🔄 STX: $4M Call Roll Shows Sophisticated Profit-Taking Strategy!

📅 January 6, 2026 | 🔥 Extremely Unusual Activity Detected

🎯 The Quick Take

Someone just executed a $4 million call roll on Seagate Technology (STX) - closing deep in-the-money March $280 calls and opening June $300 calls. This is extremely unusual with z-scores of 9.33 and 4.22, and it's a textbook example of locking in profits while maintaining bullish exposure. Translation: A sophisticated player is taking chips off the table but staying in the AI storage game! 🎰

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the exact play that went down at 10:15 AM:

| Time | Ticker | Type | Strike | Expiry | Side | Premium | Size | Spot | IV | Strategy | Z-Score |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:15:17 | STX | CALL | $300 | 2026-06-18 | BUY | $2.1M | 320 | $317.46 | - | Long Call (BTO) | 9.33 |

| 10:15:17 | STX | CALL | $280 | 2026-03-20 | BUY | $1.9M | 320 | $317.46 | - | Close Short Call (BTC) | 4.22 |

Combined Premium: $4.0 MILLION 💰

🤓 What This Actually Means

Real talk: This is a call roll - one of the smartest moves in the options playbook. Here's what happened:

Step 1 (Close Position): The trader bought back their March 20 $280 calls that were $37.46 deep in-the-money. They paid $1.9M to close this position, likely locking in substantial profits since these were probably opened when STX was much lower.

Step 2 (Open New Position): Simultaneously opened June 18 $300 calls for $2.1M. These are now just $17.46 in-the-money, giving them 5+ months of time value and exposure to further upside.

The Strategy:

- 🎯 Lock in profits from the March position (it had almost no time value left)

- 🚀 Maintain bullish exposure with more time and higher strike

- 💪 Roll up and out - classic move when you're right but want to de-risk

- ⏰ Extend time to capture the Mozaic 4+ ramp and Q2 earnings (late January)

Why it's EXTREMELY unusual:

- Z-score of 9.33 on the June calls means this is roughly 555x larger than typical activity

- Z-score of 4.22 on the March close is also 265x larger than average

- This is institutional-grade positioning - not retail YOLO trading

🏢 Company Overview

Seagate Technology Holdings is a leading supplier of hard disk drives for data storage serving enterprise and consumer markets. With a market cap of $72 billion, STX has emerged as one of 2025's top-performing stocks, surging over 225% year-to-date thanks to explosive AI-driven storage demand.

Why STX Matters Right Now:

- AI Storage Leader: Pioneering HAMR (Heat-Assisted Magnetic Recording) technology with drives up to 40TB+

- Duopoly Market: Competes primarily with Western Digital in a consolidated market

- Tech Lead: Shipped 1 million+ Mozaic HAMR drives; Western Digital won't have HAMR until late 2027

- Demand Visibility: Unprecedented demand locked in through 2026-2027 build-to-order contracts

