FCX $1.1M Call Bet Ahead of Earnings - Smart Money Positioning for Copper Rally!

January 15, 2026 | Unusual Activity Detected

The Quick Take

Someone just dropped $1.1 MILLION on FCX April calls targeting the $70 strike - that's a 16.4% move higher from current prices! With Q4 earnings on January 22 (just 7 days away), the Grasberg Block Cave restart expected in Q2 2026, and copper hitting record highs above $13,000/tonne, this trader is betting big on the world's largest publicly traded copper producer. Translation: Institutional money sees upside in the copper supercycle story.

Company Overview

Freeport-McMoRan (FCX) is the world's largest publicly traded copper producer and a major gold and molybdenum miner:

- Market Cap: $80.93 billion

- Industry: Copper Ores Mining

- Current Price: $60.11 (near 52-week high of $60.64)

- Primary Operations: Grasberg mine (Indonesia), Morenci mine (Arizona - largest copper producer in North America), Cerro Verde (Peru)

The company sits at the intersection of multiple structural demand trends: AI data center buildouts requiring massive copper wiring, electric vehicle adoption (EVs use 3x more copper than traditional cars), and global grid infrastructure upgrades. With copper prices at all-time highs and supply constrained by the September 2025 Grasberg mudslide incident, FCX is positioned as the go-to proxy for copper exposure.

The Option Flow Breakdown

The Tape (January 15, 2026 @ 12:45:07):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:45:07 | FCX | MID | BUY | CALL $70 | 2026-04-17 | $1.1M | $70 | 5,100 | 349 | 4,960 | $60.11 | $2.16 |

What This Actually Means

This is a bullish directional bet on FCX rallying through the Q4 earnings catalyst and into the Grasberg restart timeline. Here's the breakdown:

- Premium paid: $1.1M ($2.16 per contract x 5,100 contracts)

- Target strike: $70 represents a 16.4% rally from current $60.11 price

- Strategic timing: 93 days to April 17 expiration captures Q4 earnings (Jan 22), potential Grasberg restart news (Q2 2026), and US copper tariff decision (June 2026)

- Volume vs OI: 5,100 volume against only 349 open interest = 14.6x ratio indicating new position opening

- Breakeven: Stock needs to reach $72.16 by expiration for this trade to profit

What's really happening here: This trader is making a levered bet that copper's supercycle momentum will push FCX through current all-time highs. At $2.16 per contract, they're paying about 3.6% of the stock price for the right to participate in upside above $70. If FCX reaches $75 by April, these calls would be worth ~$5.00 (131% gain). If FCX reaches $80, they'd be worth ~$10.00 (363% gain). The risk? If FCX stays below $70, the entire $1.1M premium evaporates.

Vol/OI Ratio: 14.6x indicates HIGH ACTIVITY - this isn't normal hedging, this is a conviction directional bet opening a new position.

