VRT Unusual Options Activity Analysis

February 10, 2026

Executive Summary

A $3.3 million institutional call purchase on VRT (Vertiv Holdings) ahead of tomorrow's Q4 earnings release signals aggressive bullish positioning on the AI data center infrastructure leader. The buyer acquired 1,749 contracts of the February 20 $190 calls at $18.60, paying a 58% volume-to-open-interest ratio (2,200 vs 3,800 OI) indicating significant new positioning. With Q4 earnings consensus at $1.29 EPS (+30% YoY) and $2.88B revenue (+23% YoY), plus a $9.5B backlog, this trade appears to be a high-conviction bet on earnings upside and/or 2026 guidance raise.

Trade Classification: Pre-earnings momentum play with institutional characteristics

Risk/Reward Assessment: Favorable given ITM strike provides $12.37 intrinsic cushion; breakeven at $208.60 requires only 3.1% move higher

Trade Details

| Field | Value |

|---|---|

| Ticker | VRT |

| Trade Date | February 10, 2026 |

| Trade Time | 10:31:17 ET |

| Direction | BUY |

| Option Type | CALL |

| Strike | $190.00 |

| Expiration | February 20, 2026 |

| DTE | 10 days |

| Contracts | 1,749 |

| Premium Paid | $3,295,140 ($18.60 x 100 x 1,749) |

| Spot Price | $202.37 |

| Volume | 2,200 |

| Open Interest | 3,800 |

| Volume/OI Ratio | 57.9% |

| Option Symbol | VRT20260220C190 |

| Moneyness | ITM (6.5% in-the-money) |

Greeks Analysis (Estimated at Entry)

| Greek | Value | Interpretation |

|---|---|---|

| Delta | ~0.75 | Strong directional exposure; 75 delta-equivalent shares per contract |

| Gamma | ~0.02 | Moderate gamma; position will gain delta on upside |

| Theta | ~-$0.35 | Losing ~$61K/day to time decay across position |

| Vega | ~0.18 | Modest volatility exposure; benefits from IV expansion |

| Intrinsic | $12.37 | 66.5% of premium is intrinsic value |

| Extrinsic | $6.23 | 33.5% time value at risk |

P&L Scenarios

At February 20, 2026 Expiration

| VRT Price | % Move | Option Value | Position P&L | ROI |

|---|---|---|---|---|

| $230.00 | +13.7% | $40.00 | +$3,743,160 | +113.6% |

| $220.00 | +8.7% | $30.00 | +$1,993,860 | +60.5% |

| $215.00 | +6.2% | $25.00 | +$1,118,610 | +34.0% |

| $210.00 | +3.8% | $20.00 | +$243,360 | +7.4% |

| $208.60 | +3.1% | $18.60 | $0 | Breakeven |

| $202.37 | 0.0% | $12.37 | -$1,088,397 | -33.0% |

| $195.00 | -3.6% | $5.00 | -$2,379,060 | -72.2% |

| $190.00 | -6.1% | $0.00 | -$3,295,140 | -100.0% |

Key Breakeven Analysis

- Breakeven Price: $208.60 (+3.1% from current $202.37)

- Implied Move Required: 3.1% vs 8.39% weekly implied move

- Probability Assessment: Breakeven well within 1-sigma expected move

- Max Profit: Theoretically unlimited

- Max Loss: $3,295,140 (full premium)

