🎰 WYNN: $23M Bullish Call Position Closed Before Q4 Earnings - What Smart Money Knows!

📅 December 31, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just cashed out a $23 MILLION bullish call position in Wynn Resorts with 80 days until expiration! This isn't some retail trader taking profits - this is institutional money closing 16,000 contracts at the $110 strike, likely banking massive gains after WYNN's 46.5% YTD run. With quarterly earnings expected in mid-February and the stock trading near recent highs at $121.11, smart money is de-risking ahead of potential volatility.

💰 Company Overview

Wynn Resorts (WYNN) is a luxury casino and resort operator with flagship properties in Las Vegas, Macau, and Massachusetts. The company operates premium gaming destinations including Wynn Las Vegas, Encore Boston Harbor, and two major properties in Macau (Wynn Palace and Wynn Macau). WYNN is currently building a $5.1 billion integrated resort in the UAE set to open Spring 2027 - the region's first casino resort.

Key Metrics:

- 💵 Market Cap: $12.51 billion

- 🏢 Sector: Hotels & Motels / Gaming & Leisure

- 📊 Current Price: $121.11 (as of trade time)

- 📈 YTD Performance: +46.5% (vs S&P 500's +16%)

- 💰 Dividend Yield: 0.83% ($1.00 annually)

📊 The Option Flow Breakdown

🔥 What Just Happened

| Time | Symbol | Buy/Sell | C/P | Expiration | Strike | Premium | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:20:15 | WYNN | SELL | CALL | 2026-03-20 | $110 | $23.0M | 16,000 | 30,000 | 15,626 | $121.11 | $15.00 | WYNN20260320C110 |

🤓 What This Actually Means

Real talk: This is a massive position closing trade, not someone opening a new bet. Here's why this matters:

🎯 Trade Classification: Close Long CALL (STC - Sell to Close) 📊 Confidence Level: MEDIUM 🔬 Z-Score: 2.98 (HIGHLY UNUSUAL - this is 298% larger than typical WYNN options activity) 📈 Volume Signal: HIGH ACTIVITY - 16,000 contracts vs 30,000 open interest (53.3% ratio)

Translation for us regular folks: Someone who bought these $110 calls weeks or months ago is now selling them for a profit. At a spot price of $121.11, these calls are $11.11 in the money. If they originally paid, say, $5-8 per contract, they're walking away with profits of $7-10 per contract on a $23M position. That's potentially $11-16 million in gains 💰

Why close now?

- ✅ Stock up 46.5% YTD - mission accomplished

- ✅ Q4 earnings in ~6 weeks - reduce risk before potential volatility

- ✅ Still 80 days until expiration - plenty of time value left, but they're taking the money and running

