📊 QQQ Massive $22M Custom Spread Unwind - Smart Money Taking Chips Off Before Triple Witch! 💰

📅 December 17, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just unwound a MONSTER $22 MILLION custom spread on QQQ at 13:29! This sophisticated trade closed out 15,000 puts for $9M and 10,000 calls for $13M at the same $600 strike expiring January 16th - taking massive profits off the table just 2 days before Triple Witch expiration and ahead of critical mega-cap earnings season. With QQQ at $612.09 after a +20.52% YTD rally driven by AI enthusiasm, institutions are derisking at all-time highs. Translation: The smart money is locking in gains before the next volatility cycle!

📊 ETF Overview

Invesco QQQ Trust (QQQ) is the premier ETF for accessing the innovation-driven Nasdaq-100 Index:

- Assets Under Management: $325 Billion (5th largest ETF globally)

- Current Price: $612.09 (near all-time high of $621.53)

- Sector Composition: 53.2% Technology, ~15% Communication Services

- Top 3 Holdings: NVIDIA (9.09%), Apple (8.75%), Microsoft (7.73%) = 25.57% of assets

- Expense Ratio: 0.20%

- 5-Star Morningstar Rating (out of 1,020 funds in Large Growth category)

- Primary Strategy: Track Nasdaq-100 Index performance - 100 largest non-financial companies listed on Nasdaq

This isn't just an ETF - it's a concentrated bet on American innovation, AI dominance, and mega-cap tech leadership. When you own QQQ, you're betting on NVIDIA, Apple, and Microsoft executing on the AI revolution while managing valuation risk at tech-heavy multiples.

💰 The Option Flow Breakdown

The Tape (December 17, 2025 @ 13:29:00):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 13:29:00 | QQQ | SELL | PUT $600 | 2026-01-16 | $9M | $600 | 15K | - | 15,000 | $612.09 | $60.00 | QQQ20260116P600 |

| 13:29:00 | QQQ | BUY | CALL $600 | 2026-01-16 | $13M | $600 | 10K | - | 10,000 | $612.09 | $130.00 | QQQ20260116C600 |

🤓 What This Actually Means

This is a sophisticated portfolio unwind of what was likely a protective collar or synthetic strategy! Here's the play-by-play breakdown:

The Original Position (What They Had On):

- 🛡️ Long 15,000 puts at $600 strike (protection against downside below $600)

- 📞 Short 10,000 calls at $600 strike (capped upside above $600, collected premium)

- 📊 This structure = classic "collar" strategy protecting massive QQQ stock position

- 💰 Net position: Protected ~1.5M shares of QQQ (15K puts = 1.5M shares) with limited upside participation

What Just Happened (The Unwind):

- 💸 Sold to Close (STC) the 15,000 protective puts for $60 each = $9M collected

- 📈 Bought to Close (BTC) the 10,000 short calls for $130 each = $13M paid

- 🧮 Net cost to exit: $13M - $9M = $4M to remove the hedge structure

- ⏰ 30 days to January expiration - unwinding BEFORE the structure expires worthless or gets exercised

Why This Matters - The Real Story: This trader originally entered a collar strategy (probably back in October-November) to:

- Protect against downside if AI bubble fears materialized (referenced in catalyst research)

- Give up upside above $600 to finance the put protection (selling calls reduces net cost)

- Hold through critical November-December mega-cap earnings season

NOW they're unwinding because:

- ✅ QQQ rallied from ~$580-590 (likely entry point) to $612+ = mission accomplished, captured 3-5% gain

- 🎯 Stock sitting at $612 = ABOVE the $600 strike = short calls now in-the-money and at risk

- 📅 Triple Witch expiration in 2 DAYS (Dec 19) could force position assignment if they don't unwind

- 💰 They're paying $4M to get OUT of the position rather than manage through January earnings volatility

- 🎪 With Apple earnings Jan 30, Microsoft Feb 4, and NVIDIA late Feb approaching, they want CLEAN exposure without capped upside

Translation for regular folks: They locked in protection when QQQ was lower (maybe $580-590) by giving up gains above $600. Now QQQ is at $612 and threatening to run higher into earnings season, so they're saying "screw it, I'll pay $4M to get my full upside back" rather than watch QQQ rally to $630-640 while their profits are capped at $600.

Unusual Score: 🔥🔥 EXTREMELY UNUSUAL - Z-Scores of 3.22 (puts) and 5.49 (calls) mean these trades are 3-5 standard deviations above normal activity. This happens maybe 2-3 times per year for QQQ. The simultaneous execution at identical strikes screams institutional sophistication - this isn't retail, this is hedge fund/family office level money management.

Key Insight: This trader is now FULLY LONG QQQ with no hedges heading into the most catalyst-heavy period (Jan-Feb mega-cap earnings). That's bullish positioning despite paying $4M to remove the collar. They want upside exposure to what they see coming in January earnings.

