🔬 ASPI Massive $6.2M Calendar Spread - Institutional Bet on Isotope Production Timeline! ⚛️

📅 November 14, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed $6.2 MILLION across two linked ASPI call positions this afternoon at 12:35:42! This sophisticated calendar spread bought 22,000 January 2026 calls and 10,000 April 2026 calls at the $10 strike - a classic structure betting on isotope production milestones hitting right on schedule. With ASPI up +66.6% YTD at $7.55 and transitioning from development to commercial production across three facilities, smart money is positioning for precise catalyst timing. Translation: Institutional capital is making a calculated bet on Silicon-28, Ytterbium-176, and Carbon-14 revenue ramp through early 2026!

📊 Company Overview

ASP Isotopes Inc. (ASPI) is a pre-commercial stage materials company pioneering advanced isotope enrichment technology:

- Market Cap: $884.6 Million

- Industry: Miscellaneous Chemical Products (Isotope Production)

- Current Price: $7.55 (after peak of $14.21 in October)

- Primary Business: Enrichment of isotopes using proprietary Aerodynamic Separation Process (ASP) technology for quantum computing (Silicon-28), nuclear medicine (Ytterbium-176, Carbon-14), and advanced nuclear fuel (HALEU)

💰 The Option Flow Breakdown

The Tape (November 14, 2025 @ 12:35:42):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:35:42 | ASPI | MID | BUY | ASPI Jan 16 $10 Call | 2026-01-16 | $3.4M | $10 | 22K | - | 22,000 | $7.55 | $1.55 |

| 12:35:42 | ASPI | MID | BUY | ASPI Apr 17 $10 Call | 2026-04-17 | $2.8M | $10 | 10K | - | 10,000 | $7.55 | $2.80 |

🤓 What This Actually Means

This is a long double calendar spread - a sophisticated multi-leg strategy! Here's what went down:

- 💸 Total capital deployed: $6.2M ($3.4M + $2.8M)

- 📅 Front month position: 22,000 ASPI Jan 16 $10 calls at $1.55 each

- 📅 Back month position: 10,000 ASPI Apr 17 $10 calls at $2.80 each

- 🎯 Strike positioning: $10 represents 32.5% upside from current $7.55 price

- 📊 Massive size: Combined 32,000 contracts = 3.2 million shares (3.5% of float!)

- 🏦 Institutional sophistication: This is NOT retail - calendar spreads require advanced options knowledge

What's really happening here:

This trader is making a PRECISE bet on ASPI's commercial production timeline. By buying more contracts in January (22K) than April (10K), they're positioning for a catalyst sequence:

- By January 2026: Silicon-28 facility completing commissioning, first commercial samples expected

- Through April 2026: Ytterbium-176 commercial production ramp, Carbon-14 revenue stream established

- Breakeven: Stock needs to reach $11.55 (Jan) or $12.80 (Apr) - reasonable given production milestones

The calendar structure limits downside (max loss is the $6.2M premium paid) while creating leverage if ASPI rallies as production comes online. This isn't a gamble on the stock doubling - it's a calculated bet that commercial validation will drive ASPI from $7.55 to $10-12 range over the next 3-5 months.

Unusual Score: 🔥 VOLCANIC (2,106x average size, Z-score 423) - This is the largest ASPI options trade in recent history! We're talking about a position larger than the entire typical daily ASPI options premium. The 100th percentile ranking means NOTHING traded in the past 30 days came close to this size.

