🐋 GOOG $15.3M Risk Reversal — Institutions Building a Synthetic Long on Alphabet! 2026-03-09

📅 March 9, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed $15.3 MILLION across four coordinated trades to build a textbook risk reversal / synthetic long on Alphabet. They sold $12.9M worth of puts at the $295 strike across three separate legs (14,200 contracts total) and bought $2.4M in $320 calls (5,400 contracts). With GOOG trading at ~$300.44, this trader is saying loud and clear: "I am willing to own GOOG at $295 and I expect it to break out above $320." The massive 58.22 z-score on the lead trade makes this one of the most unusual options prints on GOOG this entire year.

📊 Company Overview

Alphabet Inc. (GOOG) is the holding company behind Google and one of the most valuable companies on Earth:

- Market Cap: $3.61 Trillion

- Industry: Services — Computer Programming, Data Processing & Related Services

- Current Price: ~$300.44 (down ~14% from the $350.15 ATH set February 3, 2026)

- Primary Business: Google derives ~90% of revenue from advertising services (Search, YouTube, Network), with Google Cloud (~10%), and Other Bets including Waymo, Verily, and Google Fiber

- Full-Year 2025 Revenue: $403 billion — the first year exceeding $400B

- Google Cloud: 48% YoY growth with $240B backlog and 30.1% operating margin

💰 The Option Flow Breakdown

What Just Happened

The Tape (March 9, 2026):

| Time | Symbol | Buy/Sell | Type | Expiration | Strike | Volume | Premium | Order Type | Strategy | Z-Score |

|---|---|---|---|---|---|---|---|---|---|---|

| 10:59:15 | GOOG | SELL | PUT $295 | 2026-05-15 | $295 | 8,100 | $8.5M | STO | Short Put | 58.22 |

| 11:11:49 | GOOG | BUY | CALL $320 | 2026-04-17 | $320 | 5,400 | $2.4M | BTO | Long Call | 20.71 |

| 10:56:27 | GOOG | SELL | PUT $295 | 2026-04-24 | $295 | 2,100 | $2.2M | STO | Short Put | 0.0 |

| 10:56:27 | GOOG | SELL | PUT $295 | 2026-04-24 | $295 | 4,000 | $2.2M | STO | Short Put | 0.0 |

Total Premium Across All 4 Trades: $15.3 MILLION

🤓 What This Actually Means

This is a risk reversal — one of the most aggressively bullish multi-leg strategies in the options playbook. Let's break down what's happening:

The Put Side — $12.9M Collected (14,200 contracts at $295):

- 💸 Leg 1 (lead trade): 8,100 puts sold at $295 strike, May 15 expiration — $8.5M in premium collected

- 💸 Leg 2: 2,100 puts sold at $295 strike, April 24 expiration — $2.2M collected

- 💸 Leg 3: 4,000 puts sold at $295 strike, April 24 expiration — $2.2M collected

- 🎯 What this means: The trader is saying "I will gladly buy 1,420,000 shares of GOOG at $295 if assigned." At ~$300.44 current price, $295 is only 1.8% below spot — this is NOT far out-of-the-money protection selling. This is someone who actively wants to own Alphabet at a slight discount and is getting paid handsomely to wait.

- 📊 Z-Score of 58.22 on the lead leg is extraordinary — this kind of trade volume relative to recent GOOG put activity happens maybe once or twice a year. This is serious institutional capital.

The Call Side — $2.4M Paid (5,400 contracts at $320):

- 💰 5,400 contracts at $320 strike, April 17 expiration

- 🎯 What this means: The trader is buying upside exposure above $320, which is about 6.5% above the current price. If GOOG rallies through April earnings season, these calls participate dollar-for-dollar above $320.

- ⏰ April 17 expiration means this call position captures any pre-earnings run-up ahead of the April 28 Q1 report

The Combined Structure — Risk Reversal / Synthetic Long:

Here's the genius of this trade. By selling puts at $295 and buying calls at $320, this trader has essentially built a synthetic long position with a $25-wide "dead zone" in between:

- 📉 Below $295: The trader is obligated to buy GOOG at $295 (but collected ~$12.9M in premium to cushion the downside, so effective purchase price is even lower)

- 🔄 Between $295-$320: Both sides expire worthless — the trader keeps the full $12.9M in put premium minus the $2.4M call cost = net $10.5M profit if GOOG stays in this range

- 📈 Above $320: The calls kick in and the trader participates fully in upside while still keeping the net premium from the put sales

The economics are compelling: This trader collected $12.9M in put premium and spent only $2.4M on calls, netting roughly $10.5M in credit. They only start losing money if GOOG drops well below $295 (adjusted for premium collected, the real pain starts below ~$286). Meanwhile, they have unlimited upside above $320 for essentially free.

