💎 META $14.7M Call Selling - Institutional Upside Cap Before Q4 Earnings! 🛡️

📅 January 7, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just executed $14.7 MILLION in call selling on META across two massive trades this morning! Combined, 2,594 contracts of $630 strike calls expiring March 20th were sold - strategically capping upside at $630 (4% below current price) through Q4 earnings and Q1 2026. With META at $656.43 after a 12.64% recovery from November lows, smart money appears to be either writing covered calls for income or taking a neutral-to-bearish stance heading into the Q4 earnings catalyst. Translation: Institutional players are betting META won't rally significantly above $630 through March, potentially reflecting caution around AI CapEx concerns and Reality Labs restructuring!

📊 Company Overview

Meta Platforms (META) is the global social media powerhouse owning Facebook, Instagram, WhatsApp, and Threads, while aggressively investing in AI and metaverse technologies:

- Market Cap: $1.66 Trillion (3rd largest in tech)

- Industry: Interactive Media & Services

- Current Price: $656.43 (recovered from -21% Q3 correction)

- Primary Business: Digital advertising (90%+ of revenue), AI infrastructure, Reality Labs (VR/AR/smart glasses)

💰 The Option Flow Breakdown

The Tape (January 7, 2026):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:37:04 | META | BID | SELL | CALL $630 | 2026-03-20 | $9.6M | $630 | 1,700 | 2,700 | 1,692 | $656.43 | $57.00 |

| 09:39:04 | META | BID | SELL | CALL $630 | 2026-03-20 | $5.1M | $630 | 2,600 | 2,700 | 902 | $656.19 | $56.80 |

Combined Position: 2,594 contracts at $630 strike for $14.7M total premium collected

🤓 What This Actually Means

This represents a sophisticated covered call or bearish positioning play! Here's what transpired:

- 💸 Premium collected: $14.7M total ($56.80-$57.00 per contract × 2,594 contracts)

- 🎯 Upside cap: $630 strike is 4% BELOW current $656 price - already in-the-money!

- ⏰ Strategic timing: 72 days to expiration captures Q4 2025 earnings (late Jan/early Feb) and Q1 2026 developments

- 📊 Size matters: 2,594 contracts represents 259,400 shares worth ~$170M

- 🏦 Two scenarios: Either covered call income generation OR naked short call speculation

What's really happening here:

Scenario 1 (Most Likely): Covered Call Writing This trader likely owns 259,400+ shares of META stock and is selling calls against their position. By collecting $56.80-$57.00 per share for the March 20 $630 calls, they're generating 8.7% income over 72 days while capping their upside at $630. This suggests they believe META will trade range-bound or decline slightly through March, OR they're willing to sell their shares at $630 (~4% below current levels).

Why write calls at a strike BELOW current price? Because the calls are already ITM, they provide MORE premium income ($57 vs perhaps $35-40 for ATM $655 calls). The trade-off is they'll likely be assigned if META stays above $630, but they still profit on the premium collected.

Scenario 2 (Higher Risk): Naked Short Call Speculation If this is a naked call sell (without owning stock), the trader is making an outright bearish bet that META won't remain significantly above $630 by March 20th. This carries UNLIMITED upside risk but profits if META declines or trades sideways. The fact that both trades hit the BID (seller was aggressive, willing to take lower prices) suggests urgency to establish the position.

Unusual Score: 🔥 EXTREMELY_UNUSUAL (Z-scores of 7.34 and 11.42) - This is 7-11 standard deviations above normal META call selling activity! We're talking about nearly $15M in premium collected in under 2 minutes. Only a handful of larger trades in the past 30 days.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

META shows a volatile 2025 - up +10.96% YTD at $656.43, but the chart reveals a more complex story. After hitting an all-time high of $796.25 in August 2025, META suffered a brutal 21% correction through November on AI CapEx concerns, bottoming at $585.66 on November 19th. The stock has since recovered 12.64% but remains 17.5% below its August peak.

Key observations:

- 🎢 Major volatility: From $796 high to $585 low represents 26.5% peak-to-trough drawdown

- 📉 Q3 correction: Sold off sharply after October 29th earnings despite revenue beat, driven by massive AI CapEx guidance ($70B+ for 2025)

- 📈 Recovery mode: Strong bounce from November lows on FTC antitrust victory and improved sentiment

- 🧱 Resistance ahead: $630 strike sits at a key technical level where price consolidated in November

- ⚠️ Overhead supply: $680-$700 range represents major resistance zone before August highs

