🛡️ PGY Massive $908K Put Buy - Smart Money Hedging AI Lending Rally! 💰

📅 December 2, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $908,000 on PGY puts this afternoon at 12:24:33! This substantial hedge bought 9,082 contracts of $20 strike puts expiring January 16th - protecting against downside just 44 days before expiration with PGY trading at $23.91. After an absolutely monster run from $8.20 to $44.99 (448% range!) in the past year, smart money is buying insurance at these elevated levels. Translation: Institutional investors are locking in protection after a massive AI fintech rally!

📊 Company Overview

Pagaya Technologies (PGY) is transforming the lending sector through advanced AI-driven credit technology:

- Market Cap: $1.94 Billion

- Industry: Finance Services (Fintech / AI Lending)

- Current Price: $23.91 (down from 52-week high of $44.99)

- Primary Business: AI-powered lending platform connecting banks with consumers through machine learning and data analytics

- Key Technology: Proprietary API integrates with partner networks to expand credit access and improve decisioning

💰 The Option Flow Breakdown

The Tape (December 2, 2025 @ 12:24:33):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:24:33 | PGY | BUY | PUT $20 | 2026-01-16 | $908K | $20 | 9,700 | 13,000 | 9,082 | $23.91 | $1.00 | PGY 20P 01/16 |

🤓 What This Actually Means

This is a defensive hedge on a substantial position! Here's what went down:

- 💸 Six-figure premium paid: $908K ($1.00 per contract × 9,082 contracts)

- 🛡️ Protection strike: $20 provides 16.4% downside cushion below current price

- ⏰ Strategic timing: 44 days to expiration captures any Q4 volatility, year-end positioning, and potential early 2026 concerns

- 📊 Size matters: 9,082 contracts represents 908,200 shares worth ~$21.7M at current price

- 🏦 Institutional insurance: This is sophisticated portfolio hedging after a massive rally, not necessarily a bearish bet

What's really happening here: This trader likely accumulated a LARGE position in PGY during the rally from the low-teens to mid-$40s. With the stock at $23.91 (down 47% from the recent high of $44.99 but still up significantly from 52-week lows of $8.20), they're paying $1.00 per share for the Jan 16 $20 puts as insurance against further downside. If PGY drops below $20 by January 16th, these puts pay off dollar-for-dollar. Think of it like buying a $908K insurance policy on a multi-million dollar position.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-score: 7.31) - This trade is 7.31 standard deviations above the average! The Volume/OI ratio of 0.746 shows HIGH_ACTIVITY, and with only 1 similar trade in recent history, this is definitively unusual. This happens maybe a few times per year for PGY - nowhere near "once in a lifetime" but certainly notable enough to pay attention.

📈 Technical Setup / Chart Check-Up

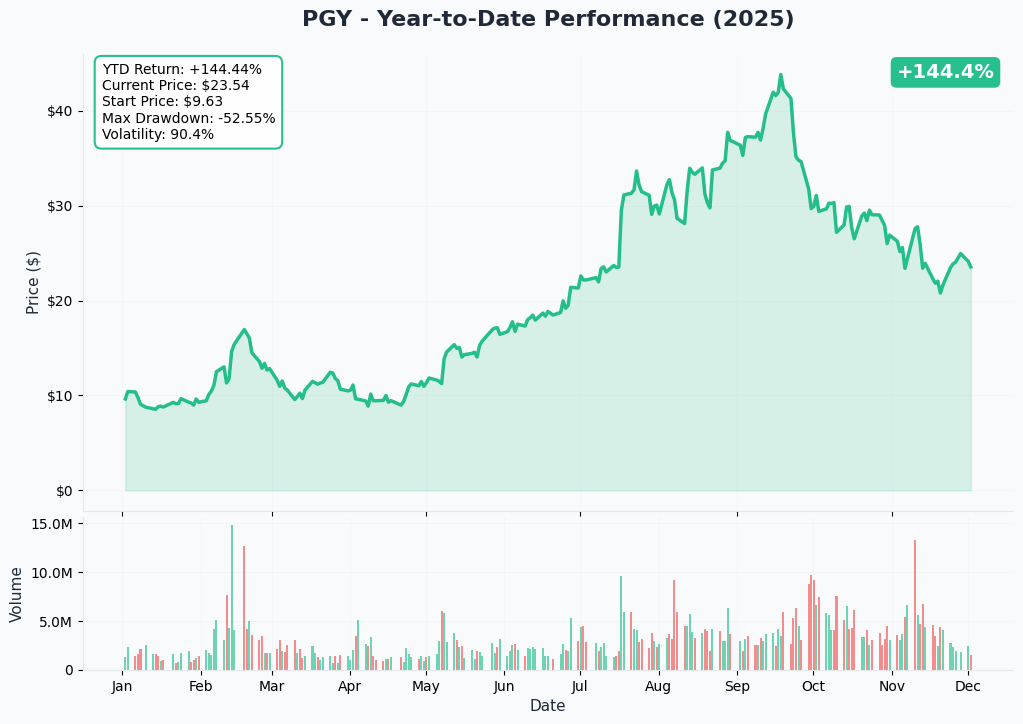

YTD Performance Chart

PGY has been on an absolute rollercoaster - with a 52-week range from $8.20 to $44.99 (448% spread!). The stock exploded from around $10 in early 2025 to hit $44.99 at its peak, fueled by Q3 2024 earnings beats, the record $6B ABS issuance, and the massive OpenAI-like momentum in AI lending.

