🍞 TOST: Someone Just Locked in $1.2M Selling Calls — What Do They Know About May?

📅 March 10, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone holding a big TOST position just dumped $1.2 MILLION in call premium by selling 6,500 May $32 calls — a strike that's 10.2% above today's price of $29.03. This isn't a random trade: volume of 6,500 contracts landed against existing open interest of just 202, meaning this player essentially built the entire open interest at this strike from scratch. With Q1 2026 earnings landing right in this May window, the question isn't if they're managing risk — it's what they're positioning for.

📊 Company Overview

Toast Inc. (NYSE: TOST) is the dominant cloud-based restaurant technology platform in North America — think of it as the operating system that powers modern restaurants end-to-end:

- Market Cap: ~$15–18 billion

- Industry: Restaurant Technology / Fintech-Embedded SaaS

- Current Price: $28.79–$29.03

- Primary Business: POS hardware, software subscriptions, payment processing, payroll, marketing, and analytics — all built specifically for the restaurant industry. Toast processes $51.5 billion in Gross Payment Volume across 164,000 restaurant locations. When a restaurant uses Toast, it's not just running its register — it's running its entire business on Toast's rails.

💰 The Option Flow Breakdown

📊 What Just Happened (The Tape — March 10, 2026)

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | OI | Size | Spot | Option Price | Premium | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-03-10 | 13:32:17 ET | TOST | SELL | CALL | 2026-05-15 | $32 | 6,500 | 202 | 6,500 | $29.03 | $1.80 | $1.2M | TOST20260515C32 |

🤓 What This Actually Means

Real talk: this is not a bearish bet — it's a ceiling being put on someone's own position.

Let's break down exactly what happened here:

- 💸 $1.2M collected: The seller received $1.80 per contract × 6,500 contracts × 100 = $1,170,000 upfront, in cash, today

- 📊 32x normal volume: Volume of 6,500 hit against open interest of just 202 — that's a 32x ratio. There was basically no one at this strike before this trade. This player didn't join existing activity; they created it

- 🎯 Strike is 10.2% OTM: $32 vs spot at $29.03. The seller is saying "I'm happy capping my upside at $32 by May 15 in exchange for collecting $1.2M today"

- ⏰ May 15 expiration is critical: Q1 2026 earnings are expected in early-to-mid May. This trade captures the earnings window entirely

- 🔥 Z-score of 254.38: This ranks as EXTREMELY_UNUSUAL — we're talking a trade this large against this strike happens maybe a few times per year in TOST options

What's really happening here:

This is almost certainly a covered call write — a large TOST stockholder selling calls against their existing shares to harvest income. Here's the scenario: they own a substantial TOST position (think 650,000 shares worth ~$18.9M at today's price). They're not excited about the stock blasting through $32 before May 15, so they sell calls at $32, pocket $1.2M cash upfront, and effectively agree to sell their shares at $32 if TOST runs past that level by expiration.

Why would they do this now?

- 📉 TOST is down -15.3% YTD, trading at $28.79–$29.03 after starting 2026 at $34.02

- 💰 They may be recovering losses by selling premium against a depressed position

- 🎯 They believe TOST will not reclaim $32 before mid-May — a reasonable view given the YTD chart tells a story of distribution, not accumulation

- ⚠️ Alternatively: they're genuinely worried Q1 earnings (inside this window) won't be strong enough to push the stock past $32, so they collect the premium as a consolation prize

The key question: If this is a covered call, the seller is effectively saying "I'll take $1.80 per share guaranteed over the chance to participate in a rally past $32." That's a meaningful statement about their conviction heading into the May catalyst window.