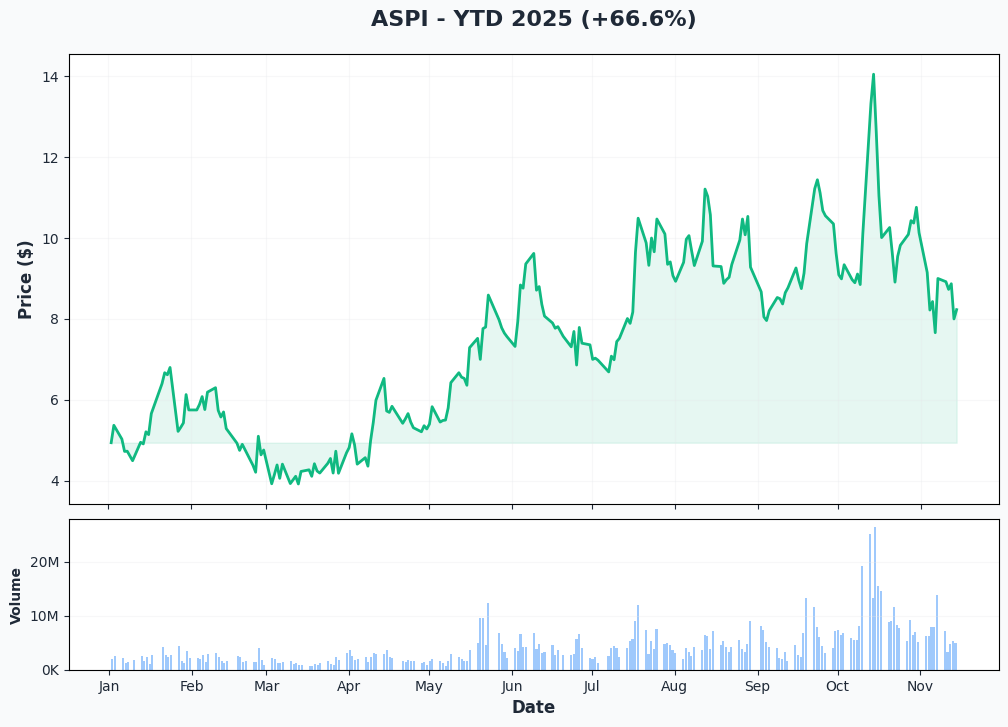

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

ASPI is up +66.6% YTD but telling a volatile story - current price $7.55 after spiking to $14.21 in late October. The chart shows a classic development-stage biotech pattern: massive volatility around production milestones and capital raises.

Key observations:

- 🎢 Extreme volatility: Started year at ~$5, rallied to $14.21, now back to $7.55 - this is a wild ride!

- 📈 October spike: Parabolic move from $9 to $14 coincided with Silicon-28 facility completion announcement

- 📉 Recent pullback: Down 47% from October high - profit-taking after capital raise

- 💹 Volume spikes: Massive institutional activity around catalyst announcements

- 🚨 High beta: This stock moves 3-5x more than the market - not for the faint of heart

