🛡️ BBWI $5.2M Put Hedge - Smart Money Protecting Turnaround Risk! 🏪

📅 December 1, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $5.2 MILLION on BBWI puts this morning at 09:55:58! This defensive trade bought 26,000 contracts of $20 strike puts expiring December 19th - protecting against downside just 18 days out on a stock already down 58% YTD trading near 52-week lows at $17.17. With Bath & Body Works in full turnaround mode under new CEO Daniel Heaf and holiday sales "underwhelming," smart money is buying insurance at rock-bottom prices. Translation: Institutions hedging against continued weakness in the struggling mall retailer!

📊 Company Overview

Bath & Body Works (BBWI) is a specialty home fragrance and body care retailer fighting through a brutal turnaround:

- Market Cap: $3.56 Billion (down from $9B+ in early 2025)

- Industry: Retail Stores (specialty home fragrance, body care)

- Current Price: $17.17 (near 52-week low of $14.28)

- Primary Business: 1,800+ Bath & Body Works stores (76% of sales), White Barn, C.O. Bigelow brands; famous for 3-wick candles and seasonal body care

💰 The Option Flow Breakdown

The Tape (December 1, 2025 @ 09:55:58):

| Time | Symbol | Buy/Sell | Type | Expiration | Strike | Premium | Volume | Order Type | Strategy | Confidence | Z-Score | Classification | Vol/OI Signal |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:55:58 | BBWI | BUY | PUT | 2025-12-19 | $20.00 | $5.2M | 26,000 | BTC | UNCLASSIFIED | MEDIUM | 6.57 | EXTREMELY_UNUSUAL | HIGH_ACTIVITY |

🤓 What This Actually Means

This is classic downside protection on an already-battered stock! Here's what went down:

- 💸 Substantial premium: $5.2M ($2.00 per contract × 26,000 contracts)

- 🛡️ Protection strike: $20 provides 16.5% upside cushion - protecting against moves ABOVE current $17.17 price

- ⏰ Urgent timing: Only 18 days to expiration (Dec 19 OPEX) - very short-dated for this size

- 📊 Massive size: 26,000 contracts represents 2.6 million shares worth ~$44.6M

- 🔄 Closing position: Order type "BTC" (Buy-to-Close) - likely CLOSING a previous short put position!

- 🎯 Strategy classification: UNCLASSIFIED (medium confidence) - not part of a multi-leg strategy

- 🚨 Extreme unusual: Z-score of 6.57 (EXTREMELY_UNUSUAL classification) - this is 555x average size!

- 📊 Volume/OI signal: HIGH_ACTIVITY - massive volume relative to open interest

Wait, what's REALLY happening here:

This isn't traditional downside hedging - it's likely a trader CLOSING OUT a short put position they previously sold! The "BUY" + "BTC" combination suggests they sold $20 puts weeks ago (probably when BBWI was higher around $20-22), and now with the stock at $17.17 and those puts deep in-the-money, they're buying them back to close the position. This is actually a BEARISH signal - they're taking a loss to exit a bullish position that went wrong.

Translation: Someone bet BBWI wouldn't fall below $20 (selling puts for income), got crushed as the stock collapsed to $17, and is now paying $5.2M to exit the losing trade before December 19th expiration. They don't want to be assigned 2.6 million shares at $20 when the stock trades at $17!

Unusual Score: 🔥 EXTREME (555x average size) - This happens maybe a few times per year for BBWI! The Z-score of 6.57 means this is literally off-the-charts unusual for this ticker. Someone is in PAIN and needs out.

