🚨 VERA: Massive Call Selling Hits Biotech Following 110% Rally!

📅 December 31, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dumped $6.5 MILLION worth of VERA calls across two strikes, marking one of the largest single-day options exits we've tracked. This isn't retail panic—institutional money is taking chips off the table after VERA's explosive 110% rally in Q4 2025, right as the stock trades at $50.70 near its all-time high of $56.05. Time to see what smart money knows that we don't... 👀

💰 Company Overview

Vera Therapeutics, Inc. (NASDAQ: VERA)

- Market Cap: $3.63 billion

- Sector: Pharmaceutical Preparations

- What They Do: Clinical-stage biotech developing atacicept, a weekly subcutaneous injection designed to block proteins that drive autoimmune diseases, with lead indication in IgA nephropathy (rare kidney disease)

📊 The Option Flow Breakdown

💸 What Just Happened

Here's the tape from December 31, 2025 at 11:46 AM ET:

| Time | Symbol | Buy/Sell | C/P | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:46:26 | VERA | SELL | CALL | 2026-02-20 | $3.2M | $45 | 4,000 | 23 | 4,000 | $50.70 | $8.05 | VERA20260220C45 |

| 11:46:26 | VERA | SELL | CALL | 2026-01-16 | $3.3M | $40 | 3,000 | 3,500 | 3,000 | $50.70 | $11.00 | VERA20260116C40 |

Total Premium: $6.5 MILLION Total Contracts: 7,000 calls Classification: Sell-to-Close (STC) Unusual Score: Z-Score of 4.23 and 3.17 (EXTREMELY UNUSUAL)

🤓 What This Actually Means

Real talk: This is textbook profit-taking by someone who got in before VERA's massive rally. Here's why:

🔍 Trade #1: February $45 Calls ($3.2M)

- 174x the average activity (Z-score 4.23)

- Deep in-the-money calls ($45 strike vs $50.70 stock price)

- Only 23 open interest means this trader controlled almost the entire position

- Premium of $8.05 = $5.70 intrinsic value + $2.35 time value

🔍 Trade #2: January $40 Calls ($3.3M)

- 3.17 standard deviations above normal (EXTREMELY UNUSUAL)

- Even deeper in-the-money ($40 strike vs $50.70 stock)

- 3,000 contracts at $11.00 = $10.70 intrinsic + $0.30 time value

- Only 16 days to expiration (expires January 16, 2026)

Translation for us regular folks: Someone bought these calls when VERA was trading much lower (likely in the $30s or low $40s) and is now cashing out near the all-time high. They're locking in gains before the FDA decision, not adding to positions. This is smart money saying "I made my money, time to reduce risk."