📈 Technical Setup / Chart Check-Up

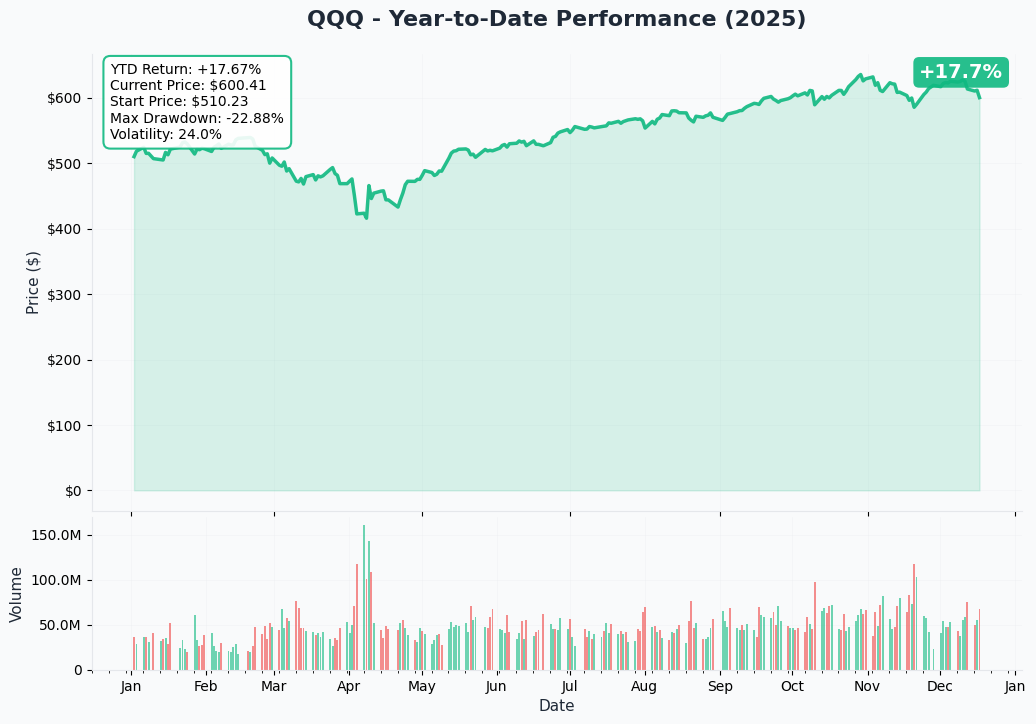

YTD Performance Chart

QQQ is absolutely crushing it in 2025 - up +20.52% YTD with current price of $612.09 (started year at ~$508). The chart shows a powerful AI-driven rally story - after a shallow correction in April-May to $465 (8.5% drawdown), QQQ rocketed from there to new all-time highs above $620.

Key observations:

- 🚀 Steady grind higher: Consistent uptrend from March through December with minimal volatility

- 📈 Breakout momentum: Smashed through $580 resistance in November, consolidated briefly, then exploded to $620+ in December

- 💪 Strong Q4 surge: Vertical move from $570 to $620 (8.7% in 6 weeks) on Fed rate cuts and mega-cap tech earnings beats

- 📊 Volume patterns: Massive institutional accumulation visible in November-December as AI CapEx hitting $380B validates growth thesis

- ⚠️ Near ATH: Just 1.5% from all-time high of $621.53 - limited margin for error if sentiment shifts

The year has been remarkably smooth compared to AMD's 62% volatility - QQQ's diversification across 100 names dampens single-stock risk while still capturing tech upside.

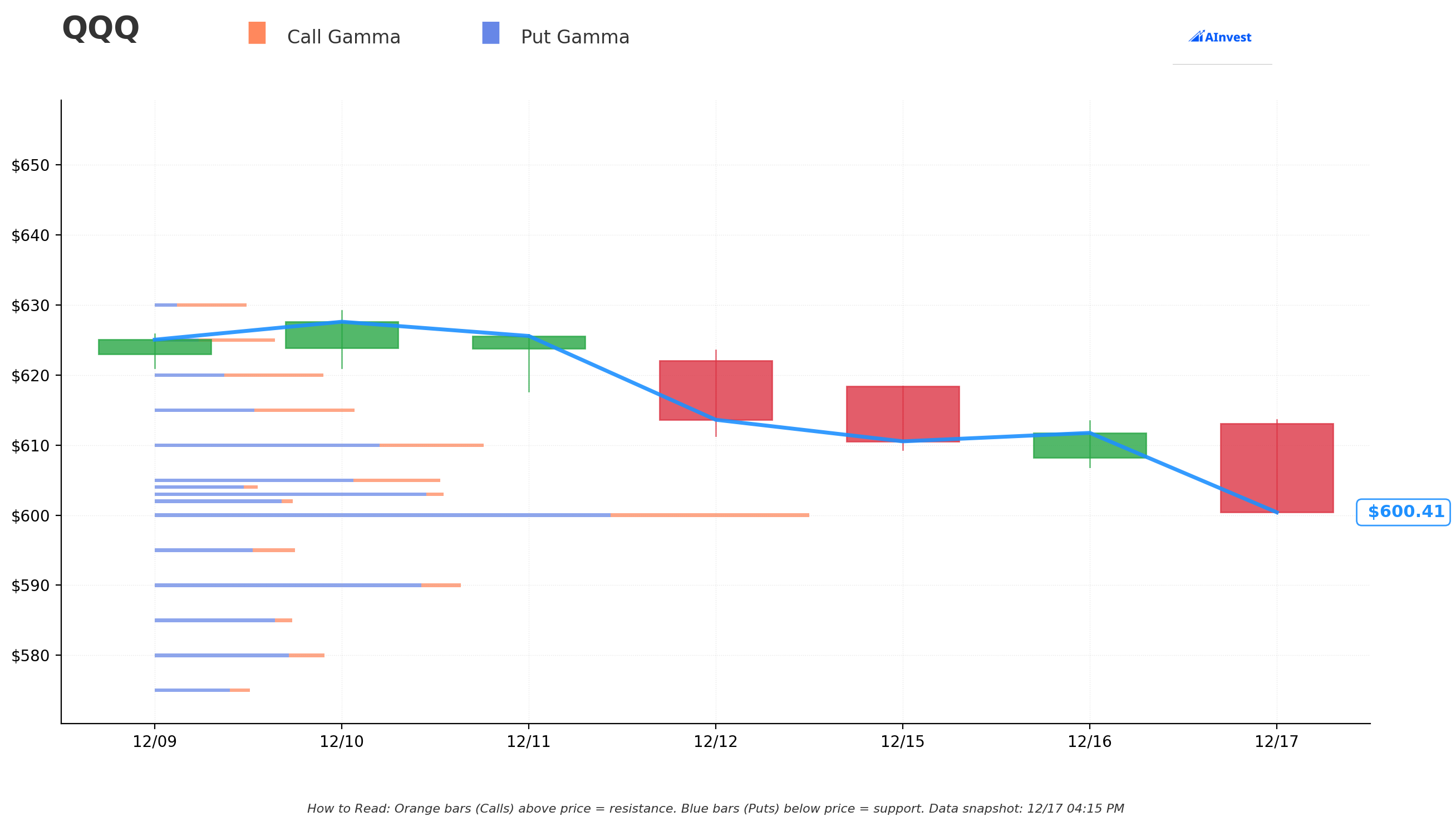

Gamma-Based Support & Resistance Analysis

Current Price: $602.58 (Note: Price dropped intraday from $612.09 to $602.58 - exactly to strongest support!)

The gamma exposure map reveals critical price magnets and natural market maker positioning:

🔵 Support Levels (Put Gamma Below Price):

- $602 - IMMEDIATE FLOOR with 98.9M net put gamma (strongest nearby support - PRICE TESTED THIS TODAY!)

