🩺 UTHR $33M Complex Roll - Institutional Position Adjustment at Biotech All-Time Highs! 🎯

📅 December 17, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just executed a $33 MILLION complex options roll on United Therapeutics at 12:10:59 today, adjusting a massive position right after the stock hit all-time highs near $511! This sophisticated three-leg trade closed out $30M worth of existing positions and opened a new $3.5M put position - suggesting institutional players are taking profits and adding downside protection ahead of critical 2026 catalysts. With UTHR up +36.5% YTD and trading at a 40% discount to biotech peers despite having multiple billion-dollar pipeline opportunities, smart money is strategically repositioning rather than abandoning ship.

📊 Company Overview

United Therapeutics Corporation (UTHR) is a biotech powerhouse specializing in pulmonary arterial hypertension (PAH) treatments and pioneering clinical xenotransplantation:

- Market Cap: $21.53 Billion

- Industry: Pharmaceutical Preparations (Biopharmaceuticals)

- Current Price: $511.06 (at all-time highs of $501.05 recently)

- Primary Business: PAH prostacyclin therapies (Tyvaso, Remodulin, Orenitram), plus breakthrough xenotransplant program with world's first clinical trial of gene-edited pig kidneys

The company operates at the intersection of established commercial success ($2.88B revenue in 2024, growing 24% YoY) and transformational pipeline optionality, including potential blockbuster label expansions into idiopathic pulmonary fibrosis (IPF) and revolutionary organ transplantation technology.

💰 The Option Flow Breakdown

The Tape (December 17, 2025 @ 12:10:59):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Premium | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:10:59 | UTHR | BUY | CALL $480 | 2026-01-16 | $480 | $17.0M | 3,900 | - | 3,900 | $511.06 | $43.59 | UTHR20260116C480 |

| 12:10:59 | UTHR | SELL | CALL $520 | 2026-01-16 | $520 | $13.0M | 7,800 | - | 7,800 | $511.06 | $16.67 | UTHR20260116C520 |

| 12:10:59 | UTHR | SELL | PUT $480 | 2026-01-16 | $480 | $3.5M | 3,900 | - | 3,900 | $511.06 | $8.97 | UTHR20260116P480 |

🤓 What This Actually Means

This is a sophisticated position adjustment executed as a single complex trade with precision institutional fingerprints all over it:

What happened:

- 🔄 Closed existing call spread: Bought back 3,900 short $480 calls ($17M) while selling 7,800 long $520 calls ($13M)

- 🆕 Opened new put position: Sold 3,900 $480 puts ($3.5M collected)

- 💵 Net cash flow: -$17M + $13M + $3.5M = -$500K net debit (minimal cost to adjust)

- ⏰ Timing: All legs expire January 16, 2026 (30 days out)

- 📊 Notional exposure: 390,000 shares worth ~$199M at current price

Translation for regular folks: This trader previously held a bullish call spread (long stock + short $480 calls covered by long $520 calls) that was deeply profitable after UTHR's monster 2025 rally. Rather than letting it ride, they:

- Closed the profitable spread, locking in gains from the 36% YTD move

- Simultaneously sold $480 puts to generate premium income and signal willingness to buy UTHR at $480 (6% below current)

Think of it like a homeowner who sold their appreciated house and agreed to buy it back if the price drops 6% - they're taking chips off the table but staying involved if there's a dip.

Unusual Score: 🔥🔥🔥 EXTREME (1,191x average size for UTHR!)

This is the largest UTHR options trade in the past 30 days by an enormous margin. With a Z-score of 80.58 and 100th percentile ranking, this happens maybe once or twice a year. The $33M total premium across all three legs represents the position size of small institutional desks. This isn't retail - this is serious money making calculated adjustments.

