🛢️ NEXT Someone Just Banked $1.8M Selling Calls on This LNG Rocket Ship - Here's the Real Story!

📅 March 24, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just collected $1.8 MILLION in premium by selling NEXT calls at 11:13 this morning! They sold 8,840 contracts of the $10 strike call expiring January 2028 - nearly two full years out - with NEXT trading at just $7.43. This is either a large shareholder locking in income by selling upside they don't expect to need, or a sophisticated trader making a bet that NEXT won't crack $10 before January 2028. Either way, the trade was hit aggressively on the BID - this seller wanted out NOW, not later.

📊 Company Overview

NextDecade Corporation (NEXT) is a Houston-based energy company building one of the largest LNG (liquefied natural gas) export facilities in the world:

- Market Cap: $1.9B

- Industry: Natural Gas Transmission & Distribution

- Current Price: ~$7.47 | YTD: +38.9%

- Primary Business: LNG liquefaction, sale of LNG, and CO2 capture/storage at the Rio Grande LNG facility in Brownsville, Texas

Real talk: NEXT is essentially a construction company right now. They have five massive LNG trains under construction worth roughly 30 MTPA of capacity, $13.4B in project financing locked in, and no revenue yet. But first LNG is expected H1 2027 - and the world just got a lot more interested in U.S. LNG after Iranian missiles struck Qatar's Ras Laffan LNG complex in March 2026.

💰 The Option Flow Breakdown

The Tape (March 24, 2026 @ 11:13:53):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Contract |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:13:53 | NEXT | BID | SELL | CALL | 2028-01-21 | $1.8M | $10 | 10K | 2.7K | 8,840 | $7.43 | $2.00 | NEXT20280121C10 |

🤓 What This Actually Means

Strategy: Short Call (STO) - LEAP covered call or naked short

This is a sold-to-open (STO) short call position - the seller is collecting premium up front and taking on the obligation to sell NEXT at $10 if it gets there by January 2028. Let's break it down:

- 💸 Premium collected: $1.8M ($2.00 per contract × 8,840 contracts × 100 shares)

- 📏 Strike distance: $10 is 34% above current price of $7.43 - a hefty buffer for the seller

- ⏰ Long runway: Nearly 2 years of time (January 21, 2028) for this position to play out

- 📊 Volume vs OI: 10,000 volume vs just 2,700 open interest = this is fresh new positioning, not someone closing out

- 🎯 Bid-side execution: This hit the BID aggressively - the seller didn't wait for a better price, they wanted the trade done immediately

Two scenarios for who's doing this:

Scenario A - Covered Call (most likely): A large NEXT shareholder is selling upside they don't expect to need. They hold thousands of shares and are pocketing $1.8M today in exchange for capping their gains at $10. With NEXT up 38.9% YTD after the Qatar crisis spike, this could be a long-term investor taking income off the table while still holding the stock.

Scenario B - Naked Short Call: A sophisticated trader is betting NEXT stays below $10 through January 2028. The $10 level is above the 52-week high area and above analyst price targets set before the Qatar crisis. This is a higher-conviction, higher-risk play - if NEXT explodes above $10, losses are theoretically unlimited.

Unusualness: 🔥 HIGH - Volume of 8,840 contracts against 2,700 open interest means this single trade is 3.3x the entire existing open interest at this strike. LEAP call selling of this size on a ~$1.9B market cap energy name happens a few times a year at most. The seller committed serious capital to a very specific view on where NEXT will trade nearly two years from now.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

NEXT is up +38.9% YTD and has been on a wild ride. The stock was grinding lower from near $6 in early March toward 52-week lows when the Iran-Qatar LNG crisis hit on March 18-19, sending the stock surging 27% in a single week. That kind of move compresses what the short call seller needs to worry about: NEXT would need to nearly double again from current levels to make the $10 short call a problem.