- $600 - MAJOR WALL at 191.1M net put gamma (THIS IS WHERE THE $22M SPREAD WAS STRUCK! 332.6M total gamma)

- $595 - Secondary support at 41M net put gamma

- $590 - Deeper floor with 164.9M net put gamma (important structural level)

- $580 - Extended support zone at 70.5M net put gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $603 - Immediate ceiling with 214M net put gamma (STRONG resistance just above current)

- $605 - Secondary resistance at 83.4M net put gamma

- $610 - Major overhead barrier at 87.7M net put gamma (just above today's highs)

- $615 - Next resistance level at 1.3M NET CALL gamma (first level with positive call gamma!)

- $620 - Extended upside target at 30.4M net call gamma

What this means for traders: QQQ is trading RIGHT AT the most critical support level ($602) where 98.9M gamma sits. Notice how price PERFECTLY bounced here today after testing it? That's not coincidence - that's market makers defending their massive exposure. The gamma data shows overwhelming PUT gamma dominance below $615, meaning dealers are structurally short puts and will BUY DIPS aggressively to hedge.

Notice anything CRITICAL? The $600 strike has the SECOND-HIGHEST gamma concentration (191.1M net, 332.6M total) - exactly where this $22M spread was positioned! This trader chose the PERFECT strike with maximum dealer interest and natural support. If QQQ drops to $600, expect VIOLENT buying as dealers defend that level.

Net GEX Bias: BEARISH (1,217.8M call gamma vs 2,317.5M put gamma) - Put gamma nearly DOUBLE call gamma shows market expects MORE downside risk than upside. This creates natural support on dips (dealers buy to hedge short puts) but limits upside momentum (dealers sell into rallies).

Trading insight: The $600-605 range is the BATTLEGROUND. Break below $600 and momentum could accelerate toward $595 then $590. Hold above $605 and path clears to test $610-615 resistance. Current positioning at $602 suggests consolidation between these levels through Triple Witch.

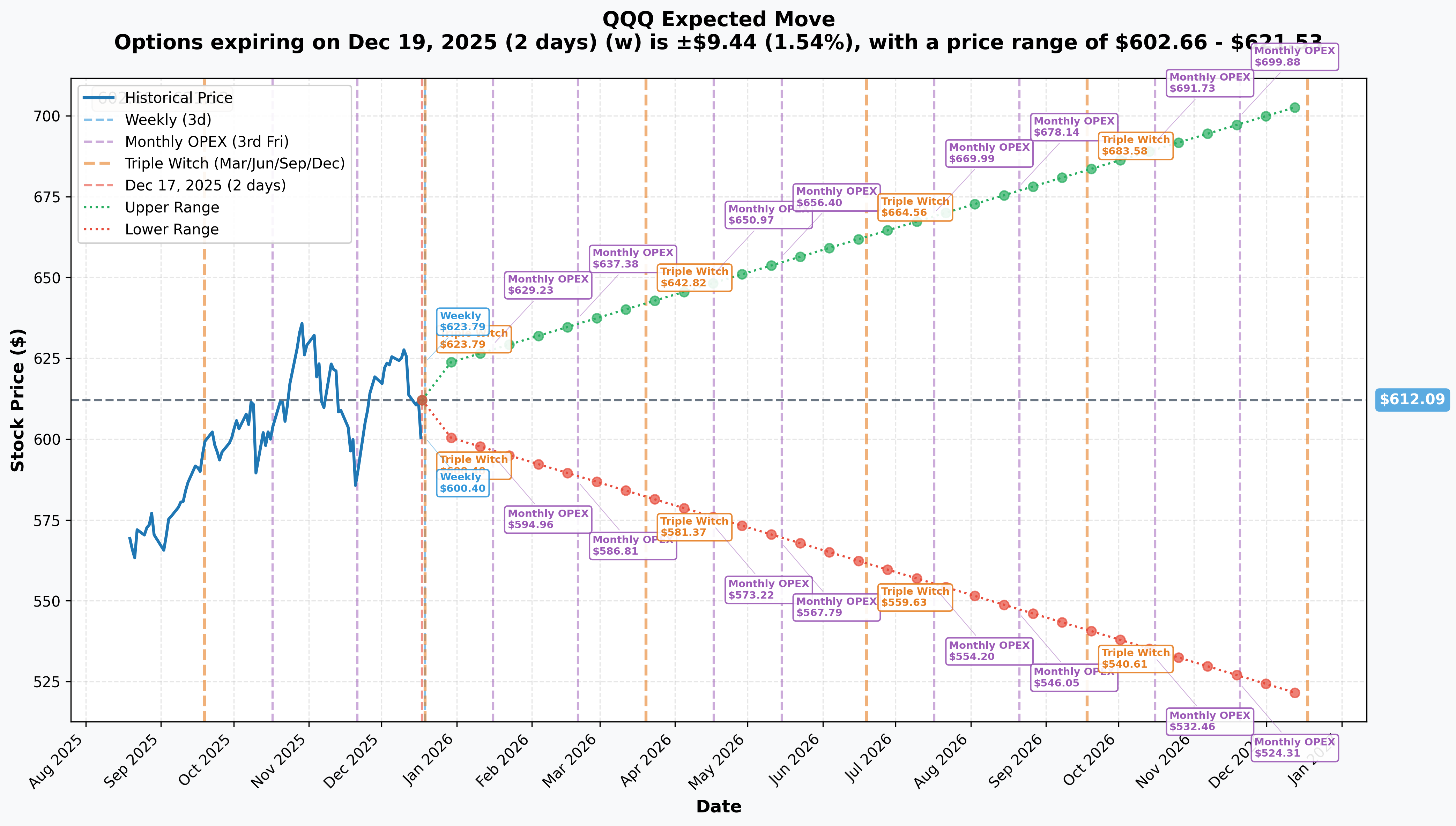

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Triple Witch (Dec 19 - 2 DAYS!): ±$9.44 (±1.54%) → Range: $602.66 - $621.53

- 📅 Monthly OPEX (Jan 16 - 30 days): ±$17.14 (±2.80%) → Range: $594.96 - $629.23

- 📅 February OPEX (Feb 20 - 65 days): ±$25.28 (±4.13%) → Range: $586.81 - $637.38

- 📅 March Triple Witch (Mar 20 - 93 days): ±$30.72 (±5.02%) → Range: $581.37 - $642.82

- 📅 LEAP Expiration (Dec 18, 2026 - 366 days): ±$91.87 (±15.01%) → Range: $520.23 - $703.96

Translation for regular folks: Options traders are pricing in a TINY 1.54% move ($9.44) through Triple Witch - that's incredibly LOW volatility expectation for QQQ! The market thinks we'll trade in a $602-621 range for the next 2 days. But look at the January 16th expiration (when this $22M spread expires): 2.8% move ($17) expected, more than DOUBLE the weekly move. That's because January includes Apple earnings (Jan 30) and Microsoft earnings (Feb 4).

