💎 WRBY Massive $2.7M Put Position - Eyewear Stock at Inflection Point! 👓

📅 December 10, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just opened a $2.7 MILLION long put position on Warby Parker this morning at 09:53:50! This substantial bearish bet bought 10,000 contracts of $20 strike puts expiring June 18, 2026 - a 6-month downside play while WRBY trades at $24.92. What makes this EXTREMELY unusual: volume of 10,000 vs existing open interest of only 28 contracts - that's a 357x increase in open interest at this strike! Translation: Someone is making a significant bet that Warby Parker's recent Google AI glasses partnership rally won't last, or they're hedging a large long position before critical 2026 catalysts materialize.

📊 Company Overview

Warby Parker (WRBY) is disrupting the traditional eyewear industry with a direct-to-consumer model that combines retail innovation with technology:

- Market Cap: $2.84 Billion

- Industry: Ophthalmic Goods / Retail Eyewear

- Current Price: $24.92 (after recent surge to $28.31 on December 10)

- Primary Business: Prescription glasses, sunglasses, contact lenses, eye exams through retail stores and online channels

- Key Innovation: Home try-on program, vertical integration, affordable pricing ($95 frames vs $300+ traditional retail)

💰 The Option Flow Breakdown

The Tape (December 10, 2025 @ 09:53:50):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:53:50 | WRBY | ASK | BUY | PUT $20 | 2026-06-18 | $2.7M | $20 | 10K | 28 | 10,000 | $24.92 | $2.70 |

🤓 What This Actually Means

This is either a large bearish position or a protective hedge on an existing long position. Here's the breakdown:

- 💸 Significant premium: $2.7M ($2.70 per contract × 10,000 contracts)

- 🎯 Strike selection: $20 provides 19.7% downside protection/target below current price

- ⏰ Time horizon: 190 days to expiration captures H1 2026 execution on Target partnership, Q1 2026 earnings, and early Google AI glasses developments

- 📊 Massive position building: 10,000 contracts represents 1 million shares worth ~$24.9M

- 🚨 Unprecedented size: Volume/OI ratio of 357x is EXTREME - this strike had virtually no interest before today

What's really happening here:

This trader is paying $2.70 per share for the June 18, 2026 $20 puts - roughly 10.8% of the stock price. There are two scenarios:

-

Bearish speculation: They believe WRBY's recent rally (from $13.63 low to $28.31 high - up 107% in 3 months) is overdone and unsustainable. The Google AI glasses partnership excitement may have created unrealistic expectations for a company still working toward sustained profitability.

-

Protective hedge: They own substantial WRBY stock (likely 1M+ shares worth $25M+) accumulated during the rally and are buying insurance against a pullback to $20 over the next 6 months. Think of it as paying 10.8% for downside protection.

Unusual Score: 🔥 EXTREME - Volume of 10,000 on existing OI of only 28 is virtually unprecedented for WRBY options. This represents a massive new position, not trading existing liquidity.

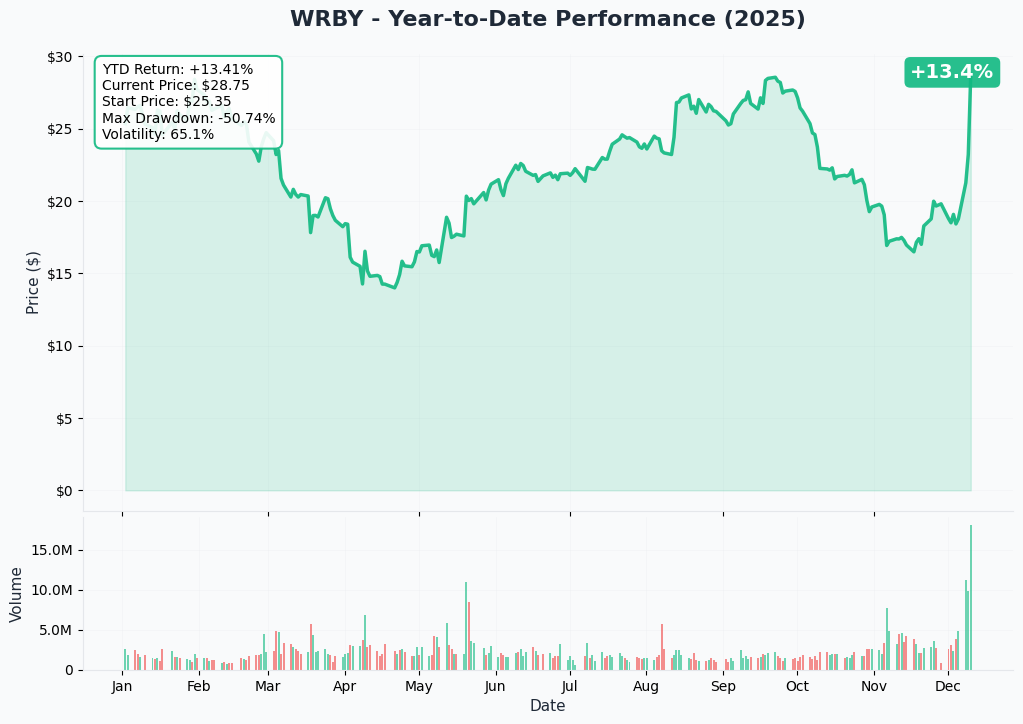

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

WRBY has staged a remarkable comeback in Q4 2025. After trading in the $13-17 range for most of the year (down from $18-20 at year start), the stock exploded higher in recent weeks on several catalysts. The chart shows extreme volatility with a 52-week range of $13.63 to $29.73.