Key observations:

- 🚀 Monster rally: Vertical move from $8.20 lows to $44.99 highs (448% gain at peak!)

- 📉 Sharp pullback: Currently at $23.91 represents a 47% correction from the high

- 🎢 Extreme volatility: This is NOT your stable dividend stock - massive swings both ways

- 📊 AI fintech momentum: Achieved GAAP profitability in Q1 2025, raised $6B in ABS in 2024, signed $2.5B+ in forward flow agreements

- ⚠️ Consolidation zone: Trading between $22-25 range after the correction - trying to find a floor

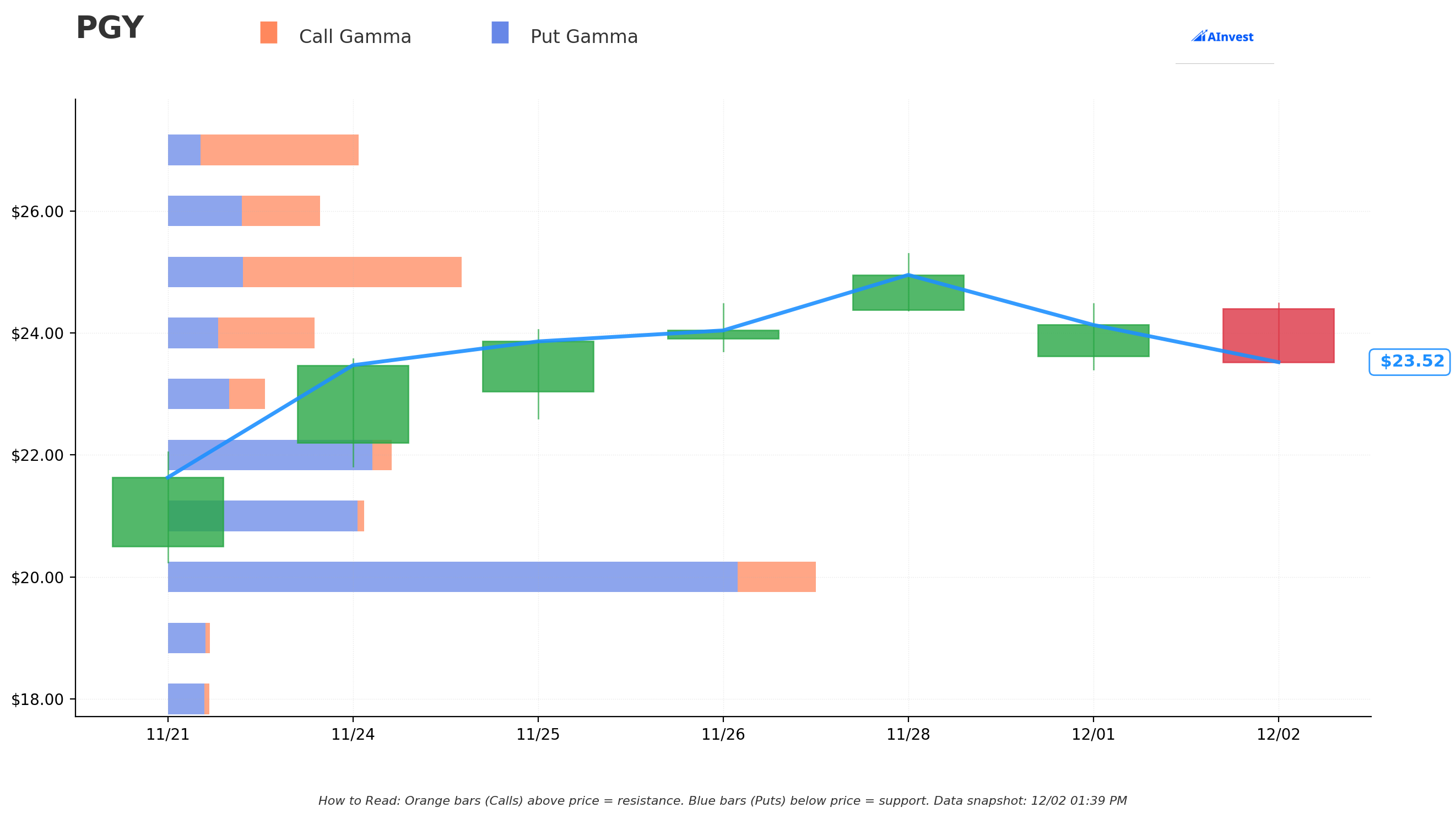

Gamma-Based Support & Resistance Analysis

Current Price: $23.56

The gamma exposure map reveals critical price magnets that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $23 - Immediate support with 0.304B total gamma exposure (closest major floor at 2.4% below current)

- $22 - Strong secondary support at 0.698B gamma (6.6% below) - dealers will defend this level