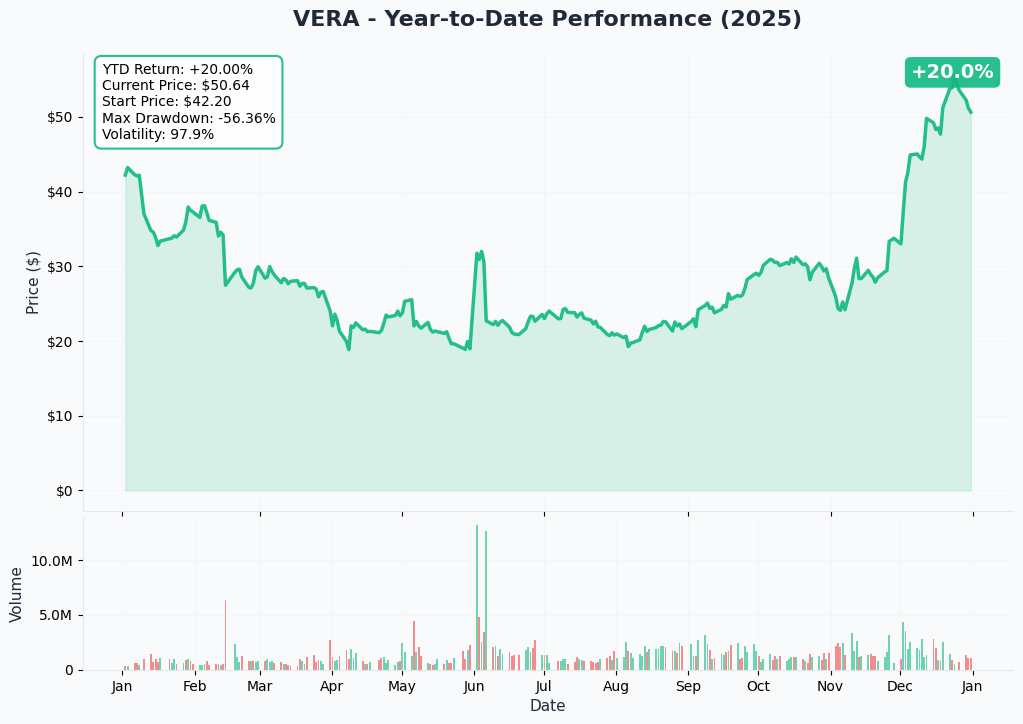

📈 Chart Check-Up

YTD Price Action

VERA's chart tells a wild story of transformation in 2025:

- Q1-Q2 2025: Brutal selloff from $40s to lows of $18.53 in April

- June-October: Slow grind back to $30s range

- November 6: +82% explosion to $44 on Phase 3 trial results

- Q4 Rally: Continued surge to $56.05 all-time high

- Current: Trading at $50.70, up 110%+ from April lows

The chart shows VERA has been on an absolute tear since the ORIGIN Phase 3 trial results were published in the New England Journal of Medicine showing 46% proteinuria reduction. The stock has more than doubled in under 2 months—this is the kind of move that forces professional traders to lock in profits.