📈 Technical Setup / Chart Check-Up

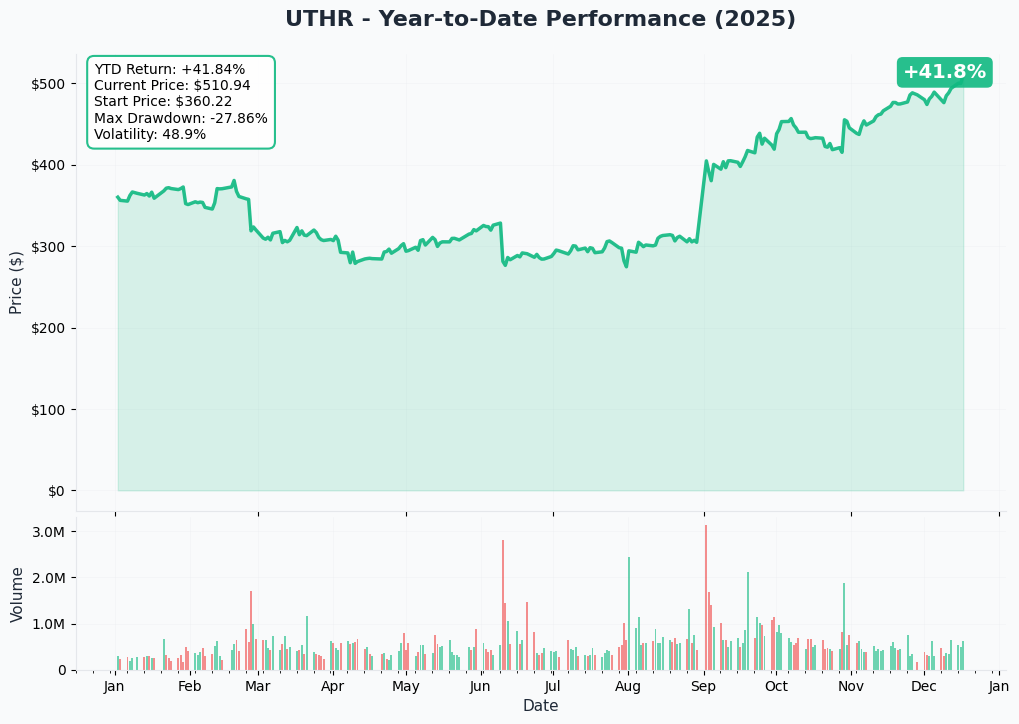

YTD Performance Chart

UTHR is having an absolute monster year - up +36.5% YTD with current price of $511.06 after starting 2025 around $375. The chart tells a powerful biotech growth story with recent acceleration following multiple pipeline catalysts.

Key observations:

- 🚀 Recent breakout: Explosive move from ~$400 in October to all-time highs above $500 in December

- 📈 Strong momentum: Made new all-time high of $501.05 on December 12, 2025 before today's session

- 🎢 Lower volatility than peers: Beta of 0.86 shows UTHR less volatile than broader market despite biotech classification

- 📊 Volume acceleration: Institutional accumulation evident in October-December as catalysts materialized

- 💪 Support building: Recent consolidation around $500 level creating platform for next leg higher

- ⚠️ Overbought near-term: After 27% rally in two months (Oct-Dec), some digestion healthy before next catalyst

The institutional roll-up trade makes perfect sense in this context - take profits after the parabolic move while maintaining exposure to 2026 upside.

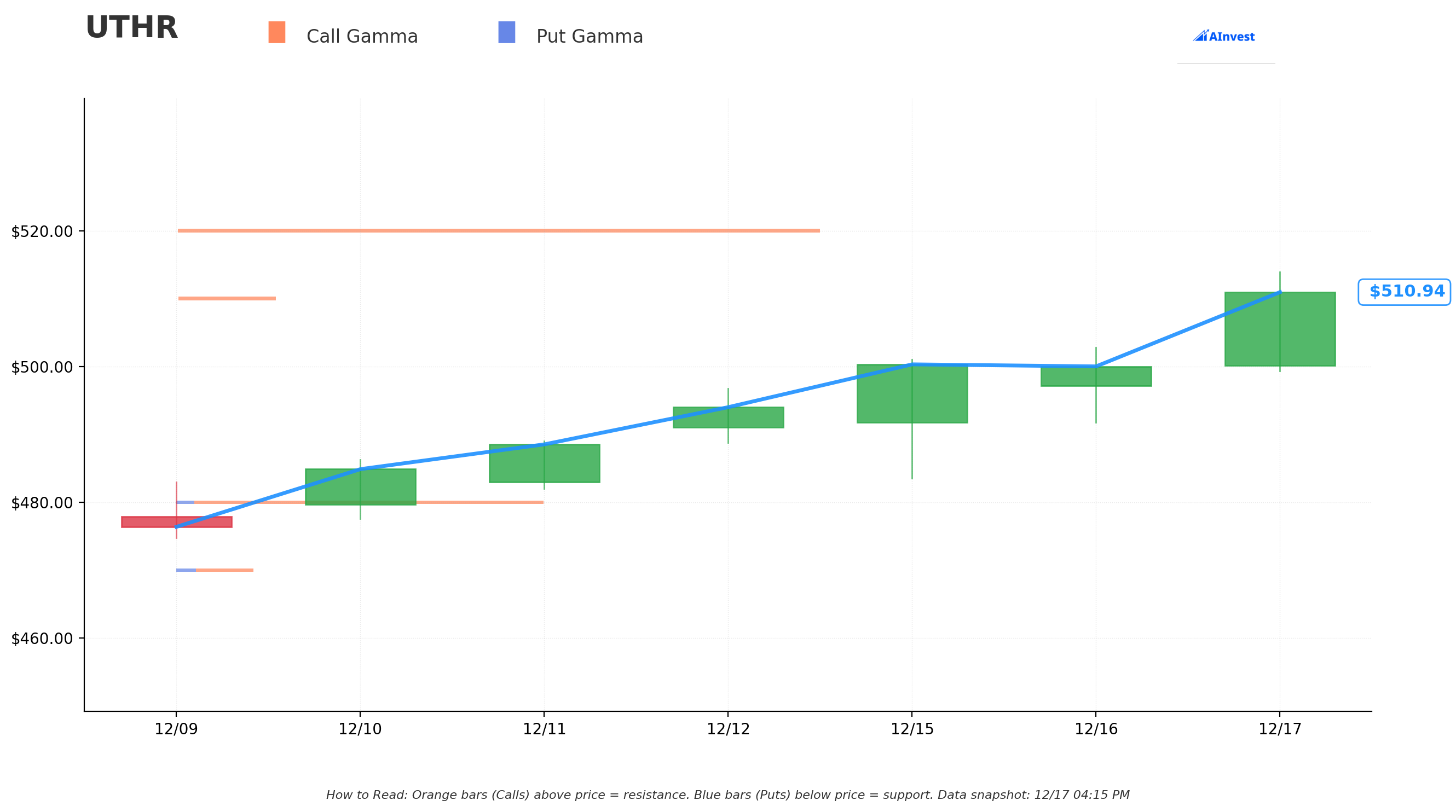

Gamma-Based Support & Resistance Analysis

Current Price: $511.06

The gamma exposure map reveals critical price magnets where dealer positioning will influence near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $510 - Immediate support with 0.31B total gamma exposure (minor floor, 0.2% below current)