Translation: This is one of the most bullish institutional structures you can build. The trader is using the options market to say: "GOOG is cheap here, I'll buy more if it dips, and I want to ride the breakout when it comes."

📈 Technical Setup / Chart Check-Up

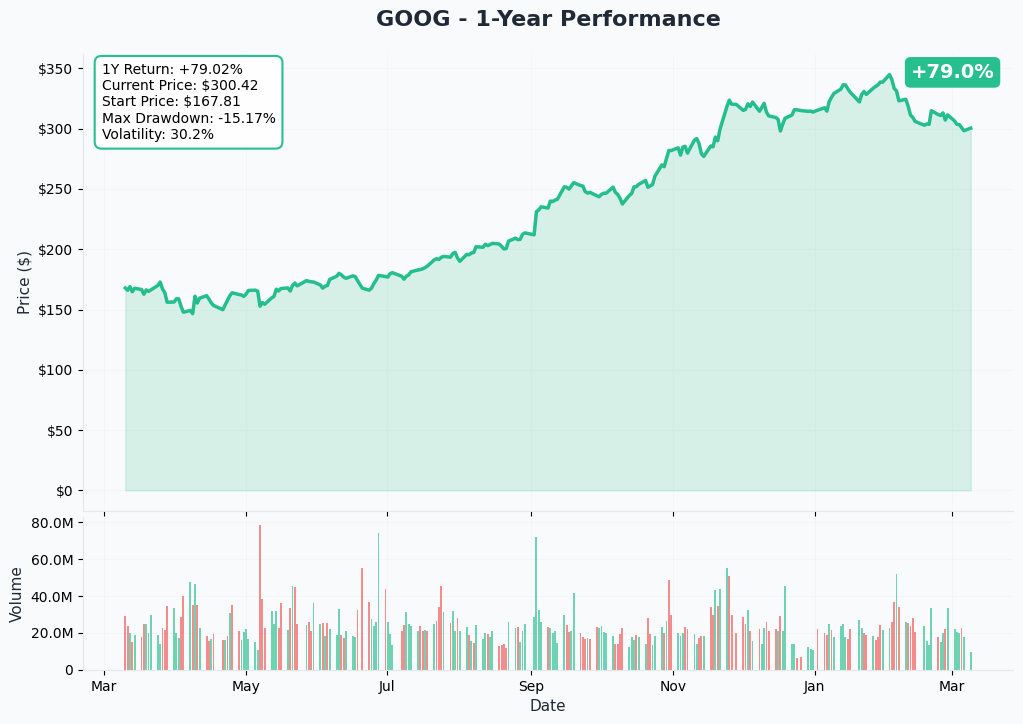

YTD Performance Chart

Alphabet is trading at ~$300.44, down approximately 14% from its all-time high of $350.15 set on February 3, 2026. The pullback was driven primarily by the market's reaction to Alphabet's $175-185B capex guidance for 2026 — roughly double 2025 spending — which overshadowed a strong Q4 earnings beat (revenue $113.8B, EPS $2.82).

Key observations:

- 📉 Consolidation zone: GOOG has been trading in a $290-$310 range since mid-February, building a base after the sharp pullback from $350

- 🎯 $295 put strike = bottom of the range: The trader's put selling is anchored right at the lower end of this consolidation — this is a level-headed risk management choice, not reckless

- 📊 $320 call strike = breakout target: To trigger the call side, GOOG needs to clear the upper end of its consolidation range — essentially betting on a bullish resolution

- 💹 52-week range: $251 to $350.15 — even after the pullback, GOOG is still up significantly over the past year

