🏠 RKT Massive $6.3M Bullish Bet - Institutions Loading Up Into Fed Rate Decision! 🚀

📅 December 1, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Big money just dropped $6.3 MILLION on RKT calls this morning in two massive trades! Someone bought 20,000 contracts each of the March 2026 $25 and $21 strike calls at 09:37:15 - positioning for a major move higher into the December Fed rate decision and February earnings. With RKT up +87.5% YTD at $19.85 following transformative acquisitions of Mr. Cooper ($14.2B) and Redfin ($1.75B), smart money is betting the mortgage refinance wave is just getting started. Translation: Institutions are loading up ahead of rate cuts that could unlock massive refinance volume!

📊 Company Overview

Rocket Companies (RKT) is America's largest mortgage lender turned financial services powerhouse following historic M&A activity:

- Market Cap: $56.3 Billion (became $40B+ company in 2025)

- Industry: Mortgage Bankers & Loan Correspondents

- Current Price: $19.85 (near YTD high of $20.08)

- Primary Business: Direct-to-consumer mortgage origination via Rocket Mortgage app/website, plus partner network for brokers. Following the October 1, 2025 Mr. Cooper acquisition, RKT now services $2.1T across 10M homeowners (1 in 6 U.S. mortgages) - the largest servicing portfolio in America.

- Recent Transformation: Completed two landmark deals in 2025 - Redfin acquisition for $1.75B closed July 1, Mr. Cooper acquisition for $14.2B closed October 1 - creating unprecedented end-to-end homeownership platform combining origination, servicing, and real estate brokerage.

Founded: 1985 (as Rock Financial) | Employees: 14,700 | Headquarters: Detroit, Michigan

💰 The Option Flow Breakdown

The Tape (December 1, 2025 @ 09:37:15):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Z-Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:37:15 | RKT | ASK | BUY | CALL $25 | 2026-03-20 | $2.1M | $25 | 20K | - | 20,000 | $19.85 | $1.05 | 19.13 | EXTREMELY UNUSUAL |

| 09:37:15 | RKT | ASK | BUY | CALL $21 | 2026-03-20 | $4.2M | $21 | 20K | - | 20,000 | $19.85 | $2.10 | 66.42 | EXTREMELY UNUSUAL |

🤓 What This Actually Means

This is a massive bullish bet on RKT rallying 25-30% over the next 109 days! Here's what went down:

- 💸 Huge premium paid: $6.3M total ($2.1M + $4.2M) split across two strikes

- 🎯 Target zone: $21 strike needs 5.8% rally (in-the-money if stock >$23.10 at expiry), $25 strike needs 26% rally (aggressive upside bet)

- ⏰ Strategic timing: 109 days to March 20, 2026 expiration captures three MASSIVE catalysts:

- December 9-10 Fed rate decision (85% probability of 25 bps cut)

- February 19, 2026 Q4 earnings (first full quarter with Mr. Cooper + Redfin consolidated)

- Potential for multiple additional Fed rate cuts through Q1 2026

- 📊 Size matters: 40,000 total contracts represents 4 million shares worth ~$79M

- 🏦 Sophisticated structure: Two-strike approach suggests institutional player - $21 strike is the "base case" (more premium, closer to money), $25 strike is the "moon shot" (cheaper lottery ticket if refinance wave explodes)

- 📊 Strategy Classification: UNCLASSIFIED - These trades don't match predefined spread patterns (calendar, vertical, butterfly, etc.), indicating pure directional long call positioning rather than complex multi-leg hedged structure

What's really happening here: This trader is betting that declining mortgage rates from Fed cuts will trigger a refinance boom that sends RKT significantly higher. With rates currently at 6.23% and the Fed expected to cut in December, each 50 bps decline historically increases refinance volume 15-25%. RKT's Q4 guidance of $2.1-2.3B revenue marks the first full quarter with both acquisitions - potential for major upside surprise if mortgage market momentum accelerates faster than expected.

Breakeven Analysis:

- 📈 $21 call breakeven: $23.10 (16.4% rally needed from $19.85)

- 📈 $25 call breakeven: $26.05 (31.2% rally needed)

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-scores of 19.13 and 66.42) - The $21 strike trade is 19x standard deviations above normal, happening maybe a few times per year. The $25 strike at 66x standard deviations is UNPRECEDENTED - this is a once-in-a-blue-moon sized bet. Combined, these trades represent approximately 13x the typical daily call volume for RKT March expiration.