- ✅ Chinese New Year (January 29, 2026) gaming volumes could be priced in

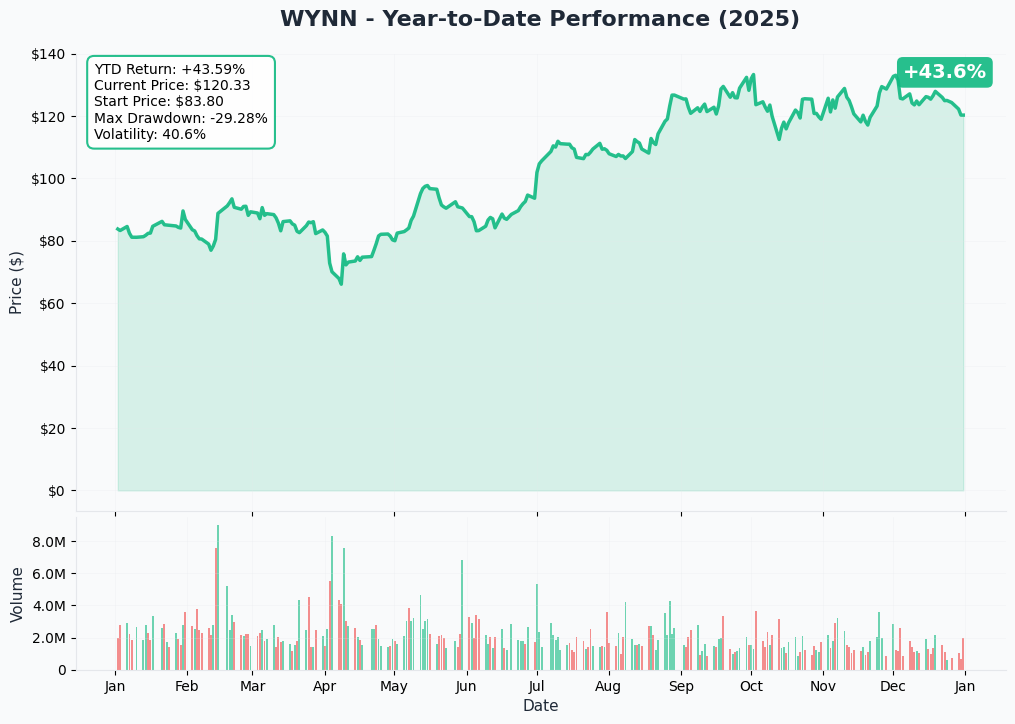

📈 Chart Check-Up

YTD Performance Chart

What the chart tells us:

WYNN has been on an absolute tear in 2025! The stock bottomed at $65.25 earlier this year and rocketed to a 52-week high of $134.72 in November - that's a 106% gain from the lows. Currently trading around $121, the stock has pulled back about 10% from those highs but remains in a strong uptrend.

Key observations:

- 📈 Strong upward momentum throughout 2025

- 🎯 November high of $134.72 represents near-term resistance

- 💪 Consistent higher lows suggest institutional accumulation

- ⚠️ Recent consolidation near $120-122 could be healthy profit-taking

The massive call closing trade makes sense when you see this chart - whoever bought those $110 calls likely got in when the stock was trading $95-105, and they're now banking double-digit gains per contract.