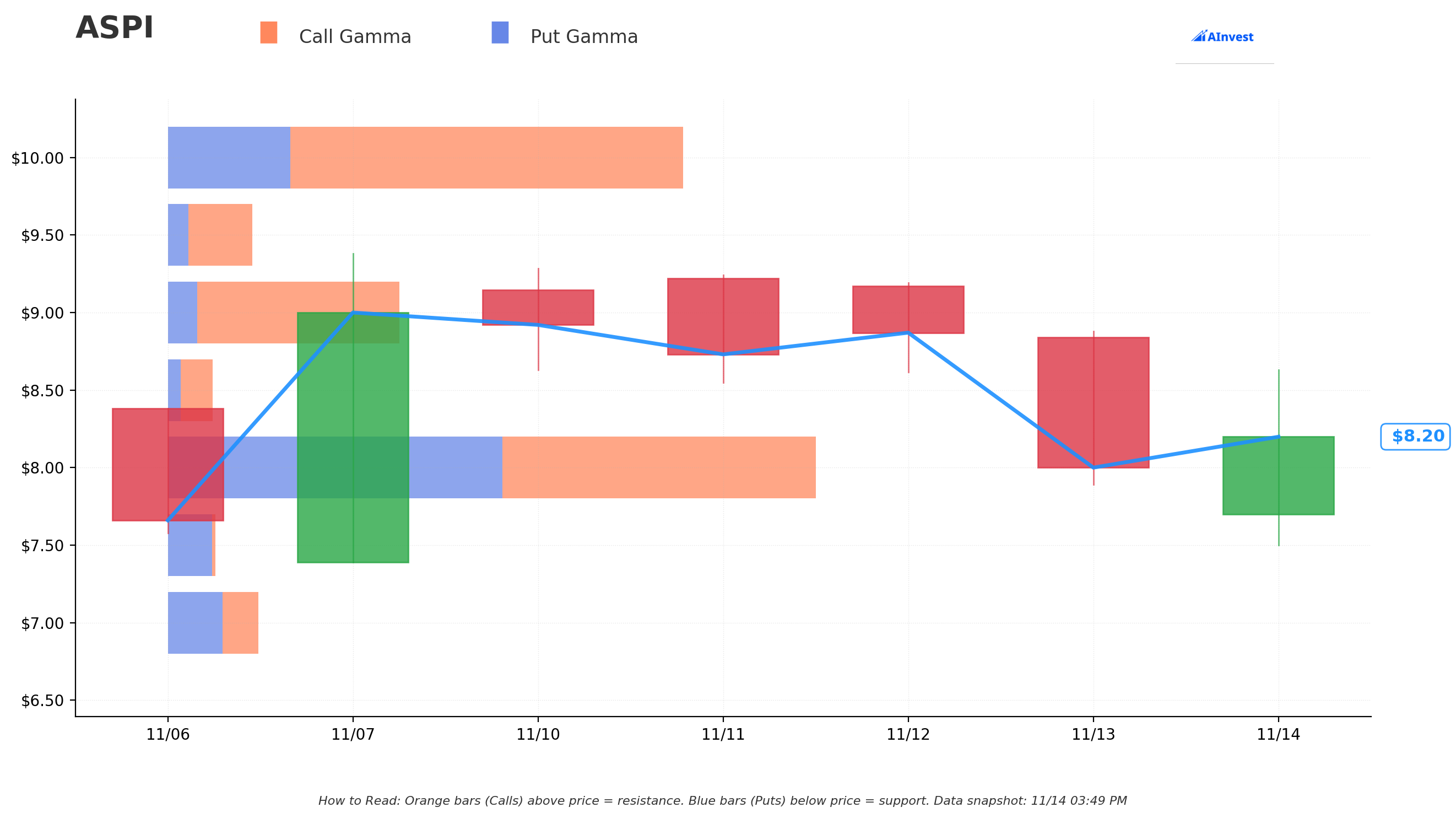

Gamma-Based Support & Resistance Analysis

Current Price: $7.55

The gamma exposure map shows critical inflection points for this pre-revenue stock:

🔵 Support Levels (Put Gamma Below Price):

- $7.50 - Immediate support where current price is stabilizing

- $7.00 - Secondary floor with moderate put gamma

- $6.50 - Major support zone (recent capital raise pricing)

🟠 Resistance Levels (Call Gamma Above Price):

- $8.00 - Immediate ceiling with modest call gamma

- $9.00 - Secondary resistance (pre-spike consolidation level)

- $10.00 - MAJOR RESISTANCE with massive call gamma (exactly where this trade is struck!)

- $10.50+ - Open road above if $10 breaks

What this means for traders:

The gamma data shows massive call open interest stacked at the $10 strike - exactly where this calendar spread is positioned. That's NOT a coincidence! The trader is betting that as ASPI approaches $10 through Q1 2026, the huge call gamma will create upward momentum as market makers hedge their short positions by buying stock. The $10 level is THE key battleground where gamma could either cap rallies or, if breached, accelerate upside to $12-15.

Net GEX Bias: Neutral with heavy call positioning - suggests market expects significant upside potential if production milestones hit.