📈 Technical Setup / Chart Check-Up

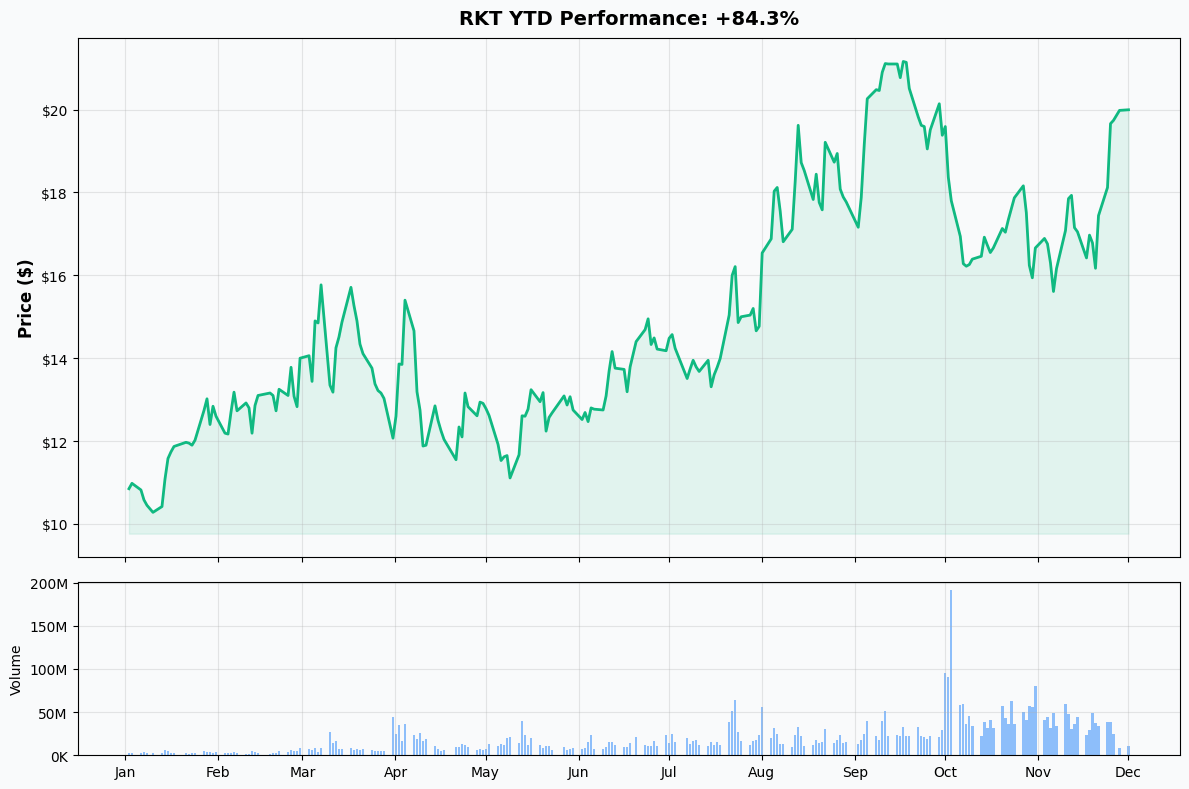

YTD Performance Chart

RKT has been absolutely on fire - up +87.51% YTD with current price of $19.85 (started 2025 at $10.58). The chart tells a dramatic M&A transformation story - after trading sideways in the $11-14 range through Q1, RKT launched a sustained rally beginning in March following the Redfin acquisition announcement on March 10.

Key observations:

- 🚀 Breakout move: Explosive rally from $13 in September to $20+ in November on rate cut optimism and Mr. Cooper deal close

- 📈 Multiple expansion: Stock re-rated from $10-11 range to $18-20 as market recognizes transformative nature of acquisitions

- 🎢 Consolidation phases: Healthy pullbacks at $15 (May-June) and $17 (September) before continuing higher

- 📊 Volume surge: Massive institutional accumulation in October-November as Fed rate cut probability increased to 85%

- ⚠️ Near resistance: Currently testing weekly highs of $20.08 - breakout above $21 would signal next leg higher to $25+

The technical picture shows strong upward momentum supported by fundamental transformation. The 87.5% YTD gain reflects market recognition that RKT is now the #1 mortgage servicer controlling $2.1T with unprecedented ability to capture both origination and servicing revenue as rates decline.

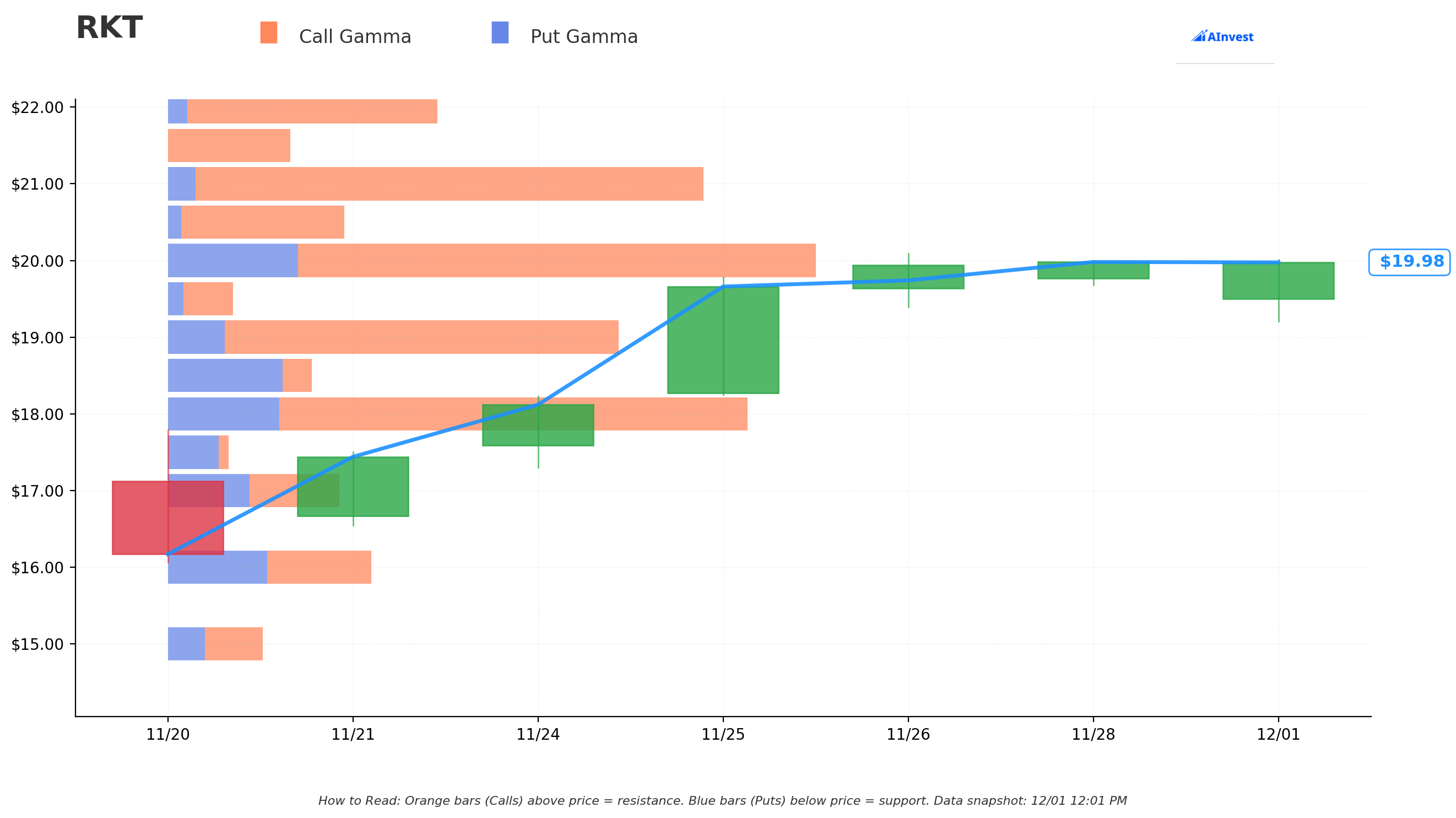

Gamma-Based Support & Resistance Analysis

Current Price: $19.85

⚠️ Limited Gamma Data: RKT currently shows minimal gamma exposure levels across strikes, indicating relatively light options positioning compared to mega-cap stocks. This actually makes the $6.3M call purchases even MORE significant - these trades are likely CREATING new gamma levels rather than following existing positioning.