Technical Setup / Chart Check-Up

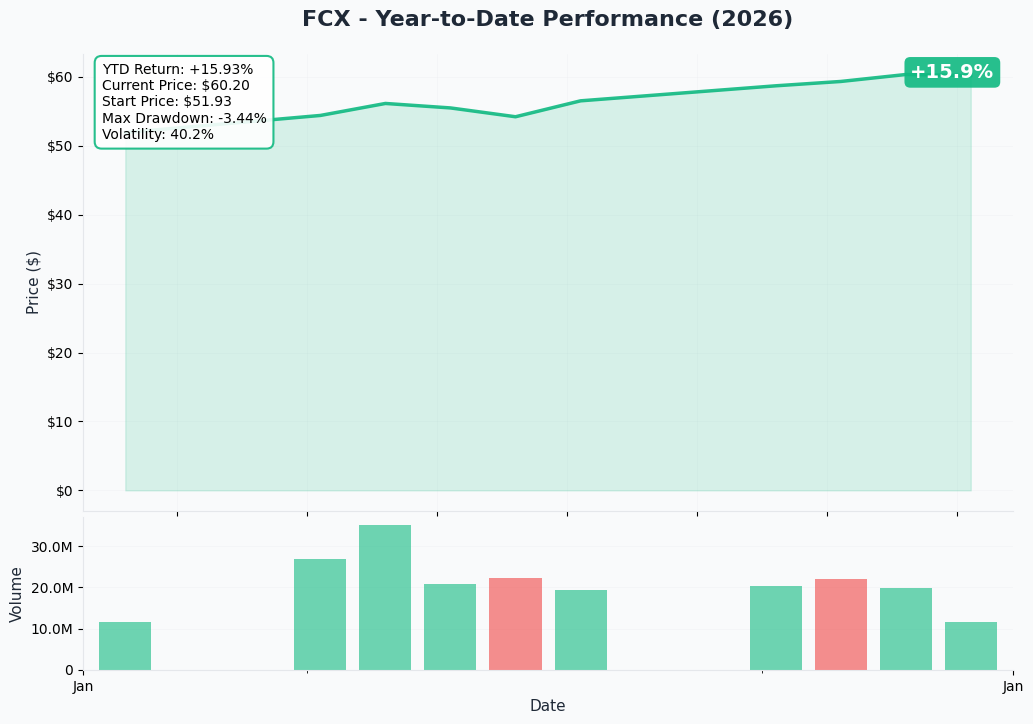

YTD Performance Chart

FCX has been on a tear - up 50.8% over the past 12 months from $40.03 (Jan 15, 2025) to $60.33 (Jan 14, 2026). After a brutal 20% sell-off in September 2025 following the Grasberg mudslide incident, the stock rallied over 30% in Q4 to reach 15-month highs.

Key observations:

- Recovery from disaster: Stock bounced from $37.67 low (September 24) to new highs above $60

- All-time high territory: Trading near 52-week high of $60.64, breaking multi-year resistance

- Volume confirmation: Institutional accumulation visible in Q4 as copper prices surged

- Earnings catalyst: Q4 results January 22 could provide next leg higher or trigger profit-taking

Gamma-Based Support & Resistance Analysis

Current Price: $60.27

The gamma exposure map reveals critical price magnets and barriers:

Support Levels (Put Gamma Below Price):

- $60 - Strongest support with 48.9B net gamma (MAJOR FLOOR - dealers will aggressively buy dips here)

- $59 - Secondary support at 6.1B total gamma

- $58 - Additional support at 5.0B gamma

- $55 - Deep support with 7.8B net gamma (significant put interest)

- $50 - Extended floor at 4.2B net gamma

Resistance Levels (Call Gamma Above Price):

- $61 - Immediate ceiling with 1.7B net gamma (first hurdle)

- $62 - Secondary resistance at 2.3B net gamma

- $63 - Additional resistance at 2.4B net gamma

- $65 - Major resistance zone with 14.6B net gamma (KEY LEVEL TO BREAK!)

- $70 - Target strike with 5.2B net gamma (this trade's target!)

What this means for traders: FCX has rock-solid support at $60 where dealers hold massive gamma positions. The stock would need significant selling pressure to break below this level. On the upside, the path to $70 faces moderate resistance at $65 (14.6B gamma wall), but the overall structure is bullish with 119.5B total call gamma vs 32.6B put gamma.

Net GEX Bias: Bullish - Call gamma dominates, suggesting market makers are positioned for upside.

