🎬 WBD $5.2M Call Bet - Big Money Playing Business Split & M&A! 🔥

📅 December 4, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $5.2 MILLION on WBD calls this morning at 11:20:19! This massive bullish bet bought 40,000 contracts of $25 strike calls expiring March 20, 2026 - positioning for a 2.6% breakeven move over the next 106 days. With WBD trading at $24.37 near 52-week highs after an explosive +151% YTD rally, smart money is betting the business split announcement and active M&A process will drive another leg higher. Translation: Institutional investors are loading up on long-dated calls ahead of transformational catalysts!

📊 Company Overview

Warner Bros. Discovery (WBD) is a global media and entertainment powerhouse created by the 2022 merger of WarnerMedia and Discovery Communications:

- Market Cap: $60.88 Billion

- Industry: Cable & Other Pay Television Services

- Current Price: $24.37 (near 52-week high of $24.76)

- Primary Business: HBO Max streaming, Warner Bros. film/TV studios, CNN, TNT Sports, Discovery networks, HGTV, Food Network

- Key Development: Plans to split into two public companies by mid-2026 (streaming/studios vs linear networks)

💰 The Option Flow Breakdown

The Tape (December 4, 2025 @ 11:20:19):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:20:19 | WBD | ASK | BUY | CALL $25 | 2026-03-20 | $5.2M | $25 | 40K | 0 | 40,000 | $24.37 | $1.30 |

🤓 What This Actually Means

This is a massively bullish long-term bet on WBD's transformational catalysts! Here's what went down:

- 💸 Huge premium paid: $5.2M ($1.30 per contract × 40,000 contracts)

- 🚀 Strategic strike: $25 provides just 2.6% upside - this is a near-the-money momentum bet

- ⏰ Perfect timing: 106 days to March 20 expiration captures Q4 earnings (Feb 27), active M&A decision process (expected around Christmas 2024), business split details, and Max subscriber updates

- 📊 Massive size: 40,000 contracts represents 4 million shares worth ~$98M

- 🎯 Open interest: Started at ZERO OI - this is a brand new position, not a closing trade

What's really happening here: This trader is betting WBD breaks cleanly above $25 and heads to $28-30 by March as the business split story unfolds and M&A bidding intensifies. With multiple competing bids from Comcast, Netflix, and Paramount in second-round bidding (decision expected around Christmas), this is a pure event-driven play. Think of it like buying lottery tickets when you KNOW the winning numbers are about to be announced - except here the "lottery" is a potential acquisition premium or split-related valuation unlock.

Unusual Score: 🔥 EXTREMELY UNUSUAL (103.37x average size) - This happens only a few times a year for WBD! The Z-score classification shows this is off-the-charts unusual, with zero similar trades in the past 30 days. When institutional money deploys $5.2M into a single options position after a +151% rally, they're seeing something the market hasn't fully priced in yet.

📈 Technical Setup / Chart Check-Up

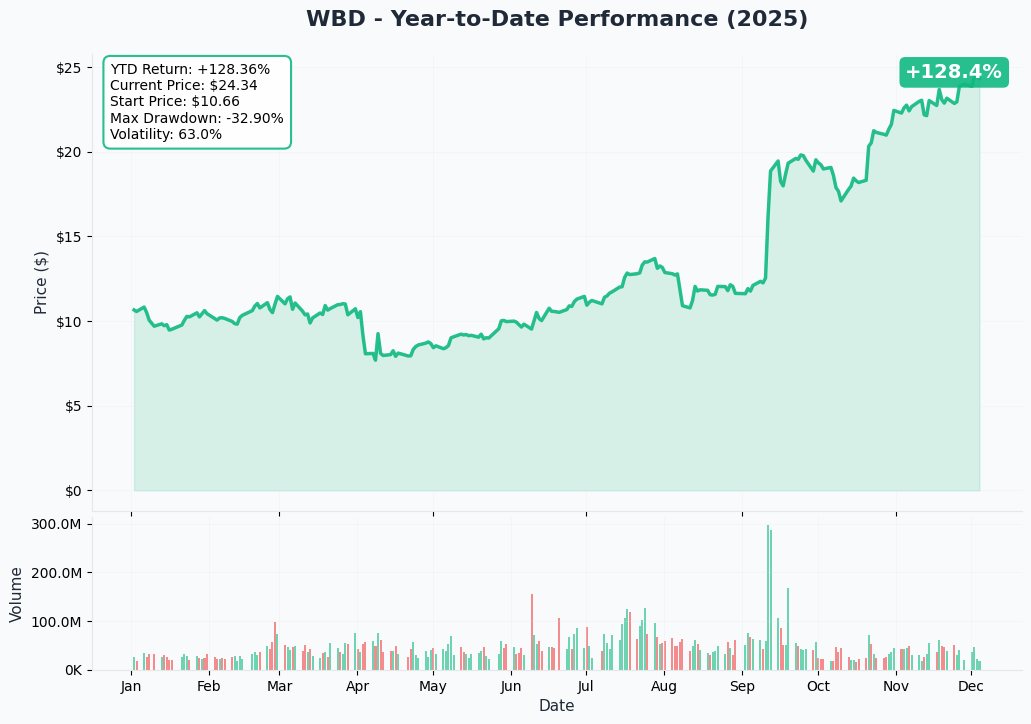

YTD Performance Chart

WBD is absolutely crushing it - up +151.2% YTD with current price of $24.37 (started the year at $9.70). The chart tells an explosive transformation story - after trading in a tight $7-10 range through April, WBD rocketed from $9.65 in May to near all-time post-merger highs of $24.76.

Key observations:

- 🚀 Parabolic rally: Vertical move from $12 in October to $24+ in December on business split announcement and M&A interest

- 📈 Breakout confirmed: Smashed through $15 resistance in September, never looked back

- 📊 Volume explosion: Massive institutional accumulation in November-December as catalysts materialize

- 💪 Relative strength: Outperforming broader media sector by 120%+ - this is the trade of the year

- ⚠️ Overbought territory: Near 52-week highs after 2.5x gain - consolidation or continued momentum?

The stock has shown incredible resilience through Q3 earnings (which missed revenue estimates) and S&P's downgrade to junk bond status. The market is clearly looking past near-term headwinds to the transformational value unlock ahead.