- $21 - Additional support at 0.611B gamma (10.9% below)

- $20 - MAJOR structural floor with 2.023B gamma (15.1% below) - EXACTLY where this put trade is struck! Not coincidental

- $19 - Extended support zone with 0.132B gamma (19.4% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $24 - Immediate ceiling with 0.475B gamma (1.9% overhead) - current battle zone

- $25 - Strong resistance at 0.920B gamma (6.1% above) - dealers will sell into rallies here

- $26 - Secondary resistance at 0.477B gamma (10.4% above)

- $27 - Major ceiling zone with 0.597B gamma (14.6% above)

- $28 - Extended upside barrier at 0.291B gamma (18.8% above)

What this means for traders: PGY is trading right at the $23-24 pivot zone with immediate support and resistance creating a narrow range. The gamma data shows the MASSIVE $20 level with 2.023B gamma (the single largest level by far) - this is THE critical support that market makers will defend. The $25 level overhead has significant call gamma (0.920B) which creates natural selling pressure.

Notice anything? The put buyer struck EXACTLY at $20 where there's the highest gamma concentration. They're positioning at the major structural support level, expecting that if PGY breaks below $22-23, it could accelerate toward $20. Smart hedging at a technically significant level.

Net GEX Bias: Bullish (6.17B call gamma vs 4.74B put gamma) - Overall positioning remains bullish, but the stock is consolidating rather than rallying, suggesting the rally may need more fuel.

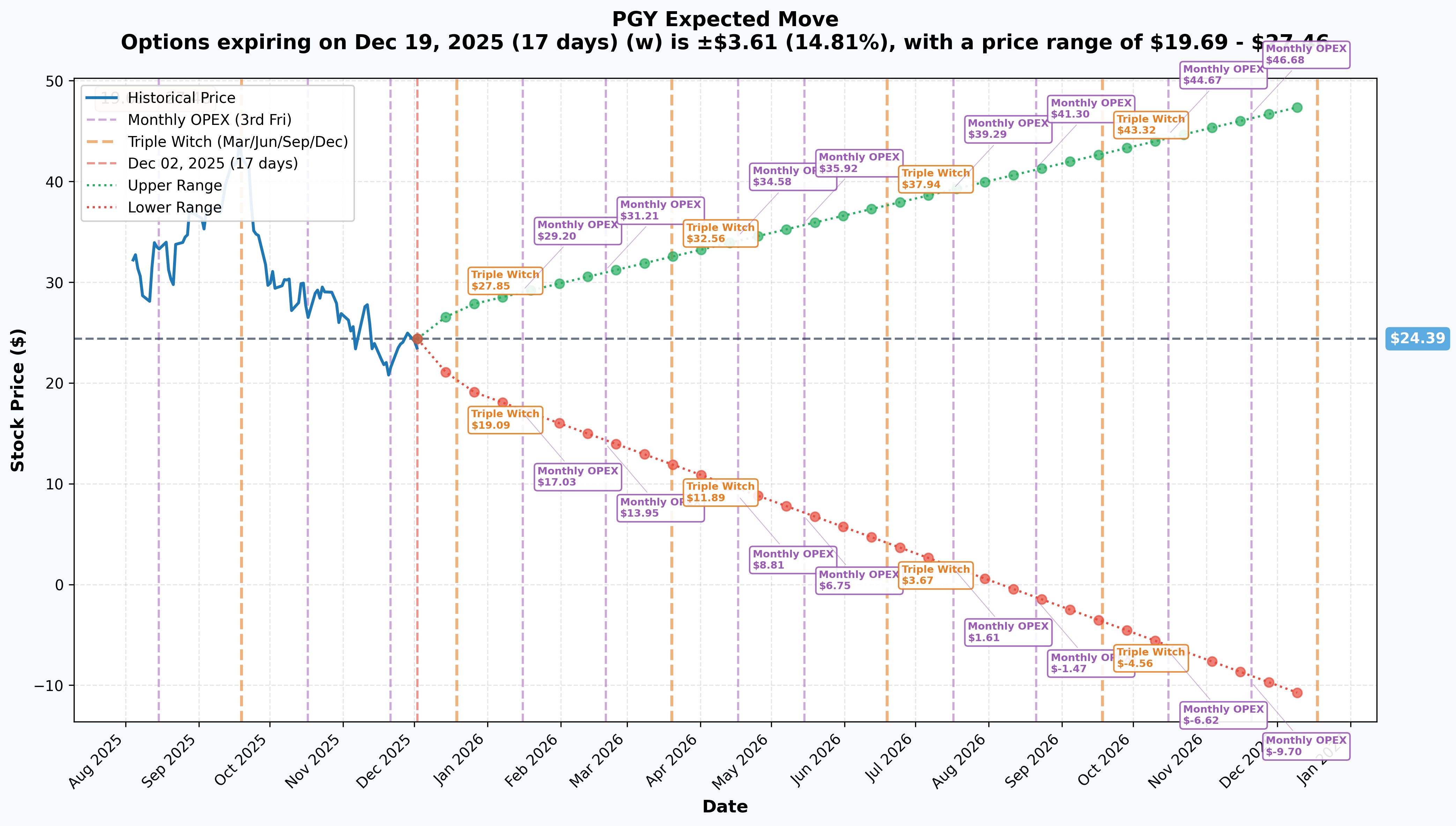

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX (Dec 19 - 17 days): ±$3.61 (±14.81%) → Range: $19.69 - $27.46