Key observations:

- 🚀 Geopolitical rocket: The 27% week-over-week surge was driven by a real supply shock, not hype

- 📉 Pre-crisis weakness: Stock was near 52-week lows at ~$5.61 on March 2 before the bounce

- 🎯 52-week range: $4.75 - $12.12 - yes, NEXT has been above $10 before (last year's highs)

- ⚠️ Pre-revenue: No operating revenue until Train 1 delivers first LNG in H1 2027

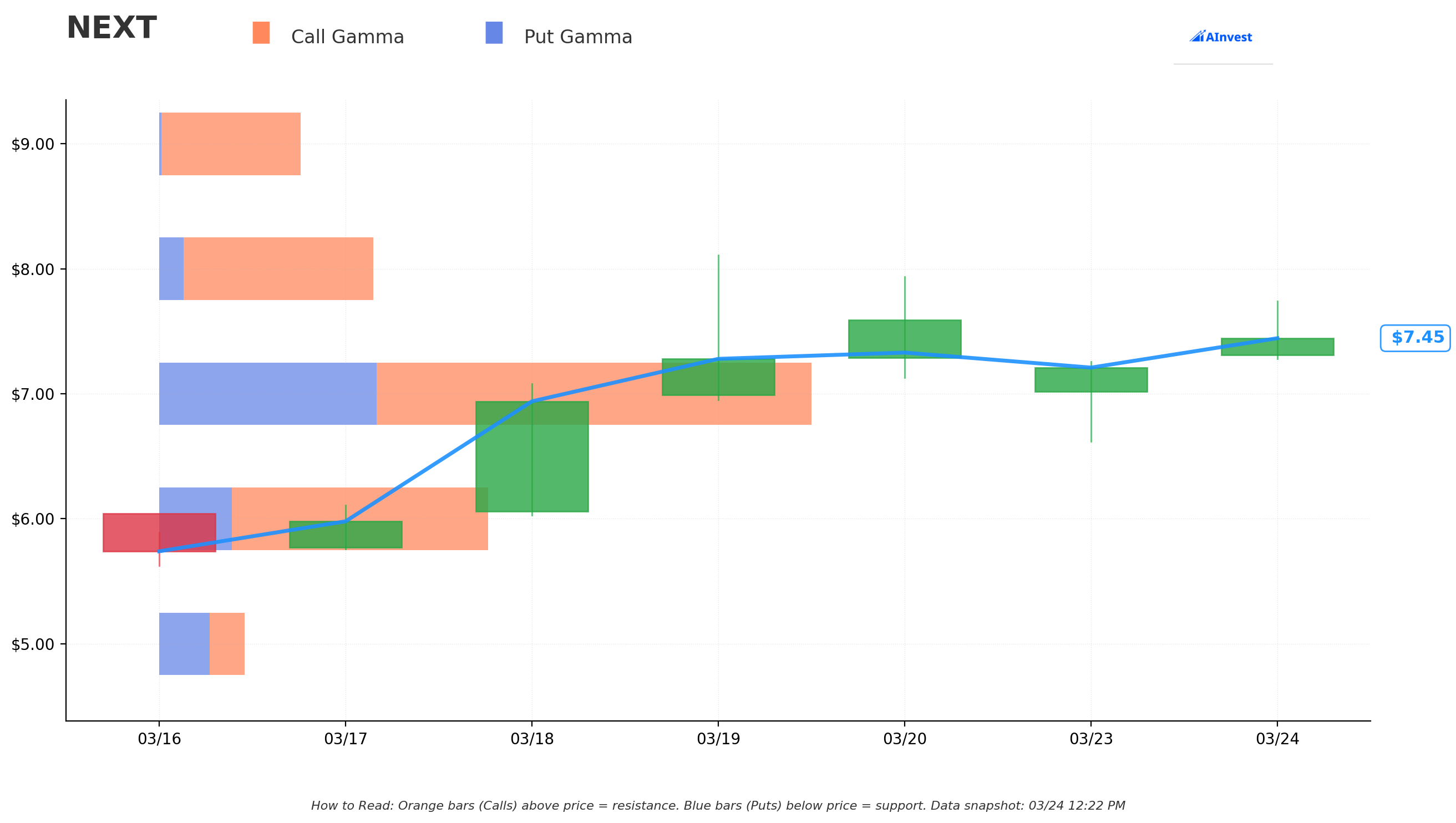

Gamma-Based Support & Resistance Analysis

The gamma exposure data shows a net bullish bias for NEXT right now, with call gamma significantly outweighing put gamma ($16.1 total call GEX vs $4.9 put GEX). Here's what the structure looks like:

🔵 Support Levels (Where the Floor Could Hold):

- $7.00 - Strongest support, 5.9% below current price. Total gamma of 8.16 with a net GEX of 2.77 makes this the key level to watch. If NEXT dips toward $7, market maker hedging activity could slow the decline.