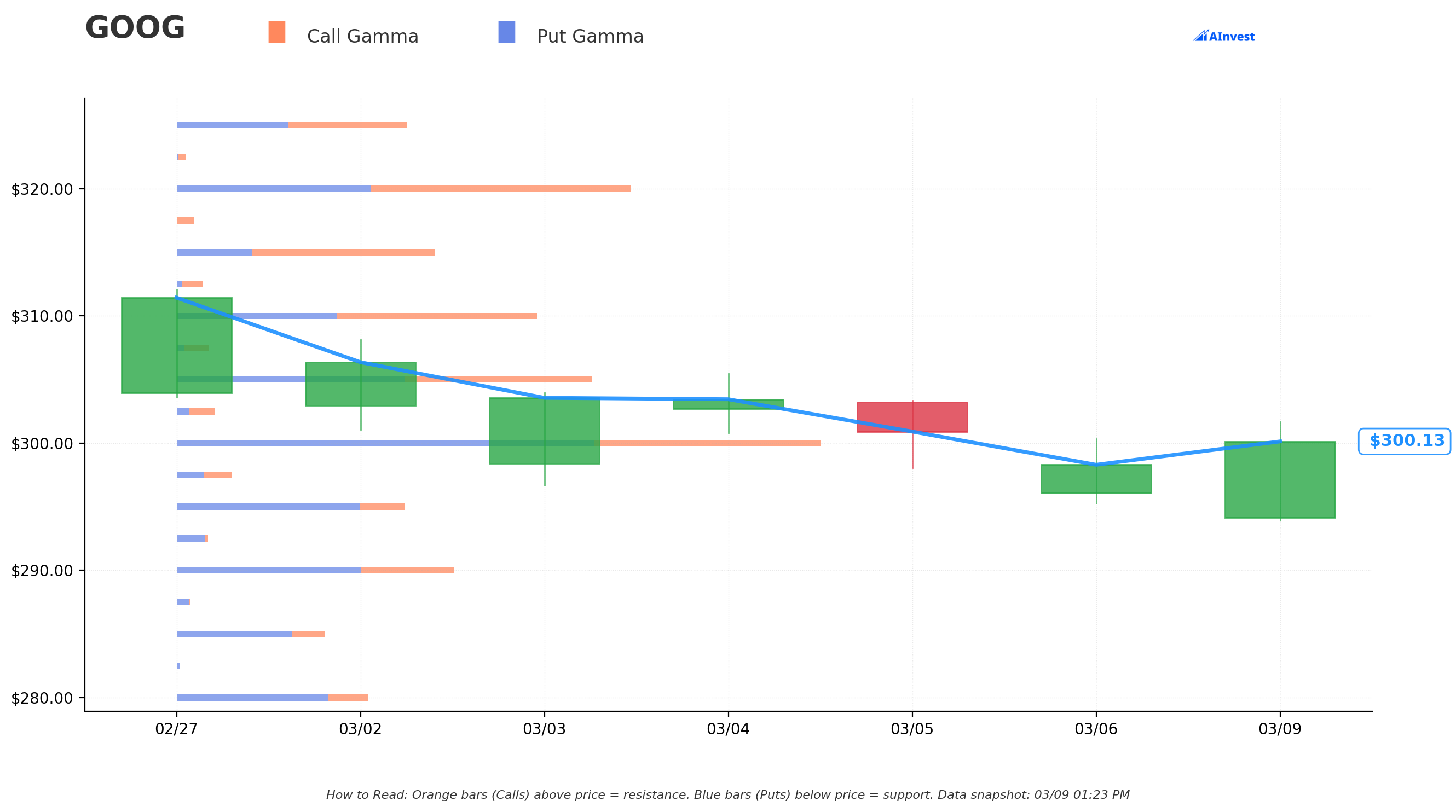

Gamma-Based Support & Resistance Analysis

Current Price: $300.44

The gamma exposure map reveals the critical price levels where market maker hedging flows will influence near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $300 — STRONGEST support on the board at 30.9B total gamma exposure — this is the big floor. Market makers will buy GOOG aggressively if it approaches this level, creating natural buying pressure. The risk reversal trader's confidence is partially backed by this massive gamma cushion sitting right below.

- $295 — Secondary support at 10.9B gamma (1.8% below current price). This is exactly where the put selling is concentrated — the trader chose a strike level that aligns with significant gamma support. Smart.

- $290 — Third tier support at 13.2B gamma (3.5% below). This is the "line in the sand" — a break below $290 would signal a structural change in the pullback dynamic.

🟠 Resistance Levels (Call Gamma Above Price):

- $305 — First resistance level above current price. This needs to be cleared for the stock to begin trending toward the $320 call strike.

- $310-$315 — Secondary resistance zone where momentum sellers will be active.

- $320 — The call strike target. Breaking through $320 would put the long call position in-the-money and likely accelerate buying as gamma flips positive.

Net GEX Bias: Bullish — Call gamma exceeds put gamma at current levels, meaning market makers are positioned to buy dips and support the stock near the $300 floor. This supports the risk reversal trader's thesis that downside is limited and the path of least resistance is higher.

What this means for the risk reversal trade: The gamma structure essentially validates this trader's playbook. There is a massive gamma floor at $300 (right above the $295 put strike), and resistance is moderate between $305-$320. If GOOG can clear the near-term resistance, there is room to run toward $320+ before encountering heavy gamma walls. The dealer positioning acts as a tailwind for this bullish structure.