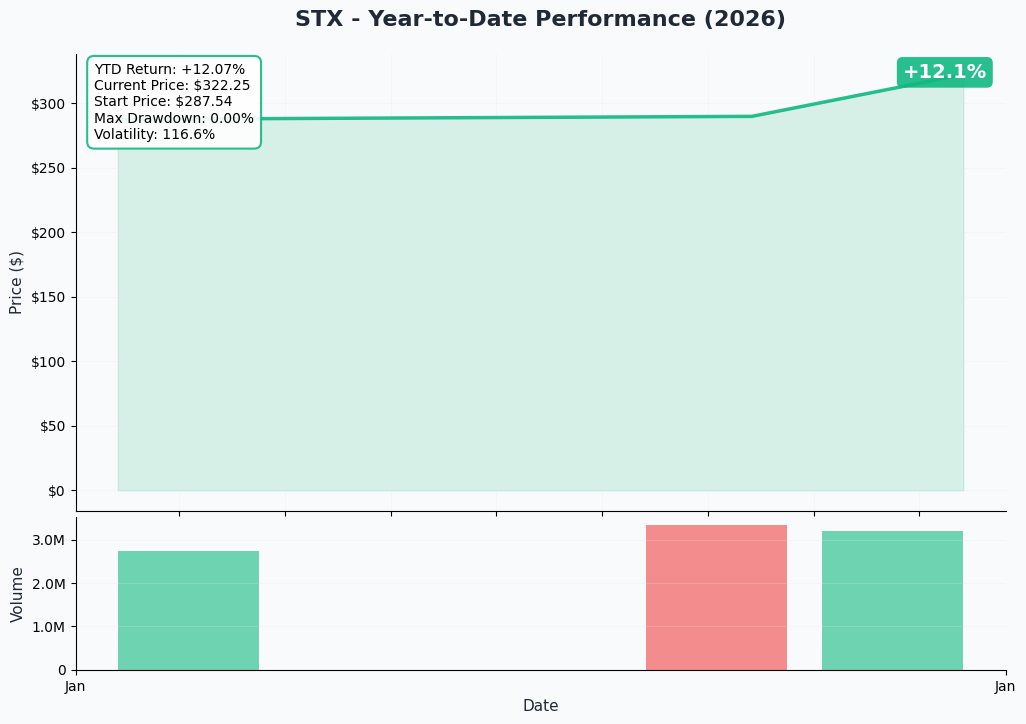

📈 Chart Check-Up

YTD Performance - The AI Storage Rocket 🚀

STX has been on an absolute tear in 2025, rallying from around $90 to current levels near $323 - that's a +225% gain! The stock joined the Nasdaq-100 Index on December 22, 2025, triggering massive passive inflows. Recent price action shows consolidation around the $300-320 zone after the parabolic run, suggesting a potential base-building phase before the next leg.