What the lack of major gamma walls means:

- 🎯 Less resistance overhead: Without massive call gamma clusters above current price, stock can move more freely on momentum

- 📊 Price discovery mode: RKT trading in relatively uncharted technical territory following transformative acquisitions

- 🚀 Easier breakouts: Low gamma exposure means market makers aren't forced to hedge by selling into rallies

- ⚠️ Higher volatility potential: Thin gamma can lead to larger moves in both directions on catalysts

Key technical levels (non-gamma based):

- 🔵 $19.00 support: Recent consolidation floor from late November

- 🔵 $18.00 support: Major accumulation zone from October rally

- 🔵 $17.00 support: August-September base

- 🟠 $21.00 resistance: Psychological level and call strike from today's trade

- 🟠 $25.00 resistance: Major target zone and second call strike

The absence of heavy gamma positioning actually supports the bullish thesis - RKT can rally more aggressively without mechanical selling pressure from market maker hedging. This is why sophisticated traders may be using calls instead of stock - lower gamma environment creates potential for explosive moves on positive catalysts.

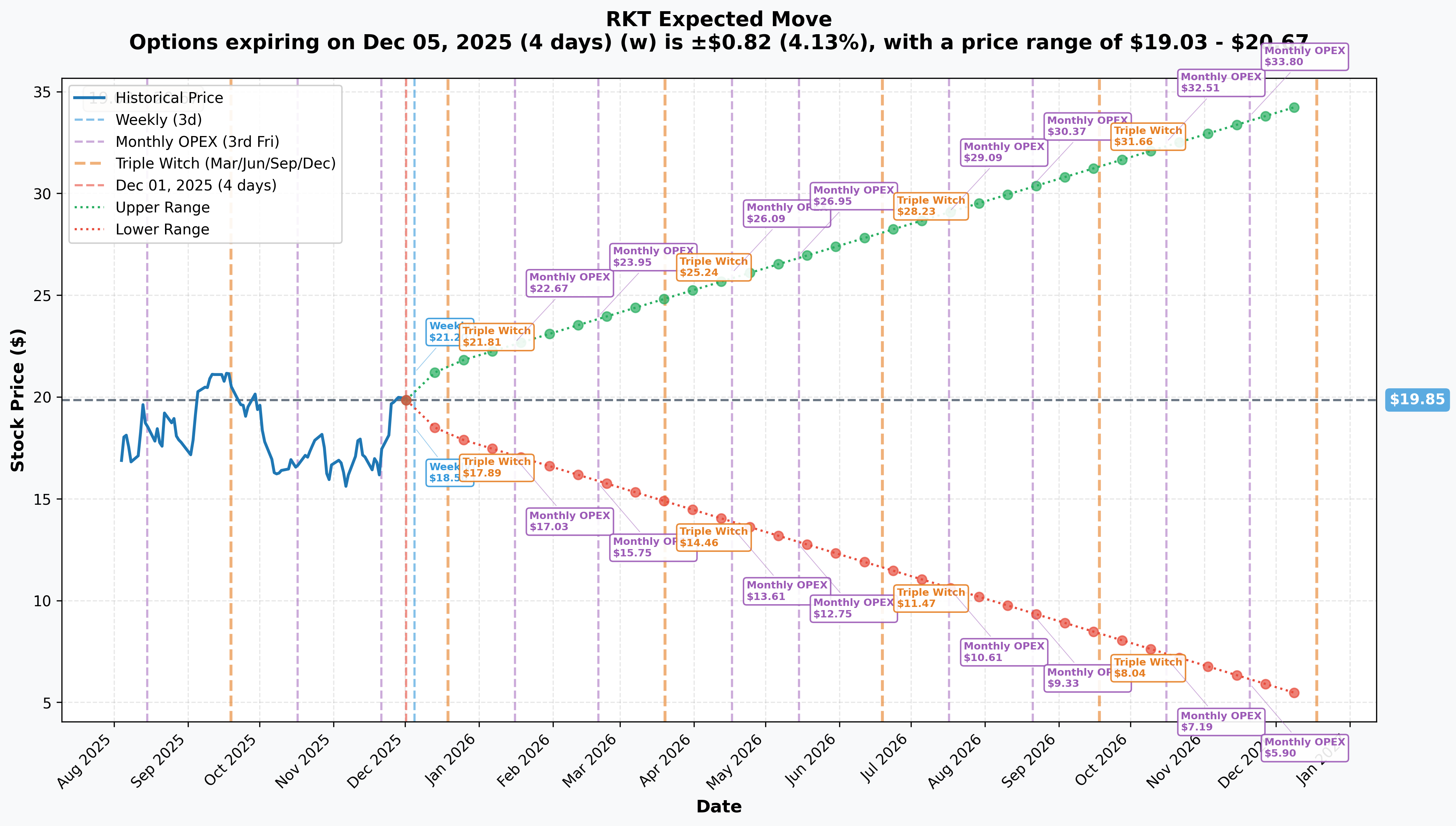

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 4 days): ±$0.82 (±4.13%) → Range: $19.03 - $20.67

- 📅 Monthly OPEX (Dec 19 - 18 days): ±$1.75 (±8.8%) → Range: $18.10 - $21.60

- 📅 Quarterly Triple Witch (Dec 19 - 18 days): ±$1.75 (±8.8%) → Range: $18.10 - $21.60

- 📅 March OPEX (Mar 20, 2026 - 109 days - THESE TRADES!): ±$14.73 (±74.2%) → Range: $5.12 - $34.58

Translation for regular folks: The market is pricing a relatively modest 4.1% move ($0.82) by this Friday for weekly expiration, but a more substantial 8.8% move ($1.75) through December OPEX which includes the critical December 9-10 Fed rate decision. The December implied move suggests options traders expect stock to trade in the $18.10-$21.60 range - notice that aligns perfectly with the $21 call strike at the upper end!

The March 20, 2026 expiration (when these $6.3M trades expire) shows a MASSIVE ±74.2% implied move with upper range of $34.58. This extreme wide range reflects enormous uncertainty over 109 days including Fed decisions, earnings, and integration progress.

Key insight: The call buyer is positioning for RKT to reach $21-25 by March expiration. Current December implied move upper range of $21.60 suggests the market thinks there's a reasonable probability of hitting the $21 strike by month-end if Fed cuts materialize. The $25 strike represents a more aggressive bet that momentum continues through Q1 2026 as refinance volume accelerates.