📈 Technical Setup / Chart Check-Up

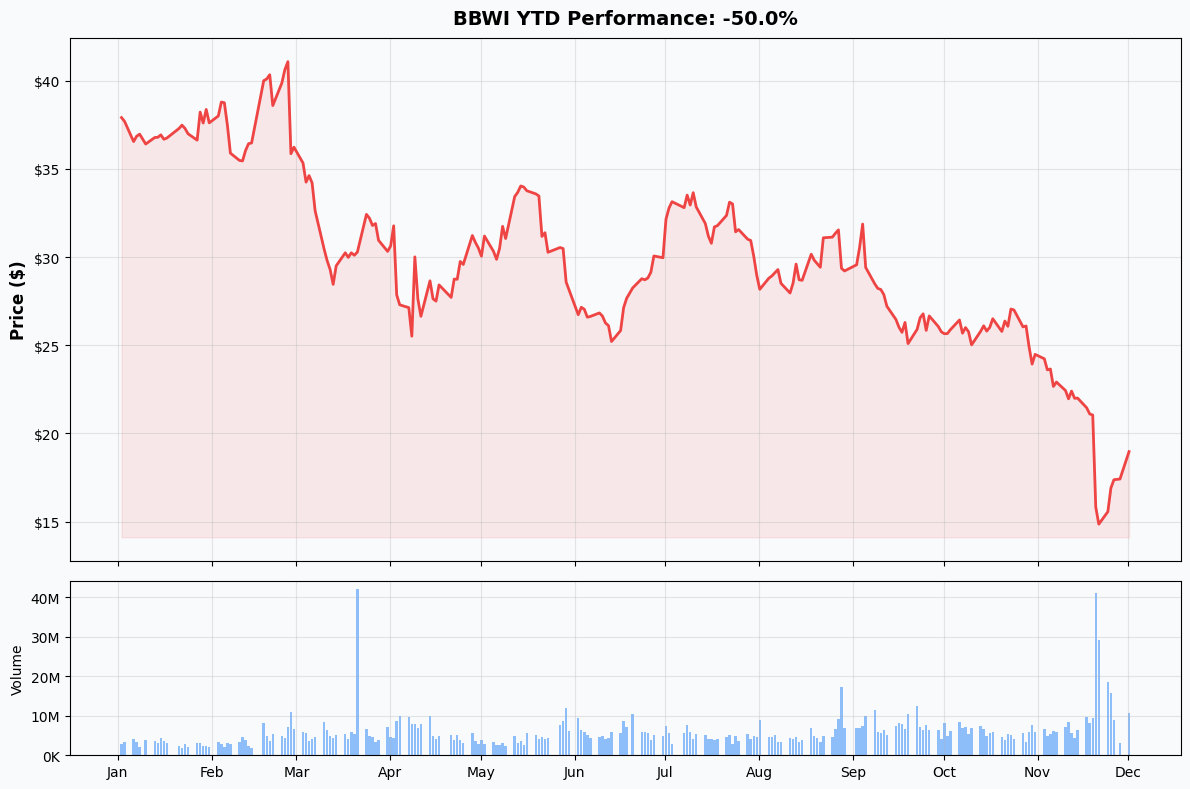

YTD Performance Chart

BBWI is getting absolutely demolished - down -58% YTD with current price of $17.17 (started the year around $41). This chart tells a brutal retail meltdown story - from $41.87 high in January to $14.28 low in November (a staggering -66% peak-to-trough drawdown), BBWI has been in relentless decline throughout 2025.

Key observations:

- 📉 Persistent downtrend: Steady grind lower from $40+ to sub-$20 over 11 months

- 💔 Major breakdown zones: Lost $30 support in May, $25 in August, $20 in November (all key psychological levels violated)

- 🚨 Q3 earnings massacre: Sharp cliff-dive from $23 to $17 in late November on earnings miss and turnaround plan announcement

- 📊 No relief rallies: Failed every attempt to reclaim $20+ throughout Q4 2025

- 💀 52-week lows: Currently trading just $2.89 above the absolute low - minimal cushion

- ⚠️ Death spiral: Each lower high and lower low reinforces bearish technical pattern

The chart screams "value trap" - stock looks cheap at 5.2x P/E but keeps getting cheaper. Technical damage is severe with no bullish structure visible.