- $6.00 - Secondary support floor, 19.4% below current. Net GEX of 2.28 here - meaningful but would represent a significant pullback from current levels.

🟠 Resistance Levels (Where Rallies May Stall):

- $8.00 - Nearest resistance, just 7.5% above current price. Net GEX of 2.06 creates selling pressure as market makers hedge their call exposure here. This is the first real test for any continued bounce.

- $9.00 - Extended resistance at 21% above current. Net GEX of 1.71 - getting into "show me" territory where the stock would need major catalyst confirmation.

What this means: The gamma structure is relatively thin for a small-cap like NEXT, which means price can move more freely than a large-cap with dense gamma. The $7.00 level is the line in the sand on the downside. The short call seller chose $10 wisely - it sits above both resistance levels and would require the stock to blast through $8 and $9 before becoming a real concern.

Implied Move Analysis

The options market is pricing significant volatility into the near term:

- 📅 Monthly OPEX (April 17, 2026 - 24 days): ±$1.15 (±15.3%) → Range: $6.36 - $8.66

Translation for regular folks: The options market is saying NEXT could swing 15.3% in either direction over the next 24 days. That's a big implied move for monthly expiration - driven by the post-Qatar geopolitical premium baked into implied volatility. The upper end of the April range at $8.66 aligns almost perfectly with the gamma resistance at $8.00 - $9.00, which tells us the options market and the gamma structure are telling the same story: $8-$9 is the realistic near-term ceiling.

The short call seller sitting at $10 is well outside even this elevated implied move range. They're positioned in the "this would require a real melt-up" zone.

🎪 Catalysts

🔥 Past Catalysts (Already Happened)

Iran-Qatar LNG Crisis (March 18-19, 2026) - THE Game Changer 🌍

Iranian missile strikes on Qatar's Ras Laffan Industrial City caused extensive damage to the world's largest LNG export facility, knocking out approximately 17% of Qatar's LNG capacity for an estimated 3-5 years. This triggered a 27% surge in NEXT stock as the market repriced U.S. LNG alternatives. With Qatar expected to be impaired through at least 2028-2031, this directly benefits NextDecade's commercial discussions for Trains 6-8 and improves pricing power on existing contracts.

Train 5 FID & Financial Close (October 16, 2025) 💰

NextDecade closed $6.7B in financing for Train 5, including $3.59B term loan, $0.50B private placement notes, and equity from GIP/BlackRock, GIC, and Mubadala. This brought total secured project financing to over $13.4 billion across all five trains - a massive de-risking milestone.

Q4 2025 Business Update (March 2, 2026) 📊

NextDecade reported all five trains tracking ahead of guaranteed completion dates, with five 20-year LNG sale and purchase agreements totaling 7.2 MTPA executed in 2025 (TotalEnergies, Aramco, JERA, EQT, ConocoPhillips). Fixed liquefaction fees of ~$1.2B annually are contracted for Trains 4 and 5 alone.

Analyst Price Targets (Set Before Qatar Crisis):

| Date | Firm | Action | Price Target | Rating |

|---|---|---|---|---|

| March 5, 2026 | TD Cowen | PT lowered | $7 → $6 | Hold |

| February 24, 2026 | Morgan Stanley | PT lowered | $10 → $7 | Equal Weight |

Note: Both of these targets are now stale - set before the Qatar crisis pushed NEXT up 27%. Expect upward revisions.