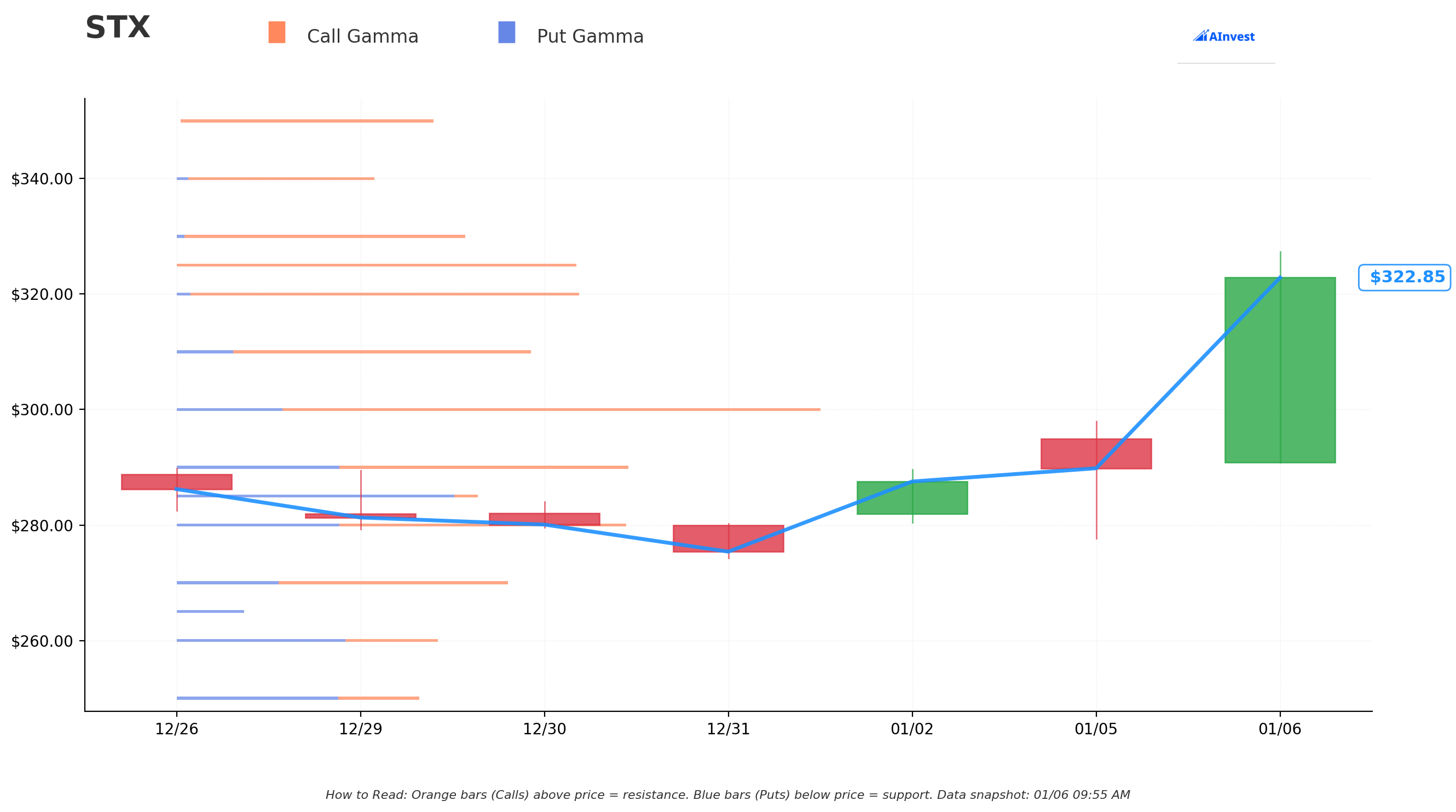

🔵🟠 Gamma-Based Support & Resistance Analysis

The gamma landscape is showing critical structural levels that align perfectly with the options positioning:

Major Support Zones (Blue Bars - Put Gamma):

- 💪 $320.00 - Strongest support with 0.6B in total gamma (current battleground!)

- 🛡️ $310.00 - Secondary support with 0.5B gamma

- 🎯 $300.00 - HUGE support zone with 0.9B gamma (this is the NEW STRIKE from the call roll!)

- 🔵 $280.00 - Major support with 0.7B gamma (the OLD STRIKE that was closed)

Key Resistance Levels (Orange Bars - Call Gamma):

- 🚧 $325.00 - Immediate resistance with 0.6B gamma

- 🎢 $330.00 - Next ceiling at 0.4B gamma

Net GEX Bias: BULLISH 📈

What This Tells Us: The $300 strike where the new calls were opened sits on massive put gamma support - this isn't coincidental! The trader is positioned at a key structural level where market makers will provide natural support. The $280 old strike also shows heavy gamma, but they rolled UP to capture more upside while the strong support shelf at $300 provides downside protection.