- $500 - Secondary support at 0.10B gamma (dealers will provide some buying support, 2.2% cushion)

- $480 - MAJOR structural floor with 1.16B gamma (THIS IS WHERE THE PUTS WERE SOLD! Not coincidental - 6.1% downside)

- $470 - Extended support at 0.24B gamma (8.0% below current)

- $450 - Deep support zone with 0.06B gamma (11.9% below - disaster scenario)

- $440 - Extreme downside at 0.72B gamma (13.9% decline)

🟠 Resistance Levels (Call Gamma Above Price):

- $520 - Immediate ceiling with 2.03B gamma (STRONGEST SINGLE LEVEL - massive dealer short calls here! 1.7% overhead)

- $530 - Secondary resistance at 0.09B gamma (3.7% above current)

- $550 - Extended upside target at 0.04B gamma (7.6% rally required)

What this means for traders: UTHR is trading in a TIGHT range between $510 support and crushing $520 resistance. The gamma data shows $520 has ENORMOUS 2.03B call gamma - the single largest concentration on the entire chain. This means market makers are massively short calls at that strike, creating natural selling pressure as price approaches (they sell stock to hedge as price rises).

Critical insight: The $480 strike where puts were sold sits exactly at the major support level with 1.16B gamma. This trader KNOWS the gamma map and positioned precisely at the structural floor. They're saying "I'll buy UTHR at $480 if it pulls back, but I don't think it goes below that major support."

Net GEX Bias: Bullish (3.99B call gamma vs 1.21B put gamma) - Overall positioning remains constructive with 3.3:1 call/put ratio. However, the massive $520 resistance creates near-term ceiling effect.

Trading strategy implications: UTHR likely stays range-bound $500-$520 until a catalyst breaks it out. The $480 floor provides excellent risk definition for long entries on pullbacks.

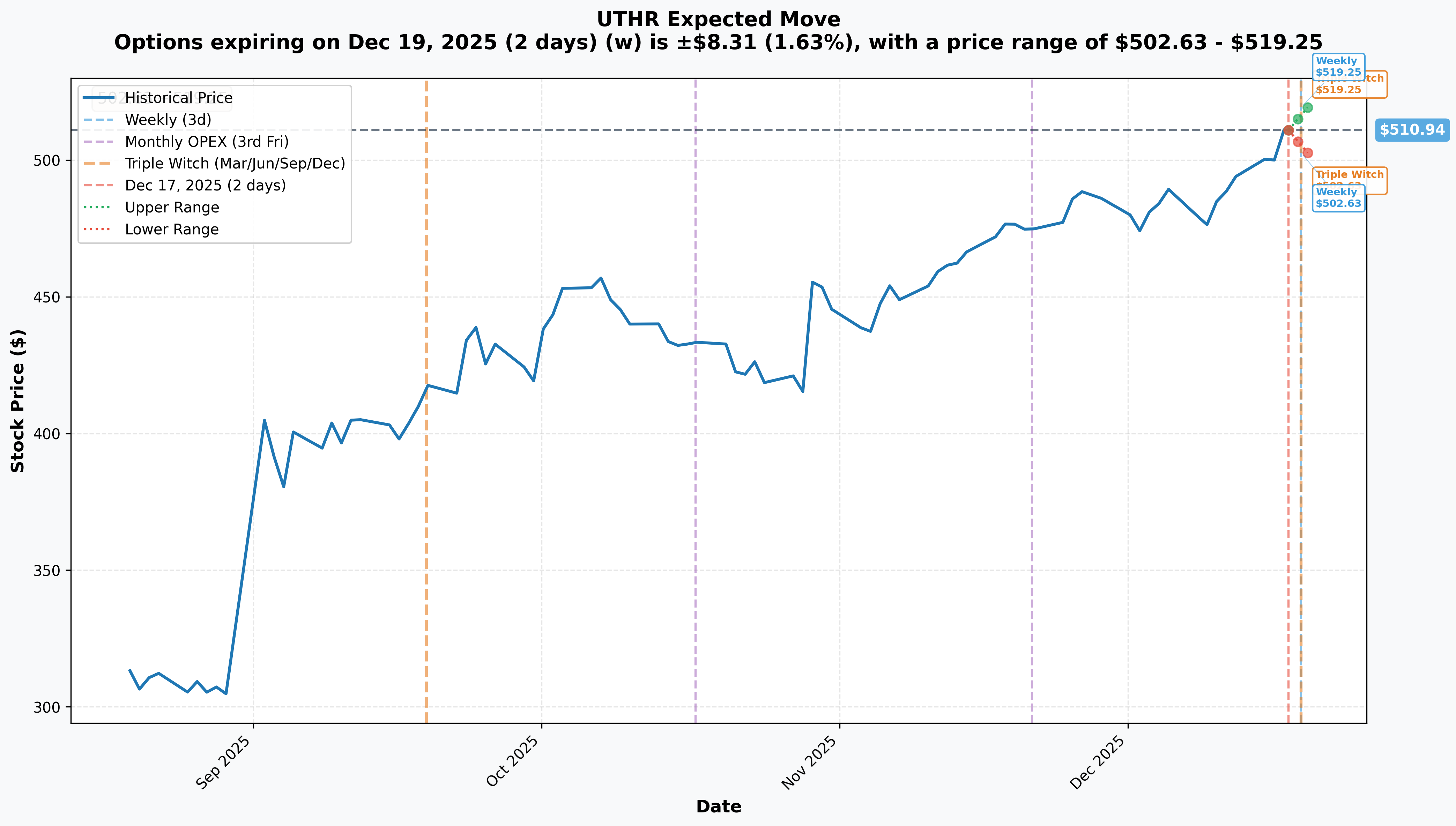

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 2 days): ±$8.31 (±1.63%) → Range: $502.63 - $519.25