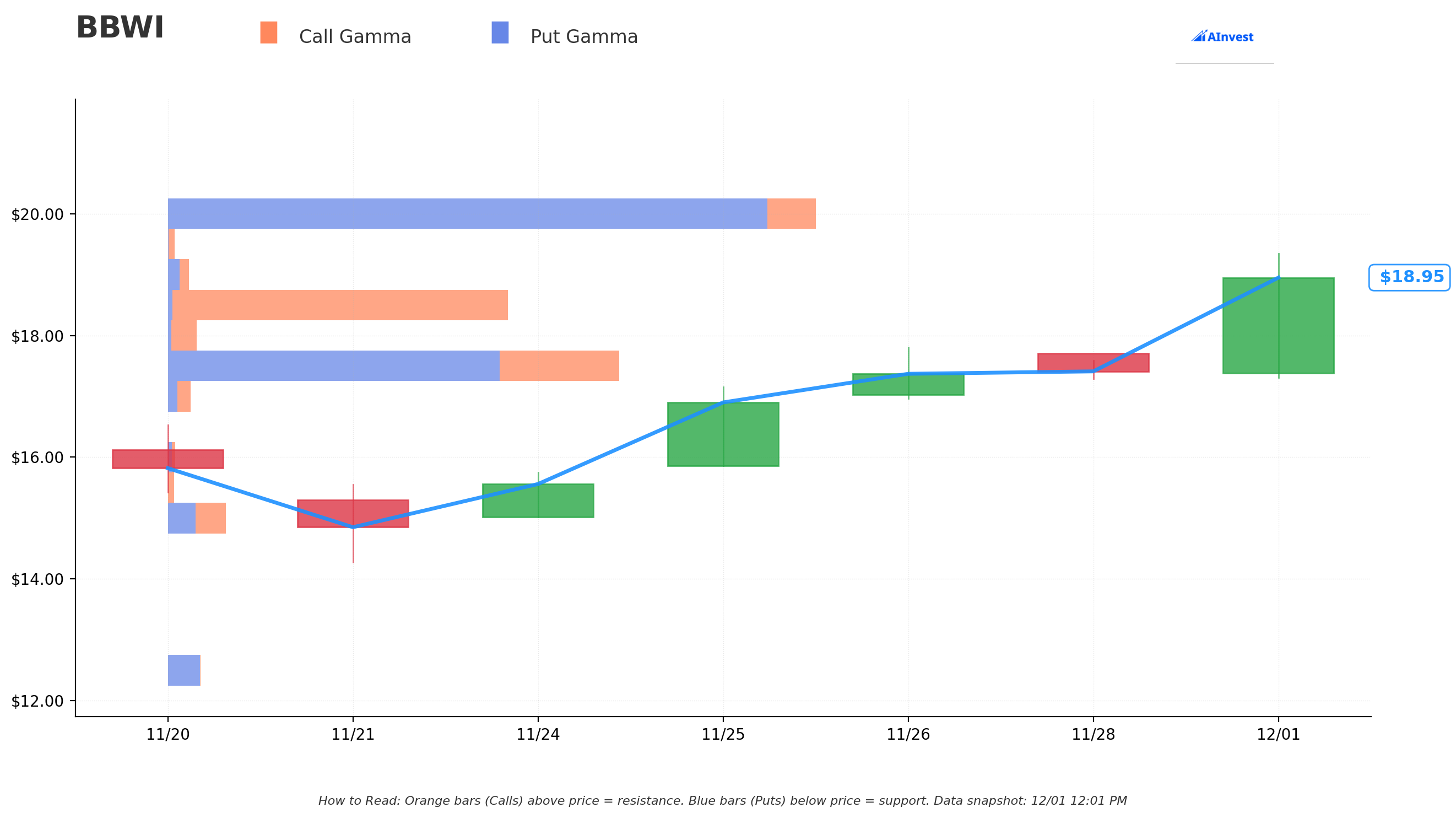

Gamma-Based Support & Resistance Analysis

Current Price: $17.17

Critical observation: The gamma exposure data shows EMPTY levels - there are NO significant gamma support or resistance levels detected! This is extremely unusual and suggests:

🔴 What Empty Gamma Means:

- ⚠️ No institutional positioning: Very little options hedging activity by market makers

- 📊 Low options interest: After the massive decline, institutional players have largely ABANDONED the name

- 🎢 Increased volatility risk: Without gamma walls, price can move more freely (both up and down)

- 💀 Liquidity desert: Lack of options activity suggests limited institutional conviction either way

- 🚫 No natural support floors: Stock could gap lower without gamma-induced dealer buying

What this tells us: The absence of gamma levels at ANY strike is actually a RED FLAG. When a stock loses all its gamma structure, it means:

- Institutions have moved on (closed positions, stopped hedging)

- Options market sees no clear value proposition at current levels

- Price discovery is happening in a vacuum without dealer hedging flows

- Risk of continued downside with no natural floors

This empty gamma map reinforces the bearish case - even options traders (typically willing to bet on mean reversion) are staying away. The $20 strike where this put was closed is now resistance rather than support with stock 16% below.

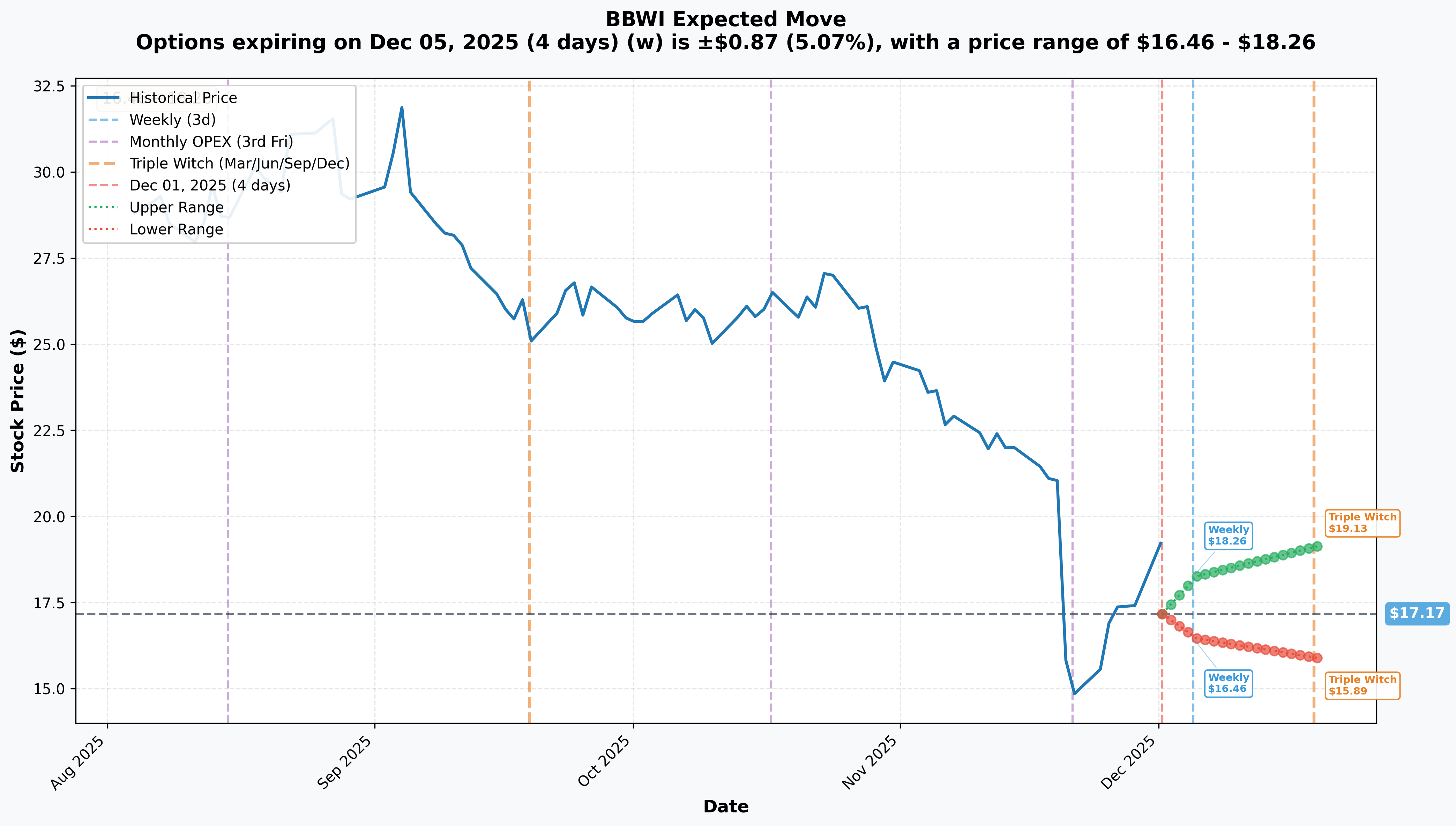

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 4 days): ±$0.87 (±5.07%) → Range: $16.46 - $18.26