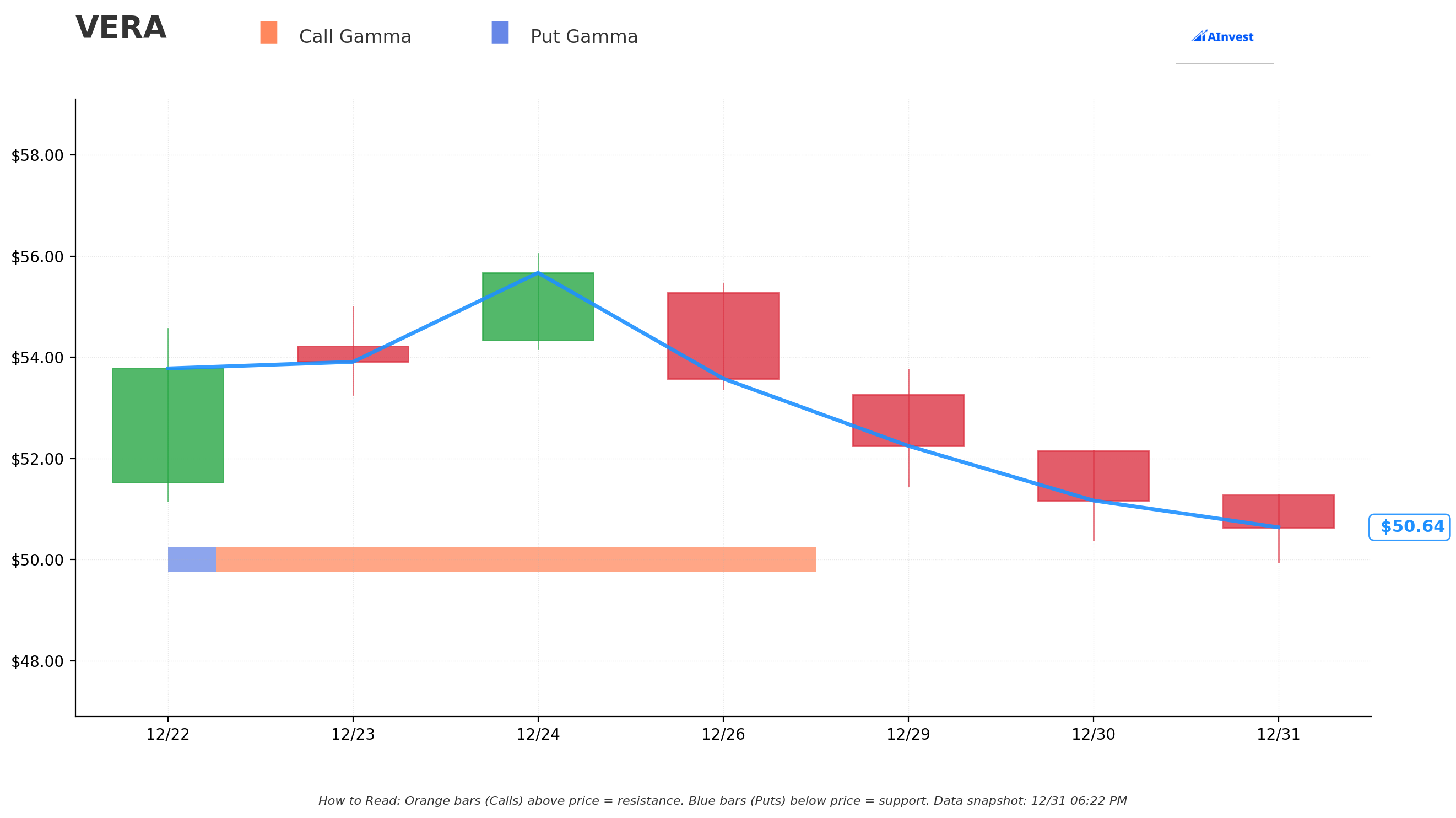

🎯 Gamma-Based Support & Resistance Analysis

Current Price: $50.02

Support Levels (Blue Bars = Put Gamma):

- $50.00 (Strongest Support) - Net GEX: 0.502, Total GEX: 0.590

- Just 0.04% below current price

- This is critical short-term floor—heavy call interest creates dealer support

- $45.00 (Secondary Support) - Net GEX: 0.132, Total GEX: 0.173

- 10% below current price

- Matches the strike from today's $3.2M call sale

Resistance Levels (Orange Bars = Call Gamma):

- $55.00 (Immediate Resistance) - Net GEX: 0.030, Total GEX: 0.036

- 9.96% above current price

- First major ceiling to break for continued upside

- $60.00 (Major Resistance) - Net GEX: 0.156, Total GEX: 0.157

- 19.95% above current price

- Significant options interest creating selling pressure

Net GEX Bias: Bullish (Call GEX 1.009 vs Put GEX 0.113)

Despite today's heavy call selling, the overall gamma structure remains bullish with 9x more call gamma than put gamma. Market makers are positioned to support rallies but will face resistance at $55 and $60.