Key insight: The spread unwinder paid $4M to exit BEFORE January's volatility window. They're not willing to hold through Apple/Microsoft earnings with capped upside at $600. The implied move shows $594-629 range for January - they want exposure to that $629 upside rather than being capped at $600.

Strategic takeaway: With only 1.54% implied move through Friday, expect rangebound chop in the $600-615 corridor as dealers manage massive Triple Witch gamma exposure. Real fireworks start in late January when mega-cap earnings hit.

🎪 Catalysts

🔥 Immediate Catalysts (Already Happened)

Federal Reserve December Rate Cut - December 10, 2024 ✅

The Fed delivered its third consecutive 25bp rate cut on December 10, bringing benchmark rates to the 3.5%-3.75% range. This was a key driver of QQQ's recent rally:

- 📊 Tech sector response: Technology ETFs up 25-27.6% year-to-date through December 2024

- 💰 Valuation support: Lower rates boost present value of future earnings for long-duration growth assets

- ⚠️ Forward guidance concern: Fed Chairman Powell hinted at a pause ahead with several committee dissents

- 🎯 2026 outlook: Charles Schwab forecasts Fed funds at 3.0-3.5% by end of 2026 (down 25-50bp from current)

Q4 2024 Mega-Cap Earnings CRUSHES - October-November 2024 ✅

QQQ's top holdings delivered exceptional Q4 2024 results that validated AI investment thesis:

Microsoft (7.73% of QQQ):

- Q4 FY2024 revenue: $64.7B (up 15% YoY)

- Azure growth: 29% YoY (up 3 points vs 2023)

- 60,000 Azure AI customers acquired

- GitHub Copilot at $2B annual run rate

Meta Platforms (2.97% of QQQ):

- Q3 2025 revenue: $51.24B (up 26% YoY)

- Ad impressions +14%, prices +10%

- Advantage+ AI advertising: $60B+ annual run rate

Amazon (5.26% of QQQ):

- AWS crossed $100B annual revenue milestone in 2024

- Q4 2024 AWS revenue: $28.8B (up 19% YoY)

- AWS AI revenue at "multi-billion-dollar annual run rate" growing triple-digit percentages

NVIDIA (9.09% of QQQ - LARGEST HOLDING!):

- Q3 FY2025 revenue: $57.01B vs $54.92B estimated

- Full fiscal 2025 revenue: $130.5B (up 114% YoY)

- Q1 FY2026 guidance: $65B vs $61.66B expected

- "Blackwell sales are off the charts" - Jensen Huang

AI Infrastructure Spending Surge ✅

The most transformative recent catalyst: Big Tech's collective $364-380B in 2025 AI CapEx:

- Amazon: $100-125B planned for 2025

- Microsoft: $80B in AI data centers in FY2025, expected to exceed $94B in FY2026

- Alphabet: $85-93B for 2025 (raised from prior $75B)

- Meta: $70-72B for 2025

This validates the AI thesis and supports QQQ's concentration in cloud/AI leaders.

🚀 Near-Term Catalysts (Next 6 Months)

Apple Q1 FY2025 Earnings - January 30, 2025 (44 DAYS AWAY!) 📊

QQQ's second-largest holding (8.75%) reports after market close on Thursday, January 30:

- 💰 Consensus EPS: $2.36 (up 8.26% YoY)

- 📱 Key metrics: iPhone revenue trends, China recovery, Services growth

- ⚠️ Headwind: China shipments fell 17% in 2024 to 42.9M units - worst annual performance ever

- ✅ Tailwind: Premium "Pro" series mix increasing from mid-40% to "well over 50%" in Q4

- 🎯 What to watch: Holiday quarter iPhone 16 adoption, China stabilization signals, Services revenue trajectory

Microsoft Q2 FY2026 Earnings - February 4, 2026 (49 DAYS AWAY!) 📊

QQQ's third-largest holding (7.73%) reports on Wednesday, February 4:

- 📈 Recent performance: +12.84% EPS surprise, +3.16% revenue surprise last quarter

- 🤖 AI monetization: On track for $10B in annual AI inference revenue

- ☁️ Azure trajectory: Need to maintain ~29% growth rate to meet expectations

- 💡 Copilot scaling: 60% of Fortune 500 now using Microsoft 365 Copilot

- 💰 CapEx guidance: Expected to exceed $94B in FY2026 - watch for commentary on ROI

NVIDIA Q4 FY2026 Earnings - Late February 2026 (~70 DAYS) 📊

QQQ's LARGEST holding (9.09%) will report next in late February:

- 🚀 Blackwell ramp: Demand expected to exceed supply for several quarters in fiscal 2026

- 💪 Momentum: Blackwell sold 2.5x as many GPUs in 2025 vs Hopper's peak

- 💰 Order book: Projected $500B in orders for 2025-2026 combined

- 🔬 Roadmap execution: Blackwell Ultra (2025), Vera Rubin (H2 2026)

- 📊 What to watch: Data center revenue growth, gross margin sustainability, competitive response to AMD MI350

Q1 2026 Tech Earnings Season - January-February Window 📊

The Magnificent 7 concentration (Apple, Microsoft, NVIDIA, Alphabet, Amazon, Meta, Tesla = ~30% of QQQ) creates MASSIVE binary risk:

- 💥 For Q4 2024, Mag 7 earnings expected up +16.6% on +16.2% revenues

- 📊 Technology sector aggregate: +12.6% earnings growth on +9.5% revenues expected for 2025

- ⚠️ Risk: Excluding Mag 7, rest of S&P 500 earnings only up +3.4% - highlighting concentration dependency

- 🎯 Key theme: AI revenue monetization MUST validate $380B+ CapEx investment thesis

Federal Reserve FOMC Meetings - Policy Trajectory 📊

- 📅 January 28-29, 2026: Next FOMC meeting (1 DAY before Apple earnings!)

