425 targets (building on recent BNP Paribas $425)

Probability assessment: 30% because multiple negative catalysts must align: earnings miss AND integration concerns AND/or China risk. However, six recent analyst downgrades, elevated valuation (32x P/E), and integration complexity create meaningful downside risk. The stock already declined 40.5% from peak to November lows - extending that weakness 10-15% more is plausible.

Put P&L in Bear Case:

- At $355 (breakeven): Profit = $0 (break even)

- At $300 (35% decline): Profit = $55/share × 500 = $2.75M (+98% ROI on $2.8M)

- At $250 (46% decline): Profit = $105/share × 500 = $5.25M (+188% ROI)

🎯 Base Case (40% probability) - PUT TRADE MODEST GAIN

Target: $390-$430 range (SLOW GRIND LOWER)

Most likely scenario:

- ✅ December 10 earnings meet expectations but guidance is conservative ($9.6-9.7B for FY2026)

- 📊 Stock drifts 5-10% lower to $410-435 range over 3-6 months on integration uncertainty

- 🎢 Volatility around earnings date - initial gap down to $430s, then stabilization

- 📈 Ansys integration proceeds slowly but without major disasters

- ⚖️ Valuation concerns prevent rallies but floor exists around $400 (29x forward P/E)

- 💰 China risk remains elevated but no immediate restrictions

- 🐳 Gradual selling pressure as cautious investors reduce exposure

- 📊 Trading in $390-430 band through mid-2026

- 🤔 Market waits for Q1/Q2 FY2026 earnings to validate integration progress

- 💤 Implied volatility normalizes post-earnings (IV crush from 8.53% to 5-6%)

This is the "slow bleed" scenario: Stock weakens on conservative outlook and execution uncertainty but doesn't collapse. Reaches $410-420 by Q1 2026, putting the $410 strike at-the-money. From there, needs further deterioration to reach $355 breakeven.

Why 40% probability: This balances the bearish setup (analyst downgrades, integration risk, elevated valuation) against the strong fundamentals (80% recurring revenue, near-monopoly market position, essential product). Stock likely weakens but doesn't crater absent major negative catalyst.

Put P&L in Base Case:

- At $430 (6% decline): Minimal gain = $20-30/share depending on time value

- At $410 (11% decline): At-the-money = $40-50/share value (+$500K-$700K, 18-25% gain)

- At $390 (15% decline): In-the-money = $55-65/share (+$1.0-1.5M, 36-54% gain)

📈 Bull Case (30% probability) - PUT TRADE LOSES

Target: $480-$550 (EARNINGS BEAT + INTEGRATION CONFIDENCE)

What could go wrong for the put:

- 🚀 December 10 earnings beat with FY2026 guidance ABOVE consensus ($9.8-10.0B revenue)

- 💪 Management provides confident Ansys integration timeline with early wins

- 🤖 NVIDIA partnership delivers immediate competitive advantages (design wins announced)

- 📊 IP business recovery exceeds expectations

- 🌍 China export risk permanently resolved or revenue replaced by other regions

- 🏆 Major customer wins announced (next-gen AI chips from NVIDIA, AMD, hyperscalers)

- 📈 Technical breakout above $465 triggers systematic buying: $470 → $480 → $500

- 💰 Analyst upgrades following earnings beat (targets raised to $550-600)

- 🎯 Multiple expansion back to 35-38x P/E on growth reacceleration

- 🌊 Broader AI tailwinds lift all EDA/semiconductor stocks

Critical support holding:

- Sustained volume above 2M shares daily (vs ~1.5M recent average)

- Break above $465-470 resistance with conviction

- Positive earnings surprise (beat + raise scenario)

- Ansys integration metrics exceed Street expectations

Probability assessment: 30% because AI tailwinds are real, EDA market is growing 8.5% CAGR, and SNPS has near-monopoly market position with 80% recurring revenue. If management executes integration well and guides confidently, the recent analyst downgrades represent opportunity for positive surprise. However, recent failure to hold $500 despite NVIDIA catalyst suggests limited buying appetite.