📈 Technical Setup / Chart Check-Up

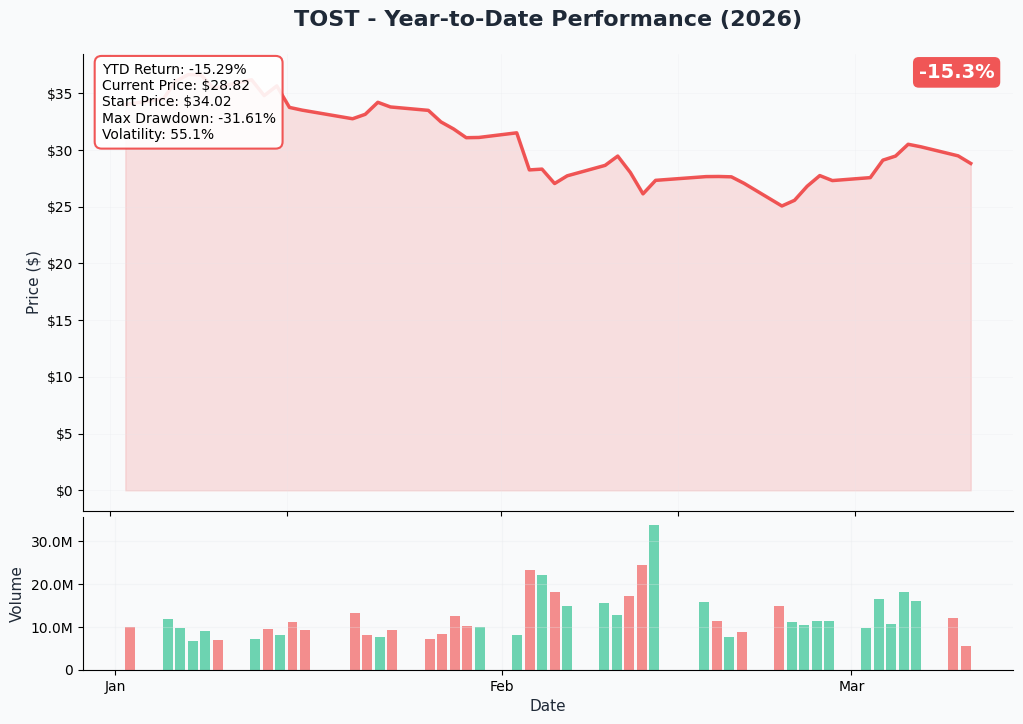

YTD Performance Chart

TOST started 2026 at $34.02 and has been steadily bleeding lower — currently down -15.3% YTD at $28.82. The chart tells a story of distribution: the stock peaked in the $34–$35 zone in early January, then sold off steadily through February before finding a floor around $25 in mid-February. March has seen a modest recovery back to the $28–$30 range, but there's been no real breakout.

Key observations from the YTD chart:

- 📉 Steady downtrend: Each attempted recovery has stalled at a lower high — $34 → $33 → $31 → $30 is the pattern

- 🔥 Volume spike in mid-February: The largest volume bars of the year coincide with Q4 2025 earnings on February 12 — heavy two-way action as buyers tried to hold and sellers used the pop to reduce exposure

- 📊 Max drawdown of -31.61%: The stock touched as low as ~$23.50 from the 2026 highs — a brutal compression despite strong fundamentals

- 🎢 Volatility at 55.1%: This isn't a sleepy fintech stock. With 55% annualized vol, TOST can swing $1.50–$2 on a random Tuesday with no news catalyst

- 🧱 $32 is a wall: Looking at the YTD chart, $32 was the mid-January support level that became resistance after the break. The covered call seller picked precisely the level where prior demand became supply. That's not random — that's someone who knows their chart.