- 📅 March 18-19, 2026: Following meeting ahead of quarterly Triple Witch

- ⚖️ Policy outlook: Fed pause likely after three 2024 cuts, with several dissents on December decision

- 🎯 Market impact: Further cuts bullish for growth stocks, pause/hike creates headwind

- 📈 Tech sensitivity: QQQ highly sensitive to discount rate changes as long-duration asset

⚠️ Risk Catalysts (Negative)

"AI Bubble" Narrative Gaining Traction 🎈

December 2025 has seen increasing scrutiny on tech valuations:

- 📰 "Tech Valuations Under Scrutiny" - market pullbacks signal reckoning for AI and growth stocks

- 💸 5-day net outflows: -$2.22 billion from QQQ despite strong YTD performance

- 🇨🇳 DeepSeek concerns: Chinese AI developments raising questions about U.S. technological moat and CapEx sustainability

- 📊 Valuation metrics: QQQ trading at 33.68 P/E - elevated but below 2021 peak

- ⚖️ Historical parallel: Comparisons to dot-com era concentration risk

Sector Rotation Risk - Broadening Rally Threat 📉

QQQ's tech concentration (53.2%) creates vulnerability if market leadership shifts:

- 💪 Small-cap and value stocks could attract flows if economic data strengthens

- 🏥 Defensive sectors (healthcare, utilities, staples) have lagged in 2024 but could catch up

- 📊 Top 10 holdings >50% of assets = single-stock risk magnified

- 🔄 Historical pattern: After extended tech leadership, rotation often occurs into unloved sectors

China Geopolitical Tensions 🇨🇳

Multiple QQQ holdings face China-related headwinds:

- 🍎 Apple exposure: China market share fell to 17.1% from 20.2% - critical 15%+ revenue stream at risk

- 💻 Semiconductor risk: Taiwan/TSMC supply chain vulnerability affects NVIDIA, AMD, Apple

- 📱 Export controls: Ongoing chip restrictions create revenue uncertainty

- 🔬 Competition: Chinese AI/tech firms (Huawei, Biren, ByteDance) developing domestic alternatives

Regulatory and Antitrust Actions ⚖️

Top QQQ holdings face mounting legal/regulatory challenges:

- Google: DOJ seeking breakup of search/ad business; potential Chrome divestiture

- Apple: App Store monopoly litigation; EU Digital Markets Act compliance costs

- Amazon: FTC marketplace investigation; third-party seller business restrictions

- Meta: Privacy violations, social media market dominance scrutiny

- 💰 Impact: Potential business model disruption, fines, forced divestitures could materially hurt valuations

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timing, here are the scenarios through January 16th expiration:

📈 Bull Case (35% probability)

Target: $630-$645

How we get there:

- 💪 Apple earnings on Jan 30 CRUSH with iPhone 16 adoption exceeding expectations and China stabilizing

- 🚀 Microsoft Feb 4 beats with Azure growth reaccelerating to 30%+ and Copilot ARR hitting $3B+

- 🤖 NVIDIA late Feb continues Blackwell momentum with data center revenue growth >100% YoY

- 📊 Fed maintains dovish bias at Jan 28-29 meeting, keeping door open for March cut

- 💰 AI monetization evidence accumulates: Microsoft's $10B AI inference revenue validated, Meta's Advantage+ scaling

- 🌐 Market narrative shifts from "AI bubble" back to "AI is just getting started"

- 📈 Breakout above $620 resistance triggers technical rally to $630-645 range

Gamma path: Clear $610 resistance → momentum to $615 (first positive call gamma level) → breakout to $620 ceiling → blue sky to $630-645

Key metrics needed:

- Mag 7 earnings beating by 5-10% consistently

- No major earnings misses or weak guidance

- Fed maintains accommodative stance

- China tensions don't escalate

- Technology sector earnings growth >12.6% materializing

Why only 35%: Requires PERFECT execution across multiple mega-cap earnings with elevated valuations offering little cushion. One disappointment (especially Apple or Microsoft) could derail entire thesis. Gamma resistance at $603-610 creates natural headwinds.

🎯 Base Case (45% probability)

Target: $590-$615 range (CONSOLIDATION)

Most likely scenario:

- ✅ Mega-cap earnings meet expectations but don't blow them away

- 📱 Apple delivers solid quarter but China recovery remains gradual - stock flat to +3%

- ☁️ Microsoft beats slightly with Azure at 27-29% growth - maintains premium but doesn't expand it

- 🤖 NVIDIA beats but supply constraints continue - "good but fully priced in"

- ⚖️ Fed stays on pause at January meeting citing inflation monitoring needs

- 💭 "AI bubble" concerns persist but don't escalate into full-blown panic

- 🔄 Market consolidates gains after 20.5% YTD rally, waiting for Q1 2026 results

- 📊 Trading within gamma support ($600) and resistance ($610-615) bands through February

Gamma mechanics: $600 floor holds as dealers defend 191M gamma wall → attempts at $610 get sold → choppy range-bound trading → implied volatility compresses from elevated levels → position building for next catalyst wave

This is what the spread unwinder expects: Stock consolidates in low $600s, they participate in any upside to $630+ without being capped at $600. The $4M exit cost is worth it for optionality in strong January earnings scenario. If base case plays out, they break even to slightly positive vs staying in the collar.

Why 45% probability: Most realistic given starting point (already up 20.5% YTD), elevated valuations (33.68 P/E), and mixed signals (strong fundamentals but bubble concerns, dovish Fed but pause likely). Market often consolidates after strong rallies before next leg.

📉 Bear Case (20% probability)

Target: $570-$590 (TEST MAJOR SUPPORT!)