Put P&L in Bull Case:

- At $480 (5% rally): Loss = -$2.0-2.2M (-71-79% loss as time value decays)

- At $500 (9% rally): Loss = -$2.3-2.5M (-82-89% loss)

- At $550 (20% rally): Loss = -$2.7-2.8M (-96-100% loss, near total wipeout)

💡 Trading Ideas

🛡️ Conservative: Wait for Post-Earnings Clarity

Play: Stay on sidelines until AFTER December 10 earnings settles, watch for entry

Why this works:

- ⏰ Earnings creates binary event risk with unpredictable short-term volatility

- 📊 December 19 OPEX implied move of ±8.53% ($39) creates wide possible range

- 💸 32x P/E valuation offers zero margin of safety at current $459 levels

- 🎯 Better entry likely post-earnings after volatility settles and direction clarifies

- 📉 If stock gaps down 10-15%, can buy at better prices with less uncertainty

- 🤔 The $2.8M institutional put signals elevated risk - why step in front?

Action plan:

- 👀 Watch December 10 earnings and guidance closely - focus on FY2026 outlook

- 🎯 Look for decline below $430 for stock entry with margin of safety (29x forward P/E)

- ✅ Need to see Ansys integration commentary BEFORE committing capital

- 📊 Monitor analyst reactions - are downgrades continuing or reversing?

- ⏰ Revisit Q1 FY2026 earnings (March) for cleaner risk/reward setup

Expected outcome: Avoid potential 10-15% earnings volatility. Get clarity on integration execution. Enter with better information and potentially better price.

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: Bull Put Spread - Play the Support

Play: AFTER Dec 10 earnings, sell bull put spread targeting technical support

Structure: Sell $430 puts, Buy $420 puts (January 16, 2026 expiration)

Why this works:

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Targets key support zone at $420-430 (recent volatility cluster)

- 💰 Collect premium betting SNPS stays above $430 through Jan 16

- 🛡️ Thesis: 80% recurring revenue + EDA monopoly prevents sustained breakdown

- ⏰ 43 days to expiration gives time for post-earnings stabilization

- 📈 Even in base case, $420 support likely holds (8.6% below current)

Estimated P&L (adjust after Dec 10 IV settlement):

- 💰 Collect ~$3.00-4.00 credit per spread

- 📈 Max profit: $300-400 if SNPS above $430 at January expiration (keep full credit)

- 📉 Max loss: $600-700 if SNPS below $420 (defined and limited)

- 🎯 Breakeven: ~$426-427

- 📊 Risk/Reward: ~1.5:1 to 2:1 (favorable for defined-risk bullish play)

Entry timing:

- ⏰ Enter 2-3 days after Dec 10 earnings once volatility normalizes

- 🎯 Only enter if stock trading $440+ (gives cushion to support)

- ❌ Skip if stock already below $435 (too close to short strike)

Position sizing: Risk only 3-5% of portfolio (defined-risk premium collection)

Risk level: Moderate (defined risk, mildly bullish) | Skill level: Intermediate

🐻 Aggressive: Copy The Whale - Buy Long Put LEAPS (SPECULATIVE!)

Play: Buy similar long-dated puts as this institutional player

Structure: Buy $410 puts (December 18, 2026 expiration) OR Buy $430 puts (June 2026 for shorter duration)

Why this could work:

- 🐋 "Following smart money" - someone with $2.8M sees downside risk here

- 💥 Earnings on Dec 10 creates immediate catalyst for decline

- 📊 $410 strike only 10.8% out of the money - achievable with earnings miss

- 🎯 Six analyst downgrades in Q4 signal deteriorating sentiment

- ⏰ 380 days to expiration captures multiple catalysts (Dec earnings, Q1/Q2 results, integration updates)

- 📈 Ansys integration risk is real - $35B acquisition with 10% layoffs during integration

- 🎢 High implied vol (8.53% for Dec 19) means options market expects big moves

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Puts cost ~$55/share ($5,500 per contract!)

