💎 GOOGL Massive $34M Deep ITM Call Sale - Profit-Taking at AI Peak! 🏆

📅 December 5, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just cashed out a $34 MILLION deep in-the-money call position on Google (GOOGL) this morning at 09:54:48! This monster trade sold 5,000 contracts of $260 strike calls expiring February 20th - locking in MASSIVE profits after Google's epic 67% YTD run to $322. With GOOGL at all-time highs following the November Gemini 3 AI model launch, Warren Buffett's $4.9B investment, and favorable antitrust ruling, smart money is banking gains at the peak. Translation: Institutional investors are taking chips off the table after the biggest AI rally of 2025!

📊 Company Overview

Alphabet Inc. (GOOGL) is the holding company that owns internet giant Google, dominating global search, cloud computing, and AI innovation:

- Market Cap: $3.83 Trillion (3rd largest company globally)

- Industry: Computer Programming & Data Processing Services

- Current Price: $322.38 (near all-time high of $328.83)

- Primary Business: Google Search (90% revenue from ads), YouTube, Google Cloud, Waymo autonomous vehicles, AI/ML platforms

Alphabet generates ~90% of revenue from Google services (advertising, subscriptions, cloud), with Google Cloud representing 10% and growing 35% annually. The company employs 190,167 people and maintains the world's most valuable internet properties including Search, YouTube, Gmail, Maps, and Android.

💰 The Option Flow Breakdown

The Tape (December 5, 2025 @ 09:54:48):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:54:48 | GOOGL | BID | SELL | CALL $260 | 2026-02-20 | $34M | $260 | 5K | 40K | 5,000 | $322.38 | $679.00 |

🤓 What This Actually Means

This is massive profit-taking on a long-held position! Here's the breakdown:

- 💰 Huge cash-out: $34M in premium ($679.00 per contract × 5,000 contracts)

- 🎯 Deep in-the-money: $260 strike is $62.38 below current price (24% ITM!)

- 📊 Intrinsic value domination: $62.38 intrinsic vs $0.62 time value - this is pure profit extraction

- ⏰ Strategic timing: 77 days to expiration (Feb 20) - selling before next earnings and Q4 results

- 💎 Position size: 5,000 contracts represents 500,000 shares worth ~$161M

- 🏦 Institutional book closing: This is "STC" (Sell To Close) - exiting a winning long position accumulated months ago

What's really happening here: This trader bought these $260 calls when GOOGL was likely trading around $260-280 (probably in September-October 2025 during the run from $251 to current levels). Now with stock at $322 and options worth $679 each, they're banking EPIC gains. Assuming original entry around $40-60 per contract, this represents a 1000-1500% profit on the options position!

Why sell now instead of riding it higher?

- ✅ Stock at all-time highs after 67% YTD rally - prudent profit-taking

- 📅 Q4 2025 earnings coming late January - remove binary event risk

- 🎢 Implied volatility relatively low (3.06% weekly) - option prices not getting better

- 💰 Already made the money - why risk giving it back?

- 🎯 Can always re-enter if consolidation provides better entry

Unusual Score: 🔥 HIGHLY UNUSUAL (2.21 Z-score) - This happens a few times per year. Volume of 5,000 contracts with only 125 volume-to-OI ratio (5,000 volume vs 40,000 OI) indicates genuine position closing rather than day trading. The classified strategy "Closing Long Call" confirms this is profit realization, not speculation.

📈 Technical Setup / Chart Check-Up

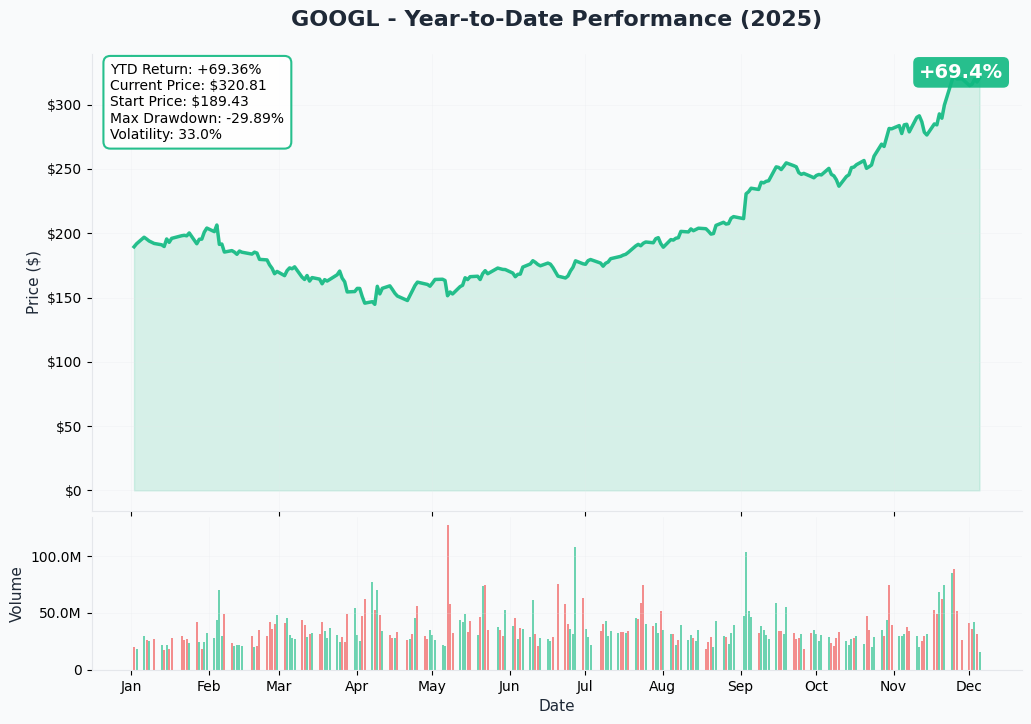

YTD Performance Chart

GOOGL is absolutely crushing it - up +67% YTD with current price of $322.38 (started the year at $193). The chart tells an explosive AI-driven growth story - after consolidating in the $140-180 range during Q1-Q2 2025, Google rockets from $193 in early September to near all-time highs of $328.83 by late November.