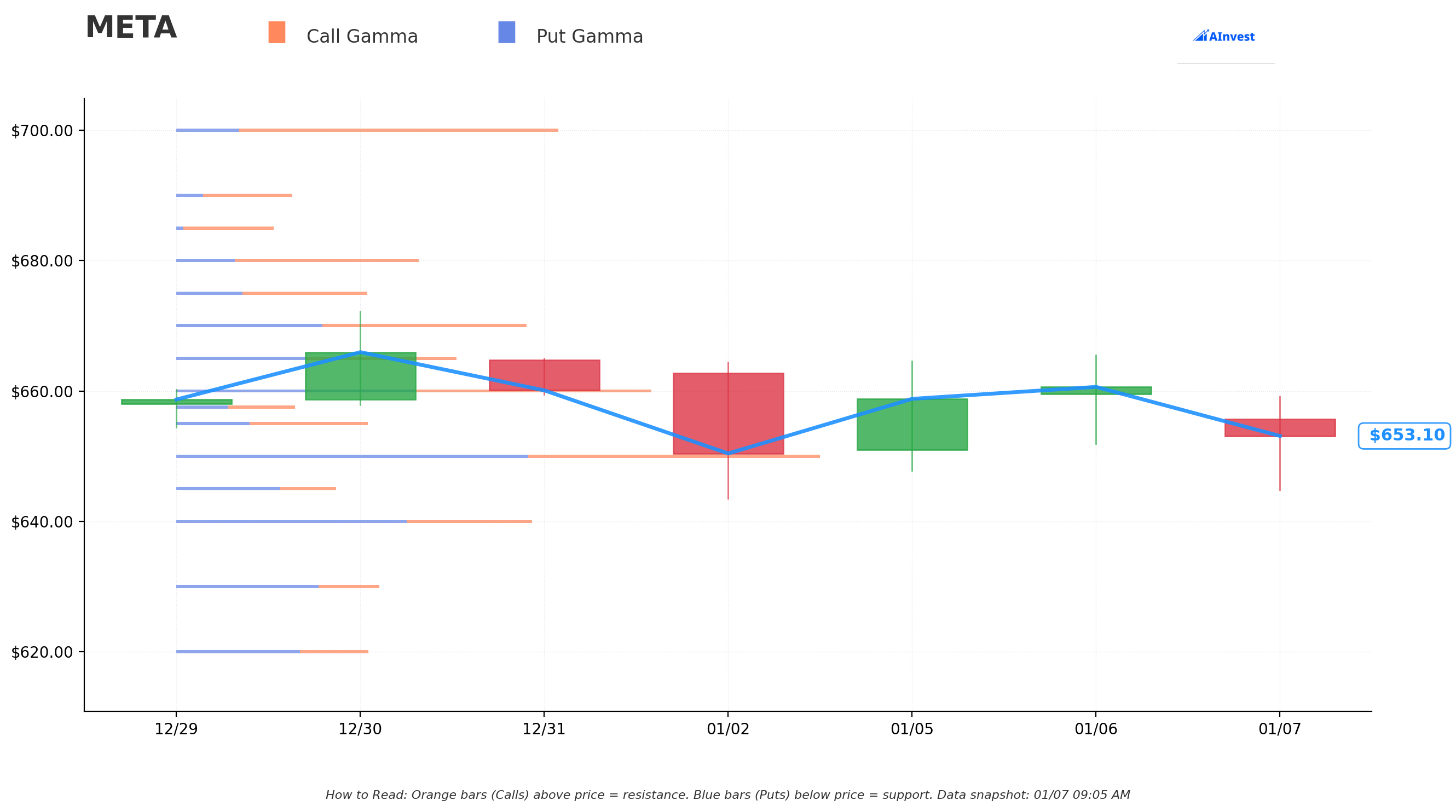

Gamma-Based Support & Resistance Analysis

Current Price: $656.43

The gamma exposure map reveals critical price magnets and barriers governing near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $655 - Immediate support with strong put gamma concentration (current floor!)

- $650 - Secondary support zone with dealer buying interest

- $640 - Major structural floor with heavy gamma exposure (sellers likely defend this level)

- $630 - Deep support corresponding to the call strike! (14.8B gamma - NOT COINCIDENTAL)

- $620 - Extended support zone

- $600 - Disaster floor from November lows area

🟠 Resistance Levels (Call Gamma Above Price):

- $660 - Immediate ceiling with significant call gamma (dealers will sell rallies here)

- $670 - Secondary resistance zone (2% overhead)

- $680 - Major ceiling with heavy gamma concentration (3.6% above current)

- $700 - Extended upside target requiring major catalyst

- $720 - Implied move upper bound for quarterly expiration

What this means for traders: META is trading in a consolidation range between $650-$670 with the heaviest resistance at $660 and $680. The gamma data shows market makers holding large positions at these strikes, creating natural selling pressure as price approaches. Notice the $630 strike aligns PERFECTLY with a major gamma support level - the call sellers are positioned just below key technical support, expecting that IF META breaks down, it could flush to $630 quickly.

Net GEX Bias: Neutral-to-slightly-bearish short-term, with consolidation expected in $630-$680 range through March expiration.