- 📅 Monthly OPEX (Dec 19 - 2 days): ±$8.31 (±1.63%) → Range: $502.63 - $519.25

- 📅 Quarterly Triple Witch (Dec 19 - 2 days): ±$8.31 (±1.63%) → Range: $502.63 - $519.25

Key observations:

- ⏰ All expirations converge at December 19 (Friday) - this week's triple witching

- 🎯 Implied move of just 1.63% ($8) reflects low expected volatility near-term

- 📊 Range of $502-$519 brackets current $511 price perfectly between gamma support ($500-$510) and resistance ($520)

- 😌 Market NOT pricing major binary event risk this week - suggests quiet consolidation expected

- 📅 January 16 options (this trade's expiration) would have ~3-4% implied move through that cycle

Translation for regular folks: Options traders expect UTHR to trade in a narrow $502-$519 band through Friday's triple witch expiration. This is TINY for a biotech - reflects the stability of UTHR's established commercial franchise versus typical binary FDA/trial catalysts. The put seller is comfortable with this range - stock would need to drop >$22 from current to breach their $480 strike.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 6 Months - Why This Trade Was Made!)

TETON-1 Data Readout and FDA Engagement (H1 2026) 🫁

Following the overwhelmingly positive TETON-2 results announced September 2, 2025, UTHR is expecting top-line data from the companion TETON-1 study in first half of 2026:

- 📊 Timeline: H1 2026 data readout expected (potentially March-June)

- ✅ De-risked: TETON-2 already met primary endpoint with statistically significant FVC improvement (p <0.0001)

- 🏥 Market: IPF comprises 100,000+ U.S. patients currently served by Boehringer's Ofev and Roche's Esbriet

- 💰 Revenue potential: $1+ billion peak sales from IPF label expansion

- 📋 Regulatory: FDA meeting planned before end of 2025 to discuss expedited review pathway

- 🎯 Probability: High (70-80%) given TETON-2 success validates mechanism

Why this matters for the trade: Positive TETON-1 data could drive 10-15% stock appreciation to $560-580 range, while negative results could send stock back to $450-480 (right where puts are struck). The put seller is betting TETON-1 succeeds OR that $480 floor holds even if it doesn't.

Ralinepag Phase 3 ADVANCE OUTCOMES Data (H1 2026) 💊

Ralinepag represents UTHR's once-daily oral prostacyclin receptor agonist with enrollment completed June 23, 2025 at 728 patients:

- 📅 Timeline: Top-line data expected first half 2026 (likely April-May)

- 🎯 Primary endpoint: Time to first clinical worsening event in PAH patients

- 💪 Phase 2 results: 29.8% reduction in pulmonary vascular resistance; 36.3-meter improvement in 6-minute walk distance

- 💰 Market opportunity: $500M+ peak sales potential with long patent runway

- 🏆 Strategic value: Once-daily oral could capture significant share from existing PAH therapies

- 🎯 Probability: Moderate-to-high (60-70%) based on strong Phase 2 data

CEO Martine Rothblatt stated ralinepag is "exceeding expectations" with "best-in-class results" at the enrollment completion announcement.

Why this matters: Positive ralinepag data adds another growth driver to already-strong PAH franchise, potentially driving stock toward $580-600. Failure would cap upside but likely wouldn't crater stock given established Tyvaso/Remodulin revenues.

UKidney Xenotransplant Clinical Milestones (Ongoing through 2026) 🧬

UTHR is conducting the world's first clinical trial of gene-edited pig kidneys with first patient transplant completed November 2025:

- 🏥 EXPAND study: First-in-human xenotransplantation for end-stage renal disease

- 📊 First cohort: 6 participants with 12-week safety review before proceeding

- 🧬 Technology: 10 gene edits (6 human added, 4 porcine inactivated) via Revivicor subsidiary

- 🏭 Manufacturing: World's first clinical-scale DPF facility with 125 organ/year capacity

- 💰 Market potential: $20B+ kidney transplant market (100,000 U.S. waitlist patients)

- ⏰ Timeline: Multiple safety/efficacy milestones throughout 2026

- 🎯 Probability: Low near-term commercial impact (2028-2030 earliest), but clinical data could drive significant multiple expansion

Why this matters: Successful xenotransplant data could unlock $5-10B in optionality value currently NOT priced in $21B market cap. This is CEO Martine Rothblatt's vision for UTHR's "third pillar" alongside PAH and oncology. Even early positive signals could drive stock to $600-650.

📊 Already Happened (Past 3 Months - What Drove Recent Rally)

TETON-2 Phase 3 Success in IPF (September 2, 2025) ✅

Overwhelmingly positive top-line results triggered initial rally from $400s to $480s:

- ✅ Primary endpoint met: Statistically significant FVC improvement (95.6 mL, p <0.0001)

- ✅ Secondary endpoints: Most showed significant improvements including clinical worsening

- ✅ Safety: Well-tolerated, no new signals versus known prostacyclin profile

- 🎯 Next step: FDA meeting before end 2025 to discuss regulatory strategy

This was the catalyst that proved Tyvaso's efficacy in fibrotic lung disease beyond PAH, validating the IPF expansion thesis.