- 🤯 Deep breakeven: Need 22.8% decline to $355 just to break even

- ⏰ Massive theta decay: Burns ~$14.50 per contract per day ($5,500 / 380 days)

- 😱 IV crush risk: After Dec 10, IV could collapse 30-50%, hurting option value

- 📊 One-way risk: Stock could easily stabilize at $430-450 and puts lose 50-70%

- ⚠️ AI tailwinds: EDA market growing 8.5% CAGR - SNPS has 31% market share

- 💀 Bull case: NVIDIA partnership + Ansys synergies could drive upside surprise

Estimated P&L:

- 💰 Cost: ~$55/share ($5,500 per contract)

- 📈 Modest profit: Stock at $380 by June 2026 = $25 profit (45% ROI)

- 🚀 Solid return: Stock at $350 by Dec 2026 = $60 profit (109% ROI)

- 📉 Break even: Stock at $355 by Dec 2026 = $0 profit

- 💀 Moderate loss: Stock at $430 by Dec 2026 = -$50 loss (91% loss)

- 💀 Total loss: Stock above $410 by Dec 2026 = -$55 loss (100% wipeout)

Breakeven point: $354.60 (22.8% decline from current $459.43)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand long-dated options and can monitor position daily/weekly

- ✅ Can afford to lose ENTIRE premium (real 100% loss possibility!)

- ✅ Accept that even if directionally correct, timing is everything

- ✅ Plan exit strategy BEFORE entering (take profits at 50%, cut losses at -50%)

- ⏰ Consider taking profits at 50-75% gain rather than holding for max

- 📊 Size position at 2-5% of portfolio MAX (this is speculation, not investment)

Alternative structure (less aggressive):

- Buy shorter-dated puts (June 2026 $430 strike) for ~$30-35 per contract

- Less time decay, closer to current price, but less time for thesis to play out

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~25-35% (need 15-23% decline over 12 months during volatile period)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💰 Valuation at 32x Forward P/E is STRETCHED but not absurd: Trading at 32x forward earnings vs. historical 25-28x range and sector average 25x. Stock is priced for successful Ansys integration, sustained AI-driven EDA demand, and no China disruption. However, this is only 14-28% premium to historical average, not the extreme 430x P/E we saw with PLTR. Still, any execution stumble could trigger multiple compression to 25-29x range, implying 10-22% downside to $358-410. Wells Fargo's $445 target assumes 29x multiple. If management guides conservatively AND integration concerns surface, 25x multiple on $12-13 EPS = $300-325 stock price (30-34% downside).

-

🏢 $35B Ansys integration is UNPRECEDENTED complexity: Merging 6,500 Ansys employees while simultaneously cutting 10% of workforce (2,650 jobs) creates organizational chaos risk. Different corporate cultures, product philosophies, customer relationships must align. Historical precedent: Large tech M&A frequently disappoints with knowledge loss from layoffs, customer churn, synergy delays (2-3x longer than projected), and cultural misalignment persisting for years. If integration stumbles - evidenced by customer departures, product delays, or cost overruns - the $35B price tag becomes an albatross. Management's December 10 guidance and commentary will be CRITICAL.

-

🌏 China geopolitical risk (16% of revenue = $1B) remains ELEVATED: May 29, 2025 export restrictions caused 9.6% single-day decline. July 2 lifting provided temporary relief, but fragile detente continues. 30-40% probability of renewed restrictions within 12-18 months as U.S.-China tech decoupling accelerates. China actively developing domestic EDA alternatives (Huawei, X-Epic, government-funded startups). A renewed, comprehensive ban would force SNPS to write off 16% of revenue stream with limited ability to replace. This represents $1B annual revenue risk that could trigger 15-25% stock decline.

-

🥊 Cadence competitive momentum threatens market share: Main rival gained verification market share from 30% to 35.1%, taking share directly from SNPS. Aggressive cloud and AI investments narrowing technology gap. Risk of major design wins at TSMC 3nm/2nm nodes, NVIDIA next-gen AI chips, or hyperscaler custom silicon projects. If Cadence wins key customers, SNPS' premium valuation erodes rapidly. Additionally, Chinese domestic tools (5-10 year timeline) and vertical integration by Samsung/Intel create long-term threats.