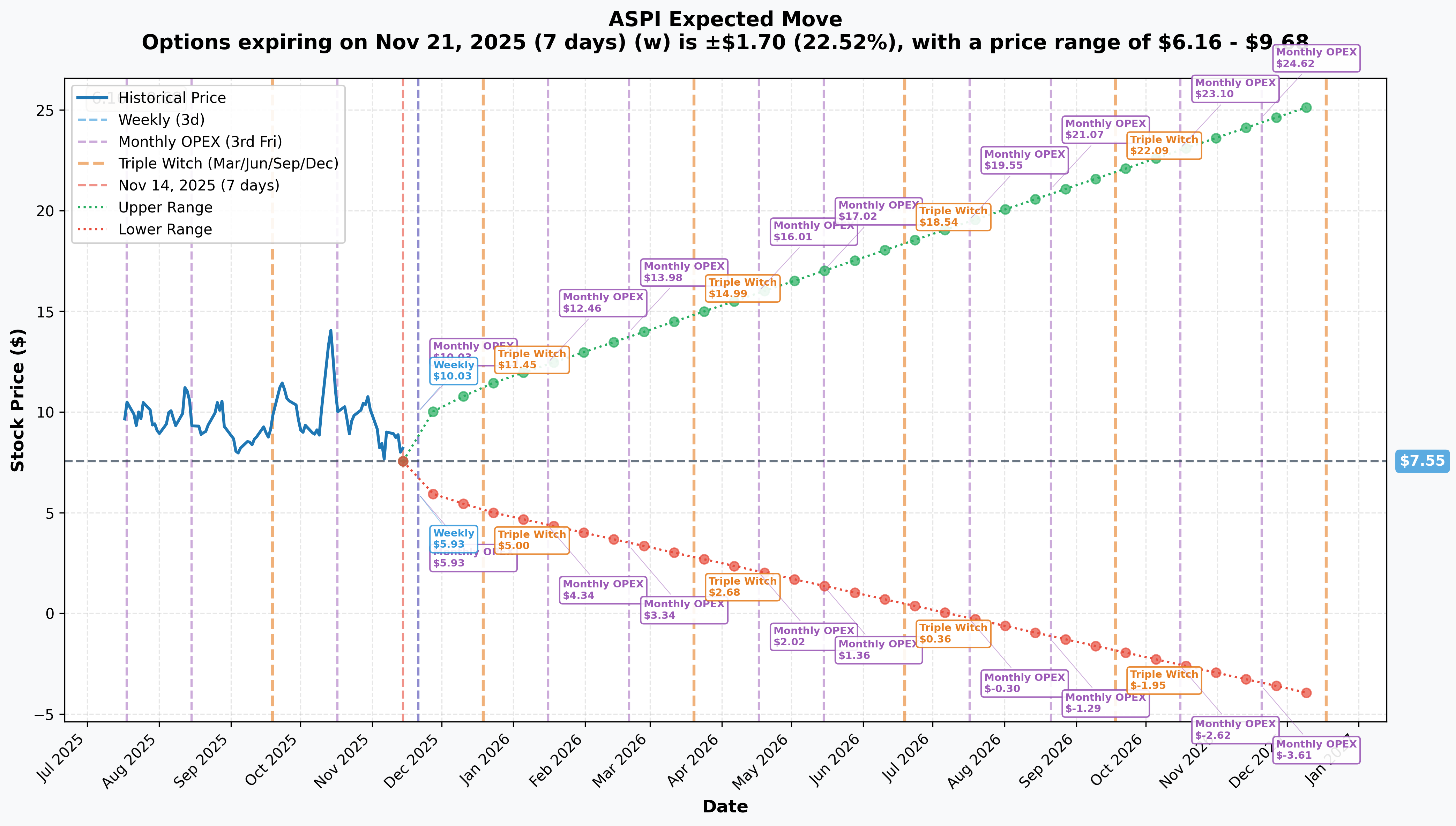

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Nov 21 - 7 days): ±$1.70 (±22.5%) → Range: $6.16 - $9.68

- 📅 Monthly OPEX (Nov 21 - 7 days): ±$1.70 (±22.5%) → Range: $6.16 - $9.68

- 📅 Quarterly Triple Witch (Dec 19 - 35 days): ±$2.78 (±36.9%) → Range: $5.10 - $11.29

- 📅 January OPEX (Jan 16 - 63 days - FRONT LEG!): ±$4.82 (±51.3%) → Range: $4.34 - $12.46

- 📅 April OPEX (Apr 17 - 154 days - BACK LEG!): ±$7.00 (±70%) → Range: $2.02 - $16.01

Translation for regular folks:

Options traders are pricing in MASSIVE volatility for ASPI - a 22.5% weekly move and 51% move through January! This is development-stage biotech volatility levels. The market expects huge swings as commercial production data comes in.

The January implied range of $4.34-$12.46 perfectly captures the risk profile: downside to $4 if production ramp disappoints, upside to $12+ if milestones hit on schedule. The ASPI Jan 16 $10 call strike sits right in the middle of the expected range - not too aggressive, not too conservative.

Key insight: The 70% implied move through April reflects uncertainty around THREE simultaneous production ramps (Silicon-28, Ytterbium-176, Carbon-14). This calendar spread is betting those catalysts resolve BULLISHLY.

🎪 Catalysts

🔥 Already Happened (Building Blocks)

Silicon-28 Facility Construction Completion (November 26, 2024) 💻

ASPI completed construction of its Silicon-28 enrichment facility in Pretoria, South Africa and began commissioning phase:

- 🎯 Annual capacity upgraded to >50 kg at 99.995% enrichment (up from initial 10 kg guidance)

- 📈 Further upgraded to >80 kg annually based on first three months of production (started March 2025)

- 🖥️ Applications: Quantum computing, AI, and large data center semiconductors

- 🤝 Two purchase agreements signed with US-based customers (one semiconductor company, one industrial gas company)

Ytterbium-176 First Production (October 2024) ⚛️

Completed first Quantum Enrichment Facility 9 months ahead of schedule and produced first semi-finished enriched Ytterbium-176:

- 🎯 Target enrichment: 99.75% Ytterbium-176

- 💊 Application: Key isotope for producing Lutetium-177 used in Novartis' Pluvicto oncology drug

- 📅 Commercial production started April 2025 at 92.4% enrichment

TerraPower HALEU Partnership (October 30, 2024) ⚡

Signed definitive agreements with TerraPower (Bill Gates-backed advanced nuclear company) for massive HALEU production facility:

- 🏭 15 metric tons annual HALEU capacity at Pelindaba, South Africa

- 💰 10-year supply agreement for up to 150 metric tons (2028-2037)

- 💵 All financing non-dilutive to shareholders through TerraPower commitments

- 📅 Expected production start: 2027

Capital Raises Throughout 2024 💸

Multiple equity raises with concerning dilution:

- November 2024: $18.6M at $6.75/share (significantly below market, closed Nov 4)

- July 2024: $32.3M from 13.8M shares

- Impact: Multiple dilutive raises raising questions about cash burn and path to profitability

🚀 Upcoming Catalysts (Next 6 Months - CRITICAL FOR THIS TRADE!)

Q4 & FY2024 Earnings Release (March 31, 2025) 📊

ASPI will report full year 2024 results after market close on March 31, 2025:

- 💰 FY2024 Revenue: $4.14M (up 857% from $433K in 2023) - still pre-commercial scale

- 📉 FY2024 Net Loss: -$35.11M (115.6% increase in losses)

- 🎯 What to watch: Production facility status updates, 2025 revenue guidance, path to profitability timeline

- ⚠️ Limited analyst coverage (only 2 analysts) creates uncertainty

Silicon-28 First Commercial Shipments (Q2 2025) 🖥️

Critical milestone for revenue validation:

- 📅 First commercial batches expected Q2 2025

- 📅 Finished commercial product (99.995% enrichment) shipping August 2025

- 💵 Estimated revenue potential: $50-70M in 2026-2027 from Silicon-28 and Ytterbium-176 combined

Ytterbium-176 Commercial Samples (August 2025) 💊

Commercial samples expected to ship August 2025:

- 🎯 Already commenced commercial production in April 2025

- 💰 Contributing to $50-70M revenue potential 2026-2027

- 💊 Breaking into nuclear medicine supply chain currently dominated by Russia

Carbon-14 Commercial Production (February 2025 - ALREADY STARTED!) ⚛️

Commercial production commenced February 2025:

- 💵 Multi-year take-or-pay contract with RC-14 Inc. for minimum $2.4M annual revenue

- 📅 Expected to ship commercial product mid-2025

- 🌍 Breaks Russia's 85% global Carbon-14 monopoly

Renergen Acquisition Close (Q3 2025 Target) 🔥

Transformational M&A announced May 20, 2025:

- 🎯 Acquisition of South African helium/LNG producer Renergen

- ✅ 99.80% Renergen shareholder approval (July 10, 2025)

- 💰 Renergen 2026 revenue guidance: minimum $20M

- 🚀 Combined group targeting >$300M EBITDA by 2030

- 💵 $750M US government debt financing committed for Renergen's helium asset

- 📅 Expected close: Q3 2025 (by September 30) - awaiting final regulatory approvals

⚠️ Risk Catalysts (What Could Derail This Trade)

Production Ramp Challenges 🏭

Simultaneously scaling three facilities is unprecedented for ASPI:

- ⚠️ Limited operational track record in commercial-scale isotope production

- 🔧 Technology proven for some isotopes but scaling risk remains

- 🚧 Dependency on third-party suppliers creates supply chain fragility

- ⏰ Any delays in Silicon-28 Q2 shipments or Ytterbium-176 samples could trigger selloff

Regulatory & Permitting Delays ⚖️

Isotope industry heavily regulated:

- 📋 HALEU facility requires extensive approvals - 2027 timeline could slip

- 🌍 Renergen acquisition still awaiting final regulatory approvals

- ⏳ Rigorous licensing procedures can delay commercialization

Financial & Dilution Risks 💸

Cash burn remains severe:

- 💰 -$35.11M net loss in 2024 with only $4.14M revenue

- 📉 Multiple equity raises at declining prices ($6.75 in November below market)

- ⚠️ Likely requires additional funding before reaching profitability

- 🔴 Insider selling: CEO sold $6.7M, COO $1.19M in 2024 - raises questions about confidence