Q3 2025 Earnings Beat & Record Revenue (October 30, 2025) 💰

Strong Q3 results maintained upward momentum:

- 📊 Q3 Revenue: Exceeded expectations with continued PAH franchise growth

- 💪 Tyvaso: Maintained market leadership in PAH/PH-ILD indications

- 📈 Full-year 2024: $2.88B revenue (up 24% YoY), 11 consecutive quarters of double-digit growth

- 🎯 Guidance: Management commentary on TETON FDA engagement boosted confidence

All-Time Highs (December 12, 2025) 🚀

Stock reached $496.73 (then revised to $501.05) creating natural profit-taking opportunity:

- 📈 YTD gain of 36.5% outpaced biotech sector

- 💰 Market cap expanded to $22.3B

- ⚖️ Valuation still attractive: P/E of 18.73 vs biotech median of ~27

- 🎯 Analyst price targets: Average $487.90, range $314-$600

This is precisely when smart money adjusts positions - at all-time highs before major 2026 catalysts.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timing through January 16th expiration:

📈 Bull Case (30% probability)

Target: $560-$600

How we get there:

- 🎯 Early positive signals from TETON-1 trial enrollment completion or interim data

- 💪 Q4 2025 earnings (late February) exceed with Tyvaso revenue accelerating

- 🏥 UKidney trial updates showing successful organ function in first patient(s)

- 📊 Analyst upgrades following FDA meeting readouts on IPF filing strategy

- 🚀 Break above $520 gamma resistance triggers technical rally

- 💰 Institutions accumulate ahead of ralinepag data anticipated April-May

- 🇺🇸 Potential partnership/collaboration announcements for xenotransplant platform

Key metrics needed:

- Tyvaso revenue growth >25% YoY maintaining momentum

- IPF regulatory pathway clarity (Priority Review designation possible)

- Xenotransplant safety data continuing to meet expectations

- No unexpected competitive or regulatory setbacks

Probability assessment: 30% because it requires multiple positive catalysts to align before January expiration. More likely these catalysts play out over Q1-Q2 2026 timeframe. However, any one major positive (early TETON-1 data leak, spectacular earnings) could push to $560+.

🎯 Base Case (50% probability)

Target: $480-$530 (CONSOLIDATION AT HIGHS)

Most likely scenario:

- 📊 Stock consolidates recent gains in $480-$520 gamma range

- ⏰ Market waits patiently for H1 2026 catalyst clarity (TETON-1, ralinepag)

- 💰 Q4 earnings solid but not spectacular - meets expectations

- 🧬 UKidney trial progresses normally without major newsflow

- 📈 Occasional tests of $520 resistance rejected by dealer gamma selling

- 🛡️ Pullbacks to $500-$510 support met with institutional buying

- 😌 Low implied volatility environment persists (1.6% moves)

- 💤 Trading volume normalizes after recent breakout surge

This is EXACTLY what the put seller expects: Stock trades sideways-to-up in $490-$530 range, puts expire worthless collecting full $3.5M premium. They're effectively saying "UTHR won't drop below $480 before January expiration - I'll collect premium while waiting for 2026 catalysts."

Why 50% probability: Stock at technical equilibrium after big move. No near-term binary catalysts to force breakout or breakdown. Valuation reasonable so no urgency to sell, but rally needs fresh catalyst to continue. Most institutions will hold through year-end and reassess in Q1.

Put P&L in Base Case:

- Stock at $500-$530: Puts expire worthless, seller keeps $3.5M (100% profit on premium collected)

- Stock at $490: Puts worth ~$1-2, seller still profits $2.5-3M (70-85% gain)

- Stock at $480: Puts at-the-money worth ~$5-8, seller profits $1-2M (30-60% gain)

📉 Bear Case (20% probability)

Target: $440-$480 (TEST THE PUT STRIKE!)

What could go wrong:

- 😰 TETON-1 enrollment issues or unexpected FDA feedback delays IPF filing

- 🚨 Ralinepag trial safety concern or enrollment delay surfaces

- ⚠️ UKidney trial experiences rejection episode or safety event requiring pause

- 💸 Broader biotech sector selloff (rising rates, risk-off sentiment)

- 📉 Competitor threat: Merck's Winrevair gains PAH share faster than expected

- 🇨🇳 China export restrictions impact international expansion plans

- 💰 Q4 earnings disappoint on Tyvaso growth deceleration or margin compression

- 🔨 Break below $500 support triggers technical selling cascade

- ⚖️ Liquidia's YUTREPIA generic competition bites harder than anticipated

Critical support levels:

- 🛡️ $510: Immediate gamma support (0.31B) - first test

- 🛡️ $500: Secondary floor (0.10B gamma) - psychological level

- 🛡️ $480: MAJOR GAMMA WALL (1.16B) + put strike - THIS IS THE LINE IN THE SAND

- 🛡️ $470: Extended support (0.24B gamma) - would trigger stop losses

- 🛡️ $450: Deep support (0.06B gamma) - disaster scenario

Probability assessment: Only 20% because UTHR's fundamentals remain extremely strong. The company has:

- ✅ Established $2.88B revenue base growing 24% YoY (not a speculative biotech)

- ✅ Multiple products (Tyvaso, Remodulin, Orenitram) reducing single-product risk

- ✅ Already-successful TETON-2 trial de-risks IPF program significantly

- ✅ 40% valuation discount to biotech peers provides cushion

- ✅ Strong balance sheet with $1B buyback completed 2024

For bear case to play out, would need multiple negative catalysts simultaneously OR a broader market crash. The put seller clearly thinks bear case is <20% likely or they wouldn't collect just $3.5M premium to risk buying $199M notional at $480.