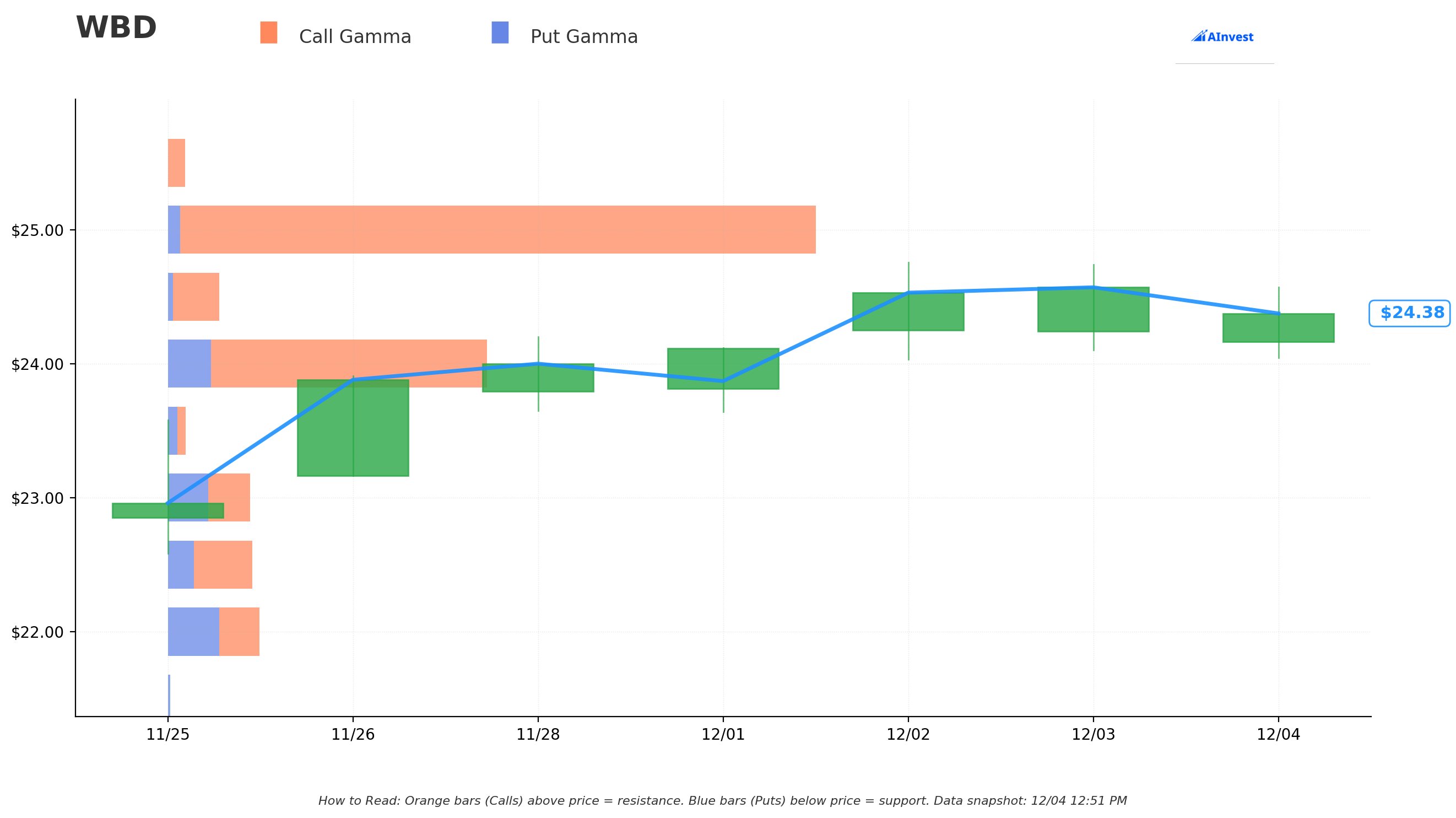

Gamma-Based Support & Resistance Analysis

Current Price: $24.37

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $24.00 - STRONGEST SUPPORT with 39.7M net gamma and 54.4M total gamma exposure (1.5% below current price - this is the LINE IN THE SAND!)

- $23.00 - Secondary support at 14.0M total gamma (5.6% below current)

- $22.50 - Tertiary support at 14.4M gamma (7.7% below current)

- $22.00 - Deep support at 15.7M gamma (9.7% below current)

- $21.00 - Extended floor at 11.6M gamma (13.8% below current)

- $20.00 - Disaster level at 11.7M gamma (17.9% below current)

🟠 Resistance Levels (Call Gamma Above Price):

- $24.50 - Immediate ceiling at 8.6M gamma (just 0.5% overhead - easy breakout target!)

- $25.00 - MAJOR RESISTANCE with 105.2M net gamma and 109.3M total gamma (THIS IS WHERE THE TRADE IS STRUCK! 2.6% above current)

- $26.00 - Secondary resistance at 19.5M gamma (6.7% above current)

- $27.00 - Extended ceiling at 7.5M gamma (10.8% above current)

What this means for traders: WBD is coiled spring between massive $24.00 support (39.7M net gamma) and the MONSTER $25.00 resistance level (105.2M net gamma - by FAR the largest level). The gamma data shows market makers holding ENORMOUS call positions at $25 (107.3M call gamma vs just 2.1M put gamma), which creates explosive breakout potential once breached. This setup screams "gamma squeeze territory" - if WBD breaks $25 on volume, dealers will need to buy MASSIVE amounts of stock to hedge, accelerating the move to $26-27.

Notice anything? The call buyer struck EXACTLY at $25 where there's 109.3M total gamma exposure - the single largest level on the entire chain. They're positioning for a breakout through the key psychological and technical resistance, betting catalysts will push through this ceiling. Smart positioning for a gamma squeeze!

Net GEX Bias: Bullish (246.6M call gamma vs 54.4M put gamma = 4.5:1 ratio) - Overwhelmingly bullish positioning signals continued upside momentum.