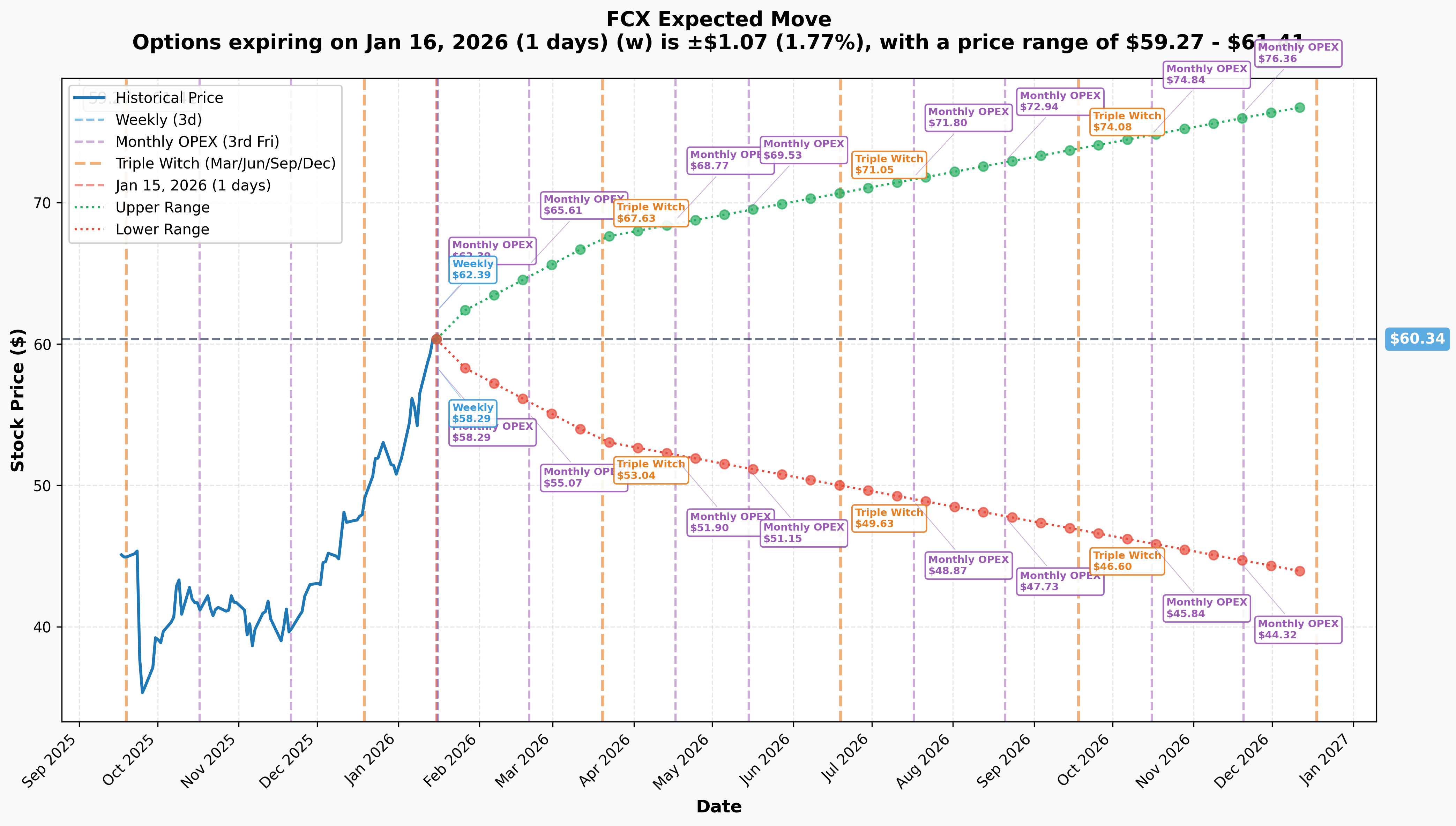

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 16 - 1 day): +/-$1.07 (+/-1.77%) -> Range: $59.27 - $61.41

- Monthly OPEX (Feb 20): +/-$5.27 (+/-8.7%) -> Range: $55.07 - $65.61

- Quarterly Triple Witch (Mar 20): +/-$7.22 (+/-11.97%) -> Range: $53.11 - $67.56

- April OPEX (Apr 17 - THIS TRADE!): +/-$8.44 (+/-14.0%) -> Range: $51.90 - $68.77

- LEAPS (Dec 18): +/-$16.64 (+/-27.58%) -> Range: $43.70 - $76.98

Translation for regular folks: The options market is pricing in about a 14% move by April expiration (the trade's timeframe). The upper implied range of $68.77 falls just short of the $70 strike, meaning this trader is betting FCX will OUTPERFORM what the market currently expects. They need copper momentum, strong earnings, and Grasberg restart news to drive the stock beyond the implied move.

Key insight: The $70 strike sits just outside the upper implied range, making this a moderately aggressive bet that requires multiple catalysts to align.

Catalysts

Upcoming Catalysts

Q4 2025 Earnings - January 22, 2026 (7 DAYS AWAY!)

This is the immediate catalyst that could set the tone for FCX's Q1 trajectory:

- Confirmed Date: January 22, 2026, before market open

- Conference Call: 10:00 AM ET

- Revenue Estimate: $5.64 billion

- Key Focus Areas: Updated 2026 production guidance, Grasberg restart timeline, Indonesia smelter status, copper price outlook

Q3 2025 set the bar high: FCX delivered a significant beat with revenue of $6.97B vs $6.7B expected and EPS of $0.50 vs $0.41 expected. Management guided to $8 billion operating cash flows in 2026, rising to $11.5 billion in subsequent years.