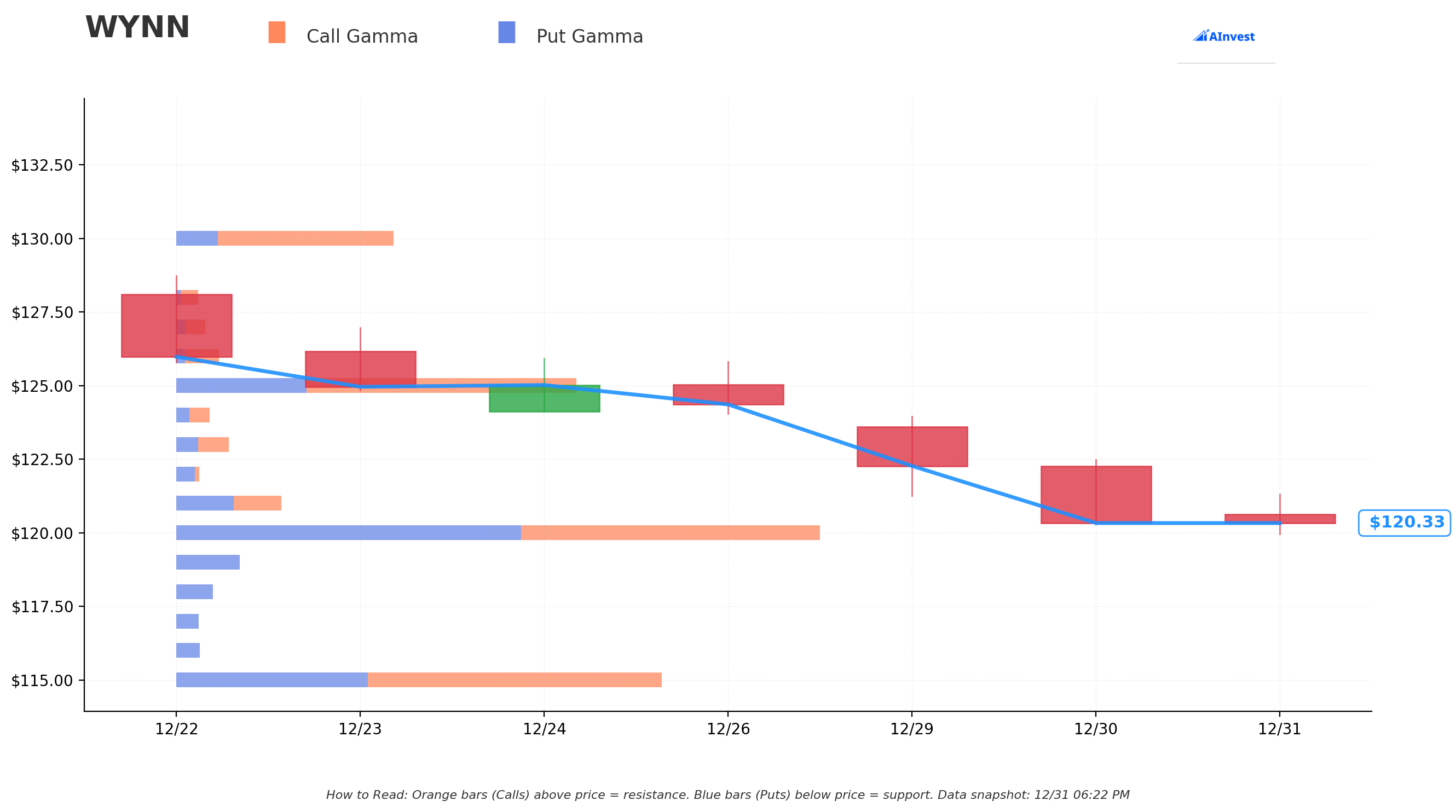

🎯 Gamma-Based Support & Resistance Analysis

The gamma landscape shows interesting dynamics:

Support Levels (Blue Bars - Put Gamma):

- 🛡️ $120 - STRONGEST SUPPORT: Total GEX of 3.44M with slight put bias (-0.24M net). This is literally where we're trading RIGHT NOW, suggesting this level has serious institutional interest

- 🛡️ $115: Total GEX of 2.59M with call bias (+0.55M net). This is your first major support zone if $120 breaks

- 🛡️ $110: Total GEX of 6.47M with MASSIVE call bias (+5.05M net). This is where the big trade happened! Makes sense - huge open interest here acting as a magnet

- 🛡️ $105: Weaker support at 0.61M total GEX

Resistance Levels (Orange Bars - Call Gamma):

- 🚧 $121 - IMMEDIATE RESISTANCE: Total GEX of 0.56M, right at current price

- 🚧 $125: Total GEX of 2.14M with call bias (+0.75M net). First meaningful resistance level

- 🚧 $130: Total GEX of 1.16M - psychological round number

- 🚧 $135: Total GEX of 1.52M - approaching the November highs

- 🚧 $140 - MASSIVE RESISTANCE: Total GEX of 3.97M with HUGE call bias (+3.88M net). This is the ceiling for now

Net GEX Bias: Bullish (26.5M call GEX vs 9.1M put GEX)

What this means for traders: The stock is sandwiched between $120 support (where we're trading) and $125 resistance. The fact that someone just closed 16,000 contracts at $110 suggests they expect the stock to stay rangebound or potentially pull back. The $110-115 zone has become a fortress of support given all that gamma.