Key observations:

- 🚀 Recent parabolic move: Vertical spike from ~$14 in late November to $28.31 on December 10 (surge of 14.6% just today!)

- 📈 Catalyst-driven: Google AI glasses partnership announcement and Citizens JMP upgrade to "Outperform" ($30 target) ignited rally

- 🎢 High volatility: Trading volume spiked to 15.82M vs average 4.49M (253% increase)

- 📊 Breaking out: Clearing resistance at $20, testing all-time high territory near $30

- ⚠️ Overextended?: Near-vertical price action suggests momentum exhaustion risk

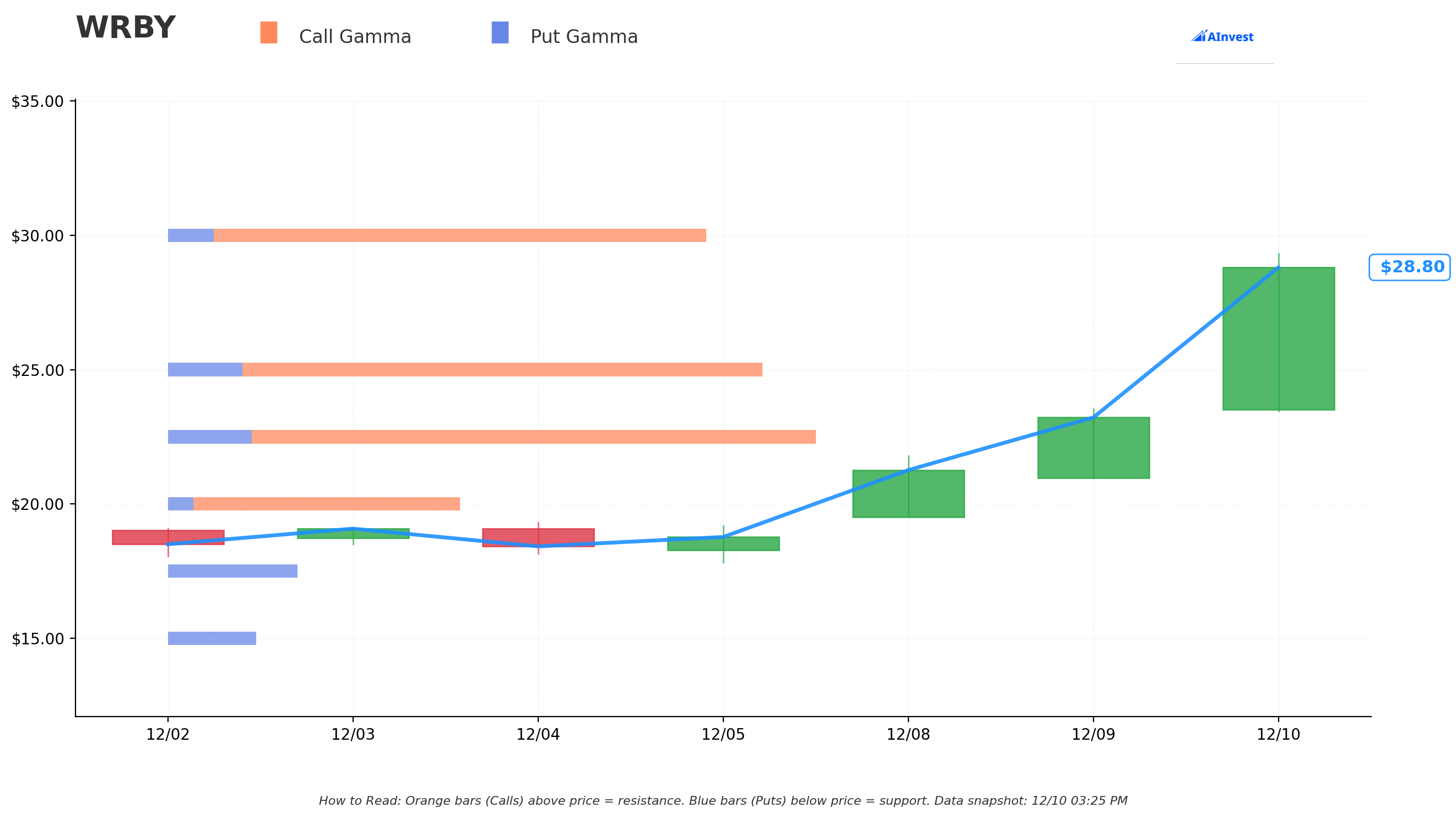

Gamma-Based Support & Resistance Analysis

Current Price: $28.83 (intraday)