Grasberg Block Cave Restart - Q2 2026

The biggest operational catalyst on the horizon:

- Expected Timeline: Phased restart beginning Q2 2026

- 2026 Production: Approximately 1.0 billion pounds copper, 0.9 million ounces gold (35% below pre-incident levels)

- 2027-2029 Target: 1.6 billion pounds copper, 1.3 million ounces gold annually

- Significance: Block Cave accounts for 70% of projected Grasberg production through 2029

Successful restart would remove a major overhang and demonstrate operational recovery from the September 2025 incident.

US Copper Tariff Decision - June 30, 2026

A potential tailwind for domestic producers like FCX:

- Timeline: Commerce Secretary must provide recommendation by June 30, 2026

- Potential Impact: 15% tariff on refined copper starting January 1, 2027

- Goldman Sachs View: Base case expects at least 25% tariff implementation shortly after June 2026

- FCX Benefit: As largest domestic US copper producer, FCX would gain pricing power for North American operations

Recent Catalysts (Past 3 Months)

Grasberg Mine Disruption - September 2025

The event that temporarily derailed the FCX thesis:

- September 8, 2025: Catastrophic mudslide released 800,000 metric tons of wet material into the Grasberg Block Cave, resulting in seven worker fatalities

- Stock Impact: Shares dropped 5.9% on September 9 and additional 17% on September 24, falling from $45.36 to $37.67

- Recovery: Stock has since rallied 60% from September lows as copper prices surged

Copper Price Surge - Q4 2025 through January 2026

The macro tailwind driving FCX's rally:

- Current Price: Copper hit all-time high above $13,300 per tonne in January 2026

- Drivers: AI data center demand, EV adoption, grid infrastructure spending

- Supply Deficit: International Copper Study Group expects 150,000 tonne refined copper shortfall in 2026

Analyst Upgrades

Wall Street has become increasingly bullish:

- JP Morgan: Price target raised to $68 from $58 (Overweight)

- Citigroup: Target raised to $67 from $48 (Buy)

- Wells Fargo: Target raised to $64 from $55 (Overweight)

- Consensus: Strong Buy with 15 buy ratings, 1 hold, 0 sells

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through April 17 expiration:

Bull Case (30% probability)

Target: $70-$77

How we get there:

- Earnings crush expectations with strong Q4 numbers and bullish 2026 guidance

- Grasberg restart timeline confirmed or accelerated (ahead of Q2 schedule)

- Copper prices sustain above $13,000/tonne on continued supply tightness

- US tariff decision favors domestic producers, boosting sentiment

- Breakout above $65 gamma resistance triggers momentum to $70+

- April OPEX upper implied range of $68.77 gets exceeded

Why this is the trade's thesis: The $70 call buyer is betting on this scenario - FCX breaking through resistance and riding the copper supercycle to new all-time highs. With S&P Global projecting 50% demand surge by 2040 and AI data center copper consumption expected to reach 2.5 million metric tons by 2040, the structural bull case is real.

Trade P&L at $70:

- Calls worth $0 at expiration (at-the-money)

- Loss: -$2.16/contract = -$1.1M (100% loss)

- Need FCX above $72.16 for profit

Trade P&L at $75:

- Calls worth $5.00 at expiration

- Profit: +$2.84/contract x 5,100 = +$1.45M (131% gain)

Base Case (50% probability)

Target: $58-$66 range (CONSOLIDATION)

Most likely scenario:

- Solid earnings meeting expectations without major surprises

- Grasberg restart on track for Q2 2026 but no acceleration

- Copper prices hold $11,000-13,000 range with normal volatility

- Stock consolidates between $60 gamma support and $65 resistance

- April OPEX implied range of $51.90-$68.77 holds

This is the scenario where the trade struggles: In a sideways market, the $70 calls bleed theta (time decay) and expire worthless or near-worthless. The trader loses most or all of the $1.1M premium.