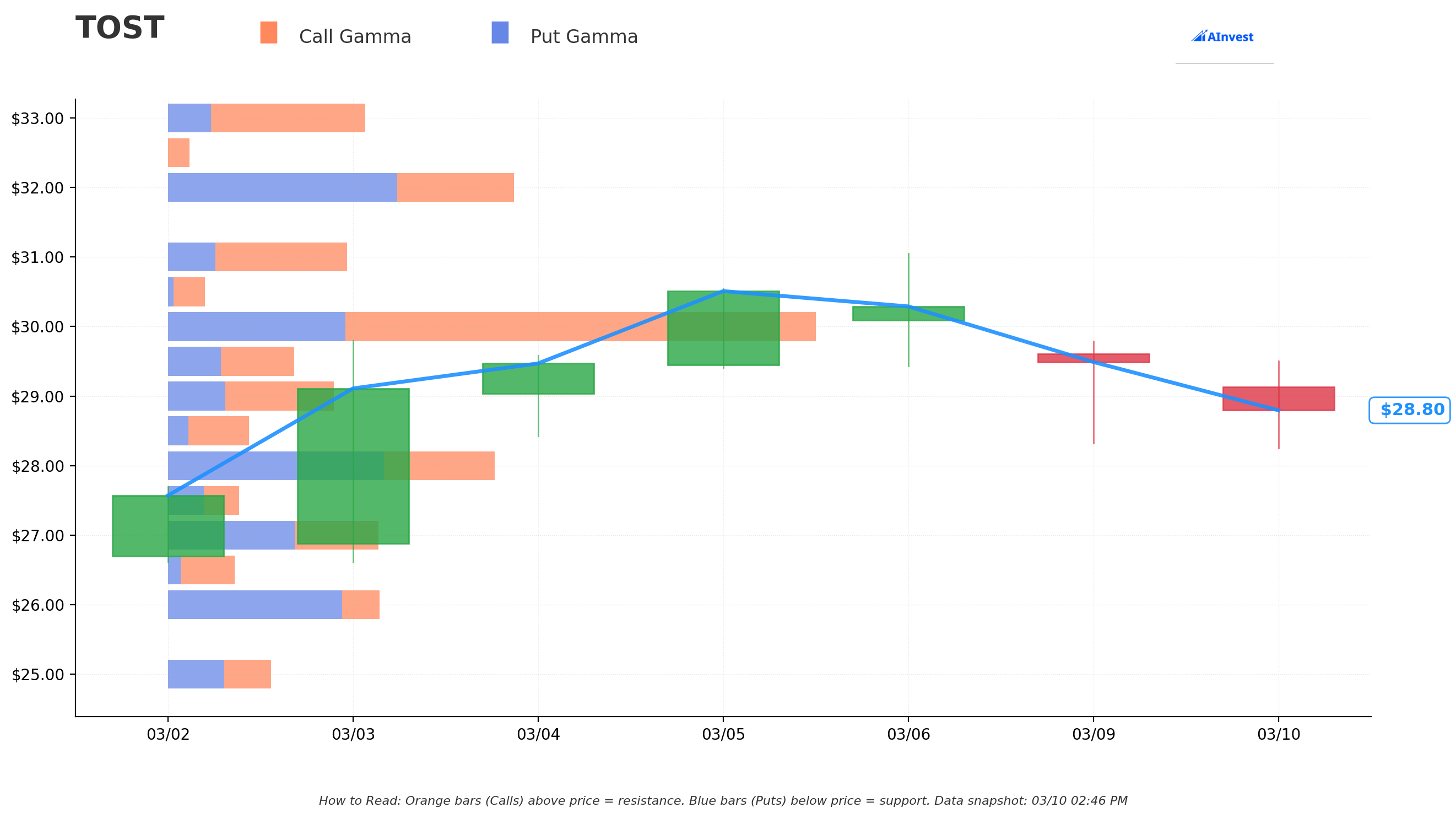

Gamma-Based Support & Resistance Analysis

Current Price: $28.80

The gamma exposure map (data snapshot: March 10, 2:46 PM) shows TOST pinned right between two zones of moderate options activity. Here's what the bars are telling us:

🔵 Support Levels (Put Gamma Below Price — Blue Bars):

- $28 — Nearest put concentration below current price; this is the immediate floor market makers are defending. A break of $28 would force dealers to sell shares as a hedge, accelerating downside

- $27 — Secondary support; moderate put open interest

- $26 — Extended support zone with some put accumulation

- $25 — Deep floor; residual put positioning from the February lows

🟠 Resistance Levels (Call Gamma Above Price — Orange Bars):

- $29 — Immediate overhead resistance. Orange call gamma just above current price means market makers are actively hedging by selling stock as price approaches $29, creating natural friction

- $30 — Moderate resistance; the psychological round number with call open interest

- $31 — Secondary resistance zone with orange call bars

- $32 — THIS IS THE TRADE STRIKE. The sold calls create a massive new call gamma exposure at $32. If TOST approaches this level, dealers who are now long these calls will sell stock into the rally to hedge — creating exactly the ceiling the seller wants

- $33–$34 — Extended resistance from January 2026 supply zone

Net GEX Bias: Bullish — Put gamma below price (support) is currently outweighing call gamma above, suggesting dealers are positioned to buy dips more aggressively than they sell rips. This is a modest tailwind for the stock at current levels around $28–$29.

What this means for the trade: The covered call seller placed their ceiling at $32 — which is exactly where the gamma chart shows a meaningful resistance cluster developing. They're essentially letting the options market structure work for them. Even if TOST wants to run, the $29 gamma resistance acts as a speed bump, and $32 becomes a near-impenetrable wall by May expiry given the new open interest they just created.