The gamma exposure map reveals critical price levels that will govern near-term trading:

🔵 Support Levels (Put Gamma Below Price):

- $27.00 - Immediate support with 0.002M total gamma (nearest floor)

- $26.00 - Secondary support at 0.093M gamma (stronger accumulation)

- $25.00 - Major structural floor with 0.888M gamma (STRONGEST SUPPORT - highest total GEX)

- $24.00 - Deep support at 0.0002M gamma (relatively weak)

- $23.50 - Extended support zone (neutral gamma)

🟠 Resistance Levels (Call Gamma Above Price):

- $30.00 - Major ceiling with 0.817M gamma (STRONGEST RESISTANCE - price target from analysts)

What this means for traders:

WRBY has established very strong support at $25.00 with 0.888M in total gamma exposure - this is the critical level to watch. The stock is currently trading between $27 support and $30 resistance, creating a tight consolidation zone after the explosive rally. If WRBY breaks above $30 (analyst price target level), there's limited gamma resistance above, suggesting potential for continuation to $32-35 range.

Notice anything? The put buyer struck at $20, which is well below current gamma support levels. This isn't about protecting against a small 5-10% pullback - they're positioning for a potential 20%+ decline that would break through all technical support zones. This suggests either major fundamental concerns OR this is tail-risk hedging on a very large long position.

Net GEX Bias: Bullish (2.89M call gamma vs 0.72M put gamma) - Overall positioning remains heavily bullish, reflecting the recent rally and bullish sentiment around Google partnership.