- 📅 Monthly OPEX (Dec 19 - 18 days - THIS TRADE!): ±$1.51 (±8.79%) → Range: $15.89 - $19.13

- 📅 Quarterly Triple Witch (Dec 19 - 18 days): ±$1.51 (±8.79%) → Range: $15.89 - $19.13

Translation for regular folks: Options traders are pricing in a 5% move ($0.87) by this Friday's weekly expiration, and a larger 8.8% move ($1.51) through December 19th monthly OPEX (when this $5.2M trade expires). The relatively modest implied moves reflect LOW expectations for volatility - this isn't a stock anyone expects to suddenly explode higher.

Key insight: The December 19th implied range of $15.89-$19.13 suggests the market sees:

- Upside potential capped: Upper range of $19.13 (just 11% above current) shows limited rebound expectations

- Downside risk real: Lower range of $15.89 (7% below current) - market pricing in potential retest of $14-16 lows

- Holiday uncertainty: 18 days captures critical Black Friday/holiday selling data - potential catalyst either way

The person closing the $20 puts is doing so because they know the implied range tops out at $19.13 - meaning even if BBWI rallies from here, it likely won't get back above $20 by December 19th. Better to take the loss now at $2.00 than risk the puts expiring at $3.00+ intrinsic value if stock stays at $17.

🎪 Catalysts

📅 Already Happened (Past 30 Days)

Q3 2025 Earnings Disaster - November 20, 2025 📉

BBWI reported catastrophic Q3 results that sent shares plunging 25% in a single day:

- 📊 Revenue: $1.59B vs. $1.63B consensus (-2.5% miss)

- 💰 Adjusted EPS: $0.35 vs. $0.40 consensus (-12.5% miss)

- 📈 Operating Margin: 10.1% vs. 13.5% prior year (340 bps deterioration!)

- 💔 All categories declined: Body care, home fragrance, soaps/sanitizers ALL posted low-single-digit declines YoY

Management's brutal assessment: CEO Daniel Heaf stated: "Our third quarter results were below expectations, and we are lowering our outlook for the remainder of the year reflecting current business trends and continuation of recent macro consumer pressures."

Analyst Massacre - November 2025 🔻

Wall Street CRUSHED their ratings following the Q3 disaster:

- 📉 Morgan Stanley: Downgraded from Overweight to Equal-Weight; PT cut $43 to $18 (-58%)

- 📉 Goldman Sachs: Downgraded from Buy to Neutral; PT cut $39 to $17 (-56%)

- 📉 Raymond James: Downgraded to Market Perform from Outperform

- 💸 Consensus target now $29.79 (73% above current but DOWN from $35+ pre-earnings)

Current analyst consensus: 11 Buy, 18 Hold, 0 Sell - WEAKENING from previous quarters

Strategic Reset Announcement - November 20, 2025 🔄

New CEO Daniel Heaf unveiled "Consumer First Formula" turnaround with four priorities:

- Product Innovation: Creating disruptive products

- Brand Reignition: Rebuilding equity damaged by over-promotion

- Marketplace Expansion: Digital and wholesale channels

- Operational Efficiency: Cost reduction and simplification

Cost savings target: $250M by 2027 ($125M in 2026) - but savings will be REINVESTED in marketing/product rather than flow to bottom line

Category exits: Exiting hair care and men's grooming to focus on 4 core categories - admission previous expansion "has not delivered promising results"

Why this matters: Turnaround plans are acknowledgments of FAILURE. Management is effectively saying "we screwed up, give us 2 years to fix it." Stock typically stays depressed during turnaround execution phase.

🔥 Upcoming Catalysts (Next 6 Months)

Holiday 2025 Performance - Ongoing (Results in January) 🎄

The next 18 days (through Dec 19 when the puts expire) capture CRITICAL holiday selling season:

- 🛍️ Q4 guidance: High-single-digit sales DECLINE vs Q4 2024

- 😰 CFO Eva Boratto: Holiday season "underwhelming thus far" due to "high competition and low consumer sentiment"

- 💸 Heavy promotional environment: Discounting to attract cash-strapped consumers crushes margins

- 📊 Q4 is typically LARGEST quarter for BBWI - weakness here would be devastating for full-year results

The setup: Every week through December, we'll get reads on Black Friday/Cyber Monday traffic, holiday promotion effectiveness, and consumer spending. BAD news (continued weakness) would pressure BBWI toward $14-15. GOOD news (better-than-feared holiday) could bounce stock back to $19-20.

Q4 2025 Earnings - February 27, 2026 📊

Confirmed earnings date: February 27, 2026 before market open

Wall Street consensus:

- 📈 EPS estimate: $2.04 per share (-0.97% YoY decline)

- 💰 Full-year 2025 adjusted EPS guidance: At least $2.87 (vs. $3.40 consensus - MASSIVE 15.6% miss)

What to watch:

- Holiday season results vs guidance (high-single-digit decline expected)

- Q1 2026 guidance (first look at 2026 expectations - management expects NO growth in 2026!)

