🚀 QQQ: $48M Bullish Put Sale Signals Tech Conviction Into Year-End!

📅 December 16, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $48 MILLION selling puts on QQQ at the $615 strike - basically betting the NASDAQ-100 stays above $615 through March 2025! This isn't retail money - this is institutional conviction that tech's dip to $610 is a buying opportunity, not the start of something worse. With the Fed's hawkish pivot still fresh and semiconductor stocks wobbly, this whale is stepping in saying "I'll own QQQ at $615, thank you very much."

💰 The Option Flow Breakdown

📊 What Just Happened

The Tape at 10:10 AM ET:

- 🐋 Premium: $48M (20,000 contracts × $24.23)

- 📉 Strike: $615 PUT (0.7% below spot)

- 📅 Expiration: March 20, 2026 (94 days out)

- 💵 Spot Price: $610.61

- 🔄 Volume: 20,000 contracts

- 📊 Open Interest: 6,900 (Volume 2.9x OI!)

- 🎯 Side: MID execution (sophisticated institutional flow)

Unusual Score Analysis:

- Z-Score: 39.02 (EXTREMELY UNUSUAL)

- Volume Signal: OPEN (new position, not a roll)

- Vol/OI Ratio: 2.9x (HIGH ACTIVITY - this is 290% above normal!)

- Strategy: Short Put - cash-secured income strategy

- Confidence: MEDIUM (standalone position)

🤓 What This Actually Means

Translation: A massive player just said "I'll happily own $123 million worth of QQQ at $615" (20,000 contracts × 100 shares × $615). They collected $48M in premium upfront, meaning their effective entry price is actually $590.77 ($615 - $24.23).

Let me break down why this is bullish:

- ✅ They're selling puts (obligated to BUY if QQQ drops below $615)

- ✅ $615 is just 0.7% below current price - very aggressive

- ✅ They need $123M in buying power reserved (likely institutional)

- ✅ Breakeven at $590.77 is 3.2% below current - solid cushion

- ✅ This is 555x the average daily activity for this strike (not a typo!)

Why sell puts instead of buying shares? They generate $48M in income while waiting to get filled. If QQQ stays above $615, they keep the entire premium. If it drops below, they buy at an effective 3.2% discount to today's price. Win-win for patient money.

📈 Chart Check-Up

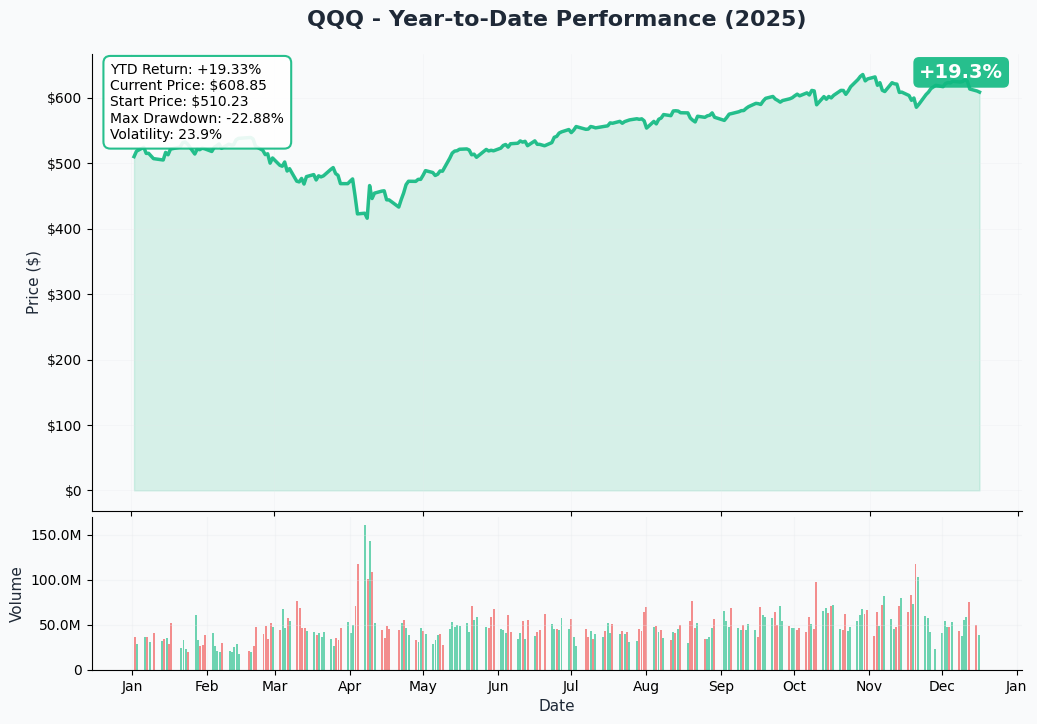

YTD Performance

2025 Has Been a Tech Party: QQQ closed at $610.61, up approximately 20.4% year-to-date according to TS2 Tech's analysis. The ETF hit a peak near $637 in early December before pulling back 4.1% to current levels.