🎪 Catalysts

🔥 Immediate Catalysts (Next 10 Days)

Federal Reserve Interest Rate Decision - December 9-10, 2025 (8 DAYS AWAY!) 📊

The Fed's December FOMC meeting represents THE most critical near-term catalyst for RKT and mortgage stocks:

- 📊 Probability: 85% chance of 25 bps rate cut per CME FedWatch Tool as of November 26

- 💪 Fed Official Support: Governor Christopher Waller publicly advocated for December cut citing labor market concerns - rare explicit forward guidance

- 💰 Direct Impact on RKT:

- Immediate reduction in Rocket's funding costs, improving loan origination spreads

- 30-year mortgage rates expected to decline 10-20 bps from current 6.23% toward critical 6.0% refinance threshold

- Each 50 bps mortgage rate decline historically increases refinance volume 15-25%

- Potential to add $300-500M in quarterly adjusted revenue if refi wave accelerates

- 🎯 Market Catalyst: RKT jumped 8.44% on November 25 purely on Fed rate cut optimism - actual cut could trigger even larger move

- 📈 Refinance Context: 69% of homeowners currently locked into sub-5% mortgages - but as rates approach 6%, the refinance opportunity expands dramatically for improvement loans, cash-outs, and rate-term refinances

Why this matters: The $21 call buyer is clearly positioning for the Fed cut to be the catalyst that pushes RKT above $21 in coming weeks. If Fed cuts 25 bps and signals more cuts ahead, mortgage rates dropping toward 6% could unlock refinance wave and send stock toward $22-23 by year-end.

UBS Global Technology and AI Conference - December 3, 2025 (2 DAYS AWAY!) 🎤

- Date: Wednesday, December 3, 2025 at 12:55 PM MT

- Participant: CFO Brian Brown (fireside chat format)

- Topics Expected:

- AI investments in Rocket's mortgage platform technology

- Technology differentiation vs traditional lenders

- Mr. Cooper and Redfin integration progress updates

- Q4 2025 business momentum commentary

- Catalyst Potential: MEDIUM - CFO appearances often include updated business outlook and strategic direction

- Market Sensitivity: Any positive commentary on Q4 origination volume or integration synergies could provide near-term lift

🚀 Near-Term Catalysts (Q1 2026)

Q4 2025 Earnings Report - February 19, 2026 (80 Days Away) 📊

This will be THE defining moment for RKT's transformation story - the first full quarter with both Mr. Cooper and Redfin consolidated:

- 📅 Confirmed Date: February 19, 2026 after market close

- 💰 Company Guidance: $2.1B - $2.3B adjusted revenue vs Q3's $1.783B

- 📈 Consensus Estimates: $0.09 EPS for fiscal Q4

- 🎯 Critical Metrics to Watch:

- Net Rate Lock Volume: Q3 was $36B (+26% QoQ), need to see continued momentum

- Closed Loan Volume: Q3 was $32B (+11% QoQ), Q4 should show seasonal strength

- Gain on Sale Margin: Q3 was 2.80% - maintaining premium pricing power is critical

- Integration Progress: $500M Mr. Cooper synergies + $200M Redfin synergies on track?

- Purchase Market Share: Targeting doubling to 8% by 2027 from current 5.87%

- Servicing Revenue: First full quarter with $2.1T servicing portfolio

- 📊 Why It Matters: This earnings report will validate or refute the entire acquisition thesis. Strong results proving $700M combined synergies are achievable could send stock toward $25-30. Disappointing integration or margin compression could sink it back to $15-17.

Historical Context: Q3 2025 results (reported November 12) showed adjusted revenue of $1.783B beating $1.67B consensus, Q4 should build on this momentum with full quarter of acquisitions included.

Mr. Cooper Integration Milestones - Q4 2025 through Q1 2026 🏭

The $14.2B Mr. Cooper deal closed October 1, 2025 represents the largest independent mortgage transaction in U.S. history - execution is make-or-break:

- 🎯 Scale of Deal:

- Combined servicing portfolio: $2.1T across 10M homeowners (1 in 6 U.S. mortgages)

- Expected synergies: $500M annual run-rate revenue and cost synergies

- Exchange ratio: 11.0 RKT shares per COOP share ($143.33/share, 35% premium)

- 💼 Leadership: Jay Bray (former Mr. Cooper CEO) joined as President/CEO of Rocket Mortgage and board director - strong continuity signal

- 🏦 Regulatory Status: FHFA cleared with 20% counterparty risk limit stipulation - manageable constraint

- 📊 Key Milestones to Watch:

- Servicing platform consolidation progress (technology integration)

- Cross-selling initiatives: Rocket origination → Mr. Cooper servicing book

- System integration updates on earnings calls

- Employee retention at Mr. Cooper (critical for servicing quality)

- Synergy realization timeline: $125M quarterly run-rate by mid-2026?

- ⚠️ Risk: Integration complexity on unprecedented deal size - any delays or customer service issues could be catastrophic for stock

Redfin Integration & Product Expansion - Ongoing through Q1 2026 🏡

The $1.75B Redfin acquisition closed July 1, 2025 creates first true end-to-end homeownership platform:

- 🌐 Redfin Assets: 50M monthly visitors, 1M active listings, 2,200+ agents in 42 states

- 💰 Expected Synergies: $200M run-rate by 2027 ($140M cost savings, $60M revenue gains)

- 🎁 New Product: Rocket Preferred Pricing offering 1% interest rate reduction for clients using both Rocket Mortgage and Redfin - powerful value proposition

- 📱 Branding: "Redfin Powered by Rocket" branding launched

- 📊 Q1 2026 Metrics to Watch:

- Agent conversion rates: How many Redfin agents successfully funnel buyers to Rocket Mortgage?

- Rocket Preferred Pricing adoption: Attach rate and customer feedback

- Purchase market share gains: Target is 8% by 2027, need 6-6.5% by Q1 2026

- Technology platform unification announcements

- 💡 Strategic Value: Redfin gives Rocket direct access to homebuyers BEFORE they need a mortgage - massive competitive advantage vs. traditional lenders who only interact at application stage

Revenue Potential: $50M quarterly run-rate by 2027 implies ~$12-15M per quarter in 2026 from Redfin synergies.