Key observations:

- 🚀 Gemini 3 launch catalyst: Vertical move from $280 to $323 following November 18 AI model announcement

- 📈 Breakout confirmed: Smashed through $200 resistance in early September, never looked back

- 💪 Buffett endorsement pop: Stock jumped on news of Berkshire's $4.9B stake announcement in November

- 📊 Institutional accumulation: Massive volume in October-November as AI narrative accelerates

- ⚠️ Near resistance: Trading just below all-time high - near-term consolidation likely

- 🎯 Clean trend: Series of higher highs and higher lows throughout 2025

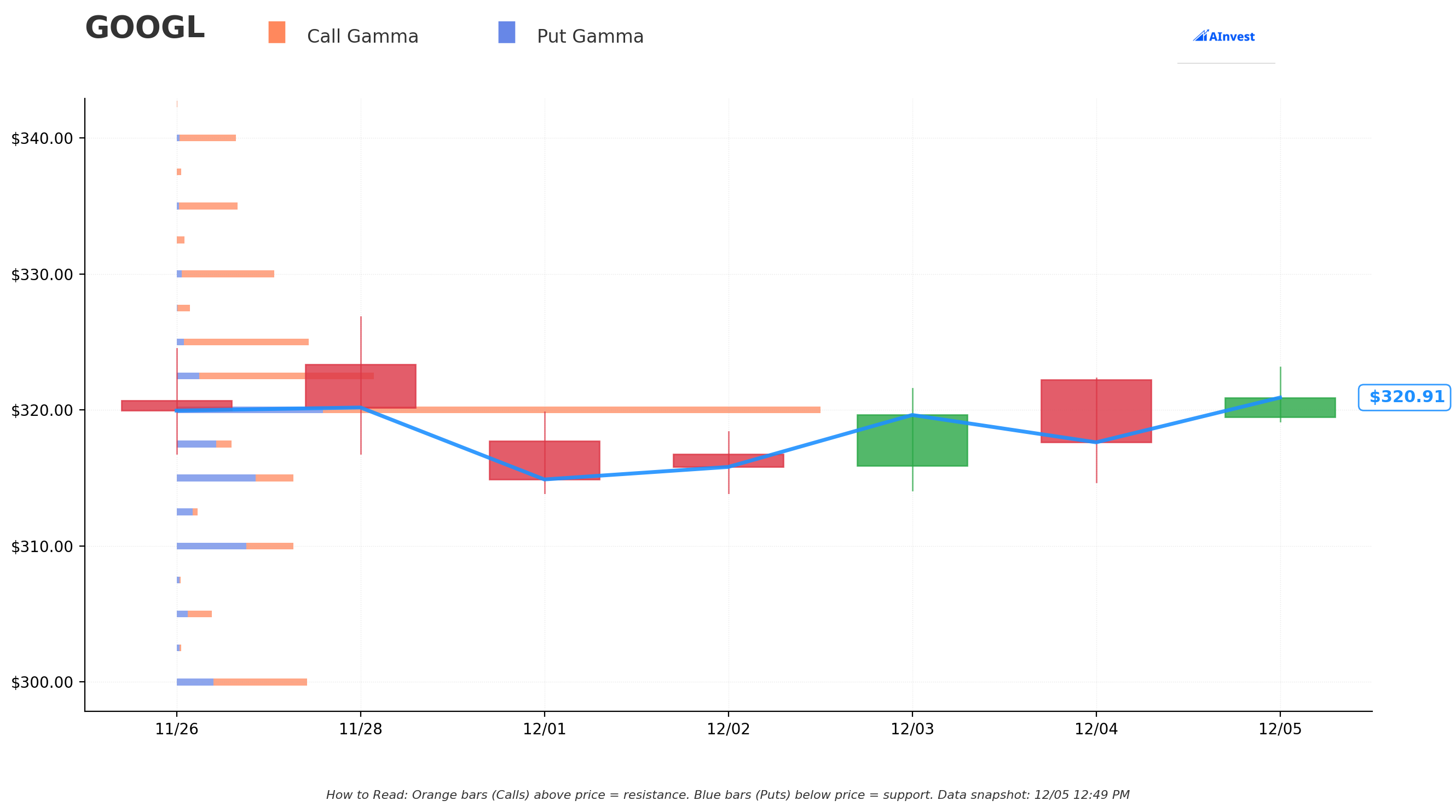

Gamma-Based Support & Resistance Analysis

Current Price: $321.06

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $320 - Immediate support with 183.2M total gamma exposure (STRONGEST NEARBY FLOOR - net 99.3M bullish!)

- $315 - Secondary support at 35.2M gamma (5.0M net bearish from puts)

- $310 - Tertiary support at 33.5M gamma (6.6M net bearish)

- $300 - Major structural floor with 37.4M gamma (16.3M net bullish - key psychological level)

🟠 Resistance Levels (Call Gamma Above Price):

- $322.50 - Immediate ceiling with 58.5M gamma (45.1M net bullish - minor resistance)

- $325 - Secondary resistance at 39.6M gamma (33.2M net bullish - 1.2% overhead)

- $330 - Major ceiling zone with 28.1M gamma (25.2M net bullish - 2.8% above current)

- $335 - Extended resistance at 17.7M gamma (16.4M net bullish)

- $340 - Upper target at 17.0M gamma (15.3M net bullish)

- $350 - Long-term target with 22.1M gamma (20.1M net bullish - 9% rally required)

What this means for traders: GOOGL is trading in a tight consolidation zone just above MASSIVE $320 support (183.2M gamma - by far the strongest level). The gamma data shows market makers holding enormous call positions above price, creating natural resistance but also upside potential if momentum continues. The $320 level is THE critical support - as long as stock holds above here, the bullish structure remains intact.