- 📅 Quarterly Triple Witch (Dec 19 - 17 days): ±$3.61 (±14.81%) → Range: $19.69 - $27.46

- 📅 January OPEX (Jan 16 - 44 days - THIS TRADE!): ±$4.87 (±19.97%) → Range: $17.03 - $29.20

- 📅 Yearly LEAPs (Dec 18, 2026 - 381 days): ±$27.61 (±113.19%) → Range: -$11.50 - $47.86

Translation for regular folks: Options traders are pricing in a 14.81% move ($3.61) by December 19th - that's HUGE volatility for a 17-day period! The market expects continued wild swings typical of high-growth fintech stocks. The January 16th expiration (when this $908K trade expires) has a lower range of $17.03 - meaning the market thinks there's a real possibility PGY could trade as low as $17 over the next 44 days.

Key insight: The 14.81% implied move through December reflects massive uncertainty around year-end positioning and potential Q4 earnings volatility. The put buyer is clearly concerned about the downside scenario where PGY tests $20 or lower.

🎪 Catalysts

🔥 Already Happened (Past Catalysts That Set The Stage)

Q3 2024 Earnings Beat - November 12, 2024 📊

PGY's Q3 2024 results crushed expectations:

- 📊 Revenue: $257.23M (up 27.7% YoY), beat consensus of $253.21M by 1.59%

- 💰 EPS: $0.44 vs expected $0.25 per share (+76% beat!)

- 💪 FRLPC: $100M (4.3% of network volume)

- 📈 Adjusted EBITDA: $56M with 21.8% margin

- 🚀 Network Volume: $2.4B (up 11% YoY)

- ⚠️ GAAP Loss: Still posted $67M loss vs $22M in Q3 2023, but adjusted metrics showed profitability path

Q4 2024 Earnings Beat - February 13, 2025 📈

- 💰 Revenue: $279M vs consensus $266.68M (+4.6% beat!)

- 📊 YoY Growth: 28% revenue growth

- 🎯 Full Year 2024: $1B revenue (+27% YoY)

- 🚀 Stock Reaction: +27.61% in pre-market following results

- 🏆 Validation: Proved the Q3 beat wasn't a fluke - consistent execution

Q1 2025 GAAP Profitability - May 7, 2025 🎊

- 🎯 GAAP Net Income: $8M - first time profitable as public company!

- 💰 Revenue: $289.99M (beat by 1.63%)

- 📈 Revenue Growth: 18% YoY, annualized run rate ~$1.2B

- 🔥 FRLPC Growth: 26% YoY, annualized run rate >$460M

- ⚡ Adjusted EBITDA: Doubled to ~$320M annualized

- 🏆 Major Milestone: Achieved profitability AHEAD of Q2 guidance

Record $6 Billion ABS Issuance - 2024 💵

Became #1 U.S. personal loan ABS issuer by issuance size:

- 🏦 Total 2024 ABS: $6B across 17 transactions

- 🥇 Market Position: #1 personal loan ABS issuer in U.S.

- 📊 Recent Deals: $1B raised in November across PAID 2024-10 and RPM 2024-3

- 🌟 Credit Quality: 4th AAA-rated personal loan ABS, first AA-rated auto transaction

- 👥 Investor Base: 130+ institutional investment firms, deals substantially oversubscribed

Major Partnership Momentum 🤝

Strategic partnerships validating the platform:

- 🏦 U.S. Bank partnership for AI-powered credit decisioning

- 💳 Mastercard Engage Program for POS lending (June 2024)

- 💰 $2.4B forward flow agreement with Blue Owl Capital

- 💵 $2.5B forward flow agreement with Castlelake

- 📊 Total Forward Flow: Nearly $3.7B in funding capacity secured

🚀 Upcoming Catalysts (Next 6 Months)

Q4 2025 Earnings Report - February 12, 2026 📅

Next earnings report scheduled:

- 📆 Date: February 12, 2026 before market open (71 days away)

- 💰 EPS Forecast: $0.35 for fiscal Q4 2025

- 📊 Note: This is AFTER the January 16th put expiration, so these puts won't directly play the earnings event

- 🎯 Focus: Full year 2025 guidance raise expectations, GAAP profitability continuation, partner onboarding progress

Full Year 2025 Guidance (Already Raised!) 📈

Guidance raised following Q3 2025 results:

- 🎯 Network Volume: $10.5B - $10.75B

- 💰 Total Revenue: $1.3B - $1.325B

- 📊 Adjusted EBITDA: $372M - $382M

- 🏆 GAAP Net Income: $72M - $82M (raised from initial $10M-$45M guidance!)