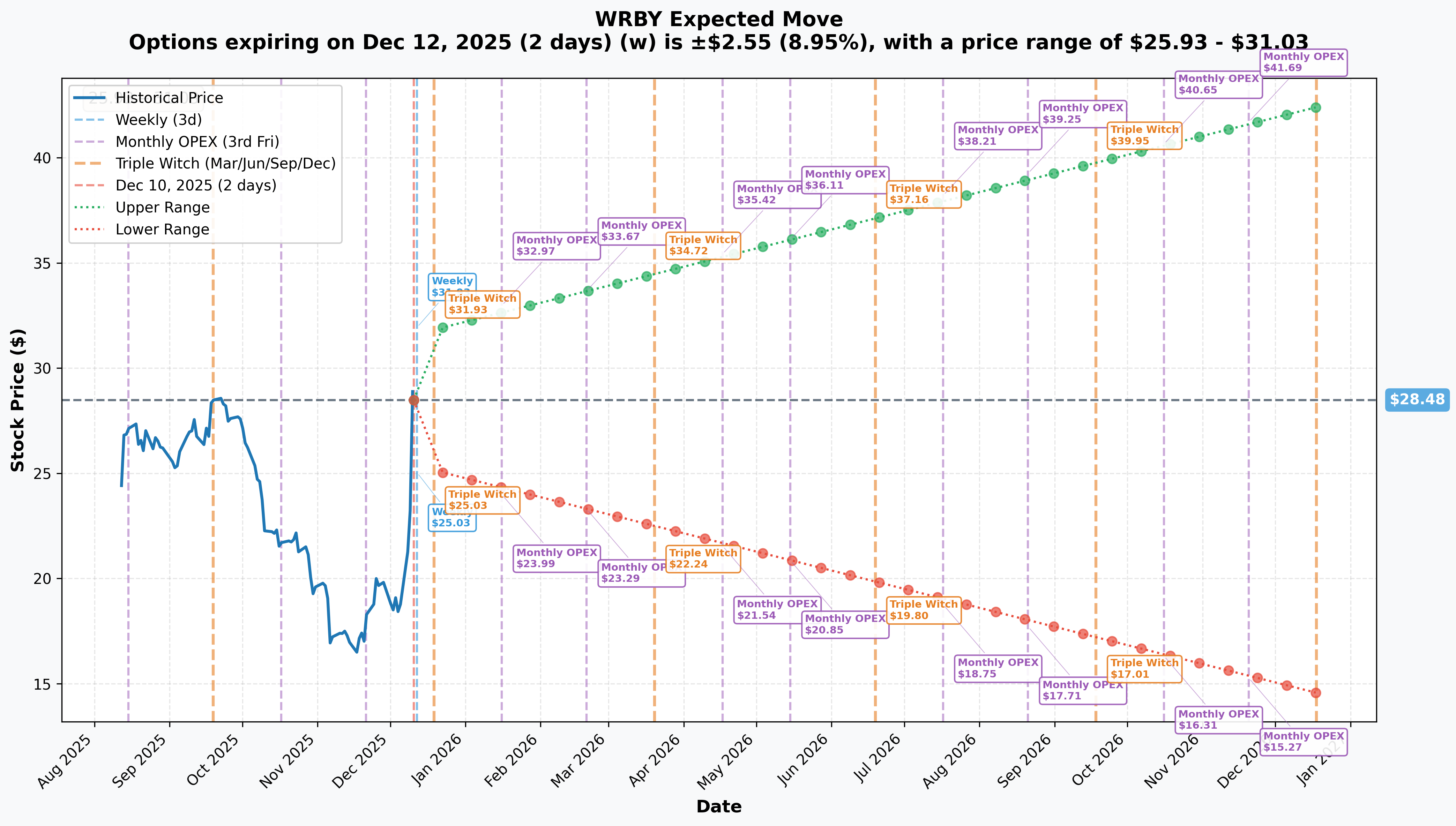

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 2 days): ±$2.55 (±8.95%) → Range: $25.93 - $31.03

- 📅 Monthly OPEX (Dec 19 - 9 days): ±$3.36 (±11.79%) → Range: $25.12 - $31.84

- 📅 Quarterly Triple Witch (Dec 19 - 9 days): ±$3.36 (±11.79%) → Range: $25.12 - $31.84

- 📅 Yearly LEAPS (Dec 18, 2026 - 373 days): ±$13.94 (±48.95%) → Range: $14.54 - $42.42

Translation for regular folks:

Options traders are pricing in a 9% move ($2.55) by this Friday - that's MASSIVE volatility for a 2-day period! The market expects continued wild swings, likely as the Google AI glasses news gets digested and traders reassess valuation after the 14.6% surge today.

The June 18, 2026 expiration (close to when this $2.7M trade expires June 18) shows the market pricing a potential move all the way down to $14.54 on the low end - validating the put buyer's downside scenario. The 48.95% implied move reflects massive uncertainty about WRBY's ability to execute on the Google partnership and Target expansion while maintaining profitability.

Key insight: The near-term implied volatility spike (9% weekly) suggests traders expect continued price swings as momentum traders battle with value investors over whether $28 is justified for a company that just achieved its first profitable quarter.

🎪 Catalysts

🔥 Recent Catalysts (Last 30 Days)

Google AI Glasses Partnership - December 2024 🤖

The catalyst that ignited today's 14.6% surge - Google committed up to $150 million to develop AI-powered smart glasses with Warby Parker:

- 💰 Initial investment: $75 million for product development and commercialization

- 💸 Conditional investment: Additional $75 million equity investment contingent on milestones

- 🤖 Technology: Built on Google's Android XR platform with Gemini AI

- 📱 Product types: AI glasses with speakers/microphones/cameras, plus display glasses with in-lens navigation

- 📅 Timeline: First products expected in 2026

- 📊 Analyst reaction: Citizens JMP upgraded to "Outperform" with $30 price target, calling WRBY "a high-beta AI and retail hybrid"

Market impact: This transforms WRBY's narrative from "affordable eyewear retailer" to "AI wearables innovator" - but execution risk is enormous. Meta's failures with similar products demonstrate the challenges.

Target Shop-in-Shop Partnership - February 2025 Announcement 🎯

Warby Parker's first retail partnership with Target Corporation:

- 🏬 Initial rollout: Five shop-in-shops opening in H2 2025 (6 months away)

- 📍 Locations: Illinois, Minnesota, New Jersey, Ohio, Pennsylvania

- 🛒 Services: Full offering including glasses, sunglasses, contacts, exams

- 💵 Pricing: Starting at $95 including prescription lenses

- 📈 Expansion potential: Additional locations planned for 2026 and beyond

Why this matters: Target serves ~100M customers annually. If successful, this could be a blueprint for massive distribution expansion - but it's unproven territory for WRBY's brand positioning.

🚀 Near-Term Catalysts (Q1-Q2 2026 - Within Put Expiration Window)

Q4 2024 Earnings - Late February 2026 📊

WRBY will report Q4 2024 results in late February 2026, providing critical updates on:

- 📈 Holiday performance: Q4 typically strongest quarter for eyewear retail

- 💰 Profitability trajectory: Q1 2025 marked first profitable quarter ($3.5M net income) - can they sustain it?

- 🏬 Store expansion progress: Targeting 45 new stores in 2025 including Target locations

- 👓 Contact lens growth: Tracking toward 20% of revenue (currently 11%)

- 👁️ Eye exam penetration: Growing from 5% to industry average 15% of revenue

- 🎯 Target partnership update: Progress on H2 2025 openings

Upside scenario: Beat on revenue and EPS, raised full-year guidance, positive Target commentary could push stock to $32-35

Downside risk: Miss on margins, cautious guidance on Target rollout, or slowing same-store sales growth could trigger 15-20% selloff to $22-24 range

Q1 2026 Earnings - Early May 2026 📊

Critical report just 1 month before put expiration:

- 🎯 Target launch status: Will be imminent (H2 2025 = June/July start)

- 🤖 Google partnership updates: Development milestones, product previews

- 💸 Sustained profitability: Second or third consecutive profitable quarter validates model

- 📊 Guidance for 2026: Sets expectations for full-year performance

This earnings report will likely be the KEY catalyst determining whether these puts expire worthless or become profitable.