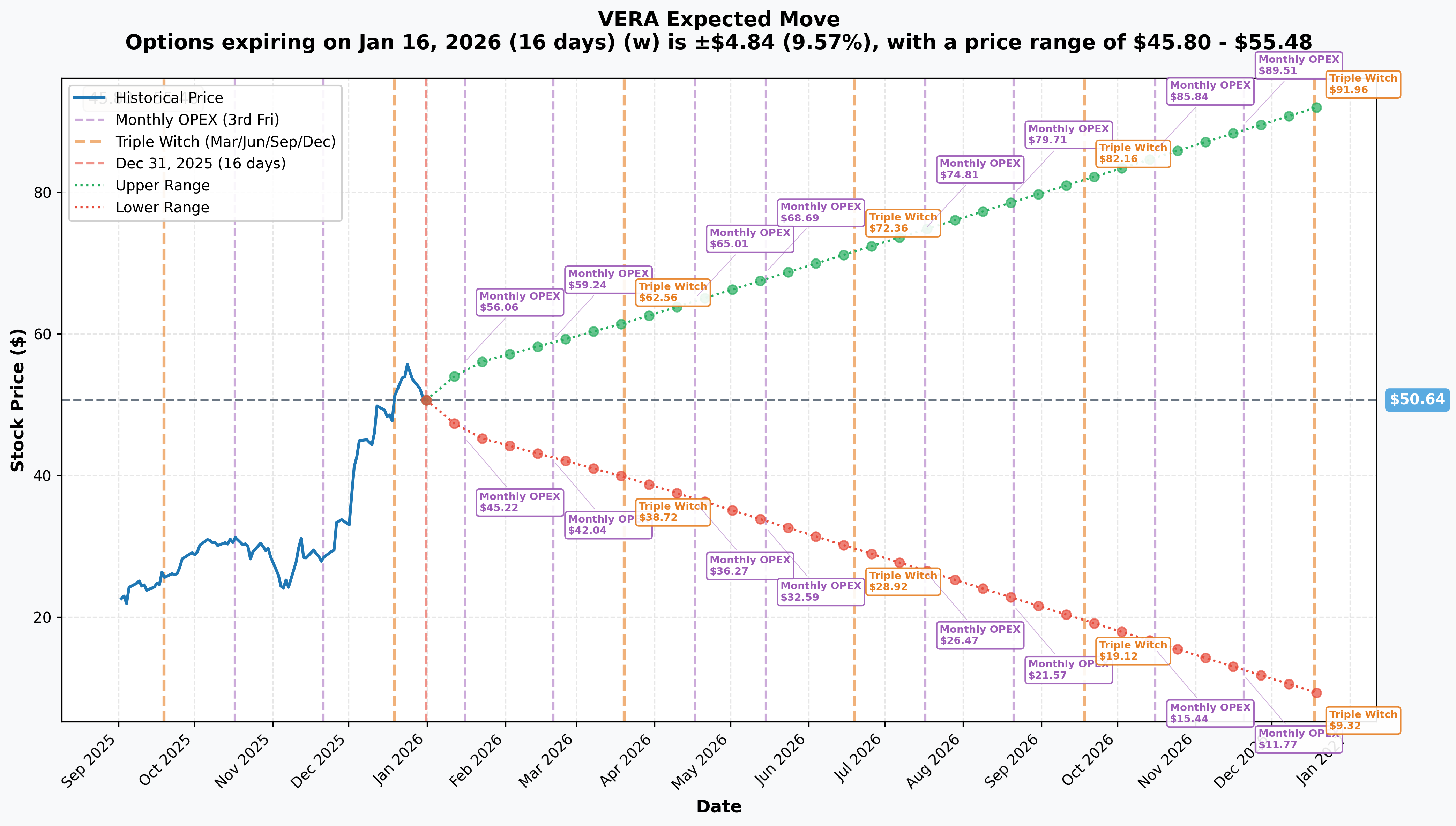

📊 Implied Move Analysis

The options market is pricing in significant volatility ahead. Here's what the straddles tell us:

Monthly OPEX (January 16, 2026 - 16 days):

- Implied Move: 9.57% ($4.84)

- Upper Range: $55.48

- Lower Range: $45.80

Quarterly Triple Witch (March 20, 2026 - 79 days):

- Implied Move: 21.57% ($10.92)

- Upper Range: $61.56

- Lower Range: $39.72

Yearly LEAPS (December 18, 2026 - 352 days):

- Implied Move: 81.6% ($41.32)

- Upper Range: $91.96

- Lower Range: $9.32

Translation: The market expects VERA to trade between $46-$55 by mid-January, with a wider $40-$62 range by March. The massive 82% implied move for full-year 2026 reflects the binary FDA approval event expected mid-2026.