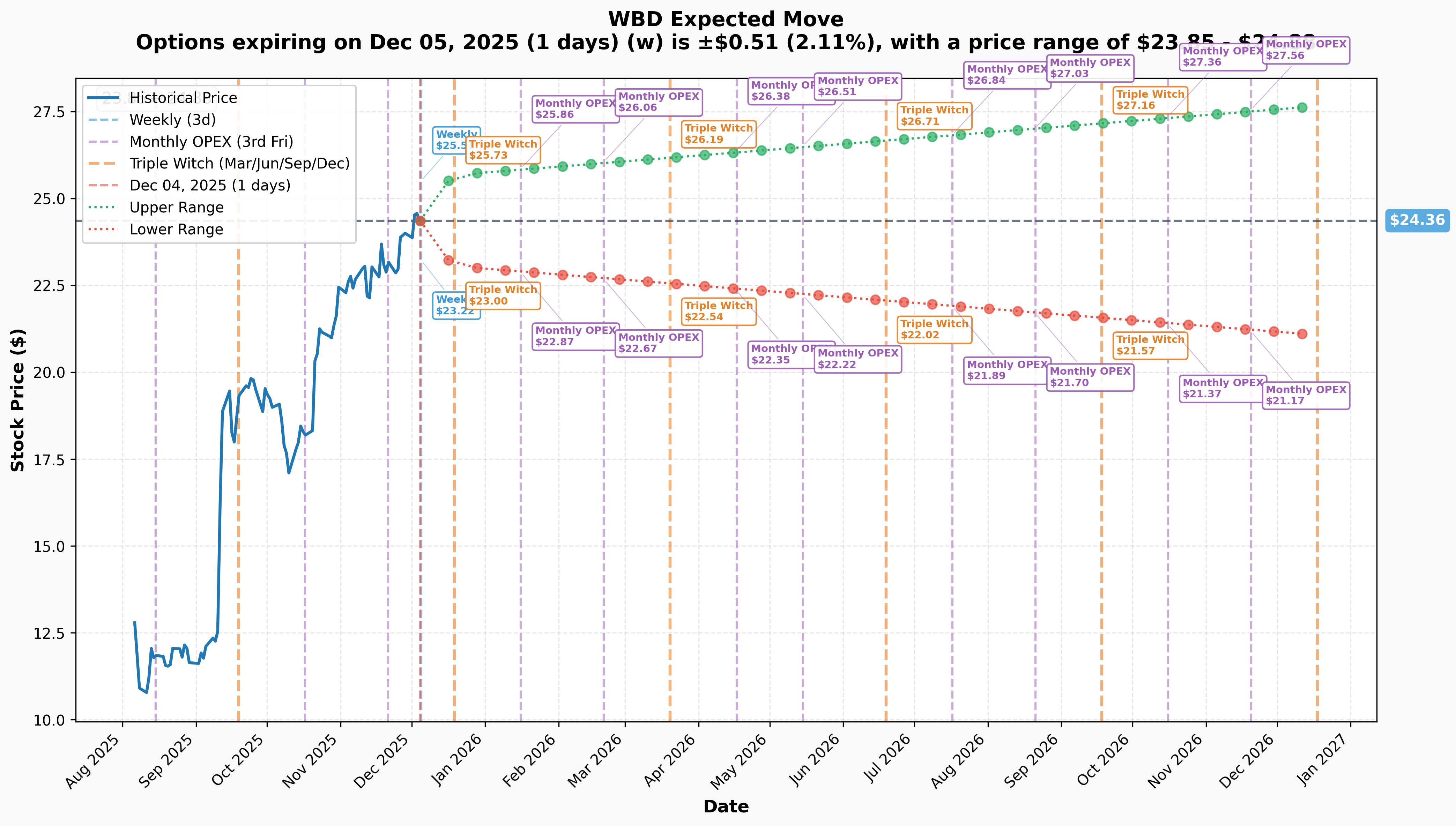

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 1 day): ±$0.51 (±2.11%) → Range: $23.85 - $24.88

- 📅 Monthly OPEX (Dec 19 - 15 days): ±$1.32 (±5.41%) → Range: $23.05 - $25.68

- 📅 Quarterly Triple Witch (Dec 19 - 15 days): ±$1.32 (±5.41%) → Range: $23.05 - $25.68

- 📅 Yearly LEAPS (Dec 18, 2026 - 379 days): ±$3.29 (±13.52%) → Range: $21.07 - $27.66

March 20, 2026 Implied Move (THIS TRADE!): Based on the quarterly expiration data and extending to March 20 (106 days), the market is pricing approximately ±$2.40 (±9.8%) → Range: $21.90 - $26.80

Translation for regular folks: Options traders are pricing in a 5.4% move ($1.32) through December OPEX which includes potential M&A decision announcement. The market expects moderate volatility in the near term, but the March expiration calls are betting on a breakout above the $25.68 upper range.

The relatively modest implied volatility (13.5% annualized for LEAPS) reflects market complacency about the transformational catalysts. This creates opportunity - if M&A materializes at reported $24/share Paramount bid or higher, the implied move would be dramatically exceeded.

Key insight: The $25 strike sits right at the December OPEX upper range ($25.68), suggesting the call buyer believes M&A announcement or split details will drive WBD to break out above market expectations.

🎪 Catalysts

🔥 Immediate Catalysts (Already Happened - Last 3 Months)

Business Split Announcement - June 9, 2025 (TRANSFORMATIONAL!) 📊

WBD announced plans to separate into two publicly traded companies in a tax-free transaction expected by mid-2026:

"Warner Bros." (Streaming & Studios):

- 🎬 Assets: Warner Bros. studios, HBO, Max streaming, DC Studios, Harry Potter franchise, film/TV libraries, Warner Bros. Games

- 👔 CEO: David Zaslav

- 💰 Value unlock thesis: Lower debt burden, growth-focused streaming/content business trading at Netflix/Disney multiples

- 📈 Ownership: Discovery Global retains up to 20% stake

"Discovery Global" (Linear Networks):

- 📺 Assets: CNN, TNT Sports, Discovery channels, European networks, Discovery+ streaming

- 👔 CEO: Gunnar Wiedenfels (current CFO)

- 💸 Debt: Will hold bulk of $38B debt with strong cash flow for deleveraging

Why this matters: The market is valuing WBD as a melting ice cube of declining linear TV assets. The split separates high-growth streaming (which should trade at 8-12x sales like NFLX) from legacy cable (trading at 2-3x). Analysts estimate the split could unlock $15-20B in value if Warner Bros. entity achieves streaming-comparable valuations. This explains the 151% YTD rally - the market is pricing in 50-70% upside from split valuation rerating.