Recent Action:

- Down 0.5% on December 15 with intraday range of $609-618

- Three consecutive days of decline from December highs

- 5-day net outflows: -$2.22 billion (short-term profit-taking)

- BUT: 1-year net flows still +$18.51 billion (long-term conviction intact)

The chart shows a classic "bull flag" pattern - strong uptrend followed by orderly consolidation. The $615 put sale targets support right at this consolidation zone.

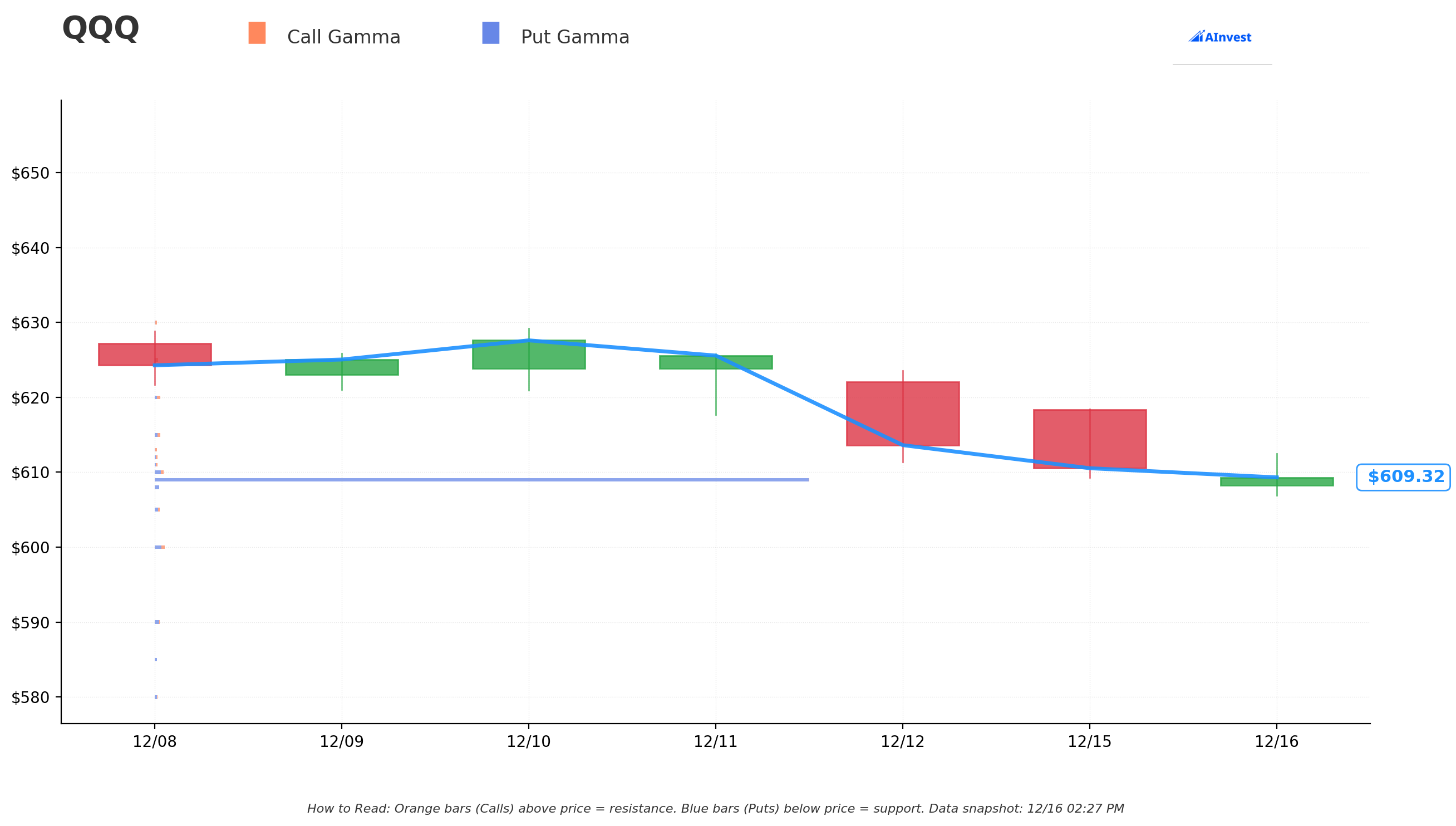

🔵 Gamma-Based Support & Resistance Analysis

Current Price: $609.40 (as of December 16, 2:29 PM ET)

Critical Support Levels (Put Gamma = Blue Bars):

- 🛡️ $608: Immediate support with 113.99M gamma (strongest nearby floor)

- Net GEX: -101.26M (massive put protection)

- Distance: Just 0.23% below - this is TODAY'S battleground

- 🛡️ $605: Secondary support with 107.79M gamma

- Net GEX: -52.83M (still heavily protected)

- Distance: 0.72% down - minor speed bump

- 🛡️ $600: MAJOR psychological support with 235.88M gamma

- Net GEX: -127.28M (HUGE put wall)

- Distance: 1.54% down - this is where institutions drew their line in the sand

- Total GEX: 344.49M (strongest support on the board)

- 🛡️ $590: Deep support with 152.96M gamma