Net GEX Bias: Bullish (465.8M call gamma vs 173.7M put gamma = 292.1M net bullish) - Overwhelmingly bullish positioning with call gamma nearly 3x put gamma. Market makers are short massive calls, which creates squeeze potential if stock breaks above $330.

Trading range outlook: Stock likely consolidates between $320 support and $330 resistance near-term as market digests 67% YTD gains. Break above $330 opens door to $340-350, while break below $320 could see quick move to $315 then $310.

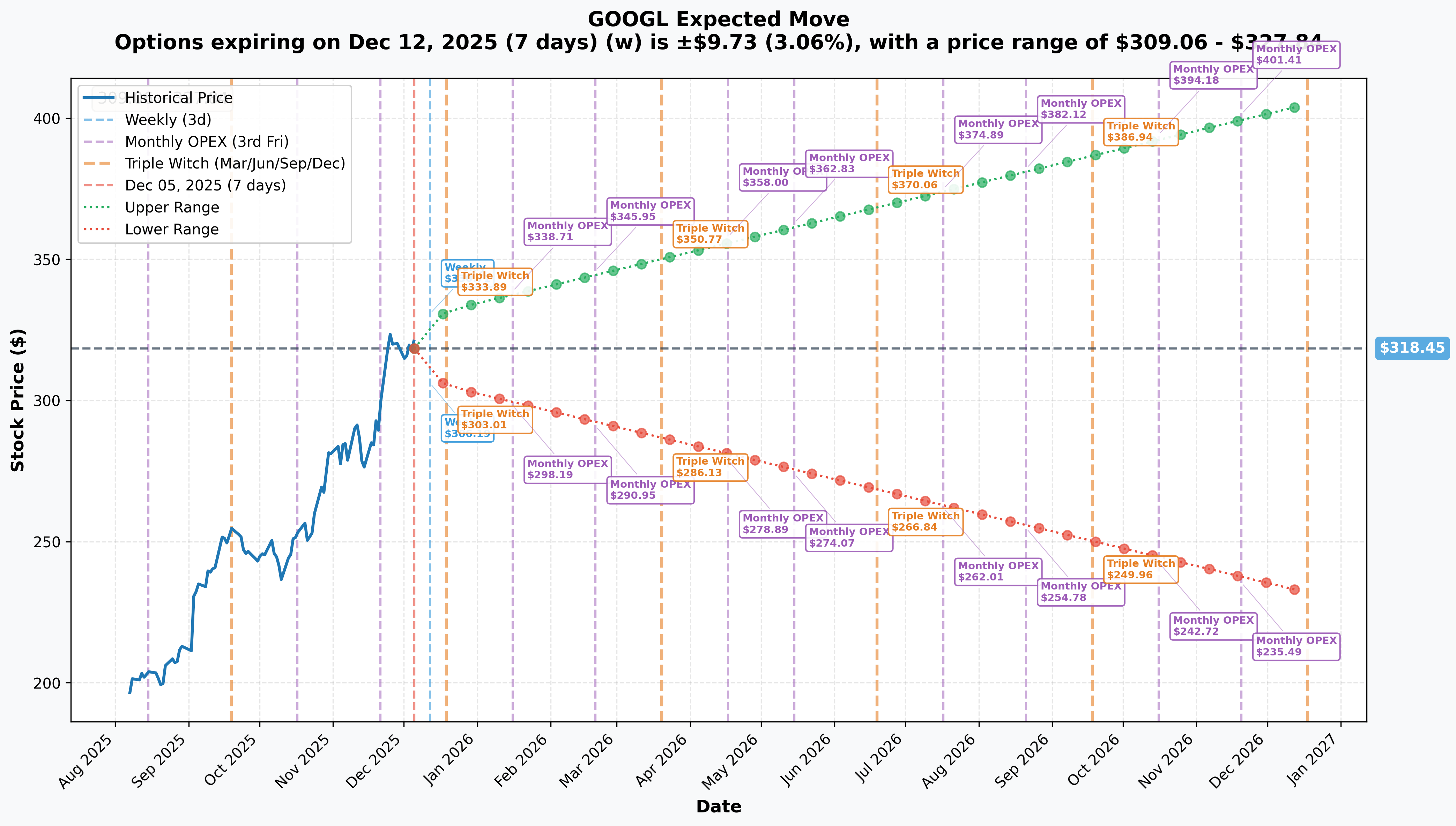

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 7 days): ±$9.73 (±3.06%) → Range: $309.06 - $327.84

- 📅 Monthly OPEX (Dec 19 - 14 days): ±$13.41 (±4.21%) → Range: $305.04 - $331.86

- 📅 Quarterly Triple Witch (Dec 19 - 14 days): ±$13.43 (±4.22%) → Range: $305.02 - $331.88

- 📅 Yearly LEAPS (Dec 18, 2026 - 378 days): ±$81.77 (±25.68%) → Range: $231.87 - $405.03

Translation for regular folks: Options traders are pricing in a 3.1% move ($9.73) by next week for weekly expiration, and a 4.2% move ($13.41) through December monthly OPEX. This is relatively LOW volatility for a mega-cap tech stock - the market expects STABILITY rather than fireworks into year-end.

The December 19th Triple Witch expiration (same as monthly OPEX) has upper range of $331.88 - meaning the market thinks there's good probability GOOGL trades between $305-$332 through December 19th. This aligns with the gamma levels showing strong $320 support and $330 resistance creating a consolidation range.