Put P&L in Bear Case:

- Stock at $460: Puts worth $20, seller LOSES -$11/share × 3,900 = -$4.3M (loss exceeds premium collected!)

- Stock at $450: Puts worth $30, seller LOSES -$21/share × 3,900 = -$8.2M (major loss)

- Stock at $440: Puts worth $40, seller LOSES -$31/share × 3,900 = -$12.1M (ouch!)

The put seller is taking REAL risk here - if UTHR drops to $450-460 zone, they lose multiples of premium collected and are forced to buy stock at $480 while it trades $450. This isn't a riskless premium collection - it's a conviction trade that $480 holds.

💡 Trading Ideas

🛡️ Conservative: Follow Smart Money on Pullbacks

Play: Wait for pullback to $480-490 zone to establish long position

Why this works:

- 🎯 Institutions just signaled $480 is the floor they're willing to defend

- 📊 Major 1.16B gamma support at $480 provides structural cushion

- 💰 Buying 6% below current price ($511) provides margin of safety

- ⏰ H1 2026 catalysts (TETON-1, ralinepag) provide clear upside drivers within 3-6 months

- 📈 Valuation attractive: 18.7x P/E vs biotech median 27x (40% discount)

- 🛡️ Established revenue base ($2.88B) limits downside versus speculative biotechs

- 💪 Stock hasn't visited $480 since October - pullback would be healthy consolidation

Action plan:

- 👀 Set alert for UTHR at $485 (would indicate move toward institutional floor)

- 🎯 Accumulate shares in $480-490 range if pullback materializes

- 📊 Initial position size: 50% of intended allocation

- 🔄 Add remaining 50% if stock holds $480 and reverses higher

- ⏰ Target hold through Q1 2026 earnings and catalyst updates

- 📈 Price targets: $540 conservative (5% above $520 resistance), $580 bull case (break above resistance)

- 🛡️ Stop loss: Close below $470 (below major gamma support signals technical breakdown)

Position sizing: 5-10% of portfolio (core long-term holding size for quality biotech)

Risk level: Low-to-moderate (buying pullback with institutional support) | Skill level: Beginner-friendly

Expected outcome: Capture 8-15% gain from pullback entry to next leg higher. Minimize risk by buying where institutions are positioned.

⚖️ Balanced: Cash-Secured Put at Institutional Strike

Play: Sell cash-secured $480 puts (February or March expiration)

Structure: Sell $480 puts, collect premium, use cash to secure obligation

Why this works:

- 🤝 Copy the trade: Institutions just sold $480 puts - follow their lead at same strike

- 💰 Premium income: Collect $8-12 per share (~2-2.5% return in 30-60 days)

- 🎯 Comfortable entry: If assigned, buying UTHR at $480 provides 6% discount to current $511

- 🛡️ Gamma support: Major 1.16B support at strike provides technical floor

- ⏰ Catalyst timing: February expiration captures Q4 earnings (late Feb), March captures pre-TETON-1 period

- 📊 Breakeven protection: $471-472 effective entry if assigned (after premium collected)

- ✅ Win-win: Either collect premium if stock stays above $480, or buy quality biotech at discount

Estimated P&L (adjust based on current IV):

- 💰 Collect: ~$8-12 per contract ($800-1,200 per put)

- 📈 Max profit: $800-1,200 if UTHR above $480 at expiration (stock assigned away)

- 📉 Breakeven: $471-472 (strike minus premium collected)

- 🎯 Downside: Obligated to buy UTHR at $480 if below, but offset by premium

- 📊 Return on capital: 2-2.5% in 30-60 days (annualized 12-18%)

Entry timing:

- ⏰ Enter when UTHR trades $500-515 (provides cushion above strike)

- ❌ Skip if UTHR below $490 (too close to strike)

- 📊 Target IV percentile >40% (avoid selling puts when vol too low)

Position sizing: 1-2 puts per $100K portfolio (manage assignment risk)

Risk management:

- 🛡️ Must have cash to buy 100 shares per put at $480 ($48,000 per contract)

- 📉 If assigned, holding quality company with 2026 catalysts ahead

- 🔄 Can roll down and out if UTHR drops toward $480 before expiration

- ⚠️ Avoid if unable to accept assignment (this is effectively buying with extra steps)

Risk level: Moderate (obligation to buy on assignment) | Skill level: Intermediate

🚀 Aggressive: Bullish Call Spread Targeting Catalyst Breakout (ADVANCED!)