Target Shop-in-Shop Opening - H2 2025 (June-July Estimated) 🏬

The five initial Target locations will open during the put expiration window:

- 📈 Success metrics: Customer traffic, conversion rates, sales per square foot

- 🔄 Cannibalization check: Impact on nearby Warby Parker standalone stores

- 📣 Brand positioning: Does operating in Target hurt premium perception?

- 🚀 Expansion decision: Performance will dictate 2026 rollout plans

Critical risk: If Target partnership underperforms or creates brand dilution issues, stock could gap down 15-20% overnight. The put buyer may be specifically hedging this execution risk.

Google AI Glasses Development Updates - Throughout 2026 🤖

Product development milestones could create volatility:

- 📱 Product unveiling: Google I/O (May 2026) or dedicated launch event

- 🧪 Beta program: Developer previews, early tester feedback

- 🏭 Manufacturing: Partner announcements, production timelines

- ⚠️ Delays or issues: Any technical problems or pushed timelines would be catastrophic

Why this matters for the put: Google's $150M investment sounds massive, but it's contingent on milestones. If product development stalls or Google reduces commitment, WRBY's AI narrative collapses and stock gaps to $18-20 range.

📊 Medium-Term Catalysts (Beyond Put Expiration)

2025 Store Expansion - 45 New Locations 🏬

- 📍 Growth rate: 15-16% fleet expansion in single year

- 💰 Capital intensive: New stores take 2-3 years to reach maturity

- 📉 Near-term margin pressure: Dilutes profitability until stores ramp

- 🎯 Eye exam expansion: Targeting 90%+ of stores with exam capability

Contact Lens Market Penetration 👁️

- 📈 Current: 11% of revenue, growing 36% YoY

- 🎯 Target: Industry average 20% of revenue

- 💵 Revenue potential: Could add $70M annual revenue at current scale

- 🔄 Subscription model: Higher customer lifetime value, recurring revenue

Vision Insurance Network Expansion 💳

- 🏥 Current partners: VSP, MetLife, other major plans

- 📊 Opportunity: Reducing out-of-pocket barriers drives customer acquisition

- ⏰ Timeline: Ongoing negotiations throughout 2026

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst analysis, here are scenarios through June 18, 2026 expiration:

📈 Bull Case (30% probability)

Target: $35-40

How we get there:

- 💪 Google AI glasses development exceeds expectations - product previews generate buzz

- 🎯 Target partnership launches successfully with strong traffic and sales metrics

- 📊 Q4 2024 and Q1 2026 earnings both beat, showing sustained profitability ($5-8M net income per quarter)

- 🏬 Store expansion executing flawlessly - new stores ramping faster than expected

- 👓 Contact lens penetration reaching 15%+ of revenue

- 💰 Gross margins expanding to 55-56% from scale efficiencies

- 📈 Analyst upgrades cascade as AI wearables narrative gains credibility

- 🚀 Breakout above $30 gamma resistance triggers technical rally to $35-40

Key metrics needed:

- Revenue growth 15-18% YoY

- Sustained positive GAAP net income

- Same-store sales growth 8-10%

- Target partnership economics proven viable

Why only 30%: Requires nearly perfect execution on multiple fronts (Google partnership, Target rollout, profitability, store expansion) while avoiding any missteps. Stock already up 107% in 3 months - much of upside captured.

🎯 Base Case (45% probability)

Target: $22-28 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Decent earnings meeting expectations - profitable but not spectacular

- 🎯 Target partnership progresses on schedule but early data inconclusive

- 🤖 Google AI glasses development on track but no major milestones/reveals

- 💰 Margins remain in 54-55% range - stable but not expanding

- 🏬 Store expansion continues but some locations underperform

- 📊 Market digests massive Q4 2025 gains, waits for concrete proof points

- 🔄 Trading between $25 gamma support and $28-30 resistance for months

- 💤 Volatility normalizes from current extreme levels

This is the put buyer's nightmare scenario: Stock consolidates in $22-28 range, puts lose significant time value but don't go in-the-money. They paid $2.70 for protection that expires with stock at $25, resulting in 50-70% loss on premium.

Why 45% probability: Most realistic outcome given current elevated valuation and execution uncertainty. Market needs tangible results before awarding higher multiples. Consolidation allows time for catalysts to develop.

📉 Bear Case (25% probability)

Target: $18-22 (PUTS PROFIT!)