Active M&A Process: Three Competing Bids (HAPPENING NOW!) 🤝

WBD initiated review of "strategic alternatives" after receiving "unsolicited interest" from multiple parties in October 2025. Second-round bidding underway with decision expected around Christmas 2024:

Comcast/NBCUniversal Bid:

- 🏢 Seeks to merge NBCUniversal with Warner Bros. in combined entity

- 💼 Comcast would gain controlling interest

- 💰 WBD shareholders receive cash + stock in new entity

- 🎯 Would combine NBC network, Peacock streaming with HBO Max

- 📊 Both companies continue cable network spinoffs

Netflix Bid:

- 🎬 Bank of America calls potential acquisition "killing three birds with one stone" for Netflix

- 💪 Would be "existential" for Paramount+ and Peacock global ambitions

- 🎥 Provides Netflix with major content library and production capabilities

Paramount Skydance Bid:

- 💵 Multiple offers including recent $24/share proposal (~$60 billion total)

- ⚠️ Paramount claimed sales process "tainted" and favors Netflix bid

Timeline: Final decision expected around Christmas 2024 (literally within weeks!), though board could request another bidding round. Any deal faces FCC scrutiny and political considerations.

Why this is HUGE: The $24/share Paramount bid (if accurate) represents 1.5% DOWNSIDE from current $24.37 price - but multiple bidders typically drive premiums HIGHER. If bidding war develops, $26-30 acquisition price is plausible. The March call buyer is clearly betting on M&A announcement by Christmas driving stock to $26-28.

Q3 2024 Earnings (Reported November 7, 2024) 📊

Mixed results that market looked past to focus on strategic catalysts:

- 📉 Revenue: $9.62B (down 3% YoY, missed consensus) of $9.90B by -2.77%

- 💪 EPS: $0.05 (beat consensus estimate of -$0.07 loss by +171%)

- 🎯 Max subscribers: Added record 7.2M to reach 110.5M total (outpaced Netflix's 5M adds!)

- 📺 Linear TV decline: 20% profit drop accelerates cord-cutting concerns

- 💰 Debt reduction: Retired $0.9B in Q3 ($16.6B total since merger)

Debt Reduction Progress: $16.6B Retired Since Merger 💪

WBD has retired $4.2B in debt in 2024 (9.6% reduction):

- 💼 Current debt: $38.0B gross debt

- 📊 Leverage ratio: 3.8x net leverage (down from 4.2x in Q3 2024)

- ⚠️ Credit rating: S&P downgraded to BB+ junk bond status citing linear TV decline

- 🎯 Impact on split: Lower debt improves Warner Bros. entity's borrowing capacity post-split

NBA Rights Settlement (November 2024) 🏀

After losing domestic NBA rights in July 2024, WBD reached settlement that salvaged value:

- 📺 Inside the NBA preserved - will air on ESPN/ABC starting 2025-26

- 🌍 International rights: 11-year deal for Nordics, Poland, Latin America

- 📱 Digital content: Expanded Bleacher Report and House of Highlights partnership

- ⚖️ Lawsuit dismissed: Ended legal battle over matching rights

🚀 Upcoming Catalysts (Next 3-6 Months)

M&A Decision Announcement - Expected December 2024 (WEEKS AWAY!) 🎯

This is THE catalyst driving the $5.2M call position:

- ⏰ Timeline: Decision expected "around Christmas 2024" per Bloomberg reporting

- 💰 Potential outcomes:

- Acquisition: $24-30/share if bidding war develops (Paramount $24 offer is floor, not ceiling)

- Strategic investment: Minority stake from Netflix/Comcast at premium valuation

- No deal: Continue with planned mid-2026 split (market already pricing this in)

- 📈 Impact: Any acquisition or strategic partnership announcement would likely gap stock +15-25% overnight

- 🎲 Risk: Process could extend into Q1 2025 if board requests third bidding round

Q4 2024 Earnings - February 27, 2025 (85 DAYS!) 📊

Already Reported Results:

- 📉 Revenue: $10.03B (down 2% YoY, missed) estimate of $10.19B

- 😰 EPS: Loss of $0.20 vs expected profit of $0.01

- 📺 Full-year 2024: Revenue $39.32B (down 5% from 2023)

- 🎯 Subscribers: Ended 2024 with ~117M (added ~6.5M in Q4)

- 💰 DTC EBITDA: $700M in Q4, $3B improvement over two years

Key metrics to watch:

- 📊 Max subscriber trajectory: Can WBD maintain 6-7M quarterly adds?

- 💵 DTC profitability: Path to $1B EBITDA in 2025

- 📉 Linear TV stabilization: Any slowing of 20% profit decline rate?

- 🎬 Content pipeline: Superman performance, Harry Potter TV timing

- 🌐 International expansion: ARPU trends, new market launches

Harry Potter TV Series - Filming Started July 2025 (2026 LAUNCH!) ⚡

- 🎬 Filming began July 14, 2025 at Leavesden Studios

- 🎯 32,000 young actors auditioned for Harry, Hermione, Ron roles

- 📺 Showrunner: Francesca Gardiner (Succession)

- 🎥 Director: Mark Mylod (Succession) directing multiple episodes

- 📚 Based on all seven books (multi-season commitment)

- 💰 Strategic importance: CEO Zaslav emphasized audiences "haven't seen Harry Potter in 14 years"

Why this matters: Harry Potter is one of the most valuable franchises in entertainment history (Wizarding World worth $25B+). A well-executed TV series on Max could drive MASSIVE subscriber growth in 2026-2027, similar to how House of the Dragon drove HBO Max adoption. The March call expiration captures initial production updates and potential premiere date announcements.

