💎 ALB Massive $8.4M + $2.2M Call Selling Spree - Institution Capping Lithium Rally! 🔥

📅 December 1, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just DUMPED $10.6 MILLION in ALB calls this morning at 10:29:16! Two massive blocks totaling 13,200 contracts ($120 and $140 strikes, December 19th expiration) hit the tape simultaneously in what appears to be a sophisticated covered call strategy. With ALB at $127.85 and lithium markets at an inflection point ahead of February 18th earnings, smart money is monetizing volatility and capping upside at peak prices. Translation: Institutions are collecting premium while betting ALB stays range-bound through year-end!

📊 Company Overview

Albemarle Corporation (ALB) is the world's largest lithium producer, positioned at the epicenter of the electric vehicle and energy storage revolution:

- Market Cap: $15.3 Billion

- Industry: Chemicals & Materials (Lithium & Bromine Production)

- Current Price: $127.85

- Primary Business: Integrated lithium manufacturing (mining, refining, conversion) supplying EV batteries; global leader in bromine-based flame retardants

- Key Operations: Chile salt brine reserves, Australia hard rock mining JV, refining facilities across Chile, US, Australia, and China

Albemarle's catalyst report highlights the company navigating a turbulent lithium oversupply environment through aggressive cost restructuring ($450M achieved) while positioning for the projected 30% YoY demand surge driven by EV and energy storage growth.

💰 The Option Flow Breakdown

The Tape (December 1, 2025 @ 10:29:16):

| Time | Symbol | Buy/Sell | Type | Expiration | Strike | Volume | Premium | Order Type | Strategy | Z-Score | Vol/OI Ratio | Strategy Type |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:29:16 | ALB | SELL | CALL | 2025-12-19 | $120 | 6,600 | $8.4M | STO | UNCLASSIFIED | 7.15 (Extremely Unusual) | 0.93 | STANDALONE |

| 10:29:16 | ALB | SELL | CALL | 2025-12-19 | $140 | 6,600 | $2.2M | STO | UNCLASSIFIED | 232.19 (Extremely Unusual) | 22.92 | STANDALONE |

🤓 What This Actually Means

Note: Our automated strategy detection classifies these as UNCLASSIFIED/STANDALONE trades, indicating the algorithm couldn't definitively identify the structure. However, based on the characteristics below, this appears to be a premium collection strategy - likely covered calls on a MASSIVE long stock position! Here's the breakdown:

- 💸 Total premium collected: $10.6M ($8.4M + $2.2M)

- 📊 Massive size: 13,200 contracts represents 1.32 million shares worth ~$169M

- 🎯 Strategic strikes: $120 just 6% OTM (high probability assignment), $140 at 9.4% OTM (lower probability but higher premium/share)

- ⏰ Timing is everything: 18 days to December 19th expiration captures year-end positioning but expires BEFORE critical Q4/FY2025 earnings on February 18, 2026

- 🛡️ Smart hedging: Trader likely holds 1.32M shares (possibly from earlier accumulation during the year's bottom at $49.43 in April) and is now monetizing the +114% rally

What's really happening here:

This institution accumulated [ALB shares during the brutal lithium downturn](https://stockanalysis.com/stocks/alb/) when the stock hit multi-year lows in April 2025. Now, with ALB up 114% YTD at $127.85 and lithium prices recovering but still volatile, they're writing covered calls to:

- Generate $10.6M in immediate income (8.0% yield on the $133M position if we assume avg basis ~$100)

- Cap upside at $120-$140 through year-end (they're okay getting called away if ALB rallies another 5-10%)

- Reduce effective cost basis by $8.03/share ($10.6M ÷ 1.32M shares)

- Position for potential re-entry post-December expiration if shares get called away

Unusual Score: 🔥 EXTREMELY UNUSUAL - The $140 strike shows Z-score of 232.19 (literally off the charts - happens maybe once or twice a year!). The $120 strike at 7.15 Z-score is also highly unusual. Combined, this is one of the largest single-day covered call programs in ALB's recent history.

Translation: This isn't bearish - it's sophisticated income generation by someone who's already made HUGE money on the lithium recovery and wants to lock in gains while keeping upside optionality if lithium really takes off. The simultaneous execution at 10:29:16 suggests algorithmic institutional order, not retail.