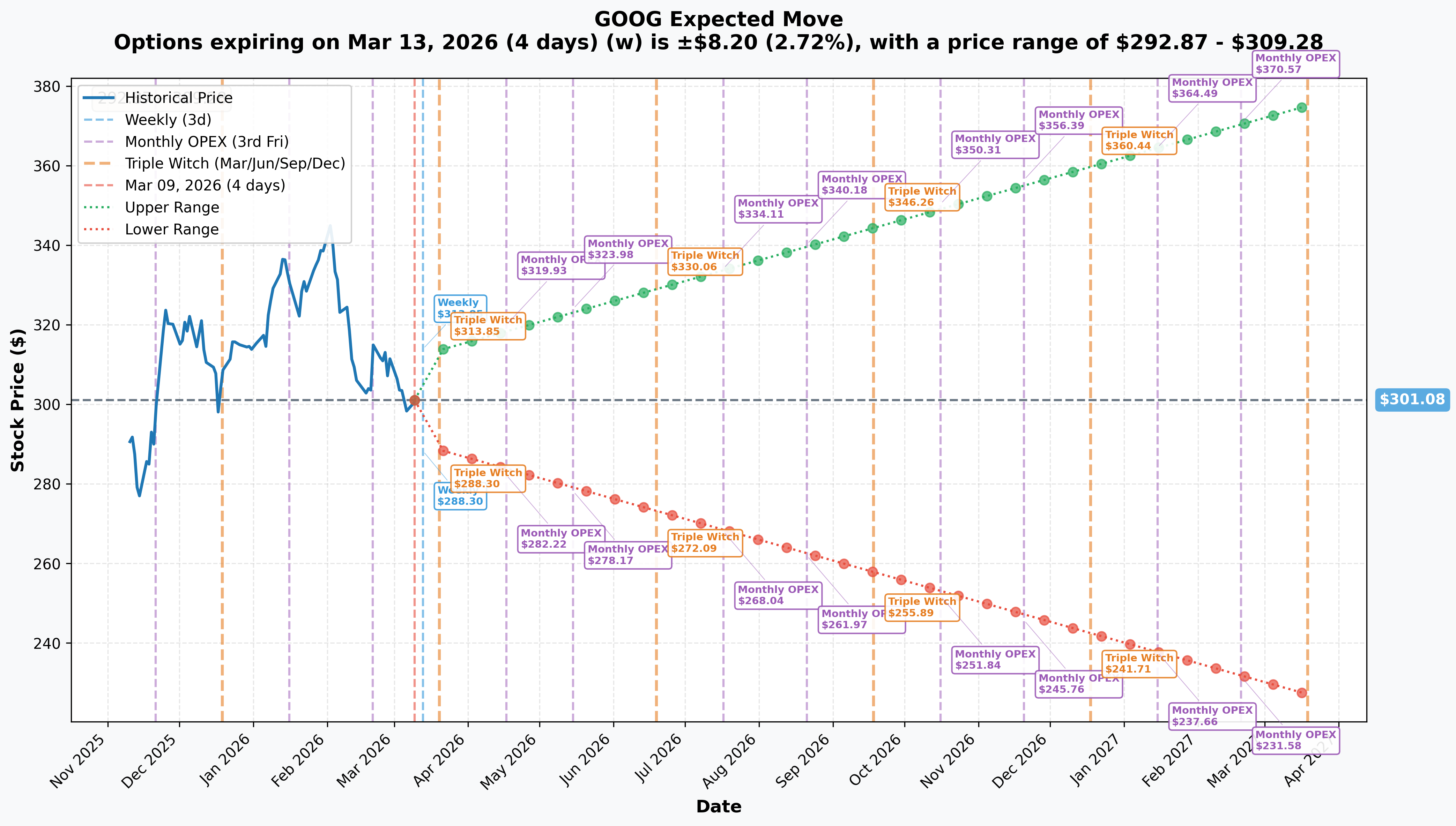

Implied Move Analysis

Options market pricing for upcoming expirations:

| Timeframe | Expiry Date | Days | Implied Move % | Dollar Range |

|---|---|---|---|---|

| Weekly | March 13 | 4 | ±2.72% | $292.87 - $309.28 |

| Monthly OPEX | March 20 | 11 | ±4.19% | $288.47 - $313.68 |

| April 17 (Call expiry) | April 17 | 39 | TBD | Estimated $282 - $319 |

| April 24 (Put expiry) | April 24 | 46 | TBD | Estimated $278 - $323 |

| May 15 (Lead put expiry) | May 15 | 67 | TBD | Estimated $271 - $330 |

Translation for regular folks: The market is pricing in a 2.72% move ($8.20) over the next week and a 4.19% move ($12.60) through the March 20 monthly OPEX. That means traders think GOOG will trade between roughly $288 and $314 by the triple witch.

How does this map to the risk reversal?

- The $295 put strike is right at the lower end of the weekly implied range ($292.87) — the market gives roughly a 15-20% chance of GOOG being below $295 by Friday. By the May 15 expiration of the lead put leg, the implied range expands further, but $295 remains within the expected range.