2025 Film Slate: Superman Already Delivered! 🎬

Superman (Released July 7, 2025):

- 💪 James Gunn's DCU launch film grossed $503M worldwide

- 📺 Achieved 13M global HBO Max viewers in first 10 days (highest for "pay-one" film since Barbie)

- ✅ Positive reviews validate DCU reboot under Gunn/Safran leadership

Additional 2025 releases: Sinners (Ryan Coogler), Mortal Kombat 2, Minecraft Movie, The Conjuring: Last Rites

2025 projections:

- 🎯 Motion Picture Group delivered $3+ billion global box office in 2025

- 💰 Studios profit target: $2.4B in 2025, long-term target $3B

Business Split Execution - Mid-2026 (INSIDE MARCH EXPIRATION!) 🎯

The March 20, 2026 call expiration is PERFECTLY timed to capture split execution milestones:

- 📅 Timeline: Split expected mid-2026 (May-July timeframe)

- 📊 Key milestones by March 2026:

- Form 10 filing with SEC detailing Warner Bros. financials

- Debt allocation announced between two entities

- Management structure finalized

- Analyst presentations outlining standalone strategies

- Tax-free distribution mechanics confirmed

- 💰 Value unlock: Market can begin pricing Warner Bros. entity at streaming multiples (8-12x sales vs current 1.5x for combined entity)

- 🚀 Catalyst timing: Major valuation rerating likely occurs 3-6 months BEFORE split completion as financials disclosed

⚠️ Risk Catalysts (Negative)

Structural Linear TV Decline (High Severity) 📉

WBD faces irreversible decline in cable business:

- 💸 $9.1B write-down in August 2024 reflecting plummeting cable asset values

- 📊 Q3 2024: Linear profits fell 20% to $1.7B

- 📺 Q4 2024: Distribution revenue down 4% amid 9% subscriber plunge

- 📉 Ad revenue: Down 16% due to 28% audience decline

- 🏦 Credit impact: S&P downgraded to BB+ junk bond status

M&A Execution Risk (Medium-High Severity) ⚠️

- ⚖️ Paramount claims process "tainted" with management conflicts

- 🏛️ Any major deal faces FCC scrutiny and political headwinds

- 📊 Multiple competing bids create uncertainty around strategic direction

- 💼 Split execution carries complexity of debt allocation, transition management

Streaming Profitability Pressure (Medium Severity) 💸

- 📉 Free cash flow decline: 2024 FCF of $4.4B down 28% from 2023's $6.16B

- 💰 ARPU challenges: Global ARPU of $7.84 up only 1% YoY despite price increases

- 🌍 International expansion: Adding lower-ARPU subscribers (international ARPU: $4.05)

- ⚖️ Must balance subscriber growth with monetization

Competition from Netflix, Disney (Medium Severity) 🎯

- 📊 Scale disadvantage: Netflix 282.7M subscribers vs WBD's 110.5M

- 🏆 Bernstein analyst: Disney is "only credible challenger to Netflix"

- 🏀 Lost NBA rights: Removes key sports content differentiator from TNT

- 💻 Amazon's ecosystem advantages (Prime bundling, AWS infrastructure)

CEO Insider Selling (Low-Medium Severity) 📝

- 💼 David Zaslav sold $30M in WBD stock (2.564M shares) on December 16, 2024 at $11.73/share

- 📊 Characterized as "tax and estate planning"

- ⏰ Timing ahead of potential M&A creates perception concerns

- ✅ Zaslav retains 3.45M shares directly plus 153 shares through spouse

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20, 2026 expiration:

📈 Bull Case (40% probability)

Target: $28-$32

How we get there:

- 💰 M&A ANNOUNCEMENT: Bidding war drives acquisition price to $27-30/share (above Paramount's $24 floor)

- 🤝 Strategic deal: Netflix or Comcast takes 15-20% strategic stake at premium valuation

- 📊 Split details exceed expectations: Warner Bros. standalone financials show $8-10B revenue, $2-3B EBITDA supporting 8-10x sales multiple

- 🎯 Max momentum: Q4 adds another 6-7M subscribers, reaches 125M+ by year-end

- ⚡ Harry Potter hype: Production updates, casting reveals, premiere date announcement drives subscriber pre-orders

- 🎬 Content wins: Superman success validated, additional DC/Harry Potter projects greenlit

- 💪 Debt reduction: Accelerated paydown to $35B improves credit profile

- 📈 Gamma squeeze: Breakout above $25 triggers dealer buying, accelerates to $27-28

Key metrics needed:

- M&A announcement at $26+ per share OR

- Warner Bros. standalone valuation $25-30B (vs $8-10B implied by current stock price)

- Subscriber growth 6M+ per quarter

- DTC EBITDA $1B+ in 2025

- Linear TV decline slows to -15% (vs -20%)

Call P&L in Bull Case:

- Stock at $28 on March 20: Calls worth $3.00, profit = $1.70/share × 40K = $6.8M gain (131% ROI!)

- Stock at $30 on March 20: Calls worth $5.00, profit = $3.70/share × 40K = $14.8M gain (285% ROI!)

- Stock at $32 on March 20: Calls worth $7.00, profit = $5.70/share × 40K = $22.8M gain (438% ROI!)

Probability assessment: 40% because multiple viable paths to $28-30 exist - M&A premium (most likely), split valuation rerating, or subscriber momentum + content execution. The $25 strike provides just 2.6% breakeven cushion, signaling high conviction this happens.

🎯 Base Case (35% probability)

Target: $23-$26 range (CONSOLIDATION WITH BIAS HIGHER)

Most likely scenario:

- ✅ M&A process extends: Decision delayed to Q1 2025, but confirmed active bidding keeps bid under stock

- 📱 Split on track: Form 10 filing shows solid Warner Bros. fundamentals but not spectacular

- 📊 Q4 earnings solid: Revenue $10.0-10.2B, subscribers add 6M, DTC EBITDA $700-800M

- 🎯 Max growth steady: Continues 6-7M quarterly adds but ARPU growth remains muted at 1-2%

- 🎬 Content pipeline progressing: Harry Potter on schedule for 2026, film slate performing

- 📉 Linear TV continues declining: 18-20% profit drop rate persists

- 💰 Debt reduction steady: $2-3B retired in 2025

- 🔄 Trading within ranges: Gamma support at $24 holds, resistance at $25-26 caps upside until catalyst

- 💤 Volatility stays elevated: Market awaits M&A clarity

This is the "hold and wait" scenario: Stock consolidates in $23-26 range, calls finish slightly in-the-money ($25.50-26.00) with modest profit, but no explosive move materializes. The $5.2M buyer makes 20-40% return but not the home run they're betting on.