Bear Case (20% probability)

Target: $50-$58

What could go wrong:

- Earnings disappoint or guidance comes in below expectations

- Grasberg restart delayed beyond Q2 2026

- Copper prices correct from record highs (Goldman expects decline to $10,000-11,000 range)

- Securities litigation creates overhang (class action lawsuits pending)

- Break below $60 gamma support triggers cascade to $55

- China demand weakens (GDP growth expected to decelerate to 4.5%)

Trade P&L at $55:

- Calls worth $0 at expiration

- Loss: -$2.16/contract = -$1.1M (100% loss)

Trading Ideas

Conservative: Wait for Post-Earnings Clarity

Play: Stay on sidelines until after January 22 earnings volatility settles

Why this works:

- Earnings in 7 days creates binary event risk with implied +/-8.7% move through February OPEX

- Stock at all-time highs near $60.64 - limited upside cushion if results disappoint

- Pending securities litigation creates headline risk

- Better entry likely post-earnings after direction becomes clear

- Grasberg restart timeline (Q2 2026) gives time to accumulate on dips

Action plan:

- Watch January 22 earnings for revenue ($5.64B target), 2026 production guidance, and Grasberg restart update

- Look for pullback to $55-58 range (gamma support zone) for stock entry

- If earnings beat AND stock breaks $62, consider following the call buyer's thesis with smaller position

- Monitor copper prices - sustained above $12,000/tonne supports bullish thesis

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: Post-Earnings Call Spread (Defined Risk Bullish)

Play: After earnings, buy call spread targeting $65-$70 zone

Structure: Buy $65 calls, Sell $70 calls (April 17 expiration - SAME as the $1.1M trade)

Why this works:

- Defined risk spread ($5 wide = $500 max risk per spread)

- Targets gamma resistance breakout at $65 with profit cap at $70

- Lower cost than outright calls - better risk/reward after IV crush post-earnings

- Aligns with analyst price targets ($64-$68 range)

- Captures Q2 Grasberg restart catalyst window

Estimated P&L (adjust after seeing post-earnings IV):

- Pay ~$1.50-2.00 net debit per spread post-earnings

- Max profit: $300-350 if FCX at or above $70 at April expiration

- Max loss: $150-200 if FCX below $65 (defined and limited)

- Breakeven: ~$66.50-67.00

Entry timing:

- Wait 2-3 days post-earnings (by Jan 24-27) for IV to settle

- Only enter if stock holds above $58 and shows bullish momentum

- Skip if stock breaks below $55 (thesis invalidated)

Position sizing: Risk 2-5% of portfolio

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

Aggressive: Follow The Flow - Long April $70 Calls

Play: Mirror the institutional trade with smaller position

Structure: Buy April 17 $70 calls at ~$2.16

Why this could work:

- Institutional money sees something - $1.1M isn't a casual bet

- Copper supercycle thesis supported by AI demand, EV adoption, and supply deficits

- Multiple catalysts: Earnings (Jan 22), Grasberg restart (Q2), Tariff decision (June)

- JP Morgan target of $68 nearly validates the thesis

- Leverage to copper rally without stock ownership

Why this could blow up (SERIOUS RISKS):

- $70 strike is 16.4% above current price - needs significant move

- Stock at all-time highs already - limited room for "surprise" upside

- Time decay kills value if stock consolidates (-$0.02-0.03/day)

- Implied move upper range of $68.77 falls short of breakeven ($72.16)

- Any Grasberg delay or earnings disappointment = total loss

- Securities litigation could create sudden downside

Estimated P&L:

- Cost:

$2.16 per contract ($216 per contract for 1 lot of 100 shares exposure) - Breakeven: $72.16 (need 20% rally)

- Profit at $75: +$2.84/contract (131% ROI)

- Profit at $80: +$7.84/contract (363% ROI)

- Loss at $70: -$2.16/contract (100% loss)

- Loss at $65: -$2.16/contract (100% loss)

CRITICAL WARNING - Only attempt if you:

- Can afford to lose ENTIRE premium (real possibility)

- Understand theta decay will erode value daily

- Have conviction in copper supercycle thesis

- Plan to cut losses if stock breaks below $55 support

- Accept this is a momentum/catalyst trade, not a value play

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

Risk Factors

Don't get caught by these potential landmines:

-

Earnings binary event in 7 days: Q4 results January 22 could validate or invalidate the thesis. Management needs to deliver strong numbers AND bullish 2026 guidance to support current valuation. Any disappointment at all-time highs could trigger 10-15% selloff.

-

Grasberg restart execution risk: The Q2 2026 timeline is management's target, but underground mining recovery is complex. Expert assessment characterized the September 2025 incident as "preventable, not just a natural disaster", suggesting systemic safety concerns. Any delays would compress the window for this trade to work.