📅 Upcoming Catalysts (Watch These Dates)

| Date | Event | Why It Matters |

|---|---|---|

| May 2026 (est.) | Q1 2026 Earnings Report | First earnings post-Qatar crisis; watch for updated guidance and new SPA announcements |

| Mid-2026 | Train 1 Commissioning Activities Begin | Critical de-risking milestone - validates Bechtel's execution |

| Mid-2026 | Train 6 Full FERC Application | Would add another ~6 MTPA if approved - significant value catalyst |

| Q2-Q3 2026 | Post-Qatar Commercial Acceleration | Global buyers actively seeking alternative long-term LNG supply |

| H1 2027 | Train 1 First LNG | The single most transformative catalyst for the company - pre-revenue ends here |

| Q4 2027 | Train 1 Guaranteed Substantial Completion | Contractual backstop date |

The short call seller's $10 strike expires January 2028 - that's after Train 1 first LNG but before Trains 2 and 3 complete. The seller is betting the market won't fully price in a multi-train production story to above $10 in the next 22 months.

🎲 Price Targets & Probabilities

Based on the gamma structure, implied move data, and catalyst timeline:

🐻 Bear Case: $6.00 - $6.36

- Probability: ~25%

- Gamma support at $6.00 | Lower end of April implied move range at $6.36

- What gets us here: Qatar repair progresses faster than expected, LNG oversupply thesis reasserts, construction delays at Train 1, or a broad energy sector selloff

- The short call seller loves this scenario - keeps the full $2.00 premium

📊 Base Case: $7.00 - $8.66

- Probability: ~50%

- Gamma support at $7.00 | Gamma resistance at $8.00 | Upper April implied move at $8.66

- What keeps us here: Continued construction progress, post-Qatar commercial discussions ongoing, no major macro shock

- Short call seller still wins here - collects full premium as $10 stays far away

🚀 Bull Case: $9.00 - $12.00

- Probability: ~25%

- Above gamma resistance at $9.00 | Approaching analyst targets that existed pre-crisis ($8-$10) | Prior 52-week high was $12.12

- What gets us here: Multiple new SPAs announced post-Qatar, Train 1 commissioning ahead of schedule, global LNG price spike, analyst upgrades with revised targets well above $10

- Short call seller starts sweating above $9 but doesn't lose money until NEXT closes above $12 ($10 strike + $2.00 premium collected)

💡 Trading Ideas

🛡️ Conservative - "The Income Machine"

Strategy: Mirror the whale trade at smaller scale - sell covered calls on NEXT shares you own

- Setup: Own 1,000 shares of NEXT (

$7,470 cost), sell 10 contracts of the Jan 2028 $10 call ($2.00 per share) - Premium collected: ~$2,000 (27% return on your share cost)

- Breakeven: You keep premium regardless unless forced to sell at $10

- Max profit: $4,530 ($2.00 premium + $2.57 stock appreciation to $10 = $4.57/share × 1,000 shares)

- Why this works: If you're long-term bullish on NEXT's LNG story but think $10+ is unlikely in 22 months, this generates meaningful income while you wait for Train 1 first LNG. You still participate in any rally up to $10.

- Risk: If NEXT rockets above $10, you miss out on gains above $12 (your net effective sell price).

⚖️ Balanced - "The Strangle Play"

Strategy: Buy a bull call spread to participate in upside while IV is elevated post-Qatar

- Setup: Buy the April 2026 $8 call, sell the April 2026 $9 call (one month out)

- Approximate cost: ~$0.25-$0.40 net debit

- Breakeven: ~$8.25-$8.40

- Max profit: ~$0.65-$0.75 per share if NEXT closes above $9 at April OPEX

- Why this works: The April implied move upper range of $8.66 lines up nicely with this spread. You're playing for a continued post-Qatar bounce toward resistance at $8-$9 without paying through the nose for naked calls. Limited risk, defined reward.

- Risk: If NEXT pulls back below $7.00 support, this expires worthless. Max loss is the premium paid.

🚀 Aggressive - "The LNG Squeeze Play"

Strategy: Buy out-of-the-money calls timed to Train 1 commissioning newsflow

- Setup: Buy the January 2027 $10 call options (capturing first LNG catalyst timing)

- Approximate cost: ~$0.60-$0.90 per contract (estimate based on current vol levels)

- Breakeven: ~$10.60-$10.90 at January 2027 expiration

- Max profit: Unlimited above breakeven

- Why this works: Train 1 commissioning activities are expected mid-2026 and first LNG is targeted H1 2027. If the market starts pricing in production reality and post-Qatar commercial momentum through late 2026, you could see a significant re-rating. The same $10 strike the whale just sold is your target.