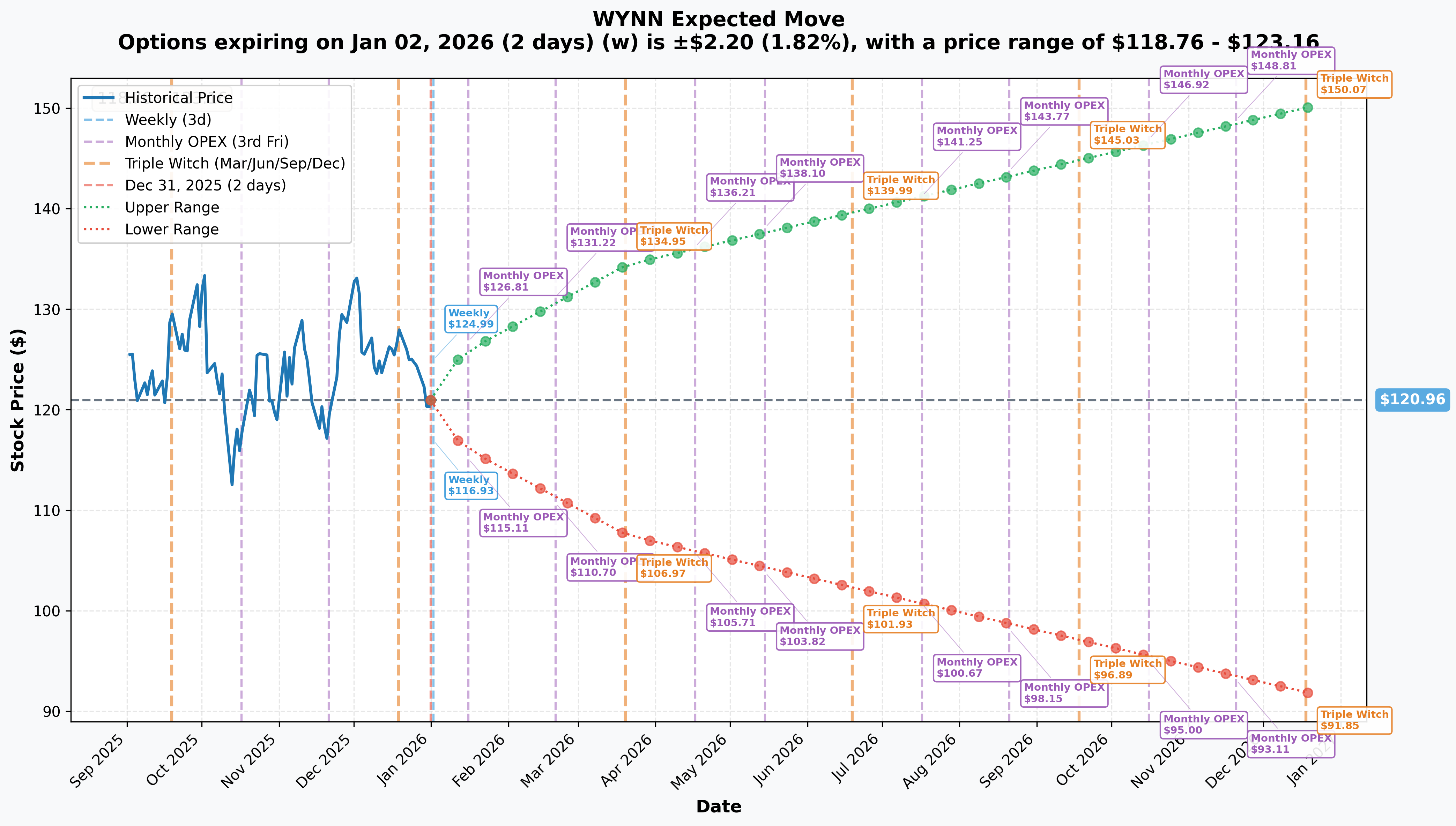

📊 Implied Move Analysis

What options are pricing in:

The implied volatility tells us exactly what kind of moves traders are expecting:

- 📅 Weekly (Jan 2, 2026): ±1.82% ($2.20 move) - Range: $118.76-$123.16

- 📅 Monthly OPEX (Jan 16, 2026): ±4.17% ($5.05 move) - Range: $115.91-$126.01

- 📅 Quarterly Triple Witch (Mar 20, 2026): ±11.14% ($13.47 move) - Range: $107.49-$134.43

- 📅 Yearly LEAPS (Dec 18, 2026): ±24.07% ($29.11 move) - Range: $91.85-$150.07

Translation: Options markets are pricing in relatively calm action near-term (under 2% weekly moves) but bigger swings around earnings. The March expiration - which is when this big trade expires - is expecting an $11.14% move. That means the market sees WYNN trading between $107.49 and $134.43 by then. The smart money who closed at $110 is protecting against the downside scenario.

🎪 Catalysts

🔮 Upcoming Catalysts

Short-Term (Next 30 Days):

- 🧧 Chinese New Year (January 29, 2026): CLSA projects low-teens GGR growth in H1 2026, with Q1 typically benefiting from Chinese New Year travel to Macau. Mass-market dominance at 75% of Macau GGR provides more stable revenue base. Premium mass segment tracking 8,000 players with average bets of HK$24,018 (+6% YoY) according to Citigroup research.