Implied Move Analysis

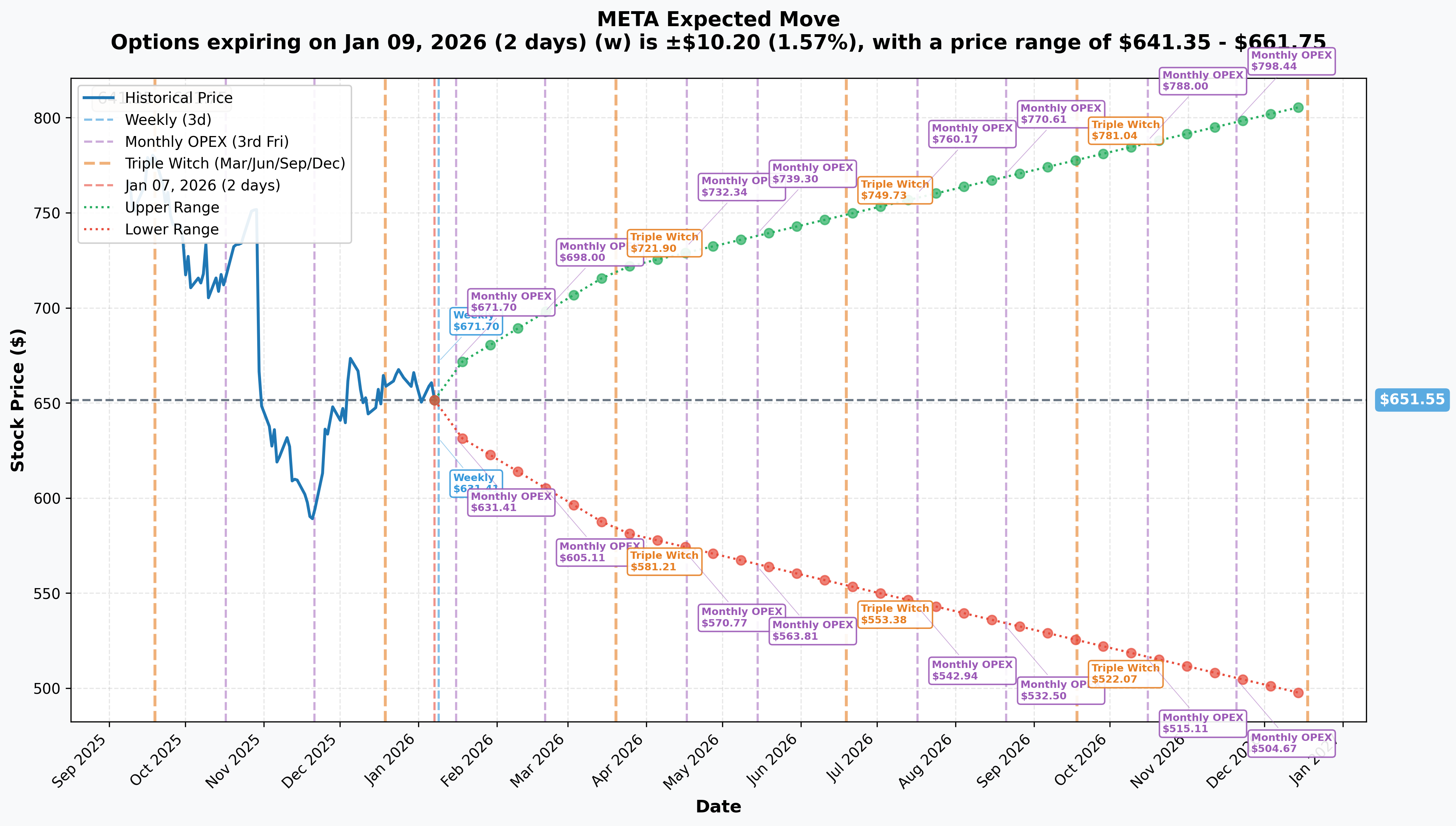

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 2 days): ±$10.20 (±1.57%) → Range: $641.35 - $661.75

- 📅 Monthly OPEX (Jan 16 - 9 days): ±$18.55 (±2.85%) → Range: $633.00 - $670.11

- 📅 Quarterly (Mar 20 - 72 days - THIS TRADE!): ±$68.77 (±10.55%) → Range: $582.79 - $720.32

Translation for regular folks: Options traders are pricing in a modest 1.57% move ($10) this week, expanding to a 2.85% move ($18.55) through monthly OPEX which likely includes Q4 earnings volatility. However, by March 20th quarterly expiration (when these calls expire), the market expects a MASSIVE 10.55% potential move ($68.77) - reflecting significant uncertainty around Q4 earnings, Reality Labs restructuring, and the Avocado AI model launch.

The March 20th expiration has an upper range of $720.32 - meaning the market assigns reasonable probability META could trade as high as $720 over the next 72 days IF execution is flawless. However, the call sellers at $630 strike are betting this won't happen - they're capping their exposure $90 BELOW the implied move upper bound.