- 🚀 Translation: Management confident in continued growth and profitability expansion

Product Expansion Momentum 🌱

Auto Lending Acceleration:

- 🚗 Auto volumes increased nearly 50% sequentially in Q1 2025

- 🏭 ~$1.7B in auto ABS issued year-to-date in 2025 (annual record)

- 📈 Fastest growing segment with sequential acceleration

Point-of-Sale (POS) Expansion:

- ⚡ Newest and fastest-growing category

- 🤝 Partners: Klarna, Elavon/U.S. Bank (Avvance), Mastercard Engage program

- 💡 Significant untapped potential with established merchant networks

Personal Loans:

- 📊 17% YoY growth in Q1 2025

- 🥇 Market leader: #1 U.S. personal loan ABS issuer

Partner Onboarding Acceleration 🏦

Record high partner onboarding queues:

- 👥 Current Network: 31 lending partners with ~60M existing customers

- 📈 Penetration: Only 3% of addressable market tapped per President Sanjiv Das

- 🎯 Target: Double partners contributing $100M+ in volume

- 🏭 Efficiency Initiative: Prebuilt products to accelerate partner integration

- 💪 Recent Wins: Onboarded top 5 bank in POS vertical, advanced discussions with several top 20 lenders

Analyst Upgrade Cycle 📊

Strong Buy consensus building:

- 🎯 Rating: "Strong Buy" based on 9 buy ratings, 1 hold, 0 sell

- 💰 Average Price Target: $38.33 (range: $27.00 - $54.00) → 60% upside from current levels

- 📈 Alternative Consensus: $41.62 (range: $27.27 - $56.70)

- 🏆 Recent Upgrades: Canaccord Genuity raised PT from $36 to $39, B. Riley Securities raised to $54, Citizens JMP raised to $35

⚠️ Risk Catalysts (Negative)

Credit Risk & Subprime Exposure 🚨

- 💸 Subprime Holdings: $756M in subprime loans with significant 2024 write-downs

- 📉 2023 Impairment: $229M charge tied to underperforming 2021-2023 vintages

- ⚠️ Ongoing Risk: Macroeconomic weakness could trigger more delinquencies

- 🛡️ Management Response: Tightened underwriting standards, re-marked investments

Valuation & Execution Risk 📊

Despite recent pullback, valuation concerns remain:

- 💔 2024 Losses: -$401.41M (212.5% increase vs 2023)

- 📉 Stock Volatility: 52-week range $8.20-$44.99 shows extreme swings

- ⚖️ Non-GAAP Reliance: Heavy dependence on adjusted metrics for profitability narrative

- 🎯 High Expectations: Street pricing in aggressive growth that requires flawless execution

Competitive & Regulatory Pressures 🔨

Multiple headwinds to monitor:

- 💪 Upstart Competition: Direct competitor in AI lending space with stronger brand

- ⚖️ Regulatory Scrutiny: Heightened regulatory focus on AI in consumer lending

- 🌍 Macro Sensitivity: Consumer lending highly cyclical, vulnerable to recession

- 💰 Debt-to-Equity: >200% leverage creates financial risk

Insider Selling Activity 📉

Recent insider selling raises questions:

- 🚨 3-Month Activity: Insiders sold only (no purchases)

- 💸 Total Sales: 95,081 shares worth $3,475,010

- 👔 CFO Evangelos Perros: Sold 14,356 shares at $37.34 (September 9) - 19.55% of holdings

- 👨💼 President Sanjiv Das: Sold 13,304 shares at $40.62 (September 15) - 12.07% of holdings

- ⚖️ Mitigation: Some sales via pre-scheduled 10b5-1 plans

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through January 16th expiration:

📈 Bull Case (30% probability)

Target: $27-$30

How we get there:

- 💪 Partner onboarding continues to accelerate with multiple top 20 lenders signing in Q4

- 🚗 Auto lending momentum exceeds expectations with 50%+ sequential growth continuing

- 💰 Additional ABS issuances announced at favorable terms, expanding AAA-rated deals

- 📊 2025 guidance trajectory confirmed or raised again on strong Q4 preliminary results

- 🌐 Market recognizes 3% penetration of 60M customer base as massive opportunity

- 📈 Breakout above $25 gamma resistance triggers technical rally toward $27-28

- 🏦 Major new bank partnership announced (top 10 financial institution)

Key metrics needed:

- Network volume trending toward $11B+ (above guidance)

- Gross margins expanding (proving pricing power)

- Partner count accelerating beyond current 31

- Auto/POS revenue mix expanding faster than personal loans

Probability assessment: 30% because it requires sustained execution momentum with the stock having already corrected 47% from highs. Need multiple positive catalysts to align. Gamma resistance at $25-$26 creates headwinds, but breaking through could trigger momentum.

🎯 Base Case (50% probability)

Target: $20-$25 range (CONSOLIDATION)

Most likely scenario:

- ✅ Continued steady execution on 2025 guidance ($1.3B-$1.325B revenue)

- 📱 Partner additions progressing but not spectacular - steady onboarding

- ⚖️ ABS market remains favorable but no major surprises either way

- 🤖 GAAP profitability continues but margins don't expand dramatically

- 🇺🇸 Macro environment stable - no recession but no boom either

- 🔄 Trading within gamma support ($20-$23) and resistance ($24-$26) bands

- 📊 Market waits for Q4 earnings (Feb 12) and full-year 2025 results

- 💤 Volatility remains elevated but range-bound

This is likely what the put buyer expects: Stock consolidates in $20-25 range, puts expire near worthless or with minimal value, but downside protection served its purpose. The $908K is the "insurance premium" for peace of mind during uncertain times.