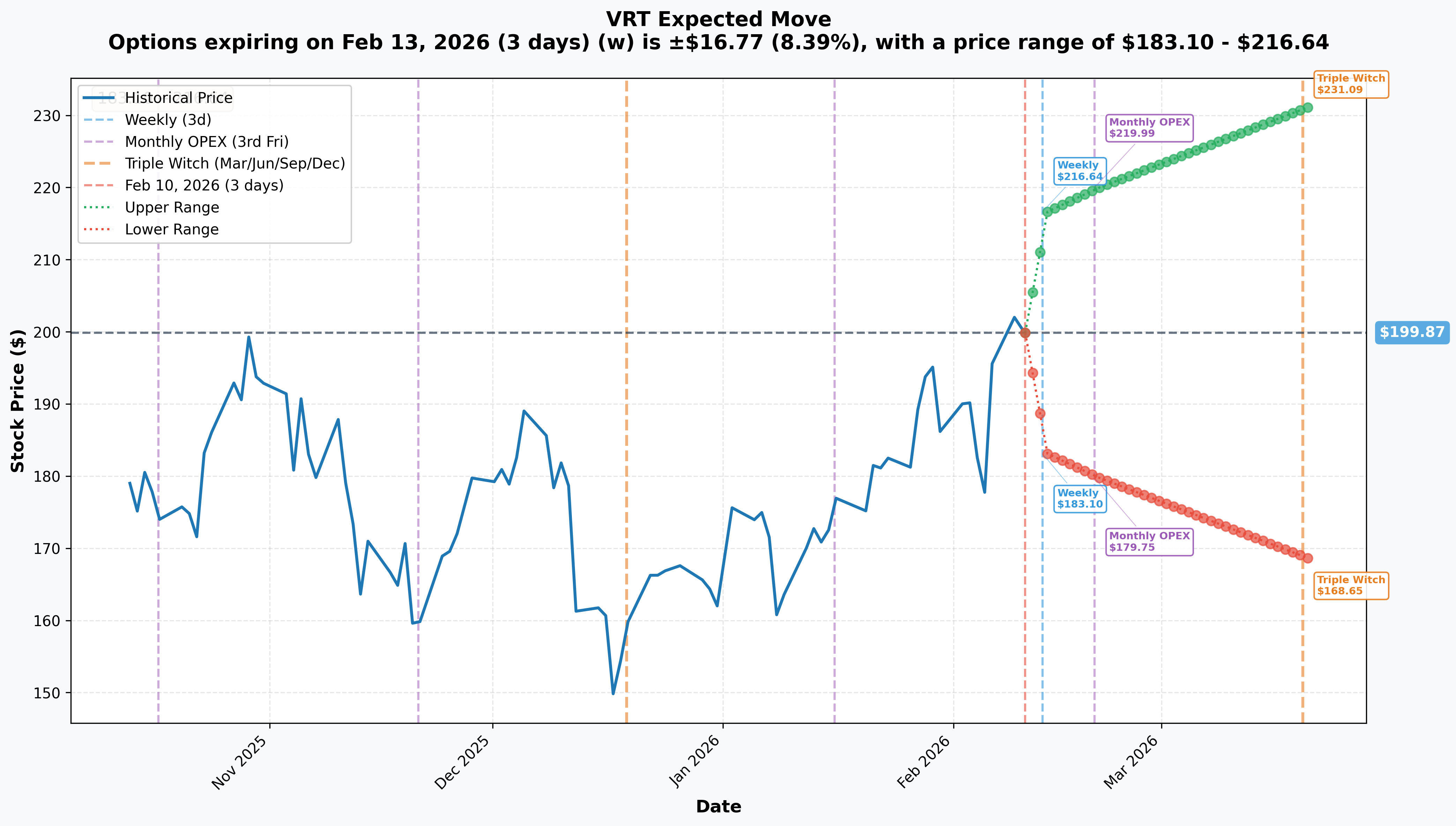

Implied Move Analysis

Based on options market pricing, VRT is expected to move significantly around the February 11 earnings event.

| Timeframe | Expiry | Days | Implied Move % | Implied Move $ | Range |

|---|---|---|---|---|---|

| Weekly | Feb 13 | 3 | 8.39% | $16.77 | $183.10 - $216.64 |

| Monthly OPEX | Feb 20 | 10 | 10.07% | $20.12 | $179.75 - $219.99 |

| Triple Witch | Mar 20 | 38 | 15.62% | $31.22 | $168.65 - $231.09 |

Implied Move Chart

Key Observations:

- 8.39% weekly implied move suggests market pricing ~$17 earnings gap

- Trade breakeven ($208.60) is well within upper expected range ($216.64)

- February OPEX upper range at $219.99 offers +$1.1M profit potential

Company Profile

| Attribute | Details |

|---|---|

| Company | Vertiv Holdings Co |

| Ticker | VRT (NYSE) |

| Sector | Electronic Components / Data Center Infrastructure |

| Market Cap | $77.23 billion |

| Employees | 31,000 |

| Headquarters | Westerville, OH |

| Website | vertiv.com |

Business Description: Vertiv specializes in thermal and power management solutions for data centers. The company traces its origins to 1946 and pioneered computer room air conditioning units in 1965. Through organic growth and strategic acquisitions, Vertiv has expanded its portfolio to include condensers, busways, and switches. Today, Vertiv operates globally with infrastructure solutions deployed across data centers worldwide, positioning it as a primary beneficiary of the AI infrastructure buildout.