📈 Technical Setup / Chart Check-Up

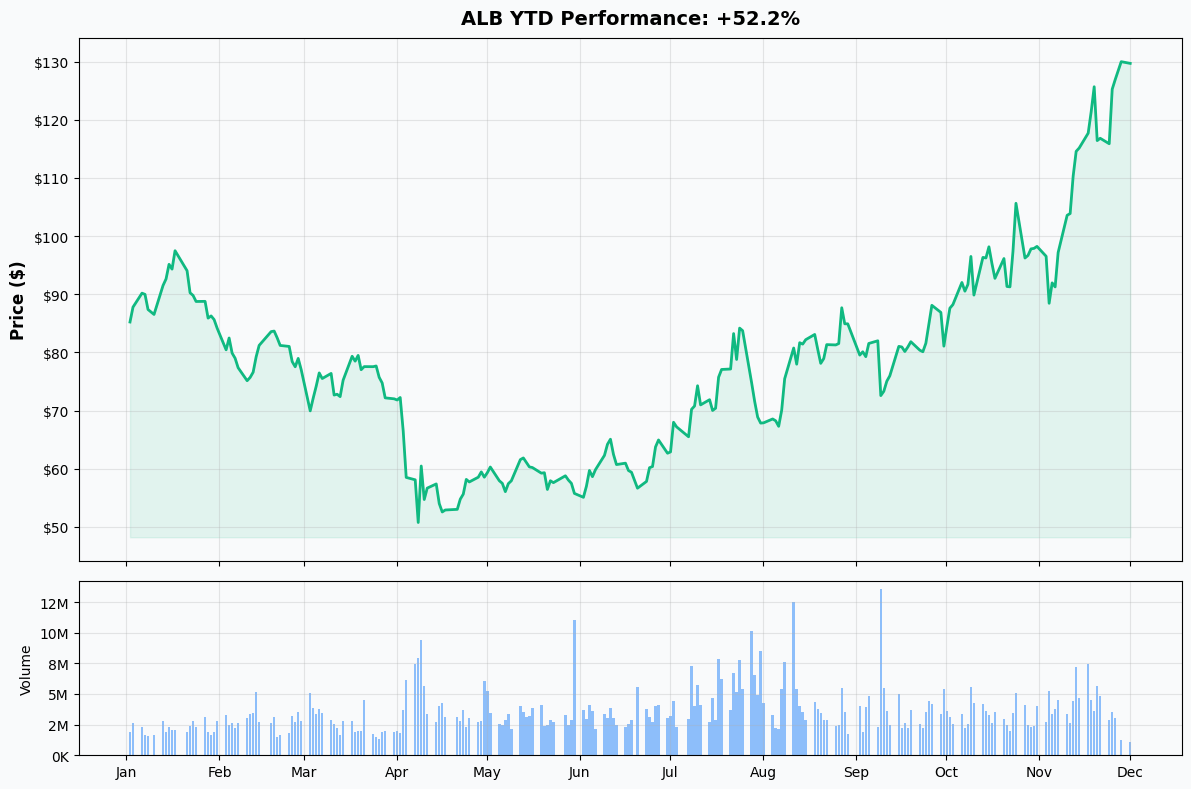

YTD Performance Chart

Albemarle has delivered an impressive recovery - up +114% YTD with current price of $127.85 (started the year around $59). The chart tells a remarkable turnaround story from the April 8th bottom at $49.43 during peak lithium pessimism.

Key observations:

- 🚀 Epic recovery: Surged 159% from April lows at $49.43 to near $128, driven by lithium market stabilization and cost restructuring

- 📊 Recent momentum: 36% surge from mid-year lows as lithium fundamentals improved

- 📈 Breakout confirmed: Shattered through $100 resistance in October/November on improving lithium pricing and analyst upgrades

- 🎢 High volatility play: Beta of 2.05 means ALB moves 2x the market - not for the faint of heart

- ⚠️ Near 52-week highs: Trading just below peak levels with limited overhead resistance but also less margin of safety

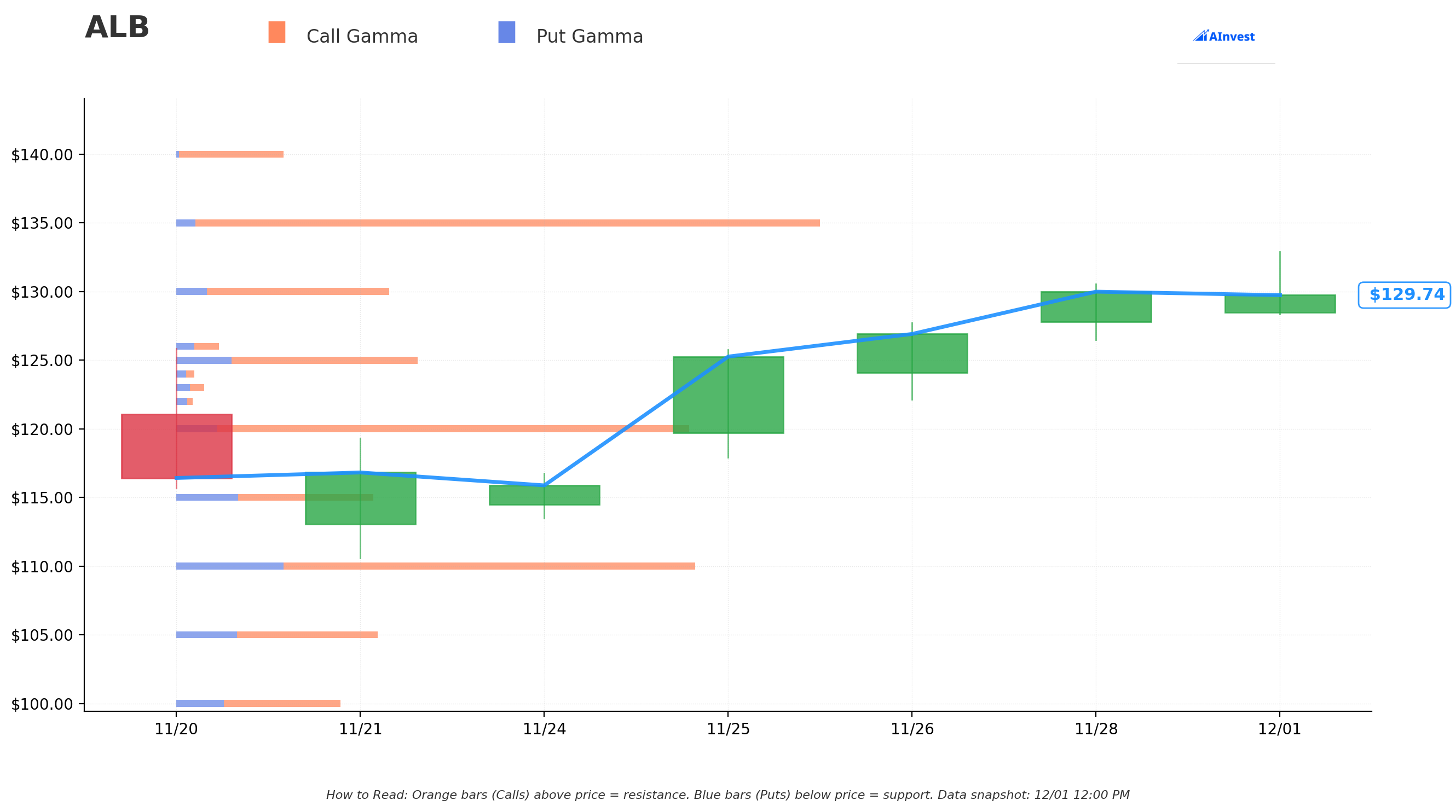

Gamma-Based Support & Resistance Analysis

Current Price: $127.85

Critical Insight: The gamma exposure data shows NO significant gamma levels for ALB currently. This is actually VERY telling:

What this means for traders:

- 🎯 Low options activity: Limited dealer positioning suggests institutional players aren't heavily active in ALB options compared to mega-cap tech names

- 📊 Price freedom: Without major gamma walls, ALB can move more freely based on fundamental catalysts rather than technical dealer hedging

- ⚠️ Higher volatility potential: Absence of gamma support/resistance means less cushioning during moves - gaps more likely

- 🤔 Follow the tape: With minimal gamma reference points, today's massive $10.6M covered call sale becomes EVEN MORE significant as a rare institutional signal

The $120 and $140 strikes from today's trades will NOW create future gamma reference points as market makers hedge these positions, potentially creating new technical levels.