Why 50% probability: Stock at consolidation phase after massive rally and 47% correction. Fundamentals improving (GAAP profitability, ABS success) but valuation still requires proof. Most institutional players will hold and monitor through year-end.

📉 Bear Case (20% probability)

Target: $17-$20 (TEST THE PUT STRIKE!)

What could go wrong:

- 😰 Credit performance deteriorates with delinquencies rising on 2024-2025 vintages

- 🚨 Partner onboarding slows - one or two expected deals fall through

- ⏰ Auto/POS expansion disappoints vs expectations

- 💸 Broader consumer lending market weakens (recession fears, rate concerns)

- 📊 Competitive pressure from Upstart intensifies with better execution

- 🤖 ABS market tightens, spreads widen, reducing profitability

- 💰 Q4 guidance reduced or 2026 outlook conservative

- 🔨 Break below $22 gamma support triggers cascade to $20

- 📉 Insider selling continues, creating negative sentiment

Critical support levels:

- 🛡️ $23: Immediate support - currently testing

- 🛡️ $22: Strong support (0.698B gamma) - must hold or momentum shifts bearish

- 🛡️ $20: MAJOR floor (2.023B gamma) + this put strike - ultimate line in sand

- 🛡️ $19: Extended support (0.132B gamma) - disaster scenario

Probability assessment: 20% because it requires multiple negative catalysts or a major credit event. PGY's fundamentals have improved significantly (GAAP profitability, $6B ABS success, partner growth), but credit risk and execution challenges remain real. The put buyer clearly thinks this scenario has enough probability to warrant $908K protection.

Put P&L in Bear Case:

- Stock at $18 on Jan 16: Puts worth $2.00, profit = $1.00/share × 9,082 = $9,082 gain (100% ROI)

- Stock at $15 on Jan 16: Puts worth $5.00, profit = $4.00/share × 9,082 = $36,328 gain (400% ROI!)

- Stock at $20 on Jan 16: Puts worth $0 (at-the-money), loss = -$1.00/share × 9,082 = -$9,082 (100% loss)

💡 Trading Ideas

🛡️ Conservative: Wait and Watch Mode

Play: Stay on sidelines until clearer direction emerges post-year-end

Why this works:

- ⏰ Year-end window creates unpredictable volatility - tax loss harvesting, rebalancing

- 💸 Stock already down 47% from highs but no clear bottom yet

- 📊 Next major catalyst is Q4 earnings Feb 12 (after put expiration)

- 🎯 Better risk/reward likely after January 16th when this overhang clears

- 📉 The $908K institutional put buy signals smart money is cautious - why fight it?

- 🤔 Implied move of 14.81% through Dec 19 shows options market expects wild swings

Action plan:

- 👀 Watch for break above $25 (clear bullish signal) or below $22 (bearish breakdown)

- 🎯 Look for entry near $20 gamma support IF stock tests it (offers 20-25% margin of safety vs analyst targets)

- ✅ Need to see Q4 partner onboarding data and credit performance trends

- 📊 Monitor unusual options activity - if institutions add more puts, stay defensive

- ⏰ Revisit after Jan 16 when options overhang clears

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential volatility in consolidation range. Wait for clearer setup with better risk/reward. Maintain capital preservation.

⚖️ Balanced: Small Position with Defined Risk

Play: Take small stock position with protective put or put spread

Structure Option 1: Buy 200 shares at $23.50, buy 2x $22 puts (Jan 16 expiration)

Structure Option 2: Buy $22/$20 put spread (1-2 contracts)

Why this works:

- 🎯 Positioning at current consolidation level with defined downside protection

- 📊 Gamma support nearby at $23 and $22 provides technical floor

- 🤝 Essentially joining smart money with protection, but at smaller scale

- ⏰ 44 days gives time for any year-end surprises to materialize

- 🛡️ Limited downside if credit concerns or macro weakness emerge

Stock + Put Strategy:

- 💰 Buy 200 shares @ $23.50 = $4,700

- 🛡️ Buy 2x Jan 16 $22 puts @ ~$1.50 = $300 protection

- 📈 Max profit: Unlimited above $25 (breakeven ~$24.00 including put cost)

- 📉 Max loss: $400 if stock drops below $22 (puts protect below)

- 🎯 Exit: Take profits at $27+ or if breaks below $22

Put Spread Strategy:

- 💰 Buy $22 puts, Sell $20 puts @ ~$0.75 net debit

- 📈 Max profit: $1.25 if stock below $20 (167% ROI)

- 📉 Max loss: $0.75 if stock above $22 (100% loss)

- 🎯 Breakeven: ~$21.25

- 📊 Risk/Reward: 1:1.67 (favorable for bearish play)