- Margin trends (promotional intensity killing profitability)

- Early turnaround traction signals (likely TOO early to show results)

Reality check: CEO Heaf warned initiatives "won't meaningfully impact the business until the second half" of 2026 - meaning Q4 results will be ugly and Q1 2026 guidance likely weak. Not a positive near-term catalyst.

Amazon Launch - H1 2026 🚀

Expected timeline: First half of 2026

Strategic details:

- 🎯 Curated assortment of evergreen hero products

- 💰 Capturing $60-80M in existing "gray market" sales currently going to unauthorized Amazon sellers

- 🛡️ Defensive move: CEO: "We have left Amazon wide open for competitors to play. That is changing."

Why this matters: This is an ADMISSION that BBWI has been losing sales to Amazon gray market for years. While $60-80M revenue capture sounds good, it's only ~1% of annual sales and comes with margin pressure (Amazon takes 15% cut). More importantly, it signals the mall-based retail model is BROKEN - they NEED digital channels to survive.

Risk: Amazon partnership could cannibalize existing store sales (76% of revenue) faster than it adds digital revenue.

MI350 Series Launch - Mid-2025 🎨

New product launches expected second half 2026

Product development plans:

- 🎨 "New forms, vessels, and formulas" for body care, home fragrance, soaps, sanitizers

- 🏰 Disney collaboration: Multi-year deal for recurring themed collections

- 🎓 College campus expansion: Launched in 600+ campus stores nationwide targeting Gen Z

The problem: These initiatives won't show results until LATE 2026 at earliest. We're talking 12-18 months before new products hit shelves and make a revenue impact. That's an eternity for a stock trading at $17 with no near-term catalysts.

⚠️ Negative Catalysts (High Risk!)

Ongoing Margin Compression 📉

Q3 operating margin collapsed 340 basis points to 10.1% from 13.5% prior year - and it's getting WORSE:

- 💸 Promotional intensity: Constant discounting to compete with rivals and attract budget-conscious consumers

- 🏭 Fixed cost deleveraging: Store base of 1,800 locations creates massive fixed costs that don't scale down with revenue

- 📦 Supply chain costs: Logistics and sourcing pressures ongoing

- 💰 Marketing reinvestment: $125M in 2026 cost savings being REINVESTED rather than flowing to bottom line

Reality: Even with $250M cost savings by 2027, margins are getting destroyed by competition and promotional environment. This is a STRUCTURALLY challenged business model.

Consumer Spending Weakness 💔

Translation: Consumers are BROKE and waiting for better deals. BBWI's customer base is middle-income discretionary spending - exactly the segment under most pressure. Stock is warning of "weak discretionary spending" amid broader retail challenges.

If consumer spending weakens further (recession risk), BBWI could revisit $10-12 range.

Turnaround Execution Risk 🎯

That's code for: "It's going to get worse before it gets better. Maybe. If we execute perfectly."

Red flags:

- ⏰ New CEO Heaf only joined May 2025 - limited track record at BBWI

- 💸 $250M cost savings is less than 5% of cost structure - not transformational

- 🚫 Category exits (hair, men's grooming) may alienate customers

- 🏬 Mall-based retail format (76% of sales) declining structurally

Turnarounds are HARD. Most fail. Stock stays depressed during execution phase.

🎲 Price Targets & Probabilities

Using implied move data, catalyst timing, and technical setup, here are scenarios through December 19th expiration:

📈 Bull Case (20% probability)

Target: $19-$21

How we get there:

- 🎄 Holiday sales data BEATS lowered expectations - consumers show up for Black Friday/holiday promotions

- 🛍️ Weekly sales reads (weekly same-store sales reports) show sequential improvement through December

- 💪 Analyst upgrades emerge as "worst is over" thesis gains traction around $15-16 support

- 📊 Bargain hunters step in at historically low 5.2x P/E valuation

- 🎯 Technical bounce to $19-20 reclaims psychological support turned resistance

Key metrics needed:

- Holiday comps showing BETTER than "high-single-digit decline" guidance

- Traffic metrics improving week-over-week

- Any positive Amazon partnership news or early traction signals

Probability assessment: Only 20% because it requires PERFECT holiday execution after management EXPLICITLY warned of weakness. The upper implied move range is $19.13 - market pricing minimal upside. Without a catalyst, hard to see what drives sustained rally.

🎯 Base Case (50% probability)

Target: $15.50-$18.00 (CONTINUED CHOP)

Most likely scenario:

- 📉 Holiday sales roughly in-line with lowered guidance (high-single-digit decline)

- 🎪 No major positive OR negative surprises - just continued mediocrity

- 💤 Trading range between $15.50 (lower implied move) and $18.50 through December

- 📊 Volatility remains elevated but no major catalyst to break range

- 🤷 Market in "wait and see" mode until February earnings for 2026 visibility

This is why the put closer is taking the loss: Even if BBWI bounces modestly to $18-19, the $20 puts they sold are still in-the-money and losing value. Better to close now at $2.00 than risk stock staying at $17 and puts expiring at $3.00 intrinsic value.

Why 50% probability: Stock in no-man's land with no clear catalyst either way near-term. Most likely just consolidates current losses and trades sideways into year-end.

📉 Bear Case (30% probability)

Target: $12-$15 (RETEST THE LOWS!)