-

🤖 NVIDIA partnership creates DEPENDENCY RISK: December 1 announcement of $2B investment at $414.79/share (9.7% discount to current $459) raises red flags. Was this discount negotiated because NVIDIA had leverage? Does partnership reduce SNPS' pricing power? Does it lock SNPS into NVIDIA ecosystem while freeing Cadence to partner with AMD, Intel, and other GPU providers? The 2.6% dilution without immediate revenue benefit is negative. If NVIDIA relationship sours or partnership underdelivers, SNPS loses key competitive narrative.

-

💸 Restructuring charges ($300-350M) will pressure near-term margins: Starting fiscal 2026, pre-tax costs from 10% workforce reduction hit reported earnings. Management must communicate clearly how these charges impact quarterly results and when margin benefits materialize. If Street misinterprets or charges exceed guidance, negative earnings surprises likely.

-

📊 80-85% recurring revenue is DOUBLE-EDGED: Provides stability and downside protection (even in downturn, existing customers locked in). However, also means growth depends on new customer additions and upselling existing accounts - both harder during integration period. If net new business slows while integrating Ansys, growth decelerates. Near-100% retention protects base but doesn't guarantee upside.

-

🚨 Analyst sentiment deteriorated rapidly in Q4 2025: Six downgrades (Bank of America to Underperform, BNP Paribas $425 target, Wells Fargo $445 target, Rosenblatt to Neutral, KeyBanc cut, others) signal Street losing confidence. When analyst momentum shifts negative, stocks often overshoot to downside as institutional holders reduce positions. Consensus target of $553 (+20% upside) masks recent negative revision trend.

-

💔 AI tailwinds could ACCELERATE rather than slow: EDA market growing 8.5% CAGR to $28.85B by 2030 driven by AI chip complexity, advanced nodes, multi-die systems. If AI investment cycle continues unabated, SNPS' essential position in chip design validates premium valuation. NVIDIA partnership could deliver breakthrough competitive advantages. Ansys synergies could exceed expectations. This is the primary risk to the put trade - structural AI demand overwhelming near-term integration uncertainty.

-

⚡ Earnings binary creates extreme volatility: December 10 catalyst with ±8.53% implied move ($39 swing) means put value could fluctuate wildly. Even if directionally correct long-term, near-term IV crush post-earnings could cause temporary losses. Options traders must understand that BOTH price movement AND volatility changes impact P&L.

🎯 The Bottom Line

Real talk: Someone just bet $2.8 MILLION that SNPS faces meaningful downside over the next 12 months, positioning with long-dated puts extending through December 2026. This isn't a short-term earnings gamble - this is STRUCTURAL BEARISH CONVICTION betting on integration struggles, valuation compression, or geopolitical disruption driving the stock toward $410 or below.

What this trade tells us:

- 🎯 Sophisticated player expects significant weakness from current $459 levels (10.8% to strike, 22.8% to breakeven)

- 💥 The 380-DAY time horizon shows they're betting on SUSTAINED problems, not just earnings miss

- 📊 $2.8M commitment suggests either portfolio hedging (protecting concentrated SNPS/EDA exposure) OR high-conviction bearish speculation

- ⏰ Timing 7 days before earnings maximizes option value while positioning for post-catalyst decline

- 💰 Breakeven at $354.60 is just 3% below November 2025 low of $365.74 - achievable extension of recent weakness

This is NOT a "guaranteed winner" - it's a HIGH RISK/HIGH REWARD bet on multiple negative catalysts aligning.

If you own SNPS:

- ✅ Consider trimming 10-20% ahead of December 10 earnings to reduce risk

- 📊 Set mental stop at $430 (6.4% below current, key support level)

- ⏰ Watch earnings guidance closely - if FY2026 outlook is below consensus or integration commentary negative, reduce exposure further

- 🎯 If holding long-term, be prepared for 10-20% volatility around earnings

- 🛡️ Consider selling covered calls at $470-480 strikes to generate income if you're bullish but want protection

If you're watching from sidelines:

- ⏰ December 10 earnings is the catalyst to watch - don't enter before clarity!