📊 Medium-Term Catalysts (Q2-Q4 2026)

Mortgage Rate Environment Inflection Point 📉

The trajectory of mortgage rates through 2026 will determine RKT's revenue growth:

- 📍 Current Rate: 6.23% (30-year fixed, November 26, 2025)

- 🎯 Fannie Mae Forecast: 6.4% by end of 2025, 5.9% by end of 2026

- 🏦 MBA Forecast: 6.5% by end of 2025

- 💥 Refinance Catalyst Threshold: Rates below 6.0% unlock refinance wave - 69% of homeowners with sub-5% mortgages become candidates

- 📈 Market Impact: Fannie Mae projects $1.85T total mortgage originations in 2025 → $2.32T in 2026, with refinance share rising from 26% to 35%

- ⏰ Expected Timing: Mid-2026 if Fed continues cuts through H1 2026

- 💰 Revenue Impact for RKT: Each 1% market share = ~$23B origination volume at $2.32T market size. At 5.87% current share, that's $136B originations. Growing to 8% target = $186B (+$50B increase = +37% volume growth!)

Purchase Market Share Expansion Campaign 🎯

RKT has clear strategic target to transform from refinance-heavy to balanced originator:

- 📊 Current Position: 5.87% market share in 2024, tied with UWM at 5.95%

- 🎯 Stated Goal: Double purchase market share to 8% by 2027; expand refinance share to 20%

- 📈 2024 Progress: +8% YoY purchase market share growth - on track

- 🏡 Redfin Advantage: 50M monthly web visitors provides direct access to purchase market that traditional lenders can't match

- 💰 Revenue Impact: Each 1% market share gain = ~$15-20B annual origination volume at current market size

- 📅 Milestones: Quarterly progress updates starting February 2026 earnings - watch for 6%+ purchase share in Q4 2025

Market Position & Competitive Dynamics

🏆 Market Leadership Post-Acquisitions

RKT has transformed from pure originator to end-to-end mortgage platform:

- 🥇 #1 Servicer: $2.1T servicing portfolio post-Mr. Cooper deal - largest in America

- 🥈 #2-3 Originator: 5.87% market share, tied with UWM as top independent lenders

- 💰 2024 Performance: $101.2B origination volume (+29% YoY)

- 🎯 Client Retention: 97% retention rate in 2024 - industry-leading loyalty

- 🔄 Vertically Integrated: Only major lender with origination + servicing + brokerage under one roof

🥊 Competitive Positioning

vs. UWM Holdings (Primary Non-Bank Competitor):

UWM remains the key rival in independent mortgage lending:

- 📊 Business Models: Rocket's retail/direct model (2.80% gain-on-sale margin) vs UWM's wholesale/broker model (1.30% GOSM)

- 💪 Differentiation: Rocket = higher revenue per loan with brand premium; UWM = volume leader with lower margins

- 📈 2024 Volume: Rocket $101.2B vs UWM $108.3B (UWM slightly ahead in originations)

- 🛡️ Post-Acquisition Edge: Rocket's servicing dominance ($2.1T) vs UWM's origination focus creates different earnings profiles - Rocket more defensive in high-rate environments with recurring servicing revenue

- ⚔️ Market Battle: UWM's "All In" ultimatum to brokers created friction, but Rocket's direct-to-consumer model avoids broker channel conflicts

vs. Traditional Banks (Wells Fargo, Bank of America, Chase):

- 🚀 Technology Advantage: AI-driven platform, 50M monthly web visitors via Redfin

- ⚡ Speed to Close: Digital-first process vs traditional branch-based competitors

- 📊 Market Share Gains: Winning share from traditional banks in purchase market as consumers prefer digital experience

- 💻 Platform Effect: Redfin integration creates "browse → buy → finance" experience banks can't replicate

Key Advantage: The combination of #1 servicing position + direct consumer access via Redfin + technology platform creates sustainable moat. No other lender has this trifecta.

📊 Valuation Context

RKT's valuation must be viewed through transformation lens:

- 🎯 Analyst Targets: Average price target $18.18-$20.68 depending on source

- 🚀 Bull Case Targets: $25 (BTIG, Oppenheimer) - see 25%+ upside

- 😰 Bear Case Targets: $10.50-12.50 (JPMorgan range) - concerned about margin compression

- 📊 Rating Mix: 15% Strong Buy, 8% Buy, 69% Hold, 8% Sell (13 analysts)

- 💰 Recent Upgrades:

- 📉 Recent Downgrades:

The $6.3M call buyer is clearly in the bullish camp, betting on $21-25 price targets within 4 months.

🎲 Price Targets & Probabilities

Using technical levels, implied moves, Fed timing, and earnings catalysts, here are the scenarios through March 20, 2026 expiration:

📈 Bull Case (35% probability)

Target: $25-28 (Call strikes profitable!)

How we get there:

- 💪 Fed Delivers: 25 bps cut December 9-10 confirmed, with guidance for 2-3 more cuts in H1 2026

- 📉 Mortgage Rates Drop: 30-year rates decline from 6.23% toward 6.0% or below by February

- 🚀 Refinance Wave Begins: Q4 volume accelerates as homeowners refinance at improving rates

- 📊 Earnings Crush: February 19 Q4 report shows revenue at high-end of $2.1-2.3B guidance, beat on EPS

- 💼 Integration Progress: Mr. Cooper synergies tracking toward $500M target, no major hiccups

- 🏡 Redfin Momentum: Rocket Preferred Pricing showing strong adoption, purchase market share growing toward 6.5%

- 📈 Margin Stability: Gain-on-sale margins maintain 2.70-2.80% range proving pricing power

- 🎯 Market Recognition: Street upgrades accelerate as transformation narrative validated

Key metrics needed:

- Net rate lock volume >$40B in Q4 (vs $36B Q3)

- Purchase market share 6.3-6.5% (vs 5.87% in 2024)

- Integration costs declining sequentially

- Q1 2026 guidance implying continued momentum

Call P&L in Bull Case:

- $21 calls at $25 stock: Worth $4.00, profit = $1.90/share × 20,000 = $3.8M gain (90% ROI)

- $25 calls at $28 stock: Worth $3.00, profit = $1.95/share × 20,000 = $3.9M gain (186% ROI!)

- Combined profit: ~$7.7M on $6.3M investment = 122% return

Probability assessment: 35% because it requires Fed cooperation (85% likely) + strong execution on dual integrations (70% likely) + favorable housing market conditions (80% likely). This is the scenario the $6.3M call buyer is betting on.