- The $320 call strike is well above the weekly and monthly implied upper bounds ($309.28 and $313.68 respectively). This tells us the market does not expect GOOG to reach $320 in the near term — the trader needs a positive catalyst (like Q1 earnings anticipation) to push through.

- The risk reversal structure profits in the most likely scenario — GOOG staying between $295 and $320. The trader wins if the stock goes up, and still wins if the stock goes sideways. They only lose if GOOG drops significantly below $295. The implied move data says that scenario is the least likely outcome.

🎪 Catalysts

🔥 Immediate Catalysts (This Week!)

Ex-Dividend Date — March 9, 2026 (TODAY!) 💰

Today is GOOG's ex-dividend date with a $0.21/share quarterly dividend. While the yield is minimal on a ~$300 stock, institutional flow around ex-dividend dates is common. The put selling coinciding with ex-div is typical of funds managing their cost basis around dividend capture.

🚀 Near-Term Catalysts (Next 60 Days)

Q1 2026 Earnings — April 28, 2026 (7 WEEKS AWAY!) 📊

This is the big one and likely the reason the call buyer chose the April 17 expiration — to capture the pre-earnings run-up:

- 💰 Consensus Revenue: $106.7B

- 📊 Consensus EPS: $2.62-$2.66

- 🤖 Key metrics to watch: Can Google Cloud sustain 48% YoY growth? Cloud backlog conversion ($240B), Gemini monetization signals, capex deployment pace, depreciation trajectory

- 📈 Why this matters for the trade: If earnings are strong, GOOG could rally from $300 toward $320+ in the days following the report — putting the calls deep in-the-money. The April 17 call expiration is 11 days BEFORE earnings, so the trader is playing the pre-earnings anticipation, not the event itself. Smart positioning to avoid IV crush.

Google I/O 2026 — May 19-20, 2026 🤖

Confirmed at Shoreline Amphitheatre, Mountain View. Expected announcements include next-gen Gemini model updates, Android features, agentic AI coding tools, and Chrome/Cloud product updates. I/O has historically been a positive catalyst for sentiment. The May 15 put expiration on the lead leg sits just 4 days before I/O — this trader will have their put exposure fully cleared before the event.

⚖️ Regulatory Catalysts

DOJ Antitrust — Search Case Appeal 🏛️

The antitrust saga continues to loom over Alphabet. Judge Mehta rejected structural relief in September 2025 — no Chrome divestiture, no Android breakup. Behavioral remedies were imposed instead: prohibition of exclusive search distribution contracts and restrictions on AI product distribution deals.

However, in February 2026, Google filed an appeal against the behavioral remedies, and the DOJ and 35 state AGs filed a cross-appeal seeking tougher remedies including Chrome divestiture. The D.C. Circuit Court is expected to hear arguments in the second half of 2026, with resolution likely 12-18 months out.

EU Digital Markets Act Fine — Expected Q1-Q2 2026 ⚖️

The EU is expected to impose its first fine under the Digital Markets Act for Google Search self-preferencing (Google Shopping, Flights, Hotels). DMA fines can reach up to 10% of global revenue (~$40B based on 2025 revenue), though analysts expect a smaller initial fine. Google is reportedly developing a new search layout for vertical search competitors to mitigate the penalty. This adds a layer of headline risk but is unlikely to materially impair earnings.

🤖 AI & Growth Catalysts

Gemini AI Momentum 🚀

Gemini surpassed 750 million monthly active users with web visits surging from 267.7 million to 2 billion monthly (Jan 2025 to Jan 2026). Chatbot market share surged from 5.4% to 18.2% YoY — the fastest growth of any major AI platform — while ChatGPT's share dropped from 87.2% to 68%. Gemini 2.5 Pro achieved #1 on LMArena benchmarks with a 1M token context window.

Waymo Expansion — Throughout 2026 🚗

Waymo closed a $16B funding round valuing the unit at $126B, more than doubling its October 2024 valuation. Currently delivering ~400,000 paid rides per week and targeting 1 million by year-end 2026. Expansion planned to 20+ cities including Miami, Dallas, Houston, Las Vegas, San Diego, and internationally to London and Tokyo. The 6th-generation Waymo Driver began fully autonomous operations in February 2026.

🎲 Price Targets & Probabilities

Wall Street Consensus: 59 Buy, 7 Hold, 0 Sell from 66 analysts. Average price target of $367-$377 (varies by source), implying 23-27% upside from current levels. Wells Fargo upgraded to Overweight on February 23 and Seeking Alpha upgraded to Strong Buy on January 30.