Key insight: The 10.55% quarterly implied volatility reflects elevated uncertainty around multiple catalysts. The call sellers are taking the OPPOSITE side of this volatility, betting on range-bound trading or downside.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Q4 2025 Earnings - Late January/Early February 2026 (20-30 DAYS AWAY!) 📊

META will report fiscal Q4 2025 results in late January or early February 2026. This is THE most critical catalyst that could break the stock out of its current range or send it tumbling. Wall Street consensus:

- 📊 Revenue: $56-59B (company guidance from Q3 call) - representing 18-24% YoY growth

- 💰 EPS: $8.19-$8.29 consensus (significant growth from $7.25 in Q3)

- 🤖 AI Revenue Run Rate: Watching for progress beyond current $60B+ annual run rate

- 📈 Family DAP: Expected 3.55B+ daily active people (continued 7-8% growth)

- 💻 Reality Labs: Critical to see if losses remain at $4.4B quarterly or if budget cuts materialize

- 🎯 2026 CapEx Guidance: Market terrified of further expansion beyond $70-72B 2025 levels

Upside surprise potential: If META demonstrates AI tools driving better-than-expected ad pricing power (+12-15% vs Q3's +10%), announces Ray-Ban glasses holiday blowout sales, or provides conservative 2026 CapEx guidance, stock could rally to $700+.

Downside risk factors: Any disappointment in revenue ($55B or below), Reality Labs losses INCREASING beyond $4.4B, aggressive 2026 CapEx guidance ($80B+), or weak Threads monetization progress could trigger selloff to $600-620 range. The Q3 2025 earnings reaction (stock down despite revenue beat) shows how sensitive investors are to CapEx concerns.

Historical precedent: META has shown 8-15% post-earnings moves on guidance surprises. Given 29.15x trailing P/E (elevated for Meta historically), expectations are HIGH.

🚀 Near-Term Catalysts (Q1 2026 - Through March 20 Expiration)

Avocado AI Model Launch - Q1 2026 🤖

META's next-generation text LLM represents a MAJOR strategic shift and potential catalyst:

- 🎯 Built by Meta Superintelligence Labs (led by Alexandr Wang from $14.3B Scale AI acquisition)

- 🔒 CRITICAL CHANGE: Expected to be closed-source, departing from Llama's open-source philosophy

- 💰 Revenue potential: Could significantly enhance AI ad tools beyond current $60B run rate

- 📊 Improved coding and reasoning capabilities targeting enterprise applications

- ⚠️ MAJOR RISK: CNBC reported internal confusion around shifting AI strategy in December 2025 - execution risk elevated

- 🎪 Launch timing within March 20 expiration window could move stock dramatically either way

Why this matters for the call trade: If Avocado launch encounters delays, performance issues, or negative developer reception (backlash against closed-source shift), META could decline sharply. The call sellers are positioned to profit from disappointment scenarios.

Reality Labs Restructuring - January 2026 🔨

Bloomberg reported potential 30% budget cut to metaverse teams with layoffs potentially beginning January 2026:

- 💸 Current Reality Labs losses: $4.4B per quarter, ~$70B cumulative since 2020

- 🎯 Budget cuts could IMPROVE profitability significantly (reduce quarterly losses to $3B range)

- 📉 But signals strategic retreat from metaverse vision that Zuckerberg championed

- 🎮 Quest 4 development reportedly delayed; focus shifting to ultralight tethered headset

- ⚖️ Mixed implications: Cost reduction bullish for margins, but strategic pivot could disappoint true believers

Potential catalyst timing: Announcements likely during or shortly after Q4 earnings call. If cuts are deeper than expected (40-50% reduction), could be viewed positively. If minimal cuts announced, suggests Meta doubling down despite losses.

Threads Monetization Progress 💬

- 📊 Current: 400M monthly users, 150M daily users (surpassed X in September 2025)

- 💰 Evercore ISI projects: $8B revenue end of 2025, ramping to $11.3B in 2026

- 🎯 Ad integration expansion expected throughout Q1 2026

- 📈 Watching for Q4 earnings commentary on Threads revenue contribution

- ⚠️ Risk: If monetization slower than expected, questions Meta's ability to build new revenue streams

2026 CapEx Expansion Concerns 💸

CFO Susan Li already confirmed 2026 CapEx dollar growth will be "notably larger" than 2025's $70-72B:

- 🚨 This is THE biggest overhang on the stock - market fears $80-90B CapEx in 2026

- 📊 Primarily for AI infrastructure (data centers, NVIDIA GPUs) and talent

- ⚖️ Bulls argue necessary investment for long-term AI dominance; bears see profitless growth

- 💰 Every $10B incremental CapEx reduces EPS by ~$1-2, impacting valuation

- 📉 Q3 correction (-21%) was ENTIRELY driven by CapEx concerns despite revenue beat

The call sellers may be betting: If 2026 CapEx guidance comes in at $85B+ during Q4 earnings, stock sells off 10-15% regardless of Q4 results quality.