- Distance: 3.18% down - panic buyers would emerge here

Key Resistance Levels (Call Gamma = Orange Bars):

- 🚧 $610: Immediate ceiling with 217.61M gamma (we're right here)

- Net GEX: -100.68M (mixed, but heavy dealer hedging)

- Distance: 0.10% up - minor breakout needed

- 🚧 $615: The target strike with 93.86M gamma

- Net GEX: +10.03M (slight bullish tilt)

- Distance: 0.92% up - this is where the $48M put seller wants us

- 🚧 $620: Strong resistance with 82.78M gamma

- Net GEX: +29.02M (dealers would sell rallies here)

- Distance: 1.74% up - meaningful breakout level

- 🚧 $625: Upper range resistance with 47.75M gamma

- Distance: 2.56% up - bull case target for Q1 2026

Net GEX Bias: Bearish (-599.39M net) suggests dealers are short gamma and will amplify moves. This means:

- If QQQ breaks above $615, squeeze potential to $620-625

- If QQQ breaks below $600, acceleration risk to $590

What the Gamma Profile Tells Us: The $600-608 zone is LOADED with put protection. Institutions have stacked put hedges creating a trampoline effect. The $48M put sale at $615 sits right at a natural resistance level, suggesting the seller expects consolidation between $600-615 before a Q1 breakout.