🎯 Base Case (45% probability)

Target: $18-22 range (Partial profit on $21 calls)

Most likely scenario:

- ✅ Fed Cuts as Expected: 25 bps in December, 1-2 more cuts by March

- 📊 Mortgage Rates Grind Lower: Slow decline to 6.0-6.1% by Q1 2026 - refinance uptick but not explosion

- 💼 Solid Earnings: Q4 revenue $2.1-2.2B meeting guidance, EPS in-line

- ⚖️ Integration On-Track: Progress visible on synergies but not spectacular, some costs offsetting gains

- 🏡 Redfin Steady: Purchase market share growing modestly to 6.0-6.2%

- 💰 Margin Pressure: GOSM compresses slightly to 2.60-2.70% due to competitive pricing to win share

- 📈 Stock Consolidates: Trading range-bound $18-22 as market waits for bigger catalysts

- 🎪 Volatility Post-Earnings: Stock initially rallies to $22-23 on earnings beat, then pulls back to $19-21 range

Why 45% probability: This reflects "good but not great" execution where all elements work but none exceed expectations dramatically. Fed cuts help but refinance boom takes longer to materialize than bulls hope. Integrations proceed without major issues but also without wow factor.

Call P&L in Base Case (stock at $21):

- $21 calls at $21 stock: Worth $0-2.00 (depends on timing), profit/loss = -$0.10 to +$0.30 per share = -$200K to +$600K (0-14% return)

- $25 calls at $21 stock: Worth $0 (expire worthless), loss = -$1.05/share × 20,000 = -$2.1M (100% loss)

- Combined outcome: Breakeven to small loss overall - $21 calls cushion losses from $25 calls

This is the "premium paid for upside optionality" scenario - doesn't make money but doesn't blow up either.

📉 Bear Case (20% probability)

Target: $15-18 (Both call strikes lose money)

What could go wrong:

- 🚨 Fed Holds or Cuts Less: December cut happens but Fed signals "higher for longer" in 2026 - only 1 more cut vs 3-4 expected

- 📈 Rates Stuck High: Mortgage rates stay 6.2-6.5% range through Q1 2026, refinance wave delayed to H2 2026

- 😰 Integration Stumbles: Mr. Cooper technology integration hits delays, customer service issues emerge, synergies pushed back 6-12 months

- 💸 Margin Compression: Jefferies survey concerns materialize - GOSM drops to 2.40-2.50% as UWM's lower-cost model wins share

- 📉 Earnings Miss: Q4 revenue $2.0B (below $2.1B low-end), weak Q1 guidance

- 🏚️ Housing Market Weakness: Home prices decline or affordability crisis worsens, transaction volumes fall

- 🇨🇳 Broader Market Selloff: Tech/growth names crater on recession fears, drags financials down

- 📊 Legal Issues: Girard Sharp Law securities investigation uncovers material problems with acquisition disclosures

Call P&L in Bear Case (stock at $17):

- $21 calls at $17 stock: Worth $0 (expire worthless), loss = -$2.10/share × 20,000 = -$4.2M (100% loss)

- $25 calls at $17 stock: Worth $0 (expire worthless), loss = -$1.05/share × 20,000 = -$2.1M (100% loss)

- Combined loss: -$6.3M (100% of premium paid)

Probability assessment: Only 20% because it requires multiple negative catalysts. RKT's fundamentals remain strong (returned to profitability in 2024 with $636M net income), acquisitions strategically sound, Fed likely to cut. Main risk is timing - refinance wave delayed beyond March expiration.

💡 Trading Ideas

🛡️ Conservative: Wait for Fed Clarity, Buy Dips

Play: Stay in cash until after December Fed decision, then buy stock on pullbacks

Why this works:

- ⏰ Fed Decision in 8 Days: Binary event with 85% cut probability but 15% hold risk - why guess?

- 📊 Avoid Overpaying: RKT at $19.85 near YTD highs of $20.08 - better entry likely on any Fed disappointment

- 💰 Stock Over Options: At 109 days, time decay isn't your friend - stock ownership captures upside without theta bleed

- 🎯 Support Levels: Buy at $18-18.50 if Fed cuts (likely quick dip then rally), or $16.50-17.50 if Fed holds (bigger discount)

- 📈 Multi-Month Hold: Position for 6-12 month refinance wave story, not just March expiration

Action plan:

- 👀 Watch December 9-10 Fed decision closely - look for 25 bps cut + dovish forward guidance

- 🎯 Target entry: $18.00-18.50 (8-10% below current) within 2-3 weeks post-Fed

- 📊 Size position: 3-5% of portfolio (meaningful but not reckless)

- ⏰ Hold through February 19 earnings - reassess based on Q4 results and Q1 guidance

- 🛡️ Set mental stop at $16 (support from October breakout) to protect capital

Expected outcome: Avoid potential -10% drawdown if Fed disappoints, capture upside if refinance thesis plays out in 2026. Conservative 20-30% gain target by mid-2026.

Risk level: Low-Moderate (stock position, defined stop) | Skill level: Beginner-friendly

⚖️ Balanced: Post-Fed Bull Call Spread (Defined Risk)

Play: After Fed decision, enter bull call spread similar to institutional structure but with risk management

Structure: Buy $20 calls, Sell $24 calls (March 20, 2026 expiration - SAME as the $6.3M trade)

Why this works:

- 🎯 Defined Risk: $4 wide spread = $400 max risk per spread (vs unlimited risk of naked calls)

- 💸 Lower Cost: Net debit ~$1.50-2.00 per spread (vs $2.10-1.05 for straight calls)

- 📊 "Copy The Whale": Positioning between their $21 and $25 strikes captures the same thesis

- ⏰ Post-Fed Entry: Wait for Fed to cut before entering - removes binary risk

- 🎢 Earnings Catalyst: February 19 earnings still 80 days away provides major catalyst

- 📈 Risk/Reward: Max profit $2.00-2.50 on $1.50-2.00 risk = 100-150% return if stock >$24 at expiration

Estimated P&L (after Fed cuts):

- 💰 Cost: ~$1.50-2.00 net debit per spread (adjust for actual post-Fed prices)

- 📈 Max profit: $2.00-2.50 if RKT above $24 at March expiration (100-150% gain)

- 📉 Max loss: $1.50-2.00 if RKT below $20 at expiration (100% loss, but defined)

- 🎯 Breakeven: ~$21.50-22.00 (8-11% rally from current)

- 📊 Profit zone: Stock anywhere $22-30 produces profit

Entry timing:

- ⏰ Wait for Fed cut: Enter December 11-13 after Fed confirms 25 bps cut

- 🎯 Stock location: Only enter if RKT trading $19-20.50 range (gives room to work)

- ❌ Skip if: RKT already above $21 (spread too expensive), or Fed holds rates (thesis broken)

Position sizing:

- Risk 3-5% of portfolio (5-10 spreads depending on account size)

- Each spread costs $150-200, so $1,500-2,000 total for 10 spreads

- Max profit potential: $2,000-2,500 if RKT rallies to $24+

Risk level: Moderate (defined risk, directional bullish) | Skill level: Intermediate

Why better than straight calls: Selling the $24 call reduces cost and caps upside, but dramatically improves probability of profit. You don't need RKT to moon to $28 - just reach $22-24 range which is very achievable if Fed cuts and earnings deliver.