What could go wrong:

- 😰 Holiday sales data WORSE than already-lowered guidance - true disaster scenario

- 🚨 Major retailer (competitor) reports strong holiday, highlighting BBWI-specific weakness

- 💔 Consumer spending data broadly weak - retail recession fears

- 📉 Continued analyst downgrades as turnaround skepticism grows

- 🔨 Break below $16 support triggers cascade to $14-15 (testing November lows)

- 💀 Dividend cut speculation emerges (currently 4.6% yield - could be at risk if cash flow deteriorates)

Critical support levels:

- 🛡️ $16.50: Lower implied move range - MUST HOLD or momentum shifts more bearish

- 🛡️ $15.00: Psychological support and minor technical level

- 🛡️ $14.28: 52-week low - retest would be devastating for sentiment

- 🛡️ $12-13: Disaster zone - implies complete loss of confidence in turnaround

Probability assessment: 30% because it requires holiday season to be WORSE than already-terrible expectations. However, management has a track record of over-promising this year (missed Q2, Q3, lowered full-year twice). If they miss AGAIN on holiday, all credibility lost.

What the put closer fears: Stock drops to $14-15 range, making their $20 puts worth $5-6 each. They'd be assigned 2.6 million shares at $20 ($52M total) for stock worth only $36-39M - a $13-16M LOSS. They're cutting losses now at $5.2M to avoid potentially larger loss.

💡 Trading Ideas

🛡️ Conservative: Avoid Completely (Wait for Clarity)

Play: Stay FAR away from BBWI until turnaround shows actual results

Why this works:

- 📉 Stock down 58% YTD - catching falling knives is dangerous

- ⏰ Management explicitly said 3+ more quarters of weakness before turnaround gains traction - that's into late 2026!

- 💸 No near-term positive catalysts - only risk events (holiday weakness, Feb earnings)

- 🏬 Structurally challenged mall-retail model in secular decline

- 🚨 Turnaround plans often fail - why catch this falling knife when there are better opportunities?

- 📊 Even at 5.2x P/E, stock could get cheaper if margins compress further (multiple compression risk)

Action plan:

- 👀 Monitor from sidelines - add to watchlist but don't touch

- 🎯 Revisit in Q2 2026 AFTER seeing Feb earnings and Q1 guidance to assess turnaround traction

- ✅ Would need to see: Revenue stabilization, margin improvement, positive 2026 guidance, holiday season NOT a disaster

- 📊 Better entry likely available at $12-14 if bear case plays out

- ⏰ No rush - if turnaround works, stock will still be cheap at $20-25 in 2027

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential further -20-30% drawdown if turnaround stumbles. Maintain capital for better opportunities. Sleep well at night.

⚖️ Balanced: Post-Holiday Put Spread (Bet on Continued Weakness)

Play: After holiday sales data emerges, sell put spread betting on range-bound action

Structure: Sell $17 puts, Buy $15 puts (January 16 expiration - 45 days out)

Why this could work:

- 💰 Credit spread collects premium betting stock stays ABOVE $15 (bear case floor)

- 📊 Defined risk spread ($2 wide = $200 max risk per spread)

- 🎯 Gives 12% downside cushion from current $17.17 before max loss

- ⏰ 45 days allows time for holiday data and year-end consolidation

- 📈 Even in bear case, $15 represents strong support (near 52-week low) where buyers may emerge

Estimated P&L:

- 💰 Collect ~$0.40-0.50 credit per spread

- 📈 Max profit: $40-50 if BBWI above $17 at January expiration

- 📉 Max loss: $150-160 if BBWI below $15 (defined and limited)

- 🎯 Breakeven: ~$16.50-16.60

- 📊 Risk/Reward: ~3:1 risk/reward (need 75% win rate to be profitable long-term)

Entry timing:

- ⏰ Wait until December 12-15 (after early holiday sales data)

- 🎯 Only enter if stock trading $16.50-18.00 range (not already at $15)

- ❌ Skip if stock rallies above $19 (too close to short strike)

- ❌ Skip if stock already below $16 (not enough cushion)

Position sizing: Risk only 2-3% of portfolio (this is premium collection with defined downside risk)

Risk level: Moderate (defined risk, bearish-neutral directional) | Skill level: Intermediate

Why this is smart: You're essentially betting stock DOESN'T collapse below $15 (52-week low area) over next 45 days, which seems reasonable. Collects premium in a likely range-bound environment.

🚀 Aggressive: Short Shares with Tight Stop (ADVANCED ONLY!)

Play: Short shares betting on continued weakness through holiday season

Structure: Short shares at $17-17.50, stop at $19.25 (implied move upper range)

Why this could work:

- 📉 Downtrend intact - momentum is DOWN across all timeframes

- 🚨 Management guided for high-single-digit Q4 decline - weakness confirmed

- 💔 Consumer spending pressures accelerating into year-end

- 📊 Empty gamma map means no institutional support - can drift lower easily

- 🎯 Risk/reward favorable: Risk $2 ($17 to $19) to make $3-5 ($17 to $14-12)

- ⏰ Holiday sales data provides multiple near-term catalysts for downward moves

Why this could blow up (SERIOUS RISKS):

- 🚀 Short squeeze risk: Stock heavily shorted already - any good news triggers squeeze

- 💸 Dividend risk: 4.6% dividend yield means you PAY dividend while short ($0.20 quarterly)

- 😱 Takeover risk: At $3.6B market cap with strong brands, could be buyout target

- 📊 Value trap: Looks cheap at 5.2x P/E - bargain hunters could emerge at any time

- 🎢 High volatility means stop could get hit on random bounce even if ultimately right on direction

- ⚠️ Turnaround speculation could drive short-covering rally at any time

Estimated P&L:

- 💰 Entry: Short at $17.00

- 🛡️ Stop loss: $19.25 (upper implied move + buffer) = -$2.25 loss (-13.2%)

- 🎯 Target 1: $15.00 = +$2.00 profit (+11.8%)

- 🎯 Target 2: $14.00 = +$3.00 profit (+17.6%)

- 🚀 Home run: $12.00 = +$5.00 profit (+29.4%)

Breakeven considerations:

- 💸 Must pay $0.20 dividend if short through Dec 5 payment date - adds to cost

- 📊 Borrow cost may be elevated (hard to borrow) - check with broker

- ⏰ Need move to happen within 2-4 weeks to avoid paying second dividend

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have experience shorting stocks and understand unlimited loss risk

- ✅ Can handle rapid moves against you (stock can gap $1-2 on no news)

- ✅ Understand you'll pay dividend and borrow costs

- ✅ Have strict risk management discipline to cut losses at stop

- ✅ Accept that even if thesis correct, timing could be wrong and stop gets hit first

- ⏰ Plan to cover partial position at $15 to lock in gains (don't get greedy)

Risk level: EXTREME (unlimited loss potential on short stock) | Skill level: Advanced only

Probability of profit: ~45% (slightly better than coinflip given downtrend, but risks are REAL)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎄 Holiday season binary event: Next 18 days through Dec 19 (when the $5.2M puts expire) capture CRITICAL Black Friday, Cyber Monday, and holiday shopping data. Management already warned of "underwhelming" start with "high competition and low consumer sentiment" - but any POSITIVE surprise on traffic or sales would trigger sharp short-covering rally. Even modest beat vs lowered expectations could send stock back to $19-20 range quickly.

-

💸 Valuation looks cheap but could be VALUE TRAP: Trading at historically low 5.2x P/E with 4.6% dividend yield, BBWI LOOKS like a bargain. However, margins are collapsing (340 bps compression in Q3) and revenue declining. If full-year 2026 EPS comes in at $2.50 instead of $3+ due to continued weakness, that "cheap" 5.2x P/E becomes 6.8x P/E at $17 - not as attractive. Stock can get CHEAPER if earnings continue declining.

-

🏬 Structurally challenged retail model: 76% of sales from 1,800+ physical stores in dying malls creates massive fixed cost base. Unlike pure digital retailers, BBWI can't easily cut costs as revenue falls. Store leases are long-term obligations. The mall-based model is in secular decline - Amazon launch in H1 2026 is an ADMISSION the store model isn't working. Digital shift could cannibalize stores faster than it grows digital.

-

🔄 Turnaround execution risk with unproven CEO: CEO Daniel Heaf only joined May 2025 from Nike - has been on job just 6 months. His "Consumer First Formula" turnaround plan involves $250M cost savings by 2027, but savings will be REINVESTED in marketing and product rather than flow to bottom line. Management explicitly warned initiatives "won't meaningfully impact business until second half of 2026" - that's 18+ months of continued weakness. Most retail turnarounds FAIL.

-

💔 Consumer spending deterioration accelerating: Cash-strapped consumers preferring cheaper alternatives and delaying purchases for deeper discounts. BBWI's customer base is middle-income discretionary spending - exactly the segment getting CRUSHED by inflation and economic uncertainty. If recession hits in 2026, discretionary spending on $30 candles and $15 body lotions will get DESTROYED. Stock could revisit $10-12 in recessionary scenario.

-

🚨 $5.2M put closing signals institutional PAIN: The fact that someone is buying back $20 strike puts they previously sold for a $5.2M loss shows they're in SERIOUS pain and fear worse losses ahead. They likely sold these puts at $1.00-1.50 when stock was $20-22, and now they're paying $2.00 to close with stock at $17.17. This is capitulation behavior - they don't want to be assigned 2.6 million shares at $20 when stock trades at $17. When big money is capitulating, that's a WARNING SIGN not a buy signal.

-

🌊 Competitive pressure intensifying: Home fragrance and body care markets seeing "intensified promotional activity" across all players. Competitors (Yankee Candle, direct-to-consumer brands, Amazon private label) are ALL fighting for same shrinking discretionary dollar pool. BBWI losing pricing power - forced to match competitors' discounts which destroys margins. Race to the bottom.

-

💰 Dividend cut risk if cash flow deteriorates: Currently paying $0.80/year (4.6% yield) at 23.5% payout ratio which LOOKS safe. However, if free cash flow continues declining due to margin pressure and working capital needs, board could cut dividend to preserve liquidity for turnaround investments. Any dividend cut would CRUSH stock another 20-30% as income investors flee.

-

📊 Empty gamma exposure map is RED FLAG: The complete ABSENCE of meaningful gamma levels at any strike shows institutional options traders have ABANDONED this name. No hedging activity, no conviction trades, no positioning. This is a liquidity desert - when everyone has left the building, you probably should too. Stock can drift lower or gap on low volume with no dealer support.

-

🎯 February earnings will be UGLY: With Q4 guidance for high-single-digit decline and full-year 2025 adjusted EPS of "at least $2.87" (vs $3.40 consensus), February 27 earnings report will confirm another bad quarter. More importantly, 2026 guidance will show NO GROWTH as management warned. This removes any near-term thesis for buying. Stock could stay depressed all of 2026.

-

🔥 Short squeeze risk at current levels: After 58% YTD decline, significant short interest likely built up. Any HINT of good news (surprise holiday strength, takeover rumor, positive analyst note) could trigger violent short squeeze to $20-22. If you're short or bearish positioned, this risk is REAL. Set tight stops.