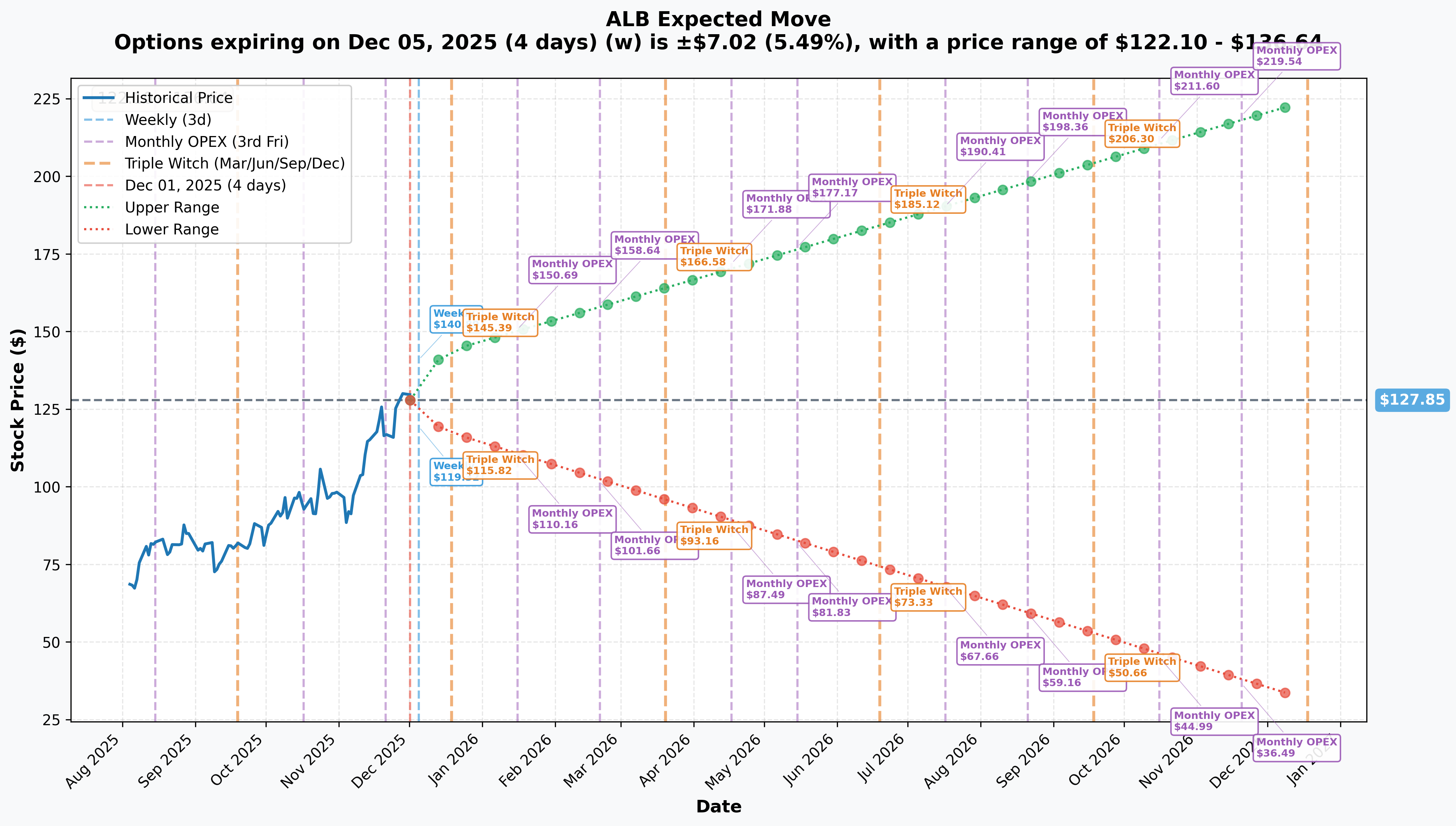

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 4 days): ±$7.02 (±5.49%) → Range: $122.10 - $136.64

- 📅 Monthly OPEX (Dec 19 - 18 days - THIS TRADE!): ±$12.47 (±9.76%) → Range: $117.24 - $144.07

- 📅 January OPEX (Jan 16 - 46 days): ±$16.98 (±13.28%) → Range: $110.87 - $144.83

- 📅 February OPEX (Feb 20 - 81 days): ±$24.09 (±18.84%) → Range: $103.76 - $151.94

Translation for regular folks:

Options traders are pricing in a 5.5% move ($7) by this Friday's weekly expiration, but a more substantial 9.8% move ($12.50) through December 19th monthly OPEX (when these calls expire). The market expects moderate volatility - not as dramatic as high-beta tech names, but meaningful moves for a materials/chemical stock.

Key insight: The December 19th implied move of ±9.76% means:

- Upper range of $144.07 is ABOVE the $140 call strike (85% probability assigned, 15% chance of breach)

- Lower range of $117.24 is BELOW the $120 call strike by $2.76 (stock could trade down 8% and both calls expire worthless)

The call seller is betting ALB stays within the $117-$144 implied volatility cone through December 19th, maximizing premium collection without assignment risk at $120 (and very low risk at $140).

Notice the sharp jump to 18.84% implied move by February 20th expiration? That's the market pricing in Q4/FY2025 earnings volatility scheduled for February 18, 2026. The covered call seller DELIBERATELY chose December 19th expiration to collect premium while avoiding earnings binary risk!

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Ex-Dividend Date - December 12, 2025 (11 DAYS!) 💰

Albemarle's quarterly dividend of $0.405 per share goes ex-dividend on December 12, 2025 (11 days away):

- 💵 Quarterly Payment: $0.405/share ($1.62 annual dividend)

- 📊 Current Yield: 1.28% ($1.62 annual ÷ $125.26 price)

- ⚠️ Sustainability Question: Payout ratio at -119.56% (paying dividend despite losses) raises concerns about potential cut

- 🎯 Strategic Significance: Management maintaining dividend signals confidence in cash generation and lithium recovery thesis

- 📅 Payment Date: Following ex-date (typically 2-3 weeks later)

Why this matters for the covered call trade: Stock typically experiences minor downward pressure after ex-dividend date as dividend buyers exit. The call seller positioned AFTER this date, avoiding the technical headwind.