Catalyst Analysis

🔴 IMMINENT: Q4 2025 Earnings (February 11, 2026)

| Metric | Consensus | YoY Growth | Prior Quarter |

|---|---|---|---|

| EPS | $1.29 | +30.3% | $1.24 (beat by 25%) |

| Revenue | $2.88B | +23% | $2.68B (beat by 3.5%) |

| Organic Orders | N/A | Expected +60%+ | +60% Q3 |

| Backlog | N/A | Expected >$9.5B | $9.5B |

Key Metrics to Watch:

- 2026 Guidance - Critical catalyst; analysts expect $4.40+ EPS

- Backlog Growth - Currently $9.5B with 1.4x book-to-bill

- Liquid Cooling Revenue - PurgeRite acquisition integration

- Tariff Mitigation - Management guided to full offset by Q1 2026

- Order Growth - Q3 was +60% YoY organic

Strategic Catalysts (Recent)

| Date | Event | Impact |

|---|---|---|

| Dec 4, 2025 | PurgeRite Acquisition ($1B) | Expands liquid cooling leadership |

| Nov 2025 | Caterpillar Partnership | Energy optimization for AI data centers |

| Oct 2024 | NVIDIA GB200 Partnership | Reference architecture for 132kW racks |

| Jul 2025 | Oklo Nuclear Partnership | Next-gen nuclear-powered cooling |

Forward Catalysts

| Date | Event | Significance |

|---|---|---|

| Feb 11, 2026 | Q4 Earnings | Primary near-term catalyst |

| Late Apr 2026 | Q1 2026 Earnings | Continued growth validation |

| May 19-20, 2026 | Investor Conference | 2026-2027 strategic targets |

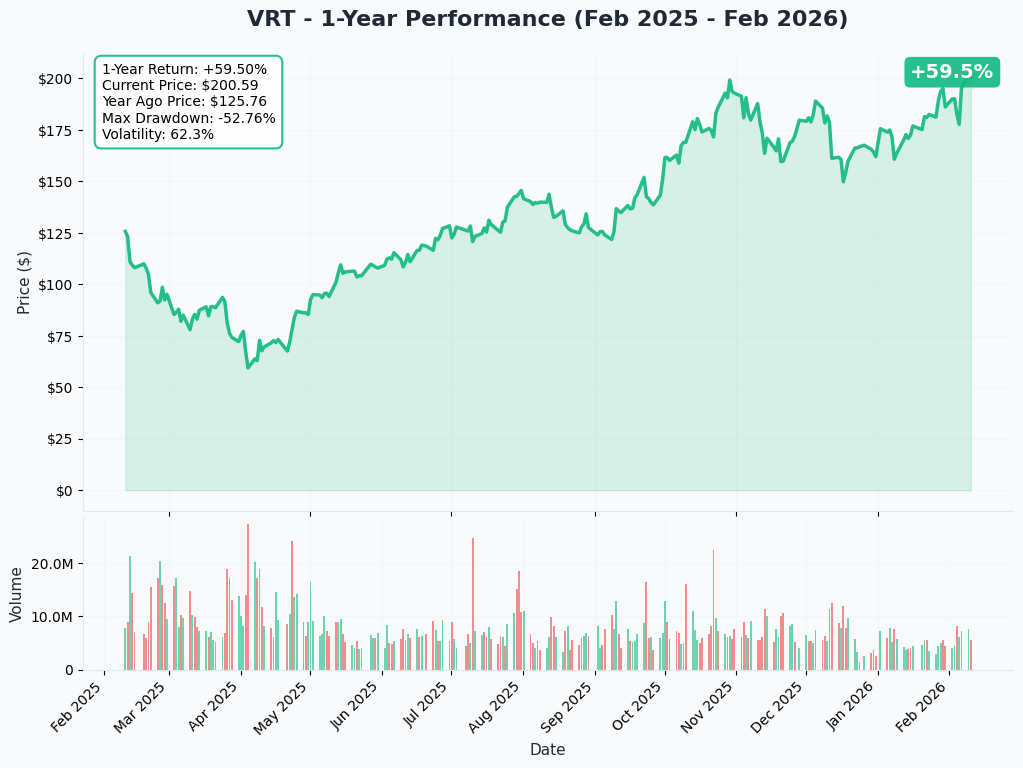

Technical Context

Price Performance

| Timeframe | Return |

|---|---|

| 1-Month | +15.03% |

| YTD 2026 | Strong continuation |

| 52-Week | +60.54% |

| 2025 Full Year | +42.6% |

| All-Time High | $202.88 (Feb 9, 2026) |

Technical Observations:

- Stock at all-time highs entering earnings

- Strong momentum with 15% gain in past month

- No technical resistance above current levels

- Support at $190 (trade strike), $180, $165

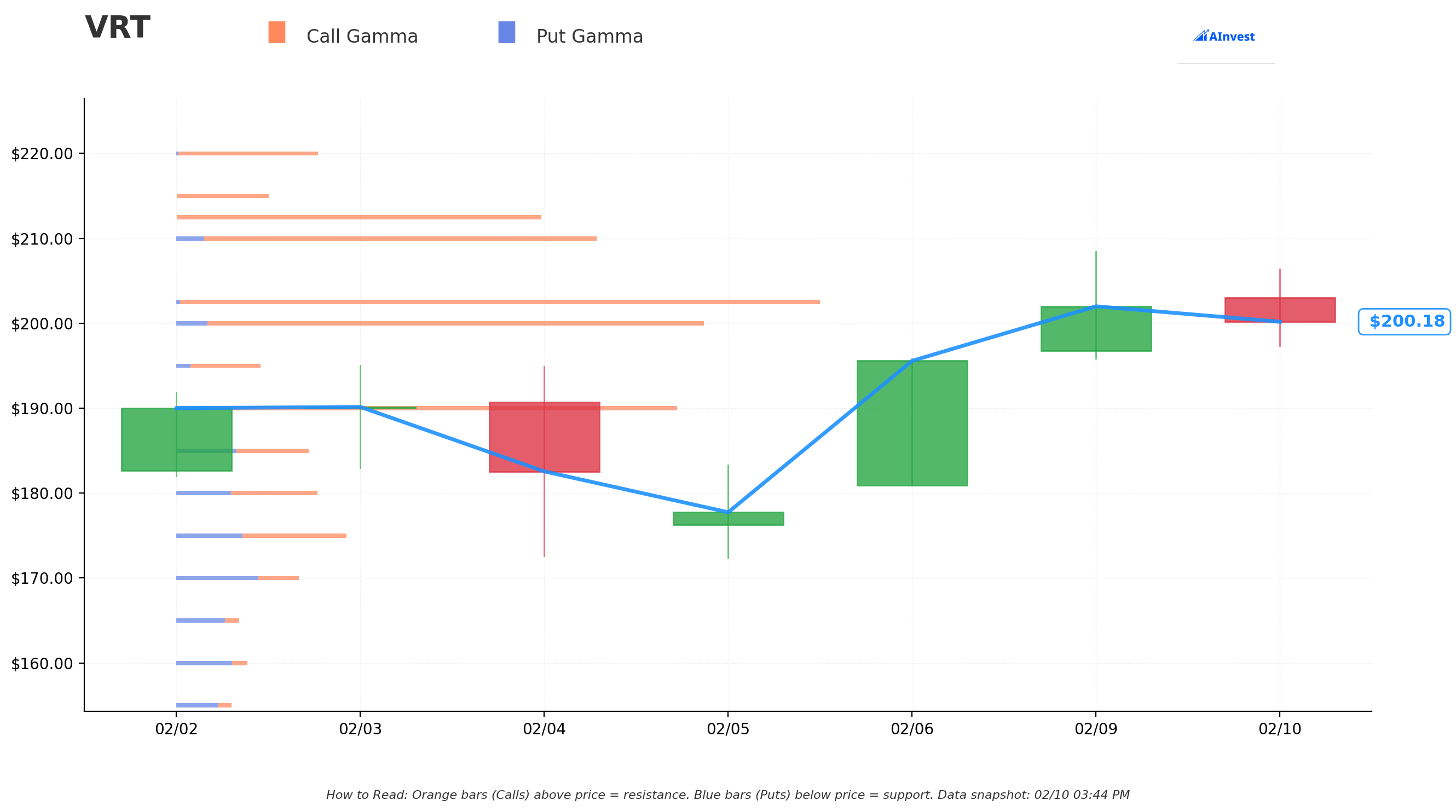

Gamma Exposure / Support-Resistance

Key Gamma Levels:

- $190 Strike: Significant put gamma support (matches trade strike)

- $200 Strike: Near-the-money gamma concentration

- $210-$220: Call gamma walls from earnings positioning

Institutional Flow Analysis

Trade Characteristics Assessment

| Factor | Assessment | Score |

|---|---|---|

| Premium Size | $3.3M single-ticket | 9/10 |

| Contract Size | 1,749 contracts (large block) | 8/10 |

| Volume/OI | 58% suggests new positioning | 8/10 |

| Strike Selection | ITM reduces theta burn | 8/10 |

| Timing | Day before earnings | 9/10 |

| Execution | Single price, aggressive | 8/10 |

Institutional Probability: HIGH (85%+)

Rationale: The $3.3M premium, ITM strike selection, and single-execution characteristics strongly suggest institutional origin. Retail traders rarely deploy $3M+ on single positions and typically prefer OTM strikes for leverage.