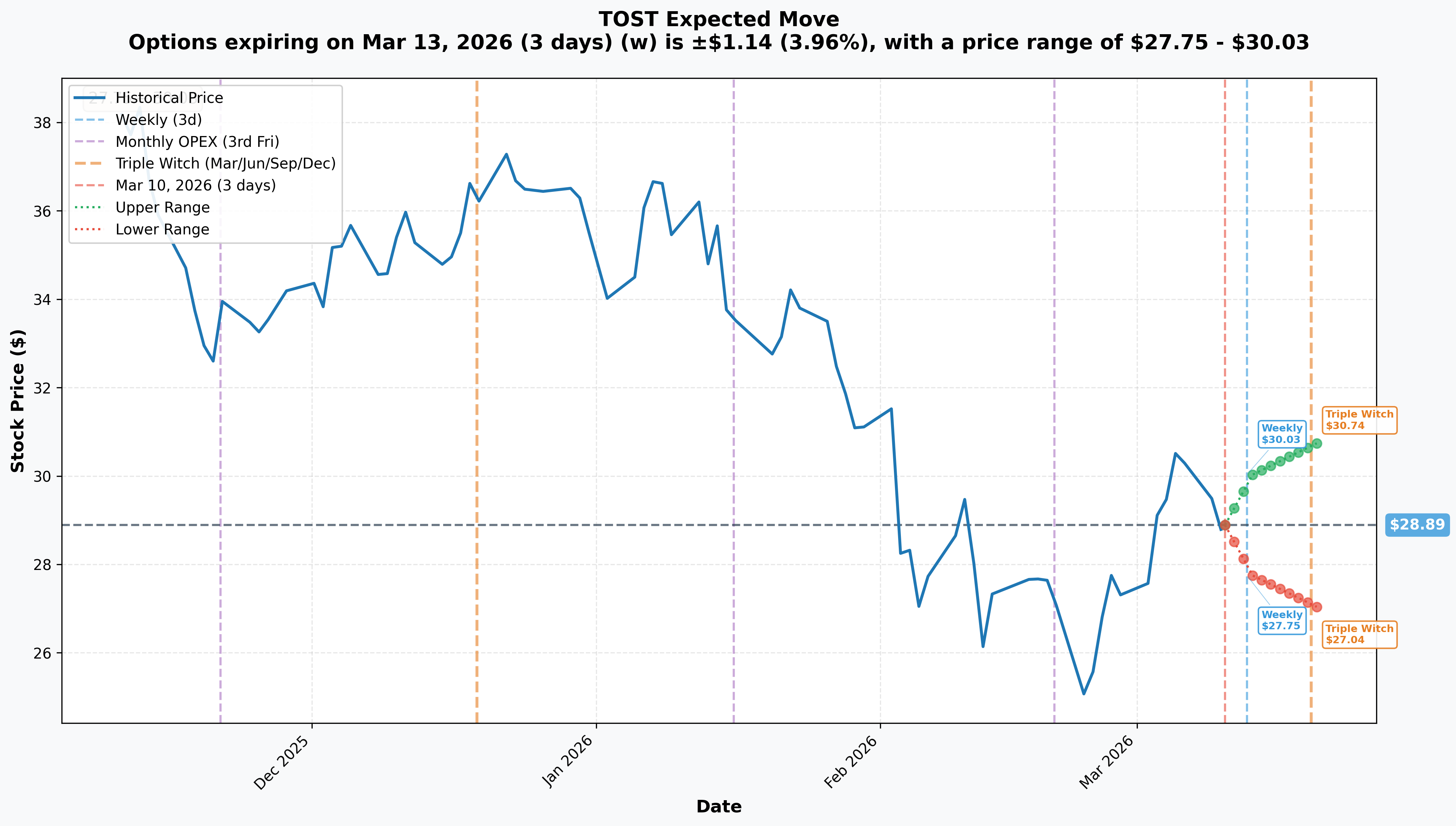

Implied Move Analysis

Options market expectations through key expirations:

- 📅 Weekly (March 13 — 3 days): ±$1.14 (±3.96%) → Range: $27.75 – $30.03

- 📅 Monthly OPEX (March — 3rd Friday): Range widens modestly from the weekly

- 📅 Triple Witch (Mar/Jun/Sep/Dec): Broader range captures macro events

- 📅 Current level: $28.89 (as shown on chart)

Translation for regular folks:

Options traders are pricing in a 3.96% move by Friday — roughly $1.14 either direction. That puts the ceiling for this week right at $30.03 and the floor at $27.75. Notice that $30 cap aligns almost perfectly with the gamma resistance identified above. The market is telling you: don't expect $32 this week.

For the May 15 expiration (when the sold calls expire), the implied move is considerably wider given the 66-day window and the Q1 earnings event embedded in that timeframe. But the covered call seller collected premium reflecting that wider implied move — they got paid because May options are pricier than weekly options. Smart timing.