🚀 Aggressive: Replicate The Institutional Trade (BIG RISK!)

Play: Copy the exact trade structure - buy both March $21 and $25 calls

Structure:

- Buy $21 calls @ ~$2.10 per contract

- Buy $25 calls @ ~$1.05 per contract

- March 20, 2026 expiration (109 days)

Why this could work:

- 🐋 Follow Smart Money: This institutional player risked $6.3M - they know something or see opportunity we might not

- 🎯 Two Strike Strategy: $21 calls = base case (5-10% rally), $25 calls = home run case (25-30% rally)

- 💥 Multiple Catalysts: Fed cut (8 days) + Earnings (80 days) + potential additional Fed cuts in Q1 2026

- 📈 Refinance Explosion Potential: If rates hit 5.9% by March (Fannie Mae forecast), refinance volume could surprise massively to upside

- 🚀 Leverage: Control large stock position with relatively small capital outlay

- ⏰ Time to Work: 109 days gives thesis time to play out through earnings and rate cuts

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Each $21 call costs $210, each $25 call costs $105 - total $315 per pair

- ⏰ TIME DECAY KILLER: Losing ~$2-3/day in time value across both positions as expiration approaches

- 😱 Binary Risks: Fed holds rates = immediate -20-30% loss on positions. Earnings miss = another -30-50% loss

- 📉 Need Big Move: Stock must rally to $23+ just to breakeven on $21 calls, $26+ on $25 calls

- 🎢 Volatility Risk: Even if stock goes to $21-22, might not be enough to profit after time decay

- 💀 Total Loss Possible: If RKT stays $18-20 range through March, lose 70-100% of premium

Estimated P&L:

- 💰 Cost: $315 per pair of calls ($210 + $105)

- 📈 Profit scenario: Stock at $25 = $21 calls worth $4.00 (+$190 profit), $25 calls worthless (-$105 loss) = +$85 net (+27% return)

- 🚀 Home run: Stock at $28 = $21 calls worth $7.00 (+$490 profit), $25 calls worth $3.00 (+$195 profit) = +$685 net (+217% return!)

- 📉 Loss scenario: Stock at $20 = both calls expire worthless = -$315 (100% loss)

Breakeven points:

CRITICAL WARNINGS - DO NOT attempt unless you:

- ✅ Can afford 100% loss of entire premium with zero impact to lifestyle

- ✅ Have traded options through earnings/Fed decisions and understand volatility dynamics

- ✅ Understand you're betting WITH the institutional trade but they may have hedges/information you don't

- ✅ Accept that institutional player may be WRONG - smart money loses too

- ✅ Can monitor positions daily and take profits if stock hits $22-24 before expiration

- ✅ Will cut losses if Fed doesn't cut in December - don't diamond hands into zero

Position sizing: Risk ONLY 2-3% of total portfolio maximum. If you have $50K account, risk $1,000-1,500 max (3-5 call pairs).

Exit strategy:

- 🎯 Take profits early: If RKT hits $23-24 by January, consider selling 50-75% to lock in gains

- 🛡️ Stop loss: If Fed doesn't cut or RKT breaks below $18, close position immediately

- ⏰ Don't hold to expiration: Plan to close 2-3 weeks before March 20 to avoid final theta crush

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~30-35% (need multiple things to go right - Fed cuts, earnings beat, rates drop, integration smooth)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📅 Fed Decision Binary Risk (8 days!): While 85% probability of 25 bps cut is high, 15% hold probability remains real. Recent inflation data has caused volatility - RKT shares sank when yields rose on inflation concerns. If Fed holds or cuts but signals "one and done," mortgage refinance thesis crumbles and stock could gap down 10-15% overnight. Options would lose 30-50% value immediately.

-

💸 Integration Execution on Largest Mortgage Deal Ever: The $14.2B Mr. Cooper acquisition represents the largest independent mortgage transaction in U.S. history - unprecedented complexity. Technology platform consolidation of servicing for 10M homeowners is massive undertaking. Any customer service degradation, system outages, or compliance issues would be catastrophic. Legal scrutiny from Girard Sharp Law over potential securities claims adds regulatory risk. FHFA's 20% counterparty limit constrains growth flexibility.

-

🏚️ Margin Compression From Competitive Pressure: Jefferies downgrade cited broker survey showing "Competition & Margins are Worse than Expected". RKT's 2.80% gain-on-sale margin vs UWM's 1.30% wholesale model creates pricing pressure. In race for market share, RKT may sacrifice margins to win volume. Q3 2025 concern showed adjusted EPS revised down to $0.01 from $0.10 and book value declined 13% QoQ to $3.72 from $4.30.

-

⏰ Refinance Wave Timing Uncertainty: While Fannie Mae forecasts rates at 5.9% by end of 2026, timing is uncertain. Rates could stay 6.2-6.5% through Q1 2026 if inflation proves sticky. 69% of homeowners locked into sub-5% mortgages won't refinance until rates hit 5.5-6.0% zone. March expiration may be too early to capture refinance boom. The call buyer may need to roll positions forward if wave delayed to H2 2026.

-

📉 Valuation Risk After 87.5% YTD Rally: RKT has already rallied from $10.58 to $19.85 (+87.5%) pricing in substantial good news. Trading near YTD highs of $20.08 leaves little margin of safety. At current $56.3B market cap, stock is priced for flawless execution on ambitious $8.7B revenue and $3.2B earnings by 2028 targets requiring 19.3% annual revenue growth. Any stumble could trigger 20-30% correction back to $14-16 range erasing most 2025 gains.

-

🏦 Housing Market Macro Headwinds: Persistent housing affordability challenges threaten origination volume as high prices + high rates = reduced transactions. Fannie Mae forecasts only 2.8% price growth in 2025, potential -0.2% decline in 2026 per MBA. Rate lock-in effect prevented 1.72M home sales 2022-2024 - could persist if rates don't drop aggressively. Recession risk would crater mortgage volumes regardless of rates.