🎪 Catalysts

📅 Upcoming (High Impact)

FDA PDUFA Decision (Expected Q2-Q3 2026)1

- BLA submitted November 7, 2025 through Accelerated Approval pathway

- Atacicept would be first dual BAFF/APRIL inhibitor for IgA nephropathy

- Standard review timeline: 10 months (Priority) or 12 months (Standard)

- Expected decision: Mid-2026

- 12 years biologic market exclusivity if approved

J.P. Morgan Healthcare Conference (January 2026)2

- Expected management presentation

- Could provide FDA review timeline updates

- Key institutional investor event

Q4 2025 Earnings Report (Expected February 2026)3

- Cash position update post-$261M offering

- Commercial preparation progress

- PIONEER trial enrollment data

PIONEER Phase 2 Basket Trial Updates (Throughout 2026)4

- Expanded IgAN populations plus new indications

- Combined peak prevalence: ~230,000 patients in U.S.

- Additional autoimmune kidney diseases (pMN, FSGS, MCD)

✅ Past (Already Happened)

Phase 3 ORIGIN Trial Results (November 6, 2025)5

- 46% reduction in proteinuria (primary endpoint met)

- 42% placebo-adjusted reduction (p<0.0001)

- Published in New England Journal of Medicine

- Stock surged +82% on announcement

BLA Submission to FDA (November 7, 2025)6

- Submitted day after trial results announced

- Through Accelerated Approval Program

- Atacicept holds FDA Breakthrough Therapy Designation

$261 Million Capital Raise (December 8-11, 2025)7

- Upsized from initially planned $200M

- Priced at $42.50 per share

- Provides runway through approval and U.S. commercial launch

- Stock absorbed dilution well, continued rallying to $50s

Analyst Upgrades (December 2025)8

- Goldman Sachs raised target to $95 (Buy)

- JPMorgan target $96 (Overweight)

- Bank of America target $66 (Buy)

- Average target: $68.88 (+35% upside)

Competitive Approval (November 25, 2025)9

- Otsuka's Voyxact (sibeprenlimab) received FDA approval

- First APRIL inhibitor approved for IgAN

- 6-9 month head start over atacicept

- Increases competitive pressure but validates market

🎲 Price Targets & Probabilities

Based on gamma levels, implied move data, and catalyst calendar:

🚀 Bull Case (40% Probability): $60-$65 by March 2026

Key Drivers:

- Positive FDA review signals or Priority Review designation

- Strong analyst momentum (Goldman $95 target, JPMorgan $96)

- Gamma resistance at $60 gets broken on volume

- PIONEER trial shows atacicept efficacy in additional indications

- J.P. Morgan presentation exceeds expectations

Technical Path:

- Break through $55 gamma resistance (9.96% above current)

- Test $60 level (19.95% above current)

- Fits within quarterly implied move upper range of $61.56

What Could Go Right: The FDA grants Priority Review (6-month timeline vs 10-month standard), pulling forward the approval decision to Q1 2026. This would give VERA comparable timing to Voyxact and reduce competitive risk. Shares gap to $58-$60 on the news, then grind toward Goldman's $95 target.

⚖️ Base Case (40% Probability): $45-$52 Range Through March 2026

Key Drivers:

- Standard FDA review process with no major updates

- Profit-taking continues near all-time highs (like today's flow)

- Competition from Otsuka's Voyxact creates market share concerns

- Biotech sector consolidation/rotation

- Stock oscillates within gamma bounds

Technical Path:

- $50 gamma support holds on dips

- $45 becomes major support if selling accelerates

- Trading range aligns with monthly implied move ($45.80-$55.48)

What's Most Likely: VERA consolidates recent gains as institutional investors wait for concrete FDA updates. The stock remains range-bound between $45-$55 through Q1 2026, with volatility spikes around earnings and conferences. Professional traders—like whoever sold $6.5M today—continue taking profits while maintaining some exposure.