Key insight: The weekly implied range of $27.75–$30.03 shows that even the market's optimistic scenario for this week doesn't reach the $32 strike. The seller has a comfortable 10.2% buffer today, and for TOST to threaten $32 by May 15, it would need either a blowout Q1 earnings report or a powerful re-rating catalyst. The seller is betting neither materializes strongly enough to move the stock 10%+ from here.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened — Context)

Q4 2025 Earnings — February 12, 2026 (BLOWOUT!) 📊

Toast reported an exceptional Q4 on February 12, 2026:

- 💰 Revenue: $1.6 billion, up +22% YoY

- 🎯 GAAP EPS: $0.16, beating consensus by 33.1%

- 🏆 First-ever GAAP quarterly profit: $101 million net income — a milestone for a company that burned cash for years

- 📈 ARR surpassed $2 billion — growing 26% YoY; this is the threshold that signals SaaS maturity

- 🤖 Toast IQ AI adoption: >50% of locations using it within 4 months, generating 8 million queries

- 🏢 Enterprise wins: Applebee's, Firehouse Subs, and Papa Murphy's all signed on

Despite the strong report, the stock sold off — a classic "buy the rumor, sell the news" dynamic, and a signal that expectations had been running ahead of results. Q4 revenue actually missed the analyst estimate slightly even as EPS crushed, suggesting the market is watching revenue growth more closely than profitability.

Morgan Stanley TMT Conference — March 3, 2026 (+5.6%) 🎤

Toast presented at the Morgan Stanley TMT Conference on March 3, with CEO Aman Narang and CFO Elena Gomez. Stock rallied 5.6% on the day as investors revisited the Q4 results, the expanded $500M buyback, and the 2026 profitability trajectory. That pop from ~$27.50 to ~$29.00+ has essentially held through March 10 — the covered call was likely placed near the top of that recovery rally.

$500M Share Buyback Authorization 🛡️

Toast expanded its buyback program alongside Q4 earnings, providing structural price support. A $500M program against a ~$15B market cap represents ~3.3% of float — meaningful for a stock that's been under distribution pressure.

Instacart Partnership — February 10, 2026 🤝

Toast and Instacart announced a strategic partnership integrating delivery and restaurant management workflows. This deepens Toast's embedded position in the restaurant tech stack.

🚀 Upcoming Catalysts (Next 90 Days — What Matters for This Trade)

Q1 2026 Earnings — Expected May 2026 (INSIDE THE TRADE WINDOW!) 📊

This is THE catalyst the May 15 sold calls were built around. First quarter results will be the first proof point for Toast's 2026 guidance of $775–$795M adjusted EBITDA. Key metrics the market will focus on:

- 🎯 Revenue tracking toward 20%+ growth — any deceleration from Q4's 22% would be a red flag

- 📍 Net location adds — consensus expects 7,000–8,000 net new locations in Q1 (Toast ended 2025 with 164,000)

- 🌍 International revenue — Australia was the first market; any UK or European announcement would be explosive

- 🤖 Toast IQ monetization — management has hinted at converting IQ's 50%+ adoption into a premium paid tier ($5–$15/location/month would add meaningful incremental ARR)

- 💰 Buyback pace — how much of the $500M has been deployed provides insight into management's price conviction

The covered call seller is making an implicit bet: Q1 results will be "solid but not spectacular" — good enough to not crash the stock, but not the blowout needed to push TOST from $29 past $32 (10%+ move) in a single earnings reaction.

International Expansion — Europe/UK Announcement 🌍

Following the Australia launch, Toast has indicated European expansion as a strategic priority. Any announcement of a UK or Western European launch before May 15 would materially expand the perceived TAM and could trigger the kind of re-rating that threatens the $32 ceiling.

Toast IQ Premium Tier Decision 🤖

Toast IQ reached >50% penetration within 4 months at zero cost to users. A decision to monetize it as a paid tier — even at $5–$15/location/month — adds $10–$30M quarterly revenue at high margins. An announcement here before May 15 could meaningfully re-rate ARPU estimates.

🎲 Price Targets & Probabilities

Using the gamma levels, implied move analysis, and the May 15 catalyst landscape, here are the three scenarios through expiration:

📈 Bull Case (20% probability)

Target: $32–$35 | Covered Call Gets Exercised

How we get there:

- 💥 Q1 2026 earnings deliver a genuine beat-and-raise — revenue accelerates to 25%+ and EBITDA guidance gets lifted

- 🌍 European market announcement drops before May 15, expanding the TAM narrative

- 🤖 Toast IQ premium tier launch — even a $10/location/month fee across 80,000+ locations is ~$10M/quarter of new high-margin ARR

- 📈 Stock clears $29 gamma resistance → $30 psychological level → $32 (the strike wall)

- 🛒 Buyback acceleration provides mechanical buying support during any pullbacks

- 🏢 Additional enterprise chain announcement (a 1,000+ location QSR deal on the size of Papa Murphy's) triggers institutional re-rating

For the covered call seller: If TOST hits $32, they sell their shares at $32 regardless. Net effective price with the $1.80 premium collected = $33.80 — which is actually above where the stock started the year ($34.02). Not a terrible outcome, just one where they capped upside in a strong recovery scenario.