📊 Market Position & Competitive Dynamics

Advertising Market Dominance:

- META, Alphabet, and Amazon expected to capture 50%+ of global ad spending in 2025, expanding to 56.2% in 2026

- AI-driven ad targeting delivering both impression growth (+14% in Q3) AND pricing power (+10%)

- Family of Apps: 3.54B daily active users - largest social media ecosystem globally

Smart Glasses Success (Bright Spot):

- Ray-Ban Meta glasses sales tripled YoY in H1 2025 (200%+ growth)

- 73% market share in smart glasses segment - dominant position

- 2M+ pairs sold, with Ray-Ban Display models selling out within 2 days

- $3B investment in EssilorLuxottica (3% stake) - strategic partnership locked in

Competitive Threats:

- TikTok continues capturing younger demographics' attention

- YouTube/Google competing directly in short-form video

- Apple potential entry into smart glasses market

- OpenAI, Google, Anthropic in AI model race - Avocado must deliver

⚠️ Risk Catalysts (Negative)

FTC Antitrust Victory - Mixed Blessing:

- November 18, 2025 court ruling in Meta's favor eliminated major regulatory overhang

- However, Congressional proposals (S. 130) could enable future enforcement actions

- EU ongoing scrutiny despite DMA fine resolution - regulatory risk remains

China Relations & Manus AI Acquisition:

- $2B Manus AI acquisition (December 2025) drew scrutiny over Chinese roots

- Geopolitical tensions could complicate future M&A or partnerships

Valuation at 29.15x Trailing P/E:

- Trading near historical high-end of valuation range

- Requires continued 20%+ revenue growth to justify multiple

- Limited margin of safety if execution stumbles

🎲 Price Targets & Probabilities Through March 20 Expiration

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20, 2026:

📈 Bull Case (25% probability)

Target: $700-$720

How we get there:

- 💪 Q4 earnings CRUSH with revenue at $59B+ (high-end of guidance) and margins expanding

- 🚀 Avocado AI model launches successfully with strong developer adoption despite closed-source approach

- 💰 Reality Labs budget cuts announced (~30-40% reduction) improving profitability outlook

- 📊 2026 CapEx guidance comes in BELOW feared levels ($75-78B vs feared $85B+)

- 🤖 AI ad tools revenue run rate accelerates to $75B+ annual, demonstrating clear ROI

- 📱 Ray-Ban glasses Q4 sales exceed expectations, Threads monetization progressing faster than expected

- 🌐 Breakout above $670 gamma resistance triggers technical rally to $700+

Key metrics needed:

- Q4 revenue >$58.5B with Q1 2026 guidance showing acceleration

- Reality Labs losses declining below $4B quarterly

- Family DAP growth maintaining 7-8% YoY

- Gross margins stable or expanding despite AI investments

Probability assessment: Only 25% because it requires nearly perfect execution across multiple dimensions with stock already 17.5% below August highs. The $14.7M call selling at $630 suggests smart money doesn't believe this scenario is likely. Gamma resistance at $660-$680 creates mechanical headwinds.

🎯 Base Case (50% probability)

Target: $620-$670 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Q4 earnings meet consensus (~$57-58B revenue, $8.20-8.30 EPS)

- 📱 Avocado AI model launches but reception mixed - no major positive or negative surprise

- ⚖️ Reality Labs budget cuts announced but modest (20-25% reduction, not 30%+)

- 💸 2026 CapEx guidance in-line with fears ($80-82B) - neither positive nor negative surprise

- 🤖 AI revenue growth steady but not accelerating - maintains current trajectory

- 🔄 Trading within gamma support ($640-$650) and resistance ($660-$670) bands

- 📊 Market digests 2025 gains, waits for 2026 proof points before next major move

- 💤 Volatility normalizes post-earnings from elevated levels

This is the call sellers' IDEAL scenario: Stock consolidates in $620-660 range, calls expire worthless or minimal value at March 20 expiration. If stock is at $625 at expiration, they keep the full $14.7M premium collected and their stock (if covered call). If stock is at $650, they keep ~$8-10M of the premium (calls worth $20 intrinsic value).

Why 50% probability: Stock at technical inflection point without clear fundamental catalyst for major move either direction. Valuation reasonable but not cheap (29x P/E). Most institutions will hold and wait for tangible Avocado/Reality Labs results before major repositioning.