Play: Buy call spread betting on $520 resistance break from 2026 catalysts

Structure: Buy $520 calls, Sell $560 calls (March 20, 2026 expiration)

Why this could work:

- 🎯 Catalyst-timed: March expiration captures Q4 earnings (late Feb) and potential early TETON-1/ralinepag updates

- 💥 Defined risk: $40 wide spread = $4,000 max risk per spread (instead of buying stock)

- 🚀 Leverage: If UTHR rallies to $560-580 on positive catalysts, spread pays $40 (10x return on $4 cost)

- 📊 Break resistance: $520 has massive 2.03B call gamma - breakout above could trigger squeeze to $550-560

- 💪 Multiple shots on goal: TETON-1 interim data, ralinepag final enrollment updates, Q4 earnings all potential catalysts

- ⏰ Time value: 90+ days to expiration gives catalysts time to play out

- 🎰 Risk/Reward: Risk $4 to make $36 (9:1 payoff if catalysts deliver)

Why this could blow up (SERIOUS RISKS):

- ⏰ Catalyst timing risk: TETON-1/ralinepag data might not come until April-May (after expiration)

- 🛡️ Gamma ceiling: $520 resistance is MASSIVE (2.03B) - dealers will fight breakout attempts

- 📉 Consolidation scenario: Stock could trade $490-520 entire time, spread expires worthless

- 😰 Negative catalyst: Any trial delay/issue sends stock to $480, full loss

- 💸 Time decay: Theta burns value daily if stock doesn't move

- ⚠️ Earnings risk: Q4 earnings could disappoint, sending stock lower

Estimated P&L (adjust based on entry timing):

- 💰 Cost: ~$4-6 net debit per spread (pay for $520 call, collect for $560 call)

- 📈 Max profit: $34-36 if UTHR above $560 at expiration (850-900% ROI!)

- 🚀 Partial profit: $15-20 if UTHR at $540 (300-500% ROI)

- 📉 Partial loss: -$2-3 if UTHR at $510 (50-75% loss)

- 💀 Total loss: -$4-6 if UTHR below $520 at expiration (100% loss)

Breakeven: ~$524-526 (long strike plus net debit paid)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand catalysts might not materialize before March expiration

- ✅ Can afford to lose ENTIRE premium (real possibility if consolidates)

- ✅ Accept you're betting AGAINST the $520 gamma resistance wall

- ✅ Have traded biotech catalyst events before (understand binary nature)

- ✅ Won't panic sell if stock dips to $490-500 range before rallying

- ⏰ Can monitor position and adjust if catalyst timing shifts

Alternative structure if more conservative:

- 🎯 Use April or May expiration (more time for catalysts)

- 📊 Tighten spread to $520/$540 (lower cost, lower max gain)

- 🔄 Scale into position - buy 1/3 now, 1/3 after earnings, 1/3 on pullback

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35-40% (below 50% due to massive gamma resistance and catalyst timing uncertainty)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🧪 TETON-1 trial risk: While TETON-2 succeeded, TETON-1 failure would complicate FDA approval pathway for IPF indication. Would likely trigger 15-20% selloff back to $400-420 range. Company planning FDA meeting before end 2025 - any negative regulatory feedback could spook market. IPF expansion represents $1B+ revenue opportunity - loss would cap growth story.

-

💊 Ralinepag Phase 3 execution risk: ADVANCE OUTCOMES trial success is NOT guaranteed despite strong Phase 2 data showing 29.8% reduction in pulmonary vascular resistance. Phase 3 trials measure harder endpoint (clinical worsening events) over longer duration. Safety issues, enrollment problems, or efficacy miss would eliminate $500M+ peak sales opportunity and trigger 10-15% drop. Data expected H1 2026 but timing uncertain.

-

🧬 Xenotransplant program binary risk: UKidney first-in-human trial is revolutionary but HIGHLY experimental. Organ rejection, immune complications, or safety events would halt program and damage company credibility. While not material to near-term revenues, negative xenotransplant data could crater "third pillar" thesis and remove $5-10B optionality value from market cap. Timeline to commercial revenue not until 2028-2030 even if successful.

-

⚖️ Competitive pressure from Merck's Winrevair: Sotatercept's 84% reduction in clinical worsening represents first disease-modifying PAH therapy versus UTHR's symptom management prostacyclins. While positioned for combination therapy initially, could shift treatment paradigms structurally away from treprostinil products. Faster-than-expected Winrevair adoption could pressure Tyvaso/Remodulin market share and pricing.

-

💸 Liquidia YUTREPIA generic competition: Direct treprostinil DPI competitor approved May 2025 represents first generic-style threat to Tyvaso DPI. Pricing pressure and market share erosion possible over 2026-2027. Q4 2024 revenue miss ($735.9M vs $739.9M consensus) and EPS shortfall ($6.19 vs $6.68) raised concerns about Tyvaso growth deceleration already - Liquidia could accelerate this.

-

📊 Valuation concentration risk at all-time highs: Stock at $511 near recent high of $501 after 36.5% YTD gain. While P/E of 18.7x remains attractive versus biotech median 27x, stock has limited margin of safety if catalysts disappoint. Already priced for successful pipeline execution - no cushion for errors. Any negative surprise could trigger 15-20% correction to $410-435 zone rapidly.

-

🌐 Part D benefit design policy risk: While 2024 Inflation Reduction Act initially boosted utilization, future Medicare policy changes could impact commercial dynamics for specialty pharmaceuticals. Drug pricing legislation could limit pricing power for new indications (IPF). CMS reimbursement cuts would pressure margins.

-

💰 Insider selling and institutional repositioning: EVP & General Counsel Paul Mahon sold 11,000 shares in August 2025 under 10b5-1 plan. Wellington Management reduced stake by 28.69%. This institutional roll-up trade signals more sophisticated players are taking chips off table at highs. When smart money derisks, retail should pay attention.

-

🏭 Manufacturing capacity constraints: Current DPF facility has just 125 organ/year capacity - insufficient for commercial-scale xenotransplantation. Would need hundreds of millions in additional facility investment before seeing revenue, creating near-term cash burn if trials succeed. Supply chain complexities for biologic products could delay launches.