Position sizing: Risk only 2-3% of portfolio (this is speculative, not core holding)

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: Volatility Play with Calendar Spread (ADVANCED)

Play: Sell near-term premium, buy longer-dated protection

Structure: Sell Dec 19 $23 puts, Buy Jan 16 $22 puts

Why this could work:

- 💥 Implied move of 14.81% through Dec 19 creates fat premium to sell

- 🎰 Betting stock stays in $22-25 range near-term but want longer protection

- 📊 Gamma support at $23 provides floor for short puts

- ⚡ Capture theta decay on near-term while maintaining Jan protection

- 📈 If stock consolidates, Dec puts expire worthless, keep Jan puts for Feb earnings

Why this could blow up (SERIOUS RISKS):

- 💸 NAKED SHORT RISK: Selling puts creates unlimited downside if stock crashes

- ⏰ Assignment risk: Could be forced to buy stock at $23 if it drops

- 😱 Gap risk: Year-end illiquidity could cause violent moves through your strikes

- 📊 Margin requirement: Broker may require $2,000+ margin per contract

- ⚠️ Need active management - can't set and forget

Estimated P&L:

- 💰 Sell Dec 19 $23 puts @ ~$1.20, Buy Jan 16 $22 puts @ ~$1.50 = $0.30 net debit per spread

- 📈 Best case: Dec puts expire worthless, Jan puts lose value, net loss ~$20-30 but had protection

- 🚀 Volatility scenario: Stock drops to $21, Jan puts profit $1+, Dec puts assigned but manageable

- 📉 Disaster: Stock gaps to $18, short Dec puts lose $5+, long Jan puts gain $4 = net $1 loss capped

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand calendar spread mechanics and assignment risk

- ✅ Have margin available for potential stock assignment

- ✅ Can actively monitor position daily (especially into Dec 19 expiration)

- ✅ Comfortable managing early assignment if stock drops sharply

- ✅ Have experience with short option positions

Risk level: HIGH (undefined risk on short leg) | Skill level: Advanced only

Probability of profit: ~50% but requires active management

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💸 Credit risk exposure remains significant: $756M in subprime loans with history of write-downs ($229M in 2023). If macroeconomic conditions weaken or unemployment rises, delinquencies could spike on 2024-2025 loan vintages. Management tightened underwriting but newer vintages untested in downturn. Consumer lending is inherently cyclical and sensitive to economic weakness.

-

🎢 Extreme volatility creates whipsaw risk: 52-week range from $8.20 to $44.99 (448% spread!) shows this stock can move VIOLENTLY in either direction. Currently at $23.91 means it's down 47% from highs but still up 191% from lows. This isn't a stable stock - it can gap 10-15% on no news. The 14.81% implied move through December reflects market expectations of continued wild swings. Traders without strong conviction will get shaken out.

-

📊 Valuation still requires flawless execution: Despite pullback from $45 to $24, stock trades at premium to many fintech peers based on 2025 revenue guidance of $1.3B-$1.325B. Market pricing in continued partner growth, margin expansion, and credit quality. Any disappointment in Q4 partner additions, ABS spreads widening, or guidance reduction would trigger another leg down. Current levels offer little margin of safety.

-

🏦 Partner concentration risk: Large percentage of revenue from small number of partners. Loss of a major partner or slowdown in onboarding pace vs management's aggressive targets (doubling $100M+ volume partners) could significantly impact growth trajectory. Currently at 31 lending partners with 60M customers but only 3% penetration - execution on the other 97% is unproven.

-

⚖️ Competitive pressure intensifying: Upstart (UPST) remains formidable competitor with stronger brand recognition despite PGY's superior business model (B2B2C vs balance sheet). Traditional banks developing in-house AI capabilities. Commoditization risk as AI lending becomes table stakes rather than differentiator. Margin compression possible if forced to price aggressively to win share.

-

🚨 Regulatory scrutiny on AI lending: Heightened regulatory focus on AI in consumer lending with potential for increased compliance costs or restrictions on AI-driven decisioning. Consumer Financial Protection Bureau (CFPB) actively examining AI/ML models for bias and fairness. Changes to lending regulations could impact business model operations or economics.

-

💰 High leverage with >200% debt-to-equity: Balance sheet carries significant debt which limits financial flexibility. While $3.7B in forward flow agreements provides funding capacity, any credit market disruption (like 2008, 2020) could severely constrain capital access. Cash position of ~$200M provides limited buffer.

-

🐋 Smart money buying $908K insurance signals caution: This institutional put purchase (Z-score 7.31 = extremely unusual) shows sophisticated players protecting against downside despite improved fundamentals. When funds pay $908K for $20 strike protection with stock at $24, it signals concern about 15-20% downside risk over next 44 days. The 0.746 volume/OI ratio indicates this is opening activity, not closing - fresh defensive positioning.

-

📉 Insider selling activity concerning: Total insider sales of $3.5M over 3 months with zero purchases sends mixed message. While some sales via pre-scheduled 10b5-1 plans, CFO sold 19.55% of holdings and President sold 12.07% near recent highs. Insiders closer to business than we are.