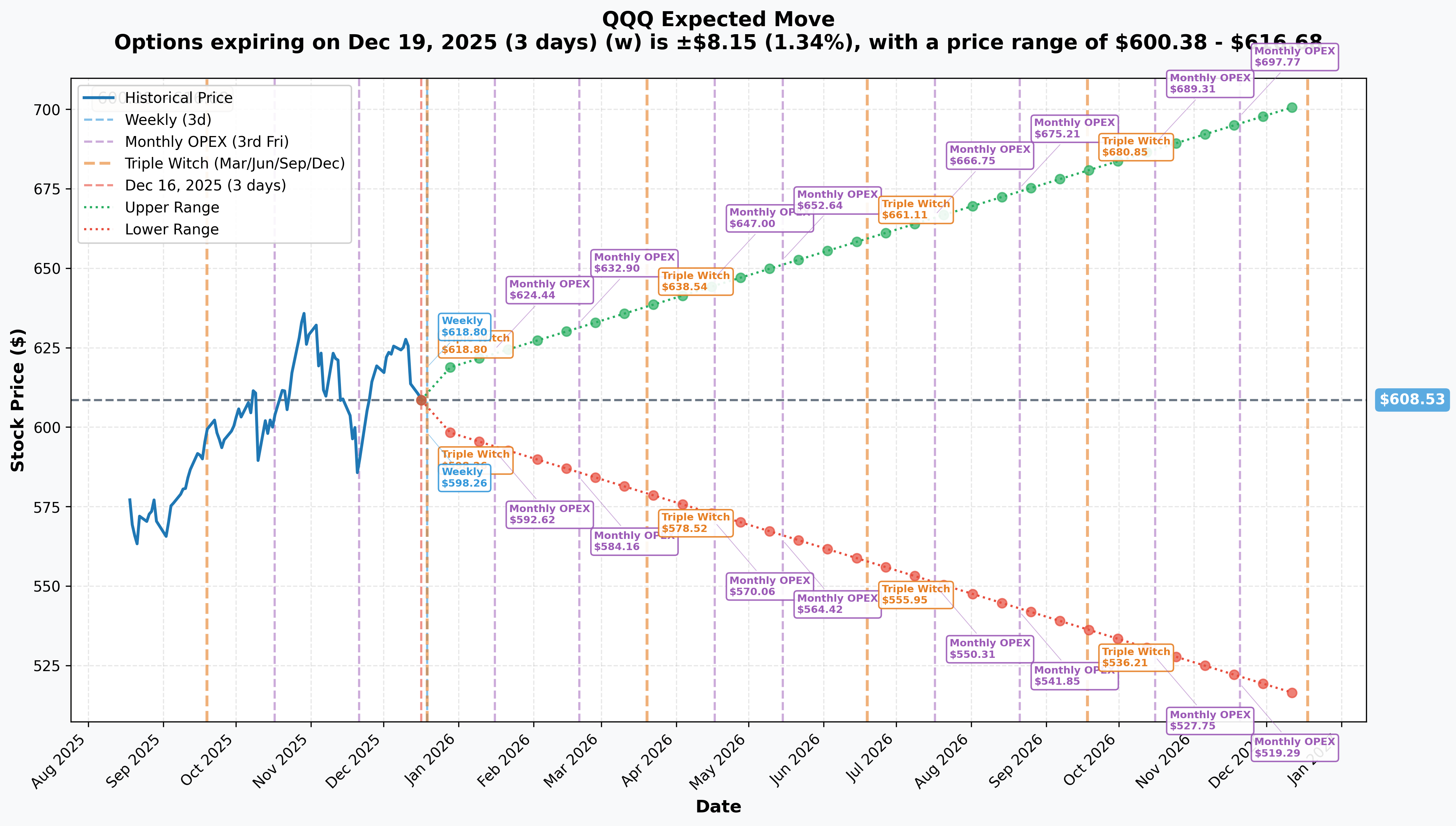

📊 Implied Move Support & Resistance

Options Market Expectations Through March 2026:

December 19 Triple Witching (3 days out):

- 📈 Upper Range: $616.68 (+1.34%)

- 📉 Lower Range: $600.38 (-1.34%)

- 🎯 Implied Move: ±$8.15 (1.34%)

- ⚠️ Key Takeaway: Options pricing a TIGHT $16.30 range through Friday's massive quarterly expiration. This suggests dealers expect choppy, rangebound action into year-end.

January 2026 Monthly OPEX (31 days):

- 📈 Upper Range: $624.44 (+2.61%)

- 📉 Lower Range: $592.62 (-2.61%)

- 🎯 Implied Move: ±$15.91

- ⚠️ Key Takeaway: Market pricing wider swings in January around Q4 earnings

March 20, 2026 (The Put Sale Expiration - 94 days):

- 📈 Upper Range: $638.54 (+4.94%)

- 📉 Lower Range: $578.52 (-4.94%)

- 🎯 Implied Move: ±$30.01

- 🎯 Critical Analysis: The $615 put strike sits WELL WITHIN the expected range. Options market gives it ~68% probability of expiring above $615 (one standard deviation). The seller is taking calculated risk with 68% success odds.

Year-End LEAPS (367 days to December 2026):

- 📈 Upper Range: $702.24 (+15.4%)

- 📉 Lower Range: $514.82 (-15.4%)

- 🎯 Implied Move: ±$93.71

- 🎯 Wall Street Consensus: Average 12-month target of $734.84 per TipRanks (+20.4% upside) aligns with this bullish long-term view

Strategic Implications: The implied move framework suggests:

- Choppy action through year-end (Santa rally uncertainty)

- Volatility spike in January around tech earnings

- Resolution by March toward either $580 (bear case) or $640 (bull case)

- Long-term 2026 trajectory toward $700+ if AI spending thesis holds

The $615 put seller is effectively saying: "I'm comfortable owning QQQ anywhere in the expected range, but I think we stay above $600 support with high probability."