-

⏰ Catalyst timing uncertainty creates theta risk: H1 2026 is broad window for TETON-1 and ralinepag data. Could come in March (early) or June (late) - dramatically affects option positioning. January 16 expiration (this trade) likely too early for data, but March/April expirations face timing risk. If catalysts slip to Q3 2026, near-term options expire worthless.

-

🎢 Beta of 0.86 provides limited downside protection: While lower volatility than market is typically good, means UTHR won't significantly outperform in risk-off environments. Broader biotech sector selloff or market crash would drag UTHR down despite strong fundamentals. March 2024 drawdown example: UTHR not immune to macro.

🎯 The Bottom Line

Real talk: Someone just executed a $33 MILLION complex options adjustment on UTHR right after it hit all-time highs - this is TEXTBOOK profit-taking by sophisticated institutional money. They're not abandoning the story (they're staying involved via the put sale), but they're definitely locking in gains from the 36% YTD rally and reducing exposure before 2026's high-stakes binary catalysts.

What this trade tells us:

- 💰 Institutions are HAPPY with gains from $375 → $511 rally (36.5%) and taking money off the table

- 🎯 They're willing to buy back at $480 (6% lower) if pullback materializes - signals that's the floor

- ⚖️ They're derisking BEFORE TETON-1 and ralinepag data (smart!) rather than hoping for home runs

- 📊 The $480 put sale shows conviction that major gamma support holds through January

- 🔄 This is position management, not bearishness - they're adjusting, not exiting

This is NOT a "sell everything" signal - it's a "take some profits and wait for better entry" signal.

If you own UTHR:

- ✅ Consider trimming 20-30% at $505-515 levels to lock in triple-digit gains

- 📊 Remaining position protected by strong fundamentals ($2.88B revenue base, 24% growth)

- 🛡️ Set mental stop at $470 (below major $480 gamma floor signals technical breakdown)

- ⏰ Don't get greedy - up 36% YTD is EXCELLENT for a large-cap biotech

- 🎯 If stock pulls back to $480-490, consider rebuying trimmed shares (institutions signaling support there)

- 💡 Consider selling covered calls at $520 (collect premium against massive gamma resistance)

If you're watching from sidelines:

- 🎯 $480-490 is your entry zone - that's where institutions are positioning to buy

- ⏰ Be patient - let profit-takers finish selling after the big run

- 📊 Pullback would be HEALTHY consolidation, not breakdown (support at $480 strong)

- 🚀 Longer-term (3-6 months), TETON-1 data, ralinepag results, and xenotransplant milestones are legitimate catalysts for $560-600+

- ⚠️ Current valuation (18.7x P/E) is attractive but requires execution - one stumble and it's back to $450-470

- 💪 Quality biotech with established revenue, multiple products, and transformational pipeline - rare combination

If you're bearish:

- ⚖️ Fighting 36% momentum at all-time highs is tough, but institutional profit-taking validates caution

- 🎯 Wait for break below $500 before initiating shorts - $510 support needs to fail first

- 📊 Major support at $480 (1.16B gamma) - that's the level to watch

- ⚠️ Selling cash-secured puts at $480 offers better risk/reward than outright shorts

- 📉 Watch for negative catalysts: TETON-1 delays, ralinepag safety concerns, xenotransplant issues

- ⏰ Timing is EVERYTHING - premature bearish positioning risks missing further upside if catalysts deliver early

Mark your calendar - Key dates:

- 📅 Late December 2025 - FDA meeting results on IPF regulatory pathway (timing uncertain)

- 📅 January 16, 2026 - Monthly OPEX, expiration of this $33M roll trade

- 📅 Late February 2026 - Q4 2025 earnings report (critical Tyvaso revenue trends)

- 📅 March-June 2026 (H1) - TETON-1 top-line data expected (timing uncertain)

- 📅 April-May 2026 (H1) - Ralinepag ADVANCE OUTCOMES data expected (timing uncertain)

- 📅 Throughout 2026 - Multiple UKidney trial milestones and safety reviews

Final verdict: UTHR's story remains INCREDIBLY compelling - the IPF expansion could add $1B+ peak sales, ralinepag represents best-in-class oral PAH therapy, and xenotransplantation offers legitimate "third pillar" optionality worth billions. The $2.88B revenue base growing 24% YoY provides stability rare in biotech. Trading at 40% discount to biotech peers (18.7x vs 27x median P/E) offers valuation cushion.

BUT, at $511 near all-time highs after 36% YTD gain, the risk/reward is NO LONGER screaming BUY at current levels. The $33M institutional roll is a CLEAR signal: smart money is derisking at the peak and will reload at $480 if given the chance.

Be patient. Wait for the $480-490 pullback that institutions are positioning for. The 2026 catalysts will still be there in 6-8 weeks, and you'll sleep better at night paying $485 instead of $515.

The biotech innovation story is real. The catalysts are legitimate. But timing matters. Let the profit-takers finish. Buy where smart money is willing to step in. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 1,191x unusual score reflects this specific trade's size relative to recent UTHR history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Clinical trials carry binary risk with potential for 15-25% moves either direction on data releases. The put seller may have complex portfolio hedging needs not applicable to retail traders.

About United Therapeutics Corporation: United Therapeutics specializes in treating pulmonary arterial hypertension with a focus on the prostacyclin pathway, marketing five primary treatments while pioneering clinical xenotransplantation with the world's first gene-edited pig kidney trial. Market cap: $21.53 billion in the Pharmaceutical Preparations sector.