What could go wrong:

- 😰 Q4 2024 or Q1 2026 earnings disappoint - revenue miss or margin compression

- 🚨 Target partnership underperforms - low traffic, cannibalization issues, or brand dilution concerns

- ⏰ Google AI glasses development delays announced - timeline pushed to 2027 or technical issues

- 💸 Google reduces commitment or makes contingent $75M investment conditional on tougher milestones

- 🇨🇳 Macro headwinds hit consumer discretionary spending - eyewear purchases deferred

- 🏬 Store expansion economics deteriorate - new locations not reaching profitability targets

- 📊 Competitive pressure from EssilorLuxottica intensifies

- 💰 Cash burn returns if profitability proves unsustainable

- 🔨 Break below $25 gamma support triggers cascade to $22, then $20

Critical support levels:

- 🛡️ $25.00: Major gamma floor (0.888M) - MUST HOLD or momentum shifts bearish

- 🛡️ $22.00: Psychological support - prior trading range high

- 🛡️ $20.00: This put strike - likely strong buying at this level

Put P&L in Bear Case:

- Stock at $20 on June 18: Puts worth $0 (at-the-money), loss = -$2.70/share × 10,000 = -$2.7M (100% loss)

- Stock at $18 on June 18: Puts worth $2.00, loss = -$0.70/share × 10,000 = -$700K (26% loss)

- Stock at $15 on June 18: Puts worth $5.00, profit = $2.30/share × 10,000 = $2.3M (85% gain!)

- Stock at $12 on June 18: Puts worth $8.00, profit = $5.30/share × 10,000 = $5.3M (196% gain!)

Breakeven: Stock needs to fall below $17.30 ($20 strike - $2.70 premium) for puts to profit.

Probability assessment: 25% because it requires either major execution failures OR significant macro deterioration. WRBY's fundamentals are improving (first profitable quarter, store expansion working, partnerships materializing), but the Google AI narrative creates massive disappointment risk if development stalls.

💡 Trading Ideas

🛡️ Conservative: Wait For Consolidation Entry

Play: Stay on sidelines until post-rally consolidation creates better risk/reward

Why this works:

- 📈 Stock up 107% in 3 months - momentum exhausted, pullback likely

- 💸 Implied volatility extremely elevated (9% weekly move) - options overpriced

- 🎯 Better entry at $22-25 offers 15-20% margin of safety from current $28

- 📊 Multiple catalysts (earnings, Target launch, Google updates) create binary risks

- 🤔 The $2.7M put buy signals someone expects downside - respect the signal

- ⏰ Target partnership and Google development need 6-12 months to validate

Action plan:

- 👀 Watch for pullback to $25 gamma support (first attractive entry)

- 🎯 $22-23 range would be ideal entry (prior resistance becomes support)

- ✅ Wait for Q4 2024 earnings in late February - need profitability confirmation

- 📊 Monitor Target partnership launch in June/July for early performance data

- ⚠️ If stock breaks below $20, major thesis damage - stay away

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 20-30% drawdown if rally fails. Get better entry with lower risk if consolidation occurs.

⚖️ Balanced: Bull Put Spread Above Support

Play: After consolidation, sell bull put spread above $25 gamma support

Structure: Sell $25 puts, Buy $22.50 puts (June 2026 expiration - same as the $2.7M trade)

Why this works:

- 📊 Collect premium assuming WRBY stays above strong $25 gamma support

- 🎯 Defined risk spread ($2.50 wide = $250 max risk per spread)

- ⏰ 190 days to expiration provides cushion for volatility

- 💰 Credit spread benefits from time decay and volatility crush

- 🛡️ Only at risk if stock breaks major support level

Estimated P&L (wait for better entry timing):

- 💰 Collect ~$0.80-1.00 credit per spread initially

- 📈 Max profit: $80-100 if WRBY above $25 at June expiration (keep full credit)

- 📉 Max loss: $150-170 if WRBY below $22.50 (spread width minus credit)

- 🎯 Breakeven: ~$24.00-24.20

- 📊 Win rate: ~65-70% if entered when stock consolidates near $26-27

Entry timing:

- ⏰ Wait for pullback to $25-27 range (don't enter at current $28+ levels)

- 🎯 Only enter if implied volatility drops below 50% (currently elevated)

- ❌ Skip if stock showing breakdown below $25 support

Position sizing: Risk only 1-3% of portfolio per spread (10-30 spreads max)

Risk level: Moderate (defined risk, bullish bias) | Skill level: Intermediate

🚀 Aggressive: Long Stock + Protective Puts (Replicating The Trade)

Play: Buy WRBY stock with protective put hedge - similar structure to the unusual activity

Structure: Buy 100 shares WRBY + Buy 1x $20 put June 2026

Why this could work:

- 🎯 Participate in Google AI glasses upside (potential to $35-40)

- 🛡️ Protected below $20 - maximum loss defined

- 💰 If WRBY executes on Target + Google partnerships, substantial upside

- 📊 Copying institutional positioning structure (synthetic collar)

- ⏰ 190 days gives time for catalysts to develop

Capital required per unit:

- 📊 Stock purchase: $2,850 (100 shares × $28.50)

- 🛡️ Put protection: $270 (1 contract × $2.70)

- 💰 Total investment: $3,120

Estimated P&L:

- 📈 Bull scenario (stock to $35): Gain $650 on stock, lose $270 on put = $380 profit (12% return)

- 📈 Moderate bull (stock to $30): Gain $150 on stock, lose $270 on put = -$120 loss (4% loss)

- 📊 Flat (stock at $28): Lose $270 on put = -9% loss

- 📉 Bear scenario (stock to $20): Lose $850 on stock, gain $850 on put minus $270 cost = -$270 loss (9% max loss)

- 📉 Disaster (stock to $15): Maximum loss still only $270 (protected below $20)

Key insight: This structure limits downside to ~9% while maintaining unlimited upside - exactly what the institutional trader is doing but scaled to retail size.