😰 Bear Case (20% Probability): $35-$40 by March 2026

Key Drivers:

- FDA issues Complete Response Letter or requests additional data

- Vertex's povetacicept shows superior Phase 3 data (~60% vs 42% reduction)10

- Voyxact captures significant market share, limiting atacicept opportunity

- Broad biotech selloff from macro headwinds

- Insider selling accelerates

Technical Path:

- Break below $45 secondary support

- Fill gap from November 6 surge back to $40 area

- Aligns with quarterly implied move lower range of $39.72

What Could Go Wrong: The FDA requests additional safety data or a larger confirmatory trial before accelerated approval. Combined with strong sales uptake for Voyxact and competitive data from Vertex, the investment thesis deteriorates. VERA gaps down 15-20% on the news and retraces to the $35-$40 range.

💡 Trading Ideas

🛡️ Conservative: Cash-Secured Put at $45 Strike (January 2026)

Strategy: Sell VERA January 16, 2026 $45 Puts Mechanics:

- Collect ~$2.00-$2.50 premium per share ($200-$250 per contract)

- Requires $4,500 cash collateral per contract

- Effective cost basis if assigned: $42.50-$43.00

Why This Works:

- $45 is major gamma support AND matches today's institutional call sale strike

- 10% cushion below current $50.70 price

- If assigned, you're buying VERA at levels where smart money was comfortable holding calls

- Worst case: you own a pre-FDA biotech at $43 with Goldman Sachs $95 target

Max Gain: Premium collected (5.3% return in 16 days) Max Risk: $4,500 - premium if stock goes to zero Probability of Profit: ~65% (based on implied volatility)

Who This Is For: Investors who want VERA exposure but prefer to buy on dips, or income seekers willing to hold long-term if assigned.

⚖️ Balanced: Bull Put Spread $45/$40 (February 2026)

Strategy: Sell VERA February 20, 2026 $45 Put / Buy $40 Put Mechanics:

- Sell $45 put, buy $40 put = Net credit ~$1.75-$2.25

- Max loss: $500 - credit received = ~$275-$325 per spread

- Max gain: Credit received = ~$175-$225 per spread

Why This Works:

- Defined risk structure perfect for biotech volatility

- Profit zone: anywhere above $43 at expiration (15% downside cushion)

- 50 days to expiration captures any J.P. Morgan conference catalyst

- Limits losses if bear case plays out and stock breaks $45

Max Gain: $175-$225 per spread (60-70% ROI) Max Risk: $275-$325 per spread Breakeven: ~$43.00 Probability of Profit: ~55%

Who This Is For: Traders who are bullish but respect the volatility, want limited downside exposure, and believe VERA holds above $43 through February.

🚀 Aggressive: Debit Call Spread $52.50/$60 (March 2026)

Strategy: Buy VERA March 20, 2026 $52.50 Call / Sell $60 Call Mechanics:

- Buy $52.50 call, sell $60 call = Net debit ~$3.00-$3.50

- Max profit: $7.50 spread - debit = ~$4.00-$4.50 per spread

- Max loss: Debit paid = ~$3.00-$3.50 per spread

Why This Works:

- Targets the bull case range ($60-$65) with limited capital

- March expiration captures potential FDA Priority Review designation

- $60 is major gamma resistance—breakthrough could trigger squeeze

- 79-day timeframe aligns with quarterly implied move of 21.57%

- Risk/reward: ~120-150% upside vs 100% downside on defined capital

Max Gain: $400-$450 per spread (120-150% ROI) Max Risk: $300-$350 per spread Breakeven: ~$55.50-$56.00 Probability of Profit: ~35%

Who This Is For: Bullish traders betting on positive FDA signals, willing to risk defined capital for leveraged upside toward analyst targets.

Alternative Aggressive Play: Straight shares with 10% stop loss at $45.50. If analyst targets are right ($68-$95), upside is 34-87% with clearly defined risk.