Using gamma levels, implied move data, and the catalyst calendar:

📈 Bull Case (30% probability)

Target: $330-$370

How we get there:

- 🚀 Q1 earnings beat with Google Cloud sustaining 40%+ growth and Cloud operating margin expanding above 30%

- 🤖 Gemini monetization signals (ads in AI Overviews scaling to new markets, enterprise adoption accelerating)

- 🚗 Waymo city launches gain media attention and drive Hidden Value re-rating

- 📈 Capex concerns ease as management provides clear ROI metrics

- ⚖️ DOJ and EU regulatory outcomes are manageable (behavioral, not structural)

- 🎯 Breaks through $305 resistance, then $310, $320 gamma levels on sustained institutional buying

- 📊 Analyst targets of $367-$377 become achievable as multiple re-rates

What happens to the risk reversal: This is the dream scenario. The $295 puts expire worthless (trader keeps full $12.9M). The $320 calls go deep in-the-money — at $350, they'd be worth $30 each x 5,400 contracts = $16.2M in intrinsic value alone. Combined with the put premium retained, total profit could exceed $25M on the structure.

🎯 Base Case (50% probability)

Target: $295-$320 (CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q1 earnings meeting consensus ($2.62-$2.66 EPS) with steady but not explosive Cloud growth

- 📊 Stock continues consolidating in the $295-$315 range through April

- ⚖️ DOJ and EU headlines create noise but no material impact

- 🤖 Gemini progress is impressive but monetization ramp is gradual

- 💤 Market digests the capex overhang while waiting for 2026 deployment results

- 🔄 Stock oscillates between $300 gamma support and $310-$315 resistance

This is still a great outcome for the risk reversal trader: Both the puts and calls expire near/at the money or out-of-the-money. The trader pockets the net $10.5M credit (put premium collected minus call premium paid) while the stock sits in the dead zone. That's a massive payday for a position that requires GOOG to do... basically nothing.

📉 Bear Case (20% probability)

Target: $265-$295

What could go wrong:

- 😰 Q1 earnings miss or guide-down, particularly if Cloud growth decelerates sharply

- 💸 $175-185B capex shows no clear return path, free cash flow compresses further (FCF margin already declined from 25.7% to 21.6% in Q4)

- ⚖️ DOJ wins Chrome divestiture on appeal or EU DMA fine exceeds expectations

- 📉 Broader tech selloff on macro fears (tariff uncertainty, rate concerns)

- 🤖 AI competition intensifies — OpenAI and Anthropic maintain enterprise leadership

- 🔨 Break below $295 gamma support triggers cascade through $290 to $280

What happens to the risk reversal: The puts get assigned. The trader buys 1,420,000 shares at $295, but the $12.9M in premium collected provides a cushion, lowering the effective cost basis to roughly $286-$290 depending on which legs are assigned. The $320 calls expire worthless ($2.4M loss). Net: the trader owns a massive GOOG position at an attractive cost basis — painful in the short term, but these are clearly long-term oriented investors who wanted to own the stock anyway.

💡 Trading Ideas

🛡️ Conservative: Ride the Gamma Floor at $300

Play: Buy GOOG shares on any dip to $295-$300, targeting $320+

Why this works:

- 🎯 The 30.9B gamma wall at $300 creates a massive institutional buying floor — market makers are obligated to buy GOOG aggressively near this level

- 💰 A $15.3M institutional risk reversal centered at $295-$320 confirms smart money sees value at these levels

- 📊 Analyst consensus of $367-$377 implies 23-27% upside from a $300 entry

- 🛡️ Shares don't expire — no time decay pressure. You have the luxury of patience

- 📈 Multiple catalysts (Q1 earnings April 28, Google I/O May 19-20) provide shots at upward re-rating

- 📊 At $300, GOOG trades at ~27x trailing earnings — reasonable for a company with 48% Cloud growth and 18.2% AI chatbot market share

Action plan:

- 👀 Scale in: 50% at $300, 50% at $295

- 🎯 Target: $320-$330 (7-10% upside)

- 🛡️ Stop loss at $280 (6-7% below entry)

- ⏰ Hold through at least Q1 earnings (April 28)

Risk level: Low-Moderate | Skill level: Beginner-friendly

⚖️ Balanced: Sell a Cash-Secured Put at $295 (Follow the Whale)

Play: Sell cash-secured put at $295 strike, April or May expiration

Structure: Sell 1x $295 put, May 15 expiration

Why this works:

- 🐋 You're literally copying the institutional playbook — this trader just sold 14,200 puts at $295 for $12.9M. If it's good enough for a fund running nine figures, it's worth considering at a smaller scale

- 💰 Collect premium while agreeing to buy GOOG at $295 — a level backed by 10.9B in gamma support