Call P&L in Base Case:

- Stock at $25.50 on March 20: Calls worth $0.50, loss = -$0.80/share × 40K = -$3.2M loss (61% loss)

- Stock at $26.00 on March 20: Calls worth $1.00, loss = -$0.30/share × 40K = -$1.2M loss (23% loss)

- Stock at $26.50 on March 20: Calls worth $1.50, profit = $0.20/share × 40K = $0.8M gain (15% gain)

Why 35% probability: Stock near 52-week highs after 151% rally - some consolidation natural. M&A timing uncertain (could extend beyond March expiration). Split execution milestones may not occur until April-May. WBD needs catalyst to break above $25-26 resistance given already-explosive move.

📉 Bear Case (25% probability)

Target: $18-$23 (RETEST SUPPORT)

What could go wrong:

- 😰 M&A collapse: All bidders walk away citing regulatory concerns or valuation disconnect

- 🚨 Split execution issues: Debt allocation worse than expected, Warner Bros. standalone margins disappoint

- ⏰ Q4 earnings miss: Revenue below $10B, subscriber adds slow to 4-5M, DTC losses widen

- 📉 Linear TV accelerates decline: Profits drop 25-30% in Q1 2025 as cord-cutting intensifies

- 🇨🇳 Macro recession: Ad market collapses, enterprise streaming budgets cut

- 💸 Debt concerns: Credit downgrade to B+ triggers higher borrowing costs

- 🎬 Content disappointments: Harry Potter delayed, DC slate underperforms

- 🤖 Streaming competition: Netflix/Disney bundle aggressively, pressure subscriber growth

- 🔨 Break below $24 gamma support: Triggers cascade to $22-23, then $20

Critical support levels:

- 🛡️ $24.00: MUST HOLD - 39.7M net gamma (1.5% below current)

- 🛡️ $23.00: Secondary floor - 14.0M gamma (5.6% below current)

- 🛡️ $22.00: Deep support - 15.7M gamma (9.7% below current)

- 🛡️ $20.00: Disaster scenario - 11.7M gamma (17.9% below current)

Call P&L in Bear Case:

- Stock at $24.00 on March 20: Calls expire worthless (below strike), loss = -$1.30/share × 40K = -$5.2M (100% loss)

- Stock at $22.00 on March 20: Calls expire worthless, loss = -$5.2M (100% loss)

- Stock at $20.00 on March 20: Calls expire worthless, loss = -$5.2M (100% loss)

Probability assessment: 25% because it requires multiple negative catalysts to align. WBD's strategic catalysts (split, M&A interest, Max growth) remain intact. The massive $24 gamma support (39.7M) provides strong technical floor. However, execution risk is real and 151% YTD gain offers no valuation cushion for disappointment. If M&A collapses AND split details disappoint, rapid retracement to $20-22 is plausible.

💡 Trading Ideas

🛡️ Conservative: Wait for M&A Clarity, Then Buy Split Story

Play: Stay on sidelines until M&A decision announced (expected by Christmas), then evaluate entry

Why this works:

- ⏰ Binary catalyst weeks away: M&A announcement could gap stock +15-25% or -10-15% - too risky to front-run

- 💸 Already up 151% YTD: Zero margin of safety at current levels after parabolic rally

- 📊 Gamma resistance at $25: 105.2M net gamma creates mechanical ceiling - need catalyst to break through

- 🎯 Better entry post-announcement: If M&A fails, pullback to $22-23 provides 8-12% margin of safety

- ⏳ Split story plays out 2026: Plenty of time to participate in valuation unlock

Action plan:

- 👀 Watch for M&A announcement (expected around Christmas 2024)

- 🎯 If acquisition announced: Stock likely gaps to $26-28 immediately - miss the pop but validate thesis

- 📉 If M&A collapses: Look for pullback to $22-23 gamma support for stock entry (10% off highs)

- 📊 Monitor Q4 earnings: Feb 27 for subscriber trajectory, DTC profitability progress

- ⏰ Revisit in Q1 2025: When split Form 10 filing reveals Warner Bros. standalone financials

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -10-15% drawdown if M&A collapses. Get better entry if stock consolidates. Maintain optionality for split valuation rerating in 2026.

⚖️ Balanced: Post-M&A Decision Call Spread (Defined Risk)

Play: After M&A decision, sell call spread to reduce cost and define risk

Structure: Buy $25 calls, Sell $28 calls (March 20, 2026 expiration - SAME as the $5.2M trade)

Why this works:

- 🎢 Reduce cost: Selling $28 calls reduces net debit from $1.30 to ~$0.80-0.90

- 📊 Defined risk spread: $3 wide = $300 max profit, ~$90 max risk per spread (3.3:1 reward/risk)

- 🎯 Target realistic move: $25-28 range captures M&A premium or split rerating without requiring moon shot

- 🤝 Copy smart money structure: Using same strike and expiration as $5.2M institutional trade

- ⏰ 106 days: Gives time for split Form 10 filing, Q4 earnings, Harry Potter updates

- 🛡️ Caps upside at $28: Acceptable tradeoff for 40% cost reduction

Estimated P&L:

- 💰 Pay ~$0.80-0.90 net debit per spread (vs $1.30 for naked call)

- 📈 Max profit: $210-220 if WBD above $28 at March expiration (240% ROI)

- 📉 Max loss: $80-90 if WBD below $25 (defined and limited)

- 🎯 Breakeven: ~$25.80-25.90

- 📊 Risk/Reward: 2.4:1 which is excellent for defined-risk bullish play

Entry timing:

- ⏰ Ideal entry: After M&A decision announced (clarity on strategic direction)

- 🎯 Enter if stock trades $24-25 range (gives room to work)

- ❌ Skip if stock already above $26 (spread too close to max profit)

Position sizing: Risk 3-5% of portfolio per spread (directional speculation with favorable R/R)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

Expected outcome: 100-150% return if split details/M&A drives WBD to $26-28 by March. Full loss if stock fails to break $25.