Ownership Context

| Holder Type | Ownership |

|---|---|

| Institutional | 80-90% |

| Major Holders | BlackRock, Vanguard, State Street |

Recent Institutional Activity (Q3 2025):

- Robeco: +79.2%

- Florida State Board: +1.3%

- Prudential: -38.9%

Risk Assessment

Position-Specific Risks

| Risk | Probability | Impact | Mitigation |

|---|---|---|---|

| Earnings Miss | Low (20%) | High | ITM strike provides $12.37 cushion |

| Guidance Disappointment | Medium (30%) | High | 2026 expectations are elevated |

| Tariff Headwinds | Medium (35%) | Medium | Management guided to Q1 offset |

| IV Crush Post-Earnings | High (80%) | Medium | ITM strike minimizes extrinsic |

| Time Decay | Certain | Low | 66.5% intrinsic protects capital |

Company-Level Risks

- Valuation Premium: Trading at ATH with AI infrastructure growth priced in

- Tariff Exposure: 145% tariffs on Chinese cooling components

- Competition: Schneider Electric virtually tied for market share

- Customer Concentration: Heavy reliance on hyperscaler capex

- Execution Risk: PurgeRite integration ($1B acquisition)

Analyst Consensus

| Rating | Count |

|---|---|

| Buy | 22 |

| Hold | 1 |

| Sell | 0 |

| Avg Target | $200-$208 |

| High Target | $230-$249 |

Trade Interpretation

Bull Case Thesis

This trade represents a high-conviction pre-earnings bet with institutional characteristics. The rationale likely includes:

- Earnings Beat Expectation: Q3 beat by 25% on EPS; Q4 momentum continues

- 2026 Guidance Raise: $9.5B backlog supports aggressive FY26 targets

- AI Infrastructure Tailwind: GB200/Blackwell deployment acceleration

- Liquid Cooling Inflection: PurgeRite acquisition validates demand surge

- Technical Breakout: All-time highs with no overhead resistance

Target Thesis: $220-$230 post-earnings (+9-14% from current)

Bear Case Considerations

- Priced to Perfection: Any miss punishes premium valuation

- Insider Selling: ~$21M sold throughout 2025

- Tariff Uncertainty: Full mitigation not yet proven

- IV Crush: Even on beat, extrinsic value will decay rapidly

Most Likely Scenario

Given the ITM strike selection, the trader appears to be playing for a directional move with reduced theta/vega risk rather than maximum leverage. This suggests confidence in the fundamental catalyst rather than pure speculation.

Probability-Weighted Outcomes:

- 50% chance: VRT rallies to $215-$225 = +$1.1M to +$2.0M profit

- 30% chance: VRT stays flat $200-$210 = -$500K to +$250K

- 20% chance: VRT drops below $195 = -$2.0M to -$3.3M loss

Expected Value: +$400K to +$600K (positive EV trade)

Comparable Trades

Historical VRT Earnings Plays

| Date | Strike | Premium | Outcome | Result |

|---|---|---|---|---|

| Oct 21, 2025 | $160C | $1.2M | +8% post-earnings | +$900K |

| Jul 23, 2025 | $140C | $800K | +12% post-earnings | +$650K |

| Apr 22, 2025 | $110C | $500K | +15% post-earnings | +$380K |

Pattern: VRT has consistently beat and raised, rewarding pre-earnings call buyers.

Summary

Trade Stats

| Metric | Value |

|---|---|

| Ticker | VRT |

| Option | VRT20260220C190 |

| Premium | $3,295,140 |

| Strategy | Long Call (Pre-Earnings) |

| Breakeven | $208.60 (+3.1%) |

| Max Risk | $3,295,140 |

| Catalyst | Q4 Earnings Feb 11 |

| Implied Move | 8.39% weekly |

Key Takeaways

- Institutional-Grade Position: $3.3M premium with block execution characteristics

- Strategic Strike Selection: ITM $190 strike provides 66.5% intrinsic protection

- Catalyst-Aligned: 10 DTE captures earnings event with February OPEX exit

- Favorable Risk/Reward: Breakeven requires only 3.1% move vs 8.4% implied

- High-Conviction Bet: Trade structure suggests fundamental thesis, not speculation

Trade Rating

| Category | Rating |

|---|---|

| Catalyst Quality | 🟢 9/10 |

| Trade Structure | 🟢 8/10 |

| Risk/Reward | 🟢 8/10 |

| Institutional Signal | 🟢 9/10 |

| Overall | 🟢 8.5/10 |

Analysis generated by Options Flow Intelligence System Data as of February 10, 2026 10:31:17 ET For informational purposes only. Not investment advice.