Short Seller Pressure 🐻

Fuzzy Panda Research published critical report November 26, 2024:

- Company rebutted as "speculative conjecture and inaccurate"

- Continued short pressure could create volatility

- Stock down 47% from October highs suggests profit-taking

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and production catalysts, here are the scenarios:

📈 Bull Case (35% probability)

Target: $12-14

How we get there:

- ✅ Silicon-28 commercial shipments hit Q2 2025 timeline with quality meeting customer specs

- 💊 Ytterbium-176 samples ship August 2025, securing first nuclear medicine contracts

- 💰 Carbon-14 revenue stream validates $2.4M annual minimum

- 🤝 Renergen acquisition closes Q3 2025, adding immediate $20M revenue base

- 📊 Q4 earnings (March 31) provides strong 2025 revenue guidance ($50M+ from isotopes)

- 🚀 Market re-rates from "development story" to "commercial execution" - multiple expansion

Calendar spread payoff: Both legs profitable - ASPI Jan 16 $10 calls worth $2-4 (up from $1.55), ASPI Apr 17 $10 calls worth $4-6 (up from $2.80). Potential 50-100% return on $6.2M.

🎯 Base Case (45% probability)

Target: $8-10 range

Most likely scenario:

- ✅ Production milestones mostly on track but with minor delays/quality issues

- 📅 Silicon-28 shipments slip from Q2 to Q3 2025, but customers remain committed

- 💊 Ytterbium-176 samples delayed or lower enrichment than 99.75% target

- 💰 Carbon-14 revenue comes in but at lower volumes than hoped

- ⚠️ Renergen close delayed from Q3 to Q4 2025 due to regulatory approvals

- 📊 Q4 earnings shows progress but path to profitability still 2-3 years away

- 🔄 Stock trades in $8-10 range as market waits for production proof points

Calendar spread payoff: Front leg (Jan) expires near breakeven or small loss. Back leg (Apr) retains value for potential 2026 catalysts. Net result: -20% to +30% on $6.2M.

📉 Bear Case (20% probability)

Target: $5-6

What could go wrong:

- 😰 Major production delays or quality issues at one or more facilities

- 🏭 Silicon-28 commissioning extends beyond Q2, customer contracts cancelled

- 💊 Ytterbium-176 fails to meet pharmaceutical-grade specifications

- 💸 Need for additional dilutive capital raise at depressed prices

- ⚖️ Renergen deal fails to close due to regulatory/financing issues

- 🐻 Short seller report gains traction with new evidence

- 📉 Broader biotech/small-cap selloff drags ASPI lower

- 🛡️ Support at $6.50 (capital raise pricing) fails to hold

Calendar spread payoff: Both legs expire worthless or nearly so. Loss of 60-80% of $6.2M premium.

💡 Trading Ideas

🛡️ Conservative: Wait for Production Proof

Play: Stay on sidelines until Silicon-28 commercial shipments validated

Why this works:

- ⏰ Too much execution risk with three simultaneous production ramps

- 💸 High implied volatility (51% through January) makes options expensive

- 📊 Stock already up 66% YTD - substantial move already priced in

- 🎯 Better entry likely after Q4 earnings (March 31) provides clarity

- ⚠️ Development-stage companies have high failure rate - let them prove it first

Action plan:

- 👀 Watch March 31 earnings for production status updates

- 🎯 Monitor for first Silicon-28 commercial shipment announcement (Q2 2025)

- ✅ Wait for Ytterbium-176 sample validation from pharmaceutical customers

- 📊 Look for pullback to $6-6.50 range (capital raise pricing) for stock entry

- 🔍 Verify Renergen acquisition closes before committing capital

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: Small Position in Jan $10 Calls

Play: Buy small position in ASPI January 2026 $10 calls

Structure: Buy 5-10 contracts (not thousands like this whale!) at current $1.55

Why this works:

- 📅 63 days to expiration captures critical production milestones

- 💰 Defined risk: Max loss is premium paid ($775-1,550 for 5-10 contracts)

- 🎯 Breakeven at $11.55 (53% upside) reasonable if production validates

- 📊 Piggyback on institutional positioning at same strike

- ⏰ Time value decays slower than weekly options

- 🚀 Captures upside if Silicon-28 shipments or Ytterbium-176 samples news hits

Estimated P&L:

- 💰 Cost: $155 per contract × 5-10 contracts = $775-1,550 total

- 📈 Bull case (ASPI at $12-14): Worth $2-4 per contract = 130-160% gain

- 🎯 Base case (ASPI at $9-10): Worth $0-1 per contract = -100% to -35% loss

- 📉 Bear case (ASPI below $8): Expire worthless = -100% loss

Entry timing: Wait for any pullback below $7.50 to enter

Exit strategy:

- ✅ Take profits if ASPI hits $10-11 before expiration

- ⏰ Cut losses if stock breaks below $7 support

- 📅 Don't hold into last week (theta decay accelerates)

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: Replicate the Calendar Spread (Scaled Down)

Play: Build mini version of this institutional trade

Structure:

- Buy 10 ASPI Jan 16 $10 calls at $1.55 = $1,550

- Buy 5 ASPI Apr 17 $10 calls at $2.80 = $1,400

- Total investment: $2,950

Why this could work:

- 📅 Captures both Q1 and Q2 2026 production milestones

- 🎯 Same strikes as $6.2M institutional position - following smart money

- 📊 Front-weighted (10 Jan vs 5 Apr) mirrors institutional structure

- 💰 Limited downside to $2,950 premium paid

- 🚀 Leveraged upside if production timeline accelerates

- ⏰ Back leg (April) provides cushion if timing slightly off

Why this could blow up (SERIOUS RISKS):

- 💥 Development-stage execution risk is MASSIVE - facilities might not work at commercial scale

- 😱 Stock down 47% from October highs - momentum already broken

- 💸 Multiple dilutive capital raises - could do another at even lower prices

- 🐻 Short seller targeting the stock

- ⚠️ Heavy insider selling ($6.7M by CEO) - management cashing out

- 🏭 Technology risk: ASP enrichment unproven at commercial scale for some isotopes

- 💰 -$35M annual losses - path to profitability uncertain

Estimated P&L:

- 💰 Max loss: $2,950 (100% of premium if both legs expire worthless)

- 📈 Bull case (ASPI at $12-14 by April): Worth $6,000-8,000 = 100-170% gain

- 🎯 Base case (ASPI at $9-10): Worth $1,500-3,000 = -50% to breakeven

- 📉 Bear case (ASPI below $8): Both legs worthless = -100% loss

Risk level: EXTREME (development-stage company) | Skill level: Advanced only

⚠️ WARNING: DO NOT attempt this unless you:

- Understand biotech/development-stage company risks

- Can afford to lose 100% of premium

- Have experience with calendar spreads

- Can monitor production announcements and adjust position

- Recognize this is essentially venture capital investing through options

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🏭 Unprecedented execution challenge: Scaling THREE isotope facilities simultaneously from commissioning to commercial production is something ASPI has never done. Limited track record creates massive execution risk. Any failure at one facility could crater the stock.

-

💸 Cash burn death spiral: -$35M annual losses with only $4.14M revenue and multiple dilutive equity raises (November at $6.75, July for $32M). Company likely needs more capital before reaching profitability, risking further dilution at depressed prices.

-

👤 Insider selling red flag: CEO Paul Mann sold $6.7M and COO Robert Ainscow sold $1.19M in 2024 with 11 insider sales and ZERO purchases. When management is cashing out while asking shareholders to fund operations, that's a major concern.

-

🔬 Technology scaling risk: ASP enrichment technology proven in lab but commercial-scale production is different ballgame. Silicon-28 capacity upgraded from 10kg to 50kg to 80kg suggests they're still figuring it out.

-

⚖️ Regulatory minefield: Isotope industry heavily regulated. Any delays in permits for HALEU facility (targeting 2027) or Renergen acquisition could derail timeline.

-

🐻 Short seller targeting: Fuzzy Panda Research published critical report in November 2024. While company rebutted, stock down 47% from October highs suggests concerns resonated with some investors.

-

🎯 Customer concentration: Heavy reliance on small customer base for each isotope. Loss of semiconductor customers for Silicon-28 or pharma partners for Ytterbium-176 would be devastating.

-

🌍 Geopolitical risk: All production facilities in South Africa. Political instability, power grid issues (load shedding), or regulatory changes in SA could disrupt operations.

-

💰 Valuation disconnect: $885M market cap for company with $4M revenue and -$35M losses. Entire valuation based on future production that hasn't been proven commercially. Multiple compression risk if execution stumbles.

-

📅 Timeline slippage: Development-stage companies ALWAYS face delays. Silicon-28 commercial shipments slipping from Q2 to Q3 or Ytterbium-176 samples delayed past August would disappoint this calendar spread thesis.