🎪 Catalysts

📅 Upcoming Catalysts (What's Next)

This Week:

- 🗓️ December 19, 2025: Quarterly Triple Witching Expiration - Massive option expiry creating volatility

- 🗓️ December 19, 2025: NASDAQ-100 Reconstitution Announcement - Forced rebalancing flows

- 🗓️ December 24-January 5: Santa Claus Rally Window - Last 5 trading days of 2025 + first 2 of 2026 (S&P 500 averages +1.3%, but QQQ historically underperforms SPY in December)

Next 30 Days:

- 🗓️ January 27-28, 2026: First FOMC Meeting of 2026 - Rate path guidance critical for growth stocks

- 🗓️ Late January 2026: Q4 2025 Magnificent Seven Earnings Begin

- Expected: +13% tech sector earnings growth on +15.8% revenue growth

- Apple: Q4 revenue at record $102.5B, CEO Tim Cook projects "best quarter ever" in December

- Microsoft: Q1 FY2026 showed $77.7B revenue (+18% YoY), Azure +40%

- NVIDIA: Wall Street consensus implies 39% upside with 60 of 64 analysts rating buy

Next 60-90 Days (Through March Expiration):

- 🗓️ February 2026: Full Q4 2025 earnings cycle completes

- 🗓️ March 2026: Fed potentially cuts rates if data softens (Bank of America expects cuts in June-July, but March possible)

- 🗓️ March 20, 2026: $48M Put Sale Expiration - Decision day!

2026 AI Capital Expenditure Mega-Catalyst:

- 💰 Hyperscalers (Amazon, Microsoft, Alphabet, Meta, Oracle) projected to spend $602 billion with 75% dedicated to AI infrastructure

- Microsoft FY2026 CapEx expected to accelerate to $94B+ with some estimates at $121B

- Meta's 2026 CapEx projected at $100 billion (double 2024 levels)

- Bull Case: Validates secular AI growth thesis supporting premium valuations

- Bear Case: CapEx at 22% of revenue vs 11-16% historical average raises sustainability questions per Oracle's December warning

📰 Past Catalysts (What Already Happened)

Recent Headwinds:

- ❗ December 10, 2025: Fed delivered hawkish rate cut - Only ONE projected cut in 2026 (vs market expecting 2-3), signaling higher-for-longer rates that pressure growth stock valuations

- ❗ December 11-12, 2025: Oracle AI CapEx warning sparked semiconductor selloff - Philadelphia Semiconductor Index fell 5.1% on concerns about AI spending ROI

- ❗ December 2025: Broadcom slides on margin outlook concerns - Second-largest QQQ holding (6.62%) under pressure

- ❗ November 2025: Tesla U.S. sales fell 23% YoY to 39,800 vehicles (lowest since January 2022)

Recent Tailwinds:

- ✅ Q3 2025: Tech sector earnings +22.6% YoY on +12.6% revenue growth - 10th consecutive quarter of double-digit earnings growth

- ✅ October 2025: $6.93 billion in QQQ inflows extending monthly positive streak to 7 months

- ✅ November 2025: One-year U.S.-China tariff truce including semiconductor and rare earth breakthroughs - Removes immediate trade war threat

- ✅ December 10, 2025: Fed Chair Powell's comments on AI productivity running at 2% annually validate tech spending thesis

🎲 Price Targets & Probabilities

Bull Case: Tech Breaks Out on Earnings ($625-630 by March) - 35% Probability

The Setup:

- Q4/Q1 earnings deliver 15%+ upside surprises on AI monetization progress

- Fed rhetoric softens in January, market prices 2-3 cuts back in for 2026

- Hyperscaler CapEx guidance for 2026 comes in at $400B+ validating infrastructure build

- Santa Claus rally momentum extends into January effect

- Semiconductor concerns fade as demand remains robust

Price Path:

- Break above $615 resistance triggers short covering to $620

- Gamma squeeze through $620 resistance accelerates move to $625

- Wall Street revisions lift targets toward consensus $734 by mid-2026

Supporting Factors:

- Magnificent Seven expected +16.6% Q4 earnings growth on +16.2% revenues

- NVIDIA's 39% consensus upside with 60 of 64 analysts rating buy or better

- Amazon trading at lowest historical P/E below 33x positioned as 2026 outperformer

- March 2026 implied move upper range at $638.54 supports this target

Options Impact: $48M put seller collects full premium. $615 puts expire worthless. Effective return: 3.95% in 94 days (15.3% annualized).