🚀 Near-Term Catalysts (Q4 2025 - Q1 2026)

December 19th Options Expiration - THESE CALLS EXPIRE! ⏰

The $10.6M covered call position expires in 18 days on December 19th:

Outcome scenarios:

- 📈 ALB above $120 at expiration: $120 calls assigned, seller delivers 660,000 shares at $120 (realizes ~$8M gain if avg cost was ~$100, PLUS keeps $8.4M premium = ~$16.4M total)

- 🚀 ALB above $140 at expiration: Both strikes assigned, all 1.32M shares called away at blended $130 avg (realizes gains + keeps full $10.6M premium)

- 📊 ALB between $120-$140: Partial assignment likely on $120 calls (seller keeps shares + premium), $140 calls expire worthless (seller keeps premium + shares)

- 📉 ALB below $120: All calls expire worthless, seller keeps full $10.6M premium AND all shares, can write new calls for January

This becomes a KEY technical level to watch - if ALB approaches $120, the 6,600 contracts worth of dealer short hedges may need to be covered, creating buying pressure. Conversely, if ALB surges toward $140, dealers will sell stock to hedge, creating resistance.

Year-End Positioning & Tax Loss Harvesting (December 2025) 📅

As calendar year-end approaches, institutional positioning dynamics could impact ALB:

- 📊 Window dressing: Fund managers may adjust holdings for year-end reporting (could support or pressure price)

- 💰 Tax considerations: Some investors may realize gains after 114% YTD return to manage tax bills

- 🔄 Rebalancing flows: ALB's massive rally may trigger mechanical selling by momentum/value funds

- 📈 January effect setup: Post-tax selling often creates Q1 buying opportunities

The covered call seller may be positioning for year-end volatility while capturing premium decay through holiday thin trading.

📊 Major Upcoming Catalyst (Q1 2026)

Q4 2025/Full Year Earnings Release - February 18, 2026 📊

Albemarle reports fiscal Q4 and full-year 2025 results on February 18, 2026 after market close - this is THE catalyst that will determine ALB's 2026 trajectory:

Wall Street consensus expectations:

- 📊 FY 2025 Revenue: $4.9-5.2B guidance range (down from $6.7B in 2024 due to lithium pricing)

- 💰 FY 2025 EPS: Loss of ($2.07) expected, an 11.5% improvement from prior year losses

- 🤖 Adjusted EBITDA: $0.8-1.0B range (down from $1.7B in 2024 but improving sequentially)

- 💸 Free Cash Flow: $300-400M anticipated (critical metric showing cash generation despite accounting losses)

- 🏭 CapEx: $600M (65% reduction from $1.7B in 2024, showing capital discipline)

Key metrics Wall Street will focus on:

- 📈 Energy Storage volume: Segment showed +8% growth in Q3 - continuation critical

- 💪 Cost savings sustainability: Whether $450M annual run-rate improvements maintained

- 🌍 Lithium pricing realization: Gap between spot prices ($8,500-9,600/mt range) and contract pricing

- 🎯 2026 Guidance: Revenue growth expectations as lithium market recovers

- 🔄 Ketjen transaction update: $660M cash proceeds from 50% stake sale timing and capital allocation plans

Why covered call seller avoided earnings:

By expiring December 19th, the call seller collects premium through year-end volatility but exits before the February earnings binary event. This is sophisticated risk management - they can reassess positioning in January based on lithium price trends and industry dynamics before deciding whether to write new calls or stay long uncovered into earnings.

Greenbushes Mine Expansion (Australia) - Q4 2025/Q1 2026 🏭

First ore processing expected in Q4 2025 from the Greenbushes expansion (joint venture with Tianqi Lithium at the world's largest hard rock lithium mine):

- 📊 Production impact: Significant volume contribution to 2026 production

- 💰 Revenue catalyst: Expanded capacity hits market as demand accelerates

- 🎯 Cost advantage: Low-cost hard rock source improves margin profile

- ⏰ Timing uncertainty: Any delays would disappoint given capital invested

- 🌍 Strategic importance: Secures supply for conversion facilities globally

Meishan Lithium Conversion Facility (China) - Ramping Now 🇨🇳

Ramp-up progressing ahead of schedule at Albemarle's Chinese conversion facility:

- 🎯 Market access: Positions ALB in Asian battery supply chain (China = 51.6% EV penetration in 2025)

- 💪 Low-cost production: China-based conversion leverages local infrastructure

- 📈 Volume growth: Enhanced capacity meets surging regional demand

- ⚠️ Geopolitical risk: U.S.-China tensions could complicate operations

Salar Yield Improvement Project (Chile) - H1 2026 Full Ramp 🇨🇱

Currently at 50% operating rate, full ramp-up expected through H1 2026:

- 💰 Revenue potential: Increases low-cost Chilean brine production

- 🌍 Strategic asset: Atacama Salar = world-class lithium brine resource

- ⏰ H1 2026 timeline: Should contribute meaningfully by mid-year

- 📊 Margin accretive: Brine extraction cheaper than hard rock mining

🌍 Market Dynamics (2025-2026)

Lithium Market Inflection Point - The Big Picture ⚡

The lithium market is at a critical crossroads, and Albemarle's positioning could not be more strategic:

Supply-Demand Rebalancing:

- 📊 2025 Oversupply: Market facing estimated 120,000-ton LCE surplus as Chinese producers flooded market

- 🔄 Supply Discipline Emerging: Chinese mines reducing or halting production due to losses at current prices

- 🚀 Demand Acceleration: Global lithium demand forecasted to reach 1.8M tonnes LCE in 2025, doubling to 3.7M tonnes by 2030

- 📈 2026 Inflection: Market expected to shift from surplus to marginal deficit by 2026

Lithium Pricing Recovery:

- 💎 Current Range: Battery-grade lithium carbonate trading $8,500-9,600/mt as of November 2025

- 📊 Recovery from Bottom: Prices rallied from four-year low of $8,300/mt in June to 11-month high of $12,067/mt in August

- 🎯 2025 Forecast: Analysts project $9,000-12,000/tonne range throughout 2025

- 🚀 Long-term Outlook: Deutsche Bank forecasts rebound by 2026-2027 driven by 15-20% annual demand growth

EV Demand Drivers:

- 🚗 Global EV Sales: Projected to exceed 20M units in 2025 (+17% growth), climbing to 22.1M with 24% market share

- 🇨🇳 China Leadership: 5.85M NEVs sold in H1 2025 (+33% YoY), 51.6% of light-vehicle sales

- ⚡ Energy Storage Boom: Grid battery demand surged 105% YTD 2025

- 📱 Battery Demand: Forecast to surpass 1 TWh in 2025, doubling to 2.3 TWh by 2030

Why This Matters for the Covered Call Trade:

The call seller is betting that lithium's recovery will be gradual, not explosive through December 19th. They're positioning for ALB to consolidate in the $110-140 range as the market digests:

- Q4 lithium pricing stabilization (not spectacular)

- Year-end institutional profit-taking after 114% YTD gain

- Uncertainty around 2026 demand acceleration timing

If lithium prices SPIKE unexpectedly (major supply disruption, faster-than-expected EV adoption), ALB could breach $140 and they lose upside beyond that level. But they've calculated this is low probability over the next 18 days.

Analyst Sentiment - Recent Upgrades Wave 📊

Multiple analysts raised price targets in November 2025 following Q3 earnings beat and improving lithium fundamentals:

- 🎯 BMO Capital: Raised PT to $136, citing increased Chinese lithium demand

- 🎯 Argus Research: Boosted PT to $140 from $120, 17% premium citing balance sheet strength

- 🎯 RBC Capital: Increased PT to $117 from $80 on CATL mine halt improving supply/demand

- 🎯 Wells Fargo: Lifted PT to $100 from $90 on healthy cash flow potential

- 🎯 Mizuho: Raised PT to $110 from $92

- 🎯 Evercore ISI: Increased PT to $100 from $88

- 🎯 Baird: Raised PT to $81 from $68

Consensus:

- 📊 Average Price Target: $104.27 (range: $58-$200)

- 📊 Rating Distribution: 6 Buy, 10 Hold, 2 Sell among 18 analysts

- 📊 Consensus Rating: Hold

The $120-$140 call strikes align almost perfectly with the analyst target range! The seller positioned right at consensus fair value, suggesting they view current levels as fairly valued with limited near-term upside potential.

⚠️ Risk Catalysts (Negative)

Lithium Oversupply Overhang 💎

Despite recent price recovery, structural oversupply remains the primary headwind:

- 📊 2025 Surplus: 120,000-ton LCE oversupply as aggressive production expansions continue

- 📉 Price Collapse History: Lithium prices fell 85% from $80,000/ton peak in 2022 to below $12,000/ton

- 🏭 Production Growth: Mine output climbed 192% since 2020 (82,000 to 240,000 metric tons)

- 🇨🇳 Chinese Competition: Battery manufacturers (CATL, LG Energy) destocking inventory

Contract Renegotiation Risk (2026) 📝

As 2026 approaches, Albemarle's long-term contracts may face downward pressure:

- ⚠️ Pricing floors at risk: Fixed-price contracts may be renegotiated lower

- 📊 Volume commitment uncertainty: Customers could reduce offtake in oversupplied market

- 💰 Margin compression: Shift from contract pricing to spot exposure

- ⏰ 2026 timeline: Contracts rolling over throughout the year

Financial Vulnerability Concerns 💰

Despite cost cutting success, financial metrics show stress:

- 🚨 Altman Z-Score: 1.41 - Places company in "distress zone" indicating heightened insolvency risk within two years

- 📉 Negative Earnings: FY 2025 EPS loss of ($2.07) expected

- 💸 Dividend Sustainability: -119.56% payout ratio (paying dividend despite losses) raises cut risk

- 📊 Debt Load: $3.6B total debt with net debt/EBITDA of 2.1x

Chinese Competition Intensifying 🇨🇳

- 🏭 Chinese producers rapidly expanding capacity with government support

- 💰 Some competitors operating at losses to maintain market share

- 🌍 China accounts for over 60% of global EV production

- ⚖️ Cost disadvantage for non-Chinese producers on conversion

Geopolitical & Macro Risks 🌍

- 🇨🇳 U.S.-China Tensions: Critical minerals trade restrictions could disrupt supply chains

- 📉 EV Demand Uncertainty: Slower adoption in key markets (U.S. subsidy changes, European weakness)

- 💼 Recession Risk: Global economic slowdown would dampen automotive production

- 🔬 Battery Technology Shifts: Emerging chemistries (sodium-ion, solid-state) could reduce lithium intensity

🎲 Price Targets & Probabilities

Using implied move data, analyst targets, and upcoming catalysts, here are the scenarios through December 19th expiration:

📈 Bull Case (20% probability)

Target: $140-$150

How we get there:

- 💎 Lithium price spike: Unexpected supply disruption (major mine accident, geopolitical event) pushes spot prices toward $15,000/mt

- 🚗 EV demand surprise: December China/Europe sales data shows acceleration beyond expectations

- 💰 Ketjen transaction closes early: $660M cash proceeds hit balance sheet, reducing debt concerns

- 📊 Analyst upgrade wave: More firms raise targets following year-end positioning strength

- 🏭 Greenbushes early production: Ahead-of-schedule ramp announced

- 📈 Technical breakout: Break above $130 triggers momentum buying toward $140-145

Key metrics needed:

- Lithium carbonate sustained above $11,000/mt

- EV sales data showing >20% YoY growth

- Competitor mine closures accelerating supply discipline

Probability assessment: Only 20% because it requires multiple positive surprises in a compressed 18-day window. The analyst consensus of $104 suggests limited near-term upside. Year-end profit-taking pressures stocks that rallied 114% YTD.

Call seller outcome: OUCH! Both strikes get assigned, stock delivered at $120 and $140 (blended $130 avg). If stock reaches $145, they miss $15/share on 1.32M shares = $19.8M opportunity cost. But they still keep the $10.6M premium collected, softening the blow. Net result: Good outcome but left money on table.