Probability: 20% — requires multiple positive catalysts to converge in a 66-day window for a stock down 15.3% YTD that just bounced off $25 lows.

🎯 Base Case (55% probability)

Target: $27–$31 | Premium Decays, Covered Call Expires Worthless

The most likely scenario:

- ✅ Q1 earnings land in-line or modestly above consensus — solid execution but no explosive surprise

- 📊 Stock trades in a choppy $27–$30 range, battling between buyback support below and gamma resistance above

- ⚖️ Revenue growth holds near 20% but any sequential deceleration from Q4's 22% caps the enthusiasm

- 💤 Implied volatility normalizes after earnings (IV crush), reducing remaining option value

- 🎯 Stock closes below $32 on May 15 — covered call expires worthless, seller keeps the entire $1.2M

- 📍 Toast IQ monetization announcement gets delayed or is smaller than expected

Translation: The covered call seller collects their full $1.80 per share — $1.2M total — in 66 days while their underlying stock position sits roughly flat or maybe recovers a couple dollars. That's a 6.2% yield on the underlying position in just over two months. Not bad for doing essentially nothing beyond agreeing not to sell above $32.

Why 55% probability: The base case for a well-performing SaaS company that's already reported strong earnings is "steady as she goes." TOST needs a 10.2% rally from current levels to threaten the strike — the gamma resistance at $29 and $30 makes that a slog even in a benign environment.

📉 Bear Case (25% probability)

Target: $24–$27 | Stock Tanks, Covered Call Premium Partially Offsets Loss

What could go wrong:

- 😰 Q1 2026 revenue misses estimates — Q4 already saw a slight revenue miss despite the EPS beat; any repeat would signal deceleration

- 🇺🇸 U.S. consumer spending softens from tariff-driven inflation pressures — restaurants see traffic declines, GPV growth slows, and Toast's payment revenue gets hit directly

- 💸 Hardware margin deterioration from tariff-driven component cost increases weighs on gross margins

- 🏪 Square/Block launches aggressive restaurant POS pricing to win back SMB market share

- 📉 Broader tech/fintech selloff drags TOST below $28 gamma support, accelerating toward $25 floor

- ⚠️ International expansion (Australia) reveals weaker unit economics than expected — spooks the growth story

For the covered call seller in this scenario: Their underlying shares fall, but the $1.80/share premium collected helps cushion the blow. At $25, the $1.80 doesn't save the day — but it's $1.80 of free money that reduces the effective cost basis. The covered call was essentially free partial downside insurance.

Probability: 25% — macro risks (consumer slowdown, restaurant traffic headwinds) are real and TOST already showed it can trade to $25 earlier this year. Covered call structure protects nothing below $29.03 minus the $1.80 premium, so real downside starts at ~$27.23 net.

💡 Trading Ideas

🛡️ Conservative: Covered Call Copy — Collect Premium While You Wait

Play: Own TOST shares and sell the May 16 $31 or $32 calls to replicate the institutional strategy at smaller scale

Why this works:

- 🎯 You're doing exactly what the smart money just did — collecting premium against a position you already want to hold

- 💰 At current implied volatility of ~55%, May calls offer excellent premium relative to the risk of missing a modest rally

- 📊 The $32 strike is 10.2% above current price — you participate in nearly all of the realistic upside before getting called away

- 🛒 Buyback support at $500M provides a floor mechanism below $28

Specifics:

- 📅 Buy 100 TOST shares at ~$29, sell 1 May 15 $32 call at ~$1.80

- 💸 Net cost basis: $27.20 ($29.00 – $1.80 premium)

- 📈 Max profit: $480 per covered call position if called away at $32 (17.6% return on $27.20 basis)

- 📉 Breakeven: $27.20 — buffer against further downside

- 🎯 Probability of full premium capture: ~70% (stock stays below $32 through May 15)

Risk level: Low-Moderate (own stock + collect premium) | Skill level: Beginner-friendly

Name it: "The Toast & Collect Strategy" — because you're literally collecting premium while Toast does its thing.