Base Case: Choppy Consolidation Between $600-615 (March) - 50% Probability

The Setup:

- Tech earnings meet expectations but guidance remains cautious

- Fed stays on track for one 2026 cut, no hawkish surprises but no dovish pivot

- AI CapEx spending continues but without significant monetization acceleration

- Markets digest elevated valuations (34x P/E vs 24x historical median)

- Seasonal patterns play out with weak December, modest January recovery

Price Path:

- QQQ oscillates between $600 gamma support and $615 resistance

- Triple witching this Friday pins price near $608-610

- January earnings volatility keeps trading range intact

- March expiration finds QQQ hovering $605-612

Supporting Factors:

- Implied move framework pricing $578-638 range (QQQ likely stays mid-range)

- Put/call ratio at elevated 1.52 suggests defensive positioning limiting upside

- 5-day outflows of $2.22B indicate near-term distribution phase

- Technical resistance at $621.74 and support at $590.07 define range

Options Impact: $48M put seller keeps partial premium if QQQ expires between $590.77-615. Breakeven at $590.77 means 3.2% cushion to spot price. Risk management outcome.

Bear Case: AI Spending Concerns Trigger Correction ($580-590) - 15% Probability

The Setup:

- Q4 earnings miss with margins compressed by elevated CapEx spending

- Oracle's warning proves prescient as hyperscalers signal CapEx moderation

- Fed maintains hawkish stance with no 2026 cuts, pressuring long-duration growth

- China tensions reignite or U.S.-China tariff truce breaks down

- Regulatory actions escalate (Google antitrust remedies, Meta/Amazon FTC actions)

Price Path:

- Break below $600 gamma support triggers dealer de-hedging cascade

- Acceleration to $590 deep support zone as negative gamma amplifies selling

- Implied move lower bound at $578 becomes realistic target

- VIX spikes to 25-30 on tech selloff contagion

Supporting Factors:

- Net GEX of -599.39M means dealers are short gamma, amplifying downside moves

- Elevated 34x P/E leaves room for 15-20% multiple compression on growth concerns

- Historical precedent: QQQ's $402 2024 low vs $637 recent high shows 37% peak-to-trough range possible

- Contrarian research suggests 20-30% CapEx pullback possible in 2026 if monetization disappoints

Options Impact: $48M put seller gets assigned at $615, buying $123M of QQQ. Effective cost basis $590.77 means unrealized loss if QQQ trades below that level. However, long-term investor likely views this as accumulation opportunity.

💡 Trading Ideas

🛡️ Conservative: The "Sleep Well" Put Credit Spread

Strategy: Sell the March $605 put / Buy the March $595 put spread

- Max Credit: ~$3.50 per spread ($350 per contract)

- Max Risk: $6.50 ($650 per contract)

- Breakeven: $601.50

- Required Margin: $1,000 per spread (10-wide spread)

- Return on Risk: 54% if QQQ stays above $605 (7.1% per month)

Why This Works:

- You're selling puts at the MAJOR $605 gamma support level (107.79M gamma)

- The $600 strike below has 235.88M gamma - massive institutional protection

- Breakeven at $601.50 is 1.5% below current price with 3 months of cushion

- Even in bear case, $595 long put caps max loss at $650

- Implied move suggests 68% probability of success (stays above $605)

Risk Management:

- If QQQ breaks below $605, roll down and out to April for additional credit

- Scale position size to 2-5% of portfolio max

- This is the institutional version of the $48M whale's trade, just defined-risk

For Whom: Traders with $10K-50K accounts who want bullish exposure with capped risk. Sleep-at-night strategy.

⚖️ Balanced: The "Gamma Scalper" Iron Condor

Strategy: Sell March $625 call + March $595 put / Buy March $630 call + March $590 put

- Max Credit: ~$2.00 per spread ($200 per contract)

- Max Risk: $3.00 ($300 per contract)

- Profit Range: $595-625 (4.9% range, 2.5% above and below spot)

- Breakevens: $597 and $623

- Return on Risk: 67% if QQQ stays in range

Why This Works:

- Profits from choppy, rangebound action (base case scenario)

- Short strikes align with gamma resistance ($625) and support ($595)

- Implied move through December and January keep things bouncy

- Volatility contraction post-earnings benefits you (short vega position)

- 50% probability of max profit based on implied moves

Adjustments:

- If QQQ breaks above $620, roll call spread up for credit

- If QQQ breaks below $600, roll put spread down for credit

- Take profits at 50% of max credit ($1.00) to improve win rate

- Close early if volatility collapses post-January earnings

For Whom: Active traders comfortable managing positions. Works best in expected choppy, low-vol environment.