- 📊 The put strike is 1.8% below current price and well within the implied move range, so you're getting paid for a reasonably likely scenario

- 🛡️ If assigned, you own GOOG at an effective price of roughly $285-$290 (strike minus premium collected) — 17-19% below the all-time high and at a forward P/E below 27x

- ⏰ May 15 expiration captures the Q1 earnings event — elevated IV means fatter premiums

Estimated P&L (per contract, 100 shares):

- 💰 Premium collected: ~$600-$900 per contract (estimated based on current IV)

- 📈 Max profit: Premium collected if GOOG stays above $295 at expiration

- 📉 Max loss: $295 x 100 - premium = ~$28,500 (you own the stock at a discount)

- 🎯 Breakeven: ~$286-$289 at expiration

- 💵 Cash requirement: ~$29,500 per contract (cash-secured)

Risk level: Moderate (requires capital to secure) | Skill level: Intermediate

🚀 Aggressive: Mini Risk Reversal (Replicate the Whale at Scale)

Play: Sell $295 puts / Buy $320 calls to replicate the institutional structure

Structure: Sell 1x $295 put, May 15 / Buy 1x $320 call, April 17

Why this could work:

- 🐋 Exact same structure as the $15.3M institutional trade — just sized for a retail account

- 💰 The put premium partially or fully funds the call purchase — you could enter for a net credit or small debit

- 📈 Unlimited upside above $320 if GOOG rallies into earnings season

- 🛡️ If GOOG stays between $295-$320, you keep the net credit (both expire worthless or near-worthless)

- 📊 Risk/reward is asymmetric: defined downside (own shares at $295 if assigned), unlimited upside above $320

Why this could blow up:

- 💥 If GOOG drops below $295, you're obligated to buy at $295 — that's $29,500 per contract of stock exposure

- 😱 Assignment risk is real — you need the capital to back the put

- 📉 The call expires April 17 (before earnings), so you need the move to happen BEFORE the Q1 report

- ⚠️ Margin requirements for naked/cash-secured puts on a $300 stock are significant

Estimated P&L:

- 💰 Best case (GOOG at $340): Net credit + $20/contract call profit = ~$2,500-$3,000 gain

- 🔄 Base case (GOOG at $305): Keep net credit of ~$200-$500

- 📉 Worst case (GOOG at $275): Own stock at $295, down ~$2,000/contract plus lost call premium

Risk level: HIGH (significant capital at risk) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💸 The capex elephant in the room: Alphabet's $175-185B capex guidance for 2026 is roughly double 2025 levels. This is the #1 reason the stock pulled back 14% from its all-time high. Until the market sees clear ROI from this spend — sustained Cloud revenue acceleration, Gemini monetization — the capex overhang will cap the multiple. Free cash flow margin already declined from 25.7% to 21.6% in Q4, with further compression expected in 2026.

-

⚖️ Antitrust is a multi-year headwind: The DOJ cross-appeal seeking Chrome divestiture is a tail risk that won't resolve for 12-18 months. Separately, the EU DMA fine expected in Q1-Q2 2026 could generate negative headlines even if the financial impact is manageable. And the ad tech antitrust case seeking AdX exchange divestiture adds another layer of legal uncertainty.

-

🤖 AI competition is real and intensifying: Despite Gemini's surge to 18.2% chatbot market share, ChatGPT still commands 68%. The enterprise AI market is fragmenting, and Meta's open-source Llama models could commoditize capabilities. If Gemini fails to sustain its momentum, the AI narrative supporting Alphabet's valuation weakens.

-

📉 Put assignment risk is real: The risk reversal trader is selling puts on a stock that already dropped 14% from its high. If a negative earnings surprise or regulatory shock sends GOOG below $295, those 14,200 contracts represent $4.19 BILLION in stock assignment. Even institutional balance sheets feel that.

-

📊 The $300 gamma floor is not guaranteed: While 30.9B in gamma support at $300 provides a strong theoretical floor, gamma levels can shift rapidly as positions roll off or new trades are established. If gamma support weakens heading into March OPEX, the safety net could evaporate.

-

🌍 Macro headwinds: Tariff uncertainty, interest rate concerns, and broad market tech weakness could create selling pressure independent of Alphabet's fundamentals. Even great companies see their stocks decline in risk-off environments.

-

📊 YouTube deceleration: YouTube ad revenue grew only 9% in Q4 2025 (below the 15% pace in Q3), suggesting potential maturation or competitive pressure from TikTok and short-form video platforms. YouTube is a meaningful revenue contributor and deceleration could weigh on sentiment.