⚖️ Balanced: Bull Put Spread — Get Paid to Own TOST at a Discount

Play: Sell a put spread targeting the buyback support zone

Structure: Sell May $27 put / Buy May $25 put

Why this works:

- 💰 Collect credit upfront for expressing a bullish/neutral view — you don't need TOST to go up, just not to crash

- 🛡️ The $500M buyback provides real mechanical support near $27–$28; management proved willing to buy aggressively at $25 earlier this year

- 📊 Analyst consensus remains bullish with 20/20 analysts at Buy and median price targets of $42–$45 — the street thinks we're near floor

- 🎯 Gamma support at $28 and $27 (blue bars from chart) adds technical credence to the support thesis

- ⏰ 66 days to expiration gives the buyback time to work

Estimated P&L:

- 💸 Collect ~$0.60–$0.80 net credit per spread

- 📈 Max profit: $60–$80 per spread if TOST closes above $27 on May 15 (70%+ probability)

- 📉 Max loss: $120–$140 per spread if TOST collapses below $25 (defined and limited)

- 🎯 Breakeven: ~$26.20–$26.40

Entry timing:

- ⏰ Enter now or on any pullback toward $27.50–$28

- ❌ Skip if TOST gaps below $27 before entry — spread is no longer OTM at that point

Position sizing: Risk no more than 3–5% of portfolio on this trade

Risk level: Moderate (defined risk, neutral-to-bullish) | Skill level: Intermediate

🚀 Aggressive: Long $29/$32 Call Spread for the Q1 Earnings Pop

Play: Bet on TOST recovering toward $32 into Q1 earnings

Structure: Buy May $29 call / Sell May $32 call (vertical spread)

Why this could work:

- 📈 2026 EBITDA guidance of $775–$795M implies 22–25% profit growth — if Q1 tracks to that guidance, stock gets re-rated

- 🌍 Any European expansion announcement before May 15 is a TAM-expanding catalyst that the $32 call spread captures

- 🤖 Toast IQ at >50% penetration in 4 months — monetization announcement could be the catalyst that drives the stock from $29 back toward $32

- 🐋 The covered call seller creating 6,500 contracts of OI at $32 paradoxically creates a target zone — dealers now long gamma at $32 will be hedging in a way that can create price pinning dynamics into expiry

- 💸 You're paying for the spread the institutional seller is collecting — their premium becomes your cost, their ceiling becomes your target

Estimated P&L:

- 💸 Cost: ~$0.90–$1.10 net debit per spread ($90–$110 per contract)

- 📈 Max profit: $200 per spread if TOST closes above $32 at May 15 expiration (roughly 1.8–2.2x return)

- 📉 Max loss: Full debit paid (~$90–$110 per spread) — manageable if sized correctly

- 🎯 Breakeven: ~$29.90–$30.10

CRITICAL: Why this is AGGRESSIVE (and why it might not work):

- ⚠️ TOST needs to rally 10.2% from current levels for full profit — that's not a layup

- 📊 The exact $32 strike is NOW a massive wall of call gamma thanks to today's trade

- 💸 With 55% implied volatility, spreads are expensive relative to the probability of success

- ⏰ Q1 earnings create binary event risk — the spread could lose 60–70% on a bad print

Probability of full profit: ~20–25% | Risk level: High | Skill level: Advanced only

⚠️ Risk Factors

Don't get caught by these:

-

🍽️ Restaurant macro is the hidden risk: Toast's payment revenue moves directly with restaurant transaction volume. U.S. consumer spending pressure from tariff-driven inflation could reduce restaurant traffic and GPV growth — hitting Toast's largest revenue line. This is a risk that doesn't show up until it does.

-

📊 Revenue deceleration concern: Q4 2025 revenue actually missed the analyst estimate slightly even as EPS beat by 33%. The market rewarded TOST's first profit, but if Q1 shows a similar pattern (EPS fine, revenue decelerating), the reaction could be negative. Revenue growth is the primary valuation driver at a 9–10x gross profit multiple.

-

💻 Square / Block competitive pressure: Square has been sharpening its restaurant POS features. In the SMB segment where margins are thinner and switching costs are lower, any aggressive competitive move from Square could increase TOST's churn and slow net location adds.

-

🌍 International execution is unproven: The Australia launch is Toast's first real international foray. If unit economics abroad are worse than the U.S. core business (different payment rails, regulatory complexity, hardware logistics), international could become a margin drag rather than a growth driver.

-

🔒 Covered call ceiling is real: The 6,500 contracts at $32 now represent a structural gamma wall. Between dealer hedging and the seller's own share assignment threshold, $32 is a genuine near-term ceiling with 66 days of institutional weight behind it. Bulls face a tougher path above $32 until this expiry clears.

-

📉 Stock already down 15.3% YTD: Distribution has been going on since January 1. The recovery from $25 to $29 looks like a relief rally more than a trend reversal. The YTD chart shows lower highs — until that pattern breaks, longer-dated directional longs should be cautious.