The yearly LEAPS pricing is fascinating - upper range of $405 (+26% from current) reflects analyst price targets in the $370-380 range with upside potential to $400+ if AI monetization accelerates. Lower range of $232 (-27%) provides hedging floor if AI search cannibalization concerns materialize.

Key insight: Low near-term implied volatility (3-4%) suggests limited event risk into year-end. Q4 earnings (late January 2026) will be the next major catalyst. Smart money appears content to consolidate gains rather than chase into resistance.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened - Explaining The Rally)

Gemini 3 AI Model Launch - November 18, 2025 (THE GAME-CHANGER!) 🤖

Google's landmark Gemini 3.0 release represents perhaps its most transformative AI achievement:

- 🏆 Performance dominance: Gemini 3.0 Pro outperformed major AI models in 19 out of 20 benchmarks, topped LMArena leaderboard

- 🎯 Humanity's Last Exam: 41% accuracy vs OpenAI GPT-5 Pro's 31.64% - CRUSHING the competition

- 💪 Deep Think mode: 93.8% on GPQA Diamond benchmark vs standard models

- 🔧 TPU advantage: Trained exclusively on Alphabet's TPU v7 (Ironwood) chips delivering 100% better performance per watt than TPU v6e

- 📈 Stock reaction: Shares jumped 3% on launch day

- 🌍 Market dominance: "Gemini" became #1 global trending search term in 2025

- ⚡ Processing scale: Gemini now processing 7 billion tokens per minute via direct API

- 🚨 Competitive impact: OpenAI declared "code red" on December 1, 2025 to improve ChatGPT quality

This launch validated Google's AI strategy and proved they're NOT falling behind OpenAI/Microsoft - they're WINNING. The stock rally from $280 to $323 in the two weeks following launch reflects this paradigm shift.

Warren Buffett's Berkshire Hathaway Investment - November 2025 (INSTITUTIONAL VALIDATION!) 💎

Major vote of confidence from the Oracle of Omaha:

- 💰 Position size: 17.9 million Class A shares = $4.9 billion stake

- 📊 Average price: $209 per share (current price $322 = 54% gain already!)

- 🎯 Portfolio weight: 1.8% of Berkshire's portfolio, 10th largest holding

- 💬 Historical context: Buffett previously called missing Google's IPO a mistake, stating "we just sat there sucking our thumbs" at 2019 Berkshire meeting

- 💵 Valuation thesis: GOOGL at 26.9x forward earnings vs Microsoft 31.8x, Nvidia 31.8x, Broadcom 40.7x - relative value play

When Warren Buffett builds a $4.9B position, retail should pay attention. This legitimizes Google's AI narrative and confirms the stock isn't overvalued even at $320.

Antitrust Ruling - Search Monopoly (September 2025) - FAVORABLE OUTCOME! ⚖️

Judge Mehta's remedies ruling was almost best-case scenario for Google:

- ✅ NO forced divestitures: Google will NOT be required to sell Chrome or Android

- ❌ Exclusive contracts banned: Google barred from exclusive search distribution deals

- 📊 Data sharing: Must share search index and user interaction data with competitors (not ad data)

- 👀 Oversight: 6-year technological oversight committee established

- 💰 Payment flexibility: Still allowed to pay partners for preloading/placement

- 📈 Stock reaction: Shares jumped on ruling, viewed as "almost best-case scenario"

The market feared forced Chrome/Android spinoffs which would have destroyed billions in value. Instead, the remedies are manageable - losing some exclusive deals worth ~$20-30B annually in payments is far better than structural breakup.

Q3 2025 Earnings Results - October 2024 (BEAT AND RAISE!) 📊

Alphabet crushed expectations:

- 💰 Revenue: $88.3B vs $86.3B consensus (+15% YoY)

- 🎯 EPS: $2.12 vs $1.85 expected (+37% YoY)

- 📈 Net Income: $26.3B (+34% YoY)

- 💪 Operating Margin: 32% (+4.5 percentage points expansion)

- 🌥️ Google Cloud: $11.35B (+35% YoY) with $1.9B operating income (17% margin)

- 🔍 Google Search: $49.4B (+12% YoY)

- 📺 YouTube Ads: $8.9B (+12% YoY)

- 📊 Stock reaction: Shares rose 5% following earnings release

This earnings print validated the AI investment thesis - Cloud accelerating, Search stable despite ChatGPT concerns, YouTube crushing it.

🚀 Upcoming Catalysts (Next 6 Months)

Q4 2025 Earnings - Late January/Early February 2026 (77 DAYS - INSIDE THIS PUT EXPIRATION!) 📅

Historical pattern: Alphabet reports Q4 earnings in early February

Key metrics Wall Street watching:

- 💰 Holiday Ad Spending: Q4 traditionally strongest quarter for advertising

- 🌥️ Cloud Revenue Growth: Can Google maintain 30%+ growth trajectory?

- 🤖 Gemini 3 Monetization: First full quarter impact from November 18 launch

- 💻 CapEx Update: Execution on revised $85B spending plan

- 🎯 AI Revenue Disclosure: Potential breakout of Gemini-related revenue streams

Consensus expectations:

- 📊 FY 2025 EPS: $8.92 (up 11.1% YoY from $8.03 in FY 2024)

- 📈 Strong momentum expected from Cloud and AI products

- ⚠️ Risk: Previous Q4 2024 earnings (Feb 2025) saw stock fall 9% on revenue miss and increased CapEx guidance

Why this matters for the option trade: The $260 call seller is exiting BEFORE Q4 earnings binary event. Smart move - already made the money, why risk giving it back if earnings disappoint?

