🛰️ VSAT - $3M Bullish Call Bet Ahead of Earnings and Satellite Service Launch!

📅 January 27, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $3 MILLION on VSAT calls across two trades fired off one second apart - 3,600 contracts each at the $42 and $48 strikes, both expiring February 20th. This is a concentrated bullish bet on a company sitting on a pile of catalysts: Q3 earnings in ~2 weeks, ViaSat-3 F2 satellite entering service, and a potential defense division spin-off that activists say could be worth $50+/share alone. Translation: Big money is loading up before a potential breakout.

📊 Company Overview

Viasat Inc (VSAT) is a global satellite communications company providing broadband, defense, and aviation connectivity services:

- 💰 Market Cap: ~$5.8 Billion

- 🏢 Sector: Communications Services (Satellite)

- 📍 Headquarters: Carlsbad, California

- 👥 Employees: ~7,000

- 📈 Current Price: $44.63

- 🔑 Primary Business: Satellite broadband (aviation, maritime, residential), defense encryption/tactical comms, government satellite networks. Combined Viasat/Inmarsat fleet makes them one of the largest satellite operators globally.

💰 The Option Flow Breakdown

📊 The Tape (January 27, 2026)

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:58:14 | VSAT | MID | BUY | CALL $42 | 2026-02-20 | $2M | $42 | 4,000 | 4,100 | 3,600 | $44.63 | $5.62 | VSAT20260220C42 |

| 11:58:15 | VSAT | MID | BUY | CALL $48 | 2026-02-20 | $1M | $48 | 4,000 | 73 | 3,600 | $44.63 | $2.87 | VSAT20260220C48 |

🤓 What This Actually Means

These two trades hit the tape one second apart with identical size (3,600 contracts each). Here's the breakdown:

- 💸 Combined premium: $3M ($2M on the $42 calls + $1M on the $48 calls)

- 📍 Leg 1 - $42 Strike: In-the-money by $2.63 (stock at $44.63). This gives immediate delta exposure - basically a leveraged stock position with built-in downside protection below $42

- 📍 Leg 2 - $48 Strike: Out-of-the-money by $3.37 (7.5% above current price). This is the pure upside lottery ticket

- ⏰ Expiration: February 20th - just 24 days away, capturing Q3 earnings (~February 5-10)

- 📊 Volume vs Open Interest: The $48 strike had only 73 contracts of open interest before this trade. 3,600 contracts blowing through that is a Vol/OI ratio of 54.8x - extremely aggressive positioning

Why two separate calls instead of a spread?

Both legs are BUYS (BTO - Buy to Open), which means this is NOT a vertical spread. This trader is buying calls at two different strikes - essentially a double-barreled bullish bet. The ITM $42 calls provide safer exposure with higher delta (~0.70), while the OTM $48 calls offer explosive leverage if VSAT rips above $48. Think of it as having both a "base hit" and a "home run" ticket on the same play.

Unusual Score: 🔥 EXTREME

- $42 Call: Z-Score of 7.14 - roughly a few times per year unusual. This is significant activity for a $5.8B mid-cap

- $48 Call: Z-Score of 429.35 - this strike had essentially zero activity before today. The volume is 55x the prior open interest. You almost never see this kind of ratio on a single name

This isn't your neighbor's Robinhood account. Dropping $3M on short-dated calls in a mid-cap satellite stock with earnings coming up screams institutional conviction.