Medium-Term (1-3 Months):

-

📊 Q4 2025 Earnings (February 11, 2026 estimated): Consensus revenue estimate around $1.85 billion. Key metrics to watch include Macau market share during Q4 holiday season, Las Vegas group booking pace for 2026, UAE project capital deployment updates, and dividend sustainability. The last earnings on November 6, 2025 beat revenue estimates ($1.83B vs $1.77B consensus) but missed EPS ($0.86 vs $1.09).

-

🏗️ Encore Tower Remodel Launch (Spring 2026): $330 million renovation project starting in Las Vegas. Could create temporary headwinds from room inventory reduction but signals confidence in premium positioning.

Long-Term (3-6 Months):

- 🇦🇪 Wynn Al Marjan Island Construction Milestones (H1 2026): Hotel tower topped out at 283 meters in November 2025, with spire installation expected in 2026 to reach final 352-meter height. Over $3.4 billion (67%) of the $5.1 billion budget already spent or committed. This Spring 2027 opening represents the most significant new casino resort opening globally.

✅ Recent Catalysts (Already Happened)

Q3 2025 Earnings Beat (November 6, 2025):

- Revenue: $1.83 billion (+8.3% YoY), beat consensus by 3.88%

- Net Income: $88.3 million (vs $32.1M loss in Q3 2024)

- Wynn Palace Macau revenue +22.3% YoY to $635.5M with $200.3M EBITDA

- Record August EBITDA in Las Vegas from premium rate strategy

Analyst Upgrades (October-December 2025):

- Jefferies raised PT to $164 (December 24, 2025)

- Citigroup upgraded to Buy with $160 PT (November 2025)

- Goldman Sachs raised PT to $150 (October 2025)

- Wells Fargo initiated coverage at $151 Overweight (October 2025)

- Consensus: Strong Buy with 16 Buy ratings, 6 Hold, 0 Sell - Average PT: $142.79

Tilman Fertitta Stake Increase:

- Billionaire casino owner increased stake from 9.9% to 12.3% between November 2024 and April 2025

- Now stated he will remain a "passive investor" following Senate confirmation as US Ambassador to Italy

- Wall Street speculation of potential takeover has moderated but his conviction signals long-term confidence

🎲 Price Targets & Probabilities

Based on gamma levels, implied volatility, and upcoming catalysts, here's how the next 3 months could play out:

🐂 Bull Case: $134-140 (20% probability)

How we get there:

- Chinese New Year volumes exceed expectations in late January/early February

- Q4 earnings beat on both revenue AND EPS (unlike Q3)

- Macau market share gains continue (+22% YoY at Wynn Palace)

- UAE construction milestone announcements fuel FOMO

- Stock breaks through $125 resistance and tests November highs at $134.72

Gamma/IV support: $140 has 3.97M in total GEX and represents the upper bound of the March implied move. The yearly LEAPS price in $150 as possible by December 2026.

Key risk: This requires near-perfect execution and no earnings disappointment. The fact that smart money just took $23M off the table suggests they see this as lower probability.

⚖️ Base Case: $115-125 (55% probability)

How we get there:

- Stock consolidates in current range through earnings

- Q4 results are "good enough" - revenue beat, EPS inline

- Chinese New Year provides modest boost but nothing spectacular

- Market digests the $330M Encore remodel plans (short-term disruption, long-term positive)

- Gamma support at $120 and $115 holds any pullbacks

- Resistance at $125 caps upside until UAE opening gets closer

Gamma/IV support: Monthly OPEX implied move of $115.91-$126.01 perfectly captures this range. The $110-$115-$120 zone has 12.5M in combined GEX acting as a magnet.

Why this is most likely: The $23M position closing suggests smart money expects rangebound action. Analyst average PT of $142.79 provides long-term upside but near-term volatility from earnings and Macau comp headwinds could keep the lid on.

🐻 Bear Case: $100-115 (25% probability)

How we get there:

- Q4 earnings disappoint on EPS again (like Q3's 21% miss)

- Chinese New Year gaming volumes underwhelm due to China economic weakness

- Macau VIP recovery stalls (still 61% below 2019 levels)

- Concerns about $10.57B debt load in higher-rate environment

- Massachusetts iGaming legislation threatens Encore Boston Harbor ($200M+ annual EBITDA at risk)

- Breaks below $120 support and tests the $115 level

Gamma/IV support: March implied move bottom is $107.49. The $110 strike has 6.47M in GEX which should provide major support, but if that breaks, next stop is $105.