-

Securities litigation overhang: Multiple class action lawsuits pending alleging the company misled investors about safety protocols. Lead plaintiff deadline passed January 12, 2026. Litigation outcomes create headline risk.

-

Copper price volatility: Goldman Sachs forecasts prices declining to $10,000-11,000/tonne from current $13,000+ levels, citing "muddled near-term reality" despite bullish long-term narrative. Any copper correction would drag FCX lower.

-

Indonesia regulatory risk: Government relations reportedly strained following September 2025 incident. Officials may increase demands for greater ownership share. Export permit approval for copper concentrate remains uncertain.

-

China demand uncertainty: China accounts for ~40% of global copper consumption. Real GDP growth expected to decelerate from 5% to 4.5% with continued real estate sector weakness potentially dampening demand.

-

Valuation at multi-year highs: Stock trading near 52-week high of $60.64 after 50% rally. Much of the copper bull case may already be priced in. Limited margin of safety if execution stumbles.

The Bottom Line

Here's the deal: Someone just bet $1.1 MILLION that FCX breaks $70 by April - a 16.4% rally from current prices. This is a conviction trade on the copper supercycle thesis, betting that Q4 earnings, the Grasberg restart, and sustained copper demand will push FCX to new highs.

What this trade tells us:

- Institutional player sees upside through multiple catalysts over the next 93 days

- They're paying $2.16/share (3.6% of stock price) for levered upside exposure above $70

- The timing captures Q4 earnings (Jan 22), Grasberg Q2 restart window, and US tariff decision buildup

- Vol/OI ratio of 14.6x confirms this is a new position opening, not hedging

The copper thesis is legitimate:

- AI data centers require massive copper infrastructure - 2.5M metric tons by 2040

- EVs use 3x more copper than traditional vehicles

- Supply deficit projected at 150,000 tonnes in 2026

- FCX is the largest publicly traded pure-play on copper with world-class assets

But execution matters:

- Grasberg restart timeline (Q2 2026) needs to hold

- Copper prices need to stay elevated ($12,000+/tonne)

- Q4 earnings (Jan 22) must deliver - no disappointments at all-time highs

- Securities litigation needs resolution without material impact

If you own FCX:

- Consider taking partial profits at $60+ (stock at all-time highs after 50% rally)

- Set stop at $55 (gamma support) to protect remaining position

- Earnings January 22 will determine next move - don't add ahead of binary event

- If earnings beat AND stock breaks $62-65, can add exposure for $70 run

If you're watching from sidelines:

- January 22 earnings is the decision point - wait for clarity before entering

- Pullback to $55-58 would be attractive entry with 10-15% margin of safety

- Call spreads ($65/$70) offer defined-risk way to play upside after IV settles

- Long-term thesis (copper supercycle) supports accumulation on weakness

If you're bearish:

- $60 gamma support is the level to watch - break below triggers selloff

- Put spreads ($60/$55) offer defined-risk way to play downside

- Earnings miss or Grasberg delay would invalidate bull thesis

- Don't fight the tape into all-time highs - wait for clear breakdown

Mark your calendar - Key dates:

- January 22, 2026 (Thursday before market open) - Q4 FY2025 earnings report (7 DAYS!)

- February 20 - Monthly OPEX

- Q2 2026 - Grasberg Block Cave restart expected

- April 17, 2026 - This $1.1M call trade expiration

- June 30, 2026 - US copper tariff decision deadline

Final verdict: The copper supercycle thesis is real, and FCX is the premier way to play it. But at all-time highs with earnings in 7 days, this is NOT the time for aggressive new positioning. The $1.1M call buy shows institutional conviction, but retail traders should wait for post-earnings clarity. A pullback to $55-58 would offer much better risk/reward for the same thesis.

Be patient. Let earnings clear. The copper story will still be here next week.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The trade analysis reflects this specific trade's characteristics - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for significant gaps either direction. FCX faces ongoing securities litigation that could materially impact the stock.

About Freeport-McMoRan: Freeport-McMoRan Inc. is the world's largest publicly traded copper producer, operating major mining assets in Indonesia (Grasberg), the Americas (Morenci, Cerro Verde), with a market cap of $80.93 billion in the Copper Ores Mining industry.