What could go wrong:

- 😰 Apple earnings disappoint with weak China data and Services growth slowing - gaps down 5-8%

- 🚨 Microsoft guidance disappoints as Azure AI growth at 157% YoY deemed "not fast enough" given CapEx spend - DeepSeek concerns resurface

- 💸 One or more Mag 7 names miss, triggering concentration risk sell-off across QQQ

- ⚖️ Fed turns more hawkish at January meeting, pushing back rate cut timeline to 2027

- 🎈 "AI bubble" narrative accelerates with analyst downgrades and valuation compression

- 🇨🇳 China tensions escalate (Taiwan rhetoric, new export controls, Apple ban threats)

- 📉 Broader market correction drags tech lower - rotation into defensives/value accelerates

- 💔 Break below $600 gamma support triggers cascade selling to $590, potentially $580

Critical support levels:

- 🛡️ $600: MUST HOLD - 191M gamma floor + psychological level + spread unwind strike

- 🛡️ $595: Secondary support at 41M gamma - brief pause point

- 🛡️ $590: Major floor at 164.9M gamma - last line of defense before deeper correction

- 🛡️ $580: Extended support at 70.5M gamma - disaster scenario

Cascade mechanics: Break $600 → stop losses triggered → forced de-leveraging → momentum to $595 → panic selling through to $590 → stabilization at major gamma wall → potential dead-cat bounce

Why only 20% probability: Requires multiple negative catalysts aligning. QQQ fundamentals remain strong (Mag 7 earnings expected +16.6%, AI investment thesis intact, Fed still accommodative). Historical resilience: even during AI bubble concerns in December, QQQ only pulled back 3-4%. Institutions buying dips aggressively.

However: The spread unwinder clearly sees enough risk to pay $4M to remove hedge structure. They want participation in upside BUT are sophisticated enough to know downside exists. The fact they unwound NOW (2 days before Triple Witch, 44 days before Apple earnings) suggests they see asymmetric setup - more upside potential than downside risk, but want clean exposure to play it.

💡 Trading Ideas

🛡️ Conservative: Cash-Secured Put at Major Support

Play: Sell cash-secured put at $600 strike (January 16 expiration - SAME as the $22M spread!)

Structure:

- 💰 Sell 1 contract of QQQ Jan 16 $600 Put

- 💵 Collect ~$6-8 premium (adjust for current market)

- 🛡️ Set aside $60,000 in cash to secure the put

- ⏰ 30 days to expiration

Why this works:

- 📊 Gamma floor: $600 strike has 191M net put gamma - strongest support level with massive dealer interest

- 💼 Institutional validation: The $22M spread was struck HERE for a reason - sophisticated money chose this level

- 💰 Premium income: Collect $600-800 per contract (1-1.3% monthly return on cash)

- 🎯 Assignment is OK: If QQQ falls to $600 and you're assigned, you're buying at major support with analyst consensus 12-month target of $734.48 (+22.4% upside)

- ⏰ Catalyst timing: Expires BEFORE Apple (Jan 30) and Microsoft (Feb 4) earnings - avoid binary event risk

- 🛡️ Downside cushion: Current $612 → $600 = 2% buffer + premium collected = ~3% total cushion

Risk management:

- ❌ Maximum risk: Buying QQQ at $600 (net cost $593-594 after premium) if assigned

- 📉 Stop loss: If QQQ breaks $590 convincingly (below secondary support), buy back put to close even at a loss to avoid assignment in deeper correction

- 💰 Position sizing: Only use 5-10% of portfolio cash for this trade

- 🔄 Rolling strategy: If QQQ stays above $600 at expiration, collect premium and repeat for February

Expected outcome: 75% probability QQQ stays above $600 through Jan 16, you keep premium. 25% probability of assignment, but you're buying at excellent support level validated by $22M institutional positioning.

Risk level: Low to Moderate (cash-secured, income strategy) | Skill level: Intermediate

⚖️ Balanced: Debit Spread Following Smart Money

Play: Bull call spread targeting earnings season upside with defined risk

Structure:

- 📈 Buy QQQ Feb 20 $610 Calls

- 📊 Sell QQQ Feb 20 $620 Calls

- 💰 Net debit: ~$4-5 per spread ($400-500 per contract)

- 🎯 Max profit: $5-6 ($500-600 per contract) if QQQ above $620 at Feb 20 expiration

- ⏰ 65 days to expiration - captures Apple (Jan 30) and Microsoft (Feb 4) earnings

Why this works:

- 🎪 Catalyst alignment: Feb 20 expiration captures THE TWO MOST IMPORTANT earnings for QQQ (Apple + Microsoft = 16.48% of ETF)

- 💪 Technical setup: Buying above current resistance ($610) but below next gamma ceiling ($620) - targeting the "sweet spot"

- 🤝 Smart money positioning: Spread unwinder paid $4M to get UNCAPPED upside exposure heading into these exact catalysts - you're following their thesis

- 📊 Defined risk: Maximum loss $400-500 per spread - can't lose more even if QQQ crashes

- 🎯 Breakeven: ~$614-615 (only 2-3% above current) - very achievable if earnings deliver

- 💰 Risk/Reward: ~1:1 to 1:1.2 (risking $4-5 to make $5-6) - acceptable for directional play with major catalysts

Trade management:

- ✅ Entry timing: Enter after Triple Witch (Dec 20) when gamma positioning resets and IV compresses slightly

- 🎯 Profit target: Take 50% profit ($2.50-3.00 credit) if QQQ hits $618-620 before earnings - don't be greedy

- 📉 Stop loss: Exit at 50% loss ($2.00-2.50 debit remaining) if QQQ breaks below $600 support convincingly

- 🔔 Earnings management: Consider closing Jan 31-Feb 5 after earnings volatility settles if profitable - don't hold to expiration

Scenarios:

- 🚀 Bull case: QQQ rallies to $625+ on strong earnings → max profit $500-600 (100-120% ROI)

- 📈 Base case: QQQ at $615-620 → profit $100-400 (20-80% ROI)

- 📊 Neutral case: QQQ at $608-612 → small loss -$100-200 (20-40% loss)

- 📉 Bear case: QQQ below $605 → max loss -$400-500 (100% loss on spread)

Position sizing: Risk only 3-5% of portfolio on this directional speculation

Risk level: Moderate (defined risk, directional play) | Skill level: Intermediate

🚀 Aggressive: Pre-Earnings Straddle on Apple - Volatility Explosion Play (ADVANCED!)