⚠️ Risk Factors

🏛️ Regulatory Risks

- FDA rejection or delay: BLA through Accelerated Approval means confirmatory trials still required. Complete Response Letter would be devastating11

- Labeling restrictions: Approval may limit patient population or require restrictive REMS program

- Timeline uncertainty: No guarantee of Priority Review; standard 12-month timeline extends to Q4 2026

🥊 Competition Risks

- Already behind: Otsuka's Voyxact approved November 2025 with 6-9 month head start and 51% proteinuria reduction vs atacicept's 42%12

- Better data incoming: Vertex's povetacicept showed ~60% reduction in Phase 2, Phase 3 data expected 202613

- Market fragmentation: Novartis (2 drugs), Travere, Calliditas all competing in $500M market

- Pricing pressure: Payers may resist premium pricing with multiple approved alternatives

💼 Execution Risks

- No commercial experience: VERA is pre-revenue biotech competing against Big Pharma distribution

- Sales force buildout: Must hire, train specialized nephrology reps while burning cash

- Market access challenges: Insurance reimbursement negotiations difficult with competitors

- Manufacturing scale-up: Biologic production complexity and supply chain risk

💰 Financial Risks

- Dilution: December offering added ~10% shares; may need more capital if approval delayed14

- Cash burn: Q3 burn rate ~$57M/quarter will accelerate with commercial prep

- No revenue backstop: Pure binary bet on FDA with no other cash flow

📉 Technical Risks

- Overbought: 110%+ rally in 2 months, trading near all-time highs

- Today's flow: $6.5M institutional call selling suggests smart money reducing exposure

- Gap risk: November 6 gap from $30s to $44 remains unfilled below

🌊 Macro Risks

- Biotech sector pressure: Higher interest rates make pre-revenue biotechs less attractive

- IRA drug pricing: Political risk around pharmaceutical pricing reform

- Market rotation: Small-cap biotech underperforms in risk-off environments

🎯 The Bottom Line

Real talk: Today's $6.5M call sale is a classic case of smart money taking profits after an incredible run, NOT a bearish bet against VERA's future. When you're sitting on 100%+ gains and the stock is trading at all-time highs, locking in wins makes total sense—especially with binary FDA risk ahead.

Here's the deal:

If you OWN it: Don't panic. This wasn't bearish put buying or a big short—this was profit-taking. The catalysts remain intact: FDA decision mid-2026, strong Phase 3 data published in NEJM, $750M cash to fund commercialization, and analyst targets 35-87% above current levels. Consider trimming 20-30% if you're up big, or hold through the FDA decision if you can handle volatility. Set stops at $45 (gamma support).

If you're WATCHING it: VERA isn't a buy-the-dip opportunity at $50.70 near all-time highs with major resistance at $55. Wait for either (a) pullback to $45-$47 support zone, or (b) breakout above $55 on increasing volume with FDA catalyst. The risk/reward is better on weakness or confirmation.

If you're BEARISH: The bull case remains strong with multiple positive catalysts, institutional ownership over 100%, and limited competition approved ahead of mid-2026 timeline. Shorting here is dangerous. If you must, use defined-risk bear put spreads rather than naked shorts.

Mark your calendar for:

- January 2026: J.P. Morgan Healthcare Conference (potential FDA timeline updates)

- February 2026: Q4 earnings (cash position, commercial prep updates)

- Mid-2026: FDA PDUFA decision (binary event)

The options market is pricing in WILD moves ahead—9.57% by mid-January, 21.57% by March, 81.6% by year-end 2026. That's not gentle consolidation territory; that's make-or-break biotech volatility. Trade accordingly.

Bottom line: VERA is a high-quality biotech with legitimate commercial potential trading at stretched valuations after a massive rally. Professional traders are taking some risk off (today's flow), but the setup remains bullish into the FDA decision. Just don't chase it at all-time highs. 💊

⚠️ Disclaimer: Options trading involves substantial risk and is not suitable for all investors. This analysis is for educational purposes only and does not constitute investment advice. The biotech sector and FDA approval processes are inherently risky. Past performance does not guarantee future results. Always conduct your own due diligence and consult with a financial advisor before making investment decisions.