🎯 The Bottom Line

Real talk: An institutional player just built a $15.3 MILLION risk reversal on Alphabet — selling puts at $295 and buying calls at $320 in a structure that screams long-term conviction. This is not a hedge. This is not a cautious toe-dip. This is someone saying: "I believe GOOG is undervalued 14% off its highs, I will happily buy more on any further dip, and I want to be positioned for the breakout."

What this trade tells us:

- 🎯 The $295 put strike aligns perfectly with gamma support at $295 (10.9B) and the lower end of the consolidation range — this trader did their homework

- 💰 They are NET RECEIVING $10.5M+ in premium on this structure — this is a funded bullish bet, not a speculative gamble

- 📊 The 58.22 z-score on the lead leg means this kind of trade is exceptionally rare — this is serious institutional capital making a deliberate, high-conviction move

- 🤖 The thesis likely centers on the April 28 Q1 earnings catalyst and the broader narrative that Google Cloud's 48% growth rate, Gemini's AI market share surge, and Waymo's $126B valuation make this pullback a gift

- ⏰ The layered expirations (April 17 calls, April 24 puts, May 15 puts) are designed to capture the Q1 earnings cycle from multiple angles

If you own GOOG:

- ✅ This trade should give you confidence. When sophisticated players build $15M synthetic long positions, it validates that institutional money sees value at these levels

- 📊 Watch the $295-$300 gamma support zone as your floor — if those levels hold, the consolidation base is intact

- ⏰ Q1 earnings on April 28 is the next decisive catalyst. Google Cloud growth, capex deployment pace, and Gemini metrics will determine whether GOOG reclaims $320+

- 💰 Consider selling covered calls at $330-$340 to generate income during the consolidation period — the same institutions selling puts below are selling calls above

If you're watching from the sidelines:

- 🎯 A pullback to $295 (gamma support + institutional put strike) is a compelling entry point

- 📅 Wait for Q1 earnings clarity on April 28 before committing significant capital

- 📊 Analyst consensus of $367-$377 implies 23-27% upside — the risk/reward is getting more attractive with every pullback

- 🚀 Longer-term, the combination of Cloud growth ($240B backlog), Gemini adoption (750M+ MAUs), and Waymo expansion represents a multi-year re-rating thesis

If you're bearish:

- ⚠️ Respect the gamma structure — $300 has 30.9B in support, and fighting that is expensive

- 📊 If you want to play downside, wait for a clean break below $290 before initiating short positions

- ⚖️ The DOJ cross-appeal for Chrome divestiture is the strongest potential bear catalyst — but resolution is 12-18 months away

- 📉 Put spreads ($290/$275 for May expiration) offer defined-risk downside exposure without unlimited loss

Mark your calendar — Key dates:

- 📅 March 9 (TODAY) — GOOG ex-dividend date ($0.21/share)

- 📅 March 13 — Weekly OPEX (±2.72% implied move)

- 📅 March 20 — Monthly OPEX / Triple Witch (±4.19% implied move)

- 📅 April 17 — Monthly OPEX — $320 call leg expires

- 📅 April 24 — $295 put legs (2,100 + 4,000 contracts) expire

- 📅 April 28 (after market close) — Q1 2026 earnings report (consensus: Revenue $106.7B, EPS $2.62-$2.66)

- 📅 May 15 — Monthly OPEX — Lead $295 put leg (8,100 contracts) expires

- 📅 May 19-20 — Google I/O 2026

Final verdict: This $15.3M risk reversal is institutional conviction in its purest form. A well-capitalized player is betting that Alphabet's 14% pullback from all-time highs is a buying opportunity, not the start of something worse. They have structured the trade to profit in nearly every scenario except a significant decline below $295 — and even then, they end up owning one of the best companies in the world at a discount. The catalyst calendar (Q1 earnings, Google I/O, Waymo expansion, Gemini adoption) provides multiple shots at upside over the next 2-3 months. For retail traders, the takeaway is simple: when the whales are building synthetic longs at the bottom of a consolidation range backed by massive gamma support, pay attention. The smart money is telling you something.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. Risk reversals involve significant capital requirements and potential for loss exceeding premiums received. The 58.22 z-score reflects this trade's extreme unusualness relative to recent history — it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Selling puts obligates you to purchase shares at the strike price and requires sufficient capital or margin. Never risk more than you can afford to lose.

About Alphabet Inc. (GOOG): Alphabet is the holding company behind Google, with a $3.61 trillion market cap. The company derives ~90% of revenue from advertising services (Google Search, YouTube, Network), with Google Cloud accounting for ~10% of revenue and growing at 48% YoY with a $240B backlog. Other Bets include Waymo autonomous vehicles (valued at $126B), Verily healthcare, and Google Fiber. Alphabet generated $403B in full-year 2025 revenue — its first year exceeding $400B.