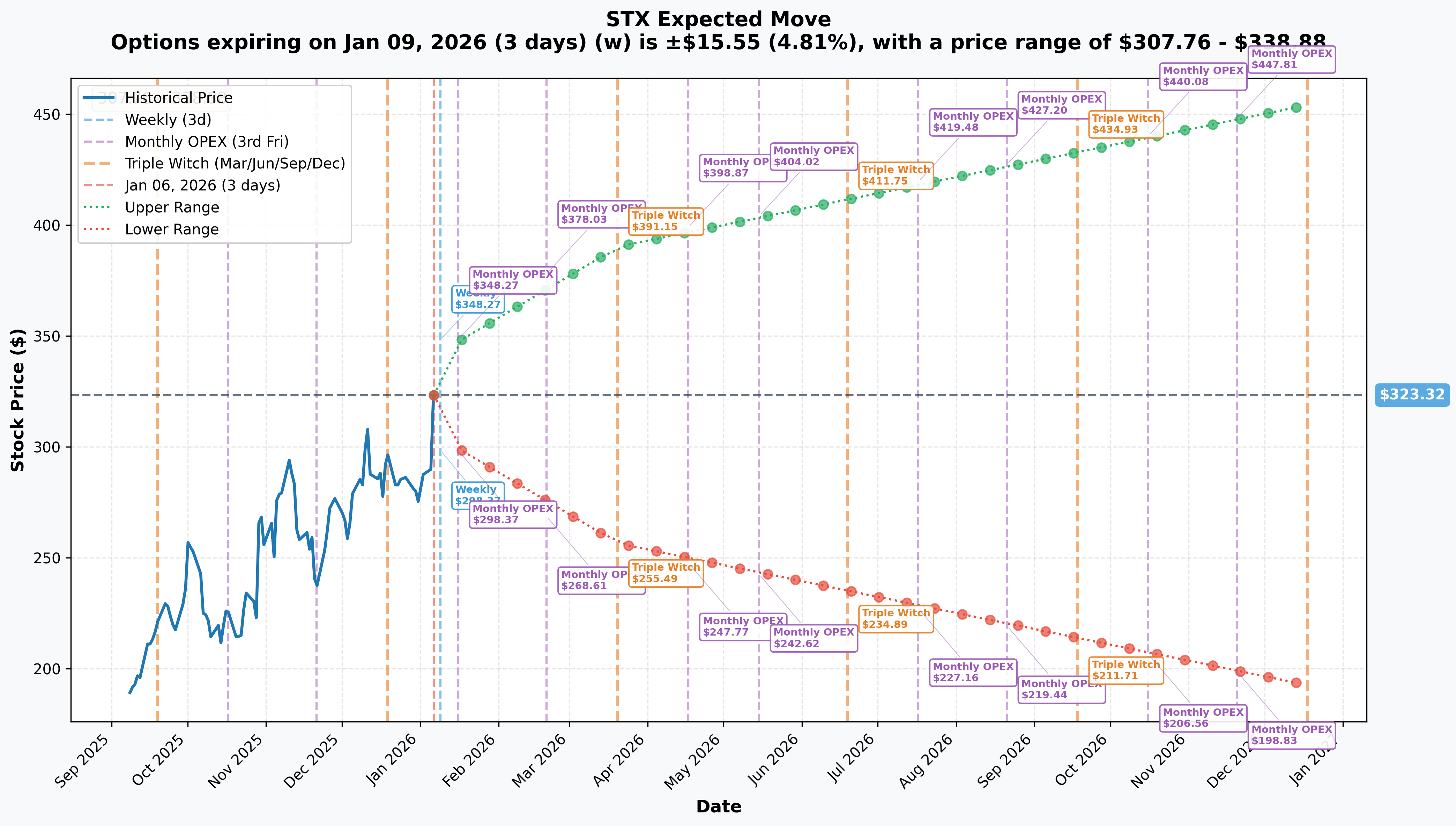

🎯 Implied Move Analysis

The market is pricing in significant volatility across all time frames:

Near-Term Moves:

- 📅 Weekly (Jan 9): ±4.81% → Range: $307.76 - $338.88

- 📅 Monthly OPEX (Jan 16): ±7.51% → Range: $299.05 - $347.59

The Rolled Expirations:

- 📅 March 20 Triple Witch (OLD position): ±20.69% → Range: $256.43 - $390.21

- 📅 June 18 Triple Witch (NEW position): Upper $411.75 / Lower $234.89

Key Insight: By rolling from March to June, the trader bought themselves 3 extra months to capture the June triple witch volatility expansion. The implied move shows potential for $411+ by June - giving the $300 strike massive upside torque while the $300 gamma support provides a safety net.

🎪 Catalysts

🔜 Upcoming (High Impact!)

Q2 FY2026 Earnings (Late January 2026)

- 📅 Expected: January 20-28, 2026

- 💰 Guidance: $2.70B revenue (+/- $100M), $2.75 EPS (+/- $0.20)

- 🎯 What Matters: HAMR shipment volumes, Mozaic 4+ qualification progress, gross margin expansion

- 🔗 According to Nasdaq's earnings calendar, consensus is for $2.79 EPS on $2.7B revenue

- ⚡ Impact: This is the FIRST major catalyst for the new June position!

Mozaic 4+ Volume Production (H1 2026)

- 📅 Timeline: First half of 2026

- 🔬 Significance: Full-scale production of 40TB+ drives following customer qualification

- 🎯 According to TechRadar's coverage, engineering samples already shipped, qualifications happening now

- 💪 Why It Matters: This is the product cycle that justifies the June expiration

Dividend Payment (January 9, 2026)

- 💵 Amount: $0.74 per share (up 3% from prior quarter)

- 📅 Payment Date: January 9, 2026

- 🔗 Per MarketBeat's dividend tracker, this marks the second consecutive year of increases

50% HAMR Exabyte Crossover (H2 2026)

- 📅 Expected: Second half of 2026

- 🎯 Milestone: 50% of nearline exabyte shipments will be HAMR drives

- 🚀 According to Blocks and Files, this represents "unprecedented demand visibility"

✅ Already Happened (Building Momentum)

Nasdaq-100 Index Inclusion (December 22, 2025)

- 🎉 Added to Nasdaq-100 as part of annual reconstitution

- 💰 Triggered mandatory buying from QQQ and 200+ tracking products with $600B+ AUM

- 🔗 Per Nasdaq's official announcement

Blowout Q1 FY2026 Results (October 28, 2025)

- 💰 Revenue: $2.63B (+8% sequential, +21% YoY)

- 📊 Non-GAAP Gross Margin: 40.1% (record high!)