🚀 Aggressive: Copy The Whale - Naked $25 Calls (ADVANCED!)

Play: Buy same calls as the $5.2M institutional trade - naked long calls betting on transformational catalysts

Structure: Buy $25 calls (March 20, 2026 expiration)

Why this could work:

- 💥 M&A bidding war: Multiple credible bidders (Comcast, Netflix, Paramount) could drive premium above $27-30

- 🎰 Split valuation unlock: Warner Bros. entity could be valued $25-35B standalone (vs $8-10B implied currently)

- 📊 Gamma squeeze potential: Breakout above $25 triggers 105.2M gamma hedge buying

- 🚀 Multiple paths to $28-30: M&A, split rerating, subscriber momentum, content wins

- ⚡ Leverage: Calls provide 4-6x leverage to stock moves above $25

- 📈 Smart money validated: $5.2M institutional bet suggests high-conviction view

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Calls cost $1.30 ($130 per contract, $13,000 per 100 contracts)

- ⏰ TIME DECAY: Theta burns value daily as March expiration approaches

- 😱 CATALYST DEPENDENT: If M&A collapses AND split disappoints, could lose 70-100%

- 📊 Already up 151% YTD: Limited margin for error after explosive rally

- 🎢 Binary outcomes: This is pure event-driven speculation, not investing

- ⚠️ Breakeven at $26.30: Need 8% move from current $24.37 just to break even

Estimated P&L:

- 💰 Cost: $1.30 per call ($130 per contract)

- 📈 Modest win: Stock at $27 = $2.00 call value = $0.70 gain (54% ROI)

- 🚀 Big win: Stock at $30 = $5.00 call value = $3.70 gain (285% ROI)

- 🌕 Home run: Stock at $32 = $7.00 call value = $5.70 gain (438% ROI)

- 📉 Loss scenario: Stock at $24 = $0 call value = -$1.30 loss (100% loss)

- 💀 Total loss: Stock below $25 at expiration = lose entire premium

Breakeven point: $26.30 (need 8.0% rally from current levels)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand you're betting on SPECIFIC catalysts (M&A or split) materializing

- ✅ Can afford to lose ENTIRE premium (25% probability in bear case!)

- ✅ Have conviction on M&A announcement driving stock above $26 by March

- ✅ Accept this is speculation, not investing - binary event-driven trade

- ✅ Can monitor position and take profits at $27-28 (don't hold for max gain)

- ⏰ Have 3-6 month time horizon and won't panic sell on -10% stock moves

Position sizing: Risk ONLY 1-3% of portfolio (this is pure speculation)

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~45% (based on bull + base case scenarios)

Expected outcome: This trade is a PURE BET on transformational catalysts. If M&A materializes at $27-30 or split details show Warner Bros. worth $25-30B standalone, this could return 200-400%. If neither happens by March, expect 50-100% loss. Only for traders willing to risk $13,000 to make $26,000-50,000.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ M&A timing uncertainty (High Risk): While decision expected "around Christmas 2024," the March 20 call expiration provides only 106 days. If board requests third bidding round or regulatory review extends timeline, announcement could slip to Q2 2025 - AFTER expiration. Process could collapse entirely if bidders can't agree on price or regulatory approval seems unlikely. Paramount claims process is "tainted" suggesting potential legal challenges.

-

💸 Valuation after 151% YTD rally (High Risk): Trading at $24.37 near 52-week high of $24.76 after gaining 2.5x in 12 months. This explosive move ALREADY prices in significant catalyst expectations. At current levels, WBD trades at ~1.5x sales - if M&A fails AND split details disappoint, rapid retracement to $18-20 (where it traded in August) is possible. Zero margin of safety for any execution stumbles.

-

📉 Irreversible linear TV decline (High Risk): Cable networks suffering 20% profit declines, 9% subscriber losses, and $9.1B asset write-down forced S&P's junk bond downgrade. The Discovery Global spinoff inherits ~$38B debt attached to DECLINING cash flow assets. If linear TV deteriorates faster than Max can compensate (Q4 ad revenue down 16%), the combined entity's value proposition erodes. This is a melting ice cube that's melting faster than expected.

-

🎯 Split execution risk (Medium-High Risk): Mid-2026 separation carries MAJOR complexity - debt allocation between entities, managing transition without disrupting operations, achieving cost synergies. Form 10 filing (expected Q1 2025) could reveal Warner Bros. standalone margins LOWER than market expects, crushing valuation thesis. What if Warner Bros. shows $8B revenue but only $1B EBITDA (12.5% margins vs. expected 25-30%)? Entire bull case collapses.

-

💰 Streaming profitability still elusive (Medium Risk): Despite record subscriber adds, free cash flow DOWN 28% to $4.4B as content spending surges. Global ARPU of $7.84 up just 1% YoY despite price increases - can't pass through inflation. International expansion adding low-ARPU subscribers ($4.05) dilutes average. Path to sustained profitability unclear - Netflix achieves $6-7 ARPU globally, WBD struggling at similar levels with smaller scale.

-

🦈 Competition from Netflix, Disney intensifies (Medium Risk): Netflix has 282.7M subscribers (2.5x WBD's 110.5M) with superior content budget and technology platform. Bernstein analyst calls Disney "only credible challenger to Netflix" and describes WBD as "sub-scale DTC" with 80% exposure to legacy businesses. Lost NBA rights removes key differentiator - what happens when Netflix launches NFL/NBA live sports?

-

🎬 Content execution risk (Medium Risk): Superman delivered solid $503M box office, but Q3 box office down 40% YoY in "Barbie-less" summer shows volatility. Harry Potter TV series is MASSIVE bet - what if production quality disappoints, casting controversies emerge, or J.K. Rowling involvement creates backlash? DC Universe reboot under Gunn requires multiple hits to work - one flop (like The Flash) could derail momentum. Dependence on tentpoles creates binary outcomes.