📈 Technical Setup / Chart Check-Up

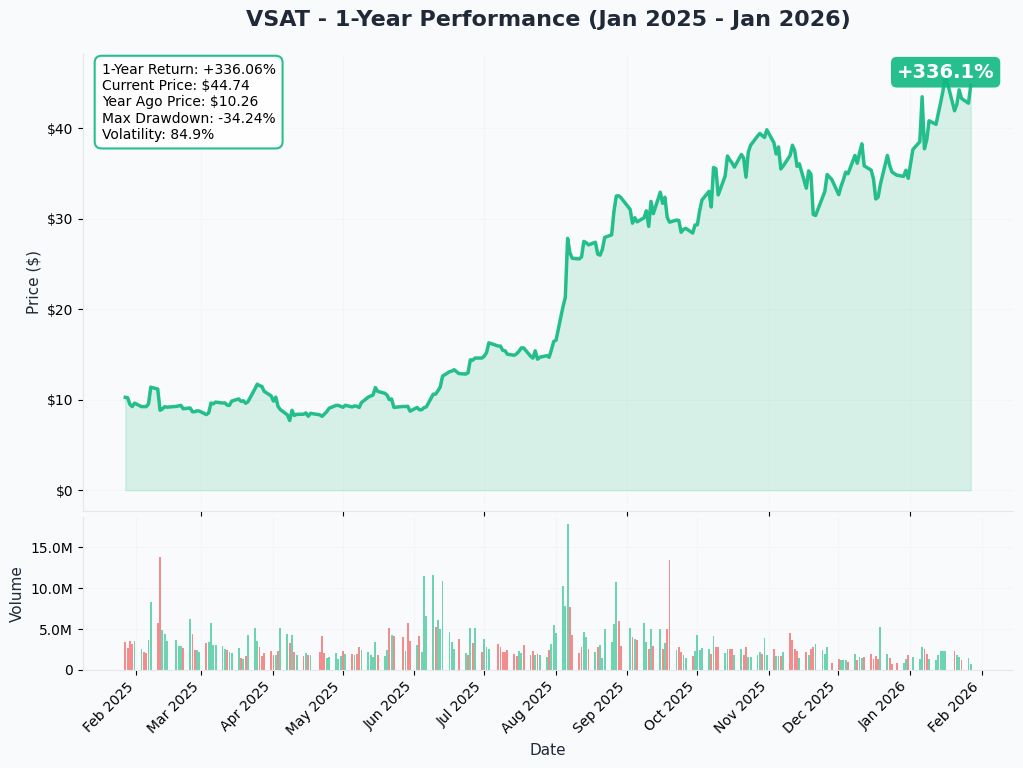

1-Year Performance Chart

VSAT has been on a steady climb. The stock is up roughly +22% YTD through mid-January, hitting a new 52-week high of $45.93 on January 16 after Morgan Stanley raised their price target 325% to $51. Over the past year, VSAT has surged approximately 330% from its 52-week low of $7.36 - a remarkable turnaround story driven by satellite launches, defense contracts, and the Inmarsat integration.

Key observations:

- 📈 Strong uptrend: Steady climb from single digits to mid-$40s over the past 12 months

- 🎯 Near 52-week highs: Current price of $44.63 is within striking distance of the $45.93 high

- 🔥 Momentum: January rally fueled by Morgan Stanley PT raise and Innospace partnership

- ⚠️ Extended move: After a 330% one-year rally, some consolidation would be healthy

🔍 Gamma-Based Support & Resistance Analysis

Current Price: $44.63

The gamma exposure map shows where options market makers have the heaviest positioning, creating natural price magnets and barriers:

🔵 Support Levels (Below Current Price):

- 🛡️ $43 - Immediate support (3.7% below) with moderate gamma. First line of defense on any dip

- 🛡️ $42 - Strong support (5.9% below) with 0.84 total gamma - this is a major floor. Notice this is EXACTLY where the big call buyer struck. Not a coincidence

- 🛡️ $40 - Secondary support (10.4% below). Below here things get ugly

- 🛡️ $37 - Deep support with 1.93 total gamma - the STRONGEST gamma level on the board. If VSAT somehow crashes, $37 is where the cavalry arrives

🟠 Resistance Levels (Above Current Price):

- 🚧 $45 - Immediate resistance (0.8% above!) with 0.39 total gamma. This is the first ceiling to crack - barely above current price

- 🚧 $46 - Secondary resistance (3.1% above). Breakout above here opens up room

- 🚧 $50 - Major resistance (12% above) with 0.46 total gamma. This is where the big money call buyer would be sitting pretty on both legs

What this means for traders: VSAT is currently pressed against $45 resistance with solid $42-$43 support below. The gamma profile is net bullish (total call gamma of 4.73 vs put gamma of 1.31) - meaning market makers are positioned in a way that tends to amplify upside moves and cushion dips. The $42 strike where the big call buyer entered has massive gamma, creating a strong floor that dealers will defend.

Net GEX Bias: Bullish - Call gamma dominates, suggesting upside moves could accelerate if $45 breaks.