Call P&L in Base Case:

- Stock at $625 at Mar 20: Calls expire worthless, sellers keep full $14.7M (100% gain)

- Stock at $650 at Mar 20: Calls worth $20, sellers keep $37/share × 2,594 = $9.6M (65% gain)

- Stock at $660 at Mar 20: Calls worth $30, sellers keep $27/share × 2,594 = $7M (48% gain)

📉 Bear Case (25% probability)

Target: $580-$620 (TEST 2025 LOWS)

What could go wrong:

- 😰 Q4 earnings disappoint with revenue $55-56B (below guidance), or weak Q1 2026 outlook

- 🚨 Avocado AI model delayed beyond Q1, or launches with poor reception/performance vs competitors

- 💸 2026 CapEx guidance shocks at $90B+ with unclear ROI timeline, triggering profitability concerns

- 📉 Reality Labs losses INCREASE to $5B+ quarterly, no meaningful budget cuts announced

- 🤖 AI ad tools growth decelerating, questions about whether $60B run rate is peak

- 🇨🇳 EU regulatory issues resurface, or U.S. antitrust concerns return despite court victory

- 💰 Broader tech selloff drags high-multiple stocks lower (macro recession fears)

- 🔨 Break below $640 gamma support triggers cascade to $620, then $600

Critical support levels:

- 🛡️ $650: Immediate support - MUST HOLD or momentum shifts bearish

- 🛡️ $640: Major gamma floor - breaking this level accelerates selling

- 🛡️ $630: Call strike + major support - heavy volume expected here

- 🛡️ $600: November 2025 low area - disaster scenario

Probability assessment: 25% because it requires multiple negative catalysts simultaneously. Meta's fundamentals remain strong (26% revenue growth, $60B AI run rate, 3.54B DAP), but elevated CapEx and Reality Labs losses create vulnerability. The call sellers clearly think this scenario has >25% odds or they wouldn't have collected $14.7M in premium on ITM calls.

Call P&L in Bear Case:

- Stock at $600 at Mar 20: Calls worth $0 (expired OTM), sellers keep full $14.7M + stock declined $56 (net wash if covered call, huge gain if naked short)

- Stock at $620 at Mar 20: Calls worth $0 (expired OTM), sellers keep full $14.7M (100% gain)

- Stock at $630 at Mar 20: Calls worth $0 (expired exactly ATM), sellers keep full $14.7M (100% gain)

This is the MAX PROFIT scenario for call sellers - stock declines to or below $630 strike, calls expire worthless.

💡 Trading Ideas

🛡️ Conservative: Cash-Secured Put Selling Below Support

Play: Sell cash-secured puts at $630 strike (March 20 expiration) if stock pulls back to $640-645

Structure: Sell $630 puts, collect ~$25-30 premium, secure with cash to buy stock if assigned

Why this works:

- 💰 Collect premium while waiting for better stock entry point

- 🎯 $630 strike aligns with major gamma support AND the unusual call selling level

- 📊 If assigned, you own META at effective cost basis of $600-605 ($630 strike - $25-30 premium)

- ⏰ 72 days time decay works in your favor

- 🛡️ Only enter if bullish long-term on META but want better entry than current $656

Estimated P&L:

- 💰 Collect $25-30 per contract ($2,500-3,000 per put)

- 📈 Best case: Stock stays above $630, keep full premium (10-12% return in 72 days)

- 📊 Neutral case: Assigned at $630, effective basis $600-605, own quality stock at discount

- 📉 Worst case: Stock crashes to $550, own stock with unrealized loss but 20-year hold quality

Risk level: Moderate (could own stock at higher basis than market if META crashes) | Skill level: Intermediate

⚖️ Balanced: Bull Put Spread Below The Strike

Play: Sell bull put spread taking advantage of elevated IV before earnings

Structure: Sell $630 puts / Buy $620 puts (March 20 expiration - SAME as unusual activity)

Why this works:

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Positioned at same $630 level where institutions are clearly active (call selling)

- 💰 Collect ~$3-4 net credit per spread (30-40% max return on risk)

- 🛡️ Breakeven around $626-627, below current price and major support levels

- ⏰ Benefits from time decay and volatility crush post-earnings

- 🤝 Essentially betting WITH the institutional call sellers that stock stays above $630

Estimated P&L:

- 💰 Collect $3-4 credit per spread ($300-400 per spread)

- 📈 Max profit: $300-400 if META above $630 at March 20 (30-40% ROI)

- 📊 Breakeven: ~$626-627

- 📉 Max loss: $600-700 if META below $620 (defined risk)

Entry timing:

- ⏰ Enter AFTER Q4 earnings (late Jan/early Feb) once IV crush occurs

- 🎯 Look for stock stabilization above $640-645 before entering

- ❌ Skip if stock already below $635 (too close to strike)

Position sizing: Risk 2-3% of portfolio maximum (5-10 spreads for $50K account)

Risk level: Moderate (defined risk, directional assumption) | Skill level: Intermediate

🚀 Aggressive: Earnings Straddle - Volatility Play (ADVANCED ONLY!)