Why this could happen: Q3 already showed revenue beats don't guarantee EPS beats. Debt-to-Equity of 2.3x is elevated. Dividend only covered 69% by recent EPS. If earnings disappoint AND guidance is cautious, the $23M seller looks like a genius.

💡 Trading Ideas

🛡️ Conservative: Cash-Secured Put at $115 (January 16 expiry)

The Play:

- Sell the $115 put expiring January 16, 2026

- Collect approximately $2.50-3.00 per contract ($250-300 per contract)

- Secure with $11,500 in cash per contract

Why this works:

- You get paid to potentially buy WYNN at $115 (5% below current price)

- $115 has strong gamma support (2.59M total GEX)

- If assigned, your effective cost basis is $112-112.50 (well below the $110 support zone)

- Monthly implied move suggests $115.91 as the lower bound - you're selling puts AT that level

- Even if earnings disappoint, $115 held as support earlier this year

Risk Management:

- Maximum loss if stock gaps to zero: $11,200 per contract (unlikely for established casino operator)

- Real risk: Assignment at $115 when stock is trading $105-110

- Best case: Keep the premium and repeat next month

Probability of profit: ~65-70% based on implied volatility

⚖️ Balanced: Bull Call Spread $120/$130 (March 20 expiry)

The Play:

- Buy the $120 call / Sell the $130 call expiring March 20, 2026

- Net cost: Approximately $4.50-5.00 per spread

- Maximum profit: $5.00-5.50 ($10 width - premium paid)

- Maximum loss: Premium paid ($4.50-5.00)

Why this works:

- You're betting on WYNN staying above $120 (current support) and reaching $130 by March

- $130 is the mid-point of the March implied move ($107.49-$134.43)

- Breakeven around $124.50-125, which is right at first resistance

- Risk/reward ratio of roughly 1:1.1

- Earnings and Chinese New Year catalysts happen during this timeframe

- This is the SAME expiration as the $23M trade that just closed - you're essentially taking the other side but with defined risk

Risk Management:

- Maximum loss is limited to premium paid ($450-500 per spread)

- If WYNN drops to $110 support, spread loses 100% of value

- Best case: WYNN at or above $130 at expiration = $550-600 profit per spread (100%+ gain)

Probability of profit: ~45-50% (stock needs to stay above breakeven of $124.50)

🚀 Aggressive: Long March $125 Calls (March 20 expiry)

The Play:

- Buy the $125 call expiring March 20, 2026

- Cost: Approximately $7.00-8.00 per contract

- Unlimited upside above $125

- Maximum loss: Premium paid

Why this works:

- You're betting on a breakout above the $125 resistance level

- If WYNN repeats November's run to $134.72, these calls could be worth $9.72+ (40%+ gain)

- March expiration captures Q4 earnings, Chinese New Year, and potential UAE news

- Analyst average PT of $142.79 suggests 17%+ upside from current levels

- $125 has 2.14M in GEX - once it breaks, next stop is $130-135

Risk Management:

- Maximum loss: $700-800 per contract (100% loss if stock stays below $125)

- Breakeven: $132-133 (stock needs to rally 9-10% from current levels)

- This is a momentum bet - ONLY take this if earnings are strong

- Consider buying 50% now, 50% after earnings if results are positive

Probability of profit: ~35-40% (requires meaningful upside move)

YOLO Factor: If Macau surprise to the upside AND UAE announces accelerated timeline, these could 2-3x. But that's a low probability scenario. Size accordingly - this is speculative.

⚠️ Risk Factors

Let's be real about what could go wrong:

💔 Earnings Execution Risk

Q3 already showed that revenue beats don't guarantee EPS beats. WYNN posted $1.83B revenue (+8.3% YoY, beat by 3.88%) but missed EPS by 21% ($0.86 vs $1.09 consensus). If Q4 repeats this pattern, the stock could sell off hard despite revenue growth. The market wants to see margin expansion, not just revenue growth.