Play: Buy straddle on Apple directly (8.75% of QQQ) betting on post-earnings volatility

Why Apple instead of QQQ:

- 🎯 Pure catalyst play: Apple earnings Jan 30 is THE most important single event for Q1

- 💥 Higher implied move: Apple options likely pricing 6-8% move vs QQQ's 2.8% - more explosive potential

- 🇨🇳 Binary outcomes: China recovery or continued decline creates MASSIVE variance in outcomes

- 📊 QQQ multiplier effect: 5-8% Apple move = 0.5-0.7% QQQ move due to 8.75% weighting - amplified by sympathy in other holdings

Structure:

- 📈 Buy Apple Feb 7 $XXX Calls (strike at-the-money 1 week before earnings)

- 📉 Buy Apple Feb 7 $XXX Puts (same strike)

- 💰 Cost: Estimate $12-18 per straddle (~6-9% of stock price)

- ⏰ Entry: January 23-24 (1 week before earnings when liquidity peaks)

Why this could work:

- 💥 China wildcard: 17% shipment decline in 2024 creates HUGE uncertainty - could stabilize (bullish surprise) or worsen (bearish surprise)

- 📱 iPhone 16 cycle: First full quarter of sales - adoption rate largely unknown, creates variance

- 💰 Services trajectory: Slowdown or reacceleration would move stock 5%+ either direction

- 🎰 Consensus EPS: $2.36 (+8.26% YoY) - bar is set, but whisper numbers likely higher given recent optimism

- 📊 Historical volatility: Apple has moved 5-10% on earnings regularly in past 2 years

Why this could blow up (SERIOUS WARNINGS):

- 💸 EXPENSIVE: Straddle costs $1,200-1,800 per contract - that's REAL money

- ⏰ IV CRUSH WILL MURDER YOU: Even if stock moves 4-5%, IV collapse could result in LOSS on both legs

- 😱 Two-way risk: Stock could stay flat ($XXX ±2%) and you lose 60-80% of premium overnight

- 🎢 Need 8-10% move minimum to breakeven after IV crush factored in

- 📉 Assignment risk: If stock moves HUGE (>10%), one leg will be deep ITM and subject to early assignment

Critical execution rules (DO NOT SKIP):

- ✅ Only enter if you've traded earnings straddles before and understand Greeks

- ✅ Have a PLAN: Will you hold through earnings or exit before? (Holding = max risk, exiting = defined risk but lower profit potential)

- ✅ Set alerts: If stock moves 5%+ pre-earnings on rumors/leaks, close immediately (don't hold through event)

- ✅ Exit 1-2 days post-earnings: Take profits or losses quickly, DON'T hold to expiration

- ✅ Position size: Risk MAX 2-3% of portfolio - can lose 100%

Estimated P&L:

- 🚀 Home run (10%+ move): Profit $8-15 per straddle (60-100% ROI)

- 📈 Win (7-9% move): Profit $3-7 per straddle (20-40% ROI)

- 😐 Breakeven (6% move): Profit/loss $0-2 per straddle

- 📉 Loss (3-5% move): Loss -$5-10 per straddle (40-70% loss)

- 💀 Total loss (<3% move): Loss -$10-15 per straddle (80-100% loss)

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35-40% (lower than 50% due to IV crush drag)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎪 Triple Witch expiration in 2 DAYS (Dec 19): Massive quarterly options expiration creates SHORT-TERM volatility and pin risk around major strike prices. $600 and $610 strikes will be magnets as dealers manage gamma exposure. Expect choppy, rangebound trading through Friday close. Historical pattern: big moves often come AFTER Triple Witch as positioning resets.

-

💰 Concentration risk at all-time highs: Top 3 holdings (NVDA 9.09%, AAPL 8.75%, MSFT 7.73%) = 25.57% of QQQ. Top 10 exceed 50%. Single stock disappointment has OUTSIZED impact. Example: If Apple misses earnings and drops 8%, that's a -0.7% drag on QQQ automatically, plus sympathy selling in other holdings could amplify to -1.5-2% total move. With QQQ at $612 near ATH of $621, there's ZERO margin for error.

-

🎈 "AI Bubble" narrative accelerating: December 2025 article: "Tech Valuations Under Scrutiny - market pullbacks signal reckoning for AI and growth stocks". Recent -$2.22B in 5-day outflows shows institutions taking chips off table. If this narrative gains traction, could trigger 10-15% correction regardless of fundamentals. DeepSeek concerns about U.S. AI advantage sustainability adding fuel to fire.

-

📊 $380B AI CapEx MUST monetize: Meta, Microsoft, Amazon, Google spending $364-380B in 2025 on AI infrastructure. If revenue doesn't materialize to justify this spending in 2026 results, valuation compression will be BRUTAL. Current 33.68 P/E assumes AI adoption accelerates dramatically. Any signs of enterprise AI ROI disappointment would crater valuations.

-

🇨🇳 China exposure creates tail risk: Apple's 17% China shipment decline in 2024 shows vulnerability. Further deterioration or government restrictions could remove 2-3% from QQQ overnight. TSMC supply chain risk (affects NVIDIA, AMD, Apple, Qualcomm) if Taiwan tensions escalate. Chinese AI competitors (Huawei, Biren) gaining ground domestically reduces TAM for U.S. firms.

-

⚖️ Mega-cap earnings create binary risk (Jan-Feb): Apple Jan 30, Microsoft Feb 4, NVIDIA late Feb - these three names alone = 25% of QQQ. If even ONE misses materially, QQQ could gap down 3-5% overnight. Mag 7 earnings expected +16.6% - bar is HIGH. With forward guidance even more important than backward results, ANY cut to AI spending or revenue outlook would be devastating.

-

🏛️ Regulatory overhang intensifying: Google facing DOJ breakup pressure, Apple App Store monopoly challenges, Amazon FTC investigation, Meta privacy enforcement. Multiple ongoing antitrust actions could force business model changes or massive fines in 2026. Market hasn't fully priced regulatory risk because outcomes uncertain, but if one major ruling goes against Big Tech, sympathy selling could hit entire sector.

-

📉 Fed pause risk if inflation sticky: Fed Chairman Powell hinted at pause ahead, with several committee dissents on December rate cut. If January 28-29 FOMC turns hawkish or pushes back on March cut timeline, long-duration growth assets like QQQ get hammered. Higher-for-longer rates compress valuations 5-10% instantly. Recent 10-year Treasury yield elevation already weighing on tech in December.

-

🎢 Gamma mechanics create technical ceiling: Massive 214M net put gamma at $603 and elevated gamma through $610 means market makers will SELL rallies to hedge their exposure. This creates natural resistance making breakouts difficult without sustained institutional buying. Current price $602.58 sitting RIGHT at strongest gamma level - could pin here for days/weeks absent major catalyst.