- 🎯 Post-earnings decline to $420-430 would be attractive entry (29-30x forward P/E with clarity)

- 📈 Looking for confirmation: Ansys integration progressing well, FY2026 guidance meets/beats, China risk stable

- 🚀 Longer-term (12-18 months), successful integration could drive stock to $550+ (analyst consensus target)

- ⚠️ Current valuation (32x P/E) is elevated but not absurd - only enter if you believe in multi-year growth story

If you're considering the put trade:

- 🎯 The $410 strike (Dec 2026) requires 22.8% decline to break even - substantial but achievable given 40.5% peak-to-trough drawdown in 2025

- 💀 This is EXPENSIVE ($55/share premium = $5,500 per contract) with massive theta decay ($14.50/day)

- ⚠️ Only allocate 2-5% of portfolio maximum - this is SPECULATION, not investment

- 📊 Have exit plan BEFORE entering: Take profits at 50% gain, cut losses at -50%

- ⏰ Consider shorter-dated, closer-to-money strikes for less capital at risk (June 2026 $430 puts)

If you're bullish:

- 🎯 Wait until AFTER Dec 10 earnings for clearer risk/reward

- 📊 Support at $450, then $430, then $410 - buyers should wait for one of these levels

- ⚠️ Bull put spreads (sell $430/buy $420) post-earnings offer defined-risk way to bet on support

- 📉 Watch for earnings beat + confident integration commentary as entry signal

- ⏰ Don't fight the bearish setup - let the catalyst pass first

Mark your calendar - Key dates:

- 📅 December 5 (Friday) - Weekly OPEX (±2.24% implied move)

- 📅 December 10 (Tuesday) - Q4 FY2025 EARNINGS + FY2026 GUIDANCE (THE CATALYST!)

- 📅 December 19 (Thursday) - Monthly OPEX (±8.53% implied move captures earnings)

- 📅 January 16, 2026 (Friday) - Monthly OPEX (shorter-dated put alternative)

- 📅 March 2026 - Q1 FY2026 earnings (second integration update)

- 📅 December 18, 2026 (Friday) - Put expiration date

Final verdict: SNPS faces a CRITICAL JUNCTURE at December 10 earnings. The fundamental story is STRONG - 31% share of growing EDA market, 80% recurring revenue, near-monopoly position, essential tools for AI chip design. BUT the near-term risks are REAL - $35B integration complexity, 10% workforce reduction during transition, 16% revenue exposure to China geopolitics, elevated 32x P/E valuation, and recent analyst downgrades signaling concern.

The $2.8M put buyer believes the risks overwhelm the fundamentals over the next 12 months. They're betting on conservative guidance, integration stumbles, or geopolitical disruption driving the stock to $410 or below.

They might be right. But they're also risking $2.8M (100% loss potential) on a thesis that requires 22.8% decline in a company with 80% recurring revenue and near-monopoly market position.

Be smart. Size appropriately. Use defined risk. Take profits. The AI/EDA growth story will still be here in 2026, and you'll sleep better with a disciplined approach.

Stay sharp, manage risk, and may the gamma be with you. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Long put positions can lose 100% of premium paid. Time decay (theta) accelerates as expiration approaches. Implied volatility changes can cause losses even when directionally correct. The Z-scores and unusual classifications reflect statistical analysis - they do not imply trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. The put buyer may have complex portfolio needs (hedging, spreads, institutional mandates) not applicable to retail traders.

About Synopsys Inc: Synopsys is the global leader in Electronic Design Automation (EDA) software and semiconductor intellectual property, with 31% market share in the $19B+ EDA market. The company provides essential tools for designing complex chips at advanced nodes (3nm/2nm) and recently completed a transformational $35 billion acquisition of Ansys to expand into simulation software, creating a comprehensive silicon-to-system design platform. Market cap: $85.6 billion.