🏗️ UAE Project Risks

The $5.1 billion Wynn Al Marjan Island project is the company's biggest bet. While 67% of the budget is already spent or committed, execution risk remains. Gaming regulatory approvals are still pending final confirmation. Construction delays, cost overruns, or regulatory hiccups could derail the Spring 2027 opening. The UAE is an unproven gaming market - no one knows if "build it and they will come" works in the Gulf region.

💰 Debt & Dividend Concerns

Total debt of $10.57 billion against a $12.51B market cap is concerning. The Debt-to-Equity ratio of 2.3x is among the highest in gaming. Net Debt/EBITDA of 4.39x vs market average of 1.29x means refinancing risk in a higher-rate environment. Worse, Q1 2025 EPS of $0.69 only covered 69% of the $0.25 dividend (down from 100% coverage in 2024). If earnings don't improve, the dividend could be at risk.

🇨🇳 China Economic Slowdown

Macau represents ~50% of EBITDA, making WYNN heavily exposed to China's economic health. The property sector stress in China, RMB volatility, and potential visa restrictions could all impact Macau volumes. While premium mass is growing (+6% YoY), VIP revenue is still 61% below 2019 levels. Any escalation in China-US tensions or domestic policy changes could crater Macau volumes overnight.

🎰 Regional Gaming Competition

- Massachusetts iGaming: Pending legislation could legalize online gambling, threatening Encore Boston Harbor's $200M+ annual EBITDA

- Japan IRs: Integrated resorts in Osaka and potentially other cities could siphon VIP traffic from Macau

- Las Vegas competition: Resorts World Las Vegas and renovated competitor properties challenging WYNN's premium positioning

📉 Technical Breakdown Risk

The stock pulled back 10% from November highs of $134.72 to current $121. If $120 support breaks (the level with 3.44M in GEX), next stop is $115. A break below $115 could trigger a cascade to $110 or even $105. The $23M position closing suggests smart money sees downside or rangebound action as more likely than a breakout to new highs.

🎯 The Bottom Line

Here's the deal: Someone with deep pockets and presumably good information just cashed out $23 MILLION in WYNN call profits ahead of Q4 earnings. That's not bearish per se - it's smart risk management after a 46.5% YTD run. They bought low (probably around $95-105), rode the wave to $121, and locked in gains.

For the rest of us, here's the action plan:

📌 If You Already Own WYNN Stock:

- Hold through earnings if you're long-term bullish on the UAE project and Macau recovery

- Consider selling covered calls at $125-130 to generate income and cap upside

- Set a stop loss at $115 if you're not comfortable with 5%+ downside

- Don't chase if it breaks to new highs above $134 without clear catalysts

📌 If You're Watching from the Sidelines:

- Wait for earnings clarity on February 11, 2026 - the Q3 EPS miss was a red flag

- Watch Chinese New Year volumes in late January as a leading indicator

- If the stock pulls back to $115-117 on earnings weakness, that's your entry for the UAE upside story

- The March $120/$130 call spread offers balanced risk/reward if you want defined exposure

📌 If You're Bearish or Want Protection:

- The bear case to $100-115 has merit given debt levels and earnings quality issues

- Buying March $115 puts or put spreads could hedge portfolio exposure

- Cash-secured puts at $110-115 let you get paid while waiting for a better entry

Mark your calendar for:

- 🧧 January 29, 2026: Chinese New Year (watch Macau volumes)

- 📊 February 11, 2026: Q4 2025 Earnings (estimated)

- 🏗️ Q1 2026: UAE construction milestones and spire installation

The Lesson: When you see $23M institutional money taking profits after a big run, it's worth paying attention. They're not saying the party's over - they're saying the easy money has been made. From here, WYNN needs to EARN its upside through execution on earnings, Macau market share, and UAE development. The implied volatility is pricing in an 11% move by March - that's a lot of uncertainty.

Trade smart. Size appropriately. And remember: options are leveraged instruments that can go to zero. Never bet more than you can afford to lose. 🎲

Disclaimer: This analysis is for educational purposes only and does not constitute financial advice. Options trading involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Always conduct your own due diligence and consult with a qualified financial advisor before making investment decisions.

Analysis based on market data as of December 31, 2025. Option prices and Greeks are estimates and subject to market conditions.