-

🎯 Gamma resistance at $25 creates mechanical headwinds: Call gamma of 0.920B at $25 strike (second largest level) means market makers will systematically sell into rallies to hedge exposure. This creates natural ceiling making breakouts difficult without sustained institutional buying. Would need major catalyst to overcome this technical barrier.

-

⏰ Year-end positioning uncertainty: December traditionally sees tax loss harvesting, window dressing, and volatile flows. With PGY down 47% from highs, could see additional selling pressure from funds crystallizing losses. Conversely, if stock bounces, short covering could create violent upside. Uncertainty elevated.

-

💔 Still GAAP unprofitable for full-year 2024: Despite Q1 2025 GAAP profitability milestone, 2024 full-year showed -$401.41M loss (212.5% increase vs 2023). Heavy reliance on non-GAAP adjusted metrics for profitability narrative. Need to prove sustained GAAP profitability over multiple quarters.

🎯 The Bottom Line

Real talk: Someone just spent $908,000 protecting a substantial PGY position with the stock consolidating after a 47% pullback from all-time highs. This isn't necessarily bearish on PGY's long-term AI fintech story - it's prudent risk management by someone who's likely sitting on significant gains from the rally and doesn't want to give them back.

What this trade tells us:

- 🎯 Sophisticated player expects potential VOLATILITY through January (14.81% implied move confirms this)

- 💰 Concerned enough about $24→$20 scenario to pay $1.00/share for insurance (4.2% of stock price)

- ⚖️ The $20 strike (16.4% below current) sits at MASSIVE gamma support - expects if stock breaks lower, $20 is the line

- ⏰ January 16th expiration captures year-end volatility, potential early 2026 concerns, but expires BEFORE Feb 12 earnings

- 🔥 Z-score of 7.31 (extremely unusual) means this happens only a few times per year - worth paying attention

This is NOT a "sell everything" signal - it's a "manage risk intelligently" signal.

If you own PGY:

- ✅ Consider trimming 20-30% at $23-25 levels if you've made significant gains (protect profits)

- 📊 If holding through year-end, set MENTAL STOP at $22 (strong gamma support) to limit downside

- ⏰ You've already won big if you bought in the teens! Taking some chips off the table is smart

- 🎯 If stock breaks cleanly above $25, could re-enter trimmed shares on momentum to $27-28

- 🛡️ Consider buying 1-2 protective puts per 100 shares if holding large position (copy this structure at smaller size)

If you're watching from sidelines:

- ⏰ Current level ($23-24) is interesting but wait for clearer direction

- 🎯 Pullback to $20-21 would be EXCELLENT entry (matches gamma support + put strike, gives margin of safety vs $38+ analyst targets)

- 📈 Looking for confirmation: Continued partner adds, auto/POS growth acceleration, credit quality stability, ABS market access

- 🚀 Longer-term (6-12 months), the AI lending thesis is compelling with only 3% penetration of 60M customer base, #1 ABS issuer position, and GAAP profitability achieved

- ⚠️ But current consolidation and options activity suggest patience will be rewarded

If you're bearish:

- 🎯 Current level offers reasonable risk/reward for bearish positioning IF you use defined risk

- 📊 Key support at $23 (immediate), $22 (strong 0.698B gamma), $20 (major 2.023B gamma floor)

- ⚠️ Put spreads $22/$20 offer way to express bearish view with limited capital at risk

- 📉 Watch for break below $22 - that's the trigger for potential cascade to $20

- ⏰ Don't short outright - borrow costs high and short squeeze risk real on positive news

Mark your calendar - Key dates:

- 📅 December 19 - Monthly OPEX (14.81% implied move window closes)

- 📅 January 16, 2026 - Monthly OPEX, expiration of this $908K put trade

- 📅 February 12, 2026 - Q4 2025 earnings report before market open

- 📅 2025 ongoing - Partner onboarding announcements, ABS issuances, auto/POS growth updates

Final verdict: PGY's transformation story remains compelling - achieved GAAP profitability, raised $6B in ABS, secured $3.7B in forward flow agreements, and operates a capital-light B2B2C model with 44% ROE. The AI lending market is huge and they're a leader.

BUT, at current levels after a 47% pullback with year-end volatility ahead, the $908K institutional put buy signals that even believers are hedging. The credit risk ($756M subprime exposure), insider selling ($3.5M), and >200% debt-to-equity create real downside scenarios that prudent investors must respect.

Be patient. Let the dust settle. Watch for $20-21 entry if stock tests support, or $26+ breakout if momentum returns. The AI fintech revolution is just beginning, and PGY is well-positioned - but timing matters.

This is chess, not checkers. Manage risk intelligently. 🛡️

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 7.31 (extremely unusual) reflects this specific trade's size relative to recent PGY history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Year-end creates elevated volatility risk with potential for 15%+ moves either direction based on implied volatility. The put buyer may have complex portfolio hedging needs not applicable to retail traders.

About Pagaya Technologies: Pagaya operates as a fintech firm transforming the lending sector through AI-driven credit technology, leveraging machine learning and data analytics to modernize credit delivery with a $1.94 billion market cap in the Finance Services industry.