- 💵 Non-GAAP EPS: $2.61 (beat guidance)

- 📈 Data center revenue: $2.1B (80% of total, +34% YoY)

- 🔗 Full details in Seagate's investor relations release

Multiple Analyst Upgrades (Q4 2025)

- 💎 Morgan Stanley: Raised to $337 target (from $270), named "Core 2026 Selection"

- 🎯 Citi: Upgraded to $320 target (from $275)

- 📈 Bank of America: Initiated with $320 target

- 🚀 Loop Capital: Eye-popping $465 high target

- 🔗 Per Yahoo Finance's analyst roundup

🎲 Price Targets & Probabilities

Using the gamma levels, implied moves, and catalyst timeline, here's how this could play out:

🚀 Bull Case (40% Probability): $350-410 by June

Path to Target:

- Q2 earnings (late Jan) beats on HAMR momentum → Stock breaks through $330 resistance

- Mozaic 4+ qualifications proceed on schedule → Momentum accelerates through Q1 2026

- March quarterly earnings confirm margin expansion path → Stock tests $370+

- June triple witch volatility expansion carries stock toward $400+

What Needs to Happen:

- ✅ Q2 earnings beat with strong Mozaic 4+ qualification commentary

- ✅ Gross margins continue expanding toward 50% target

- ✅ Cloud capex spending remains strong (hyperscalers keep ordering)

- ✅ No production issues with HAMR technology ramp

Gamma/IV Support: The implied move shows $411.75 as the upper bound for June expiration. Major gamma resistance at $325-330 needs to break, but once cleared, limited resistance until much higher levels.

⚖️ Base Case (35% Probability): $300-330 Range

Path to Target:

- Q2 earnings meet expectations but don't blow out → Stock consolidates

- Stock trades between $300 gamma support and $330 resistance

- Mozaic 4+ ramp progresses but no major surprises

- June position maintains value but doesn't explode

What Needs to Happen:

- ✅ Steady execution on HAMR roadmap

- ✅ Demand visibility remains through 2026-2027

- ✅ Competitive position vs Western Digital maintained

- ✅ No macro shocks to tech spending

Gamma/IV Support: The $300 strike sits on 0.9B in gamma support - this level should provide a strong floor. Current price of $323 is in the middle of the range, with the monthly implied move suggesting $299-347 by mid-January OPEX.

🐻 Bear Case (25% Probability): $260-290 Pullback

Path to Target:

- Q2 earnings disappoint or guidance cautious → Profit-taking accelerates

- Production issues with Mozaic 4+ delay volume ramp → Tech story questioned

- Broader market correction hits high-flyers → STX gives back 2025 gains

- Insider selling intensifies (CEO already sold $12M+ in 2025)

What Needs to Happen:

- ❌ Earnings miss or conservative guidance

- ❌ Cloud capex spending slowdown concerns

- ❌ HAMR yield or reliability issues emerge

- ❌ Western Digital competitive threats materialize sooner than expected

Risk Level: The March implied move showed $256 as the lower bound, while June shows $234. The $280 old strike has 0.7B gamma support, suggesting that level could provide a bounce zone. However, this is a high-beta name that's up 225% - pullbacks can be vicious.

💡 Trading Ideas

🛡️ Conservative: The "Gamma Floor" Strategy

The Play:

- Wait for a pullback toward the $300-305 zone (major gamma support)

- Buy shares or sell March $290 puts to collect premium at support

- If assigned, you own the stock at a 10%+ discount from current levels

Why This Works: The call roll trader is positioned at $300 for a reason - that's where 0.9B in put gamma creates a natural support shelf. Market makers will defend this level. You're essentially front-running the support.

Probability of Success: ~65%

Max Risk: If the bear case plays out and STX breaks below $280 support, you could see another 5-10% downside to the $260 area

Best For: Investors who want STX exposure but don't want to chase at all-time highs

⚖️ Balanced: The "Earnings Straddle" Play

The Play:

- Buy a January 31, 2026 $320 straddle (one call + one put, same strike)

- Cost: ~$25-30 per contract (estimate)

- You make money if STX moves +/- 8% from $320 by earnings

Why This Works: Q2 earnings (late January) will be a major catalyst with the HAMR story in focus. The monthly implied move is ±7.51%, suggesting the market expects fireworks. A straddle captures movement in either direction - if they beat and stock runs to $350+, your calls print. If they disappoint and stock drops to $285, your puts print.

Probability of Success: ~55% (based on implied volatility)

Max Risk: You lose the premium paid (~$2,500-3,000 per straddle) if stock doesn't move enough by expiration

Best For: Swing traders who want to play earnings volatility without picking a direction

🚀 Aggressive: The "Smart Money Shadow" Trade

The Play:

- Mirror the institutional roll: Buy June 20, 2026 $300 calls

- Current cost: ~$64.50 per contract ($6,450 per contract)

- Target: 50-100% return if STX reaches $370+ by June

Why This Works: You're literally copying the $2.1M institutional trade! They clearly have conviction in the June time frame to capture:

- ✅ Q2 earnings (late January)

- ✅ Q3 earnings (late April)

- ✅ Mozaic 4+ volume production ramp

- ✅ 50% HAMR crossover progress in H2

The $300 strike is already in-the-money by $17.46, giving you intrinsic value protection while the June expiration provides 5+ months of time value.