-

🎢 55% annualized volatility means big swings: TOST can move $1.50–$2 in a single session on no fundamental news. Stop-loss placement and position sizing must account for intraday noise. The weekly implied move of ±3.96% means you can be right about direction and still get stopped out.

-

💰 Stock-based compensation dilution: Toast historically runs high SBC as a percentage of revenue. As GAAP profitability improves, tracking diluted share count is important — shareholder dilution from SBC could quietly erode per-share gains even in a strong revenue environment.

🎯 The Bottom Line

Here's the deal: A large TOST holder just collected $1.2 million by selling calls against their position — telling the market "I don't think this stock is going past $32 before May 15." They sold 6,500 contracts against just 202 existing open interest (32x!), built the entire OI at this strike themselves, and chose the May expiry that captures Q1 2026 earnings.

What this trade tells us:

- 🧠 Sophisticated, not scared: This is income generation, not a panic hedge. A scared holder would buy puts. This holder is confident enough in their position to stay long — they just want to harvest premium at the current price level

- 🎯 $32 is the ceiling they believe in: They're not selling $35 calls or $40 calls. They specifically chose $32 — the level that was January 2026 support that became resistance. That's a very specific, chart-aware conviction

- ⏰ May 15 captures the Q1 earnings window: They're making a deliberate choice to include the earnings event in this trade. Either they expect a modest reaction (not enough to push TOST 10%+ to $32) or they're comfortable selling their shares at $32 as an exit strategy

- 💰 Effective sale price if called away: $32 strike + $1.80 premium = $33.80 net — which is actually close to where the stock started 2026 ($34.02). They may be engineering an exit near year-start levels while collecting income while they wait

If you own TOST:

- ✅ Consider the covered call strategy yourself — at 55% IV, May options offer excellent premium. The $32 covered call is now liquid (6,500 contracts of new OI just appeared)

- 📊 Watch for Q1 earnings in May as the critical decision point — specifically look for revenue growth direction (accelerating vs. decelerating from Q4's 22%)

- 🛡️ The $500M buyback provides a real floor — use $27–$28 as your mental support level for existing positions

- 🎯 If TOST clears $30 with volume on an up day, that's a sign the $32 wall might get tested

If you're watching from the sidelines:

- ⏰ The next major catalyst is Q1 earnings in May — resist the urge to chase the stock into that event without a defined risk framework

- 🎯 A pullback to $27–$28 (gamma support zone) would represent an attractive entry with the buyback providing downside cushion

- 📈 Analyst median price target of $42–$45 implies 45–55% upside from current levels — the long-term story remains intact if execution holds

If you're bearish:

- 📉 The stock is in a downtrend (lower highs since January), and the covered call seller's implicit bearish-to-neutral view on near-term catalysts deserves respect

- 📊 Break below $28 gamma support triggers accelerated selling pressure toward $25–$26

- ⚠️ But fighting the $500M buyback and 20/20 analyst Buy consensus is a tough trade — be careful shorting outright; use defined risk structures if you want downside exposure

Mark your calendar:

- 📅 March 13 — Weekly expiration; implied range $27.75–$30.03

- 📅 March (3rd Friday) — Monthly OPEX; gamma resets

- 📅 May 2026 — Q1 2026 earnings (exact date TBD; catalyst inside the May 15 expiry window)

- 📅 May 15, 2026 — Expiration of the 6,500-contract $32 covered call position

Final verdict: Toast's fundamentals — first GAAP profit, $2B ARR, enterprise wins at Applebee's and Papa Murphy's, and expanding into international markets — are genuinely compelling for the long term. But the smart money just planted a $32 ceiling with $1.2M of conviction, and at -15.3% YTD with 55% volatility and earnings approaching, the near-term path is anything but straight. Respect the ceiling, respect the support, and respect your position size. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance does not guarantee future results. The Z-score of 254.38 reflects this trade's size relative to recent TOST options history — it does not imply the trade will be profitable or that retail traders should replicate it. Covered call writing involves forfeiting upside above the strike price and does not protect against significant downside in the underlying stock. Earnings events create binary risk with potential for sharp moves in either direction. Always conduct your own research and consider consulting a licensed financial advisor before making any investment decisions. The covered call seller referenced in this analysis may have portfolio hedging, tax, or risk management needs that are not applicable to retail traders.

About Toast Inc.: Toast is a cloud-based restaurant technology platform providing point-of-sale hardware, software subscriptions, payment processing, payroll, and analytics services purpose-built for the restaurant industry. With 164,000 locations on the platform and $51.5 billion in Gross Payment Volume, Toast operates a fintech-embedded SaaS model with a market cap of approximately $15 billion on the NYSE.