-

🏦 Debt burden limits flexibility (Medium Risk): Despite $16.6B retired since merger, still carrying $38B at 3.8x leverage with BB+ junk bond rating. Interest expenses consume cash that could fund content/M&A. In recession, refinancing risk increases and borrowing costs spike. Discovery Global entity inherits bulk of debt with declining linear cash flows - potential death spiral if ad market collapses.

-

💼 CEO insider selling signal (Low-Medium Risk): David Zaslav's $30M stock sale in December 2024 at $11.73 (now $24.37 = 2.08x higher) raises eyebrows. While characterized as "tax planning," selling 2.6M shares ahead of transformational catalysts suggests either confidence issues OR expectations sale won't materially exceed current levels. If CEO who knows EVERYTHING about M&A process sold at $11.73, why are we buying calls at $24.37?

-

📊 Gamma resistance at $25 creates ceiling (Medium Risk): Massive 105.2M net gamma at $25 strike (107.3M call gamma) means market makers systematically SELL into rallies to hedge exposure. This creates mechanical selling pressure making breakouts difficult without MAJOR catalyst. Would need sustained institutional buying or M&A announcement to overcome. Current price $24.37 sitting just 2.6% below this ceiling.

-

🎢 Binary catalyst creates whipsaw risk (High Risk): M&A announcement (or failure) is PURE BINARY - stock could gap +20% on $28 acquisition or -15% on deal collapse in SINGLE DAY. The March calls either go to $3-5 (if catalyst hits) or $0 (if it fails). No middle ground. This isn't gradual appreciation - it's lottery ticket that either pays big or expires worthless. Most retail traders can't stomach this volatility.

🎯 The Bottom Line

Real talk: Someone just spent $5.2 MILLION on a leveraged bet that WBD breaks above $25 by March as transformational catalysts unfold. This isn't a hedge or income play - this is pure directional speculation on M&A announcement and/or business split valuation unlock.

What this trade tells us:

- 🎯 High conviction on catalysts: Institutional player expects M&A decision (Christmas timeline) OR split Form 10 filing (Q1 2025) to drive stock through $25-26 resistance

- 💰 Betting on premium valuation: $25 strike only 2.6% above current suggests they expect $27-30 target (acquisition premium or split rerating)

- ⚖️ Timing is critical: March 20 expiration captures M&A announcement window, Q4 earnings, split filing milestone

- 📊 Risk/reward attractive: Paying $1.30 for potential $3-5 payoff (230-385% upside) vs 100% downside if wrong

- ⏰ Patient capital: 106 days gives time for multiple catalyst attempts to materialize

This IS a "something big is coming" signal - institutional money doesn't deploy $5.2M on hopes and dreams.

If you own WBD:

- ✅ Hold through M&A announcement: Decision expected around Christmas 2024 (weeks away!)

- 📊 Set mental stop at $23 (gamma support) to protect if M&A collapses

- 🎯 Take profits at $27-28: Don't get greedy - 151% YTD gain is already incredible

- ⏰ Watch for Form 10 filing: Q1 2025 reveals Warner Bros. standalone financials (make-or-break for valuation thesis)

- 🛡️ Consider selling some $28-30 calls against stock to cap upside and collect premium

If you're watching from sidelines:

- ⏰ Wait for M&A decision: Binary catalyst too risky to front-run from current levels

- 🎯 If M&A announced: Stock gaps to $26-28 immediately - validate thesis but entry less attractive

- 📉 If M&A collapses: Look for pullback to $22-23 for stock entry (10% off highs, strong gamma support)

- 🚀 Longer-term (6-12 months): Business split execution and Warner Bros. standalone valuation are legitimate catalysts for $28-32

- ⚠️ Current valuation (1.5x sales) requires perfect execution - one stumble and it's back to $18-20

If you want to trade it:

- 🎯 Conservative: Wait for M&A clarity, then buy stock at $22-24 on any dip (split story plays out 2026)

- ⚖️ Balanced: Post-M&A decision, buy $25/$28 call spread for defined risk (40% cheaper than naked calls)

- 🚀 Aggressive: Copy the whale - buy naked $25 calls betting on $27-30 (ONLY for advanced traders willing to lose 100%)

- ⏰ Timing is EVERYTHING: M&A announcement (Christmas) or split filing (Q1) are the catalysts

- 📉 Watch for break below $24 - that triggers pullback to $22-23

Mark your calendar - Key dates:

- 📅 December 24, 2024 (estimated) - M&A decision announcement expected "around Christmas"

- 📅 February 27, 2025 - Q4 2024 earnings report (subscriber trajectory, DTC profitability, 2025 guidance)

- 📅 Q1 2025 (Jan-Mar) - Form 10 filing expected revealing Warner Bros. standalone financials

- 📅 March 20, 2026 - Expiration of this $5.2M call trade

- 📅 Mid-2026 (May-July) - Business split completion expected

- 📅 2026 - Harry Potter TV series premiere on Max

Final verdict: WBD's transformational story remains INCREDIBLY compelling - multiple credible M&A bidders, planned business split unlocking $15-20B in value, Max subscriber momentum (7.2M quarterly adds), and Harry Potter franchise revival are all real catalysts. BUT, at $24.37 after 151% YTD gain with M&A timing uncertain, the risk/reward is BINARY - not balanced.

The $5.2M institutional call buy is a CLEAR signal: smart money is betting something BIG happens by March. Either you believe in the catalysts and take the bet (knowing you could lose 100%), or you wait for clarity and potentially miss the initial pop.

This is a high-conviction, high-risk, event-driven trade. Only participate if you understand you're buying a lottery ticket that either pays 200-400% or expires worthless. There is no in-between.

Be bold, but be careful. This is not a stock for widows and orphans. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 103.37x unusual score reflects this specific trade's size relative to recent WBD history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. M&A processes create binary event risk with potential for 15-25% gaps either direction. The call buyer may have complex portfolio strategies or information not available to retail traders.

About Warner Bros. Discovery: Warner Bros. Discovery, Inc. is a global media and entertainment conglomerate formed by the 2022 merger of WarnerMedia and Discovery Communications, with a market cap of $60.88 billion operating HBO Max streaming, Warner Bros. film and television studios, and cable networks including CNN, TNT, Discovery, HGTV, and Food Network across the Cable & Other Pay Television Services industry.