🚀 Aggressive: The "Whale Copycat" Cash-Secured Put

Strategy: Sell March $615 naked put (the exact trade from today's tape)

- Credit Received: $24.23 per share ($2,423 per contract)

- Buying Power Required: $61,500 per contract (cash-secured)

- Effective Entry: $590.77 if assigned

- Breakeven: $590.77 (3.2% cushion to current price)

- Max Return: 3.95% in 94 days = 15.3% annualized

Why This Is The Whale Trade:

- You're literally copying the $48M institutional flow

- Get paid $2,423 to potentially buy QQQ 3.2% below current price

- If QQQ stays above $615, keep entire premium (15.3% annualized return)

- If QQQ drops, you own it at a discount with 3-month holding period cushion

- Gamma support at $600 and $608 creates floor below your strike

The Math:

- One contract = obligation to buy 100 shares at $615

- You collect $2,423 upfront

- Net cost if assigned: $59,077 per 100 shares (vs $61,061 buying today)

- You're getting paid 3.2% discount + 3 months of time value

Advanced Move: If you get assigned at $615, immediately sell April covered calls at $625 for another $3-4 of premium. This creates a "wheel strategy" generating income while waiting for price appreciation.

Risk Warning:

- If QQQ crashes to $580, you own it at $615 with unrealized loss

- This is naked put selling - requires significant capital ($61,500 per contract)

- Not suitable for small accounts or risk-averse traders

- Bear case scenario could see 5-10% drawdown before recovery

For Whom: High-conviction bulls with $100K+ portfolios who WANT to own QQQ at a discount. This is patient institutional money strategy. Not for traders trying to get rich quick.

Pro Tip: Many brokers offer portfolio margin which reduces buying power requirement to ~$12,000 per contract vs $61,500 in cash. This significantly improves capital efficiency but increases risk of margin call.

⚠️ Risk Factors

What Could Go Wrong (Honestly)

AI Monetization Failure (30-40% probability):

- Hyperscalers spending $450B+ on AI infrastructure in 2026 with uncertain revenue timeline

- Oracle's December warning about CapEx-to-revenue ratios already triggered 5% semiconductor selloff

- If AI applications fail to generate expected returns, CapEx cuts could hammer NVIDIA, Broadcom, cloud providers

- QQQ's 53.6% tech weight makes it ground zero for AI disappointment

Valuation Compression (High probability, manageable magnitude):

- Trading at 34.13x P/E vs 24.31 historical median - 40% premium to normal

- Fed's one-cut 2026 projection removes growth stock tailwind

- Each 25bp higher rate reduces growth stock NPV by 2-3%

- Multiple compression of 15-20% could happen even with earnings growth

Magnificent Seven Concentration Risk:

- Top 7 holdings account for 46% of QQQ weight

- NVIDIA alone at 9.2% means 10% NVDA move = 0.92% QQQ impact

- Tesla's 23% sales drop and bearish analyst consensus shows cracks emerging

- Single earnings miss from NVDA, AAPL, or MSFT could tank entire ETF

Regulatory Crackdown:

- Google facing European antitrust investigation on AI

- DOJ Google search monopoly case remedies expected in 2026

- Potential fines of €10-20 billion (1-2% of Google market cap)

- Meta, Amazon, Apple all under FTC scrutiny globally

Tariff Risk Returns:

- One-year U.S.-China tariff truce expires late 2026

- Trump's 100% semiconductor tariff threat remains policy option

- 25% tariff on semiconductors would cost importers $6.35B, forcing price increases

- China excluding NVIDIA from government procurement lists

Seasonal Headwinds:

- QQQ historically underperforms SPY during December

- 2024-2025 precedent: First-ever reverse Santa rally with selling every day between Christmas-New Year

- Put/call ratio at elevated 1.52 shows defensive positioning into year-end

- 5-day outflows of $2.22B suggest institutions taking chips off table

Negative Gamma Amplification:

- Net GEX of -599.39M means dealers are short gamma

- In selloffs, dealers must sell into weakness (accelerates moves)

- Break below $600 could trigger cascade to $590 or lower quickly

- Implied move lower bound at $578 represents 5% downside risk

Margin Pressure Reality Check:

- CapEx as % of revenue at 22% in 2025 vs 11-16% historical average

- Broadcom's margin outlook concerns already triggered December weakness

- Rising R&D and infrastructure costs could compress net margins 100-200bp

Real talk: This is a calculated risk play banking on AI infrastructure spending sustaining through 2026. The $48M whale is sophisticated enough to know the risks and has deep enough pockets to weather volatility. Retail traders need appropriate position sizing and risk management.