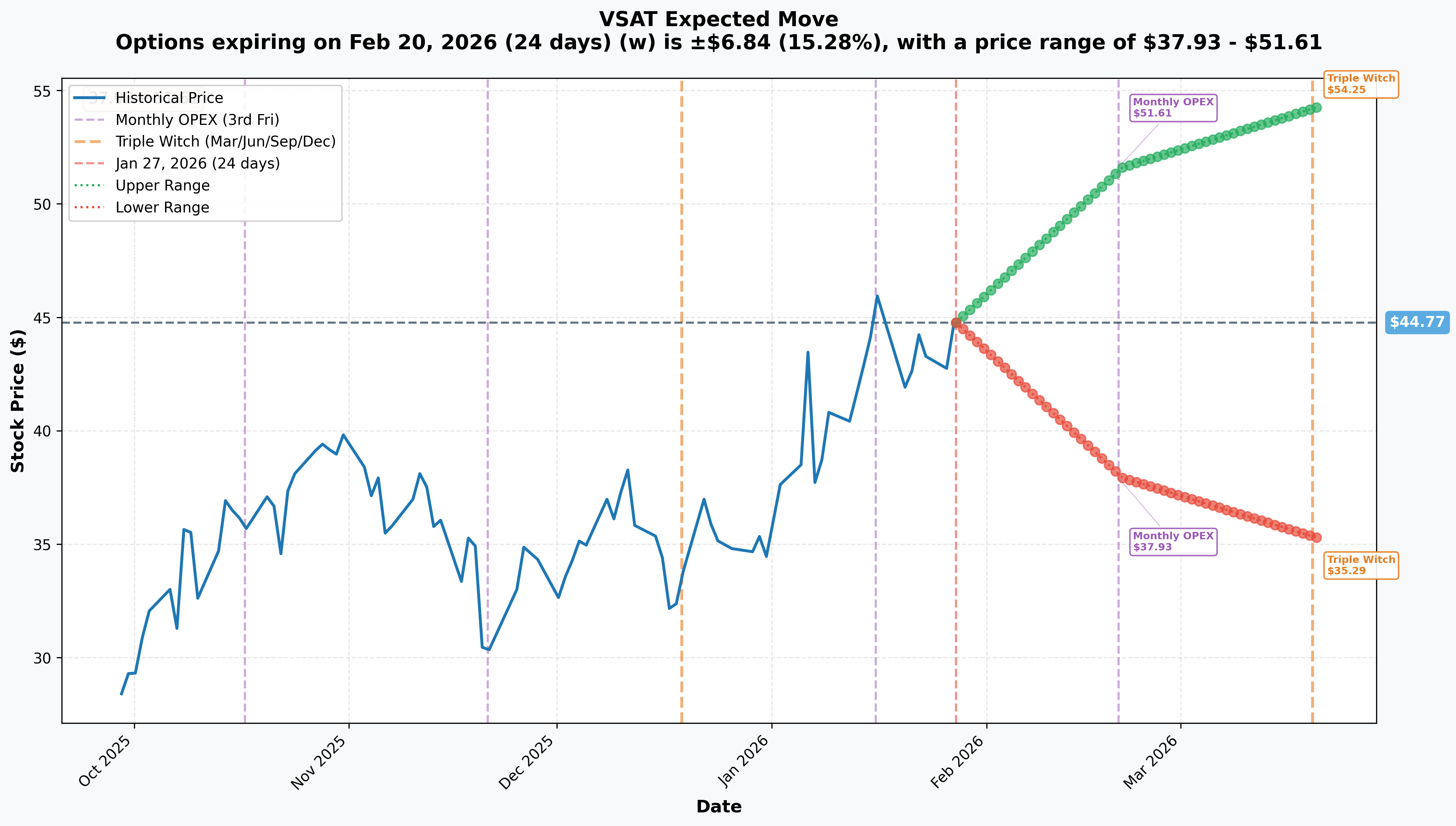

📊 Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX (Feb 20 - 24 days - THIS TRADE!): +/-15.3% ($6.84) -> Range: $37.93 - $51.61

- 📅 Quarterly Triple Witch (Mar 20 - 52 days): +/-21.2% ($9.48) -> Range: $35.29 - $54.25

Translation for regular folks: The options market is pricing in a 15% move by February 20th - that's the expiration of our mystery buyer's calls. The upper range of $51.61 would put both call legs deep in the money. The lower range of $37.93 would mean the entire $3M bet goes to zero.