Gemini 3 Rollout and Monetization - Q4 2025 through Q2 2026 🤖

Ongoing deployment across Google ecosystem:

- 💼 Enterprise adoption: Gemini 3 integration across Google Workspace, Cloud Platform

- 🔍 Search enhancement: AI Overviews powered by Gemini 3 in all markets

- 💻 API revenue: Processing 7 billion tokens/minute creates new revenue stream

- 🎯 Competitive positioning: Market share gains against OpenAI's ChatGPT

Revenue impact potential:

- 📊 Google Cloud AI products used by 70%+ of customers

- 💰 Potential for premium AI tier pricing ($20-30/month range)

- 🌐 Developer API ecosystem expansion

Google Cloud Growth and Large Deal Pipeline - Q4 2025 through Q2 2026 🌥️

Pipeline strength provides revenue visibility:

- 💎 $155 billion backlog (up 46% QoQ, 82% YoY!)

- 📈 More $1B+ deals signed through Q3 2025 than prior two years combined

- 🤖 70%+ of existing customers using Google Cloud AI products

- 🚀 TPU v7 (Ironwood) deployment to major customers including Anthropic commitment for up to 1 million TPUs by 2026

This $155B backlog is INSANE - provides multi-year revenue visibility and validates enterprise AI adoption.

Waymo Expansion and Commercialization - 2025-2026 🚗

Autonomous vehicle business reaching commercial scale:

- 🚕 Current operations: 2,500 robotaxis in service providing 250,000 paid rides/week (5x YoY growth)

- 🌆 Cities live: Phoenix, San Francisco, Los Angeles, Atlanta, Austin

- 📍 2025-2026 expansion: Miami (launched Nov 18), Dallas, Houston, San Antonio, Orlando, Nashville (partnership with Lyft), London (testing begins 2025, first European market)

- 💰 Revenue trajectory: Current ~$260M annualized (250K rides/week × $20/ride average); 10,000 vehicle fleet target = ~$2B annual revenue potential

- 💵 Funding: $5.6 billion raised in October 2024 for expansion

- 🎯 Market opportunity: Morgan Stanley: $200 billion autonomous vehicle market by 2030

Waymo is THE clear leader in autonomous vehicles - miles ahead of Tesla, Cruise, Zoox. This could be Alphabet's next $50-100B business.

Analyst Upgrades - November-December 2025 📈

Recent price target increases following Gemini 3 launch and Buffett investment:

- 💎 Guggenheim: Raised from $330 to $375 (December 1, 2025)

- 🎯 Arete Research: Lifted to $380

- 💰 HSBC: Increased to ~$370

Current consensus:

- 📊 Average Price Target: $326.57

- 📈 Price Target Range: $185 - $432

- 🎯 Rating Distribution: 59 Buy, 12 Hold, 0 Sell

- ✅ Overall Rating: Strong Buy

Street is increasingly bullish - multiple firms raising targets to $370-380 range post-Gemini 3 launch.

⚠️ Risk Catalysts (Negative)

AI Search Cannibalization Risk - ONGOING CONCERN 🚨

Revenue pressure from AI Overviews impacting click-through rates:

- 📉 CTR declines: Both paid and organic CTR at "new lows" per February 2025 analysis

- 🔍 Zero-click searches: 60% of searches now end without clicking any site

- 📊 Organic traffic drops: 18-64% decline in organic clicks on informational queries

- 💰 Advertiser concerns: Reduced conversion rates may lead to lower bids

Mitigation: New ad formats in AI Overviews, AI Mode creates premium inventory, focus on high-intent commercial queries

Competition from OpenAI and Microsoft - INTENSIFYING 🥊

ChatGPT momentum threatens Google's search dominance:

- 💵 ChatGPT revenue: $13 billion annualized revenue (vs ~$0 in early 2023)

- 📊 Market share: 9% of global queries

- 👥 Generational threat: 66% of 18-24 year olds use ChatGPT vs 69% use Google (near parity)

- 💻 Microsoft Copilot: Integration across Office 365 ($60B+ annual revenue business)

Mitigation: Gemini 3 performance superiority on benchmarks, Google's distribution advantage (default search, Chrome, Android), cost advantage via TPUs

Capital Expenditure Pressure - $85B+ SPENDING 💸

Rising AI infrastructure costs creating investor concerns:

- 💰 2025 CapEx: $85 billion (up from initial $75B guidance)

- 📈 Q1 2025 CapEx: $17.2 billion (+43% YoY)

- 📉 Investor reaction: Q4 2024 earnings: Stock fell 9% on increased CapEx guidance

Offsetting factors: TPUs more cost-effective than Nvidia GPUs long-term, $155B Cloud backlog validates demand, strong free cash flow supports spending ($82.4B net cash)

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through February 20th expiration:

📈 Bull Case (30% probability)

Target: $350-$375

How we get there:

- 💪 Q4 earnings CRUSH with holiday ad spending exceeding expectations, Cloud revenue accelerating above 35% growth

- 🤖 Gemini 3 monetization showing up in revenue - premium tier subscriptions, API revenue disclosure

- 🌥️ Google Cloud backlog grows beyond $155B, multiple new $1B+ customer wins announced

- 📊 AI Overviews ad integration showing SUCCESS - CTR stabilizing, new ad formats gaining traction

- 🚗 Waymo expansion accelerating - major city launches (Miami, Dallas, Houston) driving revenue

- 💎 Market share gains vs OpenAI - Gemini 3 proving superior in enterprise adoption

- 📈 Analyst upgrades cascade - consensus targets move to $380-400 range

- 🎯 Breakout above $330 gamma resistance triggers technical rally to $350-375 (analyst target zone)

Key metrics needed:

- Q4 revenue >$95B (vs ~$92-93B consensus)

- Cloud revenue >$13B (maintaining 35%+ growth)

- Gross margins expanding (pricing power)

- AI revenue disclosure showing material contribution

Probability assessment: 30% because it requires strong execution AND positive earnings surprise. Gamma resistance at $330 creates headwind, but momentum and fundamentals support upside.