🎯 The Bottom Line

Here's The Deal:

Someone with $123 MILLION in buying power just stepped into the post-Fed, post-Oracle selloff and said "I'm buying this dip - literally." This isn't gambling - it's institutional conviction that QQQ's pullback from $637 to $610 created an entry opportunity, not the start of a bear market.

The Trade Decoded: The $48M put sale at $615 with a $590.77 breakeven tells you everything about professional risk management. They're not betting on moonshots - they're positioning for base case (collecting 15.3% annualized premium) while being willing to own QQQ 3.2% cheaper if things get wobbly. This is patient capital deployment, not YOLO.

What Smart Money Sees:

- ✅ $450B in 2026 AI CapEx coming from hyperscalers validates tech infrastructure thesis

- ✅ Q4 earnings expected to show +13-17% growth with Magnificent Seven beating by 16%+

- ✅ Gamma profile showing massive institutional put protection at $600-608 creates safety net

- ✅ Valuation at 34x P/E is elevated but not bubble territory (historical high was 38.56x)

- ✅ Long-term Wall Street target of $734 (+20%) suggests limited downside, asymmetric upside

What Keeps Them Hedging:

- ⚠️ Oracle's CapEx warning shows cracks in AI monetization narrative

- ⚠️ Fed's one-cut 2026 guidance removes growth stock tailwind

- ⚠️ Near-term seasonal headwinds and defensive positioning into year-end

- ⚠️ Elevated valuations vulnerable to multiple compression on any growth disappointment

Your Action Plan:

If You Own QQQ:

- Hold through volatility - $600 support well-protected by gamma

- Consider selling March $625 calls against position for income (covered call strategy)

- Use December weakness to add if conviction high and you have dry powder

- Mark calendar: January 27-28 FOMC and late January earnings are decision points

If You're Watching:

- Wait for setup: break above $615 with volume = bullish momentum confirmation

- OR: Break below $605 with reversal = contrarian entry near $600 support

- December 19 triple witching likely brings volatility - don't chase, wait for setup

- Santa Claus rally window (Dec 24-Jan 5) could provide entry if markets cooperate

If You're Bearish:

- Respect this institutional flow - $48M doesn't get deployed carelessly

- If fading, target resistance at $620-625 for short entries with tight stops

- Bear case requires catalyst (earnings miss, Fed hawkish surprise, CapEx cuts)

- March put buying at $600-595 is cheap insurance given elevated valuations

Position Sizing Reality Check:

- Conservative: 2-5% of portfolio in defined-risk spreads (sleep at night money)

- Balanced: 5-10% in iron condors or covered calls (active management required)

- Aggressive: 10-15% maximum in cash-secured puts (must be willing to own at strike)

- Never risk more than you can afford to lose - options can and do expire worthless

The Final Word: This $48M put sale is bullish conviction, not reckless speculation. The trade structure (near-money strike, quarterly expiration, breakeven 3.2% below spot) screams professional risk management. For retail traders, the lesson isn't to blindly copy the trade - it's to understand the thesis: AI infrastructure spending sustains, tech earnings deliver, and QQQ's $600-608 support zone holds.

March 20 expiration gives this thesis 94 days to play out through Q4 earnings, Fed meetings, and AI CapEx guidance. The whale is betting the dip gets bought. Time will tell if they're right, but $48M says they're damn confident.

📊 Want to track this trade?

⚠️ Risk Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. The strategies discussed are for educational purposes only and do not constitute financial advice. Past performance does not guarantee future results. QQQ is leveraged to technology sector risk, and the Magnificent Seven concentration creates significant single-stock exposure. The $48M institutional trade discussed may have different risk tolerance, time horizon, and capital requirements than retail investors. Always consult with a qualified financial advisor before making investment decisions and never risk more than you can afford to lose. The author may hold positions in securities discussed.

Analysis by Ainvest Options Lab | Data sources: ThetaData, Polygon.io, Market Data Feeds "This analysis is generated with Claude Code from Anthropic for educational purposes"