🎯 Base Case (60% probability)

Target: $115-$135 range (CHOP CITY)

Most likely scenario:

- 📊 Sideways consolidation: ALB digests massive YTD gains, trading in a range

- 💎 Lithium prices stable: Range-bound $8,500-10,500/mt without major moves

- 📅 Year-end dynamics: Tax selling pressure offset by window dressing, net neutral

- 🎄 Holiday thin trading: Low volume December leads to rangebound action

- ⏰ Pre-earnings pause: Investors wait for February 18th catalyst before major positioning

- 📉 Ex-dividend adjustment: Minor dip around December 12th ex-date

- 🔄 Mean reversion: After 114% rally, natural consolidation period

Price action within implied move:

- Trades between $117 (lower implied range) and $136 (upper implied range)

- Occasional tests of $120 support create tension but holds

- Fails to sustain breakout above $135 resistance

- Volatility compression as year-end approaches

Call seller outcome: PERFECT! Both strikes expire out-of-the-money. Seller keeps:

- Full $10.6M premium collected = 8.0% return in 18 days

- All 1.32M shares for potential upside into 2026

- Option to write new covered calls in January at higher strikes if bullish

This is exactly what the trade is designed for. The seller gets paid handsomely for taking limited upside risk during a low-catalyst period. Can reassess in January based on lithium trends and write February or March calls.

Why 60% probability: Year-end typically sees consolidation after big rallies. No major near-term catalysts before February earnings. Lithium market in transition (not crashing, not exploding). Analyst consensus at $104 implies fair value near current levels.

📉 Bear Case (20% probability)

Target: $105-$115 (TEST IMPLIED SUPPORT)

What could go wrong:

- 😰 Lithium price relapse: Spot prices fall back toward $7,500-8,000/mt on renewed oversupply fears

- 🇨🇳 Chinese inventory overhang: Major battery makers announce further destocking plans

- 📉 EV demand disappointment: December sales data shows slowdown, 2026 outlook cloudy

- 💸 Dividend cut speculation: Financial media highlights unsustainable -119.56% payout ratio

- 🔨 Profit-taking cascade: After 114% YTD gain, institutional selling accelerates

- 📊 Competitor news: SQM or Ganfeng announces aggressive capacity expansion

- 🌍 Macro concerns: Recession fears resurface, cyclical stocks sold off

Support levels:

- 🛡️ $120: Major technical support + covered call strike (buyer interest likely)

- 🛡️ $117: Lower end of December implied move range

- 🛡️ $110: Psychological round number + 50-day moving average

- 🛡️ $105: Deeper support from October consolidation

Call seller outcome: EVEN BETTER! Stock pulls back to $110-115 range:

- All calls expire worthless (zero assignment risk)

- Keeps full $10.6M premium

- Unrealized loss on stock position of $13-18/share = $17-24M paper loss on 1.32M shares

- BUT: Effective cost basis now reduced by $8.03/share from premium collected

- Net position still profitable if original avg cost was $85-100 (April-June accumulation)

- Can write new covered calls at lower strikes ($115 or $120) for January, collecting more premium

Why 20% probability: Requires deterioration in lithium fundamentals or broad market selloff. Company's $450M cost savings and improving operational metrics provide fundamental support. Recent analyst upgrades to $104-140 targets suggest limited downside. Year-end is typically constructive for quality names.

💡 Trading Ideas

🛡️ Conservative: Sell Cash-Secured Puts (Copy Smart Money)

Play: Sell cash-secured puts on ALB at $115-$120 strikes (December or January expiration) to get paid while waiting for pullback entry

Why this works:

- 💰 Get paid to wait: Collect premium ($3-5/contract) while waiting for potential dip

- 🎯 Entry at discount: If assigned, effective cost basis $111-117 (strike minus premium)

- 📊 Downside buffer: Entering 10-13% below current price provides margin of safety

- 🛡️ Aligns with implied move: $115-120 strikes within December implied range of $117.24 - $144.07

- 📈 2026 upside: Positioned for lithium recovery into next year

- 💪 Strong fundamentals: $450M cost savings achieved, capacity expansions ramping

Structure:

- Sell Dec 19 $120 puts at ~$4.50 credit OR Jan 16 $115 puts at ~$3.50 credit

- Capital requirement: $12,000 per contract (must have cash to buy 100 shares at $120)

- Max profit: Premium collected if ALB stays above strike

- Effective entry: $115.50 or $111.50 if assigned

Estimated P&L:

- 📈 ALB stays above $120 (Dec) or $115 (Jan): Keep full premium = 3.75-3.9% return in 18-46 days

- 📉 ALB below strike at expiration: Assigned stock at strike price minus premium collected

- 🎯 Breakeven: $115.50 (Dec) or $111.50 (Jan) - both BELOW lower implied range of $117.24

Action plan:

- ⏰ Enter this week (higher IV = better premium)

- 📊 Choose December for shorter duration, January for more premium but longer risk exposure

- 🎯 Only sell puts on amount of stock you actually WANT to own

- ✅ Must have full cash secured ($12,000 per put or $11,500 per put)

Risk level: Low-Moderate (defined risk, require cash backing) | Skill level: Beginner-friendly

Expected outcome: Solid probability (70%+) of keeping premium without assignment given $115-120 strikes below current price and analyst support. If assigned, getting ALB at $111-116 effective cost = excellent entry for 2026 lithium recovery.

⚖️ Balanced: Bull Put Spread (Limited Risk Income)

Play: Sell bull put spread targeting December consolidation range

Structure: Sell $120 puts / Buy $115 puts (December 19 expiration - SAME as covered call trade)

Why this works:

- 📊 Defined risk: Max loss = $500 (spread width minus credit), Max gain = credit received

- 💰 Attractive premium: Collect ~$2.00-2.50 net credit per spread

- 🎯 Wide buffer: Stock can drop to $120 (6.2% decline) before reaching breakeven

- 🛡️ Psychological support: $120 is both call strike AND round number (strong technical level)

- ⏰ Time decay advantage: 18 days for theta to work in your favor

- 📈 Aligns with base case: Benefits from sideways/up action through year-end

Estimated P&L:

- 💰 Collect: ~$2.25 credit per spread ($225 per)

- 📈 Max profit: $225 if ALB above $120 at December 19 expiration (45% ROI)

- 📉 Max loss: $275 if ALB below $115 at expiration (55% risk)

- 🎯 Breakeven: $117.75 (within implied range of $117.24 - $144.07)

Position sizing: Risk only 3-5% of portfolio (2-5 spreads for $50K account)

Entry timing:

- ✅ Enter immediately: Current IV around 45-50% provides good premium

- 🎯 Target credit: Don't chase - if can't get $2.00+ credit, pass

Risk management:

- 🚨 Close at 50% profit: If spread drops to $1.10, take profits early

- ⚠️ Roll if threatened: If ALB approaches $120, consider rolling to January at lower strikes

- 💀 Exit at 2x loss: If spread doubles to $4.50, cut loss (ALB broke badly, thesis invalid)

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

Probability of profit: ~65-70% based on $120 support holding, year-end dynamics, and analyst support at $104-140 range.