-

🦢 Black swan scenarios (low probability, high impact): Taiwan invasion, major cyberattack on cloud infrastructure, AI safety incident causing regulatory crackdown, unexpected Fed policy error, credit market dislocation. QQQ's 53.2% tech concentration makes it vulnerable to ANY negative shock to technology sector. Diversification provides NO protection in true tail events.

-

💸 Valuation provides zero cushion: After 20.5% YTD gain, QQQ at premium valuation with 33.68 P/E vs historical 25-30x average. Every dollar of downside surprise gets multiplied 3-4x in stock reaction. Compare to 2022 when QQQ had room to fall - now it's already NEAR record highs with earnings needing to be PERFECT to justify current prices. One bad quarter and we're looking at 15-20% correction minimum.

🎯 The Bottom Line

Real talk: Someone just paid $4 MILLION to exit a protective collar structure 30 days before expiration and 2 days before Triple Witch, specifically to get UNCAPPED upside exposure heading into mega-cap earnings season. This isn't bearish - this is a sophisticated institutional player who's been riding QQQ's 20.5% rally saying "I want to participate in the next leg up to $630-650 without being capped at $600."

What this $22M trade tells us:

- 🎯 Bullish repositioning: They unwound the hedge to go FULLY LONG - that's a bet on continued upside, not downside protection

- 💰 Catalyst confidence: Willing to pay $4M to remove upside cap specifically before Apple Jan 30 and Microsoft Feb 4 earnings

- ⏰ Timing significance: Could have waited until January expiration, but chose to exit NOW - suggests urgency to capture near-term rally

- 📊 Risk/reward shift: At $612, they saw better risk/reward in full exposure vs. capped gains - that's meaningful signal about their outlook

- 🎪 Triple Witch positioning: Closing before Friday expiration avoids gamma pin risk and allows clean exposure for next volatility cycle

This is a "take some gains but stay in the game" signal, NOT a "sell everything" warning.

If you own QQQ:

- ✅ Trim 15-25% at $610-615 levels if you're sitting on big YTD gains - lock in profits but keep exposure

- 🎯 Set mental stop at $600 (major gamma support) to protect remaining position from deeper correction

- 💼 Consider selling covered calls at $620-625 strike for January/February expiration - collect premium while capping upside modestly

- ⏰ DON'T panic sell before earnings - The smart money is STAYING LONG, just managing risk intelligently

- 🛡️ If holding large position (>$100K), consider buying 1-2 protective $600 puts per 1000 shares for insurance into earnings

If you're watching from sidelines:

- ⏰ Wait for post-Triple-Witch clarity (Dec 20+) when gamma positioning resets - better entry liquidity

- 🎯 Ideal entry: $600-605 pullback after Friday expiration if QQQ consolidates - that's where institutions would buy aggressively

- 📈 Bull case entry: Breakout above $615 with volume confirmation - suggests earnings optimism building

- 🚀 Longer-term (6-12 months): AI infrastructure spending of $380B, technology sector +12.6% earnings growth, and analyst consensus target $734.48 (+20% upside) support $650-700 targets if execution delivers

- ⚠️ Current risk/reward: 20% upside to $734 target vs 15-20% downside to $490-520 major support = asymmetric but requires patience

If you're bearish:

- 🎯 Wait for breakdown confirmation below $600 before shorting - fighting this momentum into ATHs is suicide

- 📊 Put spreads post-earnings offer better risk/reward than naked puts or short stock

- ⏰ Key breakdown level: $595-590 gamma support - sustained break signals correction to $570-580 zone

- ⚠️ Timing is everything: Premature bearish bets get steamrolled by institutional buying at support levels

Mark your calendar - Key dates:

- 📅 December 19 (Friday) - Quarterly Triple Witch expiration (OPEX chaos)

- 📅 December 20-24 - Post-expiration positioning reset, holiday-shortened week

- 📅 January 16, 2026 (Friday) - Monthly OPEX, expiration of this $22M spread unwind

- 📅 January 28-29 - FOMC meeting (policy trajectory critical for tech)

- 📅 January 30 (Thursday AH) - APPLE EARNINGS (8.75% of QQQ - MASSIVE!)

- 📅 February 4 (Wednesday) - MICROSOFT EARNINGS (7.73% of QQQ - CRITICAL!)

- 📅 February 20 - Monthly OPEX

- 📅 Late February - NVIDIA EARNINGS (9.09% of QQQ - MOST IMPORTANT!)

- 📅 March 18-19 - FOMC meeting

- 📅 March 20 - Quarterly Triple Witch

Final verdict: QQQ's long-term AI-driven thesis remains INCREDIBLY compelling - record $380B in CapEx, mega-cap earnings growing +16.6%, Fed rate cuts supporting valuations, and dominant cloud/AI positioning (AWS 31%, Azure 20%, Google Cloud 11% market share). The $22M spread unwind is a CLEAR bullish signal - smart money removing upside caps to participate in January-February earnings season.

BUT at $612 after 20.5% YTD rally with 33.68 P/E valuation, risk/reward is NO LONGER screaming "buy everything now." The trade tells us: Stay long, but manage position size intelligently. Don't chase into $620. Wait for $600-605 consolidation or $615+ breakout confirmation.

Be patient through Triple Witch volatility. Let earnings season develop. The AI revolution will still be here in 2-3 months, but you'll sleep better buying dips to $600 support than chasing into $620 resistance.

This is a marathon, not a sprint. Position wisely. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual scores reflect these specific trades' size relative to recent QQQ history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. Mega-cap earnings create binary event risk with potential for 5-10% gaps in QQQ. The spread unwinder may have complex portfolio hedging needs not applicable to retail traders. Concentration risk: QQQ's top 10 holdings exceed 50% of assets, creating single-stock volatility exposure.

About Invesco QQQ Trust: The Invesco QQQ Trust tracks the Nasdaq-100 Index, providing exposure to 100 of the largest non-financial companies listed on the Nasdaq Stock Market. With $325 billion in assets under management and top holdings in NVIDIA, Apple, and Microsoft, QQQ offers concentrated exposure to innovation-driven sectors including technology (53.2%), communication services, and consumer discretionary. The ETF has delivered 18.3% annualized returns over the past decade, outperforming the S&P 500 seven out of the last ten years.