-

🥊 UWM's Aggressive Market Share Battle: UWM surpassed Rocket in 2023 originations ($108.3B vs $78.7B) using wholesale model advantage and "All In" ultimatum to brokers. UWM's 1.30% GOSM allows aggressive pricing that forces RKT to choose between volume or margins. UWM's "Game On" pricing strategy specifically targeting Rocket's retail business creates structural headwind.

-

📊 $700M Combined Synergy Target is Aggressive: Mr. Cooper $500M + Redfin $200M in annual synergies must materialize by 2027 to justify acquisition premiums. These targets require perfect execution on technology integration, cost rationalization, and revenue cross-selling. History shows most M&A deals achieve only 50-70% of projected synergies. Missing these targets would force major valuation reset.

-

🐋 Insider Selling at Peak: Director Matthew Rizik sold 5,000 shares totaling ~$97K on November 25-26 under Rule 10b5-1 plan during +17% weekly gain. While small size and pre-planned, insider selling near highs is noteworthy signal. Minimal institutional holding data available creates transparency concerns about smart money positioning.

-

📉 Analyst Skepticism Remains: Despite recent upgrades, JPMorgan maintains Underweight with $12.50 target (-37% downside), Goldman Sachs Neutral at $14.00 (-30% downside). Bear case argues valuation risk after acquisitions and margin compression outweigh refinance opportunity. Consensus remains cautious with 69% Hold ratings.

🎯 The Bottom Line

Real talk: Someone with serious conviction just bet $6.3 MILLION that RKT rallies 25-30% over the next 109 days. This isn't a hedge or insurance - this is pure bullish aggression targeting $21-25 by March 2026. The timing is laser-focused: 8 days until Fed decision, 80 days until transformational Q4 earnings, and capturing the potential early stages of a massive refinance wave.

What this trade tells us:

- 🎯 Fed Cut Confidence: The $21/$25 call structure screams "Fed will cut multiple times in Q4 2025 - Q1 2026"

- 💰 Refinance Wave Bet: Positioning for mortgage rates to drop from 6.23% toward 6.0% or below, unlocking refinance explosion

- 📊 Earnings Conviction: February 19 Q4 results expected to validate Mr. Cooper + Redfin transformation with revenue above $2.2B

- 🏦 Integration Confidence: Betting that largest mortgage deal in history executes smoothly with visible synergies

- 🚀 Two-Strike Strategy: $21 calls = conservative base case ($4.2M bet), $25 calls = aggressive moonshot ($2.1M lottery ticket)

This is NOT a "buy at any price" signal - it's a "major catalyst wave is building" signal.

If you own RKT:

- ✅ Hold Through Fed Decision: December 9-10 Fed meeting could provide 5-10% pop if 25 bps cut confirmed with dovish guidance

- 📊 Consider Trimming at $22-23: If stock rallies post-Fed, taking 25-30% profits protects gains while staying exposed to earnings upside

- ⏰ Hold Core Through Earnings: February 19 is THE validation moment for $15.95B acquisition strategy

- 🛡️ Mental Stop at $17: If Fed doesn't cut or earnings disappoint, protect capital by exiting below $17 (October breakout level)

If you're watching from sidelines:

- ⏰ Wait for Fed Decision December 9-10 - don't front-run this binary catalyst

- 🎯 Best Entry Scenario: Fed cuts but stock dips to $18-18.50 on "sell the news" - buy that dip

- 📈 Alternative Entry: Post-earnings pullback in late February if results good but stock overheats

- 🚀 Longer-term (6-12 months): Refinance wave thesis remains compelling if rates hit 5.9% by end of 2026 - stock could reach $25-30

- ⚠️ Avoid Chase: Don't buy at $20.50+ - risk/reward terrible with Fed decision pending

If you're considering the options trade:

- 🎯 Wait Until After Fed: Binary risk too high at 8 days out - let Fed decision clear before entering

- 📊 Bull Call Spreads Better Than Naked Calls: $20/$24 spread offers similar upside with 40-50% less capital at risk

- ⚠️ Size Appropriately: Risk only 2-5% of portfolio on directional options bet

- ⏰ Don't Hold to Expiration: Take profits if stock hits $22-24 by January/February - lock in wins early

Mark your calendar - Key dates:

- 📅 December 3 (Tuesday) - UBS Tech/AI Conference with CFO Brian Brown

- 📅 December 9-10 (Monday-Tuesday) - Fed FOMC meeting and rate decision (CRITICAL!)

- 📅 December 19 (Thursday) - Monthly/Quarterly OPEX (implied move ±$1.75 window closes)

- 📅 February 19, 2026 (Thursday after close) - Q4 2025 earnings report (TRANSFORMATION REVEAL!)

- 📅 March 20, 2026 (Friday) - Options expiration for these $6.3M call trades

- 📅 H1 2026 - Integration milestones and synergy realization updates

- 📅 End of 2026 - Fannie Mae projects mortgage rates at 5.9% - refinance wave peak

Final verdict: RKT's transformation story is REAL - becoming #1 servicer with $2.1T portfolio while adding 50M monthly Redfin web visitors creates unprecedented competitive moat in mortgage lending. The refinance wave catalyst is LEGITIMATE - Fed cuts + falling rates could add $300-500M quarterly revenue as volumes accelerate. The $6.3M institutional call buy validates this thesis.

BUT - at $19.85 after 87.5% YTD rally, timing matters. The next 10 days (Fed decision) and 80 days (earnings) will determine if this is the beginning of a move to $25-30, or if RKT needs to consolidate $16-20 range before next leg higher.

Be smart. Let catalysts develop. The mortgage refinance opportunity will build through 2026 - you don't need to nail the exact bottom in December. Better to pay $18.50 after Fed clarity than $20 before the decision.

The institutions are loading up. The question is whether you join them now, or wait for better entry. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-scores (19.13 and 66.42) reflect these specific trades' sizes relative to recent RKT history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. Fed decisions and earnings create binary event risk with potential for 10-20% gaps either direction. The institutional call buyer may have complex portfolio positions, hedges, or information not available to retail traders.

About Rocket Companies: Rocket Companies operates as America's largest mortgage lender and servicer, offering direct-to-consumer mortgage origination through the Rocket Mortgage platform and servicing $2.1T across 10 million homeowners following the October 2025 Mr. Cooper acquisition. The company combines mortgage lending with real estate brokerage (Redfin) and personal finance services (Rocket Money) to create a comprehensive homeownership platform. Market cap: $56.3 billion in the Mortgage Bankers & Loan Correspondents industry.