Play: Buy straddle betting Q4 earnings volatility exceeds implied move

Structure: Buy ATM calls + ATM puts at $655 strike (February 21 expiration to capture earnings)

Why this could work:

- 💥 Implied move only 2.85% monthly but META has history of 10-15% post-earnings moves

- 🎰 At 29x P/E with massive CapEx uncertainty, stock could EXPLODE either direction

- 📊 If Q4 beat + conservative CapEx guidance → rally to $720+

- 📉 If Q4 miss or aggressive CapEx guidance → crash to $600

- ⚡ Only need stock to move >8-10% to profit after IV crush

- 🔥 The $14.7M call selling suggests major players expect BIG MOVEMENT

Why this could blow up (SERIOUS RISKS):

- 💸 EXTREMELY EXPENSIVE: Straddle costs ~$50-60 ($5,000-6,000 per straddle)

- ⏰ TIME DECAY BRUTAL: Theta burns -$200-300/day approaching earnings

- 😱 IV CRUSH DEVASTATING: Even 10% move might result in LOSS if IV collapses 60-70%

- 📊 Two-way risk: Stock could stay in $640-670 range, lose majority of premium

- 🎢 Need 12-15% move just to breakeven after IV crush

- ⚠️ Earnings could be "solid but uninspiring" - stock gaps to $670-680 (only 5% move), straddle loses 50-60%

Estimated P&L:

- 💰 Cost: ~$50-60 per straddle

- 📈 Profit scenario: Stock moves to $720+ or $580 (12-15%+ move) = $40-50 gain (70-100% ROI)

- 🚀 Home run: Stock moves to $750 or $550 (20%+ move) = $90+ gain (150%+ ROI)

- 📉 Loss scenario: Stock ends $630-680 range = lose $30-45 (50-75% loss)

- 💀 Total loss: Stock flat at $655 = lose entire $50-60 (100% loss)

CRITICAL WARNING - DO NOT attempt unless:

- ✅ You've traded earnings straddles before and understand IV crush mechanics

- ✅ Can afford to lose ENTIRE premium (realistic possibility)

- ✅ Can monitor position immediately post-earnings and take profits within 24-48 hours

- ✅ Accept you're betting AGAINST options market pricing

- ⏰ Have plan to close position quickly if profitable (don't get greedy)

Risk level: EXTREME (can lose 100%) | Skill level: Advanced only | Probability of profit: ~35-40%

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 Earnings binary event in 20-30 days: Results in late January create MASSIVE volatility risk. Stock could gap 10-15% either direction based on revenue ($56B vs $59B makes huge difference), 2026 CapEx guidance ($75B vs $85B changes narrative dramatically), and Reality Labs restructuring details. The October Q3 earnings showed META can sell off 10-15% even on revenue beats if CapEx concerns dominate.

-

💸 AI CapEx with uncertain ROI: Already spending $70-72B in 2025 with 2026 guidance expected "notably larger" - potentially $80-90B. While AI ad tools generating $60B run rate is impressive, market fears spending will spiral without proportional revenue growth. Every $10B incremental CapEx reduces EPS significantly. Q3's -21% selloff was ENTIRELY CapEx-driven despite strong fundamentals.

-

🤖 Avocado AI execution risk: Shifting from open-source Llama to closed-source Avocado creates strategic uncertainty. CNBC reported internal confusion in December 2025 around the pivot. Developer community may resist closed-source approach. Launch delays or poor performance vs OpenAI/Google/Anthropic would be devastating to AI narrative. This is Q1 2026 deliverable within call expiration window.

-

💰 Reality Labs $70B money pit: Cumulative losses of ~$70B since 2020 with $4.4B quarterly burn rate continuing. While Ray-Ban glasses success is encouraging (73% market share, 200%+ growth), Quest headset business struggles. Budget cuts signal potential strategic retreat from metaverse vision. If cuts are LESS than expected or losses INCREASE, major negative catalyst.

-

🌍 Regulatory overhang despite FTC victory: While November 18 court ruling eliminated immediate antitrust threat, EU ongoing scrutiny continues. Congressional proposals could enable future enforcement. Manus AI acquisition ($2B, December 2025) drew scrutiny over Chinese roots. International regulatory landscape remains uncertain.

-

📊 Valuation at 29.15x trailing P/E: Trading near high-end of historical range (typically 20-30x). Requires sustained 18-25% revenue growth to justify multiple. Limited margin of safety if growth decelerates or margins compress. Forward P/E of 22.03x assumes flawless execution.

-

🎢 $14.7M institutional call selling signals caution: When sophisticated players collect $14.7M premium by selling calls at $630 (4% BELOW current price), they're signaling limited upside conviction through March. The fact they sold ITM calls (sacrificing some upside for higher premium) suggests they REALLY don't expect significant rally. This is major red flag.

-

📉 Technical resistance at $660-$680: Gamma data shows heavy call gamma at $660 (34.5B) and $680 - market makers will systematically SELL into rallies to hedge exposure. This creates mechanical selling pressure making breakouts difficult. Would need explosive earnings beat to overcome.

-

💬 Threads monetization uncertainty: While 400M MAU impressive, revenue contribution remains unclear. If Evercore's $8B 2025 revenue projection proves too optimistic, questions Meta's ability to build new revenue streams. Instagram Reels monetization took years - Threads timeline uncertain.