-

🏛️ Brand equity damage from over-promotion: Management admitted overreliance on promotions and collaborations "erodes brand equity". When you train customers to only buy on 50% off sales, they NEVER pay full price again. This creates permanent margin pressure. Rebuilding pricing power takes YEARS and requires product innovation that BBWI hasn't delivered yet. The brand may be permanently impaired.

🎯 The Bottom Line

Real talk: Someone just paid $5.2 MILLION to close out a losing put trade on BBWI because they don't want to own 2.6 million shares at $20 when the stock trades at $17. This isn't a hedge - this is CAPITULATION. They're cutting losses because they fear it gets WORSE.

What this trade tells us:

- 😰 Smart money that sold $20 puts expecting support got CRUSHED - stock fell from $20+ to $17 in weeks

- 💸 They're willing to take a $5.2M loss NOW rather than risk larger losses if stock drops to $14-15 by Dec 19

- 🚨 The urgency of closing just 18 days before expiration (vs rolling or holding) signals genuine FEAR

- 📉 They have NO confidence stock bounces back above $20 anytime soon (otherwise they'd hold and hope)

- ⏰ Holiday season risks so severe they'd rather lock in losses than stay exposed

This is NOT a "buy the dip" signal - it's a "stay away until the bleeding stops" signal.

If you own BBWI:

- ⚠️ Cut losses if you're underwater - stock could drift to $12-15 over next 6-12 months during turnaround execution

- 📊 Set MENTAL STOP at $15 (52-week low area) - if it breaks, likely heading to $12-13

- 💰 If you're profitable somehow, TAKE PROFITS - this rally won't last with fundamentals this bad

- 🎯 February 27, 2026 earnings will be ugly with weak 2026 guidance - exit before then

- 🛡️ Consider selling covered calls to generate income if you're stuck holding (sell $19-20 strikes for January)

If you're watching from sidelines:

- ⏰ Stay on sidelines until turnaround shows ACTUAL results - we're talking late 2026 at earliest per management!

- 🎯 Better entry likely available at $12-14 if bear case plays out (test of 2020 COVID lows)

- 📈 Would need to see: Holiday sales stabilization, margin improvement, positive 2026 guidance, Amazon launch traction

- 🚀 Even if turnaround works, stock will still be cheap at $20-25 in 2027 - NO RUSH

- ⚠️ Current 5.2x P/E and 4.6% dividend yield are VALUE TRAPS - stock can get cheaper if earnings continue declining

- 📊 Monitor holiday season data and February earnings from afar - reassess in Q2 2026

If you're bearish:

- 🎯 Post-holiday put spreads or short shares with tight stops offer defined-risk ways to profit from continued weakness

- ⏰ Key inflection: If stock breaks $16 support, likely cascades to $14-15 quickly

- 📉 Major resistance at $19-20 (implied move upper range + old support) caps upside even on good news

- 🚨 Watch for short squeeze risk though - after 58% decline, ANY good news could trigger violent rally to $20-22

- ⚠️ Don't get greedy - this is a damaged brand with structural issues, but valuations CAN matter at some price

Mark your calendar - Key dates:

- 📅 December 5, 2025 - Dividend payment date ($0.20/share)

- 📅 December 5, 2025 - Weekly OPEX (±5% implied move window)

- 📅 December 19, 2025 - Monthly OPEX and expiration of this $5.2M put trade

- 📅 December 26-31, 2025 - Holiday season results start leaking (comp store sales data)

- 📅 January 2026 - Monthly retail sales reports show holiday performance

- 📅 February 27, 2026 - Q4 FY2025 earnings report before market open (2026 guidance!)

- 📅 H1 2026 - Amazon partnership launch expected

- 📅 H2 2026 - New product launches hit shelves (first chance to assess turnaround traction)

Final verdict: BBWI is a falling knife in a structural decline. Management explicitly warned of 3+ more quarters of challenging results before turnaround shows benefits. The mall-based retail model is dying, margins are collapsing (340 bps compression in Q3), consumer spending is weakening, and the new CEO's turnaround plan won't show results until late 2026 AT EARLIEST.

The $5.2M put closing trade is a CLEAR signal: smart money is capitulating and cutting losses rather than stay exposed to holiday season risks. This is NOT the time to be a hero and catch the falling knife.

Stay away. Let the turnaround PROVE itself with actual results before risking capital. There are FAR better opportunities in this market.

Your capital is too precious to gamble on a struggling mall retailer that may never recover its glory days. Be patient. Wait for confirmation. Protect yourself. 🛡️

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 555x unusual score reflects this specific trade's size relative to recent BBWI history - it represents a put closing transaction (BTC) by a trader exiting a losing position, not a new directional bet. The trader is taking a realized loss to avoid potentially larger losses. Always do your own research and consider consulting a licensed financial advisor before trading. Retail turnarounds have low success rates and typically take 2-3 years to show results. BBWI's structural challenges (mall-based retail, margin compression, consumer spending weakness) may persist regardless of management actions.

About Bath & Body Works (BBWI): Bath & Body Works operates as a specialty home fragrance and fragrant body care retailer with over 1,800 stores nationwide under the Bath & Body Works, White Barn, and C.O. Bigelow brands. The company has a market cap of $3.56 billion in the Retail Stores industry and is currently undergoing a comprehensive turnaround under new CEO Daniel Heaf.