🚀 Aggressive: Long Call Calendar Spread (Volatility Play - ADVANCED!)

Play: Bet on year-end consolidation (low volatility) followed by February earnings volatility spike

Structure:

- Sell: December 19th $130 calls (these will decay quickly)

- Buy: February 20th $130 calls (hold into earnings on Feb 18)

Why this could work:

- 📊 Capture calendar effect: December IV collapse (year-end low volatility) while February IV stays elevated (pre-earnings)

- 💎 Neutral price assumption: Bet that ALB stays near $130 through December (near ATM for max time decay on short calls)

- 📈 Volatility expansion: February implied move at 18.84% vs December at 9.76% - you profit from this IV differential

- ⏰ Earnings catalyst: February 18th earnings DURING February expiration cycle creates vol explosion

- 🎯 Risk defined: Max loss = net debit paid if ALB moves far away from $130 in either direction

Why this could blow up (SERIOUS RISKS):

- 💸 Complex execution: Must understand how calendar spreads work and Greeks dynamics

- 📉 Early move kills spread: If ALB moves to $115 or $145 in December, both legs lose value

- ⚡ December assignment risk: Short December calls could get assigned early if ALB surges, leaving naked long February call

- 🎢 Vega risk: If overall market volatility collapses, even February calls lose value

- ⏰ Timing critical: Need to close December leg at expiration and manage February position carefully

- 📊 Theta decay both directions: Both legs decay, need IV expansion to overcome time decay

Estimated P&L:

- 💰 Net cost: ~$5-7 debit per spread (pay this upfront)

- 📈 Max profit: $8-12 per spread if ALB at $130 at December expiration, then volatility expands into February

- 📉 Max loss: $5-7 (full debit) if ALB moves far away from $130 quickly

- 🎯 Ideal scenario: ALB trades $125-135 through December, then you close December leg for profit and hold February into earnings run-up

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded calendar spreads before and understand Vega and Theta interactions

- ✅ Can monitor position DAILY and adjust if needed

- ✅ Have margin approval for short options (Level 3 or higher)

- ✅ Understand early assignment risk on short calls

- ✅ Plan to actively manage the trade (not set-and-forget)

- ⏰ Will close December leg at expiration (Dec 19) and reassess February position

Exit plan:

- 🎯 Target profit: 40-60% gain on net debit (spread widens from $6 to $9-10)

- 🚨 December 19: MUST close or roll short leg - don't risk assignment

- ⏰ Post-December: Hold February calls into earnings run-up (Jan 15-Feb 15), sell before earnings announcement to capture IV expansion without binary risk

Risk level: HIGH (complex strategy, multiple moving parts) | Skill level: Advanced only

Probability of profit: ~45% (requires correct price action AND volatility behavior)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💎 Lithium price volatility remains extreme: Despite recovery to $8,500-9,600/mt range, prices collapsed 85% from 2022 peak and remain volatile. Any renewed oversupply concerns (Chinese production restarts, demand disappointment) could send prices crashing again. Albemarle's revenue is HIGHLY sensitive to spot pricing despite long-term contracts - 192% increase in global mine output since 2020 creates persistent oversupply risk through 2025.

-

📊 Altman Z-Score of 1.41 signals financial distress risk: Company's Z-score places it in "distress zone" indicating elevated insolvency probability within two years. While liquidity of $3.5B including $1.9B cash provides near-term cushion, the combination of $3.6B total debt plus expected FY 2025 loss of ($2.07) per share raises concerns. The -119.56% dividend payout ratio is UNSUSTAINABLE - dividend cut risk looms if lithium prices don't recover meaningfully.

-

🇨🇳 Chinese competition operating at losses to maintain share: Chinese lithium producers expanding capacity with government support, willing to run at losses to preserve market position. This creates persistent pricing pressure - Albemarle can't control spot prices when competitors flush market with supply. China accounts for over 60% of global EV production, giving Chinese producers structural advantage in serving the largest market.

-

⚠️ 2026 contract renegotiation overhang: As 2026 approaches, long-term fixed-price contracts face downward pressure for renegotiation. With spot market increasingly dominant over contracts, customers will push for pricing floors to decline or shift to spot-linked contracts. This directly threatens Albemarle's pricing stability and margin protection. Volume commitments could also be reduced given oversupply environment.

-

🚀 Execution risk on three major ramp-ups simultaneously: Albemarle is ramping Greenbushes expansion (Q4 2025), Meishan China facility, and Salar yield improvement project (currently 50% rate) all at once. ANY delays or technical issues at these critical facilities would immediately impact 2026 production targets and undermine the growth narrative. Operating three major projects across different geographies and technologies (hard rock, brine, conversion) creates significant execution complexity.

-

📉 Post-114% rally, significant technical correction risk: After surging from $49.43 April lows to $127.85, ALB is vulnerable to "sell the news" profit-taking. Beta of 2.05 means extreme volatility - stock moves 2x the market. Any disappointment in lithium pricing, production ramps, or financial metrics could trigger 20-30% correction back to $90-100 range. Year-end tax selling after triple-digit gains adds technical pressure.

-

💰 $10.6M institutional covered call signals limited near-term upside: When sophisticated institutions write $10.6M in covered calls at $120-$140 strikes through December, they're explicitly signaling they see LIMITED upside potential over the next 18 days. These players have access to better information, models, and market intelligence than retail. The Z-score of 232.19 on the $140 calls (literally unprecedented size) shows this isn't casual hedging - this is deliberate upside capping. Listen to what smart money is doing, not saying.

-

🌍 EV adoption uncertainty could undermine demand thesis: While global EV sales projected at 20M+ units in 2025, near-term headwinds include: U.S. subsidy changes depending on political environment, European economic weakness slowing adoption, EV price wars compressing OEM margins (reducing battery spending), and consumer preference shifts. Any material slowdown in EV adoption growth would immediately crater lithium demand forecasts and pricing expectations.