Probability of Success: ~45% (moderate probability of 50%+ profit)

Max Risk: You can lose 100% of premium if STX craters below $300. With the stock at $323, you have a $23 cushion, but this is a momentum name that's up 225% - volatility cuts both ways.

Position Sizing: Risk no more than 2-3% of portfolio on this trade. If you have a $100K account, that's 1 contract maximum.

Best For: Experienced options traders comfortable with risk who believe in the AI storage thesis

⚠️ Risk Factors

Let's be real about what could go wrong:

🚨 Valuation Stretched AF

- Stock is up 225% in 2025 - much of the good news may be priced in

- Trading at 23x forward P/E vs historical average of 17x

- If growth story stalls, multiple contraction could be brutal

👔 Insider Selling Red Flag

- CEO William Mosley sold $12M+ in stock throughout 2025

- Multiple sales at $270-280 levels (below current price, but still...)

- While under 10b5-1 plans, the pattern is concerning

- 🔗 Per Investing.com's insider tracking

🏭 Execution Risk on HAMR Ramp

- Mozaic 4+ qualification delays could derail the thesis

- Production yield issues on 40TB drives would be a major problem

- According to Blocks and Files, customer qualifications are "unprecedented in complexity"

💻 Competition Heating Up

- Western Digital has 62.83% market share vs STX's 37.17%

- WDC's HAMR launch (late 2027) will intensify competition

- SSD prices declining could make flash more competitive in certain workloads

📉 Cloud Capex Cycle Risk

- 80% of STX revenue comes from data center segment

- Any slowdown in hyperscale spending hits STX hard

- Customer concentration risk with the big cloud providers

🎢 Cyclicality Never Dies

- HDD market is historically super cyclical

- Current "supercycle" will eventually normalize

- When it ends, the stock could give back gains quickly

🎯 The Bottom Line

Real talk: This $4M call roll is a masterclass in professional positioning.

Here's what the smart money is telling us:

- 💰 They're locking in profits from the March $280 calls (probably up big)

- 🚀 But they're staying IN the trade with June $300 calls - still bullish

- ⏰ The June expiration captures Q2 earnings, Q3 earnings, and Mozaic 4+ ramp

- 🛡️ The $300 strike sits on massive gamma support - risk-managed positioning

- 💪 Combined z-scores of 9.33 and 4.22 = institutional conviction

Action Plan Based on Your Position:

If You Own STX:

- 📈 Hold through Q2 earnings (late January) - the setup is strong

- 🎯 Take profits at $350+ if we get there - don't be greedy after a 225% run

- 🛡️ Set a stop at $295 (below gamma support) to protect gains

- ⚠️ Watch for any Mozaic 4+ delays or disappointing earnings guidance

If You're Watching:

- 👀 Wait for a dip to $300-305 to enter (gamma support zone)

- 📅 Mark your calendar for late January earnings - could provide entry point

- 🎯 Consider the balanced straddle play if you want earnings exposure

- ✅ Only chase current levels if you have strong conviction in the AI storage thesis

If You're Bearish:

- 🐻 Wait for Q2 earnings - if they disappoint, we could see $280-290 fast

- 🎯 Look for bearish setups if stock fails at $330 resistance multiple times

- ⚠️ Don't fight the tape yet - this is a strong uptrend with institutional support

- 💭 Remember: Up 225% doesn't mean it can't go higher (but odds get worse)

The Lesson: When you see institutional money rolling options (not just closing), pay attention. They're rebalancing risk but maintaining exposure - that's a bullish sign when done at major gamma support levels. This isn't blind optimism; it's calculated conviction.

Bottom line: The AI storage supercycle is real, STX has the technology lead, and demand visibility through 2027 is unprecedented. But at 225% YTD gains and 23x forward P/E, you're paying up for perfection. The call roll suggests smart money still sees upside, but they're taking chips off the table too. Follow their lead - stay bullish but manage risk! 💪

⚠️ Disclaimer: This analysis is for educational purposes only. Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. The unusual activity described may not predict future price movements. Always do your own research and consider consulting with a financial advisor before making investment decisions. The author may or may not hold positions in STX.

Analysis generated January 6, 2026 Analysis by Ainvest Option Flow