-

🔄 Competition emergence: Russia controls 85% of global isotope production. While geopolitics favor Western suppliers, established players (Urenco, Orano) could enter market.

🎯 The Bottom Line

Real talk: Someone just bet $6.2 MILLION that ASPI's three isotope production facilities will hit their commercial production timelines over the next 3-5 months. This isn't a gamble on the stock doubling - it's a sophisticated calendar spread betting on steady execution from $7.55 to $10-12 range as Silicon-28, Ytterbium-176, and Carbon-14 facilities validate commercial operations.

What this trade tells us:

- 🎯 Institutional capital believes production milestones are achievable (not guaranteed, but probable)

- 📅 The precise timing structure (heavier Jan position, lighter Apr) suggests confidence in Q1-Q2 2026 catalysts

- 💰 $6.2M commitment shows conviction - this isn't a spec play, it's a calculated bet

- 🏭 Positioning at $10 strike (32.5% upside) reflects reasonable expectations, not moonshot hopes

- ⚖️ Calendar structure limits downside while maintaining upside leverage - smart risk management

If you own ASPI:

- ✅ This trade validates your thesis IF you bought for production story

- 📊 Set realistic targets: $10-12 is the institutional target, not $20+

- ⏰ Key dates: March 31 earnings, Q2 Silicon-28 shipments, August Ytterbium samples

- 🛡️ Consider taking partial profits if stock rallies to $9-10 before production validated

- 🚨 Watch for any negative production updates - development stage can disappoint fast

If you're watching from sidelines:

- ⏰ March 31, 2025 - Q4 earnings provides production facility status updates

- 🎯 Q2 2025 - Silicon-28 first commercial shipments - THE key catalyst

- 💊 August 2025 - Ytterbium-176 commercial samples ship to pharma customers

- 🤝 Q3 2025 - Renergen acquisition close adds $20M revenue base

- 📊 Waiting for production proof before entering is the conservative play

- 💸 High implied volatility (51% through January) means options expensive - let institutions pay the premium

If you're bearish:

- 🎯 Development-stage execution risk is real - many ways this can fail

- 💸 Cash burn and dilution pattern concerning - could do another raise

- 📉 Stock already down 47% from October highs - momentum broken

- 🐻 Put spreads ($7.50/$5 or $10/$7.50) offer defined risk way to play downside

- ⏰ Wait for production disappointment to initiate shorts - don't fight this institutional positioning

Mark your calendar - Key dates:

- 📅 March 31, 2025 - Q4 & FY2024 earnings after market close, webinar April 1

- 📅 Q2 2025 (April-June) - Silicon-28 first commercial batch shipments expected

- 📅 August 2025 - Ytterbium-176 commercial samples to customers, Silicon-28 finished product (99.995%) shipping

- 📅 September 30, 2025 - Renergen acquisition target close date

- 📅 November 11-13, 2025 - Institutional investor tour of South Africa facilities

- 📅 2026 - Molybdenum-100/98 production start, four new laser plants construction

- 📅 2027 - HALEU facility initial production for TerraPower

Final verdict: This $6.2M calendar spread is a precisely calculated bet on production timeline execution, not a speculative gamble. The structure shows institutional sophistication - heavier weighting on near-term January expiration to capture Q1 milestones, lighter April position for Q2 validation. At 2,106x average trade size, this is unprecedented ASPI options activity signaling serious institutional conviction. However, development-stage execution risk remains enormous. Conservative investors should wait for production proof points. Aggressive traders can consider scaled-down versions of this spread, but only with capital they can afford to lose 100%. The next 3-5 months will determine whether ASPI transitions from "promising development story" to "commercial execution" - and this trade has $6.2M riding on that outcome.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Development-stage companies like ASPI carry extreme risk including potential total loss of investment. The unusual score (2,106x average) reflects trade size relative to recent history - it does not imply the trade will be profitable or that you should follow it. Calendar spreads are complex strategies requiring advanced knowledge. Past performance doesn't guarantee future results. Commercial production timelines are estimates and frequently slip. Always do your own research and consider consulting a licensed financial advisor before trading.

About ASP Isotopes Inc.: ASP Isotopes Inc is a pre-commercial stage materials company with an $884.6 million market cap, dedicated to development of technology and processes for production of isotopes used in quantum computing, nuclear medicine, and advanced nuclear energy in the Miscellaneous Chemical Products industry.