-

🌐 Competition from TikTok, YouTube: Despite 3.54B Family DAP, attention share shifting to competitors especially among younger demographics (18-34). Court ruling acknowledged TikTok/YouTube as direct competitors. Any engagement metric deterioration would be catastrophic.

-

💎 Smart glasses market untested long-term: Ray-Ban Meta success impressive (2M+ units) but total addressable market unknown. Apple potential entry could disrupt. Technology refresh cycles uncertain - will consumers upgrade annually like phones?

🎯 The Bottom Line

Real talk: Two separate institutional traders just collected $14.7 MILLION by selling calls at $630 (4% below current price) expiring in March. This isn't bearish on META's 5-year AI story - it's strategic positioning by sophisticated players who see limited upside through Q4 earnings and Q1 2026 developments.

What this trade tells us:

- 🎯 Smart money expects RANGE-BOUND trading between $600-$680 through March 20 expiration

- 💰 They're comfortable capping upside at $630 to collect $56.80/share premium (8.7% yield in 72 days)

- ⚖️ If covered calls, signals willingness to sell shares at $630 rather than hold through uncertainty

- 📊 If naked calls, outright bet that stock won't sustain levels above $630 through March

- ⏰ Timing (before Q4 earnings) shows they see binary risk - earnings could trigger sharp move either way but ultimate range likely $600-670

This is NOT a "sell everything" signal - it's a "don't expect $700+ near-term" signal.

If you own META:

- ✅ Consider writing covered calls at $670-$680 strikes (collect premium, cap upside at more reasonable levels than $630)

- 📊 If holding through earnings, set MENTAL STOP at $640 (major gamma support) to protect gains

- ⏰ Don't chase above $670 - resistance is real and institutional selling will cap rallies

- 🎯 If earnings beat AND stock breaks $680, could re-enter on momentum to $700-720

- 🛡️ For large positions, consider protective puts at $630 strike (copy this trade's level in reverse)

If you're watching from sidelines:

- ⏰ Late January/Early February Q4 earnings is the moment of truth - DO NOT enter before results!

- 🎯 Post-earnings pullback to $630-640 would be EXCELLENT entry (8-10% off current levels at major support)

- 📈 Looking for: Q4 revenue $58B+, 2026 CapEx <$80B, Reality Labs cuts 30%+, Avocado on-track for Q1

- 🚀 Longer-term (12-24 months), AI ad tools scaling and Avocado success could drive $800-900 if execution delivers

- ⚠️ Current valuation (29x P/E) requires flawless execution - one stumble and it's back to $600-620

If you're bearish:

- 🎯 Wait for earnings before aggressive shorting - fighting recovery momentum into all-time highs is dangerous

- 📊 First support at $650 (gamma), major support at $640, critical support at $630 (call strike)

- ⚠️ Post-earnings put spreads ($650/$630 or $640/$620) offer defined-risk way to play downside

- 📉 Watch for break below $640 - that's the trigger for cascade to $630, then $600

- ⏰ Timing critical: Premature bearish positioning risks getting squeezed if earnings beat

Mark your calendar - Key dates:

- 📅 Late January/Early February 2026 - Q4 2025 earnings report (CRITICAL!)

- 📅 January 2026 - Reality Labs restructuring announcements expected

- 📅 Q1 2026 - Avocado AI model launch expected

- 📅 January 16 - Monthly OPEX (2.85% implied move through here)

- 📅 March 20, 2026 - Quarterly OPEX, expiration of this $14.7M call trade

- 📅 H2 2026 - Ultralight VR headset potential unveiling at Meta Connect

Final verdict: META's long-term fundamentals remain STRONG - 26% revenue growth, $60B AI ad tools run rate, 3.54B daily users, Ray-Ban glasses dominance (73% market share). BUT, at 29x P/E after recovering from November lows with Q4 earnings uncertainty ahead, the risk/reward favors patience. The $14.7M institutional call selling at $630 is a CLEAR signal: smart money doesn't expect explosive upside through March.

Wait for earnings clarity. The AI advertising revolution will still be here in February, and you'll sleep better paying $630-640 after volatility clears rather than chasing $656 into uncertainty.

Range-bound trading is the highest probability outcome. Protect your capital and wait for your pitch. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual call selling represents these specific traders' positions - they may have complex hedging strategies not applicable to retail traders. Earnings create binary event risk with potential for 10-15% gaps either direction. Always do your own research and consider consulting a licensed financial advisor before trading.

About Meta Platforms: Meta Platforms owns and operates Facebook, Instagram, WhatsApp, and Threads, serving 3.54 billion daily active users globally. The company generates 90%+ of revenue from digital advertising while investing heavily in AI infrastructure and Reality Labs (VR/AR/smart glasses), with a market cap of $1.66 trillion in the Interactive Media & Services industry.