The wide implied move makes sense - Q3 FY2026 earnings are estimated for February 5-10, and this is a $5.8B company that just launched a satellite designed to double its network capacity. There's genuine uncertainty about how much of the good news is already priced in after a 330% rally.

Key insight: The $48 call strike sits comfortably within the implied upper range ($51.61), meaning the market considers a move to $48+ as a realistic possibility by February 20th. The call buyer isn't reaching for the stars - they're playing within the expected range.

🎪 Catalysts

🔥 Upcoming Catalysts (What Could Move the Stock)

Q3 FY2026 Earnings (~February 5-10, 2026) 📊

This is THE big one. VSAT reports fiscal Q3 results in roughly two weeks, right before the call buyer's February 20th expiration:

- 📊 Consensus EPS: -$0.46 (range: -$0.47 to -$0.45)

- 👀 Key metrics to watch: ViaSat-3 F2 deployment progress, free cash flow generation, defense backlog growth, debt reduction trajectory

- 🔥 Wild card: Any commentary on the DAT spin-off evaluation could send the stock flying

ViaSat-3 F2 Service Entry (Early 2026) 🛰️

The ViaSat-3 F2 satellite launched successfully in November 2025 and is currently being positioned:

- 🚀 Designed to add 1 Tbps of capacity - more than Viasat's entire existing network combined

- 🌎 Will cover the Americas, allowing F1 to shift to EMEA coverage

- 💰 Revenue impact: Enables higher-bandwidth aviation and maritime services

- ⚠️ Must complete reflector deployments and in-orbit testing first

Ligado $100M Lump Sum Payment (March 31, 2026) 💵

Viasat's comprehensive agreement with Ligado Networks includes a remaining $100M payment plus ~$16M quarterly installment due March 31st. Cash that helps manage the $5.5B debt load.

DAT Division Spin-Off Decision 🏭

This is the sleeper catalyst. Activist investor Carronade Capital (2.6% stake) argues the Defense & Advanced Technologies division alone could be worth $50/share as a standalone company. Viasat has confirmed they are "evaluating a potential separation". J.P. Morgan upgraded VSAT partly based on spin-off potential, and William Blair noted L3Harris's rocket engine spinoff may "inspire" Viasat.

✅ Recent Catalysts (Already Happened)

- 🛰️ ViaSat-3 F2 launched successfully (November 13, 2025) - doubling network capacity

- 💰 $420M Ligado lump sum received (October 2025) - major cash injection

- 🏛️ PTS-G Space Force contract (October 2025) - $4B ceiling IDIQ with initial $37.5M task order

- 📈 Morgan Stanley PT raised 325% (January 16) - from $12 to $51, sum-of-parts valuation

- 🤝 Innospace partnership (January 6) - stock rose 9.09% on the announcement

- 🔐 Ethernet Data Encryptor - selected by U.S. Government, drove 150%+ stock appreciation since late July 2025

- 🏦 Ex-Im Bank $188.7M loan facility (January 27, 2026) - financing for ViaSat-3 F1 satellite costs

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and the catalyst calendar, here are the scenarios through the February 20th expiration:

📈 Bull Case (30% probability)

Target: $48-$52

How we get there:

- 💪 Q3 earnings beat expectations with strong free cash flow and DAT backlog growth

- 🛰️ ViaSat-3 F2 service entry announced on schedule, validating capacity doubling thesis

- 🏭 Management drops hints about DAT spin-off timeline - even vague language sends this flying

- 📈 Breakout above $45 gamma resistance triggers momentum through $46, $47, toward $50

- 🎯 Morgan Stanley's $51 sum-of-parts PT becomes the consensus view

- 📊 Carronade's $50-$100/share separated value estimate gains traction

P&L for the call buyer:

- Stock at $50: $42 calls worth ~$8.00 (+$2.38/contract) + $48 calls worth ~$2.00 (-$0.87/contract) = Combined profit of ~$5.4M

- Stock at $52: Both legs deep ITM = Combined profit of ~$10M+ on a $3M bet

🎯 Base Case (45% probability)

Target: $42-$47 (Range-Bound)

Most likely scenario:

- ✅ Earnings come in roughly in-line (-$0.46 EPS as expected)

- 📊 ViaSat-3 F2 testing progresses but no definitive service entry date announced

- 🤷 No major DAT spin-off update - "still evaluating"

- 📉 Stock consolidates between $42 gamma support and $45-$46 resistance

- 💤 Post-earnings IV crush reduces option premiums significantly

P&L for the call buyer:

- Stock at $44-$45: $42 calls worth $2-$3 (modest loss after theta decay) + $48 calls likely worthless = Net loss of ~$1-1.5M

📉 Bear Case (25% probability)

Target: $37-$42

What could go wrong:

- 😰 Earnings disappoint - revenue misses or ViaSat-3 F2 deployment issues surface

- 🚨 ViaSat-3 F2 encounters anomaly similar to F1's antenna problem - capacity thesis collapses

- 💸 $5.5B net debt concerns resurface if free cash flow disappoints

- 📉 Broader market selloff drags satellite/defense names lower

- 🏷️ CEO selling $11M in shares (Dec-Jan) gets flagged as warning signal

- 🔨 Break below $42 gamma support sends stock toward $37 deep gamma floor

P&L for the call buyer:

- Stock at $40: Both legs expire worthless = Total loss of $3M

💡 Trading Ideas

🛡️ Conservative: Wait for the Earnings Print

Play: Sit on the sidelines until after Q3 earnings (~February 5-10)

Why this works:

- ⏰ Earnings in ~2 weeks creates binary risk with +/-15% implied move - too risky to jump in blind

- 💸 Options are expensive right now due to earnings IV premium

- 📊 After a 330% one-year rally, the easy money has been made. Buying at $44+ requires strong conviction

- 🎯 Post-earnings pullback to $40-$42 would be a much better entry with gamma support underneath

- 🤔 If earnings are great AND you miss the initial pop, you can still enter on a pullback - strong earnings create durable moves

Action plan:

- 👀 Watch earnings report for: FCF generation, ViaSat-3 F2 timeline, DAT spin-off commentary, and debt reduction progress

- 🎯 If stock pulls back to $40-$42 gamma support post-earnings, consider buying shares or April calls

- ✅ If earnings crush it, wait for first pullback and enter with tight stop below $42

Risk level: Minimal | Skill level: Beginner-friendly

⚖️ Balanced: Post-Earnings Call Spread

Play: After earnings, buy a bull call spread targeting the $48-$50 zone

Structure: Buy March $44 calls, Sell March $50 calls (or adjust based on post-earnings price)

Why this works:

- 🎢 IV crush after earnings makes spreads significantly cheaper - buy AFTER volatility drops

- 📊 Defined risk ($6 wide spread = $600 max risk per spread)

- 🎯 Targets the $48-$50 gamma resistance zone where the big call buyer is positioned

- ⏰ March expiration gives time for ViaSat-3 F2 service entry news and Ligado payment catalyst

- 🛡️ If DAT spin-off news drops, you're already positioned

Estimated cost: ~$2.50-3.00 per spread post-earnings (cheaper if stock dips)

Risk/Reward: Risk $250-300 to make $300-350 per spread (1:1+ ratio). Improves significantly if you enter on a dip.

Risk level: Moderate | Skill level: Intermediate

🚀 Aggressive: Follow the Whale Into Earnings

Play: Buy February $45 calls before earnings, betting on a breakout above $45 resistance

Why this could work:

- 🐋 Someone just bet $3M that VSAT goes higher by February 20th - follow the smart money

- 📊 $45 is the immediate gamma resistance - a breakout triggers momentum

- 🏭 DAT spin-off commentary on earnings call could be a massive catalyst

- 🛰️ ViaSat-3 F2 positive update could justify Morgan Stanley's $51 target

- 🎯 Implied move upper range of $51.61 means $45 calls could be worth $6+ in a bull scenario

Why this could blow up:

- 💸 Earnings miss sends stock back to $40 and your calls expire worthless

- ⏰ Only 24 days to expiration - theta decay is brutal if stock doesn't move fast

- 😱 IV crush post-earnings could kill your calls even if stock stays flat

- 📉 You're buying near 52-week highs with 330% in the rear view mirror

Position sizing: Risk only 1-2% of portfolio. This is a speculative bet, not a core position.

Risk level: HIGH | Skill level: Advanced only

⚠️ Risk Factors

Don't get caught sleeping on these:

-

💸 $5.5B in net debt: Viasat carries significant leverage with $1.2B annual CapEx. Company remains GAAP unprofitable (-$3.97 EPS TTM). Rising interest rates make this debt load more painful. Positive free cash flow not expected until FY2027 on a full-year basis.