Risks:

- 💸 Put premium ($270) is "insurance cost" - lost if stock stays flat or rallies moderately

- ⏰ Need strong rally to $32+ to overcome put cost and profit

- 📊 Ties up $3,120 capital for 6 months

Entry timing:

- 🎯 Better entry on pullback to $25-26 reduces capital at risk

- ⏰ Consider waiting until after Q4 earnings for clarity

Position sizing: Allocate only 5-10% of portfolio (high-conviction, high-risk play)

Risk level: HIGH (requires stock rally to profit) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🤖 Google AI glasses execution risk: This is WRBY's first venture into wearable technology competing against Meta, Apple, and other tech giants with far deeper resources. Meta's Ray-Ban Stories failed to gain traction, Google Glass was famously discontinued, Snap Spectacles flopped - the wearables graveyard is full. Product delays, technical issues, or consumer rejection would destroy the AI narrative that drove the stock from $14 to $28. The $150M investment is contingent on milestones - if WRBY misses targets, Google could reduce or cancel the second $75M tranche.

-

🎯 Target partnership unproven model: WRBY has NEVER operated within another retailer's environment. This creates multiple risks: (1) Cannibalization of nearby standalone stores, (2) Brand dilution operating in mass-market retailer, (3) Operational complexity managing dual formats, (4) Lower conversion rates vs. dedicated stores, (5) Conflicts over merchandising and customer experience. If initial five locations underperform, the entire expansion thesis collapses and stock could gap down 15-20%.

-

💰 Profitability still fragile: Q1 2025 marked first profitable quarter ever ($3.5M net income) after years of losses. Full-year 2024 still showed $20.4M GAAP net loss. Path to sustained profitability depends on (1) Store expansion economics working, (2) Gross margins holding at 54-55%, (3) Operating leverage from scale, (4) No macro headwinds hitting consumer spending. A single disappointing quarter could reignite concerns about long-term viability and send stock back to $15-18 range.

-

🏬 Aggressive store expansion creates execution risk: Opening 45 new stores in 2025 (16% fleet growth!) requires flawless execution on (1) Real estate selection in competitive market, (2) Hiring and training optometrists and staff, (3) Managing construction and buildouts, (4) Initial inventory and working capital, (5) Marketing and customer acquisition. New stores dilute margins for 2-3 years before reaching profitability. Any slowdown in new store economics would force WRBY to reduce expansion, eliminating a key growth driver.

-

🦁 EssilorLuxottica dominance is formidable barrier: The Italian-French giant controls 80% of major eyewear brands and 39% U.S. market share through vertical integration (manufacturing to retail). WRBY's 7.2% market share faces constant competitive pressure from (1) LensCrafters price matching, (2) Vision insurance network leverage, (3) Premium brand portfolio (Ray-Ban, Oakley), (4) Supply chain advantages. Gaining meaningful share beyond 10-12% will be extremely difficult.

-

💸 Valuation stretched after 107% rally: At current $28-29 levels, WRBY trades at approximately 3.5-4.0x forward sales for a company that just turned profitable for one quarter. Compare to mature retail comps at 0.5-1.5x sales. The stock has priced in substantial future growth and perfect execution. Any stumble creates 25-30% downside to revert to more reasonable 2.0-2.5x sales multiple around $18-20 range.

-

📉 Limited international exposure creates single-market risk: ~90% of revenue from U.S. market means WRBY lacks diversification. A U.S. recession, consumer spending pullback, or retail sector weakness directly impacts 90% of business. International expansion requires significant capital and faces different competitive dynamics - not a near-term solution.

-

🇨🇳 China sourcing and tariff exposure: Approximately 20% of products sourced from China. WRBY targeting <10% China sourcing by end of 2025, but transition is costly. Any new tariffs or trade tensions could compress margins by 100-200bps, eliminating fragile profitability. Q2 2025 saw eyewear market contract 1.5% YoY partly due to tariff uncertainty.

-

💊 Contact lens and eye exam scaling faces headwinds: Growing from 11% to 20% revenue from contact lenses requires (1) Optometrist hiring in tight labor market, (2) Navigating state-by-state regulatory complexity, (3) Insurance reimbursement pressures, (4) Competition from pure-play contact lens retailers. Eye exam expansion from 5% to 15% of revenue faces similar challenges. If these growth drivers stall, overall revenue growth slows to mid-single digits.

-

📊 Insider selling exceeded $240M in late 2024/early 2025: Significant insider selling activity suggests executives taking chips off the table after the rally. While not necessarily bearish (could be diversification/liquidity needs), it indicates insiders don't see the current $28 level as a bargain.