🎯 Base Case (50% probability)

Target: $310-$340 range (CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q4 earnings meeting consensus (revenue ~$92-93B, in-line guidance)

- 📱 Gemini 3 adoption progressing steadily but not explosively

- 🌥️ Cloud growth maintaining 30-35% trajectory - solid but not accelerating

- ⚖️ AI search concerns persist but don't materialize into revenue decline yet

- 🇨🇳 CapEx remains elevated ($85B+ for 2025) but investors accepting it as necessary

- 🔄 Trading within gamma support ($320) and resistance ($330-340) bands for weeks

- 💤 Volatility remains low (3-4% weekly implied moves) as market digests YTD gains

- 📊 Waiting for next major catalyst (Q1 2026 earnings in April, further Gemini proof points)

This is the call seller's assumption: Stock consolidates near highs, calls remain deep ITM but limited upside potential from here. Better to bank $34M in profits than hold through earnings risk. If stock stays $310-340, they made the right move - took money off the table at the peak.

Why 50% probability: Stock at inflection point after 67% YTD run. Fundamentals solid, AI narrative strong, but valuation requiring perfect execution. Most institutions will hold and wait for next catalyst rather than chase aggressively.

📉 Bear Case (20% probability)

Target: $280-$310 (PULLBACK FROM HIGHS)

What could go wrong:

- 😰 Q4 earnings miss or conservative guidance disappoints - even small miss could trigger -8-10% gap down (precedent: Feb 2025 earnings fell 9%)

- 🚨 AI search cannibalization concerns materialize - Search revenue growth decelerates below 10%

- 💸 CapEx guidance raised AGAIN above $85B without corresponding revenue acceleration

- 🤖 Gemini 3 enterprise adoption slower than expected - ChatGPT maintaining dominance

- 📊 Google Cloud growth decelerates below 30% - competitive pressure from AWS/Azure

- 💔 Broader tech selloff drags mega-caps lower (Nasdaq correction, recession fears)

- ⚖️ New antitrust developments - additional restrictions or fines announced

- 🔨 Break below $320 gamma support triggers cascade to $310, then $300

Critical support levels:

- 🛡️ $320: MASSIVE gamma floor (183.2M) - MUST HOLD or momentum shifts

- 🛡️ $315: Secondary support (35.2M gamma) - first test zone

- 🛡️ $310: Tertiary floor (33.5M gamma) - key psychological level

- 🛡️ $300: Major structural support (37.4M gamma) - disaster scenario

Probability assessment: Only 20% because it requires multiple negative catalysts. Google's fundamentals remain incredibly strong (Cloud growth, Gemini 3 success, Buffett endorsement, favorable antitrust), but the call seller clearly sees some risk of pullback from all-time highs.

Call seller's thought process: Even if Bear Case materializes and stock drops to $300, the $260 calls would still be worth $40 (vs $679 today). That's a 94% decline in option value even though stock only fell 7%. Why risk giving back 94% of gains for potential extra 10-15% upside? Take the money and run.

💡 Trading Ideas

🛡️ Conservative: Take Profits Like The Pros

Play: If you own GOOGL shares or calls, follow the institutional playbook and trim positions

Why this works:

- 💰 Stock up 67% YTD at all-time highs - you've already WON! Protecting gains is smart

- 📅 Q4 earnings in ~6-7 weeks creates binary event risk with potential for 8-10% move either direction

- 🎯 The $34M call sale signals smart money is DERISKING at peak - why fight the tape?

- 📊 Gamma ceiling at $330 creates natural resistance making further breakouts harder

- ⏰ Limited upside potential (5-10% to analyst targets) vs downside risk (10-15% if earnings disappoint)

- 💎 Can always re-enter if consolidation provides better entry at $300-310 levels

Action plan:

- 📈 If holding stock: Trim 25-40% at current levels ($320-325), keep core position

- 💰 If holding calls: Close profitable positions, especially those expiring before Feb earnings

- 🎯 Set mental stop: $315 support - if broken, consider reducing further

- 👀 Watch Q4 earnings: Wait for clarity before adding back positions

- ⏰ Re-entry targets: $310-315 pullback post-earnings would offer 5-8% margin of safety

Position management:

- ✅ Lock in gains on 25-50% of position NOW

- 🛡️ Keep 50-75% for continued upside participation

- 📊 Use proceeds to diversify or hold cash for better entries

Risk level: Minimal (capital preservation) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -8-12% drawdown if earnings disappoint. Maintain upside exposure with reduced position. Sleep better at night.

⚖️ Balanced: Ride The Wave with Protection

Play: Keep stock position but add protective puts OR sell covered calls to reduce cost basis

Option 1 - Protective Puts (Married Put Strategy):

Structure: Buy $310 puts (February 20 expiration - SAME as the $260 call trade)

Why this works:

- 🛡️ Protects against downside below $310 (4% cushion from current price)

- 📊 Aligns with gamma support level at $310 (33.5M gamma)

- ⏰ Feb 20 expiration captures Q4 earnings event

- 💰 Relatively cheap protection given low volatility environment

- 🎯 Allows upside participation while limiting downside to defined level

Estimated costs and P&L:

- 💸 Cost: ~$8-12 per put (2.5-3.7% of stock price) based on current IV

- 📈 Upside unlimited: Stock rallies to $350+ and puts expire worthless (lost premium but made gains on stock)

- 📉 Downside protected: Stock falls to $280 → puts worth $30, offset stock loss

- 🎯 Breakeven: Need stock to stay above $320-324 to outperform selling outright

Option 2 - Covered Calls (Income Generation):

Structure: Sell $335 calls (February 20 expiration)

Why this works:

- 💰 Collect premium (~$12-18 per share) against stock holdings

- 📊 $335 strike provides 4% upside before capping gains

- 🎯 Aligns with resistance zone ($335 gamma level)