-

🛰️ Satellite deployment risk: The ViaSat-3 F1 antenna anomaly reduced capacity to a fraction of design spec. If F2 encounters similar issues during in-orbit testing, the capacity doubling thesis collapses and the stock could give back significant gains.

-

🏢 CEO selling $11M in 6 weeks: Mark Dankberg sold 100,000 shares ($4.03M) in January and 200,000 shares ($7.0M) in December. All under 10b5-1 plans, and he retains 1M+ shares, but $11M in CEO sales near highs is worth noting.

-

🌍 Starlink competition is real: SpaceX's Starlink has 72% market share with 9,000+ satellites and 20-50ms latency vs Viasat's 600ms+ GEO latency. Amazon's Project Kuiper launched 27 of 3,000+ LEO satellites. U.S. fixed broadband revenue declining as subscribers shift to LEO.

-

🎯 DAT spin-off is NOT guaranteed: Viasat said they're "evaluating a potential separation" - that's very different from "we're doing it." If they decide against it, the $50+/share activist valuation thesis evaporates overnight.

-

📈 330% rally may have priced in the good news: At ~6x EBITDA, the stock has re-rated significantly. The average analyst price target of $37.63 is actually BELOW the current price of $44.63 - meaning the consensus thinks the stock is already overvalued.

-

⏰ Short-dated expiration: These call options expire February 20th - only 24 days away. If the catalyst doesn't arrive quickly, theta decay eats the premium alive. The call buyer needs the stock to move NOW.

🎯 The Bottom Line

Real talk: Someone just made a $3M double-barrel bullish bet on VSAT with only 24 days until expiration. They bought 3,600 contracts at the $42 strike (ITM, safer exposure) AND 3,600 contracts at the $48 strike (OTM, aggressive upside bet). The $48 strike saw a volume-to-open-interest ratio of 55x, which you see maybe a handful of times per year on this name.

What this trade tells us:

- 🎯 This buyer expects VSAT to move HIGHER through the February 20th expiration, not just hold

- 💰 The dual-strike approach says they believe in both a base case ($44-$48 range) and an upside breakout ($48+)

- ⏰ The timing is not random - Q3 earnings in ~2 weeks is the catalyst

- 🏭 The $48 strike aligns with Carronade's thesis that a DAT spin-off could unlock $50+/share

- 📊 Gamma support at $42 and resistance at $45 frame the near-term battleground

If you're interested in VSAT:

- ✅ Best approach: Wait for earnings (~February 5-10) before making any moves

- 🎯 If earnings are strong and stock breaks above $45 resistance, look for pullback entry

- 📉 If earnings disappoint, $40-$42 gamma support could be a great buy-the-dip opportunity

- ⚠️ The $5.5B debt load means this isn't a "set it and forget it" stock - you need to stay on top of the catalysts

If you're already long:

- 🛡️ Consider tightening stops to $42 (strong gamma support)

- 📊 The call buyer's bet validates your thesis short-term, but don't get complacent

- ⏰ Earnings is the next major inflection - be prepared for a big move either way

Mark your calendar - Key dates:

- 📅 ~February 5-10 - Q3 FY2026 Earnings Report (THE catalyst)

- 📅 February 20 - Monthly OPEX (these calls expire!)

- 📅 March 31 - $100M Ligado lump sum payment + $16M quarterly installment

- 📅 Early 2026 - ViaSat-3 F2 service entry expected

- 📅 Mid-2026 - ViaSat-3 F3 launch for Asia-Pacific coverage

Final verdict: VSAT has a genuinely compelling catalyst stack - satellite capacity doubling, defense spin-off potential, government contract momentum, and a $568M Ligado settlement providing liquidity. The $3M call bet shows institutional conviction heading into earnings. But after a 330% rally with $5.5B in debt and CEO selling shares, this is a stock where you want to be smart, not greedy. Let earnings be your guide. The catalysts are real, but so is the risk. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual activity scores reflect these specific trades' size relative to recent VSAT history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. VSAT carries significant debt ($5.5B) and remains GAAP unprofitable. Satellite deployment carries technical risk. Earnings create binary event risk with potential for 15%+ moves in either direction.

About Viasat Inc: Viasat is a global communications company providing broadband and secure communications services through its satellite fleet, defense encryption products, and tactical data links, with a market cap of ~$5.8 billion in the Communications Services sector.