-

🎢 Options liquidity thin outside front month: The 10,000 volume vs 28 OI ratio shows this strike had virtually no liquidity before today. If you need to exit option positions, bid-ask spreads could be wide and slippage significant. This isn't AAPL or TSLA - WRBY options are thinly traded.

🎯 The Bottom Line

Real talk: Someone just committed $2.7 million to protect against WRBY falling to $20 over the next 6 months - despite the stock rallying 107% and the company landing a transformational Google partnership. This either signals sophisticated hedging by a large institutional holder who's made massive gains and wants insurance, OR outright bearish speculation that the Google AI glasses narrative is overhyped.

What this trade tells us:

- 🎯 Smart money is NOT confident WRBY holds current $28 levels through June 2026

- 💰 They're willing to pay 10.8% of stock price for downside protection - that's expensive insurance

- ⚖️ The strike at $20 (19.7% below current) suggests expectations for either correction back to pre-rally levels OR protection against major catalyst failure

- ⏰ June 2026 expiration captures critical catalysts: Q4 2024 earnings, Q1 2026 earnings, Target partnership launch, Google AI updates

- 🚨 Volume/OI ratio of 357x is unprecedented - this is a MASSIVE new position

This is a "prove it" trade - the put buyer doesn't believe the hype until WRBY demonstrates execution.

If you own WRBY:

- ✅ Consider trimming 30-50% at $27-29 levels if you rode the rally from $14 (lock in 90%+ gains)

- 📊 If holding through catalysts, set MENTAL STOP at $25 (major gamma support) to protect gains

- ⏰ You've already won! Rally from $14 to $28 is spectacular. Protecting profits is smart.

- 🎯 If Q4 earnings beat AND Target launch succeeds, could re-enter trimmed shares on confirmation

- 🛡️ Consider buying protective puts similar to this trade if holding large position (2-3 puts per 1,000 shares)

If you're watching from sidelines:

- ⏰ Late February 2026 Q4 earnings is critical inflection point - wait for results

- 🎯 Post-rally pullback to $22-25 would be attractive entry (15-25% off highs with gamma support)

- 📈 Looking for confirmation: Sustained profitability, Target partnership metrics, Google development on track

- 🚀 Long-term (12-24 months), if Google AI glasses launch successfully and Target expands to 50+ locations, $35-40 is achievable

- ⚠️ Current $28 offers poor risk/reward - too much enthusiasm priced in, too many execution risks

If you're bearish:

- 🎯 Wait for failed rally attempt above $30 or break below $25 support before initiating shorts

- 📊 First support at $27 (gamma), major support at $25 (highest total GEX), deeper at $22-23 (prior range)

- ⚠️ Put spreads ($25/$20 or $22.50/$17.50) offer defined-risk way to play downside after volatility moderates

- 📉 Watch for break below $25 - that's the trigger for potential cascade to $22, then $20

- ⏰ Bearish catalysts: Earnings miss, Target partnership issues, Google delays, macro weakness

Mark your calendar - Key dates:

- 📅 December 12 (Friday) - Weekly options expiration (implied move ±9%)

- 📅 December 19 - Monthly/Quarterly OPEX

- 📅 Late February 2026 - Q4 2024 earnings report (CRITICAL)

- 📅 Early May 2026 - Q1 2026 earnings report (1 month before put expiration)

- 📅 June-July 2026 - Target shop-in-shop openings (H2 2025 = summer start)

- 📅 June 18, 2026 - Expiration of this $2.7M put trade

- 📅 2026 - Google AI glasses product launch (exact timing TBD)

Final verdict: WRBY's partnerships with Google and Target are legitimate game-changers IF executed well - but that's a massive IF. The company just achieved its first profitable quarter ever, is expanding aggressively into new formats (Target), new product categories (smart glasses), and new geographies. This creates asymmetric opportunity - either WRBY becomes a $5-7B company worth $40-50/share if everything works, OR it's a $1.5-2B company worth $15-20/share if execution stumbles.

At current $28 levels after 107% rally in 3 months, the risk/reward is unfavorable. The $2.7M institutional put position signals smart money wants protection. Respect that signal.

Be patient. Let the company prove it can execute. Better entry points will emerge. The Google and Target opportunities will still be there in 6 months, and you'll sleep better paying $23 instead of $28.

This is a show-me story, not a believe-me story. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The volume/OI ratio reflects this specific strike's liquidity situation - it does not imply the trade will be profitable or that you should follow it. Warby Parker is a growth company with execution risk and limited profitability history. Always do your own research and consider consulting a licensed financial advisor before trading.

About Warby Parker Inc.: Warby Parker operates as a mission-driven lifestyle brand at the intersection of design, technology, healthcare, and social enterprise, offering prescription glasses, sunglasses, contact lenses, and eye exams through retail stores and digital channels, with a market cap of $2.84 billion in the Ophthalmic Goods industry.