- ⏰ Feb 20 expiration lets you participate in earnings run-up

- 💎 Reduces cost basis making it easier to weather volatility

Estimated P&L:

- 💰 Collect: $12-18 per share premium (3.7-5.6% income)

- 📈 Max profit: Stock at $335+ = $12.62 stock gain + $15 premium = $27.62 total (8.5% return in 77 days)

- 📊 Breakeven improvement: Lowers breakeven on stock position by $15

- ⚠️ Cap upside: If stock explodes to $370, you only make gains to $335 (miss $35 of upside)

Position sizing: Only hedge/sell calls against 25-50% of holdings (keeps flexibility)

Risk level: Moderate (requires options knowledge) | Skill level: Intermediate

🚀 Aggressive: Sell Cash-Secured Puts - Get Paid to Wait for Pullback

Play: Sell puts at support levels to collect premium while positioning for re-entry

Structure: Sell $310 puts (February 20 expiration)

Why this could work:

- 💰 Get paid to wait: Collect $8-12 premium for obligation to buy at $310

- 🎯 Want to own it anyway: If assigned, buying GOOGL at $310 (effective cost $298-302 after premium) is 7-8% below current price

- 📊 Gamma support confirmation: $310 has 33.5M gamma support - solid technical level

- ⏰ Earnings catalyst: If stock consolidates near highs, puts expire worthless and you keep premium

- 🛡️ Win-win scenario: Either collect premium and move on OR get assigned at attractive entry

Why this could blow up (SERIOUS RISKS):

- 😱 Assignment risk: If stock breaks below $310, you WILL own 100 shares at $310 (minus premium)

- 📉 Falling knife danger: If earnings disaster sends stock to $280, you're buying at $310 = -9% instant loss (minus premium collected)

- 💸 Capital requirement: Need $31,000 cash secured per put sold (or margin buying power)

- 🎢 Unlimited downside: If stock craters to $250 (unlikely but possible), you bought at effective $302 = -17% loss

- ⚠️ Opportunity cost: Cash tied up for 77 days could be deployed elsewhere

Estimated P&L:

- 💰 Premium collected: $8-12 per share × 100 shares = $800-1,200 per put

- 📈 Best case: Stock stays above $310, puts expire worthless, keep full premium (2.5-3.9% return in 77 days = 12-18% annualized!)

- 🎯 Neutral case: Assigned at $310, effective cost $298-302, immediate 6-7% discount to current price

- 📉 Worst case: Stock at $280 at expiration = -6% loss on $310 assignment price (-$3,000) offset by $1,000 premium = -$2,000 net loss (-6.5%)

Breakeven:

- 📊 Effective breakeven: $298-302 (assignment price $310 minus $8-12 premium collected)

- 🎯 Only lose money if stock below $298-302 at Feb 20 expiration

CRITICAL REQUIREMENTS - DO NOT attempt unless you:

- ✅ Actually WANT to own GOOGL at $310 and plan to hold long-term if assigned

- ✅ Have cash available ($31,000 per put) or sufficient margin

- ✅ Can stomach volatility - stock might hit $280-290 intraday causing mark-to-market losses

- ✅ Understand assignment mechanics and early assignment risk (low but possible)

- ✅ Are comfortable tying up capital for 77 days

Advanced variation: Sell multiple strikes ($310, $315, $320) in smaller size to average into position if assigned

Risk level: MODERATE-HIGH (assignment risk, capital intensive) | Skill level: Intermediate-Advanced

Probability of profit: ~60-70% (stock likely stays above $310 based on gamma support and technical levels)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📅 Q4 earnings binary event in ~7 weeks: Results late January/early February 2026 create SIGNIFICANT volatility risk. Stock could gap 8-12% either direction based on revenue (consensus ~$92-93B), Cloud growth (need 30%+ to maintain), and Gemini monetization commentary. Historical precedent: Feb 2025 Q4 earnings saw stock fall 9% on revenue miss. Options pricing ±4.2% implied move but actual moves can exceed this.

-

🚨 AI search cannibalization accelerating: CTR declines (paid and organic at "new lows"), 60% zero-click searches, 18-64% organic traffic drops threaten Google's $200B+ advertising business. If Search revenue growth decelerates materially below 10%, stock could re-rate lower 15-20%. AI Overviews helping user experience but potentially cannibalizing core business model.

-

💸 Capital expenditure at $85B+ with unclear ROI timeline: Stock fell 9% when CapEx guidance raised in Feb 2025. Investors remain skeptical of AI infrastructure spending without corresponding revenue growth. If ANOTHER CapEx increase announced without revenue acceleration, market could punish stock 10-15%.

-

🥊 ChatGPT competition intensifying: OpenAI at $13B annualized revenue, 9% of global queries, near-parity with Google among 18-24 year olds. Generational threat real - young users adopting ChatGPT as default. If this trend accelerates, Google's search moat erodes. Microsoft Copilot integration across Office 365 creates additional enterprise threat.

-

⚖️ Antitrust overhang not completely resolved: While September 2025 ruling avoided Chrome/Android divestitures, data sharing requirements could strengthen competitors. Appeal timeline potentially 2-3 years, creating uncertainty. Additional enforcement actions possible globally (EU DMA compliance, other jurisdictions).

-

🎯 Valuation at 31.53 P/E requires perfect execution: While cheaper than Nvidia (31.8x) and Microsoft (31.8x), Google trading above historical 20-25x average. At $3.83T market cap, stock needs continued Cloud acceleration (35%+ growth), Waymo commercialization success, and AI monetization to justify valuation. Limited margin for error.