-

📊 Analyst consensus at $104 vs current $127 = potential downside: Average price target of $104.27 suggests current price at $127.85 may already reflect much of the recovery thesis. Stock trading 23% ABOVE consensus implies elevated expectations. While some bulls have $136-140 targets, the median view suggests limited upside and 18% downside risk to fair value. Analyst consensus often correct on materials/commodity stocks given clearer fundamental frameworks.

-

🇨🇳 Geopolitical tail risk: U.S.-China tensions: Critical minerals trade restrictions and potential tariffs create unpredictable policy risk. Albemarle's Chinese conversion facility at Meishan could face operational challenges if tensions escalate. China historically represented 15-20% of revenue - any export controls or retaliatory measures would materially impact results. Taiwan risk (TSMC semiconductor parallel) adds tail risk to lithium supply chains.

-

⏰ February 18, 2026 earnings = major binary event: With FY 2025 guidance of $4.9-5.2B revenue and expected loss of ($2.07) per share, any miss or conservative 2026 guidance could trigger violent selloff. Earnings 79 days away means LOW VISIBILITY - a lot can change in lithium markets between now and then. The covered call seller deliberately avoided this binary risk by expiring December 19th.

🎯 The Bottom Line

Real talk: Someone just monetized $10.6 MILLION in option premium on 1.32 million shares of Albemarle - and they did it with surgical precision. This isn't a bearish bet on lithium's long-term future; it's sophisticated portfolio management by an institution that rode the 114% recovery from April's $49.43 bottom and now wants to lock in gains while maintaining upside optionality.

What this trade tells us:

- 🎯 Upside capping: By selling calls at $120 and $140 (6% and 9.4% above current price), they're explicitly saying "we don't expect ALB above these levels through December 19th"

- 💰 Premium over appreciation: They'd rather collect $10.6M TODAY (8% return in 18 days) than hold out for uncertain appreciation

- 📅 Avoiding binary risk: Deliberately expired BEFORE February 18th earnings - they don't want to hold through that volatility

- 📊 Alignment with consensus: The $120-$140 strikes align PERFECTLY with analyst price targets of $104-140, suggesting institutional view of fair value

- ⏰ Year-end dynamics: Positioned for holiday consolidation, tax selling, and thin trading - low-catalyst environment favors premium collection

This is NOT a "sell and run" signal - it's a "take profits and manage risk intelligently" signal.

If you own ALB:

- ✅ Consider covered calls yourself: If you bought sub-$100, writing $130-140 calls for December/January collects premium while keeping upside

- 🎯 Trim if needed: After 114% YTD, taking 25-40% profits at $125-128 levels locks in gains and reduces risk

- 📊 Key support at $115-120: If stock breaks below this range, reassess thesis - cost savings may not offset lithium pricing pressure

- ⏰ February 18th is D-Day: Mark calendar for Q4/FY2025 earnings - THE catalyst that determines 2026 trajectory

- 💰 Watch lithium spot prices: Need sustained $10,000/mt+ to validate recovery thesis

If you're watching from sidelines:

- 🛡️ Sell cash-secured puts: $115-120 strikes (Dec/Jan) get you paid to wait for better entry

- 🎯 Patient capital wins: Let December consolidation/year-end selling create $110-115 entry (14-18% discount from current)

- 📈 Confirm fundamentals: Look for Greenbushes production ramp, lithium prices above $10K/mt, and Q4 earnings beat before committing

- 🚀 12-month view compelling: 2026 lithium market inflection + demand doubling to 3.7M tonnes by 2030 supports $120-150 longer-term targets

- ⚠️ Risk management critical: This is a cyclical materials stock with 2.05 beta - position size accordingly

If you're bearish:

- 📊 Wait for breakdown: $115-120 support must break before initiating shorts

- 🎯 Bull put spreads: Sell $120/$115 spreads if confident in support holding (defined risk way to capture premium)

- ⏰ Timing is everything: Don't fight 114% momentum prematurely - let price action confirm before pressing bearish bets

- 📉 Key negatives: $120K ton oversupply in 2025, Z-score 1.41 distress signal, Chinese competition, contract renegotiation risk

Mark your calendar - Key dates:

- 📅 December 5 (Thursday) - Weekly options expiration (±5.49% implied move closes)

- 📅 December 12 (Thursday) - Ex-dividend date ($0.405/share)

- 📅 December 19 (Thursday) - Monthly OPEX, expiration of this $10.6M covered call trade (±9.76% implied move)

- 📅 January 16, 2026 - January OPEX (±13.28% implied move)

- 📅 February 18, 2026 (Wednesday after close) - Q4/FY2025 EARNINGS - THE MAJOR CATALYST

- 📅 Q4 2025/Q1 2026 - Greenbushes first ore processing expected

- 📅 H1 2026 - Salar yield project full ramp-up

Final verdict: [Albemarle's long-term lithium story remains STRUCTURALLY BULLISH](https://www.ainvest.com/news/albemarle-strategic-restructuring-blueprint-resilience-lithium-era-2508/) - EV demand doubling, energy storage surging 105% YTD, $450M cost savings achieved, and 2026 market inflection expected. BUT, after a 114% YTD rally to $127.85 with analyst consensus at $104, near-term risk/reward is NOT compelling for aggressive new longs.

The $10.6M institutional covered call sale is a CLEAR signal: smart money believes $120-$140 represents fair-to-rich value for the next 18 days.

Be patient. Let December consolidate. Look for $110-120 pullback entries. Sell puts to get paid while waiting. The lithium revolution will still be here in 8-12 weeks, and you'll sleep better paying $115 instead of $128. The February 18th earnings will provide the REAL catalyst for the next leg - either confirming the recovery thesis with $300-400M free cash flow and strong 2026 guidance, or exposing weakness if lithium pricing disappoints.

Trade smart. Manage risk. Respect what smart money is telling you. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 7.15 and 232.19 Z-scores reflect these specific trades' sizes relative to recent ALB history - they do not imply the trades will be profitable or that you should follow them. Covered call strategies cap upside in exchange for premium income. Lithium pricing is highly volatile and unpredictable. Always do your own research and consider consulting a licensed financial advisor before trading.

About Albemarle Corporation: Albemarle Corporation is the world's largest lithium producer, with fully integrated operations spanning salt brine reserves in Chile/US and hard rock mining in Australia. The company supplies lithium for EV batteries and energy storage systems, alongside being the global leader in bromine-based flame retardants. Market cap: $15.3 billion in the Chemicals & Materials sector.