- Risk: This is the highest-risk play. If NEXT stays range-bound or retreats, these expire worthless. Only use capital you can afford to lose entirely. The seller on today's tape is your counterparty - they collected your premium.

⚠️ Risk Factors

Execution Risks:

- 🏗️ Construction delays: While all five trains are tracking ahead of schedule, any significant setback to Train 1 first LNG (H1 2027) would be materially negative. The entire bull thesis hinges on Bechtel delivering on time

- 💸 Pre-revenue burn: NEXT continues to report quarterly losses of $0.42-$0.63/share with no revenue until first LNG. Ongoing dilution risk from equity commitments for expansion trains

Market Risks:

- 📉 Qatar recovery: If Qatar repairs its Ras Laffan facility faster than the estimated 3-5 years, the supply shock thesis unwinds. The IEA notes ~48 MTPA of new non-Qatar LNG capacity is coming online in 2026-2027, so the market isn't exactly starved for supply

- 🔥 Natural gas price volatility: Higher Henry Hub prices compress liquefaction margins; lower prices benefit feedstock but signal weak demand

Regulatory / Legal Risks:

- 📋 Train 6 permitting: Full FERC application expected mid-2026 starts a multi-year review process - not guaranteed to go smoothly

- ⚖️ Environmental opposition: Sierra Club, Carrizo/Comecrudo Tribe, and City of Port Isabel continue to oppose the project; expansion trains face additional legal risk

Financial Risks:

- 🏦 York Capital concentration: At ~33% ownership, York Capital represents significant overhang. Any forced reduction in their position would pressure the stock

- 📊 Share dilution: ~264.8 million shares outstanding with potential for further equity raises for Train 6-8 expansion

For Short Call Sellers Specifically:

- 🚀 Unlimited upside risk (if naked): If NEXT reaches $14, $16, or $18 on a true LNG supercycle, naked short call losses accelerate rapidly above the $12 breakeven

- 📌 Assignment risk: Any NEXT move above $10 before January 2028 creates mark-to-market losses; a move above $12 means the position is underwater

🎯 The Bottom Line

Real talk: Today's $1.8M short call trade is a premium collection play by someone with a clear view that $10 is the ceiling for NEXT over the next two years. The bid-side execution tells us they wanted this trade done fast - no price discovery, just get it on.

The structure makes sense from a covered call perspective. With NEXT up 38.9% YTD and the Qatar premium potentially baked in, locking in $2.00/share of income on a LEAP that expires well after Train 1 first LNG is a disciplined income strategy. The $10 strike gives plenty of runway - the stock would need to rally another 34% from today's levels before the seller faces a problem.

Three scenarios for what to do:

-

✅ If you own NEXT: Consider the covered call approach the whale is using. The Jan 2028 $10 calls at $2.00 represent 26-27% of your cost basis in income while you wait for the LNG story to mature. Just understand you're capping your gain at $12 (strike + premium).

-

👀 If you're watching from the sidelines: The $7.00 gamma support is your entry trigger on a pullback. A dip toward $7 with the commissioning catalyst mid-2026 approaching would be an interesting risk/reward setup. The implied move range of $6.36-$8.66 through April OPEX defines the near-term playbook.

-

😰 If you're bearish: The short call seller has the right idea about the near-term ceiling, but going bearish on NEXT outright with the Train 1 first LNG approaching in H1 2027 and the Qatar supply shock still fresh is a high-conviction trade against significant catalyst momentum. Tread carefully.

Mark your calendar for mid-2026: Train 1 commissioning activities begin and the full FERC application for Train 6 gets filed. Those two events will tell us whether NEXT's $10+ story is viable before the January 2028 expiration.

⚠️ Disclaimer: This analysis is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Options trading involves substantial risk and is not appropriate for all investors. You could lose your entire investment. Always do your own research and consult a licensed financial advisor before making investment decisions.