-

🐋 $34M institutional call sale at peak signals profit-taking: When sophisticated players exit deep ITM positions worth $34M rather than holding for additional upside, it's a yellow flag. They clearly believe risk/reward NO LONGER favorable at current levels. The 2.21 Z-score (HIGHLY UNUSUAL classification) shows this is NOT normal activity - this is intentional derisking.

-

📊 Gamma resistance at $330 creates mechanical selling pressure: Massive call gamma at $330 (28.1M) means market makers systematically SELL into rallies to hedge their short call exposure. This creates natural ceiling making breakouts difficult. Would need sustained buying to overcome.

-

🎢 Low implied volatility (3-4%) creates complacency risk: Market pricing minimal near-term movement, but Q4 earnings could deliver 8-12% surprise move. Protective options relatively cheap NOW but will become expensive as earnings approaches. Waiting too long to hedge could be costly.

-

💰 Waymo expansion requires massive capital with losses continuing: Currently part of "Other Bets" with $1.25B quarterly losses. While revenue trajectory toward $260M annually, profitability timeline unclear. Regulatory hurdles in new markets, competition from Tesla/Cruise/Zoox intensifying.

🎯 The Bottom Line

Real talk: Someone just cashed out $34 MILLION in Google call options at all-time highs after the stock's epic 67% YTD rally. This isn't bearish on Google's long-term AI story - it's SMART money management by institutions who made HUGE profits and want to lock them in before Q4 earnings risk.

What this trade tells us:

- 💎 Sophisticated player made 1000-1500% gains on these $260 calls (bought around $40-60, selling at $679)

- 🎯 They're banking profits at $322 rather than gambling on further upside to $350-370

- ⚖️ The timing (77 days before Feb expiration, ~6-7 weeks before Q4 earnings) shows they see risk/reward turning unfavorable

- 📊 They structured exit as deep ITM calls (92% intrinsic value, only 8% time value) - pure profit extraction

- ⏰ February 20th expiration would capture Q4 earnings volatility - they're AVOIDING this binary event

This is NOT a "sell everything and run" signal - it's a "mission accomplished, take some chips off the table" signal.

If you own GOOGL:

- ✅ Consider trimming 25-40% at $320-325 levels (lock in 67% YTD gains)

- 📊 If holding through Q4 earnings, set MENTAL STOP at $320 (massive gamma support) to protect remaining position

- ⏰ Don't get greedy - up 67% is INCREDIBLE! Protecting profits is smart investing

- 🎯 If earnings beat AND stock breaks $335, could re-enter trimmed shares on momentum to $350-370

- 🛡️ Consider buying protective puts at $310 level if holding large position (copy institutional hedging structure)

If you're watching from sidelines:

- ⏰ Late January/Early February 2026 is the moment of truth for Q4 earnings - DO NOT chase into all-time highs!

- 🎯 Post-earnings pullback to $310-320 would be EXCELLENT entry (5-8% off highs with strong gamma support)

- 📈 Looking for confirmation of: Cloud growth 30%+, Gemini 3 monetization, $155B+ backlog growth, AI revenue disclosure

- 🚀 Longer-term (6-12 months), Gemini 3 enterprise adoption, Waymo commercialization across 10+ cities, and Google Cloud $155B backlog conversion are legitimate catalysts for $350-380

- ⚠️ Current valuation (31.5x P/E) reasonable but requires flawless execution - one earnings stumble and it's back to $290-310

If you're bearish:

- 🎯 Don't fight 67% momentum into all-time highs - wait for earnings before shorting

- 📊 First resistance at $325, major resistance at $330 (28.1M gamma ceiling), extended resistance at $335-340

- ⚠️ Post-earnings put spreads ($330/$320 or $320/$310) offer defined-risk way to play downside after IV settles

- 📉 Watch for break below $320 - that's the trigger for potential cascade to $310, then $300

- ⏰ Timing is EVERYTHING: Premature bearish positioning risks getting steamrolled by AI optimism

Mark your calendar - Key dates:

- 📅 December 12, 2025 - Weekly OPEX (±3.06% implied move)

- 📅 December 19, 2025 - Monthly OPEX / Triple Witch (±4.22% implied move)

- 📅 Late January/Early February 2026 - Q4 2025 earnings report (MAJOR CATALYST!)

- 📅 February 20, 2026 - Monthly OPEX, expiration of this $34M call trade

- 📅 April 2026 - Q1 2026 earnings (Gemini 3 full quarter monetization data)

- 📅 Mid-2025 onward - Waymo expansion to Dallas, Houston, San Antonio, Orlando, Nashville

Final verdict: Google's long-term AI story remains INCREDIBLY compelling - Gemini 3 benchmark dominance, Warren Buffett's $4.9B endorsement, favorable antitrust ruling, $155B Cloud backlog, and Waymo commercialization are all real and material. BUT, at 31.5x P/E after 67% YTD gain with Q4 earnings in 6-7 weeks, the risk/reward is NO LONGER heavily skewed to upside. The $34M institutional call sale is a CLEAR signal: smart money is banking extraordinary gains.

Be patient. Let earnings provide clarity. Look for better entry points at $310-320. The AI revolution will still be here in 2-3 months, and you'll sleep better at night buying at $315 instead of $322.

This is a marathon, not a sprint. Protect your capital and don't chase. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 2.21 Z-score (HIGHLY UNUSUAL) classification reflects this specific trade's statistical rarity relative to recent GOOGL history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Q4 earnings create binary event risk with potential for 8-12% gaps either direction. The call seller may have complex portfolio hedging needs, tax considerations, or institutional mandates not applicable to retail traders.

About Alphabet Inc.: Alphabet is the holding company that wholly owns internet giant Google, generating ~90% of revenue from Google services (primarily advertising), along with Google Cloud, YouTube subscriptions, Waymo autonomous vehicles, and emerging technology investments, with a market cap of $3.83 trillion in the Computer Programming & Data Processing industry.